India Welding Equipment Market Size, Share, Trends and Forecast by Technology, Type, End Use, and Region, 2026-2034

India Welding Equipment Market Summary:

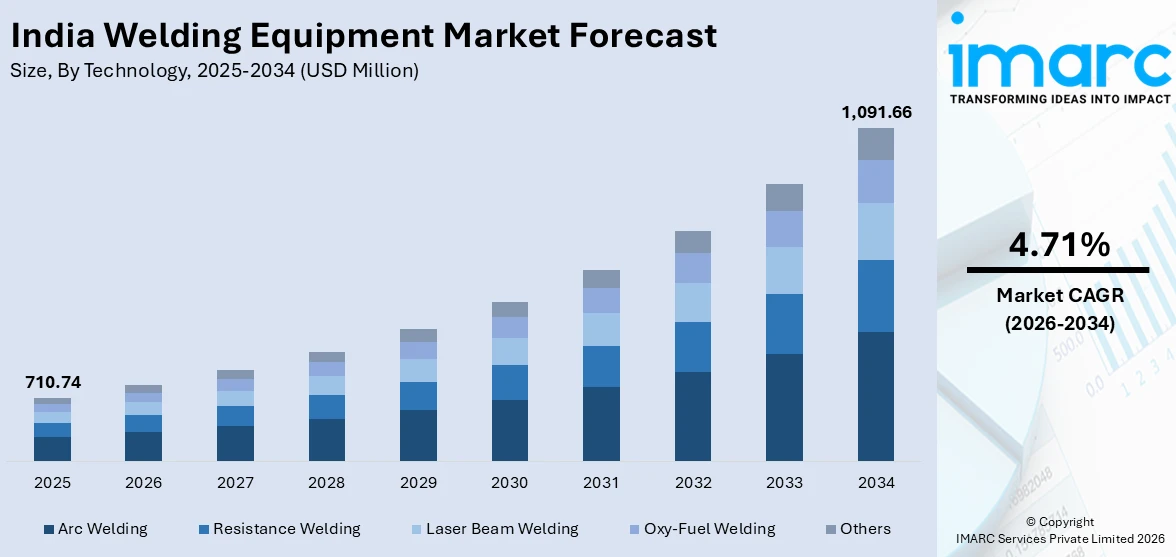

The India welding equipment market size was valued at USD 710.74 Million in 2025 and is projected to reach USD 1,091.66 Million by 2034, growing at a compound annual growth rate of 4.71% from 2026-2034.

The India welding equipment market is experiencing robust momentum as the country accelerates its industrialization drive and scales up infrastructure spending. Growing demand from the automotive, construction, and energy sectors is reinforcing adoption of advanced welding solutions. Government-backed manufacturing initiatives, expanding defense production capabilities, and increasing integration of automation technologies are reshaping welding practices. Rising investments in renewable energy, railway modernization, and smart city developments are further strengthening the demand for high-performance welding equipment, positioning India as a dynamic hub for welding technology innovation and India welding equipment market share.

Key Takeaways and Insights:

- By Technology: Arc welding dominates the market with a share of 76.2% in 2025, owing to its versatility, cost-effectiveness, and wide applicability across construction, automotive, and heavy engineering sectors. Continuous advancements in inverter-based power sources are further fueling adoption.

- By Type: Manual welding represents the largest segment with a market share of 42.5% in 2025, reflecting the continued reliance on skilled manual welders across infrastructure projects, repair and maintenance operations, and small-scale fabrication workshops throughout India.

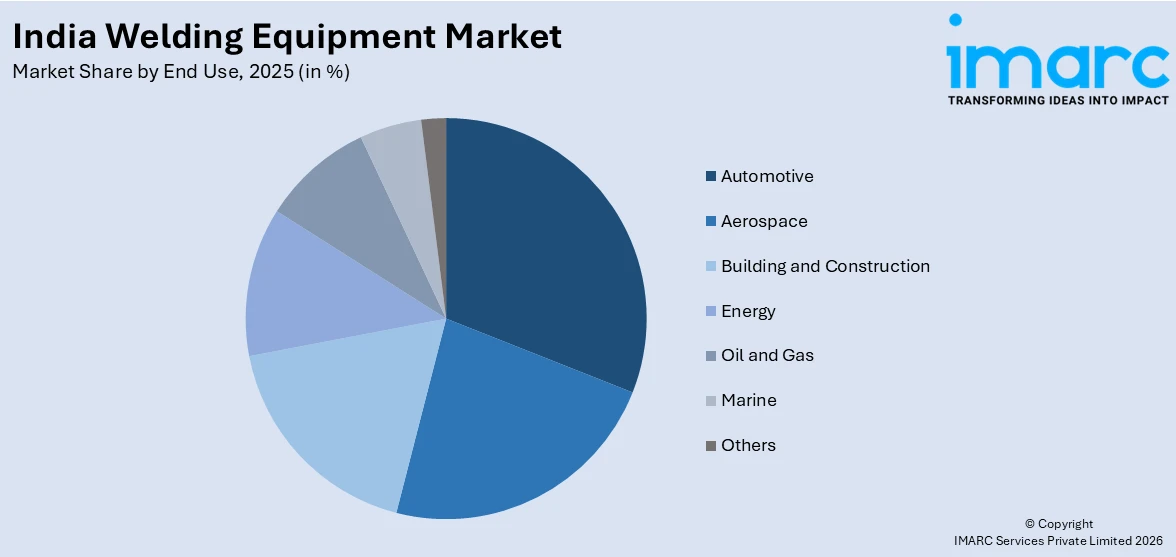

- By End Use: Automotive exhibits a clear dominance with 27.5% share in 2025, supported by India’s position as the third-largest automobile market globally, record vehicle production volumes, and expanding electric vehicle manufacturing capabilities.

- By Region: West India holds the largest region with 30.5% share in 2025, driven by the concentration of automotive manufacturing clusters, heavy industrial activity, and major infrastructure projects across Maharashtra and Gujarat.

- Key players: Key players drive the India welding equipment market by expanding product portfolios, investing in automation and robotic welding solutions, strengthening nationwide distribution networks, and introducing energy-efficient technologies to meet diverse industrial requirements.

To get more information on this market Request Sample

The India welding equipment market is advancing as industries adopt modern joining technologies to address rising production demands and quality benchmarks. A major catalyst shaping this progress is the country's unprecedented infrastructure push, supported by government programs that prioritize capital-intensive construction and manufacturing development. The need for welding equipment in structural fabrication, pipeline construction, and heavy engineering applications is increasing due to the expansion of highway networks, railway modernization initiatives, and smart city developments. Expanding automotive production, growing defense manufacturing capabilities under the Atmanirbhar Bharat initiative, and increasing adoption of automated welding systems are further reinforcing the market's upward trajectory. The convergence of policy support, industrial modernization, and technological innovation is creating a favorable environment for sustained growth. Rising investments in renewable energy infrastructure and shipbuilding activities are also broadening the application scope of advanced welding solutions, positioning the India welding equipment market for continued expansion.

India Welding Equipment Market Trends:

Rising adoption of automated and robotic welding systems

India’s welding industry is witnessing a significant shift toward automation as manufacturers seek enhanced precision and operational efficiency. Industries including automotive, heavy engineering, and construction are increasingly integrating robotic arms and collaborative robots into their welding operations. For instance, in February 2025, Delta debuted its D-Bot series of collaborative robots at ELECRAMA 2025, featuring payload ratings of up to 30 kg and speeds of 200 degrees per second for high-precision welding applications. Government initiatives promoting smart manufacturing and Industry 4.0 adoption are accelerating this transition across Indian factories.

Integration of AI-driven smart welding technologies

The fusion of artificial intelligence and IoT-enabled sensors is transforming welding equipment capabilities in India. Smart welding machines now offer real-time monitoring of temperature, voltage, and weld seam positioning, enabling predictive maintenance and instant error detection. Advanced algorithms optimize welding parameters automatically, producing high-quality welds with minimal material wastage. Integration of cloud-based data analytics and remote diagnostics is further enhancing operational efficiency across manufacturing facilities. These innovations are helping manufacturers achieve consistent weld quality while reducing equipment downtime and improving overall production throughput across diverse industrial applications.

Growing focus on energy-efficient and sustainable welding solutions

India's welding sector is increasingly prioritizing energy efficiency and environmental sustainability in equipment design and operation. Manufacturers are developing battery-powered welders, inverter-based machines, and low-emission processes aligned with national sustainability goals. The growing emphasis on reducing carbon footprints across industrial operations is driving demand for welding equipment that consumes less power and produces fewer harmful emissions. The adoption of energy management systems, eco-friendly shielding gases, and recyclable consumable materials is complementing green manufacturing practices across Indian industries. These advancements reflect a broader commitment to sustainable production methods while maintaining high-performance welding capabilities.

Market Outlook 2026-2034:

The Indian market for welding equipment is expected to experience continuous growth, driven by the acceleration of industrialization, large-scale development of infrastructure, and the expansion of automation technologies in major manufacturing industries. The synergy of government initiatives, including the Make in India program and the National Infrastructure Pipeline, and the expansion of private sector investments in advanced manufacturing technologies is expected to create continuous growth opportunities. The increase in production volumes of automobiles, modernization of railway networks, development of renewable energy sources, and expansion of defense manufacturing activities are expected to create continuous equipment purchase opportunities. The development of advanced technologies, including robotic, laser, and smart technologies, is expected to create continuous growth opportunities, thereby enhancing the overall technology maturity of the Indian welding equipment market. The market generated a revenue of USD 710.74 Million in 2025 and is projected to reach a revenue of USD 1,091.66 Million by 2034, growing at a compound annual growth rate of 4.71% from 2026-2034.

India Welding Equipment Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Technology |

Arc Welding |

76.2% |

|

Type |

Manual |

42.5% |

|

End Use |

Automotive |

27.5% |

|

Region |

West India |

30.5% |

Technology Insights:

- Arc Welding

- Shielded Metal/Stick Arc Welding

- MIG

- TIG

- Plasma Arc Welding

- Others

- Resistance Welding

- Laser Beam Welding

- Oxy-Fuel Welding

- Others

Arc welding dominates with a market share of 76.2% of the total India welding equipment market in 2025.

Arc welding continues to be the backbone of India’s welding equipment landscape, commanding the largest technology share due to its exceptional versatility and cost-effectiveness across diverse industrial applications. The technology’s ability to deliver high heat concentration, efficient metal deposition, and strong corrosion-resistant joints makes it indispensable for construction, automotive manufacturing, and heavy engineering operations. Its compatibility with a wide range of base metals and thickness levels ensures broad adoption across both organized and unorganized manufacturing sectors, reinforcing its dominant position in the country’s evolding welding ecosystem.

The ongoing modernization of arc welding equipment through inverter-based power sources and digital control systems is further strengthening its market leadership. Advanced inverter welding machines offer energy efficiency, lightweight portability, and improved arc characteristics that bridge the skill gap between highly trained and less experienced welders. The integration of programmable settings, adaptive arc control, and real-time feedback mechanisms enables consistent weld quality across diverse applications. Growing investments in welding skill development centers equipped with modern training equipment are also enhancing workforce capabilities across the country.

Type Insights:

- Automatic

- Semi-Automatic

- Manual

Manual represents the largest segment with a 42.5% share of the total India welding equipment market in 2025.

Manual welding continues to hold the largest share in India’s welding equipment market, reflecting the country’s extensive reliance on skilled manual welders across construction sites, repair workshops, and small to medium-sized fabrication units. The accessibility and affordability of manual welding equipment make it the preferred choice for a vast number of welding operations, particularly in rural infrastructure projects, maintenance applications, and unorganized manufacturing sectors. India’s diverse industrial landscape, characterized by varying scales of operation and infrastructure maturity, sustains strong demand for manual welding solutions throughout the country.

The enduring dominance of manual welding is reinforced by India’s massive infrastructure development programs that generate sustained demand for portable and versatile welding equipment. Large-scale projects including highway construction under the Bharatmala Pariyojana initiative covering over 34,800 kilometers of highways, metro rail expansions across multiple cities, and the Smart Cities Mission spanning over 100 cities require extensive on-site manual welding for structural steel fabrication, pipeline connections, and general maintenance operations. Despite the growing shift toward automation, manual welding remains foundational to India’s welding ecosystem.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Aerospace

- Automotive

- Building and Construction

- Energy

- Oil and Gas

- Marine

- Others

Automotive holds the largest share at 27.5% of the total India welding equipment market in 2025.

The automotive sector commands the largest end-use share in India’s welding equipment market, driven by the country’s position as the third-largest automobile market globally and its record-breaking vehicle production volumes. Welding is integral to automotive manufacturing processes including body-in-white assembly, chassis fabrication, exhaust system production, and component joining, creating sustained demand for both manual and automated welding equipment. The growing emphasis on lightweight materials, electric vehicle manufacturing, and high-strength steel applications is further intensifying the need for advanced welding technologies across India’s automotive sector.

India's automotive industry continues to expand at a remarkable pace, reinforcing its dominant role in driving welding equipment demand. The country's position as the third-largest automobile market globally ensures sustained procurement of welding solutions for body-in-white assembly, chassis fabrication, and component joining operations. This robust production momentum, combined with increasing electric vehicle manufacturing investments, export-oriented growth strategies, and the introduction of lightweight material applications, ensures that the automotive sector remains the primary engine of welding equipment consumption across the country.

Regional Insights:

- North India

- South India

- East India

- West India

West India represents the leading segment with a 30.5% share of the total India welding equipment market in 2025.

West India holds the maximum regional market share in the India welding equipment market due to the presence of a large number of automotive clusters, industrial activities, and mega infrastructure development projects within the region of Maharashtra and Gujarat states. The region is home to large automotive assembly units, shipbuilding yards, petrochemical complexes, which provide a consistent market demand for welding equipment for manual as well as automatic welding operations. Maharashtra contributes a welding market share of 18% to the total India welding market.

This regional market share is further supplemented by mega infrastructure development activities and healthy industrial investments within the region of West India. The region includes mega infrastructure development projects such as the Mumbai Trans Harbour Link, Pune Metro development, Gujarat industrial corridor development projects, which are maintaining a healthy demand for welding equipment services. The established distribution channel of welding equipment within the region of West India is supplemented by the presence of organized welding equipment manufacturers within this region. The region of West India includes a diverse range of automotive clusters within Pune, industrial areas within Gujarat, and shipbuilding activities along the western coast of India.

Market Dynamics:

Growth Drivers:

Why is the India Welding Equipment Market Growing?

Massive government-led infrastructure development programs

India’s unprecedented infrastructure expansion is creating substantial demand for welding equipment across construction, transportation, and energy sectors. The government’s sustained commitment to capital-intensive infrastructure spending is driving large-scale procurement of welding solutions for structural fabrication, pipeline construction, bridge building, and railway modernization projects. Highway construction under the Bharatmala Pariyojana initiative, metro rail expansions across over 15 cities, and the development of industrial corridors are generating consistent demand for both manual and automated welding equipment throughout the country. The scale of infrastructure investment continues to grow significantly, directly translating into higher welding equipment consumption. Additionally, the Second Asset Monetization Plan for 2025-30 aims to reinvest INR 10 lakh crore in new projects. These investments are catalyzing demand across structural steel welding, pipeline fabrication, and heavy engineering applications, ensuring sustained market growth.

Expanding automotive and defense manufacturing capabilities

India’s automotive industry, the third-largest globally, is a primary driver of welding equipment demand through its extensive use of welding in vehicle body assembly, component fabrication, and exhaust system production. The sector’s robust growth trajectory, coupled with increasing electric vehicle manufacturing investments, is intensifying the need for advanced welding technologies including robotic MIG welding, laser welding, and resistance spot welding across automotive production facilities. Defense manufacturing under the Atmanirbhar Bharat initiative is simultaneously expanding welding equipment requirements. The production of fighter aircraft, submarines, warships, and missile systems demands precision welding techniques including friction stir welding and electron beam welding. This record production volume directly amplifies welding equipment procurement across the country’s automotive manufacturing ecosystem.

Accelerating adoption of advanced welding technologies and automation

The integration of automation, robotics, and digital technologies into India’s welding operations is driving demand for technologically advanced welding equipment. Industries are increasingly transitioning from traditional manual processes to automated and semi-automated systems that offer superior precision, consistency, and productivity. The adoption of Industry 4.0 principles, including IoT-enabled monitoring, AI-driven quality control, and predictive maintenance capabilities, is reshaping welding equipment specifications and procurement patterns across manufacturing sectors. Government programs are actively facilitating this technological transition. Similarly, the Make in India program and Production Linked Incentive schemes are encouraging investments in advanced manufacturing equipment. These policy frameworks, combined with the growing shortage of skilled manual welders, are accelerating the shift toward automated welding solutions and creating new demand vectors for the market.

Market Restraints:

What Challenges the India Welding Equipment Market is Facing?

High cost of advanced welding equipment and automation systems

The significant capital investment required for acquiring automated and robotic welding systems presents a substantial barrier, particularly for small and medium-sized enterprises that form a large portion of India’s manufacturing base. Advanced technologies including laser welding machines, collaborative robots, and IoT-enabled systems carry premium pricing that limits accessibility. The absence of widespread affordable financing options and the high cost of maintenance and training further constrain broader adoption of technologically sophisticated welding equipment across cost-sensitive Indian industries.

Acute shortage of skilled welding professionals

India faces a persistent gap between the demand for and supply of qualified welding professionals capable of operating modern equipment and meeting stringent quality standards. While industrial demand for skilled welders continues to rise with expanding infrastructure and manufacturing activities, training infrastructure remains insufficient to produce adequately trained personnel. The limited number of specialized welding training centers, coupled with the industry’s challenge of attracting new talent to physically demanding welding occupations, creates operational bottlenecks that slow production efficiency and constrain market growth potential.

Dominance of the unorganized sector and price-sensitive competition

The prevalence of unorganized players creates intense price competition that challenges organized manufacturers seeking to introduce technologically advanced products. Many small fabrication workshops and construction contractors prioritize low-cost equipment over quality and innovation, limiting the addressable market for premium welding solutions. The lack of stringent quality enforcement standards across certain industry segments enables low-cost alternatives to compete effectively, creating pricing pressure that can compress margins and discourage investment in advanced product development.

Competitive Landscape:

The India welding equipment market has both established local players and international technology leaders competing in various product segments. Players are increasingly focusing on building product portfolios that offer manual, semi-automatic, and automatic welding solutions, along with building distribution networks across the country to cater to the needs of diverse industrial customers. Strategic investments in developing robotic welding, green technology, and artificial intelligence-based monitoring systems are the major strategies that technology leaders are adopting for differentiation. Partnerships with educational institutions, enhancing after-sales services, and developing products that meet local operating conditions are some of the major strategies that players are adopting for intense market competition, especially in the industrial segment.

India Welding Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered |

|

| Types Covered | Automatic, Semi-Automatic, Manual |

| End Uses Covered | Aerospace, Automotive, Building and Construction, Energy, Oil and Gas, Marine, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India welding equipment market size was valued at USD 710.74 Million in 2025.

The India welding equipment market is expected to grow at a compound annual growth rate of 4.71% from 2026-2034 to reach USD 1,091.66 Million by 2034.

Arc welding dominated the market with a share of 76.2%, driven by its versatility, cost-effectiveness, and extensive applicability across construction, automotive, and heavy engineering sectors throughout India.

Key factors driving the India welding equipment market include massive government infrastructure spending, expanding automotive production, defense manufacturing modernization, growing adoption of robotic and automated welding systems, and increasing renewable energy project developments.

Major challenges include high costs of advanced welding equipment and automation systems, acute shortage of skilled welding professionals, dominance of unorganized sector players, price-sensitive competition, and limited access to affordable financing for technology upgrades among small-scale manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)