India Vehicle Financing Market Size, Share, Trends and Forecast by Vehicle Type, Loan Provider, Vehicle Condition, Purpose Type, and Region, 2026-2034

India Vehicle Financing Market Summary:

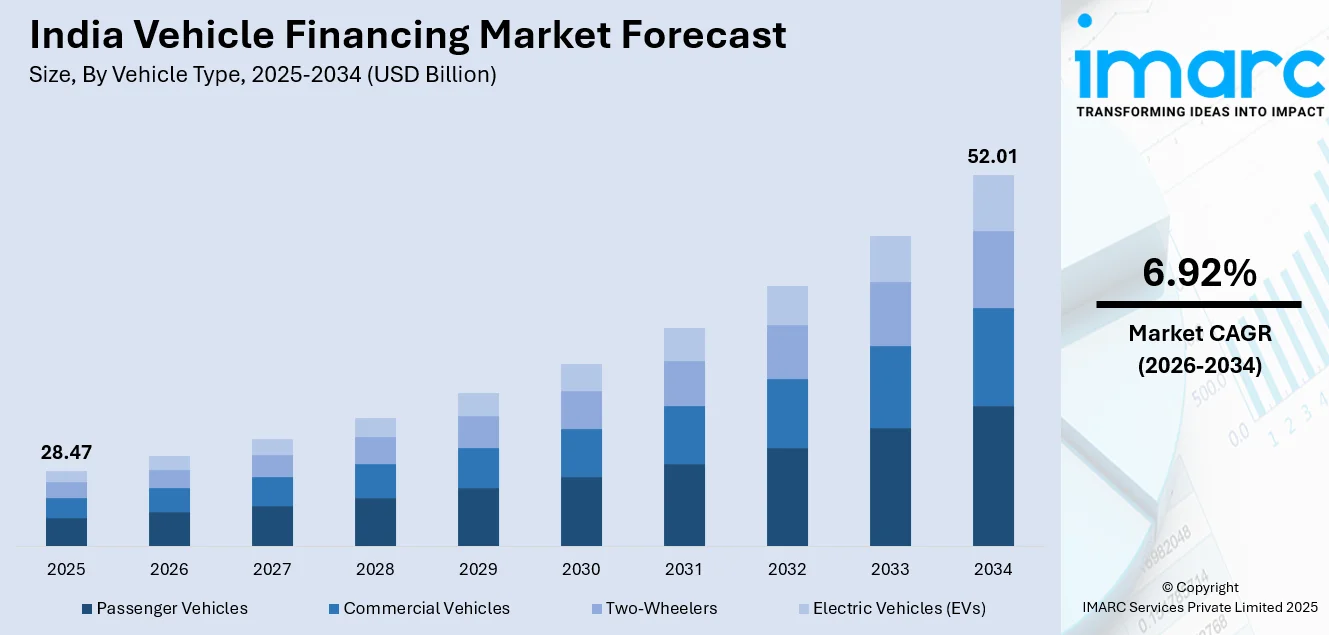

The India vehicle financing market size was valued at USD 28.47 Billion in 2025 and is projected to reach USD 52.01 Billion by 2034, growing at a compound annual growth rate of 6.92% from 2026-2034.

The vehicle financing industry in India is registering strong growth due to increasing disposable incomes, rising ambitions for car ownership, and easy access to credit facilities in urban, semi-urban, and rural areas. The rise of online lending platforms and fintech services has greatly improved access to loans, allowing for faster approval and easier documentation procedures. Government policies encouraging car ownership and the growing middle-class population are driving the demand for financing solutions for passenger cars, two-wheelers, and commercial vehicles.

Key Takeaways and Insights:

-

By Vehicle Type: Passenger vehicles dominate the market with a share of 48.0% in 2025, driven by growing urbanization, rising disposable incomes, and favorable financing schemes attracting first-time buyers across metropolitan and tier-II cities.

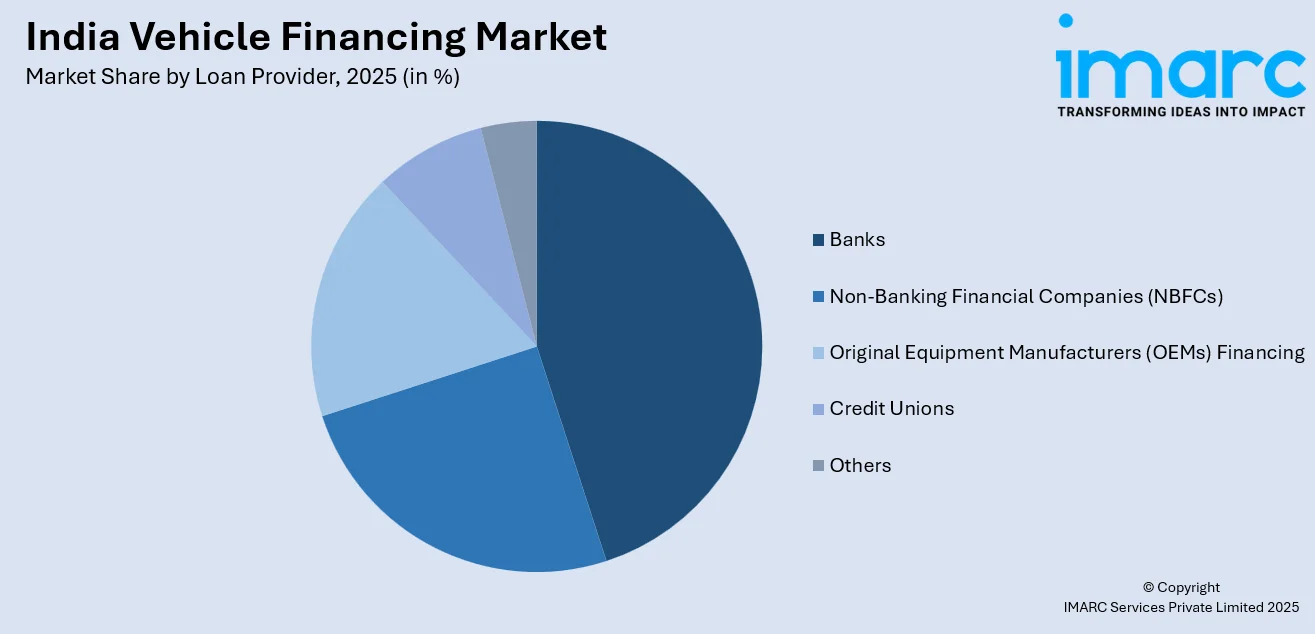

- By Loan Provider: Banks lead the market with a share of 44.3% in 2025, owing to their extensive branch networks, trusted reputations, competitive interest rates, and strong relationships with dealerships for instant loan approvals.

- By Vehicle Condition: New vehicles represent the largest segment with a market share of 74.9% in 2025, supported by manufacturer warranties, attractive financing offers, and consumer preference for latest technology and safety features.

- By Purpose Type: Loan dominates the market with a share of 88.5% in 2025, reflecting consumer preference for vehicle ownership through structured repayment schedules and affordable monthly installments.

- By Region: North India leads the market with a share of 32.2% in 2025, attributed to higher population density, strong economic activity, well-established banking infrastructure, and significant automobile dealership presence.

- Key Players: The India vehicle financing market exhibits a moderately competitive landscape with established banks, non-banking financial companies, and fintech platforms competing for market share. Major participants leverage extensive distribution networks, digital capabilities, and partnerships with automobile manufacturers to capture diverse customer segments across income levels and geographic regions.

To get more information on this market Request Sample

The India vehicle financing landscape is undergoing significant transformation with the convergence of traditional banking services and digital lending innovations. Financial institutions are broadening their presence in tier-II and tier-III cities by forming strategic partnerships with automobile dealers and fintech firms. Reflecting growing investor confidence in specialized auto lending, Mahaveer Finance raised ₹200 crore in June 2025 to expand its used commercial and passenger vehicle financing operations across India. The Reserve Bank of India's regulatory framework supporting digital lending has enhanced transparency and consumer protection while encouraging innovation in loan products. Rising vehicle prices coupled with limited upfront affordability have made financing an essential component of automobile purchases, with the growing used vehicle market creating new opportunities for specialized financing products

India Vehicle Financing Market Trends:

Digital Transformation Reshaping Loan Processing

Financial institutions are increasingly adopting advanced digital technologies to streamline vehicle loan processing and enhance customer experience. The implementation of artificial intelligence-driven underwriting systems, electronic know-your-customer verification, and instant approval mechanisms has significantly reduced loan disbursement timelines. Illustrating this shift, Bajaj Finance reported in its FY2024–25 Annual Report that AI-enabled automation now performs 43.42% of loan-application quality checks, accelerating underwriting and reducing manual processing time. Mobile applications and online platforms enable customers to compare financing options and submit documentation digitally, driving higher adoption rates particularly among younger demographics.

Expansion of Electric Vehicle Financing Solutions

The growing adoption of electric vehicles across India is prompting financial institutions to develop specialized financing products tailored to this emerging segment. Banks and non-banking financial companies are introducing green vehicle loans with preferential interest rates and extended repayment tenures to support the government's electrification agenda. Reinforcing this shift, in January 2026, the State Bank of India launched initiative to expand financing for electric mobility and battery storage projects as part of its broader support for emerging clean-energy sectors. Innovative financing models including battery-as-a-service and subscription-based ownership plans are gaining traction.

Co-Lending Partnerships Driving Market Penetration

Strategic co-lending arrangements between banks and non-banking financial companies are emerging as a significant trend, combining the funding strength of banks with the customer reach of specialized vehicle financiers. These partnerships enable financial institutions to extend credit to underserved segments including self-employed individuals and customers in remote geographic locations while optimizing capital utilization and managing risk. According to reports, the Reserve Bank of India finalized a new co-lending regulatory regime in 2025 to strengthen risk-sharing, expand joint lending beyond priority sectors, and improve transparency in bank–NBFC partnerships.

Market Outlook 2026-2034:

The Indian auto loan market is poised for growth during the forecast period due to favorable demographic factors, rising vehicle penetration, and continuous improvements in credit infrastructure. The growing middle-class population with rising income levels is expected to fuel demand for vehicle ownership, and digital lending innovations will make it more accessible and cheaper. Government support for vehicle ownership, collaborations between financial institutions and automobile dealerships, and the increasing adoption of fintech solutions in semi-urban and rural areas will further fuel the growth of the market. The market generated a revenue of USD 28.47 Billion in 2025 and is projected to reach a revenue of USD 52.01 Billion by 2034, growing at a compound annual growth rate of 6.92% from 2026-2034.

India Vehicle Financing Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Vehicle Type |

Passenger Vehicles |

48.0% |

|

Loan Provider |

Banks |

44.3% |

|

Vehicle Condition |

New Vehicles |

74.9% |

|

Purpose Type |

Loan |

88.5% |

|

Region |

North India |

32.2% |

Vehicle Type Insights:

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Electric Vehicles (EVs)

The passenger vehicles dominates with a market share of 48.0% of the total India vehicle financing market in 2025.

The passenger vehicles segment maintains its leading position in the India vehicle financing market, driven by increasing urbanization and the growing aspirations of the expanding middle-class population for personal mobility. First-time car buyers are increasingly relying on financing options rather than making outright purchases, supported by attractive loan schemes offering competitive interest rates, longer repayment tenures, and minimal documentation requirements.

Financial institutions have enhanced their associations with automobile dealers to provide instant loan approvals and hassle-free customer experiences at the point of sale. The facility of pre-approved loan offers for existing bank customers and the development of online application facilities have further eased the loan process, allowing for quicker decision-making and minimizing the entire time span from choosing the vehicle to its delivery.

Loan Provider Insights:

Access the comprehensive market breakdown Request Sample

- Banks

- Non-Banking Financial Companies (NBFCs)

- Original Equipment Manufacturers (OEMs) Financing

- Credit Unions

- Others

The banks leads with a share of 44.3% of the total India vehicle financing market in 2025.

Banks continue to dominate the vehicle financing landscape owing to their extensive branch networks, established brand trust, and access to low-cost funds that enable competitive interest rate offerings. Public and private sector banks target both salaried and self-employed individuals with customized loan products featuring flexible equated monthly installment plans and extended repayment tenures that make monthly payments affordable for diverse income groups.

The digital transformation of banking services has significantly enhanced the vehicle loan application process, enabling online submissions, document verification, and faster disbursals. Strategic partnerships with automobile dealerships facilitate on-the-spot loan approvals, accelerating the purchase decision process. Banks also finance both new and pre-owned vehicles, expanding their customer base beyond metropolitan areas into smaller towns and cities where automobile ownership aspirations are rapidly growing.

Vehicle Condition Insights:

- New Vehicles

- Used Vehicles

The new vehicles dominates with a market share of 74.9% of the total India vehicle financing market in 2025.

New vehicle financing continues to command the majority market share, supported by consumer preference for manufacturer warranties, latest technology features, and enhanced safety specifications. Financial institutions offer attractive loan-to-value ratios and promotional financing schemes in collaboration with automobile manufacturers during festive seasons and new model launches, making new vehicle ownership more accessible to aspiring buyers. According to reports, in November 2023 banks and lenders rolled out festive-season car loan offers including funding up to 100% of the on-road price, flexible EMI tenures, and quick loan approvals to boost new-vehicle purchases.

The availability of comprehensive insurance options, roadside assistance programs, and after-sales service packages bundled with new vehicle financing products adds significant value for customers. Lenders benefit from clearer vehicle valuation metrics and lower risk profiles associated with new automobiles, enabling them to offer competitive terms while maintaining healthy portfolio quality across customer segments.

Purpose Type Insights:

- Loan

- Leasing

The loan leads with a share of 88.5% of the total India vehicle financing market in 2025.

The loan segment maintains overwhelming dominance in the India vehicle financing market, reflecting the strong cultural preference for vehicle ownership among Indian consumers. Traditional loan structures providing clear ownership transfer upon completion of repayment continue to resonate with individual buyers seeking long-term asset accumulation and the flexibility to modify or sell their vehicles without restrictions.

Financial institutions have refined their loan products to offer varied tenure options, step-up payment structures, and balloon payment schemes catering to different income profiles and repayment capabilities. The widespread availability of loan calculators, transparent fee disclosures, and digital disbursement processes has enhanced customer confidence and simplified the decision-making process for prospective vehicle buyers across demographic segments.

Regional Insights:

- North India

- South India

- East India

- West India

North India exhibits a clear dominance with a 32.2% share of the total India vehicle financing market in 2025.

North India sustains its premier market position in the vehicle financing business, thanks to greater population density, economic activity, and developed banking networks in the key states of Delhi, Uttar Pradesh, Punjab, and Haryana. The presence of major automobile manufacturing facilities and dealership networks makes it easier for customers to access vehicle financing solutions.

The region enjoys greater per-capita incomes in key urban centers and an increasing number of prosperous agricultural communities in rural areas, thereby sustaining demand for both passenger and commercial vehicles. The banking sector has developed a strong regional presence with the ability to address customer service needs and tie up with local dealerships to address the varied financing needs of this important market.

Market Dynamics:

Growth Drivers:

Why is the India Vehicle Financing Market Growing?

Rising Disposable Incomes and Growing Middle-Class Population

The sustained economic growth in India has led to significant improvements in household income levels, particularly among the rapidly expanding middle-class population. This demographic shift is creating unprecedented demand for personal mobility solutions, with vehicle ownership becoming an achievable aspiration for millions of families. Financial institutions are capitalizing on this trend by developing innovative loan products with flexible repayment structures that align with varied income patterns, enabling first-time buyers to fulfill their automobile ownership dreams without straining their monthly budgets. In February 2025, the Government of India announced personal income tax reductions in the Union Budget to boost disposable income and consumer spending, a move expected to support big-ticket purchases such as automobiles

Digital Lending Innovation and Enhanced Credit Accessibility

The proliferation of digital lending platforms and fintech solutions has revolutionized the vehicle financing landscape by significantly reducing loan processing times and documentation requirements. Advanced technologies including artificial intelligence-driven credit assessment, electronic document verification, and instant approval systems enable financial institutions to serve customers more efficiently while expanding their reach to previously underserved segments. Reflecting the increasing role of digital data in lending decisions, the Account Aggregator (AA) framework, which facilitates secure, consent‑based financial data sharing between banks, NBFCs, and digital lenders, saw daily consents average around 2.8 lakh since April 2024, up 79 % from the previous year, underscoring how AA integration is accelerating credit assessments.

Expansion of Automobile Dealership Networks and Financing Partnerships

Automobile manufacturers and dealership networks are increasingly integrating financing solutions into their sales processes to facilitate customer purchases and drive volume growth. Strategic partnerships between financial institutions and dealerships enable point-of-sale financing with instant approvals, significantly reducing the time between vehicle selection and ownership. For example, in August 2025, Citroën India signed a partnership with HDFC Bank to offer comprehensive retail and dealer finance solutions, including digital loan disbursals within 30 minutes and customized dealer floorplan financing, aimed at simplifying vehicle purchases and enhancing convenience for customers and dealers alike. These collaborations often include exclusive promotional offers, reduced processing fees, and preferential interest rates during new model launches and festive seasons, creating compelling value propositions that encourage consumers to opt for financed purchases over cash transactions.

Market Restraints:

What Challenges the India Vehicle Financing Market is Facing?

Rising Vehicle Prices Affecting Affordability

The rising trend in the prices of automobiles due to supply chain disruptions, safety regulations, and cost inflation is likely to create affordability issues for potential car buyers. Higher automobile prices mean higher loan amounts and higher monthly payments, which may act as a deterrent to potential buyers and lead to longer loan terms.

Credit Quality Concerns in Expanding Portfolios

The growth in the financing portfolios of vehicles, especially in the case of non-banking financial companies catering to the underserved sections of customers, has raised concerns about the credit quality and the possibility of default. Uncertainties in the economy, which can affect the stability of employment and income, can also affect the ability of customers to repay, and financial institutions need to manage risks while pursuing growth.

Regulatory Compliance and Operational Complexities

The changing regulatory requirements, such as digital lending guidelines, enhanced disclosure requirements, and tough know-your-customer rules, require substantial investments in compliance infrastructure and changes in operations. The financial institutions are required to modify their operations to comply with the regulatory requirements while ensuring operational efficiency and competitive service delivery standards.

Competitive Landscape:

The market for vehicle financing in India has a moderately fragmented level of competition, with the presence of well-established public and private sector banks, specialized non-banking financial companies, and new-age fintech platforms. The established banks have utilized their strong network of branches, brand recognition, and access to cheap funds to provide competitive financing options, while non-banking financial companies have concentrated on serving specific customer segments and geographical areas that are not served by mainstream banking organizations. The market is experiencing growing levels of consolidation through co-lending arrangements that leverage the funding power of banks and the operational flexibility of specialized financiers. Digital innovation is rapidly altering the competitive landscape, with players investing heavily in technology platforms to improve customer experience and operational efficiency.

Recent Developments:

- In November 2025, Maruti Suzuki’s fully digital financing platform surpassed 2.5 million car loan disbursals, with a cumulative loan value exceeding ₹1,70,000 crore. The platform enables real-time loan approvals, credit-score-based pricing, QR-enabled dealership financing, and multi-lender comparisons, accelerating India’s transition toward paperless, tech-driven auto lending.

India Vehicle Financing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Electric Vehicles (EVs) |

| Loan Providers Covered | Banks, Non-Banking Financial Companies (NBFCs), Original Equipment Manufacturers (OEMs) Financing, Credit Unions, Others |

| Vehicle Conditions Covered | New Vehicles, Used Vehicles |

| Purpose Types Covered | Loan, Leasing |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India vehicle financing market size was valued at USD 28.47 Billion in 2025.

The India vehicle financing market is expected to grow at a compound annual growth rate of 6.92% from 2026-2034 to reach USD 52.01 Billion by 2034.

Passenger vehicles dominated the market with approximately 48.0% share, driven by growing urbanization, rising disposable incomes, and favorable financing schemes attracting first-time buyers across metropolitan and tier-II cities.

Key factors driving the India vehicle financing market include rising disposable incomes, growing middle-class aspirations for vehicle ownership, digital lending innovations enhancing credit accessibility, expansion of banking networks into tier-II and tier-III cities, and strategic partnerships between financial institutions and automobile dealerships.

Major challenges include rising vehicle prices affecting affordability, credit quality concerns in rapidly expanding loan portfolios, regulatory compliance requirements necessitating operational investments, competition from informal lending channels, and economic uncertainties impacting borrower repayment capabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)