India Water Pumps Market Size, Share, Trends and Forecast by Type, Pump Type, Pump Capacity, Application, and Region, 2026-2034

India Water Pumps Market Size, Share, Trends & Forecast (2026-2034)

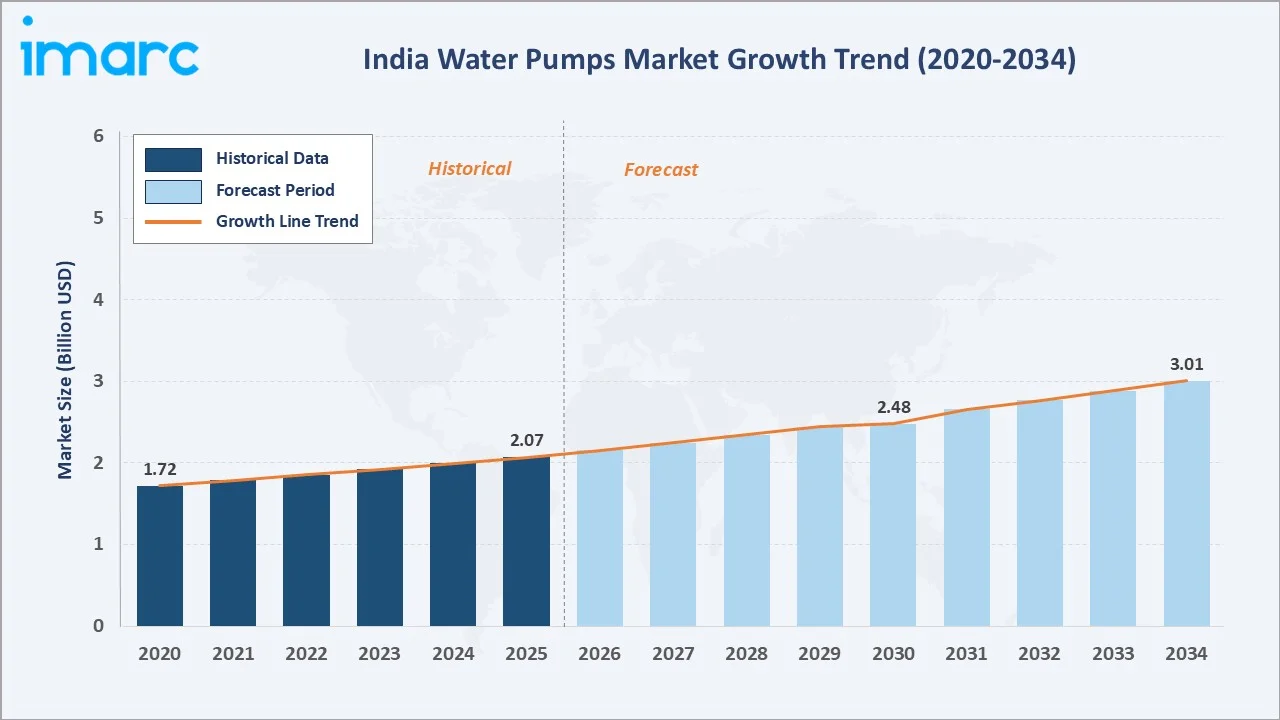

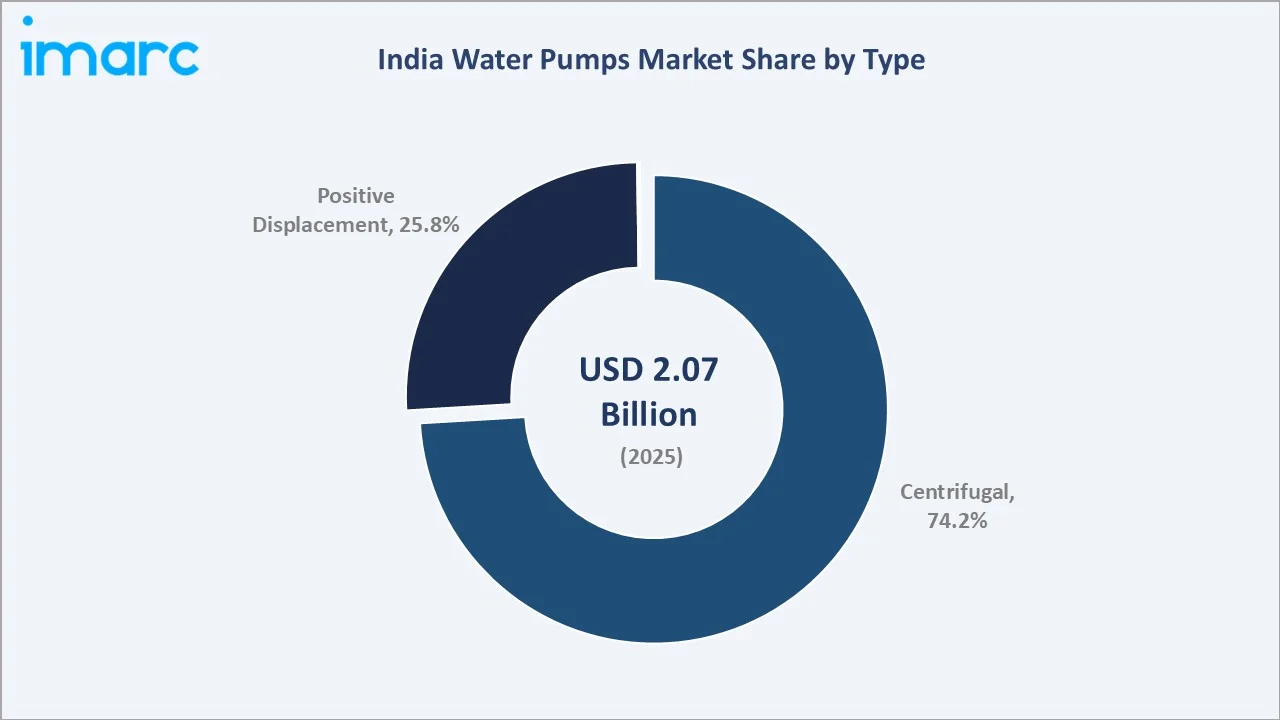

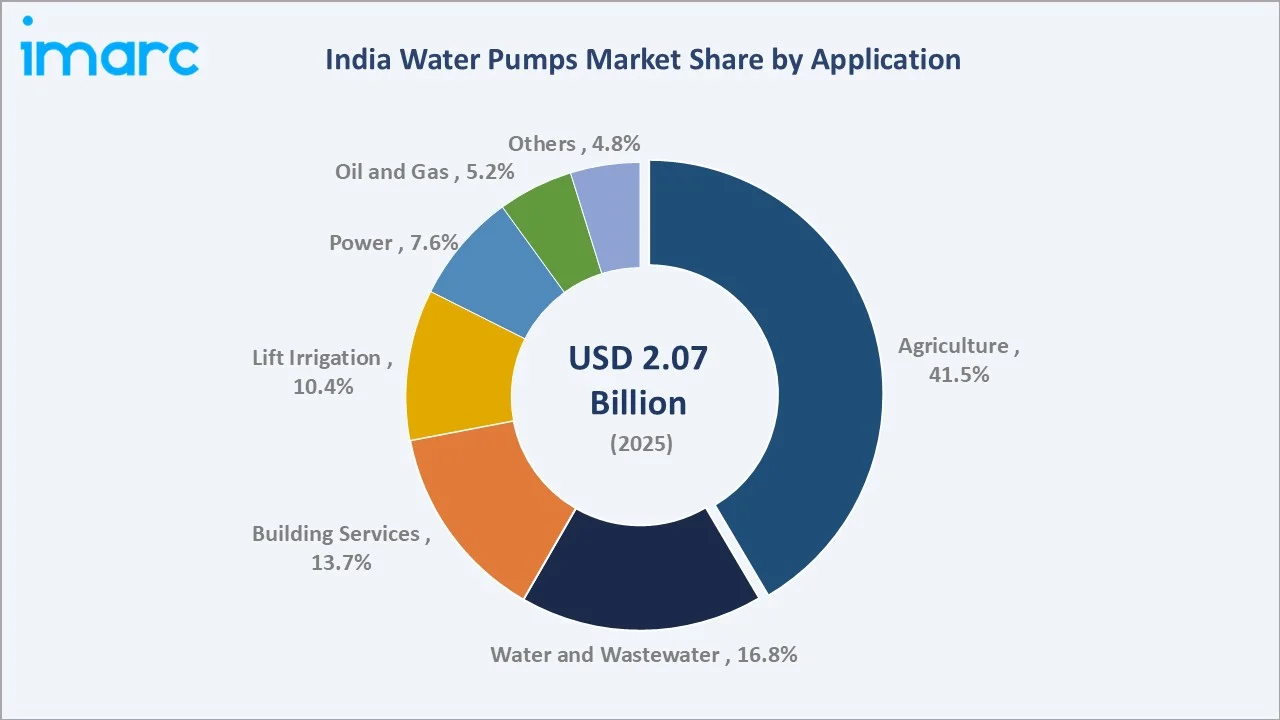

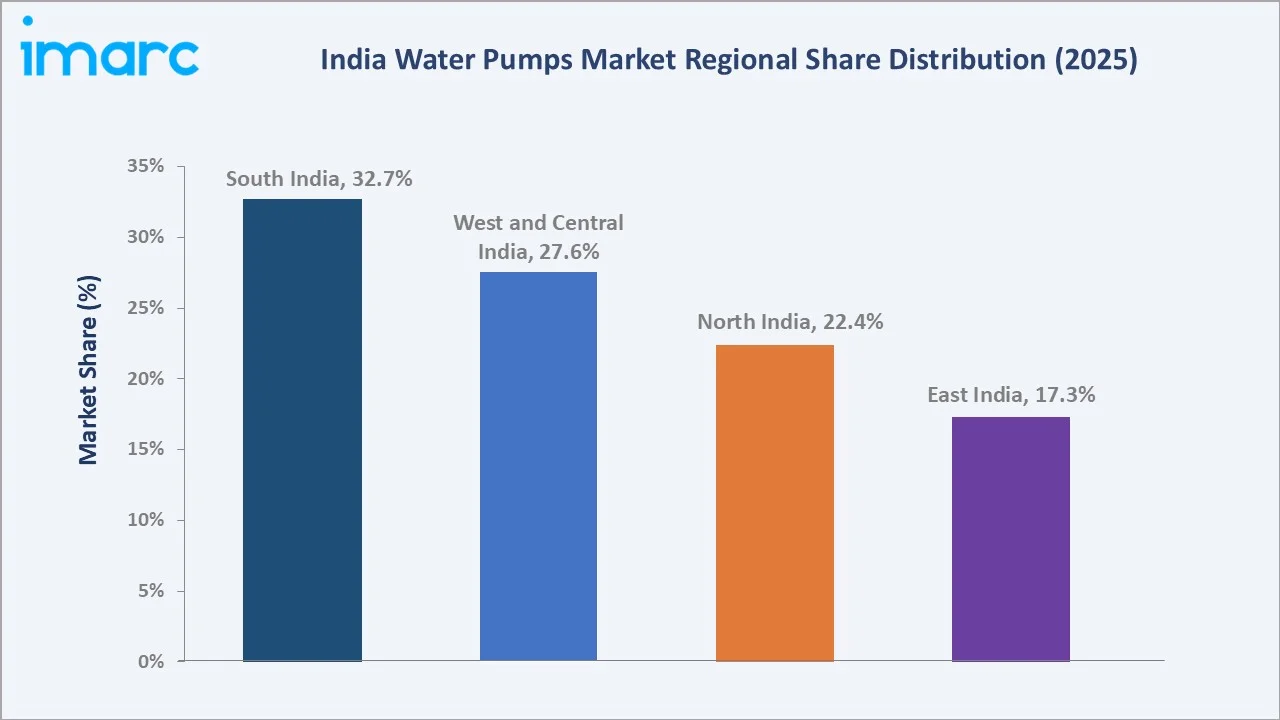

The India water pumps market reached USD 2.07 Billion in 2025 and is projected to reach USD 3.01 Billion by 2034, growing at a CAGR of 3.74% during 2026-2034. The Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan (PM-KUSUM) solar agricultural pump scheme target of 3.5 million solar pump installations, Jal Jeevan Mission piped water supply to rural households, India's real estate construction cycle, and growing industrial and infrastructure capex collectively anchor the market growth. Centrifugal type dominates at 74.2%. Agriculture leads the application at 41.5%. South India commands 32.7% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.07 Billion |

|

Forecast Market Size (2034) |

USD 3.01 Billion |

|

CAGR (2026-2034) |

3.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Centrifugal (74.2%, 2025) |

|

Dominant Application |

Agriculture (41.5%, 2025) |

|

Leading Region |

South India (32.7%, 2025) |

The market expanded from USD 1.72 Billion in 2020 to USD 2.07 Billion in 2025, anchored at USD 2.48 Billion in 2030, and forecast to reach USD 3.01 Billion by 2034. COVID-19 disrupted the market during 2020-2021, before a strong recovery cycle from 2022, driven by the acceleration of government infrastructure programs. The Jal Jeevan Mission's pump procurement for rural water supply schemes, PM-KUSUM's solar pump rollout, and India's real estate construction boom collectively created the demand recovery.

To get more information on this market, Request Sample

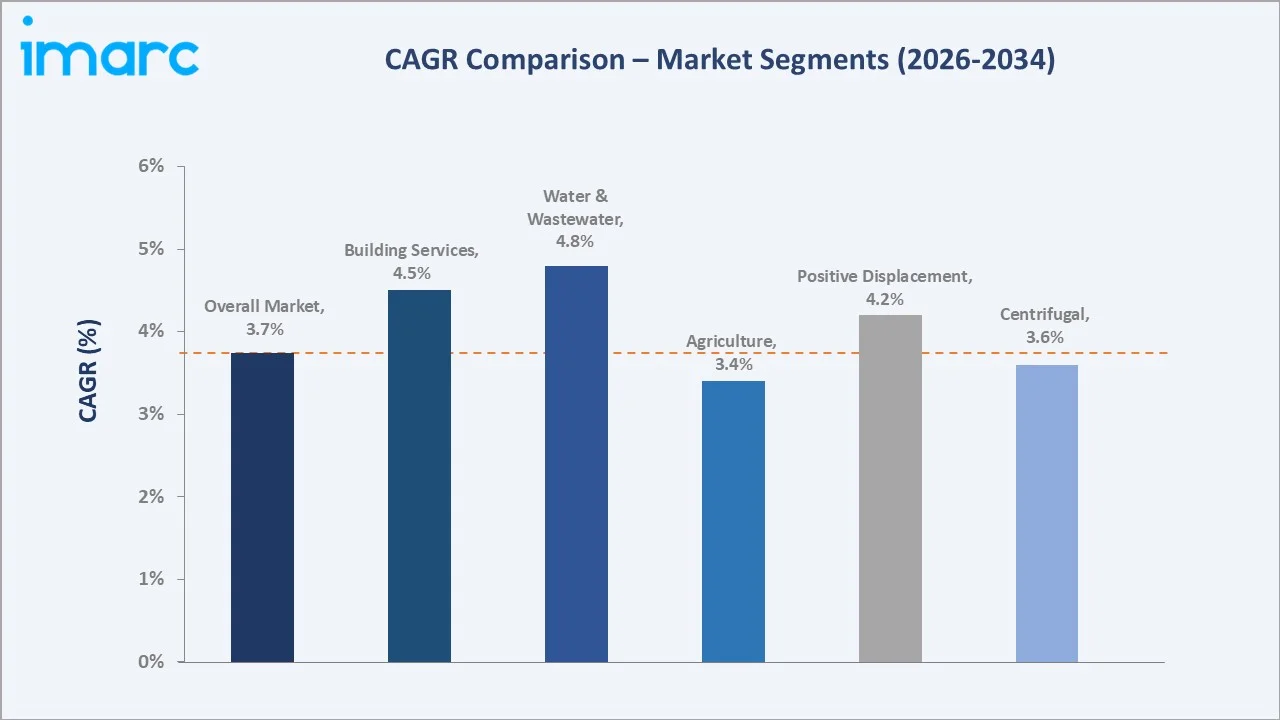

Water and wastewater grow fastest at ~4.8% CAGR as India's smart city programs, AMRUT 2.0 water distribution investment, sewage treatment plant construction, and industrial effluent treatment requirements create sustained infrastructure pump procurement. Positive displacement grows at ~4.2% CAGR through pharmaceutical, food processing, chemical, and oil and gas industry expansion, requiring dosing, metering, and viscous fluid pumps beyond the capabilities of centrifugal technology.

Executive Summary

The India water pumps market reached USD 2.07 Billion in 2025, serving the world's most diverse single-country pump application landscape from agricultural borewell pump sets irrigating India's cultivated land, through municipal water treatment and distribution pumping stations, to premium building services pumps in India's constructed real estate, and process industry pumps serving oil refining, chemical manufacturing, power generation, and pharmaceutical production. The market is projected to reach USD 3.01 Billion by 2034 at 3.74% CAGR.

Centrifugal pumps at 74.2% dominate through their mechanical simplicity, adaptability to a wide range of flows and heads, lower capital cost versus positive displacement alternatives, and suitability for the majority of India's pump applications, such as agricultural irrigation, municipal water distribution, building pressure boosting, cooling water circulation, and boiler feed water service. Agriculture at 41.5% dominates the application landscape, reflecting India's foundational agrarian economy, where irrigation pump infrastructure represents the primary productivity-enabling capital asset for farm households. South India, at 32.7%, leads through Coimbatore's manufacturing cluster dominance and Tamil Nadu's intensive agricultural pump density.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Centrifugal - 74.2% share (2025) |

|

Dominant Application |

Agriculture - 41.5% market share (2025) |

|

Leading Region |

South India - 32.7% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Centrifugal at 74.2%, reflecting the dominant technology for India's mass-market agricultural and infrastructure pump applications: Centrifugal pumps' market leadership in India derives from three application concentrations: agricultural submersible borewell pumps, monoblock centrifugal pump sets for surface irrigation and drainage, and large centrifugal pumps for Jal Jeevan Mission village water supply systems.

- Agriculture at 41.5% anchored by India's agricultural electric pump connections and growing solar pump transition: India's agricultural pump base represents the world's largest single agricultural pump market. The agriculture segment's revenue concentration at 41.5% reflects both the market's dominant volume and its per-unit value spectrum from domestic monoblock to submersible solar pump systems.

- South India at 32.7% through Coimbatore's manufacturing leadership and Tamil Nadu's agricultural pump intensity: South India's market leadership reflects a dual advantage; Tamil Nadu is simultaneously India's most pump-intensive agricultural state and the country's pump manufacturing capital.

India Water Pumps Market Overview

India's water pumps market encompasses the design, manufacture, distribution, installation, and servicing of mechanical pumping equipment for fluid transfer, pressurization, circulation, and lifting applications across agriculture, municipal water supply, industrial process, building services, power generation, oil and gas, and lift irrigation end markets.

The ecosystem integrates raw material and component suppliers, domestic pump manufacturers, Indian subsidiaries of global pump companies, the distribution network, government procurement channels, contractors executing government water infrastructure projects, and the after-sales service network for preventive maintenance and spare parts supply. Macroeconomic factors include rapid urbanization, rising infrastructure development, expanding agricultural irrigation activities, and increasing investments in residential and industrial water management systems.

Market Dynamics

To evaluate market opportunities, Request Sample

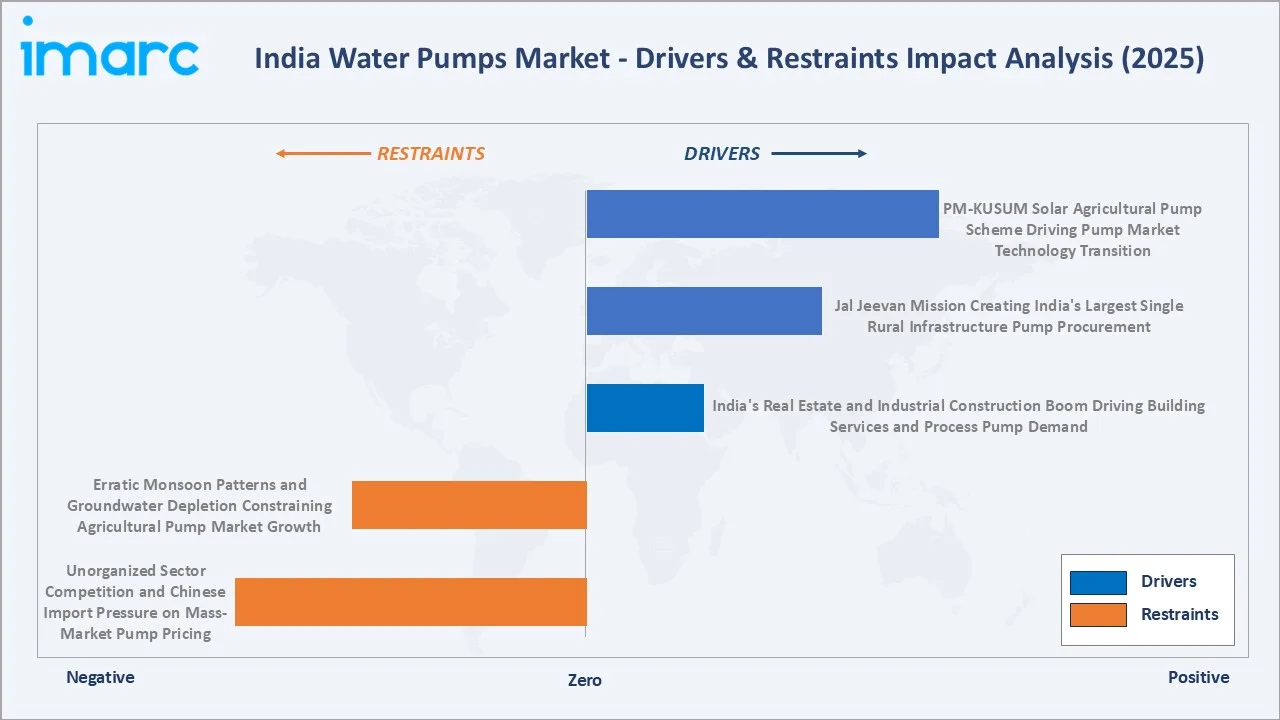

Market Drivers

- PM-KUSUM Solar Agricultural Pump Scheme Driving Pump Market Technology Transition: PM-KUSUM (Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan) is India's most significant agricultural pump market intervention in decades. Component B target of 3.5 million standalone solar agricultural pump installations, replacing diesel and grid-connected agricultural pump sets with solar-powered submersible pump systems that include solar panels, an inverter, motor, pump, and mounting structure at subsidized pricing.

- Jal Jeevan Mission Creating India's Largest Single Rural Infrastructure Pump Procurement: As of February 1, 2025, the Jal Jeevan Mission (JJM) successfully provided tap water connections to 12.20 crore additional rural households. Each village water supply scheme under JJM requires submersible borewell pumps, overhead water storage tanks, village-level distribution piping, and chlorination systems.

- India's Real Estate and Industrial Construction Boom Driving Building Services and Process Pump Demand: India's real estate sector creates continuous building services pump demand for domestic manufacturers. Each high-rise apartment building requires pressure boosting systems, fire hydrant pumps, drainage submersible pumps, swimming pool circulation pumps, and HVAC chilled water circulation pumps, collectively representing high pump system value per building project.

Market Restraints

- Erratic Monsoon Patterns and Groundwater Depletion Constraining Agricultural Pump Market Growth: India's agricultural pump market is intrinsically linked to monsoon rainfall distribution. Good monsoon years generate replacement and capacity expansion pump demand, while deficient monsoons reduce farmer purchasing power and delay pump procurement decisions.

- Unorganized Sector Competition and Chinese Import Pressure on Mass-Market Pump Pricing: India's water pump market includes a significant unorganized manufacturing segment, particularly in agricultural monoblock centrifugal pump sets and small submersible pumps, where small-scale manufacturers produce uncertified or low-quality BIS-marked pump sets that undercut organized sector pricing by 30-50%. This unorganized sector creates margin pressure for organized manufacturers and quality challenges for end users.

Market Opportunities

- BEE Energy Efficiency Upgrade Program Creating Replacement Market for High-Efficiency Pumps: The energy efficiency upgrade initiatives promoted by the Bureau of Energy Efficiency (BEE) are creating significant replacement demand for high-efficiency water pumps across India. Industries, commercial facilities, and agricultural users are increasingly replacing older pumps with energy-efficient models to reduce electricity consumption and operating costs. Government support for energy-saving technologies and stricter efficiency standards is further accelerating adoption.

- Industrial Water Management and Zero Liquid Discharge Creating Premium Pump Demand: Increasing focus on industrial water management and Zero Liquid Discharge (ZLD) compliance across India is driving demand for high-performance and specialized pumping systems. Industries such as chemicals, pharmaceuticals, power generation, textiles, and food processing require premium pumps capable of handling wastewater recycling, high-pressure fluid transfer, and corrosive liquids.

Market Challenges

- Copper and Steel Raw Material Cost Inflation Compressing Pump Manufacturer Margins: Water pump manufacturing uses significant quantities of cast iron, stainless steel, copper, and brass/bronze. India's commodity price spike created significant margin pressure for pump manufacturers who could not fully pass through input cost increases to government tender pricing.

Emerging Market Trends

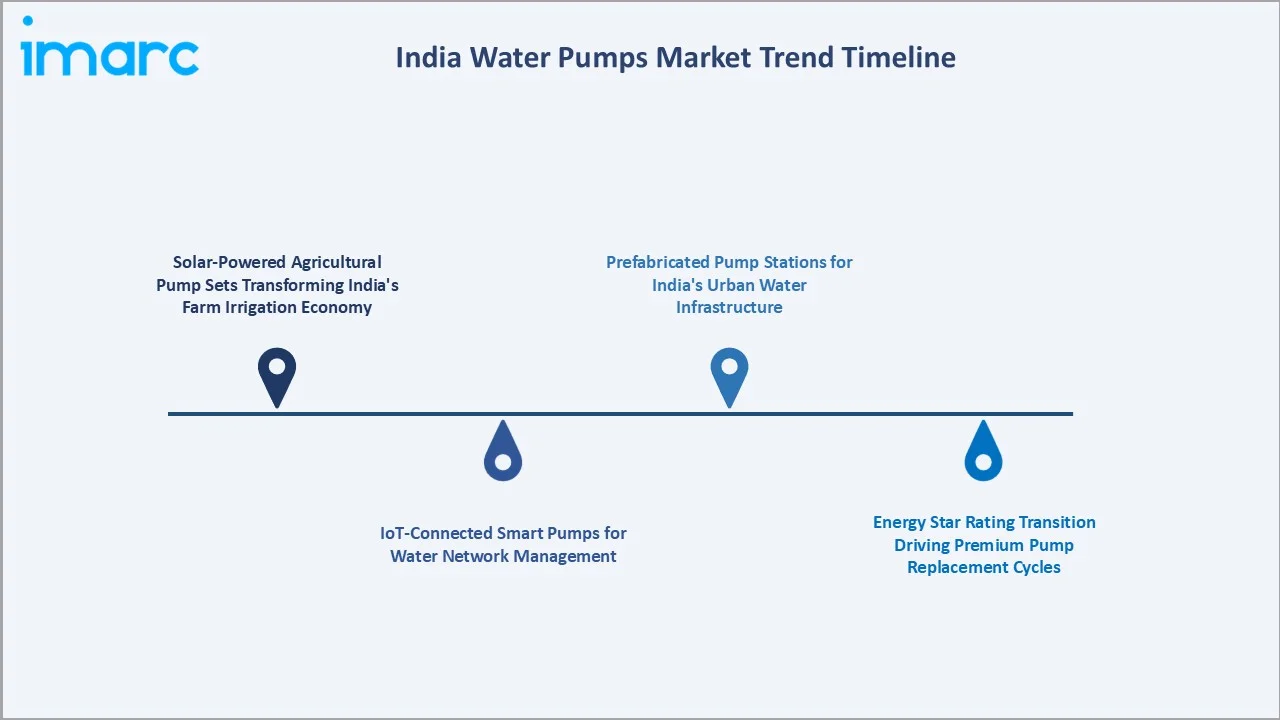

1. Solar-Powered Agricultural Pump Sets Transforming India's Farm Irrigation Economy

Solar-powered agricultural pump sets are emerging as farmers increasingly shift toward sustainable and cost-efficient irrigation solutions. Government initiatives promoting solar irrigation systems are helping reduce dependence on diesel and grid-based electricity, particularly in rural and off-grid farming regions. These pumps lower operating costs, improve irrigation accessibility, and support long-term water and energy conservation, thereby accelerating adoption across the agricultural sector.

2. IoT-Connected Smart Pumps for Water Network Management

IoT-connected smart pumps are emerging due to the rising demand for intelligent water network management and operational efficiency. These systems enable real-time monitoring of water flow, pressure, energy consumption, and predictive maintenance through remote connectivity and data analytics. In April 2026, Kirloskar Brothers Limited (KBL) introduced two new innovations, the iNSx submersible wastewater pump and KirloSmart NANO monitoring system at PLUMBEX India 2026, aimed at making water infrastructure more efficient, reliable, and digitally connected for modern needs.

3. Energy Star Rating Transition Driving Premium Pump Replacement Cycles

The transition toward higher energy star-rated pumps is emerging as consumers and industries increasingly prioritize energy-efficient equipment. Rising electricity costs and stricter efficiency regulations are encouraging the replacement of conventional pumps with premium high-efficiency models. This shift is accelerating upgrade cycles across residential, agricultural, and industrial sectors while creating strong demand for technologically advanced and low-energy pumping systems.

4. Prefabricated Pump Stations for India's Urban Water Infrastructure

Prefabricated pump stations are emerging due to rapid urbanization and increasing investments in smart water and wastewater infrastructure projects. These compact and factory-assembled systems enable faster installation, lower construction costs, and improved operational efficiency compared to conventional pump station setups. Rising demand from municipal drainage, sewage management, flood control, and urban water distribution projects is accelerating the adoption of prefabricated pumping solutions across Indian cities.

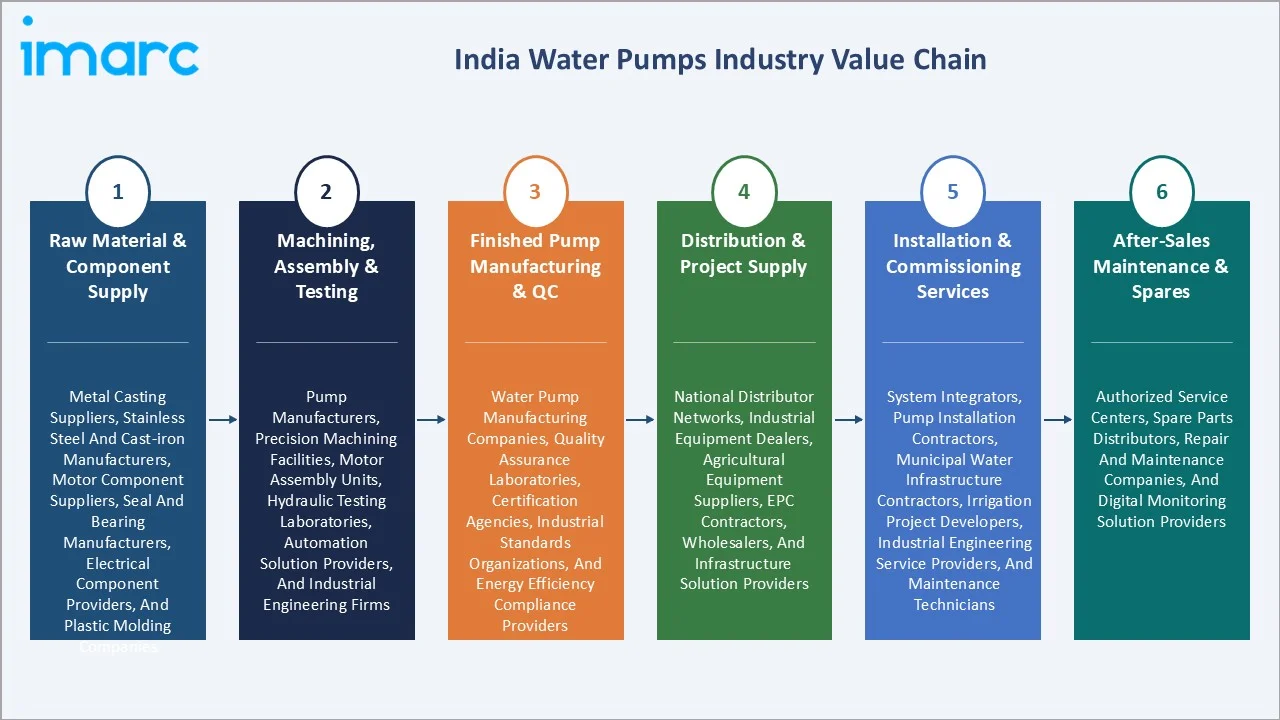

Industry Value Chain Analysis

India's water pump value chain integrates raw material and casting supply, machining and assembly operations, finished pump manufacturing with quality certification, distribution through multi-tier channel structures, installation and commissioning services, and after-sales maintenance and spare parts supply. Value addition in the manufacturing stage contributes 35-45% of finished pump value for standard products and 60-70% for premium engineered pumps. Distribution contributes 15-25% through dealer margins, freight, and warehousing.

|

Stage |

Key Participants |

|

Raw Material & Component Supply |

Metal casting suppliers, stainless steel and cast-iron manufacturers, motor component suppliers, seal and bearing manufacturers, electrical component providers, and plastic molding companies. |

|

Machining, Assembly & Testing |

Pump manufacturers, precision machining facilities, motor assembly units, hydraulic testing laboratories, automation solution providers, and industrial engineering firms. |

|

Finished Pump Manufacturing & QC |

Water pump manufacturing companies, quality assurance laboratories, certification agencies, industrial standards organizations, and energy efficiency compliance providers. |

|

Distribution & Project Supply |

National distributor networks, industrial equipment dealers, agricultural equipment suppliers, EPC contractors, wholesalers, and infrastructure solution providers. |

|

Installation & Commissioning Services |

System integrators, pump installation contractors, municipal water infrastructure contractors, irrigation project developers, industrial engineering service providers, and maintenance technicians. |

|

After-Sales Maintenance & Spares |

Authorized service centers, spare parts distributors, repair and maintenance companies, and digital monitoring solution providers. |

India's pump distribution structure is multi-tiered and regionally differentiated. Agricultural pump sales flow through kisan seva kendras, district agricultural machinery dealers, cooperative society outlets, and rural hardware stores, with the rural distribution network extending to India's villages. Industrial and building services pump sales flow through authorized distributor networks, direct sales teams for large orders, and contractor supply chains for infrastructure projects.

Technology Landscape in the India Water Pumps Industry

Centrifugal Pump Hydraulic Design Technology

Centrifugal pump hydraulic design technology improves flow efficiency, pressure performance, and energy optimization across agricultural, industrial, and municipal applications. Advanced hydraulic designs help reduce power consumption, minimize operational losses, and enhance durability under varying water conditions. Increasing demand for energy-efficient and high-capacity pumping systems is encouraging manufacturers to develop optimized impeller designs, multi-stage configurations, and smart fluid handling technologies.

Variable Frequency Drive Integration for Energy Efficiency

Variable Frequency Drive (VFD) integration enables precise motor speed control and significant energy savings. VFD-enabled pumps automatically adjust flow and pressure based on demand, reducing electricity consumption, mechanical wear, and operational costs across industrial, commercial, and municipal applications. Growing emphasis on energy-efficient infrastructure and smart water management systems is accelerating the adoption of VFD-integrated pumping solutions throughout the Indian market.

Solar Pump Drive Technology

Solar pump drive technology enables efficient irrigation and water supply solutions powered by renewable energy. These systems integrate solar panels, intelligent controllers, and energy-efficient motors to reduce dependence on grid electricity and diesel-powered pumps. In October 2024, KLK Ventures launched a new platform focused on advancing sustainable farming practices in Jammu and Kashmir through solar-powered water pumps under the PM Kusum Yojana.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Centrifugal |

74.2% |

2025 |

|

Pump Type |

🔒 |

🔒 |

2025 |

|

Pump Capacity |

🔒 |

🔒 |

2025 |

|

Application |

Agriculture |

41.5% |

2025 |

|

Region |

South India |

32.7% |

2025 |

By Type

Centrifugal pumps lead at 74.2% market share (2025). Centrifugal pumps convert rotational kinetic energy to hydrodynamic energy of fluid flow through a rotating impeller that accelerates fluid outward from the pump center. The centrifugal category encompasses the full spectrum from agricultural monoblock pump sets through multi-stage horizontal centrifugal, and submersible centrifugal.

To access detailed market analysis, Request Sample

Positive displacement pumps at 25.8% grow at ~4.2% CAGR through industrial expansion. Positive displacement pumps include reciprocating pumps for high-pressure and metering applications, rotary pumps for viscous fluid transfer, and progressive cavity pumps for sludge and slurry handling.

By Application

Agriculture leads at 41.5% market share (2025). India's agricultural pump market encompasses submersible borewell pumps for groundwater extraction, monoblock surface pumps for canal and tank irrigation, and solar pump systems under PM-KUSUM. Water and wastewater at 16.8% grow fastest at ~4.8% CAGR through sewage treatment plant construction. Building services at 13.7% grows at ~4.5% CAGR through real estate construction.

Lift irrigation at 10.4% serves India's large-scale inter-basin water transfer schemes requiring high-head centrifugal pumps for state government mega-projects. Power at 7.6% covers thermal and nuclear power plant cooling water, boiler feed, and ash slurry pumping. Oil and gas at 5.2% serves city gas distribution pump requirements. Others at 4.8% encompasses mining, construction dewatering, fire fighting, and chemical dosing applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Water Pump Market Drivers & Characteristics |

|

South India |

32.7% |

Driven by strong agricultural irrigation demand, extensive groundwater usage, and the presence of major pump manufacturing clusters. |

|

West and Central India |

27.6% |

Driven by rapid industrialization, expanding infrastructure projects, and strong demand from the agriculture and municipal water management sectors. |

|

North India |

22.4% |

Supported by large-scale agricultural irrigation activities, growing urban infrastructure development, and rising demand for residential and commercial water supply systems. |

|

East India |

17.3% |

Driven by improving agricultural mechanization, expanding rural water supply programs, and increasing investments in flood management and irrigation infrastructure. |

South India's 32.7% leadership reflects the virtuous cycle of manufacturing proximity, the region's intensive agricultural pump usage, and Karnataka's premium real estate market, driving building services pump demand at a higher per-unit value than agricultural pump sales.

West and Central India, at 27.6%, reflects Maharashtra and Gujarat's industrial and agricultural pump diversity. North India, at 22.4%, is dominated by agricultural submersible pump demand from the Indo-Gangetic Plain's intensive borewell irrigation farming, plus Delhi building services premium market. East India at 17.3% is growing from a lower base, with Odisha's mining sector, West Bengal's industrial base, and Bihar's agricultural JJM pump procurement representing the region's primary demand drivers.

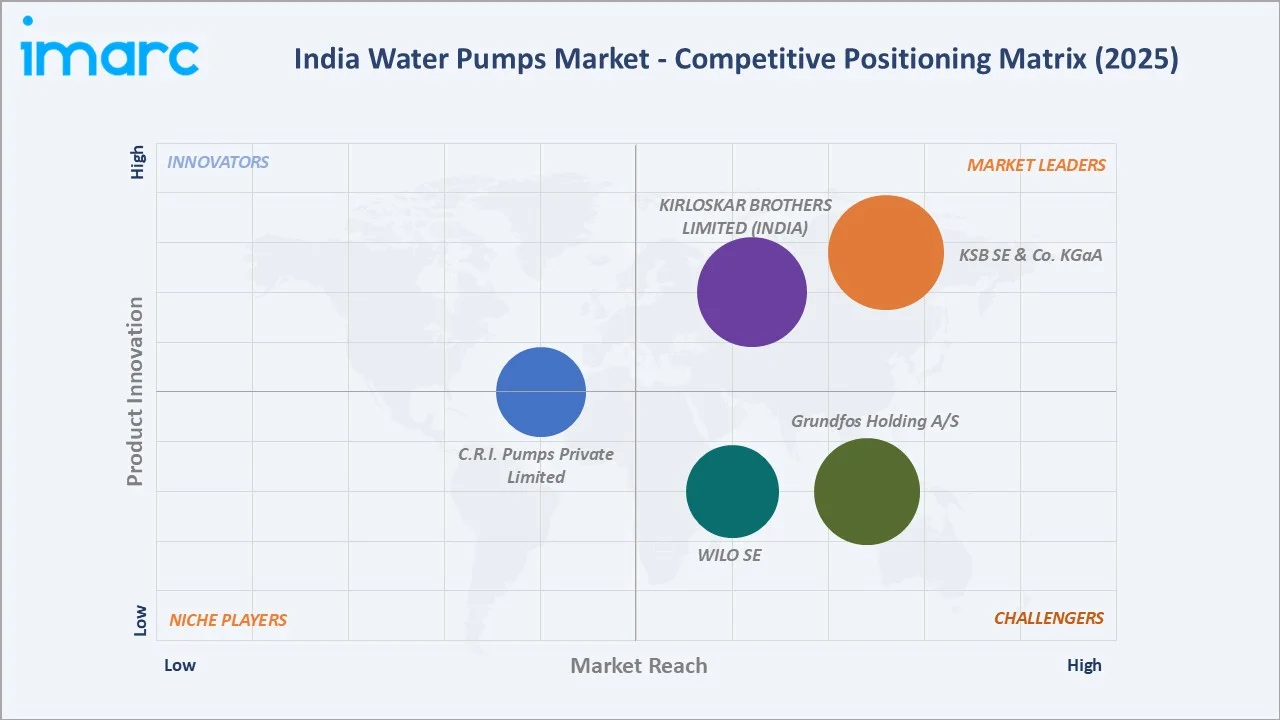

Competitive Landscape

India's water pump competitive landscape has a distinctive three-tier structure: multinational subsidiaries with global technology platforms competing for premium industrial, municipal, and building services applications; Indian-headquartered mid-to-large manufacturers competing across agricultural, municipal, and building services segments; and a large unorganized and small-scale manufacturer segment competing primarily on price in the mass-market agricultural and domestic pump categories.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

KSB SE & Co. KGaA |

AGRIBLOC, AmaCan D, Amacan K, AmaCan P, Amacan S, Amarex |

Market Leader |

Operating in India as KSB Limited. As an experienced pump manufacturer, its product portfolio includes building and industrial technology, water transport, wastewater treatment and power plant processes. |

|

KIRLOSKAR BROTHERS LIMITED (INDIA) |

Submersible Sewage Dewatering Pump - SW, Submersible Wastewater Pump- iNSx, Cutter Pump - CWC, Vertical Inline Short Coupled Pump - KW-SC, Vertical Inline Long Coupled Pump - KW-LC |

Market Leader |

A leader in fluid management solutions, delivering innovative and sustainable technologies |

|

Grundfos Holding A/S |

ALPHA1, AP, AP50, SB, SBA, TP |

Strong Challenger |

Grundfos has a wide array of products, pump solutions and services for all applications. |

|

WILO SE |

Wilo-MISO/PISO, Wilo-SK/KN/SW, Wilo-HSC Engineered Pumps, Wilo-Vertical Centrifugal Sump Pump |

Strong Challenger |

Wilo India plays a vital role in providing water supply solutions for the building services, water management, and industrial sectors. |

|

C.R.I. Pumps Private Limited |

80mm Submersible, 85mm Submersible, 100mm Submersible, 125mm Submersible, 150mm Submersible, 200mm Submersible |

Established Player |

C.R.I has decades of expertise and experience in developing and manufacturing a wide range of pump sets. |

The competitive landscape is being reshaped by PM-KUSUM's solar pump mandate, creating Shakti Pumps as a new large-cap listed player with dedicated solar pump manufacturing capability that KSB, Grundfos, and Wilo's product platforms do not match at government tender pricing. Simultaneously, Grundfos and Wilo's IoT-enabled smart pump product innovation is creating premium differentiation in the building services and municipal water management segment that domestic manufacturers cannot yet match with equivalent digital capability.

Key Company Profiles

KSB SE & Co. KGaA

KSB SE & Co. KGaA is one of the world's leading pump and valve manufacturers with a global heritage. KSB represents India's premier industrial and infrastructure pump brand, serving the country's most demanding pump applications.

- Key Products: AGRIBLOC, AmaCan D, Amacan K, AmaCan P, Amacan S, Amarex.

- Recent Developments: In September 2024, the KSB Group launched a new generation of submersible motor pumps on the market. The pumps of the type series called AmaRex Pro are driven by high-efficiency motors of class IE5.

- Strategic Focus: Focused on expanding its presence in the India water pumps market through energy-efficient pumping solutions, industrial fluid management systems, and localized manufacturing and service capabilities.

KIRLOSKAR BROTHERS LIMITED (India)

Kirloskar Brothers Limited (KBL) is India's largest domestic pump company. As the flagship company of the Kirloskar Group, KBL serves critical sectors including water supply, irrigation, power, oil & gas, and marine & defence, and has reinforced its position in India's smart water infrastructure segment.

Key Products: Submersible Sewage Dewatering Pump - SW, Submersible Wastewater Pump- iNSx, Cutter Pump - CWC, Vertical Inline Short Coupled Pump - KW-SC, Vertical Inline Long Coupled Pump - KW-LC.

- Recent Developments: In April 2026, Kirloskar Brothers Limited launched two transformative products, the submersible wastewater pump, iNSx and the compact IoT-based remote monitoring solution, KirloSmart Nano, at PLUMBEX India 2026.

- Strategic Focus: Enhancing its market presence in India by expanding its portfolio of high-efficiency pumps, digital pumping systems, and customized solutions for irrigation, municipal water supply, and industrial sectors.

Market Concentration Analysis

India's water pump market exhibits moderate concentration at the organized sector level with high fragmentation at the total market level when unorganized sector is included. The top 5 organized sector pump companies (KSB, Kirloskar, Grundfos, Wilo, C.R.I. Pumps) collectively account for approximately 40-45% of total market revenue. This moderate concentration reflects the market's structural diversity; no single company can address the full spectrum from agricultural monoblock to custom industrial centrifugal, leading to natural specialization where KSB leads industrial, Kirloskar leads government project, Grundfos leads building services premium, and CRI leads South India agricultural. The unorganized sector collectively accounts for approximately 20-25% of total market volume (units) but only 8-12% of market revenue (value) due to its concentration in low-value agricultural and domestic pump categories.

Government procurement consolidation is progressively concentrating government pump tenders toward BIS-certified organized sector manufacturers, creating market share gains for Kirloskar and CRI Pumps at the expense of uncertified small manufacturers in the agricultural segment. This formalization trend, combined with BEE energy efficiency mandatory minimum standards for new pump production, is structurally improving the organized sector's market position while constraining the unorganized sector's growth, which suggests market concentration at the organized sector level will increase gradually through 2034.

Investment & Growth Opportunities

Highest Growth Segments

Water and wastewater pumps (~4.8% CAGR), building services pumps (~4.5% CAGR), positive displacement pumps (~4.2% CAGR), solar agricultural pump systems (~15-20% CAGR for the solar subcategory specifically), and smart IoT-connected pump monitoring services (new category growing at 25%+ from a small base) represent India's highest-growth water pump investment vectors. Solar agricultural pumps, while a sub-segment of the agriculture application category, are growing dramatically faster than overall agricultural pump demand through PM-KUSUM's massive government subsidy program.

Emerging Opportunities

India's municipal non-revenue water management program represents an emerging pump-related investment opportunity. India's water utilities lose an estimated 40-50% of treated water to distribution network leakage and theft (NRW) versus the 15-20% best-practice benchmark. Advanced pump system management can reduce NRW by 10-20 percentage points, saving significant water and energy.

Investment Themes

- PM-KUSUM solar pump manufacturing capacity for government tender supply: The government is target of 3.5 million solar pump installations, representing a high annual government-supported market. New entrants or existing pump manufacturers investing in motor manufacturing capability, solar pump controller design, and test certification can address this market at competitive returns, given the government subsidy framework's revenue visibility.

- Premium building services pump market in India's tier-1 and tier-2 city real estate expansion: India's real estate sector generates building services pump demand. The premium high-rise residential segment commands specifications for intelligent variable-speed pump systems, where energy efficiency certification and smart building integration create specification preference that protects premium pricing.

Future Market Outlook (2026-2034)

The India water pumps market is projected to grow from USD 2.07 Billion in 2025 to USD 3.01 Billion by 2034, delivering a 3.74% CAGR over the forecast period. The market's anchor value of USD 2.48 Billion in 2030 represents an Indian pump industry where PM-KUSUM solar agricultural pump systems are transforming India's agrarian energy landscape, and India's industrial and real estate construction expansion has elevated building services and process pump demand substantially above the 2025 baseline.

Three structural forces define India's water pump market growth through 2034 with high confidence: India's water infrastructure deficit creates a decade-long infrastructure investment pipeline that generates pump demand that government policy, rather than market cycles, primarily drives; India's agricultural transition from flood irrigation toward micro-irrigation and borewell irrigation structurally increases per-hectare pump value; and India's manufacturing sector expansion under PLI Schemes creating industrial process pump demand growth that outpaces GDP growth as organized manufacturing share of India's economy.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including senior executives and product managers; pump system procurement managers; agricultural pump end users and dealer networks in Tamil Nadu, Maharashtra, and Uttar Pradesh; BIS and BEE certification officers providing pump standard compliance market intelligence; PM-KUSUM state nodal agencies in Rajasthan and Madhya Pradesh; and District Implementation Units in Bihar and Rajasthan.

Secondary Research

Secondary research encompassed BEE (Bureau of Energy Efficiency) pump efficiency program reports and agricultural pump star rating database; BIS mandatory pump certification portal data; PM-KUSUM implementation progress reports (2020-2025); Jal Jeevan Mission dashboard data (household tap connections, pump procurement statistics); AMRUT 2.0 project implementation monitoring data; individual company annual reports and investor presentations; Ministry of Agriculture groundwater development statistics; and groundwater assessment unit data. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up type and application models calibrated against BIS pump certification data, BEE pump star rating shipment data for agricultural pump sets, PM-KUSUM annual solar pump installation tracking data, real estate construction commencement data for building services pump demand modeling, and the industrial production index for industrial process pump demand proxy.

India Water Pumps Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Centrifugal, Positive Displacement |

| Pump Types Covered | Submersible Pumps, Multistage Pumps, End Suction Pumps, Split Case Pumps, Engineered Pumps, Others |

| Pump Capacity Covered | Up to 3 HP, 3-5 HP, 5-10 HP, 10-15 HP, 15-20 HP, 20-30 HP, More Than 30 HP |

| Applications Covered | Agriculture, Building Services, Water and Wastewater, Power, Oil and Gas, Lift Irrigation, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | KSB SE & Co. KGaA, KIRLOSKAR BROTHERS LIMITED (INDIA), Grundfos Holding A/S, WILO SE, C.R.I. Pumps Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Water Pumps Market Research Report and Industry Forecast Report

The India water pumps market reached USD 2.07 Billion in 2025, driven by the PM-KUSUM solar agricultural pump scheme, Jal Jeevan Mission piped water supply pump procurement, urban water infrastructure investment, India's real estate construction driving building services pump demand, and industrial sector expansion requiring process pumps across pharmaceutical, chemical, power, and oil and gas sectors.

The market grows at 3.74% CAGR during 2026-2034, reaching USD 3.01 Billion by 2034, driven by PM-KUSUM solar pump cumulative installations, urban water infrastructure execution, building services premium pump demand growth from India's real estate expansion, and industrial process pump demand growth from the PLI scheme manufacturing expansion.

Centrifugal pumps lead at 74.2% through dominance in agricultural submersible, monoblock surface irrigation, municipal water distribution, and building services pressure boosting applications.

Agriculture leads at 41.5% through India's agricultural electric pump connections plus PM-KUSUM solar pump additions.

South India leads at 32.7% through Tamil Nadu's agricultural pump connections, Coimbatore pump manufacturing cluster, Karnataka's premium building services pump demand from Bengaluru real estate, and Andhra Pradesh/Telangana's large-scale lift irrigation projects requiring high-head centrifugal pump supply.

Leading companies include KSB SE & Co. KGaA, Kirloskar Brothers Limited (India), Grundfos Holding A/S, WILO SE, and C.R.I. Pumps Private Limited, among others.

The market is projected to reach approximately USD 2.48 Billion by 2030, with PM-KUSUM solar pump cumulative installations, rural water supply pump installations largely complete with the replacement cycle beginning, urban water projects in execution, smart IoT pump monitoring, and India's industrial manufacturing expansion generating sustained process pump demand growth.

PM-KUSUM (Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan) is India's national solar agricultural pump scheme for 3.5 million standalone solar pump installations. Component B (solar agricultural pumps) creates supplier demand for solar submersible pump systems.

IoT-connected smart pumps are transforming India's municipal and industrial pump management from reactive maintenance to predictive maintenance.

Three priority opportunities: PM-KUSUM BLDC solar pump manufacturing for government tender supply; premium building services VFD-integrated pump systems for India's high-rise real estate market; and industrial wastewater treatment specialized pump systems for compliance-mandated Indian industrial units.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)