Indian Warehouse Market Size, Share, Trends and Forecast by Sector, Ownership, and Type of Commodities Stored, 2026-2034

Indian Warehouse Market Summary:

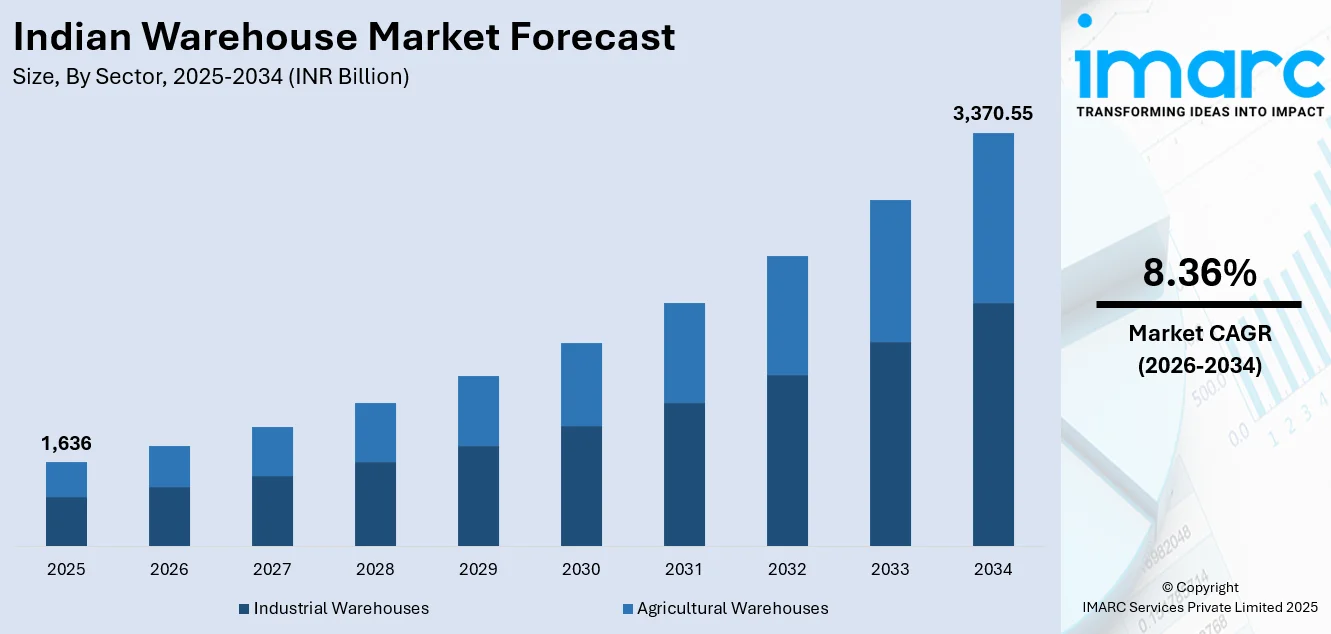

The Indian warehouse market size was valued at INR 1,636 Billion in 2025 and is projected to reach INR 3,370.55 Billion by 2034, growing at a compound annual growth rate of 8.36% from 2026-2034.

The Indian warehouse industry is witnessing strong growth due to the growing e-commerce sector, rapid industrialization, and the government's initiatives to modernize the infrastructure. The Goods and Services Tax has simplified logistics and led to the development of large warehousing facilities by the consolidation of small storage spaces. The growing demand for faster delivery and the development of quick commerce services are changing the storage needs in the cities.

Key Takeaways and Insights:

- By Sector: Industrial warehouses dominate the market with a share of 56% in 2025, driven by the expanding manufacturing sector under the Make in India initiative and the rising demand from third-party logistics providers serving diverse industrial verticals.

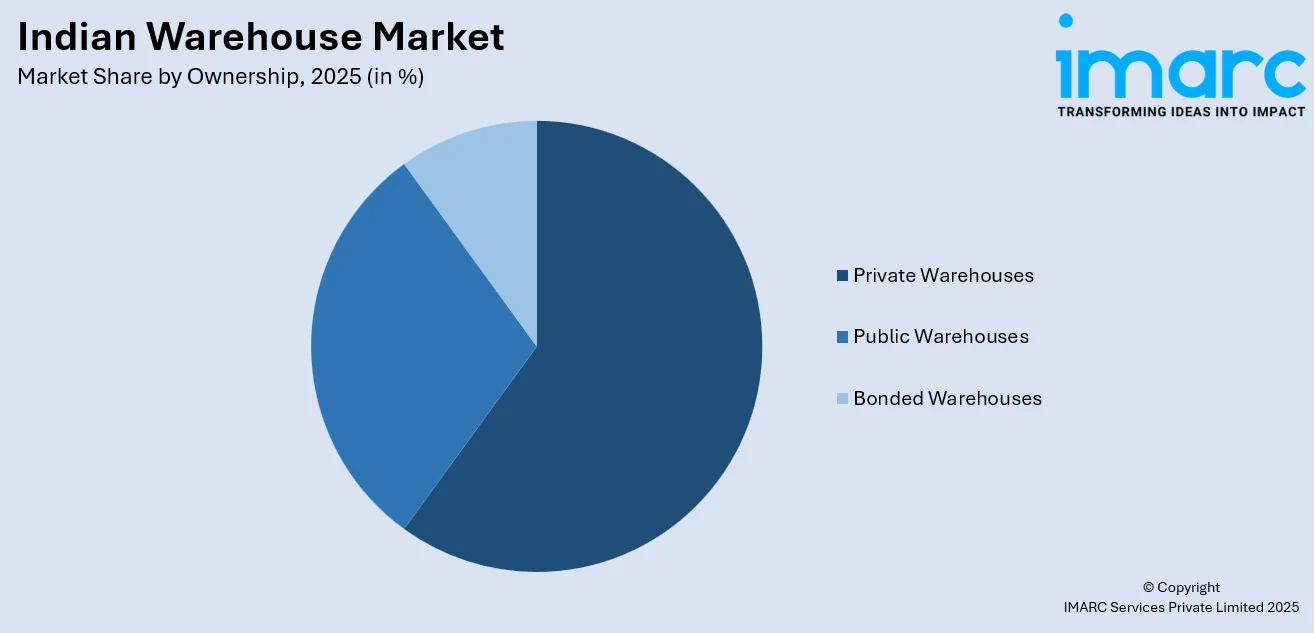

- By Ownership: Private warehouses lead the market with a share of 60% in 2025, owing to their flexibility in customization, advanced technology integration, and ability to meet the specific storage requirements of e-commerce and retail businesses.

- By Type of Commodities Stored: General warehouses represent the largest segment with a market share of 48% in 2025, attributed to their versatility in accommodating diverse product categories and their cost-effectiveness for businesses managing multi-client inventory operations.

- Key Players: The Indian warehouse market exhibits a moderately fragmented competitive structure, with both domestic operators and international logistics providers competing across different segments. The market features a mix of large-scale institutional developers, third-party logistics companies, and specialized warehousing service providers catering to various industry verticals.

To get more information on this market Request Sample

The Indian warehouse market has emerged as a critical component of the country's supply chain infrastructure, supported by favorable government policies and substantial private investments. For example, IndoSpace announced plans to invest over $1 billion to acquire new warehousing and logistics assets across India and develop an additional 30 million sq ft of Grade A facilities to meet rising demand. The sector benefits from the ongoing development of multimodal logistics parks under the PM Gati Shakti initiative, which aims to enhance connectivity and reduce logistics costs. The increasing adoption of Grade A warehousing facilities reflects the growing demand for modern storage solutions equipped with advanced safety features, automation capabilities, and sustainable design elements. Rising urbanization and changing consumption patterns continue to drive the need for strategically located distribution centers that enable efficient last-mile delivery operations. The market is also witnessing significant interest from institutional investors who recognize the long-term growth potential of logistics real estate in India.

Indian Warehouse Market Trends:

Rise of Technology-Enabled Smart Warehousing

The Indian warehouse sector is undergoing rapid digital transformation with the adoption of warehouse management systems, Internet of Things sensors, and robotics for inventory management. For example, in August 2025, Addverb Technologies, a leading Indian robotics and automation company, partnered with Siemens Xcelerator in 2025 to scale intelligent automation solutions across industries, reinforcing how advanced software and robotics are expanding warehouse tech capabilities in the country. Operators are increasingly implementing automated guided vehicles and conveyor systems to enhance operational efficiency and reduce turnaround times. The integration of artificial intelligence and machine learning enables predictive analytics for demand forecasting and inventory optimization across warehousing networks.

Expansion into Tier-Two and Tier-Three Cities

Warehousing development is progressively extending beyond metropolitan areas into emerging cities driven by rising e-commerce penetration and improved infrastructure connectivity. Secondary markets are attracting significant investment as logistics operators seek lower land costs and proximity to growing consumer bases. In October 2025, Mahindra Logistics announced the launch of new Grade‑A warehousing facilities in Guwahati and Agartala, adding over 4 lakh sq ft of capacity to strengthen its pan‑India distribution network and support regional supply chains beyond traditional metro hubs. Government initiatives supporting infrastructure development in smaller cities are accelerating this geographical diversification of warehousing capacity across the country.

Growing Emphasis on Sustainable Green Warehousing

Environmental sustainability has become a key focus area in warehouse development with increasing adoption of green building certifications and renewable energy integration. In March 2024, LP Logiscience inaugurated a state‑of‑the‑art solar power plant at its Grade A green warehouse in Bhiwandi, Maharashtra, generating around 6.10 lakh units of solar energy annually and incorporating rainwater harvesting systems as well as electric vehicles for greener distribution. Developers are incorporating solar power installations, rainwater harvesting systems, and energy-efficient lighting solutions in new warehousing facilities. The emphasis on sustainable practices is driven by corporate environmental goals and the growing preference of multinational tenants for certified green logistics infrastructure.

Market Outlook 2026-2034:

The outlook for the Indian warehouse market is very positive, with fundamentals in place to support further growth in all segments. The sector is poised to gain from the continued momentum in e-commerce growth, the expansion of the manufacturing sector under the Production Linked Incentive schemes, and the infrastructure development plans of the government. The rise in foreign direct investment in logistics real estate and the presence of international warehousing companies are improving the supply of institutional-grade warehousing space. The demand for cold chain infrastructure to support the pharmaceutical and food processing sectors offers tremendous opportunities. The market generated a revenue of INR 1,636 Billion in 2025 and is projected to reach a revenue of INR 3,370.55 Billion by 2034, growing at a compound annual growth rate of 8.36% from 2026-2034.

Indian Warehouse Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Sector |

Industrial Warehouses |

56% |

|

Ownership |

Private Warehouses |

60% |

|

Type of Commodities Stored |

General Warehouses |

48% |

Sector Insights:

- Industrial Warehouses

- Agricultural Warehouses

The industrial warehouses dominates with a market share of 56% of the total Indian warehouse market in 2025.

Industrial warehouses remain at the forefront of the Indian market due to the increasing pace of growth of the manufacturing industry and the government's efforts to develop domestic manufacturing capabilities. The growing manufacturing of automobiles, electronics, and consumer durables has resulted in a significant demand for large-format storage spaces with specialized handling equipment and climate control systems. The emergence of third-party logistics players catering to multiple industrial customers has also fueled the demand for industrial warehousing facilities located close to large manufacturing hubs and transportation nodes.

The segment is aided by the Production Linked Incentive schemes that attract global manufacturers to set up shop in India, thus fueling the demand for quality warehousing space. Industrial warehouses are also embracing new automation technology to cater to the increasing throughput volumes and the strict delivery time requirements of the modern supply chain. The development of industrial parks and manufacturing clusters remains a key driver of investment in warehousing facilities located close to these hubs and supporting just-in-time inventory management systems.

Ownership Insights:

Access the comprehensive market breakdown Request Sample

- Private Warehouses

- Public Warehouses

- Bonded Warehouses

The private warehouses leads with a share of 60% of the total Indian warehouse market in 2025.

Private warehouses dominate the Indian market owing to their ability to offer customized storage solutions tailored to specific business requirements and operational needs. The flexibility in facility design, technology integration, and service offerings makes private warehousing attractive to e-commerce companies and retail businesses seeking dedicated storage capacity. The surge in institutional investor interest underscores this trend. In 2024, institutional investment in industrial and warehousing assets in India tripled from 2023 levels to about $2.5 billion, with foreign and domestic real‑estate players significantly boosting modern logistics infrastructure development. The entry of institutional investors and global logistics real estate developers has significantly elevated the quality standards and professional management of private warehousing facilities across the country.

The trend remains attractive for significant investment as companies continue to focus on managing their supply chain infrastructure. Private warehouse companies are increasingly providing value-added services such as inventory management, order fulfillment, and distribution to distinguish themselves in a competitive environment. The implementation of technology-based warehouse management systems and automated handling equipment has improved the efficiency and service capabilities of private warehousing facilities.

Type of Commodities Stored Insights:

- General Warehouses

- Specialty Warehouses

- Refrigerated Warehouses

The general warehouses dominates with a market share of 48% of the total Indian warehouse market in 2025.

General warehouses continue to retain their leading market position with flexible storage solutions that can handle a broad range of product types without requiring any special environmental conditions. The cost-effectiveness of general warehousing solutions makes it the most sought-after option for companies dealing with a broad range of inventory types, including consumer products, electronics, and industrial parts. The market also derives growth from the rising number of multi-client logistics facilities, where third-party logistics companies aggregate storage needs of multiple customers in common facilities.

The rising e-commerce and retail industry has fueled the demand for general warehousing space with advanced racking systems and efficient material handling systems. General warehouses are also increasingly incorporating mezzanine floors and high-bay storage systems to maximize storage capacity and handle increasing volumes of inventory. The market is also witnessing the adoption of warehouse management systems that support efficient tracking, picking, and shipping processes for a broad range of product types.

Market Dynamics:

Growth Drivers:

Why is the Indian Warehouse Market Growing?

Rapid Expansion of E-Commerce and Quick Commerce Platforms

The explosive growth of online retail and the emergence of quick commerce platforms promising ultra-fast deliveries have fundamentally transformed warehousing requirements across India. The India e-commerce market was valued at USD 129.72 billion in 2025 and is projected to reach USD 651.10 billion by 2034, reflecting the scale of opportunity that is driving e-commerce companies to rapidly expand their warehousing networks. E-commerce companies are establishing extensive networks of fulfillment centers and dark stores in strategic locations to meet consumer expectations for same-day and express delivery services. The increasing digital penetration in smaller cities and rural areas is expanding the geographical footprint of warehousing demand beyond traditional metropolitan markets. The competitive intensity among e-commerce players drives continuous investment in warehousing capacity and technology to improve delivery speed and customer satisfaction.

Government Infrastructure Development Initiatives

The Indian government's comprehensive infrastructure development programs including PM Gati Shakti and the National Logistics Policy are creating an enabling environment for warehousing sector growth. Under the PM Gati Shakti initiative, the Multi Modal Logistics Park (MMLP) in Nagpur began commercial operations in 2025, offering integrated warehousing, cargo handling and multimodal connectivity that directly supports efficient storage and distribution networks. The development of dedicated freight corridors, expressways, and multimodal logistics parks is improving connectivity and reducing transportation costs that benefit warehousing operations. Policy initiatives supporting the development of logistics infrastructure have attracted substantial foreign and domestic investment into the warehousing sector. The focus on reducing logistics costs as a percentage of gross domestic product is driving the modernization of warehousing facilities and the adoption of efficient storage technologies. Infrastructure improvements in tier-two and tier-three cities are enabling the establishment of warehousing facilities in previously underserved markets.

Manufacturing Sector Growth Under Production Linked Incentive Schemes

The government's Production Linked Incentive schemes across multiple manufacturing sectors are attracting global companies to establish production facilities in India, thereby driving warehousing demand. In Q3 2025, India’s warehousing sector recorded a 16% year‑on‑year growth in overall demand, with strong traction coming from manufacturing clusters as firms expanded operations and leased additional storage space to support production and distribution. The growth of domestic manufacturing in sectors including electronics, pharmaceuticals, automotive, and textiles creates substantial requirements for raw material storage and finished goods distribution infrastructure. The emphasis on self-reliance in manufacturing has accelerated the development of industrial warehousing capacity near emerging production clusters. Global supply chain diversification strategies are positioning India as an alternative manufacturing hub, which necessitates corresponding investment in warehousing and logistics infrastructure.

Market Restraints:

What Challenges the Indian Warehouse Market is Facing?

Land Acquisition and High Real Estate Costs

The acquisition of large contiguous land parcels for warehousing development remains challenging due to complex regulatory processes and fragmented land ownership patterns. Rising real estate prices in prime logistics corridors near major cities increase development costs and impact project viability. Competition from residential and commercial developers for available land parcels further constrains the supply of suitable sites for warehousing projects.

Inadequate Last-Mile Connectivity Infrastructure

Despite improvements in major highways and freight corridors, the connectivity of many warehousing locations to end consumers through last-mile roads remains inadequate. Poor road conditions in suburban and semi-urban areas increase transportation costs and delivery times, affecting the efficiency of warehousing operations. The uneven development of supporting infrastructure including power supply and water availability in some regions limits the expansion of quality warehousing facilities.

Skilled Workforce Shortage and Technology Adoption Barriers

The warehousing sector faces challenges in attracting and retaining skilled workers capable of operating advanced automated systems and warehouse management technologies. The transition from traditional storage operations to modern technology-enabled warehousing requires significant investment in workforce training and development. Resistance to change among smaller operators and the high capital requirements for automation limit the pace of technology adoption across the industry.

Competitive Landscape:

The Indian warehouse market exhibits a dynamic competitive landscape characterized by the presence of both established logistics operators and emerging specialized providers. The market has witnessed increasing participation from global logistics real estate developers who bring international best practices and institutional capital to elevate industry standards. Domestic third-party logistics companies have expanded their warehousing capabilities to offer integrated supply chain solutions competing with multinational operators. The competitive environment is driving innovation in service offerings, technology adoption, and facility specifications as operators seek differentiation. Strategic partnerships between technology providers and warehousing operators are emerging to deliver advanced automation and digital solutions. The market structure is evolving with consolidation among smaller operators and the entry of new investors attracted by the sector's growth potential and favorable policy environment.

Recent Developments:

- In April 2025, Godrej Consumer Products inaugurated its first vertical storage warehouse in Bhiwandi, Maharashtra, spanning 2.84 lakh sq. ft. The facility features high-density G+6 vertical racking to maximize storage efficiency as part of its Project Parivartan supply chain modernization strategy, aimed at improving inventory management and distribution performance across India.

Indian Warehouse Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion INR |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Industrial Warehouses, Agricultural Warehouses |

| Ownerships Covered | Private Warehouses, Public Warehouses, Bonded Warehouses |

| Type of Commodities Stores Covered | General Warehouses, Speciality Warehouses, Refrigerated Warehouses |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Warehouse Market Report

The Indian warehouse market size was valued at INR 1,636 Billion in 2025.

The Indian warehouse market is expected to grow at a compound annual growth rate of 8.36% from 2026-2034 to reach INR 3,370.55 Billion by 2034.

Industrial warehouses dominated the Indian warehouse market with a share of 56%, driven by the expanding manufacturing sector, rising third-party logistics demand, and the government's focus on domestic production capabilities under various industrial promotion schemes.

Key factors driving the Indian warehouse market include the rapid expansion of e-commerce and quick commerce platforms, government infrastructure development initiatives under PM Gati Shakti and National Logistics Policy, manufacturing sector growth supported by Production Linked Incentive schemes, and increasing adoption of technology-enabled warehousing solutions.

Major challenges include difficulties in land acquisition and rising real estate costs in prime logistics corridors, inadequate last-mile connectivity infrastructure in certain regions, shortage of skilled workforce for technology-enabled operations, fragmented ownership patterns in the unorganized segment, and regulatory complexities affecting development approvals.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)