India Unified Payments Interface (UPI) Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Unified Payments Interface (UPI) Market Size, Share, Trends & Forecast (2026-2034)

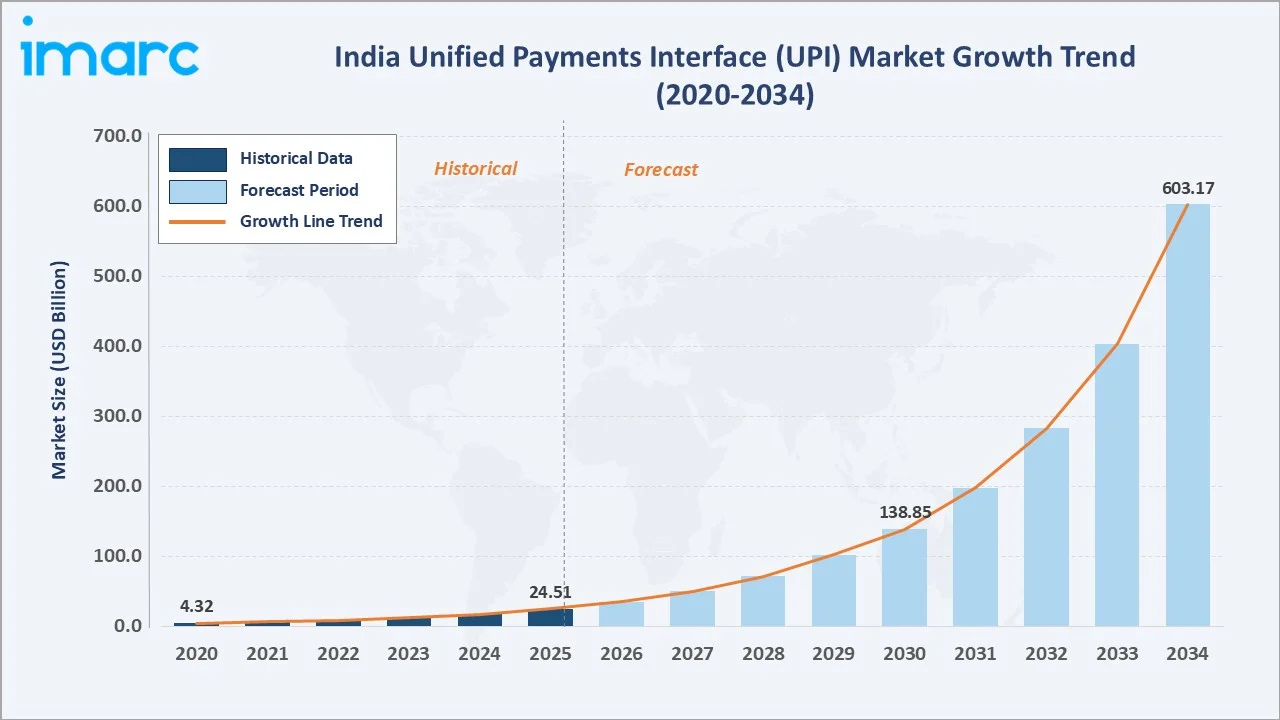

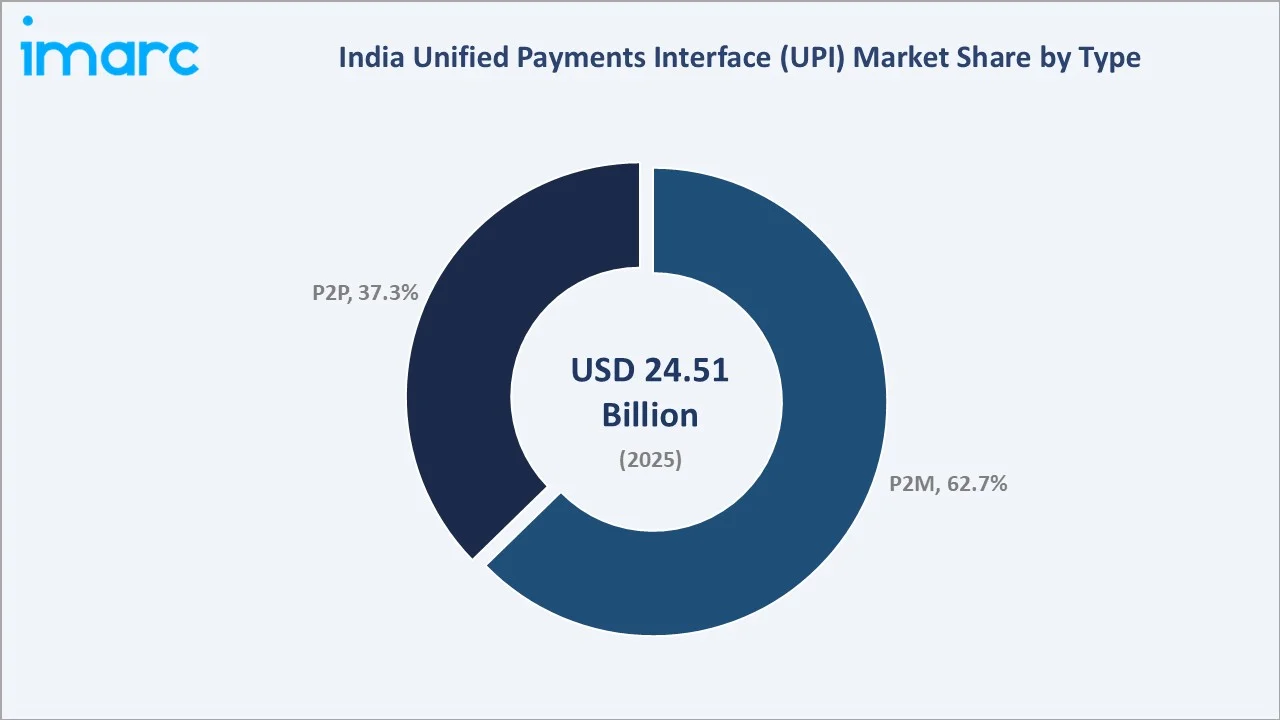

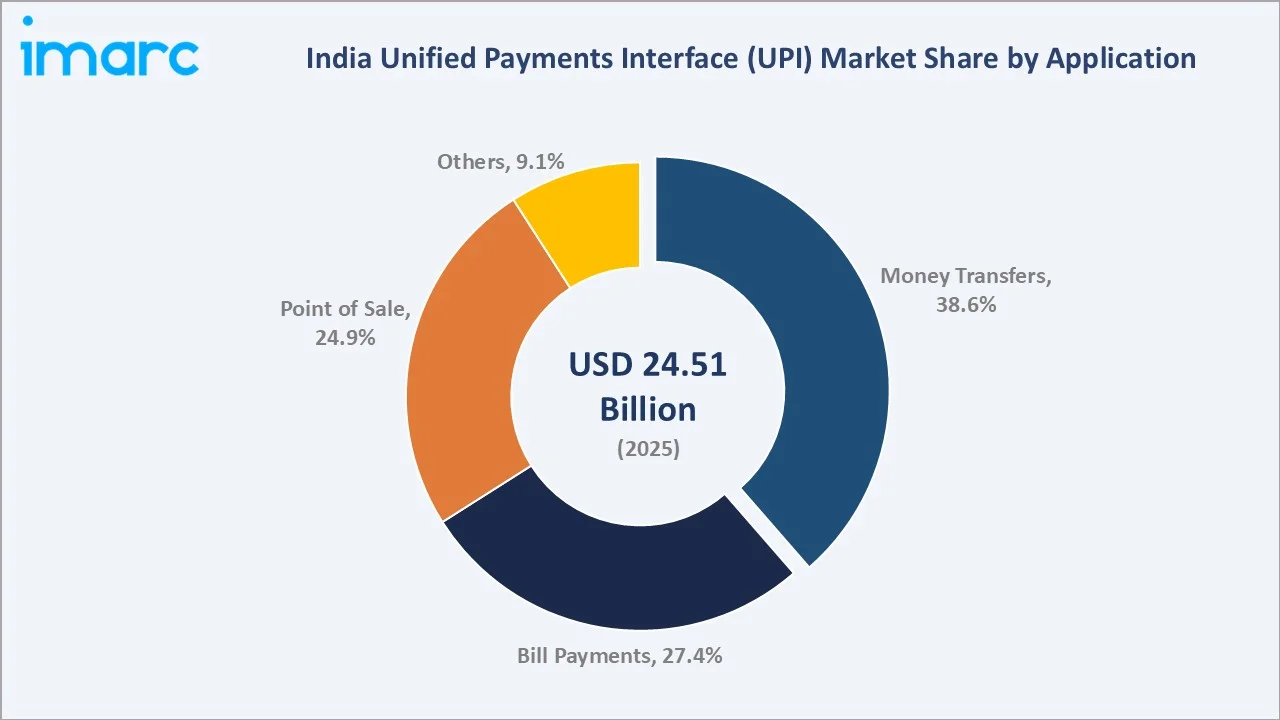

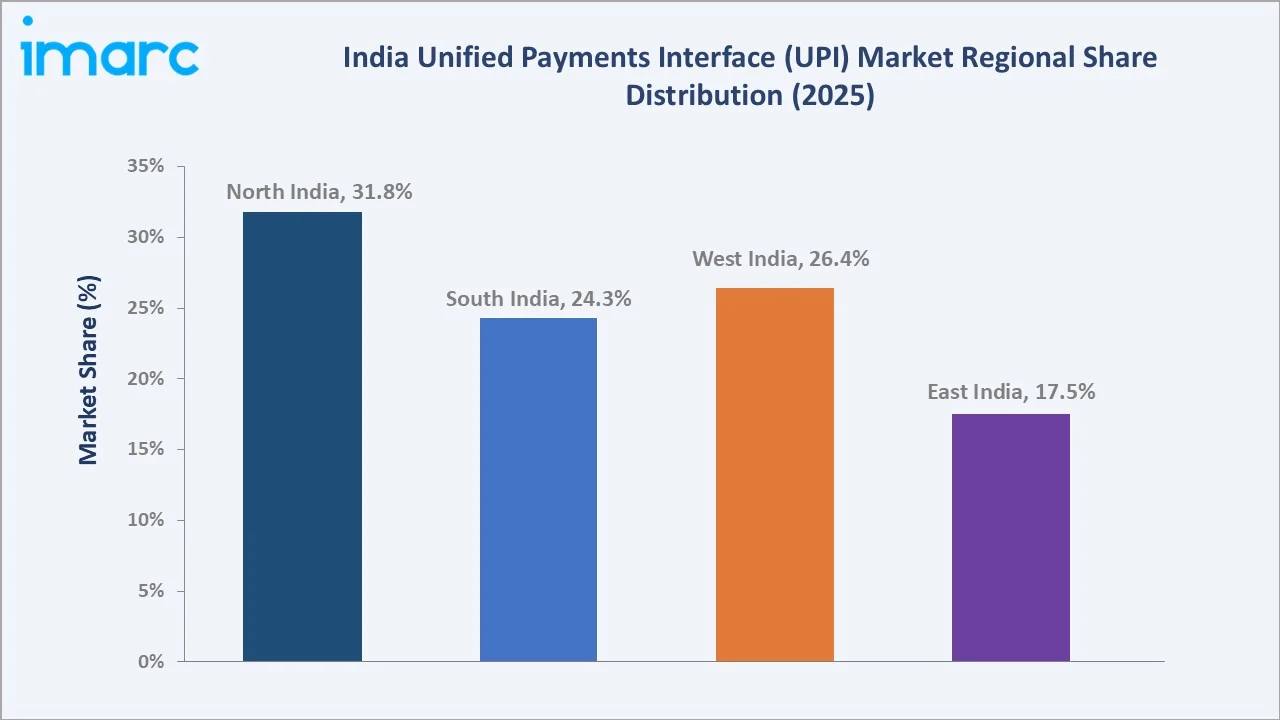

The India Unified Payments Interface (UPI) market reached USD 24.51 Billion in 2025 and is projected to reach USD 603.17 Billion by 2034, growing at a CAGR of 41.47% during 2026-2034. The market is driven by the government's Digital India initiative, rapid smartphone penetration exceeding 900 million subscriptions, and NPCI's zero-MDR framework that has onboarded around 70 million QR-enabled merchants nationwide. North India leads all regions with 31.8% market share in 2025, supported by high commercial density in Delhi-NCR and Punjab. Money Transfers leads by application at 38.6%, reflecting UPI's core remittance use case among 500+ million active users. The Reserve Bank of India's approval for credit-on-UPI, linking transactions to overdraft accounts and RuPay credit cards, is unlocking a new high-value transaction corridor, further underpinning India's global leadership in real-time payments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.51 Billion |

|

Forecast Market Size (2034) |

USD 603.17 Billion |

|

CAGR (2026-2034) |

41.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

P2M (62.7%, 2025) |

|

Dominant Application |

Money Transfers (38.6%, 2025) |

|

Leading Region |

North India (31.8%, 2025) |

India UPI market expanded from USD 4.32 Billion in 2020 to USD 24.51 Billion in 2025, anchored at USD 138.85 Billion in 2030, and forecast to reach USD 603.17 Billion by 2034. The market is commercially anchored by NPCI's interoperable real-time payment infrastructure, which processed over 24,162 crore transactions in FY 2025-26, an almost 12,000-fold surge since UPI's April 2016 launch, as reported by the Press Information Bureau (PIB), Government of India.

To get more information on this market, Request Sample

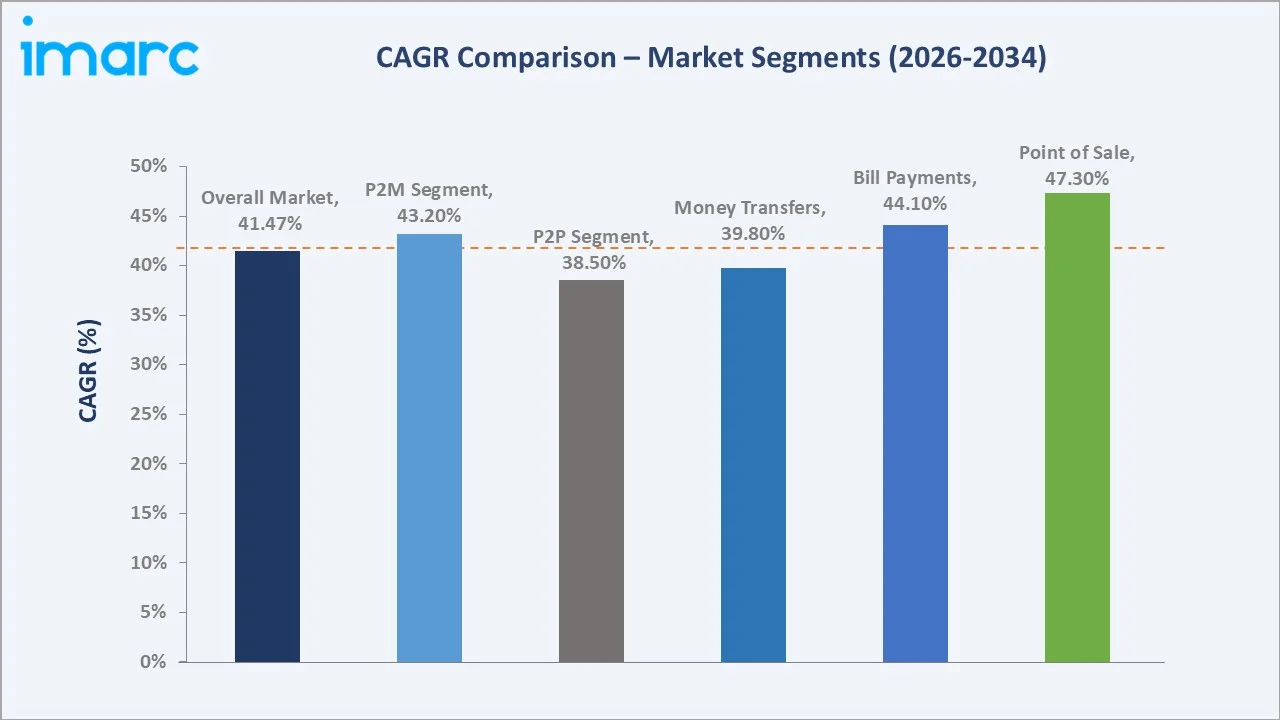

The Point-of-Sale application segment grows fastest at approximately 47.3% CAGR through India's ongoing shift from cash to digital at physical merchant points, rapid adoption of QR-code payment acceptance among MSMEs, and NPCI's merchant cashback programmes that accelerated rural merchant onboarding by an estimated 22% in 2024. UPI's integration with BBPS and e-RUPI government vouchers is extending its utility beyond consumer payments into institutional disbursements.

Executive Summary

India UPI market at USD 24.51 Billion in 2025 is one of the largest national real-time payment markets by value globally, reflecting India's 1.4 billion population's rapid adoption of digital financial infrastructure. The market's CAGR of 41.47% over 2026-2034 is among the highest of any payment system in the world, driven by the convergence of mass smartphone adoption, a regulatory framework that mandates zero merchant fees, and an expanding credit-on-UPI ecosystem. NPCI's data confirms UPI processed approximately 84% of India's retail digital payment volumes in FY 2024-25, cementing its structural dominance.

The P2M segment at 62.7% in 2025 reflects the commercial transformation of India's retail landscape, where over 700 million QR codes now enable UPI acceptance across kirana stores, fuel stations, e-commerce platforms, and government service points. Money Transfers (38.6%) and Bill Payments (27.4%) collectively account for two-thirds of UPI's application mix, while the fastest-growing Point of Sale segment (24.9%) is reshaping physical retail payments. Credit-on-UPI, including RuPay Credit Card linkage and bank overdraft integration, is emerging as the single most commercially impactful development, addressing India's 220 million credit-eligible but underserved consumer base.

The competitive landscape is anchored by PhonePe (45.3% volume share), Google Pay (34.6%), and Paytm (7.65%), which together control approximately 87.6% of UPI transaction volume as of December 2025. However, emerging challengers, including Navi, super.money, and BHIM, are gaining share through credit integration, lifestyle rewards, and government-backed inclusion initiatives. International UPI expansion across 10+ countries, NPCI's projection of 1 billion daily transactions by FY 2026-27, and the convergence of UPI with the Account Aggregator framework collectively define the market's outlook through 2034.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

P2M - 62.7% share (2025) |

|

Dominant Application |

Money Transfers - 38.6% market share (2025) |

|

Leading Region |

North India - 31.8% share (2025) |

|

Market Opportunity |

Credit-on-UPI, UPI Lite for rural markets, cross-border UPI expansion |

Key Analytical Observations Supporting The Above Data:

- P2M at 62.7%: The P2M segment dominates because zero-MDR policy eliminated the cost barrier for merchants, while NPCI's standardised QR codes enabled frictionless onboarding of 300 million+ merchant points. Urban kirana stores, fuel stations, and e-commerce platforms collectively drove P2M's rise from a minority segment in 2020 to the market's dominant category by 2025.

- Money Transfers at 38.6%: Money Transfers lead UPI applications through India's deep inter-state and intra-family remittance culture, UPI's universal interoperability across 700+ banks, and the platform's ability to process P2P transfers instantly at any time. Over 15 billion monthly transactions in FY 2024-25 were P2P transfers, per NPCI product statistics.

- North India at 31.8%: North India's leadership reflects Delhi-NCR's concentration of corporate payment activity, India's highest per-capita UPI merchant density in Greater Noida and Gurugram corridors, and Punjab's above-national adoption of UPI for agricultural input payments and cross-border remittances from the NRI diaspora.

India Unified Payments Interface (UPI) Market Overview

India UPI market is commercially positioned at a unique intersection: the world's largest democracy with a rising digital-first middle class has created one of the world's fastest-growing real-time payment ecosystems by transaction volume. UPI's architecture, an open, interoperable, account-agnostic payment rail governed by the National Payments Corporation of India (NPCI), has enabled rapid commercial scale that no proprietary payment network has matched. The platform's core innovation is the Virtual Payment Address (VPA), which decouples payment initiation from bank account details, enabling instant authenticated transfers with two-factor security (device binding + UPI PIN).

India UPI ecosystem integrates six commercial layers: infrastructure providers (telecom networks, cloud platforms), platform operators (NPCI's real-time settlement rails), financial institutions (700+ member banks as of December 2025), third-party application providers (PhonePe, Google Pay, Paytm, BHIM, and 40+ others), a merchant network of 300 million+ QR-enabled points, and 500 million+ active end users.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

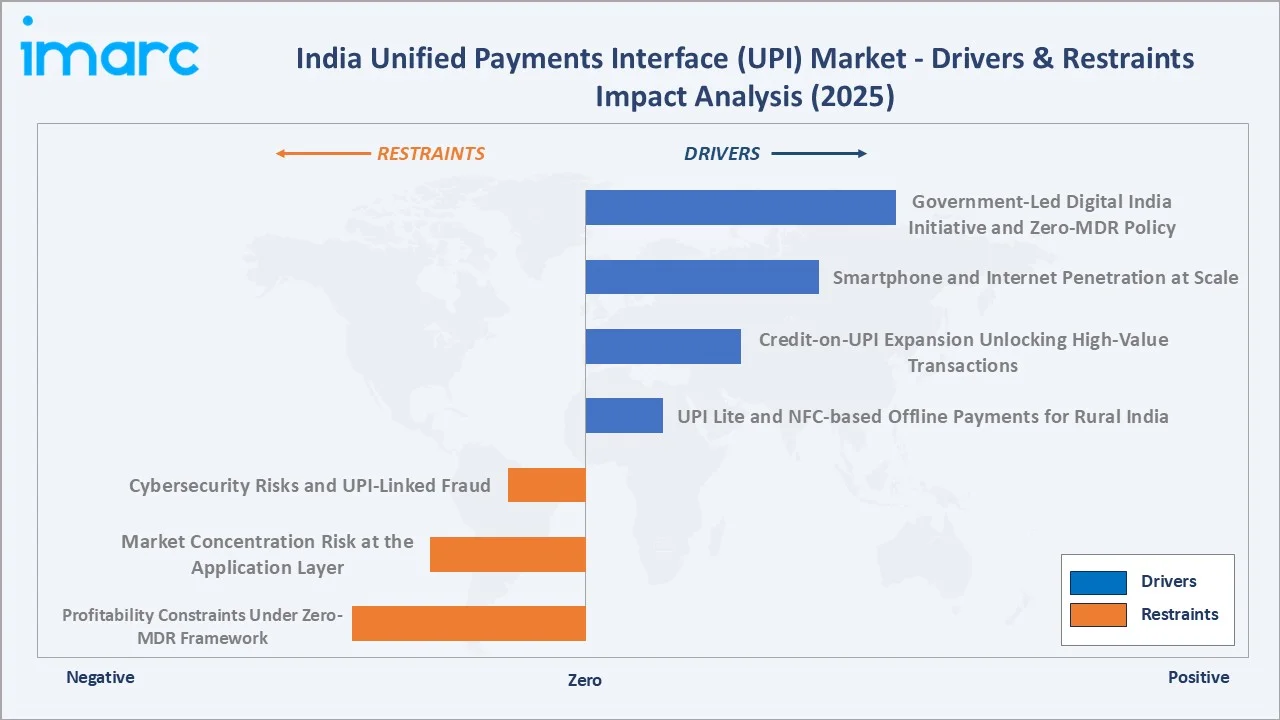

- Government-Led Digital India Initiative and Zero-MDR Policy: The Digital India programme and zero Merchant Discount Rate (MDR) policy are collectively the most commercially consequential policy interventions in India's payment history. Zero-MDR removed the cost barrier that had limited merchant adoption of digital payments, enabling 500 million+ merchant QR points to be onboarded without economic friction. RBI's Annual Report 2024-25 confirms UPI's ~84% share of India's retail digital payment volumes.

- Smartphone and Internet Penetration at Scale: India's 900+ million mobile subscriptions, declining data costs (Rs 10-15 per GB on average), and 5G rollout across 100+ cities have created the technical foundation for UPI's hypergrowth. Over 60 million new mobile internet users were added in 2024, each representing a potential UPI first-time user, as per TRAI's subscriber reports.

- Credit-on-UPI Expansion Unlocking High-Value Transactions: The Reserve Bank of India's approval for UPI credit line linkage, enabling bank overdrafts and RuPay Credit Card transactions via UPI, is transforming the platform from a utility payment tool to a credit enablement channel. In October 2024, UPI processed a record 16.58 billion transactions in a single month, driven partly by credit-linked high-value purchases in e-commerce and travel.

Market Restraints

- Cybersecurity Risks and UPI-Linked Fraud: The rapid scale of UPI has attracted sophisticated fraud schemes including phishing, social engineering ("UPI refund" scams), and SIM cloning. The Indian Cyber Crime Coordination Centre (I4C) reported a significant increase in UPI-related fraud cases in 2024. Platform providers are investing heavily in ML-based fraud detection, but the zero-MDR model limits their capacity to fund security infrastructure.

- Market Concentration Risk at the Application Layer: PhonePe (45.3%) and Google Pay (34.6%) together control approximately 80% of UPI transaction volume, creating systemic dependency on two foreign-majority-owned platforms for a nationally critical payment infrastructure.

- Profitability Constraints Under Zero-MDR Framework: India's zero-MDR mandate makes direct monetisation of UPI transaction volume impossible for third-party app providers. Players like PhonePe, Google Pay, and Paytm rely entirely on adjacent financial services (lending, insurance, investments) for revenue. This limits the capacity of smaller providers to invest in feature development and security, potentially concentrating innovation further in the top two platforms.

Market Opportunities

- UPI Lite and NFC-based Offline Payments for Rural India: NPCI's UPI Lite feature, enabling offline transactions below Rs 500 via on-device processing, targets an estimated 200 million users in low-connectivity rural areas. NFC-based UPI Lite X (Tap & Pay) is being deployed in mass transit systems, vending machines, and rural retail, positioning UPI to replace physical cash in micro-transaction environments.

- International UPI Expansion as a Cross-Border Revenue Stream: NPCI International Payments Limited (NIPL) has enabled UPI acceptance in 10+ countries including Singapore, UAE, France, and Mauritius. Japan and Malaysia rollouts are in advanced stages. Cross-border UPI transactions could contribute a USD 10+ Billion incremental market opportunity by 2027, driven by 30 million+ Indian diaspora and inbound tourist digital payments.

Market Challenges

- Rapid Technological Evolution Requiring Continuous Platform Investment: UPI's technology stack must continuously evolve to support NFC, conversational AI payments, CBDC interoperability, and international standards - requiring substantial and ongoing capital investment. Smaller PSPs and third-party providers face structural disadvantages in keeping pace with PhonePe and Google Pay's technology spending.

- Digital Literacy Gap in Rural and Semi-Urban Markets: Despite 22% growth in rural merchant UPI adoption driven by government cashback programmes, end-user digital literacy constraints continue to limit deeper rural penetration. Feature phone users in rural India, estimated at 250 million, require USSD-based UPI and voice interfaces that are nascent in commercial deployment.

Emerging Market Trends

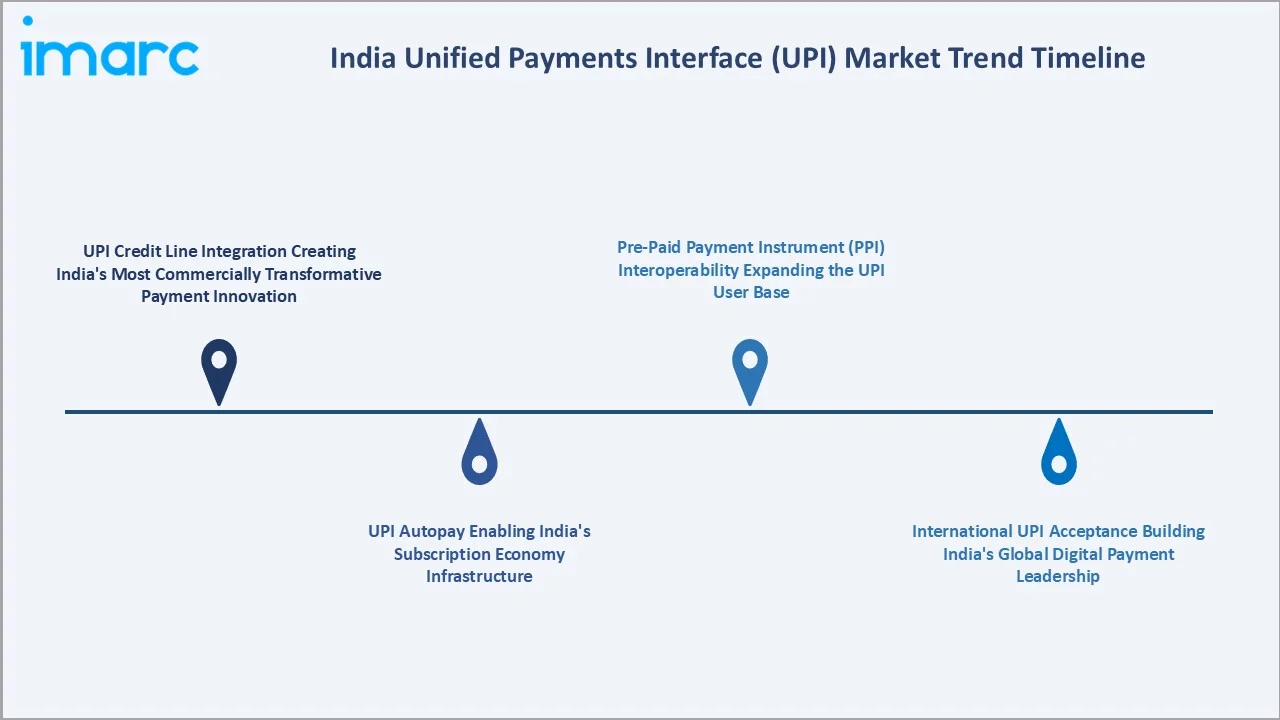

1. UPI Credit Line Integration Creating India's Most Commercially Transformative Payment Innovation

Credit-on-UPI - the integration of bank overdrafts and RuPay Credit Card transactions into the UPI flow - is the market's most commercially transformative trend. It transforms UPI from a debit-driven utility into a credit-enabled commerce platform. The RBI's approval for UPI credit line linkage, the growth of BNPL products embedded in UPI flows, and the Account Aggregator framework enabling real-time credit assessment using UPI transaction history collectively define a new USD 50+ Billion commercial opportunity within the UPI ecosystem by 2030.

2. UPI Autopay Enabling India's Subscription Economy Infrastructure

UPI Autopay (One Time Mandate) is becoming the payment backbone of India's fast-growing subscription economy. OTT platforms, insurance providers, SIP investment platforms, and utility providers are migrating recurring payments to UPI-based mandates. NPCI data shows Autopay mandates grew over 2x in FY 2024-25. The introduction of UPI Smart Mandates with enhanced controls is expected to accelerate institutional adoption of recurring UPI payments across BFSI and consumer services.

3. Pre-Paid Payment Instrument (PPI) Interoperability Expanding the UPI User Base

The RBI's December 2024 directive enabling interoperability of Pre-Paid Payment Instruments (PPIs) on UPI through third-party apps has materially expanded the UPI-accessible user base. Digital wallets including Paytm Wallet, PhonePe Wallet, and others can now participate fully in UPI transactions. This brings an estimated 70 million wallet-primary users into the UPI ecosystem, addressing a segment that previously transacted outside the interoperable UPI network.

4. International UPI Acceptance Building India's Global Digital Payment Leadership

International UPI acceptance across 10+ countries is transitioning from a regulatory pilot to a commercial reality. NPCI International Payments Limited (NIPL) reported that in January 2026, UPI processed over Rs 28.33 lakh crore in a single month, with cross-border corridors (Singapore, UAE, UK, France) contributing incrementally. Japan and Malaysia rollouts, combined with G20-level advocacy for UPI adoption as a model for global fast payment interoperability, position India's UPI as a potential global payment standard.

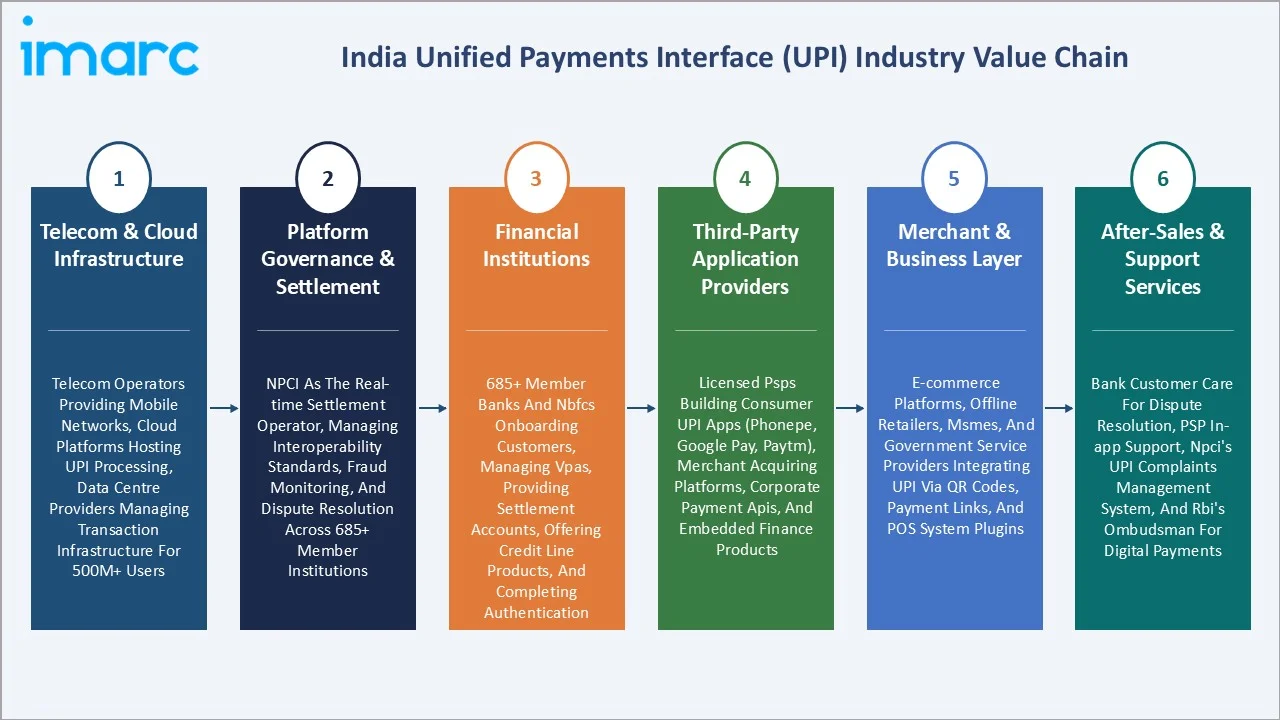

Industry Value Chain Analysis

India UPI value chain is one of the most commercially efficient of any payment system globally. Unlike card payment networks with multiple intermediary layers each extracting fees, UPI's zero-MDR architecture compresses the value chain's commercial structure: NPCI operates the settlement rails on a cost-recovery basis, member banks earn float income on settlement balances, and third-party app providers monetise through adjacent financial services. This structure is commercially consequential - it enables India's payment ecosystem to achieve global transaction volume at near-zero marginal cost per transaction.

|

Stage |

Key Participants |

|

Telecom & Cloud Infrastructure |

Telecom operators providing mobile networks, cloud platforms hosting UPI processing, data centre providers managing transaction infrastructure for 500M+ users |

|

Platform Governance & Settlement |

NPCI as the real-time settlement operator, managing interoperability standards, fraud monitoring, and dispute resolution across 700+ member institutions |

|

Financial Institutions |

700+ member banks and NBFCs onboarding customers, managing VPAs, providing settlement accounts, offering credit line products, and completing authentication |

|

Third-Party Application Providers |

Licensed PSPs building consumer UPI apps (PhonePe, Google Pay, Paytm), merchant acquiring platforms, corporate payment APIs, and embedded finance products |

|

Merchant & Business Layer |

E-commerce platforms, offline retailers, MSMEs, and government service providers integrating UPI via QR codes, payment links, and POS system plugins |

|

After-Sales & Support Services |

Bank customer care for dispute resolution, PSP in-app support, NPCI's UPI Complaints Management System, and RBI's Ombudsman for Digital Payments |

Technology Landscape in the India UPI Market

Core UPI Protocol and Two-Factor Authentication Architecture

UPI operates on a two-factor authentication (2FA) framework using device binding plus UPI PIN, built atop the Immediate Payment Service (IMPS) rails. UPI 2.0 introduced overdraft account linkage, invoice-in-the-inbox, and mandate creation for recurring payments. Transactions complete in under 10 seconds on average, with NPCI's infrastructure processing peak loads of 21.7 billion transactions in January 2026 - the highest monthly volume ever recorded by any real-time payment system globally.

UPI Lite and NFC-based Offline Payment Technology

UPI Lite enables offline payments below Rs 500 via on-device processing, eliminating the need for real-time bank server authentication for micro-transactions. UPI Lite X (NFC-based) enables contactless Tap & Pay transactions without internet connectivity, deployed in metro systems and retail. This technology stack targets India's 200 million users in low-connectivity environments and is positioned to displace physical cash at the micro-transaction level.

AI, ML, and Real-Time Fraud Prevention Systems

AI and machine learning models for real-time fraud detection are the most commercially critical technology investment in India's UPI ecosystem. PhonePe, Google Pay, and Paytm deploy multi-layer ML models analysing transaction velocity, device fingerprints, geographic signals, and social graph patterns to flag suspicious activity in milliseconds. NPCI's centralised risk management framework monitors all 700+ member institutions' transaction flows, while individual PSPs maintain proprietary fraud scoring models. The convergence of Aadhaar-based biometric authentication, face recognition UPI features, and AI-driven anomaly detection is progressively reducing the fraud rate even as transaction volumes scale exponentially.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

P2M |

62.7% |

2025 |

|

Application |

Money Transfers |

38.6% |

2025 |

|

Region |

North India |

31.8% |

2025 |

By Type

P2M leads at 62.7% (2025). The P2M segment encompasses India's most commercially diverse payment flows - from kirana store QR payments of Rs 50 to corporate B2B procurement transactions of Rs 5 lakh. P2M's commercial dominance reflects the transformation of India's 63 million MSME economy through digital payment acceptance enabled by NPCI's standardised QR architecture and zero-MDR policy.

To access detailed market analysis, Request Sample

P2P at 37.3% remains the foundation of UPI's consumer utility. Person-to-person transfers represent India's most frequent digital payment use case, driven by inter-state remittances, family fund transfers, and peer payment splitting. The average P2P ticket size in 2025 was approximately Rs 2,100, reflecting a mix of large family remittances and small friend-to-friend transfers.

By Application

Money Transfers lead at 38.6% (2025). This segment serves India's deeply embedded remittance culture - inter-state labour payments, NRI-to-family transfers, and business-to-business payments that collectively constitute India's highest-volume UPI application. UPI's 24/7 real-time settlement capability, combined with interoperability across all 700+ member banks, makes it the dominant mechanism for fund movement across India's geographically dispersed population.

Bill Payments at 27.4% reflects UPI's deep integration with BBPS (Bharat Bill Payment System), enabling utility, telecom, insurance, and subscription bill settlements through a single UPI interface. Point of Sale at 24.9% is the fastest-growing application segment at an estimated 47.3% CAGR, driven by the replacement of cash at physical retail and the expansion of merchant QR acceptance to petrol pumps, pharmacies, and roadside vendors. The Others category (9.1%) includes government disbursements, travel bookings, and UPI for capital markets transactions.

Regional Market Insights

North India's 31.8% market leadership reflects Delhi-NCR's commercial concentration, India's highest-density corporate payment activity, Punjab's above-national UPI adoption driven by NRI remittance inflows, and Uttar Pradesh's large MSME base increasingly transitioning to digital payments under government push programmes. The region accounts for the highest average UPI transaction value nationally due to its concentration of corporate, institutional, and high-value consumer payment flows.

|

Region |

Share (2025) |

Key India UPI Market Drivers & Characteristics |

|

North India |

31.8% |

High commercial density in Delhi-NCR drives corporate and institutional UPI adoption. Punjab's NRI remittance inflows create a high-value cross-border UPI use case. UP and Haryana's growing MSME base accelerates merchant QR adoption. |

|

West India |

26.4% |

Mumbai's financial sector drives institutional UPI volumes. Gujarat and Maharashtra's large MSME and manufacturing base creates high B2B UPI payment flows. Fintech ecosystem concentration in Mumbai-Pune corridor drives product innovation. |

|

South India |

24.3% |

Bengaluru's IT sector creates a digitally native, high-income UPI user base. Hyderabad and Chennai drive P2M adoption through tech-sector professional spending. Tamil Nadu's manufacturing economy drives industrial payment digitisation. |

|

East India |

17.5% |

West Bengal and Odisha show growing UPI penetration driven by government direct benefit transfers. Agricultural payment digitisation through e-RuPay and UPI is expanding rural adoption. Lowest current base creates the highest growth opportunity through 2034. |

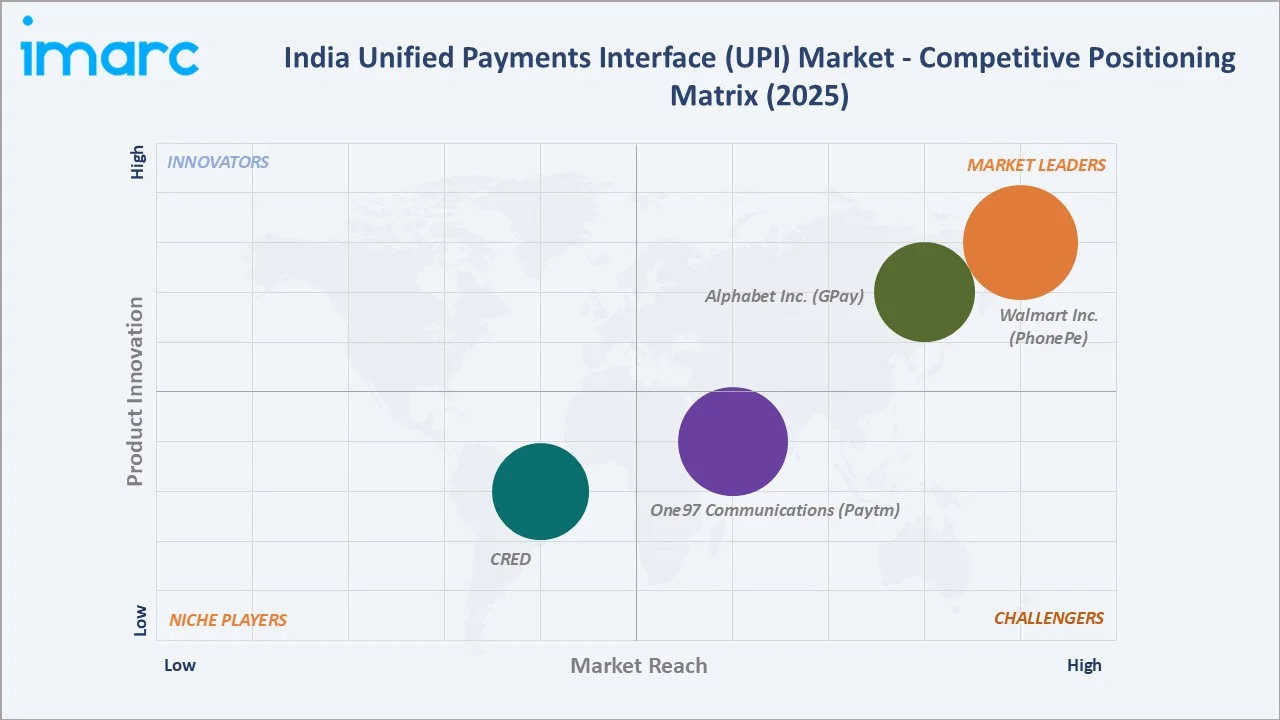

Competitive Landscape

India UPI market competitive landscape is commercially stratified into three tiers: a duopoly at the top (PhonePe + Google Pay controlling approximately 80% of transaction volume), an established third-tier (Paytm at 7.65%), and a growing challenger tier of 40+ niche and emerging players. This structure is commercially unique globally - it combines the network effects of a duopoly with the regulatory architecture of a public utility, creating a market where private competitive dynamics coexist with NPCI's public interest mandate.

|

Company |

Key Apps / Brands |

Market Position |

Core Strength |

|

|

PhonePe |

Market Leader |

Super-app with payments, insurance, investments, and lending. Largest merchant acquiring network. |

|

|

Google Pay (GPay) |

Market Leader |

Android ecosystem integration enabling pre-installed UPI access for 500M+ Android users. AI-powered financial insights and merchant discovery features. |

|

|

Paytm |

Challenger |

Pioneer of India's digital payments. Strong merchant acquiring base of 10M+ devices. |

|

|

CRED UPI |

Niche Player |

Premium credit card user base creating highest average transaction value among all UPI apps. CRED's transaction value is 3x BHIM's despite identical transaction volume. |

Key Company Profiles

Walmart Inc.

PhonePe, majorly owned by Walmart with approx. 71.77% stake, is India's largest UPI payment platform, founded in 2015. Headquartered in Bengaluru, it has grown from a UPI-only payments app to a financial super-app serving 700+ million registered users.

- Key Products: PhonePe UPI (P2P and P2M) solutions

- Recent Developments: In May 2026, PhonePe announced the launch of its AI-powered integration layer for merchants which aims to reduce integration timelines from weeks to minutes.

- Strategic Focus: Super-app expansion into financial services (insurance, lending, investments), international UPI market leadership in Southeast Asia and Middle East, and ONDC-enabled e-commerce integration to compete with Amazon and Flipkart.

Alphabet Inc. (Google)

Google Pay (GPay), a proprietary digital payment service and division wholly owned by Google, launched in India in September 2017 and rapidly became the second-largest UPI platform, leveraging Google's Android ecosystem which pre-installs on approximately 95% of India's smartphones.

- Key Products: Google Pay (P2P and P2M UPI)

- Recent Developments: In December 2025, Google announced Flex by Google Pay, a UPI-powered, digital, co-branded credit card designed to simplify and elevate the card experience for country’s financial needs.

- Strategic Focus: Deepening AI/ML financial personalisation within the GPay experience, expanding P2M market share through Google Maps and Search commerce integrations, and monetising through Google Pay's financial product distribution partnerships with leading banks.

Market Concentration Analysis

India UPI market is highly concentrated at the third-party application layer. The top three UPI apps (PhonePe, Google Pay, Paytm) collectively account for approximately 87.6% of transaction volume and approximately 89% of transaction value as of December 2025, per NPCI's public data dashboard. This concentration is commercially significant given that UPI is a nationally critical payment infrastructure handling approximately 84% of India's retail digital payment volumes.

NPCI's proposed 30% per-app volume cap, designed to prevent systemic dependency on any single private platform, has been delayed pending ecosystem readiness. Its eventual implementation would structurally reshape the competitive landscape, creating an estimated 15-20 percentage point market share opportunity for challengers. NPCI's certification requirement for UPI PSP licences maintains a high barrier to entry, protecting the ecosystem's integrity while concentrating competitive dynamics among approximately 40+ licensed providers.

Investment & Growth Opportunities

Highest Growth Segments

Point of Sale application segment at approximately 47.3% CAGR through 2034 as India's physical retail transitions from cash to digital. Credit-on-UPI at approximately 55%+ CAGR through embedded lending products for 220 million credit-eligible consumers. International UPI remittances at approximately 60%+ CAGR through NPCI International's expansion to 20+ countries by 2027, capturing inbound tourist payments and NRI diaspora remittances.

Emerging Investment Opportunities

India's UPI-infrastructure-adjacent fintech market represents India's most commercially dynamic segment for venture and growth capital. PhonePe's USD 12+ Billion valuation, CRED's premium-positioning premium, and Navi's credit-UPI strategy collectively demonstrate the diverse investment theses available within the UPI ecosystem. The certified pre-owned luxury goods and high-value consumer purchase financing via UPI credit lines represents an emerging commercial segment growing at 25-30% annually within the broader market.

Investment Themes

- Credit-on-UPI embedded lending platform investment for India's most commercially large underserved credit opportunity: India's 220 million credit-eligible but underserved consumers represent a USD 50+ Billion embedded lending opportunity accessible through UPI transaction data-based underwriting. OCEN-enabled lenders using UPI history for real-time credit scoring can price credit at significantly lower cost than traditional underwriting, creating a structural efficiency advantage.

- International UPI platform investment for India's most commercially novel cross-border payment revenue stream: NPCI International's cross-border UPI expansion creates a USD 10+ Billion cross-border transaction flow opportunity by 2027. Platforms positioning as UPI-enabled cross-border payment facilitators for the 30+ million Indian diaspora and inbound tourist digital payments can capture merchant and remittance economics outside India's zero-MDR domestic framework.

- UPI-native MSME financial services platform for India's 63 million business digital payment transition: India's 63 million MSMEs transitioning to UPI-based payment acceptance generate rich transaction data enabling merchant cash advances, invoice financing, and working capital credit products. Platforms combining UPI merchant acquiring with MSME credit underwriting can capture both payment processing relationships and high-margin lending economics.

Future Market Outlook (2026-2034)

India UPI market is projected to grow from USD 24.51 Billion in 2025 to USD 603.17 Billion by 2034, delivering a 41.47% CAGR over the forecast period. The market's anchor value of USD 138.85 Billion in 2030 represents a 5.7x increase from 2025, underpinned by three structural forces: India's digital economy expansion, the credit-on-UPI transformation, and international UPI acceptance growth. NPCI's projection of 1 billion daily UPI transactions by FY 2026-27 - versus 698 million daily average in 2025 - implies continued hypergrowth in transaction volume, which will translate to market value expansion as average transaction sizes increase through credit linkage.

The most commercially transformative development expected through 2034 is the full deployment of UPI 3.0+ features: conversational AI payments via voice interfaces, CBDC e-Rupee interoperability with UPI, NFC-based offline payments at scale, and deep credit integration through the Account Aggregator framework. By July 2025, UPI's daily transaction count had already surpassed Visa globally, positioning India's real-time payment system as the world's largest. This structural advantage - India as the world's proof-of-concept for universal, zero-cost digital payment infrastructure - will reinforce foreign investor and government interest in UPI expansion through 2034.

Three structural forces define India UPI market growth through 2034: India's wealth expansion creating a rapidly growing high-value digital payment consumer base; the credit-on-UPI framework unlocking non-cash spending by India's 220 million credit-eligible consumers; and India's international UPI expansion creating cross-border transaction economics unavailable in the domestic zero-MDR market. The convergence of these forces with 5G rollout, AI personalisation of financial services, and India's CBDC deployment will sustain the market's exceptional CAGR through the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews and expert consultations with India UPI market stakeholders, including Payment Technology Heads, Chief Digital Officers, Fintech Founders, Bank Digital Payments Heads, NPCI officials, and regulatory consultants familiar with RBI's payment policy. These primary inputs validated market sizing assumptions, competitive share estimates, and technology adoption timelines used in the quantitative model.

Secondary Research

Secondary research encompassed NPCI's UPI Product Statistics dashboard, RBI Annual Reports (2023-24, 2024-25), Ministry of Finance digital payments data, PIB government releases, BIS Papers on India's UPI organisation (BIS Papers No. 152, 2024), IMF payment system assessments, company annual reports and investor presentations (PhonePe, One97 Communications), and academic and industry publications on India's digital payment ecosystem.

Forecasting Models

Market revenue forecasts were developed using a transaction-volume-to-value conversion model: NPCI's historical transaction volume data multiplied by average transaction value per category, adjusted for the structural shift from small P2P payments toward larger P2M and credit-enabled transactions. CAGR projections incorporate NPCI's 1 billion daily transaction target by FY 2026-27, India's GDP growth forecasts, and the credit-on-UPI market expansion opportunity. Segmentation forecasts (by Type, Application, and Region) were developed using bottom-up share analysis validated against NPCI's public product statistics.

India Unified Payments Interface (UPI) Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | P2P, P2M |

| Applications Covered | Money Transfers, Bill Payments, Point of Sale, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Scope | Walmart Inc., Alphabet Inc. (Google), One97 Communications, CRED, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India unified payments interface (UPI) market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India unified payments interface (UPI) market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India unified payments interface (UPI) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Unified Payments Interface (UPI) Market Report

India UPI market reached USD 24.51 Billion in 2025, driven by NPCI's zero-MDR real-time payment infrastructure processing 228.3 billion transactions annually with 500+ million active users across 700+ member banks.

India UPI market grows at 41.47% CAGR during 2026-2034, reaching USD 603.17 Billion by 2034, driven by credit-on-UPI expansion, international UPI adoption, and India's continued transition from cash to digital payments at the merchant layer.

P2M (Person-to-Merchant) leads at 62.7% in 2025 through zero-MDR policy enabling frictionless merchant onboarding, 300 million+ QR-code merchant points, and rapid kirana and e-commerce platform adoption of UPI payment acceptance.

Money Transfers leads at 38.6% in 2025 through India's deep inter-state remittance culture, UPI's 24/7 real-time interoperability across 700+ banks, and the platform's universal adoption for family fund transfers and business payments.

North India leads at 31.8% in 2025 through Delhi-NCR's commercial density, India's highest corporate payment activity concentration, Punjab's NRI remittance inflows, and Uttar Pradesh's growing MSME digital payment base.

Leading companies include Walmart Inc. (PhonePe), Alphabet Inc. (GPay), One97 Communications (Paytm), and CRED, among others.

India UPI market is projected to reach USD 138.85 Billion by 2030, anchored by credit-on-UPI expansion reaching 220 million credit-eligible consumers, international UPI acceptance in 20+ countries, and NPCI's 1 billion daily transaction target.

Three priority investment opportunities: credit-on-UPI embedded lending for 220 million underserved consumers; international UPI cross-border payment platforms beyond India's zero-MDR domestic framework; and MSME financial services combining UPI merchant acquiring with working capital credit.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)