India Two-Wheeler Market Size, Share, Trends and Forecast by Type, Technology, Transmission, Engine Capacity, Fuel Type, End User, Distribution Channel, and Region, 2026-2034

India Two-Wheeler Market Size, Share, Trends & Forecast (2026-2034)

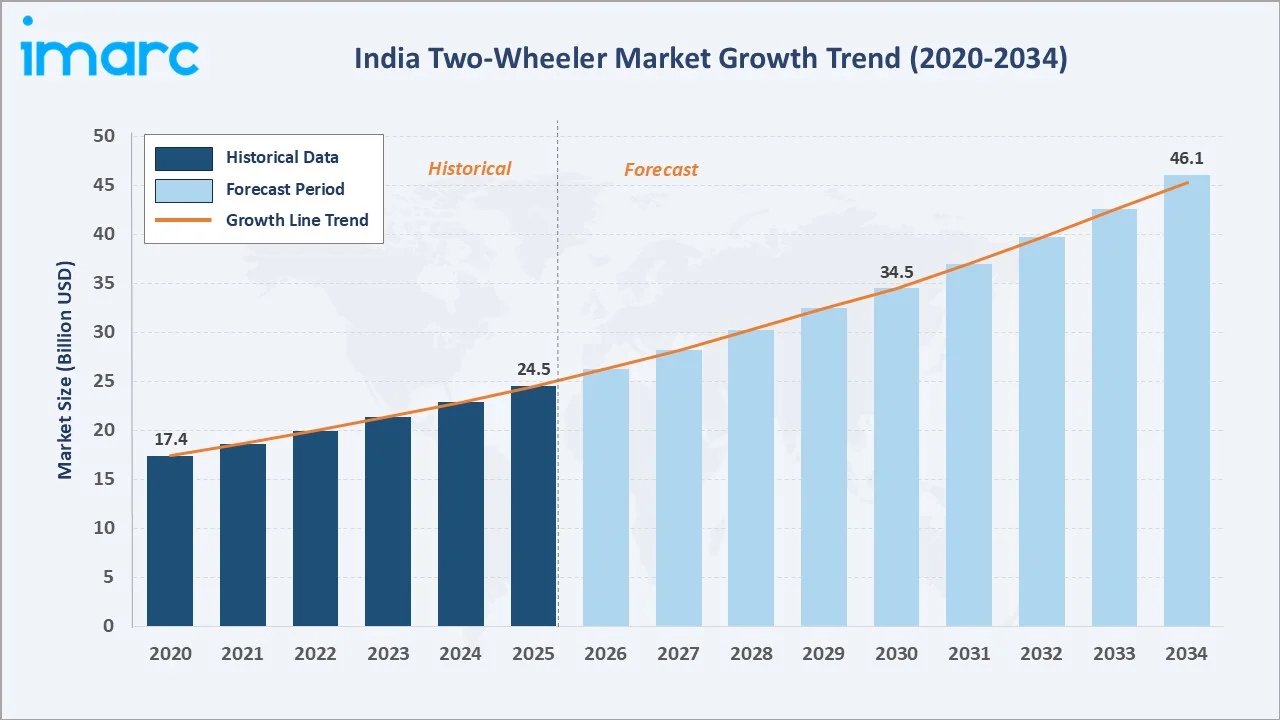

The India two-wheeler market reached USD 24.5 Billion in 2025 and is projected to reach USD 46.1 Billion by 2034, growing at a CAGR of 7.08% during 2026-2034. Rising rural incomes and aspirational personal mobility demand, government FAME-III electric vehicle subsidies accelerating EV two-wheeler adoption, the premiumization trend shifting consumer preference toward higher-cc motorcycles and feature-rich scooters, and India’s position as the world’s largest two-wheeler market by volume are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.5 Billion |

|

Forecast Market Size (2034) |

USD 46.1 Billion |

|

CAGR (2026-2034) |

7.08% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

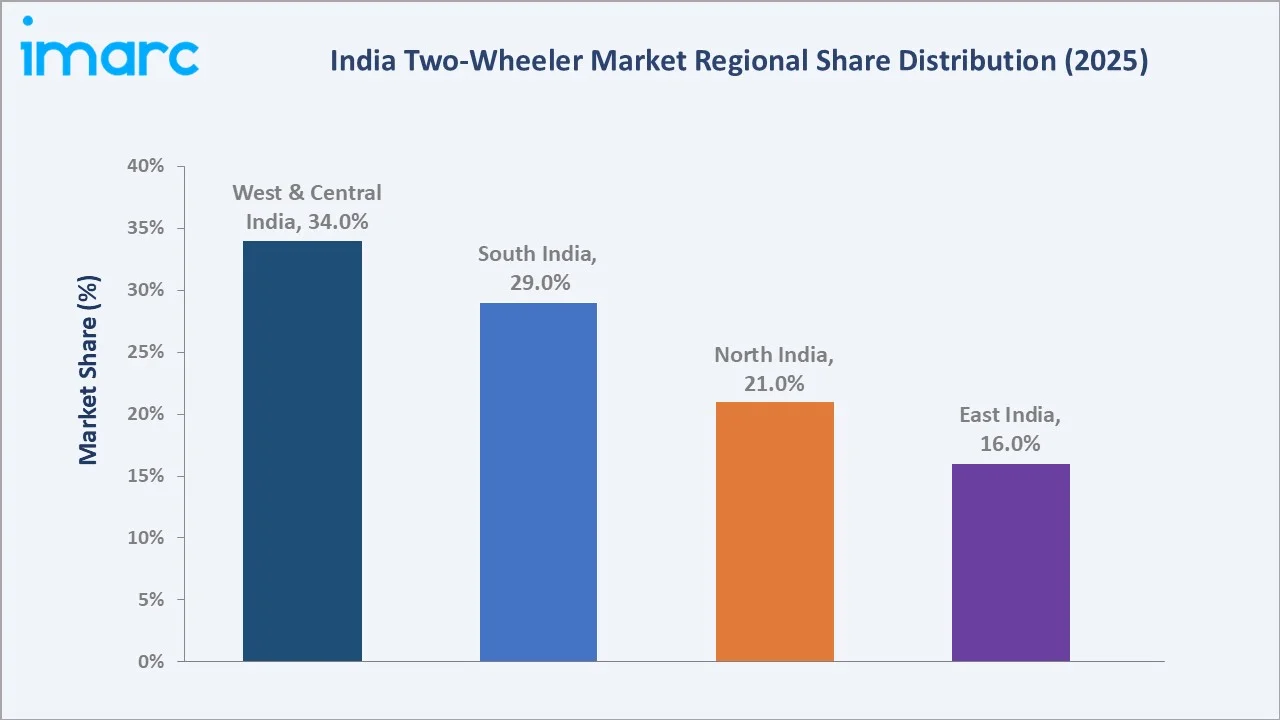

West and Central India leads with a 34.0% market share in 2025, driven by Maharashtra’s large urban and semi-urban two-wheeler demand base, Gujarat’s prominent two-wheeler manufacturing presence, and Madhya Pradesh’s and Rajasthan’s vast rural population that depends on motorcycles as the primary personal mobility solution.

To get more information on this market, Request Sample

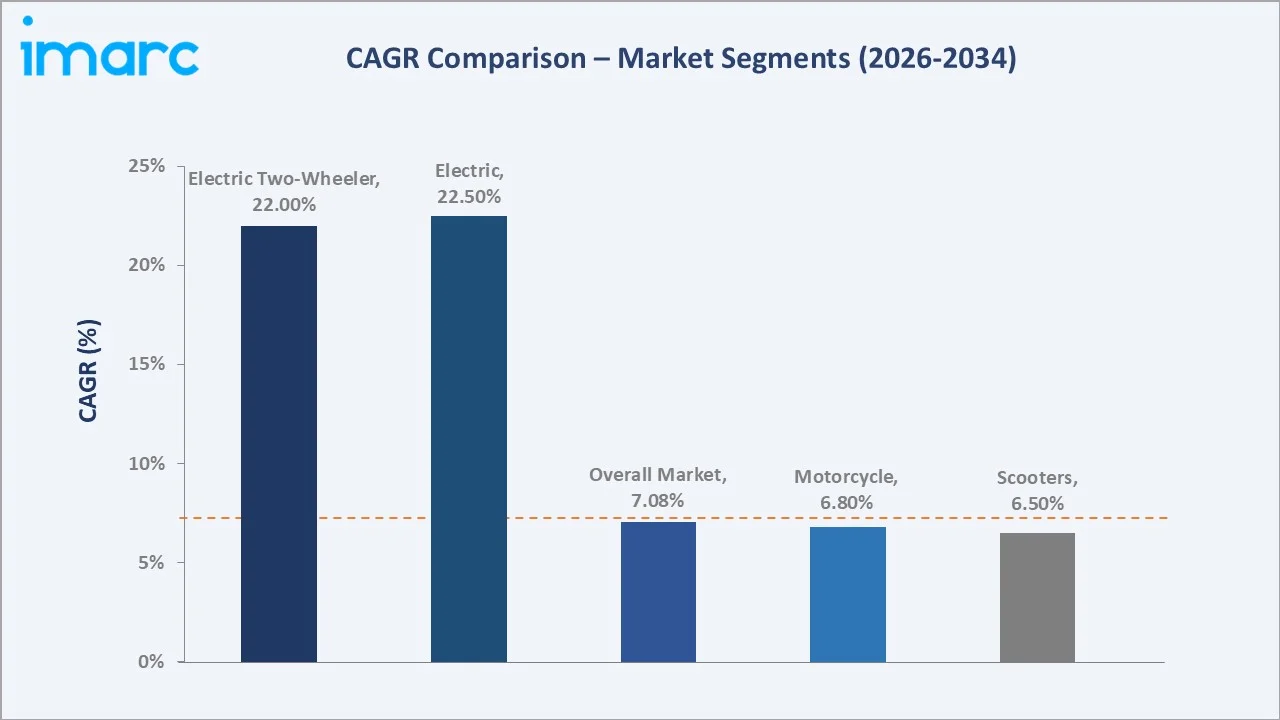

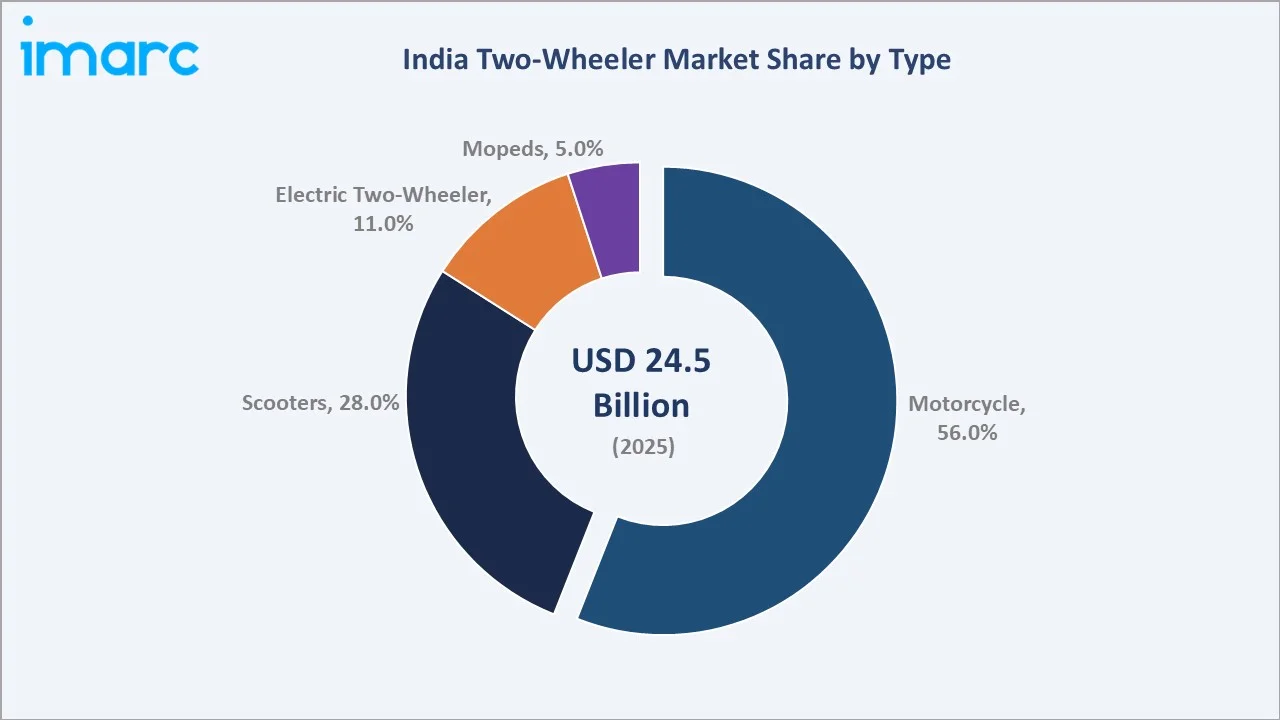

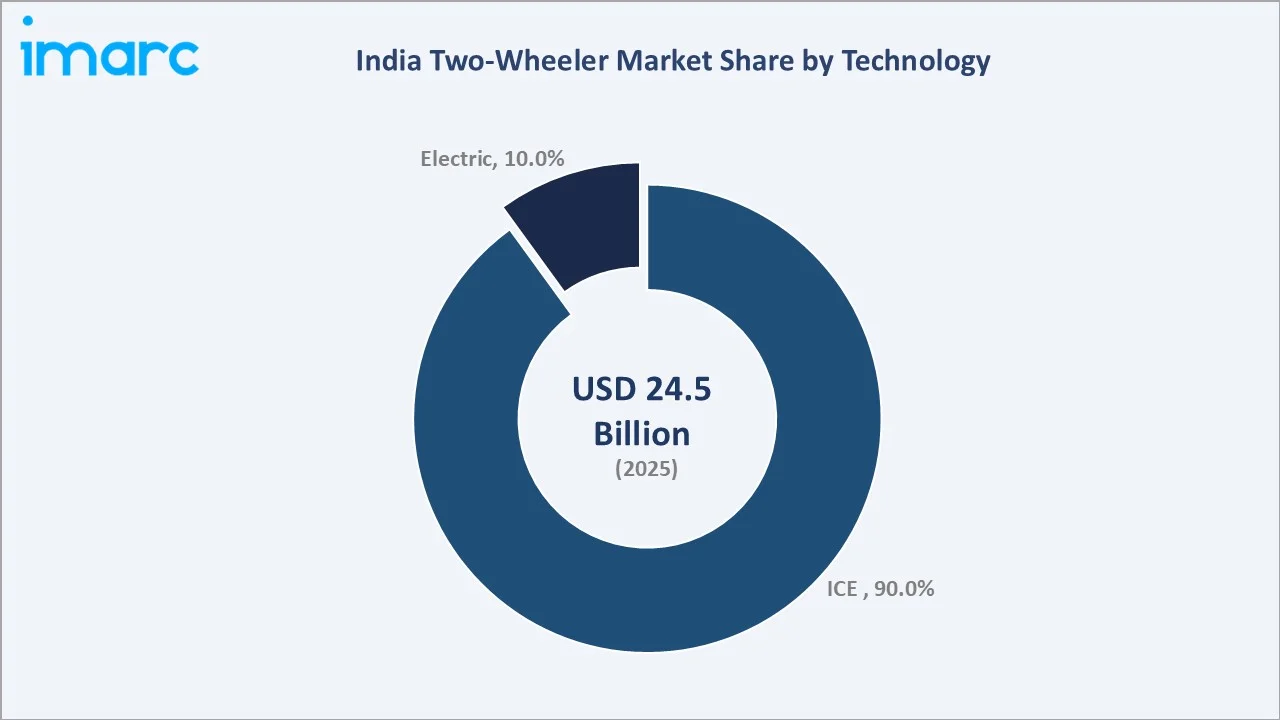

Motorcycle command the dominant type share at 56.0%, while ICE (internal combustion engine) technology represents 90.0% of the market in 2025, reflecting the established conventional powertrain base even as electric two-wheelers grow rapidly from a 10.0% technology share.

Executive Summary

The India two-wheeler market is the world’s largest by unit volume and one of Asia’s most dynamic automotive market segments, serving as the primary personal mobility solution for approximately 900 million Indians across urban, semi-urban, and rural geographies. The market was valued at USD 24.5 Billion in 2025 and is forecast to reach USD 46.1 Billion by 2034 at a CAGR of 7.08%.

Motorcycle dominate the type segment at 56.0% in 2025, encompassing commuter motorcycles (100–110cc for entry-level rural and semi-urban commuting), executive motorcycles (125–160cc for mid-market urban and semi-urban use), and premium motorcycles (200cc+ for aspirational consumers and enthusiasts). ICE technology commands 90.0% of market value in 2025, reflecting the entrenched conventional petrol-powered powertrain base across all motorcycle, scooter, and moped segments.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Motorcycle – 56.0% share (2025) |

| Fastest Growing Type |

Electric Two-Wheeler – ~22.0% CAGR (2026-2034) |

| Largest Technology |

ICE – 90.0% share (2025) |

| Fastest Growing Technology |

Electric – ~22.5% CAGR (2026-2034) |

| Leading Region | West and Central India – 34.0% share (2025) |

| Top Companies | Hero MotoCorp Limited, Honda Motor Co., Ltd., TVS Holdings Limited, Bajaj Auto Ltd. |

Key Analytical Observations Supporting The Above Data:

- Motorcycle’s 56.0% (2025) type dominance reflects the vehicle type’s dual role as a rural economic necessity and an urban aspirational product in India. In rural India, the motorcycle serves as the primary household mobility asset, transporting farm produce, accessing markets and healthcare, and enabling daily commuting. In urban and semi-urban India, motorcycles serve commuting in traffic-congested cities where the two-wheeler’s ability to navigate between vehicles provides a time and cost efficiency advantage over four-wheelers or public transport.

- ICE technology’s 90.0% (2025) share reflects the established conventional powertrain’s structural advantages in India’s two-wheeler market: ICE motorcycles and scooters start from INR 55,000–80,000 (USD 660–960), while electric equivalents start from INR 90,000–120,000 (USD 1,080–1,440), a premium that requires 2–3 years of fuel cost savings to justify based on typical Indian commuter usage patterns.

- West and Central India’s 34.0% (2025) market share reflects the region’s combination of India’s largest two-wheeler manufacturing concentration and the region’s large consumer base spanning Maharashtra’s urban motorcycle and scooter market, Gujarat’s commercial and personal two-wheeler use, and Madhya Pradesh’s and Rajasthan’s massive rural motorcycle-dependent populations.

- The 7.08% CAGR reflects India’s two-wheeler market’s dual growth dynamics: volume growth driven by annual unit sales as rural income growth brings first-time buyers into the market; and value growth driven by premiumization as mid-premium and premium motorcycle segments grow faster than entry-level commuter segments.

India Two-Wheeler Market Overview

India is one of the world’s largest two-wheeler markets by unit volume, with 20.3 million two-wheelers sold during January–December 2025, exceeding China, Indonesia, Vietnam, and all other major markets. The two-wheeler serves as the backbone of India’s personal mobility ecosystem: for the country’s rural and semi-urban population, the motorcycle or scooter is typically the first and sometimes only personal motorized vehicle owned by the household, fulfilling transportation needs ranging from daily commuting to farm-to-market produce transport, school and healthcare access, and social connectivity.

The Indian two-wheeler market’s value has grown at above-GDP rates over the 2020–2025 historical period, driven by a premiumization dynamic where consumer aspirations are systematically driving purchase decisions toward higher-displacement, feature-rich motorcycles and automatic scooters. The 100–110cc entry commuter segment is progressively losing share to the 125–160cc executive segment and 200cc+ premium segment, while the scooter segment’s urban and female rider appeal has sustained growth.

Market Dynamics

To evaluate market opportunities, Request Sample

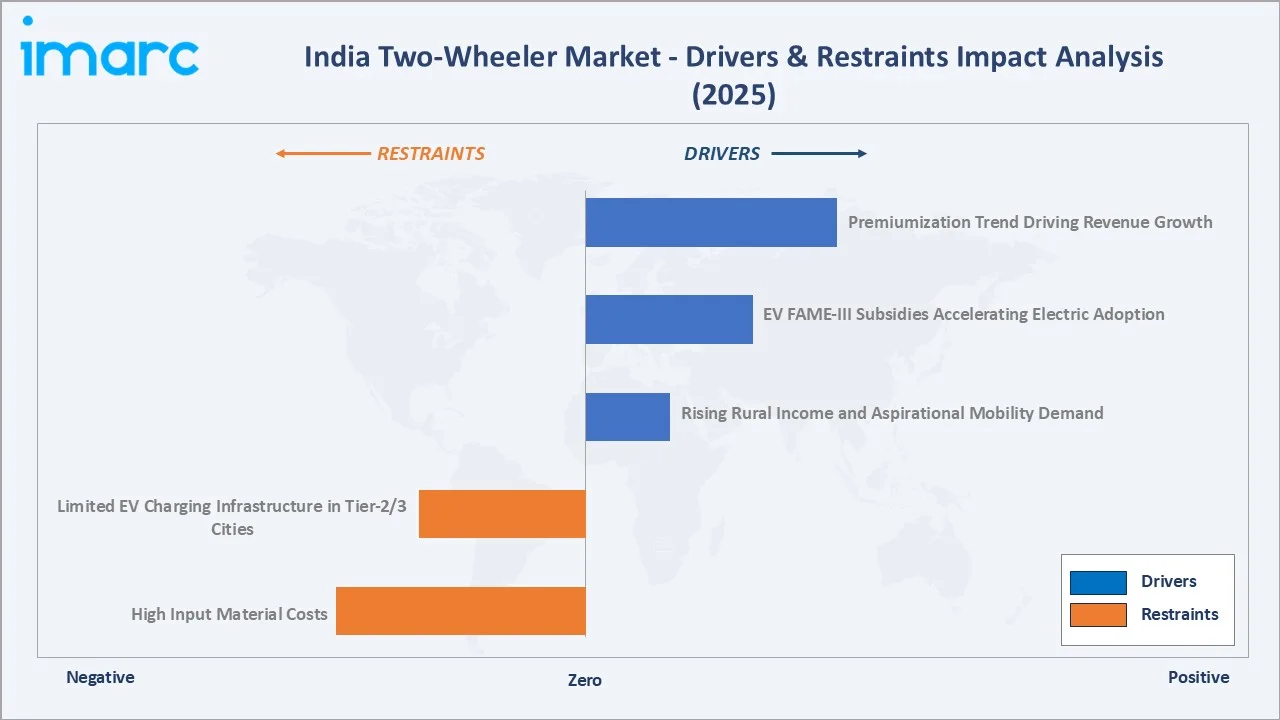

Market Drivers

- Rising Rural Income and Aspirational Mobility Demand: India’s rural economy has been experiencing above-average income growth driven by government schemes including PM-KISAN (direct income support to 9.44 crore farmers), MGNREGS (rural employment guarantee), and the progressive improvement in agricultural commodity prices benefiting farming households. Rising rural household income is the most important volume growth driver for India’s two-wheeler market, as the first purchase decision upon crossing the INR 100,000–150,000 annual household income threshold in rural India is typically a 100–125cc motorcycle.

- EV FAME-III Subsidies Accelerating Electric Adoption: India’s FAME (Faster Adoption and Manufacturing of Electric Vehicles) program’s INR 15,000 per kWh consumer subsidy (capped at 40% of vehicle cost) enabled electric scooters to be priced competitively against premium ICE scooters at INR 90,000–130,000. The forthcoming FAME-III program is expected to extend and potentially deepen subsidy support, incentivize longer-range battery pack adoption, and introduce PLI-linked domestic battery cell production requirements that simultaneously support EV manufacturing localization and reduce battery cost.

- Premiumization Trend Driving Revenue Growth: India’s two-wheeler market’s value is growing significantly faster than its unit volume due to systematic consumer premiumization, the shift from entry-level to mid-premium and premium motorcycle and scooter categories driven by rising disposable incomes, aspirational consumption, and the proliferation of accessible financing options.

Market Restraints

- High Input Material Costs: Two-wheeler manufacturing’s primary material cost inputs are subject to significant global commodity price volatility that creates OEM margin pressure during commodity price upcycles. Steel accounts for approximately 15–20% of an ICE two-wheeler’s production cost, while lithium-ion battery cells account for 30-50% of an electric two-wheeler’s cost.

- Limited EV Charging Infrastructure in Tier-2/3 Cities: Despite rapid growth in EV charging station deployment along national highways and in metropolitan cities, the majority of India’s Tier-2 and Tier-3 cities lack adequate public EV charging infrastructure for electric two-wheeler users who reside in apartments or multi-family housing without access to home charging. Industry estimates suggest that approximately 40–50% of India’s urban population lives in apartment buildings where EV two-wheeler charging access is limited to shared building-level chargers that may have insufficient capacity for all residents.

Market Opportunities

- Electric Two-Wheeler Export Market Development: India’s electric two-wheeler OEMs are positioned to develop export markets in Southeast Asia (Vietnam, Indonesia, Philippines), Africa (Nigeria, Kenya), and Latin America where battery electric scooters are growing rapidly, but local manufacturing capability is limited.

- Premium Motorcycle Tourism and Lifestyle Segment: Royal Enfield’s extraordinary commercial success in the 350–650cc premium lifestyle motorcycle segment has demonstrated the commercial viability of a premium motorcycle market in India. Royal Enfield’s success is further attracting international premium motorcycle brands into the Indian market, collectively developing a premium and super-premium motorcycle segment.

Market Challenges

- Battery Localization and Supply Chain Development: India’s electric two-wheeler market’s primary structural vulnerability is the near-complete dependence on imported lithium-ion battery cells from China, South Korea, and Japan for electric vehicle battery packs. Approximately 70–80% of battery cell content in India’s electric two-wheelers is imported, creating both a cost exposure and a supply security risk.

- Competitive Intensity from Electric Two-Wheeler Startups: Legacy ICE two-wheeler OEMs are facing unprecedented competitive pressure from electric-native startups that are willing to operate at near-zero margins to capture market share during the EV transition. The startup-legacy OEM competitive dynamic creates margin and market share risk for established players that must invest heavily in EV platform development, battery sourcing, and dealer network electrification.

Emerging Market Trends

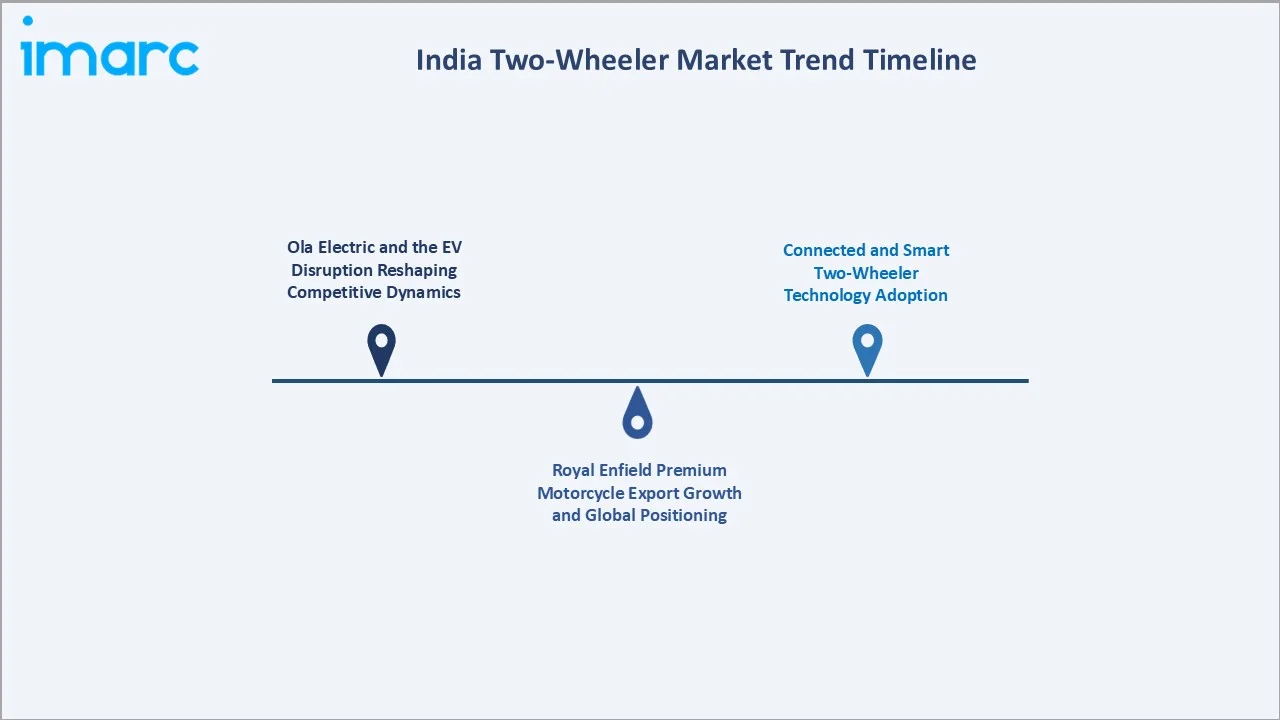

1. Ola Electric and the EV Disruption Reshaping Competitive Dynamics

Ola Electric’s emergence as India’s leading electric scooter OEM has fundamentally altered the India two-wheeler market’s competitive structure. Ola Electric’s vertically integrated model challenged the established OEM distribution and manufacturing paradigm. Ola Electric’s August 2024 Roadster series motorcycle launch signals the EV startup’s ambition to compete across the full two-wheeler product spectrum and introduces electric motorcycle competition into the segment where Hero MotoCorp, Honda, and Bajaj have traditionally dominated.

2. Royal Enfield Premium Motorcycle Export Growth and Global Positioning

Royal Enfield’s transformation from a domestic commuter heritage brand to an internationally recognized premium motorcycle manufacturer represents the India two-wheeler market’s most commercially significant premium segment development. Royal Enfield’s international sales now represent a growing percentage of total volume, with the UK, Continental Europe, Southeast Asia, and Latin America becoming significant export markets for the Meteor 350, Himalayan, Classic 350, and Hunter 350 platforms.

3. Connected and Smart Two-Wheeler Technology Adoption

India’s two-wheeler market is rapidly adopting connected vehicle technology features that were until recently exclusive to premium and luxury automobiles. Bluetooth connectivity, GPS navigation with turn-by-turn display on the instrument cluster, trip analytics mobile apps, and over-the-air software updates are now featured on mainstream 125–160cc motorcycles from Hero MotoCorp and Honda at price points below INR 100,000.

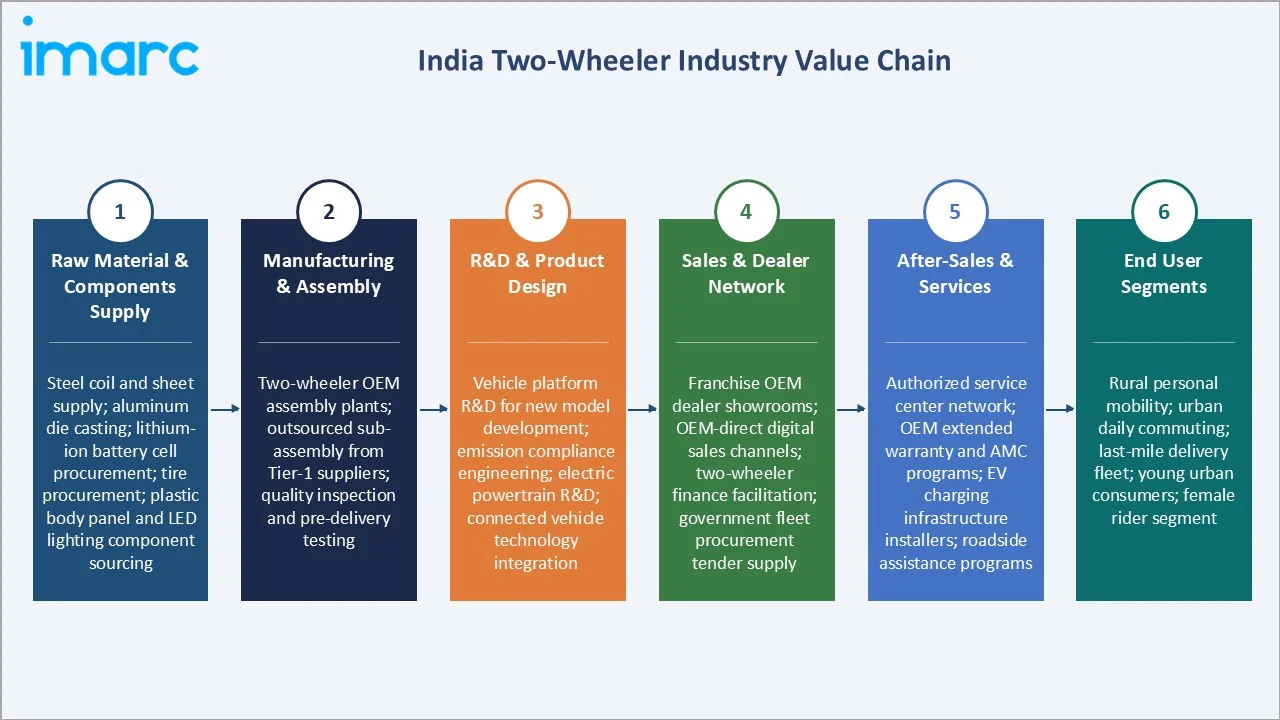

Industry Value Chain Analysis

The India two-wheeler market value chain spans raw material supply through end consumer deployment, with OEM manufacturing and dealer network distribution serving as the central commercial stages that determine competitive success.

|

Stage |

Key Players / Examples |

| Raw Material & Components Supply | Steel coil and sheet supply; aluminum die casting; lithium-ion battery cell procurement; tire procurement; plastic body panel and LED lighting component sourcing |

| Manufacturing & Assembly | Two-wheeler OEM assembly plants; outsourced sub-assembly from Tier-1 suppliers; quality inspection and pre-delivery testing |

| R&D & Product Design | Vehicle platform R&D for new model development; emission compliance engineering; electric powertrain R&D; connected vehicle technology integration |

| Sales & Dealer Network | Franchise OEM dealer showrooms; OEM-direct digital sales channels; two-wheeler finance facilitation; government fleet procurement tender supply |

| After-Sales & Services | Authorized service center network; OEM extended warranty and Annual Maintenance Contract (AMC) programs; EV charging infrastructure installers; roadside assistance programs |

| End User Segments | Rural personal mobility; urban daily commuting; last-mile delivery fleet; young urban consumers; female rider segment |

Technology Landscape in the India Two-Wheeler Industry

BS6 Phase 2 ICE Technology

India’s two-wheeler ICE technology is now operating under Bharat Stage 6 Phase 2 (BS6 Phase 2 or OBD-2) emission standards, the most stringent emission regulation India has implemented for two-wheelers, requiring fuel injection systems, catalytic converters, oxygen sensors, and onboard diagnostic systems that monitor real-time emission system performance. The transition to BS6 Phase 2 compliance has increased two-wheeler manufacturing complexity and component cost, but has also enabled the adoption of fuel injection technology that improves fuel efficiency, cold start performance, and throttle response.

Electric Two-Wheeler Powertrain Technology

India’s electric two-wheeler segment has developed a distinct technology architecture optimized for India’s urban commuter use case: battery packs of 2–3 kWh providing 80–120 km real-world range, permanent magnet synchronous motors (PMSM) of 3–6 kW peak power output, and lithium-ion NMC or LFP cell chemistry depending on OEM cost versus energy density trade-off preference. Ather Energy’s proprietary battery management system (BMS) with cell-level balancing and thermal management has set a benchmark for performance-oriented EV scooter technology in India.

Advanced Rider Assistance and Safety Technology

India’s two-wheeler market is progressively adopting advanced rider assistance and safety technologies that have been standard on premium European and Japanese motorcycles for a decade. Anti-lock Braking Systems (ABS) and Combined Braking System (CBS) are now mandatory for all two-wheelers under CMVR (Central Motor Vehicles Rules) regulation, creating a safety technology baseline that has progressively improved road safety outcomes for two-wheelers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Motorcycle | 56.0% |

2025 |

| Technology | ICE | 90.0% |

2025 |

| Transmission |

Manual |

78.0% |

2025 |

| Engine Capacity | 100-125cc | 42.0% | 2025 |

| Fuel Type | Petrol | 47.0% | 2025 |

| End-User | Personal | 94.0% | 2025 |

| Distribution Channel | Offline Channels | 89.0% | 2025 |

|

Region |

West and Central India | 34.0% |

2025 |

By Type

The type segment is analyzed across motorcycle (56.0%), scooters (28.0%), electric two-wheeler (11.0%), and mopeds (5.0%). Motorcycle encompasses three sub-segments with distinct consumer profiles: the entry/commuter segment serving rural first-time buyers and urban budget commuters; the executive/mid-segment serving urban and semi-urban aspirational commuters; and the premium/super-premium segment capturing India’s growing affluent motorcycle enthusiast market.

To access detailed market analysis, Request Sample

Scooters serve urban and peri-urban commuters prioritizing automatic transmission convenience, underbody storage, and rider comfort, with Honda Activa anchoring the automatic scooter market. Electric two-wheelers are growing at approximately 22% CAGR, concentrated in the scooter format with motorcycle formats beginning to enter the market.

By Technology

The technology segment is led by ICE (90.0%) and electric (10.0%). ICE technology encompasses the full spectrum of petrol-powered two-wheelers, all compliant with BS6 Phase 2 emission norms, with fuel injection, catalytic converters, and OBD-2 onboard diagnostics. The ICE segment’s value is growing above its volume growth due to premiumization toward higher-displacement, feature-rich models with connected technology, ABS, traction control, and riding modes.

Electric technology is growing at approximately 22.5% CAGR and is expected to reach 20–25% market share by 2028–2030 as FAME-III subsidies sustain affordability, battery costs decline, and charging infrastructure expands to Tier-2 cities. The electric segment is currently concentrated in urban markets where home charging access, shorter commute distances, and higher average income levels support the EV value proposition more strongly than in rural or semi-urban markets.

Regional Market Insights

West and Central India’s 34.0% market leadership reflects Maharashtra’s large urban two-wheeler consumption base, Gujarat’s prominent two-wheeler manufacturing and consumption concentration, and the vast rural populations of Madhya Pradesh and Rajasthan that depend heavily on motorcycles for personal mobility.

South India at 29.0% reflects Tamil Nadu’s position as India’s leading two-wheeler manufacturing state (TVS Motor, Ola Electric, Ather Energy, and Royal Enfield all with Tamil Nadu manufacturing), alongside Andhra Pradesh’s, Telangana’s, and Karnataka’s large two-wheeler consuming markets.

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

| West & Central India | 34.0% | Maharashtra’s large urban scooter and premium motorcycle market in Mumbai, Pune, and Nashik; Gujarat’s commercial and personal motorcycle demand including major manufacturing clusters; Madhya Pradesh and Rajasthan rural motorcycle demand from expanding agricultural income |

| South India | 29.0% | Tamil Nadu as India’s largest two-wheeler manufacturing state; Andhra Pradesh and Telangana rural motorcycle demand from large agricultural population; Karnataka’s Bengaluru as India’s highest EV two-wheeler adoption city |

| North India | 21.0% | UP and Bihar’s massive rural motorcycle market as the primary personal mobility solution; Punjab and Haryana’s high-income agricultural state premium motorcycle demand; Delhi-NCR urban scooter and EV two-wheeler market |

| East India | 16.0% | West Bengal’s Kolkata metropolitan scooter and motorcycle market; Odisha and Jharkhand rural motorcycle demand growing with mineral sector income; Assam and Northeast India motorcycle adoption for hill terrain personal mobility |

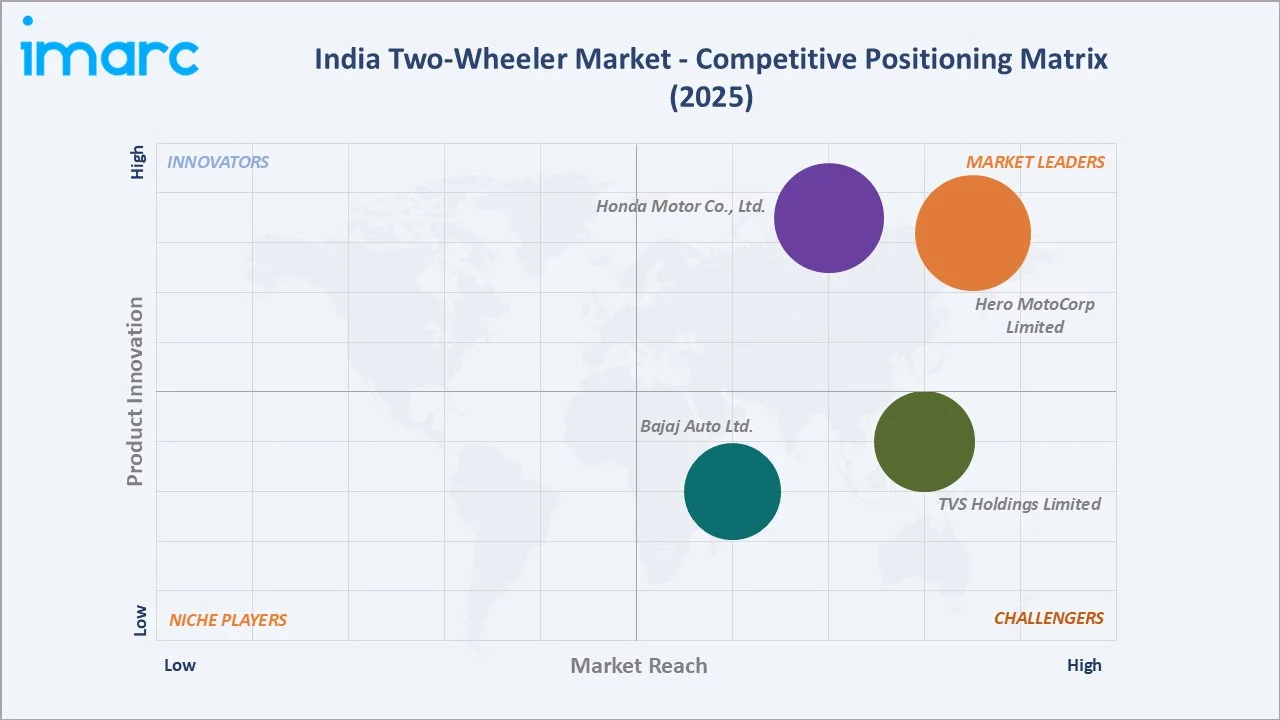

Competitive Landscape

The India two-wheeler market competitive landscape is one of the world’s most intensely contested, with top players collectively commanding approximately 80–85% of total market volume. The market’s competitive structure is being disrupted by electric vehicle entrants that are challenging the legacy OEMs’ distribution model, manufacturing approach, and product technology architecture simultaneously.

|

Company Name |

Key Products / Brands |

Market Position |

Core Strength |

| Hero MotoCorp Limited | XPluse 210, Xoom 160, Xtreme 250R, Karizma XMR, Harley-Davidson X440 T, Super Splendor XTEC 2.0, PASSION+, Splendor+ XTEC 2.0, Splendor+, among others |

Market Leader |

One of the world’s largest two-wheeler manufacturers; Splendor family the world’s highest-volume single motorcycle platform; pan-India dealer network; rural distribution leadership in North and Central India; Harley-Davidson partnership for premium segment entry |

| Honda Motor Co., Ltd. | Activa e:, QC1, CB750 Hornet E-Clutch, CB1000 Hornet SP, CB125 Hornet, CB350, CB350 H'ness, CB350RS, CB350C Special Edition, among others |

Market Leader |

Honda Activa is India’s highest-volume two-wheeler model; industry-leading fuel efficiency (kmpl) credentials for commuter models; premium CB-series and adventure motorcycles; strong brand trust in scooter and mid-segment motorcycle categories |

| TVS Holdings Limited | Apache series (RTX, RR 310, RTR 310), TVS Ntorq 150, TVS Ntorq 125, TVS Jupiter, TVS Jupiter 125, TVS iQube, TVS X, TVS Orbitor, TVS XL100 | Strong Challenger | Racing heritage brand driving premium positioning; iQube electric scooter building TVS’s EV platform capability; strong South India market presence and Tamil Nadu manufacturing scale |

| Bajaj Auto Ltd. | Pulsar series (NS125, N160, N250), Dominar 250, Dominar 400, Platina 100, Platina 110, Avenger 220 Cruise, Avenger 220 Street, CT 110X, Chetak Electric scooter, among others |

Strong Challenger |

Pulsar brand India’s leading premium mid-segment motorcycle platform; Triumph partnership for India-manufactured global premium motorcycles; Chetak Electric scooter with strong brand legacy |

New entrants including Ola Electric and Ather Energy have captured significant electric scooter market share, with Ola Electric building 30%+ electric scooter market share through aggressive pricing and direct-to-consumer sales.

Key Company Profiles

Hero MotoCorp Limited

Hero MotoCorp Limited is one of the world’s largest two-wheeler manufacturers. The company’s commercial dominance is built on the Splendor platform and a pan-India dealer network.

- Brand/Products: XPluse 210, Xoom 160, Xtreme 250R, Karisma XMR, Harley-Davidson X440 T, Super Splendor XTEC 2.0, PASSION+, Splendor+ XTEC 2.0, Splendor+, Mavrick 440, and Vida V1 and V1 Pro electric scooters, among others.

- Recent Developments: In July 2026, Hero MotoCorp Limited announced plans to launch new motorcycles under the Hero and Harley-Davidson brands in FY2026–27, targeting India’s fast-growing 150–350cc premium segment. The expansion is supported by rising premium motorcycle demand and lower GST on sub-350cc models.

- Strategic Focus: Rural market leadership defense through network expansion in Tier-3/4 markets; executive segment growth through 125–160cc model innovation; Harley-Davidson partnership leverage for premium segment credibility.

Honda Motor Co., Ltd.

Honda Motor Co., Ltd.’s subsidiary Honda Motorcycle and Scooter India is India’s second-largest two-wheeler manufacturer and the country’s leading scooter OEM. Honda Activa has been the defining product of India’s automatic scooter segment.

- Brand/Products: Honda Activa 6G/7G; Activa e:, QC1, CB750 Hornet E-Clutch, CB1000 Hornet SP, CB125 Hornet, CB350, CB350 H'ness, CB350RS, and CB350C Special Edition, among others.

- Recent Developments: In July 2026, Honda Motorcycle & Scooter India announced plans to launch two to three new premium motorcycles above 200cc as it strengthens its presence in India’s growing 151cc–350cc segment. The company also plans to expand its electric-scooter portfolio and local manufacturing capacity to reduce its dependence on commuter motorcycles.

- Strategic Focus: Activa platform leadership defense in the automatic scooter segment through continuous feature and efficiency improvements; CB-series premium motorcycle expansion building Honda’s 200cc+ market presence; Activa Electric development for EV segment entry with the market’s most trusted scooter brand.

Market Concentration Analysis

The India two-wheeler market exhibits high concentration in the ICE segment, with key players collectively commanding approximately 80–85% of ICE two-wheeler unit sales. Hero MotoCorp Limited alone holds approximately 33–35% market share by unit volume across commuter motorcycle categories, while Honda Motor Co., Ltd. leads the scooter segment with Activa’s dominant market position. Royal Enfield holds 95%+ share of the 350–500cc premium Indian motorcycle segment.

The electric two-wheeler segment is significantly fragmented, with Ola Electric, Ather Energy, TVS iQube, Bajaj Chetak, and Honda Activa Electric together competing for market share in a category where no single company has established the dominant position that Hero holds in ICE commuter motorcycles.

Investment & Growth Opportunities

Fastest Growing Segments

Electric Two-Wheeler type (~22.0% CAGR, fastest type segment); Electric technology (~22.5% CAGR); premium motorcycle 200cc+ segment (~12–15% CAGR outpacing commuter segment); last-mile delivery fleet EV electrification; export market development for electric scooters and premium motorcycles; and connected two-wheeler software and telematics services represent the highest-growth investment vectors within India’s two-wheeler market through 2034.

Emerging Market Expansion

India’s East India region represents the most significant geographic market expansion opportunity for two-wheeler OEMs and dealers. Bihar, Jharkhand, Odisha, and the Northeast states are experiencing above-average rural income growth from government schemes and natural resource sector development that is progressively converting rural households from non-motorized to two-wheeler mobility. Bihar alone represents a large incremental market as rural income thresholds enabling first-time motorcycle purchase are crossed by more households annually.

Venture and Institutional Investment Trends

- Electric two-wheeler startup investment continues at substantial scale in India: Ola Electric’s IPO and subsequent public market valuation, Ather Energy’s IPO preparation, and investment rounds for Ultraviolette, Ampere, and other EV startups collectively reflect venture and institutional confidence in India’s EV two-wheeler transition. The PLI scheme for ACC batteries is attracting strategic investment in domestic lithium-ion cell manufacturing that will progressively reduce EV manufacturing cost for Indian two-wheeler OEMs.

- Premium motorcycle market investment from international OEMs is accelerating: Triumph’s Bajaj partnership, BMW Motorrad’s TVS distribution, Harley-Davidson’s Hero MotoCorp partnership, and direct investment by KTM (through Bajaj), Kawasaki, and Suzuki in India market premium products collectively signal international confidence in India’s premium motorcycle segment growth, attracting sustained product and marketing investment across 200–650cc categories.

Future Market Outlook (2026-2034)

The India two-wheeler market is positioned for sustained, value-led growth through 2034. From a base of USD 24.5 Billion in 2025, the market is projected to reach USD 46.1 Billion by 2034 at a CAGR of 7.08%. India will remain the world’s largest two-wheeler market by unit volume throughout the forecast period, with annual sales growing from approximately 19–20 million units in 2025 toward 25–27 million units by 2034.

By 2034, electric two-wheelers will have grown from 11.0% to an estimated 25–30% of the type segment value as FAME-III subsidies, battery cost parity with ICE, and expanding charging infrastructure make electric the default choice for urban and semi-urban commuter segments. Electric technology will correspondingly grow from 10.0% to approximately 25–30% of total market value.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 65 industry participants in 2024–2025, including two-wheeler OEM product and marketing managers, franchise dealer network principals across urban and rural geographies, two-wheeler finance company (NBFC) underwriting managers with portfolio performance data, and two-wheeler accessory and aftermarket parts distributors tracking aftermarket demand trends.

Secondary Research

Secondary research encompassed SIAM (Society of Indian Automobile Manufacturers) monthly and annual two-wheeler production and sales statistics, VAHAN database retail registration data by state and vehicle category, Ministry of Heavy Industries FAME program disbursement data, IRDAI (Insurance Regulatory and Development Authority of India) two-wheeler insurance premium data tracking active vehicle base, and OEM annual reports.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating SIAM unit sales growth projections by segment, average selling price trend modelling by segment based on premiumization rate and EV penetration, FAME-III subsidy scenario analysis impact on EV share trajectory, rural income growth projections from the Ministry of Agriculture and MGNREGS data affecting first-time buyer volume, and population-to-two-wheeler penetration gap analysis by state for geographic growth modelling.

India Two-Wheeler Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Scooters, Mopeds, Motorcycle, Electric Two-Wheeler |

| Technologies Covered | ICE, Electric |

| Transmissions Covered | Manual, Automatic |

| Engine Capacities Covered | <100cc, 100-125cc, 126-180cc, 181-250cc, 251-500cc, 501-800cc, 801-1600cc, >1600cc |

| Fuel Types Covered | Gasoline, Petrol, Diesel, LPG/CNG, Battery |

| End Users Covered | Personal, Commercial |

| Distribution Channels Covered | Offline, Online |

| Regions Covered | North India, West and Central India, East India, South India |

| Companies Covered | Hero MotoCorp Limited, Honda Motor Co. Ltd., TVS Holdings Limited, Bajaj Auto Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Two-Wheeler Market Report

The India two-wheeler market reached USD 24.5 Billion in 2025 and is projected to reach USD 46.1 Billion by 2034.

The market is expected to grow at a CAGR of 7.08% during 2026-2034, driven by rising rural incomes expanding the two-wheeler buyer base, FAME-III government subsidies accelerating electric two-wheeler adoption, and last-mile delivery fleet electrification creating fleet EV procurement volume.

West and Central India lead with a 34.0% market share in 2025, driven by Maharashtra’s large urban and semi-urban two-wheeler consumption, Gujarat’s prominent manufacturing and consumer base, and the vast rural motorcycle-dependent populations of Madhya Pradesh and Rajasthan.

Motorcycle dominates with a 56.0% share in 2025, reflecting the type’s indispensable role as the primary personal mobility solution for India’s rural population and the aspirational premium product for India’s growing urban middle class, spanning entry-level commuter through super-premium subcategories.

ICE technology holds the dominant share at 90.0%, reflecting the established conventional petrol-powered powertrain’s price advantage, ubiquitous fueling infrastructure, and consumer familiarity.

Some of the key players include Hero MotoCorp Limited, Honda Motor Co., Ltd., TVS Holdings Limited, and Bajaj Auto Ltd.

Key drivers include rising rural income from PM-KISAN and agricultural income growth expanding the first-time buyer base, FAME-III electric vehicle subsidies sustaining EV two-wheeler affordability, and last-mile delivery fleet electrification driving bulk EV procurement from e-commerce and food delivery platforms.

Key challenges include high input material cost volatility, limited EV charging infrastructure in Tier-2/3 cities constraining electric adoption beyond metros, battery localization dependence on imported Chinese and Korean lithium-ion cells creating supply and cost risk, and competitive pressure from electric-native startups.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)