India Whey Protein Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

India Whey Protein Market Size, Share, Trends & Forecast (2026-2034)

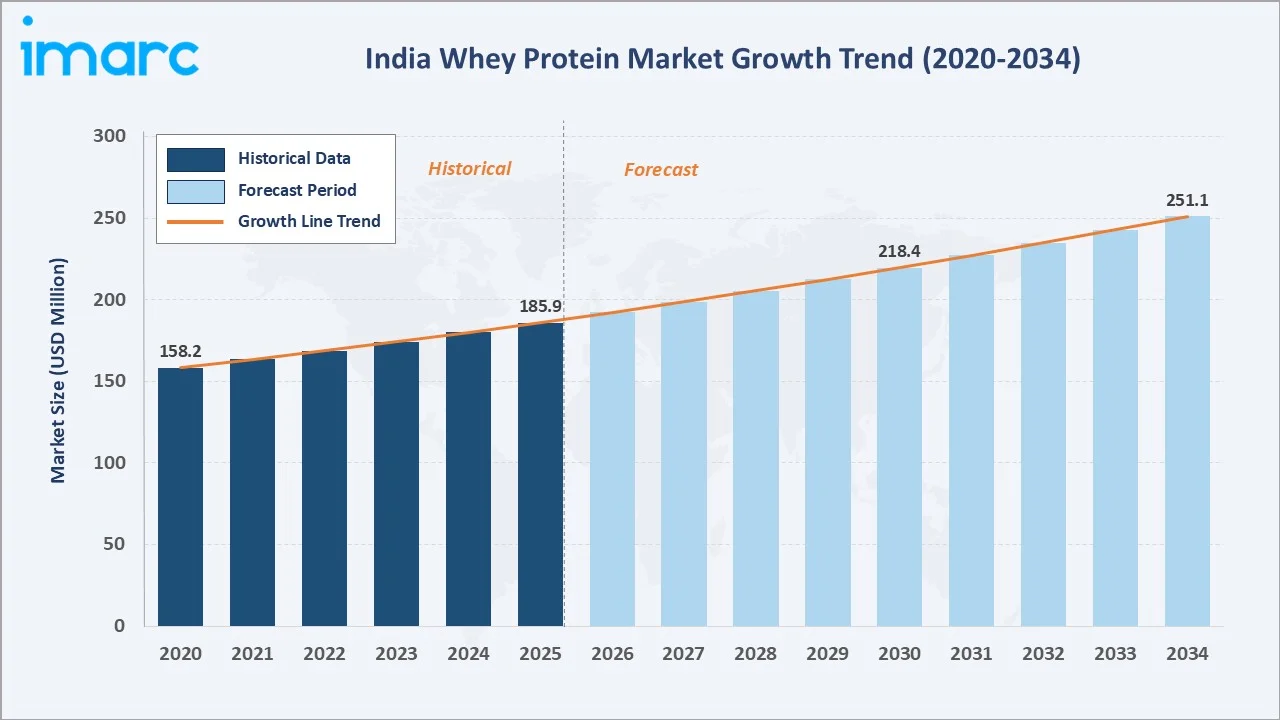

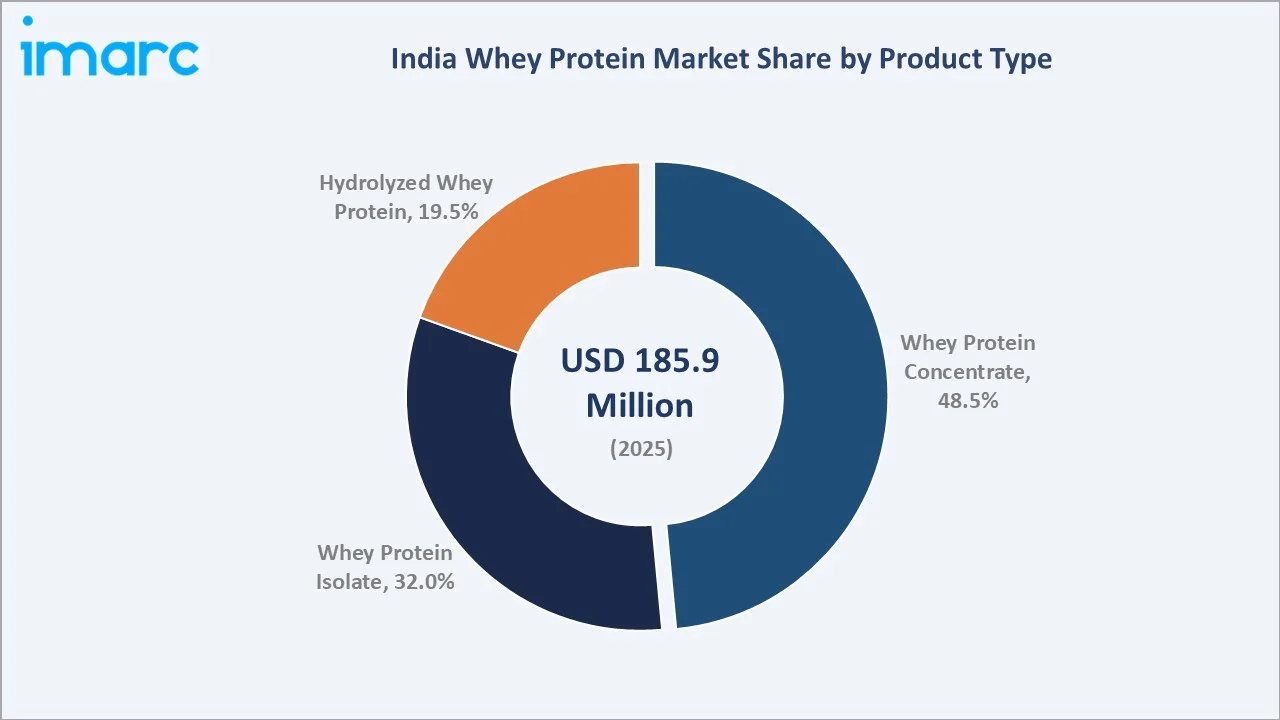

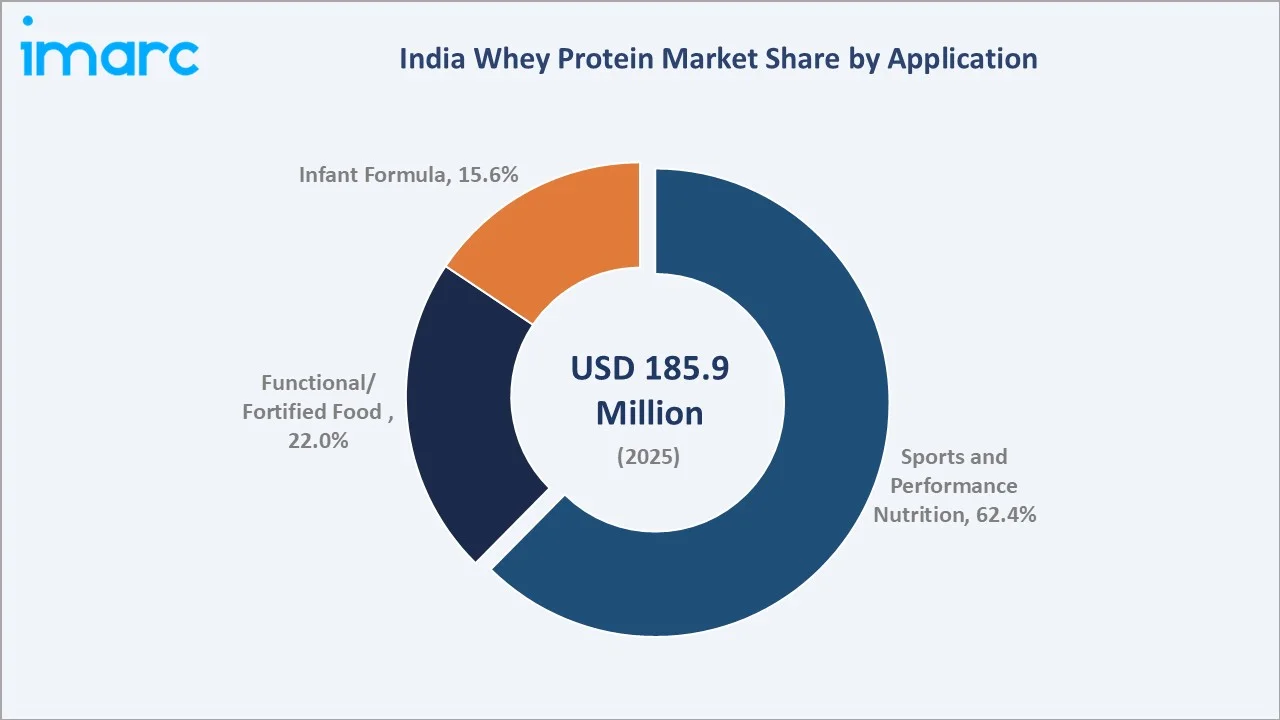

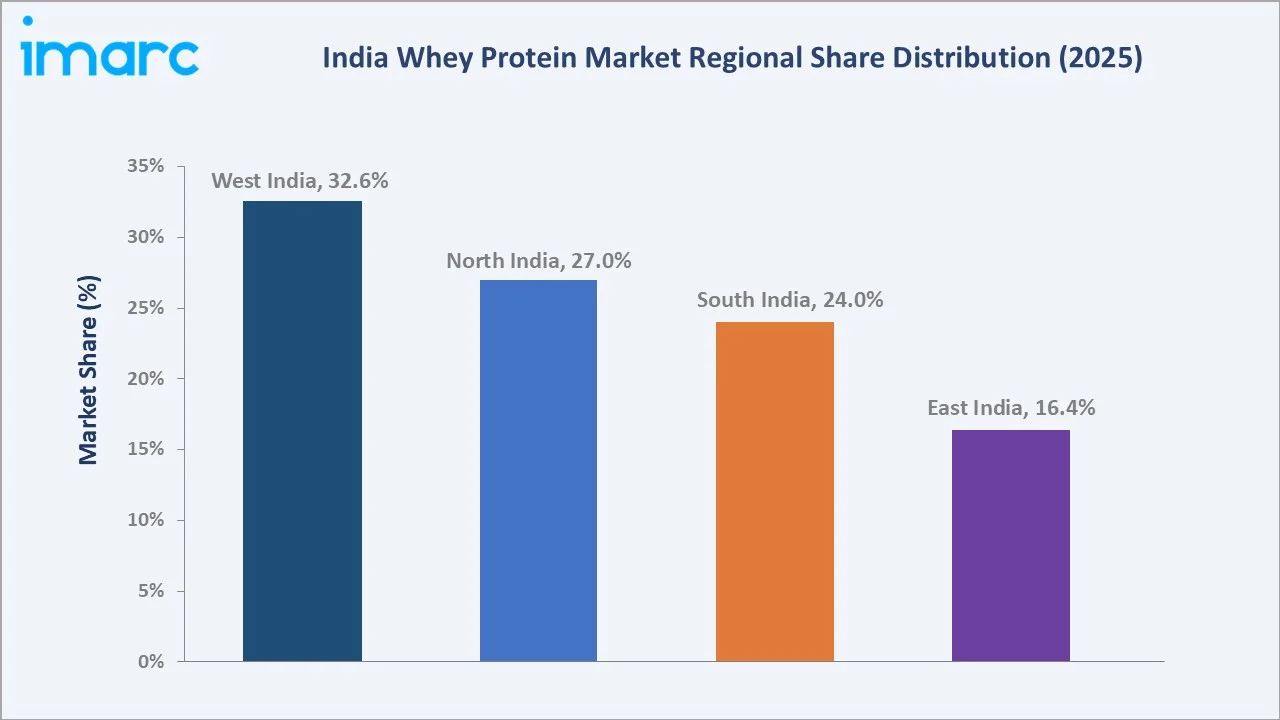

The India whey protein market reached USD 185.9 Million in 2025 and is projected to reach USD 251.1 Million by 2034, growing at a CAGR of 3.27% during 2026-2034. The market is driven by rising health consciousness, growing gym and fitness culture, and increasing demand for convenient high-protein supplements among urban consumers. India’s commercial fitness industry is growing rapidly, supported by nearly 46,500 fitness facilities and 12.3 million members in 2024. This indicates significant room for expansion, which is driving the India whey protein market as rising gym participation, fitness awareness, and demand for muscle recovery and performance nutrition increase the consumption of whey-based supplements. Whey protein concentrate leads at 48.5%. Sports and performance nutrition dominate the application at 62.4%. West India commands 32.6% of the national market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 185.9 Million |

| Forecast Market Size (2034) | USD 251.1 Million |

| CAGR (2026-2034) | 3.27% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Product Type | Whey Protein Concentrate (48.5%, 2025) |

| Dominant Application | Sports and Performance Nutrition (62.4%, 2025) |

| Leading Region | West India (32.6%, 2025) |

India whey protein market expanded from USD 158.2 Million in 2020 to USD 185.9 Million in 2025, anchored at USD 218.4 Million in 2030, and forecast to reach USD 251.1 Million by 2034. India whey protein market is defined by its transition from a niche import-dependent supplement category consumed by competitive bodybuilders and professional athletes to a mainstream sports nutrition and functional food ingredient accessed by a rapidly growing urban fitness consumer base.

To get more information on this market, Request Sample

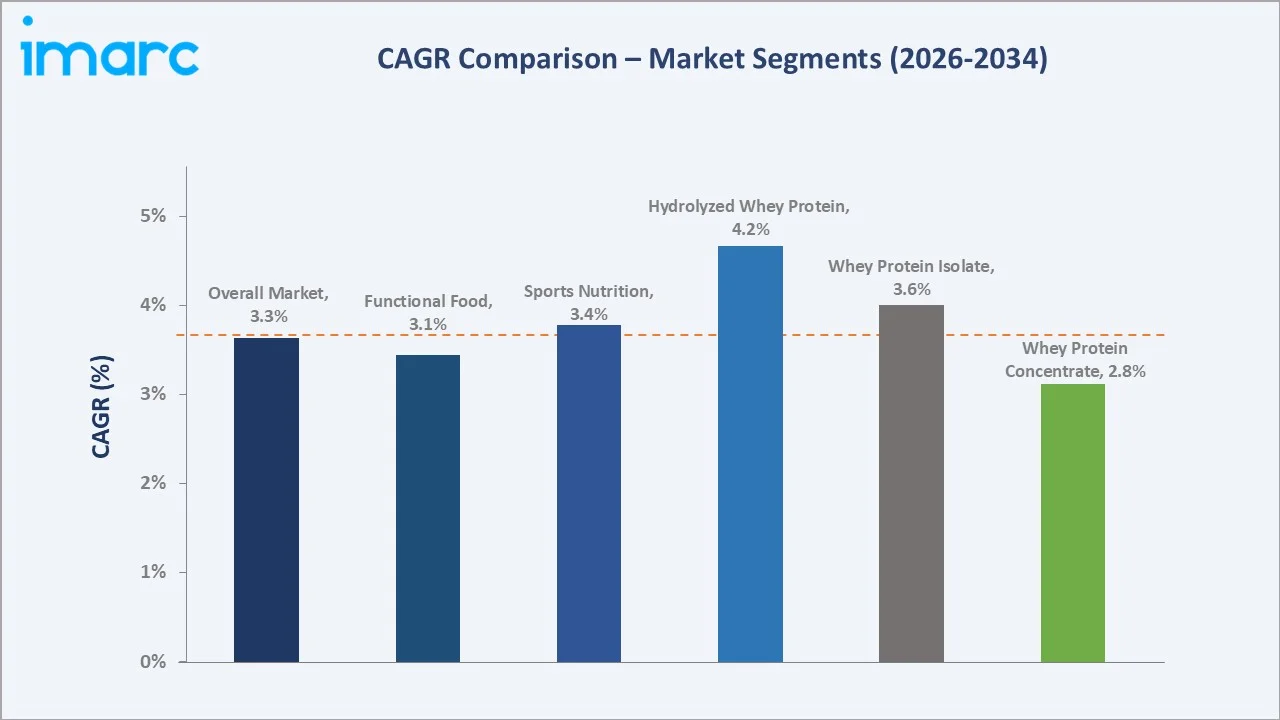

Hydrolyzed whey protein grows fastest at ~4.2% CAGR through premium clinical recovery, sports performance, and infant formula application demand. Sports and performance nutrition is growing at ~3.4% CAGR, driven by gym membership expansion and protein awareness.

Executive Summary

India whey protein market at USD 185.9 Million in 2025 represents one of Asia's most commercially dynamic sports nutrition ingredient markets, with India's combination of consumers with rapidly growing fitness culture, expanding middle class disposable income for premium nutrition, and one of the largest vegetarian populations creating the most commercially distinctive whey protein market in Asia where cultural dietary context creates both unique consumption barriers and unique consumer motivations. Whey protein is a dairy-derived protein isolate obtained as a by-product of cheese manufacturing, the liquid whey separated during cheese coagulation being filtered, pasteurized, and dried into whey protein concentrate, whey protein isolate, or hydrolyzed whey protein that provide complete amino acid profiles, making whey the most commercially valued protein supplement for muscle recovery and growth. The market is projected to reach USD 251.1 Million by 2034.

Whey protein concentrate at 48.5% leads through commercial accessibility. Sports and performance nutrition leads application at 62.4% through India's gym members, creating structured post-workout protein demand. West India leads regionally at 32.6%.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Product Type | Whey Protein Concentrate – 48.5% share (2025) |

| Dominant Application | Sports and Performance Nutrition – 62.4% market share (2025) |

| Leading Region | West India – 32.6% share (2025) |

| Market Opportunity | D2C brand growth through Amazon; domestic manufacturing; plant-protein hybrid whey; gym-chain tie-up for on-site supplement retail |

Key Analytical Observations Supporting The Above Data:

- Whey Protein Concentrate at 48.5%: The whey protein concentrate is dominant due to its lower cost, high protein content, and wider availability compared to isolates and hydrolysates. It is widely used by fitness enthusiasts and first-time supplement users, making it the preferred choice across mass-market protein products.

- Sports and Performance Nutrition at 62.4%: The sports and performance nutrition dominates owing to the growing number of gym-goers, athletes, and fitness-conscious consumers seeking protein supplementation for muscle building, recovery, and enhanced athletic performance. Rising participation in fitness activities and sports is further strengthening demand in this segment.

- West India at 32.6%: West India dominates regionally due to strong fitness culture, higher urbanization, rising disposable incomes, and the presence of major gyms, health clubs, and supplement retailers in cities such as Mumbai, Pune, and Ahmedabad.

India Whey Protein Market Overview

India whey protein market operates within the broader sports nutrition and dietary supplement industry as the most commercially dominant single product category. India whey protein market is highly import-dependent on the raw material value.

The whey protein market ecosystem integrates dairy ingredient supplier import, domestic processing and quality testing, regulatory compliance, brand marketing and D2C distribution, and multi-channel distribution. Macroeconomic factors include rising disposable incomes, rapid urbanization, an expanding middle-class population, and growing spending on health, fitness, and preventive nutrition.

Market Dynamics

To evaluate market opportunities, Request Sample

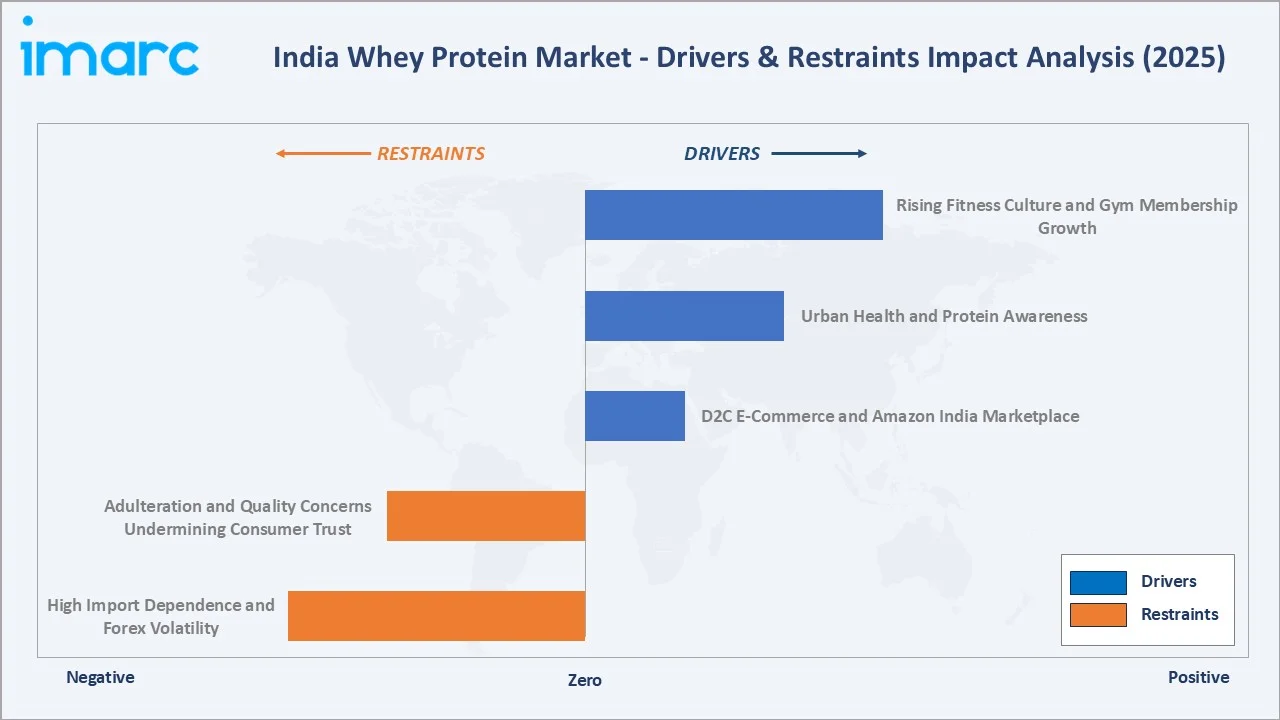

Market Drivers

- Rising Fitness Culture and Gym Membership Growth: Rising fitness culture and increasing gym memberships are boosting demand for protein-rich supplements among fitness enthusiasts. As more consumers focus on muscle building, weight management, and post-workout recovery, whey protein is becoming a preferred nutrition choice. As of 2025-2026, India had nearly 13.6 million paid gym members, and this base is projected to reach around 23.3 million by 2030, almost doubling within six years. The growing number of gyms, fitness centers, and personal training programs is further increasing product awareness and adoption across urban India.

- Urban Health and Protein Awareness: Urban health and protein awareness are driving the market as consumers increasingly recognize the importance of adequate protein intake for fitness, immunity, weight management, and overall wellness. Rising lifestyle-related health concerns, busy work schedules, and growing exposure to nutrition trends are encouraging urban consumers to adopt convenient protein supplements. As a result, whey protein is gaining popularity among working professionals, young adults, and health-conscious households.

- D2C E-Commerce and Amazon India Marketplace: D2C e-commerce and the Amazon India marketplace are making protein supplements more accessible across metro and non-metro cities. Online platforms allow brands to offer wider product ranges, discounts, subscriptions, and direct consumer engagement. Easy product comparison, reviews, and doorstep delivery are also increasing consumer trust and repeat purchases.

Market Restraints

- High Import Dependence and Forex Volatility: High import dependence is hampering the market as a large share of whey ingredients is sourced from suppliers, making prices vulnerable to international supply disruptions and freight costs. Forex volatility further increases procurement costs, forcing brands to raise product prices and limiting affordability for price-sensitive consumers.

- Adulteration and Quality Concerns Undermining Consumer Trust: Adulteration and quality concerns are reducing consumer confidence in supplement safety and authenticity. Cases of mislabeling fake products, contamination, and exaggerated protein claims make buyers cautious, especially first-time users. This pushes consumers toward only trusted or certified brands, limiting growth for smaller players and slowing wider market adoption.

Market Opportunities

- Expansion of Protein Consumption Beyond Fitness Enthusiasts to Mainstream Consumers: As working professionals, women, older adults, and health-conscious households focus on daily nutrition, immunity, weight management, and active living, whey protein demand is moving beyond gyms. This shift supports wider use in shakes, snacks, beverages, and fortified foods, helping brands target a larger mainstream consumer base.

- Development of Locally Manufactured Whey Protein Products to Reduce Import Dependence: The development of locally manufactured whey protein products reduces reliance on imported ingredients and minimizes exposure to foreign exchange fluctuations. Increased domestic production can improve supply chain stability, lower costs, and enhance product affordability. In June 2025, Nutrabay introduced India’s first gut-friendly whey protein, BioAbsorb. It is a next-generation whey protein designed to solve one of the most common yet under-addressed issues faced by protein consumers, poor absorption and digestive discomfort. It can also encourage innovation in locally tailored formulations and strengthen India's self-sufficiency in the growing sports and nutritional supplements industry.

Market Challenges

- Intense Competition from Plant-Based Proteins and Other Nutritional Supplements: Intense competition from plant-based proteins and other nutritional supplements offering consumers more alternatives for daily protein intake. Products such as soy, pea, rice, and blended plant proteins appeal to vegan, lactose-intolerant, and digestive-sensitive consumers. This puts pressure on whey protein brands to differentiate through quality, taste, pricing, clean-label claims, and functional benefits.

- Limited Protein Awareness Among a Large Section of the Population: Limited protein awareness is challenging the market, as many consumers still associate whey mainly with bodybuilders or gym users. A large section of the population remains unaware of daily protein requirements and the role of whey in general nutrition, weight management, and healthy aging. This restricts adoption beyond urban fitness-focused consumers and slows mass-market penetration.

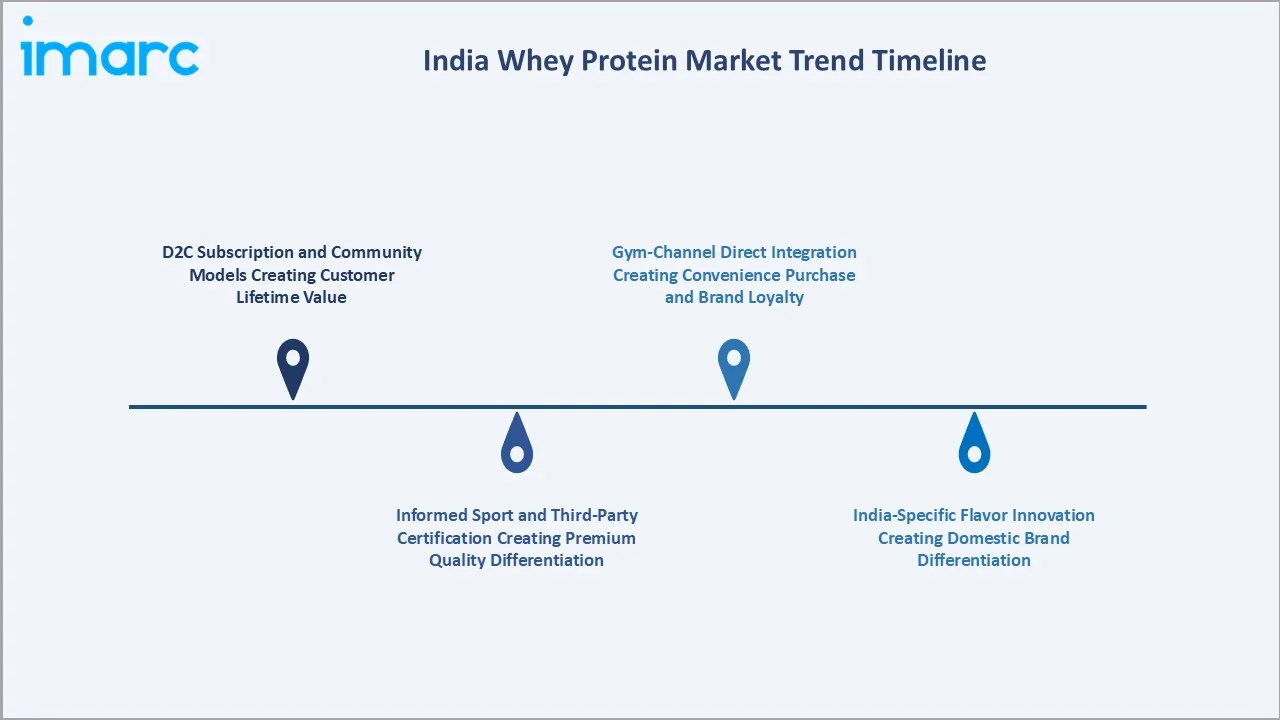

Emerging Market Trends

1. D2C Subscription and Community Models Creating Customer Lifetime Value

D2C subscription and community models enable brands to build stronger and longer-lasting relationships with consumers. Companies are offering recurring subscription plans, personalized nutrition guidance, fitness challenges, and exclusive community access to improve customer engagement and retention. These initiatives increase repeat purchases, enhance brand loyalty, and boost customer lifetime value while reducing dependence on traditional retail channels.

2. Informed Sport and Third-Party Certification Creating Premium Quality Differentiation

Informed sport and third-party certification are emerging as key quality differentiators in the India whey protein market. Certifications help brands prove product purity, accurate protein content, and the absence of banned substances or harmful adulterants. This builds consumer trust, supports premium pricing, and attracts athletes, gym users, and quality-conscious buyers seeking safer, verified supplements.

3. India-Specific Flavor Innovation Creating Domestic Brand Differentiation

India-specific flavor innovation is emerging as brands introduce flavors such as kesar badam, mango, coffee, kulfi, and masala chai. In April 2026, Wellbeing Nutrition partnered with Gaurav Gera and Mustafa Ahmed for a digital campaign promoting its whey protein blends, with Gera highlighting the mango flavor and Ahmed featuring the Swiss chocolate variant. The campaign supports India-specific flavor innovation by using familiar, taste-led positioning to make whey protein more appealing for everyday consumption and help the brand stand out in the domestic market. These localized offerings improve taste acceptance, attract first-time users, and help domestic brands differentiate from global players while building stronger consumer loyalty.

4. Gym-Channel Direct Integration Creating Convenience Purchase and Brand Loyalty

Gym-channel direct integration is emerging as brands partner with gyms, trainers, and fitness centers to promote products directly to active users. This improves convenience through on-site sampling, recommendations, and purchases, while building trust through trainer-led endorsement. It also supports repeat buying and stronger brand loyalty among regular gym-goers.

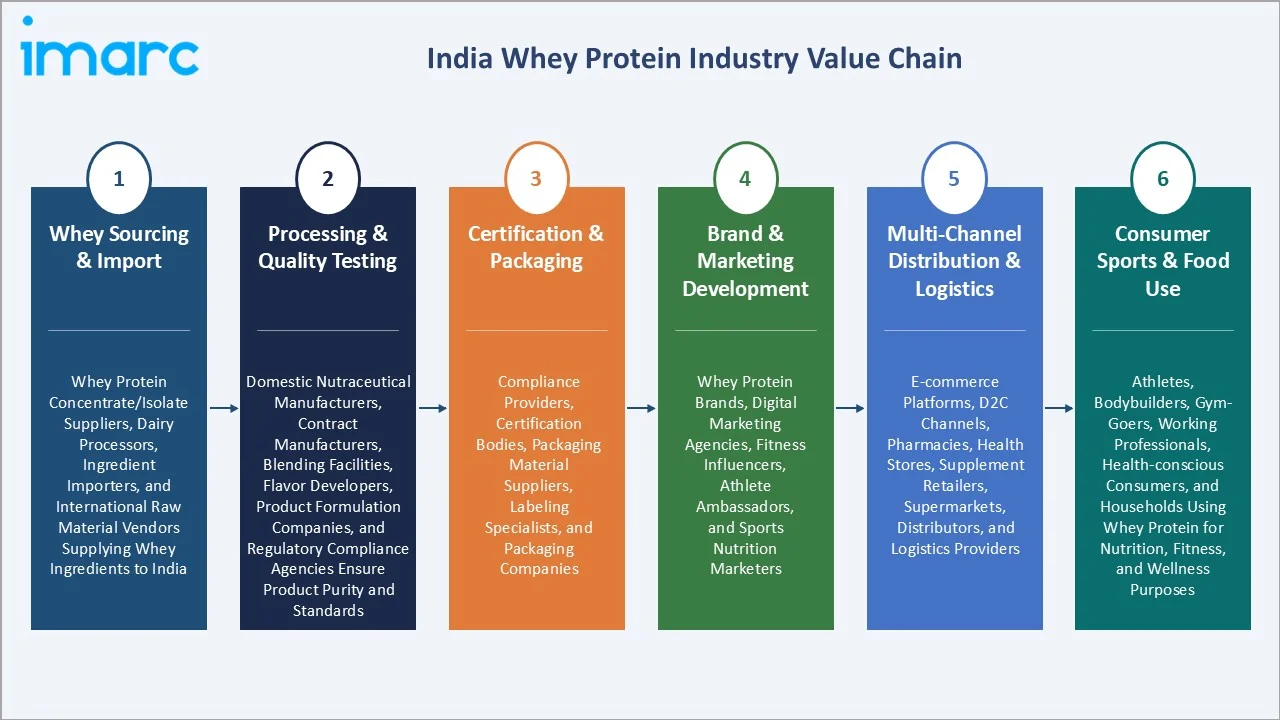

Industry Value Chain Analysis

India whey protein value chain is the most import-intensive of any major Indian dietary supplement category, finished product value entering India as either imported finished whey protein goods or imported raw material for domestic blending and packaging, creating a value chain where India's domestic commercial activity is concentrated at the brand development, quality testing, packaging, and distribution stages above primary protein processing that represents the highest raw material value-add stage of whey protein production.

| Stage | Key Participants |

|---|---|

| Whey Sourcing & Import | Whey protein concentrate/isolate suppliers, dairy processors, ingredient importers, and international raw material vendors supplying whey ingredients to India |

| Processing & Quality Testing | Domestic nutraceutical manufacturers, contract manufacturers, blending facilities, flavor developers, product formulation companies, and regulatory compliance agencies ensuring product purity and standards |

| Certification & Packaging | Compliance providers, certification bodies, packaging material suppliers, labeling specialists, and packaging companies |

| Brand & Marketing Development | Whey protein brands, digital marketing agencies, fitness influencers, athlete ambassadors, and sports nutrition marketers |

| Multi-Channel Distribution & Logistics | E-commerce platforms, D2C channels, pharmacies, health stores, supplement retailers, supermarkets, distributors, and logistics providers |

| Consumer Sports & Food Use | Athletes, bodybuilders, gym-goers, working professionals, health-conscious consumers, and households using whey protein for nutrition, fitness, and wellness purposes |

The brand development and digital marketing stage is India whey protein value chain's most commercially intensive stage. The quality testing and certification stage is the value chain's most commercially gatekeeping regulatory stage.

Technology Landscape in the India Whey Protein Industry

Advanced Flavor Masking and Formulation Technologies

Advanced flavor masking and formulation technologies are improving the taste, texture, and overall consumer experience of protein supplements. These technologies help reduce the natural bitterness of whey proteins and enable the development of localized flavors such as mango, kulfi, kesar badam, and masala chai. Enhanced formulations also improve mixability and mouthfeel, making products more appealing to mainstream consumers. As a result, brands can differentiate their offerings, increase consumer acceptance, and expand whey protein consumption beyond fitness enthusiasts.

Cold Processing Technology

Cold processing technology minimizes heat exposure during manufacturing and preserves the natural structure of proteins. This helps retain essential amino acids, bioactive compounds, and nutritional quality that can be degraded by high-temperature processing. The technology also improves protein effectiveness, digestibility, and product quality, supporting the growing demand for premium and clean-label whey protein supplements. As consumer awareness of product quality increases, manufacturers are increasingly adopting cold-processing methods to differentiate their offerings.

Enzymatic Hydrolysis Technology

Enzymatic hydrolysis technology breaks down protein molecules into smaller peptides that are easier for the body to absorb and utilize. This improves digestibility and reduces the risk of gastrointestinal discomfort, making whey protein suitable for a wider consumer base. The technology also supports the development of premium hydrolyzed whey products targeted at athletes, fitness enthusiasts, and clinical nutrition users. As demand for fast-absorbing and high-performance protein supplements grows, manufacturers are increasingly adopting enzymatic hydrolysis to enhance product value and differentiation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Whey Protein Concentrate |

48.5% |

2025 |

|

Application |

Sports and Performance Nutrition |

62.4% |

2025 |

|

Region |

West India |

32.6% |

2025 |

By Product Type

Whey protein concentrate leads at 48.5% (2025). The segment is dominant due to its lower cost and balanced nutritional profile, offering high protein content along with naturally occurring nutrients. Its affordability and widespread use among gym-goers, fitness enthusiasts, and first-time protein consumers make it the most preferred whey protein type in the country.

To access detailed market analysis, Request Sample

Whey protein isolate at 32.0% grows at ~3.6% CAGR through fitness culture premiumization and keto/low-carb diet adoption. In May 2026, Not Rocket Science launched its Protein Water, the first product of its kind in India to combine 100% whey protein isolate with a full electrolyte blend in a single, clear beverage in three flavors- Lemon Lime, Mango Orange, and Mixed Berry. Hydrolyzed whey protein at 19.5% grows fastest at ~4.2% CAGR through clinical nutrition, infant formula, and elite sports recovery demand above pure gym consumer supplement purchase.

By Application

Sports and performance nutrition leads at 62.4% (2025). India's gym members create India's most commercially significant single application market for whey protein, the post-workout recovery occasion representing the primary daily whey protein consumption event for India's fitness consumer demographic across all income segments.

Functional/fortified food at 22.0% represents India's fastest-growing B2B whey protein application, as FMCG protein enrichment creates food manufacturer ingredient procurement demand. Infant formula at 15.6% reflects pharmaceutical-grade, India's growing infant formula market, creating above-sports-supplement CAGR growth for premium hydrolyzed whey protein ingredient in infant nutrition applications.

Regional Market Insights

| Region | Share (2025) | Key India Whey Protein Market Drivers & Characteristics |

|---|---|---|

| West India | 32.6% | Driven by high urbanization, strong fitness culture, rising disposable incomes, and the presence of major metropolitan cities. |

| North India | 27.0% | Driven by growing health awareness, expanding gym memberships, and increasing participation in fitness and bodybuilding activities. |

| South India | 24.0% | Supported by a large population of health-conscious consumers, rising adoption of active lifestyles, and increasing demand for premium nutrition products. |

| East India | 16.4% | Supported by rising disposable incomes, improving fitness awareness, and increasing penetration of online supplement sales. |

West India's 32.6% market leadership reflects Mumbai's combination of one of India's highest-density premium gym infrastructure, above-national disposable income for premium nutrition, and e-commerce logistics advantage, creating above-national online whey protein purchase frequency. North India's 27.0% reflects Delhi-NCR's corporate fitness culture and Punjab's bodybuilding culture, creating complementary professional and competitive sports protein demand.

South India's 24.0% reflects Bengaluru's unique dual role as India's D2C whey protein brand innovation hub and a large health-conscious professional consumer market. East India's 16.4% is the smallest regional share but growing at above-national CAGR from a lower penetration base, as Kolkata's fitness culture development, Odisha's IT city growth, and e-commerce accessibility in East India's non-metro markets create a first-time protein supplement buyer market entry.

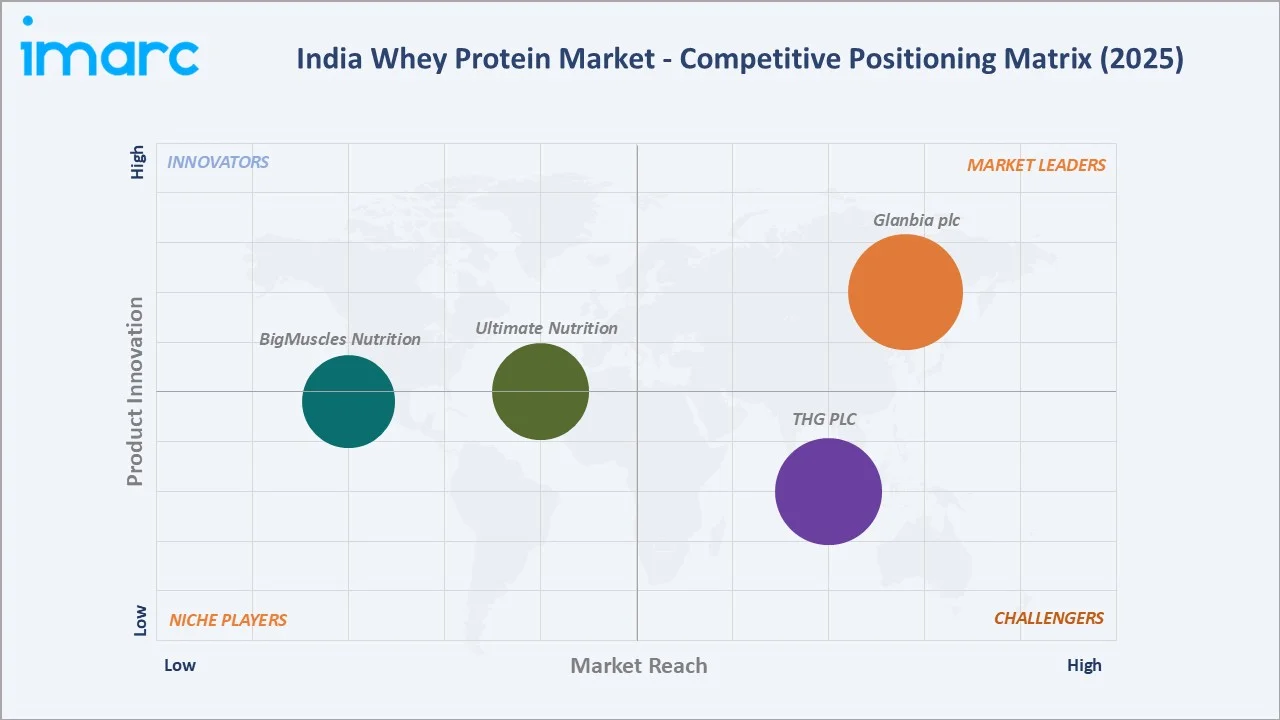

Competitive Landscape

India whey protein market competitive landscape is a commercially dynamic three-tier structure: multinational import brands, domestic D2C challengers, and economy import brands. The three-tier structure's most commercially significant dynamic is the domestic brand share capture, representing a domestic brand market share trajectory.

| Company | Key Products | Market Position | Core Strength |

|---|---|---|---|

| Glanbia plc | Optimum Nutrition (Gold Standard Whey) | Market Leader | Glanbia plc is a nutrition leader strengthening India's health and wellness sector through its subsidiary, Glanbia India Pvt. Ltd., by supplying premium whey proteins and dairy minerals. |

| THG PLC | Myprotein Impact Whey Protein, Myprotein Impact Whey Isolate, Myprotein Clear Whey Isolate | Strong Challenger | THG PLC plays a major role in India through its nutrition segment, primarily driven by Myprotein, which serves the growing demand for health, fitness, and protein supplementation directly to consumers. |

| Ultimate Nutrition | PROSTAR 100% WHEY PROTEIN | Established Player | Ultimate Nutrition is a prominent sports nutrition brand with a significant presence in India, known for providing high-quality, scientifically backed, and affordable proteins (especially Prostar 100% Whey Protein). |

| BigMuscles Nutrition | Premium Gold Whey Protein, Nitra Isolate Whey Protein, Gold Whey Isolate | Established Player | BigMuscles Nutrition is a prominent Indian sports nutrition company that offers a wide range of affordable, locally manufactured protein products. |

The competitive landscape's most commercially transformative dynamic is the integrated model. This integrated retailer-manufacturer model creates the most commercially advantaged competitive position in India whey protein market.

Key Company Profiles

Glanbia plc

Glanbia plc is a leading nutrition company, with a strong presence in the India whey protein market through its performance nutrition brand, Optimum Nutrition. The company operates across sports nutrition, lifestyle nutrition, and nutritional ingredients, serving consumers through a portfolio of recognized brands.

- Key Products: Optimum Nutrition (Gold Standard Whey)

- Strategic Focus: Strengthening its position in the India whey protein market through its flagship Optimum Nutrition (ON) brand by expanding its premium sports nutrition portfolio and increasing consumer engagement.

THG PLC

THG PLC is a consumer brands company with a strong presence in the sports nutrition industry through its flagship brand Myprotein, one of the largest online sports nutrition brands. THG operates across nutrition, health, wellness, and beauty segments, serving consumers in numerous international markets through digital-first and direct-to-consumer business models.

- Key Products: Myprotein Impact Whey Protein, Myprotein Impact Whey Isolate, Myprotein Clear Whey Isolate.

- Strategic Focus: Expanding its presence in the India whey protein market through its flagship brand Myprotein, leveraging a digital-first and direct-to-consumer (D2C) business model. The company emphasizes premium-quality whey protein products, product authenticity, and international manufacturing standards to strengthen consumer trust.

Market Concentration Analysis

India whey protein market is moderately concentrated in the premium segment and highly fragmented in the economy segment. Glanbia Plc's unique multi-brand position in India creates the most commercially concentrated single-parent company in India whey protein market, with an estimated 30-35% of India's total premium whey protein market revenue when Glanbia's India brands are aggregated. The market concentration is shifting through three mechanisms: domestic brand share capture, Glanbia's multi-brand premium consolidation, and market share fragmentation through D2C new entrant proliferation.

Investment & Growth Opportunities

Highest Growth Segments

Hydrolyzed whey protein (~4.2% CAGR through clinical nutrition and infant formula), online distribution channel (~5.5% CAGR through D2C subscription and quick commerce), infant formula application (~4.5% CAGR through India's 25 million annual births and declining breastfeeding), functional food whey fortification (~3.1% CAGR through FMCG protein enrichment), South India regional market (~4.0% CAGR through Bengaluru D2C innovation hub and above-national fitness culture), and domestic manufacturing development (structural shift from import-dependence toward India PLI-incentivized whey protein processing) represent India's highest-growth whey protein investment vectors through 2034.

Emerging Investment Opportunities

India domestic whey manufacturing opportunity represents the most commercially significant untapped value creation opportunity in India's whey protein supply chain. Exploration of whey protein manufacturing, government PLI scheme consideration for dairy protein processing, and private equity investment in Indian dairy ingredient startups collectively represent the most commercially consequential structural investment trend in India's whey protein industry that will reduce import dependence and potentially create India-origin export competitiveness by 2034.

Investment Themes

- Domestic whey protein manufacturing investment leveraging India's cheese industry liquid whey by-product stream: Building a processing facility adjacent to an established Indian cheese manufacturer creates a domestic whey protein production unit with raw material cost of INR 2-5 per litre liquid whey (cheese by-product value) versus import cost, a 40-60x raw material cost advantage that sustains domestic manufacturing economics even at below-world-scale processing investment.

- Functional food whey protein ingredient business targeting India's protein enrichment FMCG market: India's FMCG protein enrichment trend creates a B2B whey protein ingredient sales opportunity that grows independently of the sports supplement consumer market's fitness trend cyclicality. Building a B2B whey protein ingredient sales business creates a recurring institutional revenue model at high annual contract sizes that sustains above-consumer-retail business economics with below-consumer-brand marketing investment requirements.

Future Market Outlook (2026-2034)

India whey protein market is projected to grow from USD 185.9 Million in 2025 to USD 251.1 Million by 2034, delivering a 3.27% CAGR over the forecast period. The market's anchor value of USD 218.4 Million in 2030 reflects India whey protein industry at a structural maturation point. The initial rapid-growth phase transitioning toward sustainable steady-state growth anchored by replacement and upgrade purchases from India's established protein supplement consumer base, functional food application growth providing volume stability above sports supplement demand seasonality, and domestic manufacturing development reducing import cost pressure through India-origin production scale.

Three structural forces define India whey protein market growth through 2034: India's gym and fitness culture's permanent expansion creates structural demand for post-workout protein supplementation among an expanding Indian fitness consumer base, sports nutrition regulatory maturation, and India's domestic manufacturing development.

Research Methodology

Primary Research

Primary research comprised structured interviews with India whey protein industry stakeholders, including Brand Directors, E-commerce Category Managers, Founders, technical experts for Sports Nutrition Regulation implementation, and India franchise operators.

Secondary Research

Secondary research encompassed FSSAI nutraceutical/health supplement regulations and subsequent enforcement circulars; India import data protein isolates; India fitness industry data; India protein and nutrition tracking app user data summary; independent protein testing database; company annual reports; Amazon India sports nutrition category bestseller data analysis; India Sports Nutrition; India dietary supplements industry report. Over 45 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using the whey protein consumer adoption model: India urban gym member count by city tier (Tier-1, Tier-2, Tier-3) multiplied by protein supplement adoption rate by income segment multiplied by average annual whey protein spending per supplementing gym member. Functional food and infant formula applications are modelled separately using food manufacturer procurement growth rates.

India Whey Protein Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Whey Protein Concentrate, Whey Protein Isolate, Hydrolyzed Whey Protein |

| Applications Covered | Sports and Performance Nutrition, Infant Formula, Functional/Fortified Food |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Glanbia plc, THG PLC, Ultimate Nutrition, BigMuscles Nutrition, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India whey protein market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India whey protein market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India whey protein industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Whey Protein Market Report

India whey protein market reached USD 185.9 Million in 2025, driven by rising fitness awareness, growing gym memberships, and increasing consumer focus on protein-rich diets for muscle recovery, weight management, and overall wellness. Expanding e-commerce penetration, higher disposable incomes, and growing awareness of preventive healthcare are further accelerating market growth.

India whey protein market grows at 3.27% CAGR during 2026-2034, reaching USD 251.1 Million by 2034. Overall growth is sustained by India's gym membership expansion, quality market development, and domestic manufacturing investment, reducing import dependence.

Whey protein concentrate leads at 48.5% through accessible pricing, creating India's most inclusive protein supplement format serving all income segments from economy through mid-premium.

Sports and performance nutrition leads at 62.4% through India's gym members, creating structured post-workout protein demand.

West India leads at 32.6% through Mumbai's premium gym infrastructure, Maharashtra and Gujarat's above-national disposable income, and West India's e-commerce logistics advantage.

Leading companies include Glanbia plc, THG PLC, Ultimate Nutrition, and BigMuscles Nutrition, among others.

India whey protein market is projected to reach approximately USD 218.4 Million by 2030, with gym membership growth creating expanded sports nutrition demand, domestic WPC manufacturing beginning commercial scale through sports nutrition regulatory enforcement progressively eliminating quality-non-compliant economy brands, functional food whey protein application growth, and D2C brand consolidation.

India domestic whey protein manufacturing opportunity is the most commercially significant structural transformation available in India whey protein market. India's cheese manufacturing sector generates a high amount of liquid whey annually, discarded or used as animal feed at negligible value, versus the high import cost, creating a raw material cost advantage for domestic manufacturing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)