Indian Ammonia Market Size, Share, Trends and Forecast by Physical Form, End-Use, and States, 2026-2034

Indian Ammonia Market Size, Share, Trends & Forecast (2026-2034)

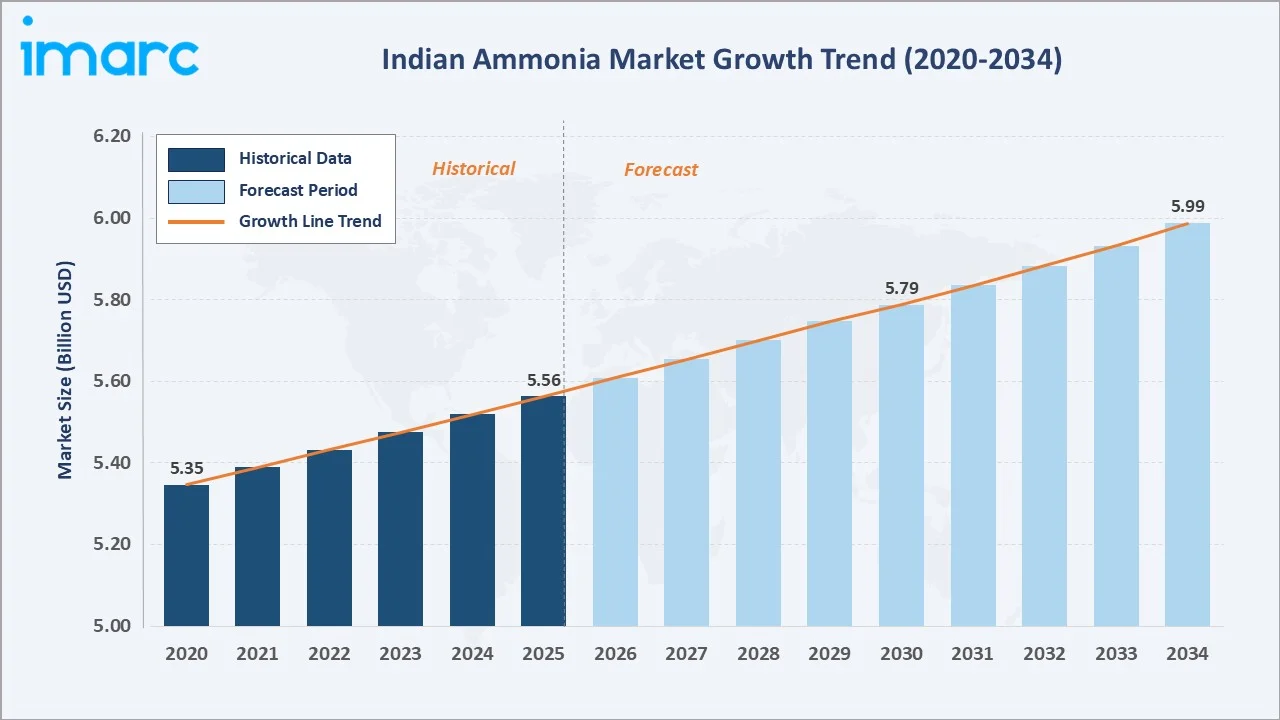

The Indian ammonia market reached USD 5.56 Billion in 2025 and is projected to reach USD 5.99 Billion by 2034. India's ammonia market reflects a mature, fertilizer-anchored industry where steady agricultural demand, government subsidy frameworks, and emerging green ammonia initiatives collectively define the market trajectory. The market is underpinned by the country's critical reliance on ammonia as the upstream feedstock for urea and complex fertilizers that sustain food security for 1.4+ billion people.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.56 Billion |

|

Forecast Market Size (2034) |

USD 5.99 Billion |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

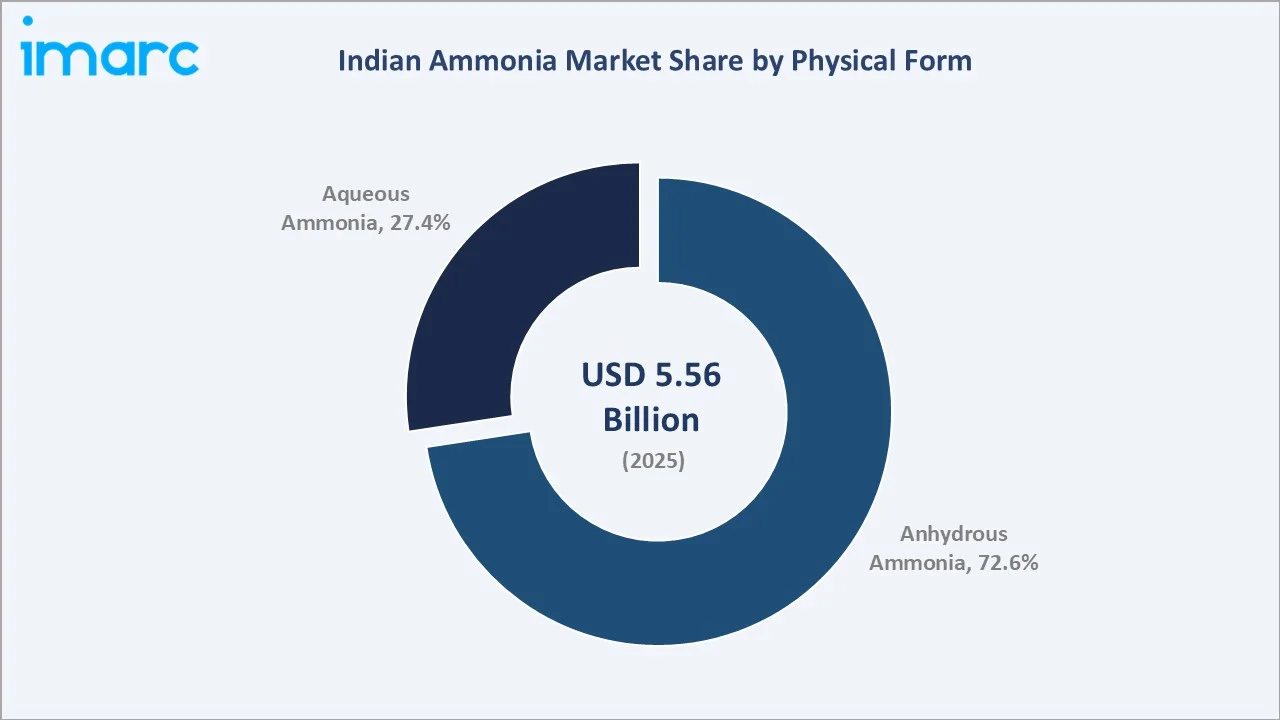

Gujarat leads state-wise with a 31.6% share in 2025, anchored by GNFC, GSFC, and IFFCO's major ammonia-fertilizer complexes. Anhydrous ammonia commands the dominant physical form segment at 72.6%, while urea leads the end-use segment at 58.9%.

To get more information on this market, Request Sample

India's ammonia market is characterized by slow but structurally stable growth, anchored by the government's Nutrient-Based Subsidy (NBS) scheme, the New Investment Policy (NIP) for urea, and India's strategic self-sufficiency targets for nitrogen fertilizer production. The growth percentage reflects a market in which volumes are near-saturation for conventional applications while green ammonia initiatives are creating incremental longer-term demand vectors.

Executive Summary

The Indian ammonia market is a large, mature commodity chemical market operating under significant government oversight through fertilizer pricing controls and urea subsidy architecture. With a USD 5.56 Billion base in 2025, the market's value trajectory reflects the combined effect of near-flat urea demand growth, government-controlled pricing that suppresses revenue expansion, and gradual industrial application uptake.

However, structural tailwinds from India's emerging green ammonia policy ambitions, the government's Production-Linked Incentive (PLI) scheme for green hydrogen and ammonia, and expanding industrial uses represent the primary growth catalysts through 2034.

Anhydrous ammonia dominates physical form with a 72.6% share, reflecting its industrial transportation and storage efficiency advantages for large-scale fertilizer production. Urea is the overwhelming end-use at 58.9%, consistent with India's position as the world's second-largest urea consumer. Gujarat leads state-level demand at 31.6%, anchored by the country's largest fertilizer industrial complex ecosystem in Bharuch, Surat, and Vadodara districts.

Key players including IFFCO, Gujarat Narmada Valley Fertilizers & Chemicals Limited, Chambal Fertilisers and Chemicals Limited, KRIBHCO, and Rashtriya Chemicals and Fertilizers Limited collectively dominate domestic ammonia production and consumption. The emergence of HHP Five Private Limited’s (subsidiary of Hygenco Green Energies Pvt Ltd) green ammonia plant in Gopalpur (construction started in June 2025) and Avaada Group's Casale-partnered facility (announced in January 2025) signals the onset of India's green ammonia transition, which will redefine market dynamics through the decade.

Key Market Insights

|

Insight |

Data |

|

Dominant Physical Form |

Anhydrous Ammonia – 72.6% share (2025) |

|

Fastest Growing Physical Form |

Aqueous Ammonia – ~1.1% CAGR (2026-2034) |

|

Largest End-Use Segment |

Urea – 58.9% share (2025) |

|

Fastest Growing End-Use |

Industrial – ~1.5% CAGR (2026-2034) |

|

Leading State |

Gujarat – 31.6% share (2025) |

|

Key Players |

IFFCO, Gujarat Narmada Valley Fertilizers & Chemicals Limited, Chambal Fertilisers and Chemicals Limited, KRIBHCO, and Rashtriya Chemicals and Fertilizers Limited |

Key Analytical Observations Supporting the Above Data:

- Anhydrous ammonia at 72.6% (2025) reflects its role as the primary industrial-grade form used in urea and ammonium phosphate manufacturing. India's large-scale fertilizer plants, including IFFCO's Phulpur and Aonla complexes, and GNFC's Bharuch facility, operate on anhydrous ammonia feedstocks requiring pipeline and pressurized cylinder logistics.

- Urea end-use at 58.9% (2025) reflects India's structurally high urea dependency, with domestic urea consumption exceeding 35-36 million tons annually. The government's neem-coating mandate and the MRP cap on urea at INR 5,360/ton ensure near-inelastic demand, anchoring ammonia consumption in this segment.

- Industrial end-use growing at ~1.5% CAGR: represents the fastest-expanding application segment, driven by rising demand for ammonia in HVAC refrigeration, mining explosives (ammonium nitrate), textiles, and pharmaceuticals as India's manufacturing sector expands under Make in India.

- Gujarat's 31.6% share (2025) reflects the state's dominant position hosting GNFC's Bharuch plant (the largest single-location ammonia producer in India), GSFC's Vadodara complex, and IFFCO's Kalol unit, making the Narmada-Surat chemical corridor the nucleus of India's ammonia industry.

Indian Ammonia Market Overview

Ammonia (NH3) is an inorganic binary hydride characterized by a distinctive pungent odor, high water solubility, and a colorless form. Produced commercially via the Haber-Bosch process combining atmospheric nitrogen and hydrogen feedstock under high pressure and temperature using iron catalysts, ammonia is the foundational nitrogen compound for India's INR 1,021.3 Billion fertilizer industry (2025). The Indian ammonia market encompasses conventional grey ammonia (from natural gas/naphtha feedstock), blue ammonia (with carbon capture), and emerging green ammonia (from electrolyzed hydrogen using renewable energy).

India imports approximately 20-25% of its ammonia requirements, primarily from Arabian Gulf countries. The government's New Investment Policy (NIP) 2012 and Urea Manufacturing Policy 2015 provide capital and feedstock cost protection to incentivize domestic capacity expansion. The fertilizer subsidy for FY26 is expected to remain broadly in line with FY25, at around ₹1.7 trillion. This continued support is expected to help keep fertilizer prices affordable for farmers and sustain agricultural input demand.

Market Dynamics

To evaluate market opportunities, Request Sample

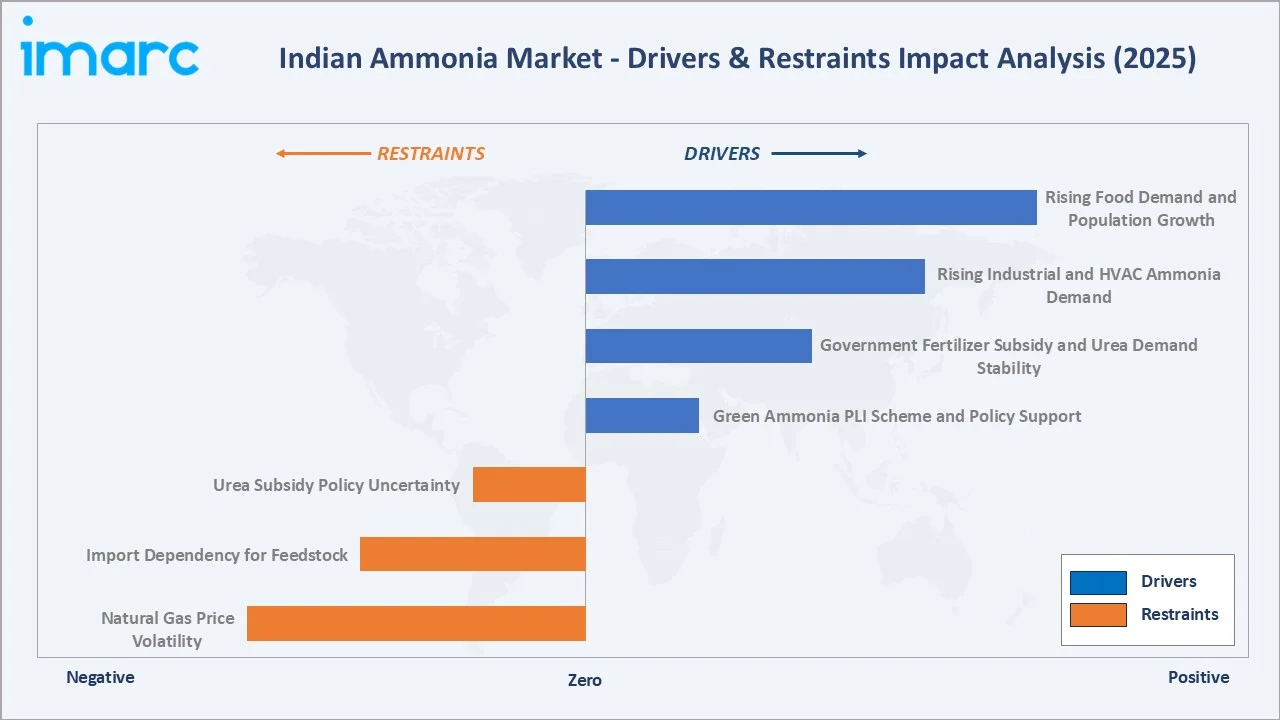

Market Drivers

- Green Ammonia PLI Scheme and Policy Support: The Ministry of Finance is considering a proposal to launch a viability gap funding (VGF) scheme to support green ammonia production of 2 million tons by FY2025–26. The Ministry of New and Renewable Energy (MNRE), along with industry stakeholders, has sought INR 10,000 crore in VGF support from the finance ministry to accelerate green ammonia production.

- Government Fertilizer Subsidy and Urea Demand Stability: The government's INR 1.22 trillion urea subsidy allocation in FY2024–25 ensures near-inelastic urea demand at farmer-affordable prices. With 135+ million farm households dependent on subsidized urea, ammonia feedstock demand for domestic urea production is structurally protected from demand volatility.

- Rising Industrial and HVAC Ammonia Demand: India's manufacturing sector expansion under Make in India, growth in cold chain logistics requiring ammonia refrigeration, and increasing ammonium nitrate demand from the mining and construction sectors are creating incremental industrial ammonia demand growing at ~1.5% CAGR.

- Rising Food Demand and Population Growth: India's population of 1.44 billion, growing at ~0.5% annually, sustains structural demand for food production and consequently for nitrogen fertilizers. India's per-hectare fertilizer consumption remains below global averages, providing long-term headroom for incremental demand growth.

Market Restraints

- Natural Gas Price Volatility: Natural gas constitutes 70–90% of ammonia production costs. India's dependency on LNG imports (sourced at USD 8–20/MMBtu spot prices) creates cost volatility that squeezes margins for domestic producers operating under regulated urea MRP constraints.

- Import Dependency for Feedstock: India's domestic natural gas production covers only 70-80% of urea demand. GAIL and CGD pipelines serve major ammonia plants, but geographic concentration of gas infrastructure excludes potential new plant sites in eastern and central India.

- Urea Subsidy Policy Uncertainty: The government's annual subsidy allocation fluctuations (INR 1.95 trillion revised to INR 1.64 trillion in FY2024–25) create investment planning uncertainty for ammonia producers whose economics are directly linked to government-determined urea pricing frameworks.

Market Opportunities

- Green Ammonia Export Potential: India targets 10% of global renewable hydrogen trade by 2030. Japan, South Korea, Germany, and the Netherlands have signed green ammonia import agreements with Indian producers. This export opportunity could add 2–3 million tons of incremental ammonia production capacity by 2034.

- Carbon-Neutral Ammonia for Industrial Decarbonization: India's 2070 net-zero commitment is compelling industrial consumers of ammonia to transition to green or blue variants. The shipping, steel, and power sectors are emerging as future ammonia consumers under their decarbonization roadmaps, creating a structural growth vector beyond conventional fertilizer applications.

Market Challenges

- Ammonia Safety and Infrastructure Constraints: Anhydrous ammonia is a Category 1 toxic gas requiring specialized pressurized storage, pipeline infrastructure, and certified handling personnel. India's limited ammonia pipeline network constrains supply chain efficiency, particularly for new plants outside Gujarat and Uttar Pradesh industrial corridors.

- Green Ammonia Cost Competitiveness Gap: Estimates indicate that green ammonia can cost anywhere from 10% more to over twice as much as grey ammonia, and in some cases, up to six times higher, depending on the underlying assumptions. Without significant renewable energy cost reductions and electrolyzer scale-up, green ammonia will require sustained government viability gap funding through 2034 to achieve commercial parity.

Emerging Market Trends

1. Green Ammonia Production Facility Commissioning

In June 2025, Hygenco Green Energies Pvt Ltd started construction of a green ammonia production facility at Gopalpur Industrial Park in Odisha, with plans to scale to 1.1 million tons annual capacity. This marks one of India's first commercial-scale green ammonia plants, powered by renewable energy, and signals the beginning of India's green ammonia production infrastructure buildout.

2. Strategic Partnership for India's Largest Green Ammonia Plant

In January 2025, Avaada Group entered a strategic partnership with Casale (a Swiss ammonia technology leader) to establish India's largest green ammonia production facility in Gopalpur, Odisha, with a planned capacity of 1,500 tons per day operating entirely on renewable energy. This facility will incorporate Casale's cutting-edge technologies to enable a fully carbon-neutral production process, representing a landmark in India's energy transition.

3. Government PLI and Viability Gap Funding for Green Ammonia

India's INR 10,000 Crore viability gap funding (VGF) for green ammonia is catalyzing investment from ACME Solar, Greenko, ReNew Power, and Torrent Power into green ammonia production projects targeting 2 million tons of capacity by 2025–26. The policy creates a bridge between current green ammonia economics and commercial viability, while positioning India as a global green ammonia exporter.

4. Energy Efficiency Modernization of Legacy Ammonia Plants

India's Amended Urea Policy (AUP) and Energy Audit programs under the Department of Fertilizers are compelling older plants to modernize to energy consumption benchmarks of 6.5–7.5 Gcal/MT ammonia from current averages of 8–10 Gcal/MT. RCFL's Trombay plant and SPIC's Tuticorin facility are undergoing revamp programs that will reduce both production costs and carbon footprint while maintaining domestic supply stability.

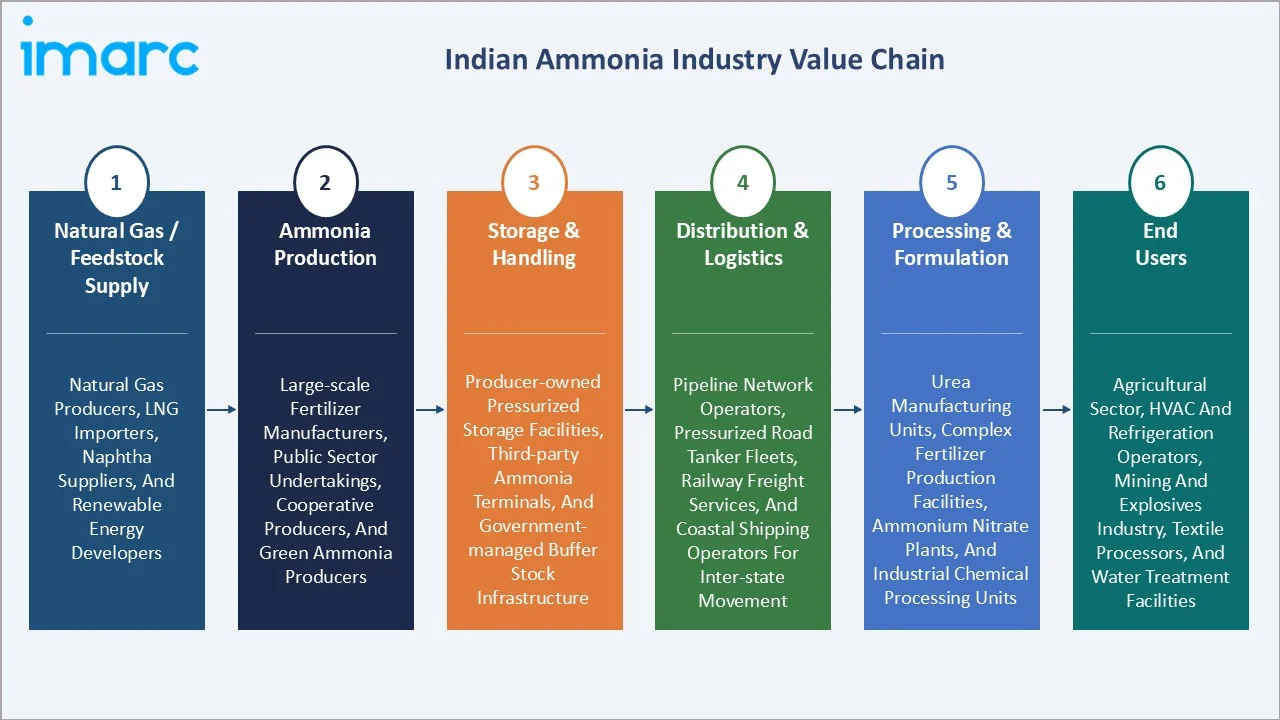

Industry Value Chain Analysis

India's ammonia value chain spans natural gas and naphtha feedstock supply through end-user fertilizer and industrial application, with government policy intervening at multiple stages through pricing regulation, subsidy disbursement, and environmental compliance mandates.

|

Stage |

Key Players / Examples |

|

Natural Gas / Feedstock Supply |

Natural gas producers, LNG importers, naphtha suppliers, and renewable energy developers |

|

Ammonia Production |

Large-scale fertilizer manufacturers, public sector undertakings, cooperative producers, and emerging green ammonia producers |

|

Storage & Handling |

Producer-owned pressurized storage facilities, third-party ammonia terminals, and government-managed buffer stock infrastructure |

|

Distribution & Logistics |

Pipeline network operators, pressurized road tanker fleets, railway freight services, and coastal shipping operators for inter-state movement |

|

Processing & Formulation |

Urea manufacturing units, complex fertilizer production facilities, ammonium nitrate plants, and industrial chemical processing units |

|

End Users |

Agricultural sector, HVAC and refrigeration operators, mining and explosives industry, textile processors, and water treatment facilities |

Technology Landscape in the Indian Ammonia Industry

Conventional Haber-Bosch Ammonia Production

The majority of operating ammonia plants in India use the Haber-Bosch process, predominantly with natural gas feedstock. Technip Energies, KBR, and Topsoe are the primary technology licensors. The average energy consumption of Indian ammonia plants is 8–9.5 Gcal/MT, creating both a competitiveness gap and a modernization opportunity.

Green Ammonia via Electrolysis and Renewable Energy

Green ammonia uses electrolyzed hydrogen from renewable energy sources combined with air-separated nitrogen through the Haber-Bosch synthesis loop. Casale's ammonia synthesis technology, combined with 24/7 renewable power from solar and wind, is the dominant technology pathway adopted by Indian green ammonia developers including Avaada, Hygenco Green Energies Pvt Ltd, and ACME.

Aqueous Ammonia for Industrial Applications

Aqueous ammonia (ammonium hydroxide solution, 25–30% concentration) is used in industrial applications including textile processing, selective catalytic reduction (SCR) for NOx removal in power plants, and semiconductor manufacturing. India's growing thermal power fleet (226.23 GW coal-based capacity) with SCR retrofits for NOx compliance, and the expanding textile industry in Gujarat and Tamil Nadu, are driving the aqueous ammonia segment's relatively faster 1.1% CAGR.

Blue Ammonia with Carbon Capture and Utilization

Blue ammonia, produced through Haber-Bosch with integrated carbon capture and storage (CCS), represents India's intermediate transition pathway between grey and green ammonia. NTPC and ONGC are evaluating blue ammonia production at existing gas-based ammonia plants, leveraging India's geological CO2 sequestration capacity. This technology pathway could extend the economic life of existing ammonia assets through 2034–2040 while meeting decarbonization commitments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Physical Form |

Anhydrous Ammonia |

72.6% |

2025 |

|

End-Use |

Urea |

58.9% |

2025 |

|

States |

Gujarat |

31.6% |

2025 |

By Physical Form

Anhydrous ammonia dominates the physical form segment with a 72.6% share in 2025. This reflects its role as the standard industrial grade for large-scale fertilizer production; it is transported and stored as a pressurized liquid at -33°C or under pressure at ambient temperature, offering the highest nitrogen content per ton of any nitrogen compound.

To access detailed market analysis, Request Sample

Aqueous ammonia at 27.4% serves industrial applications requiring diluted ammonia solutions, including textile processing, water treatment, cleaning products, and SCR NOx reduction systems. Growing at ~1.1% CAGR, this segment benefits from India's industrial expansion and increasing environmental compliance mandates for power plants requiring NOx abatement.

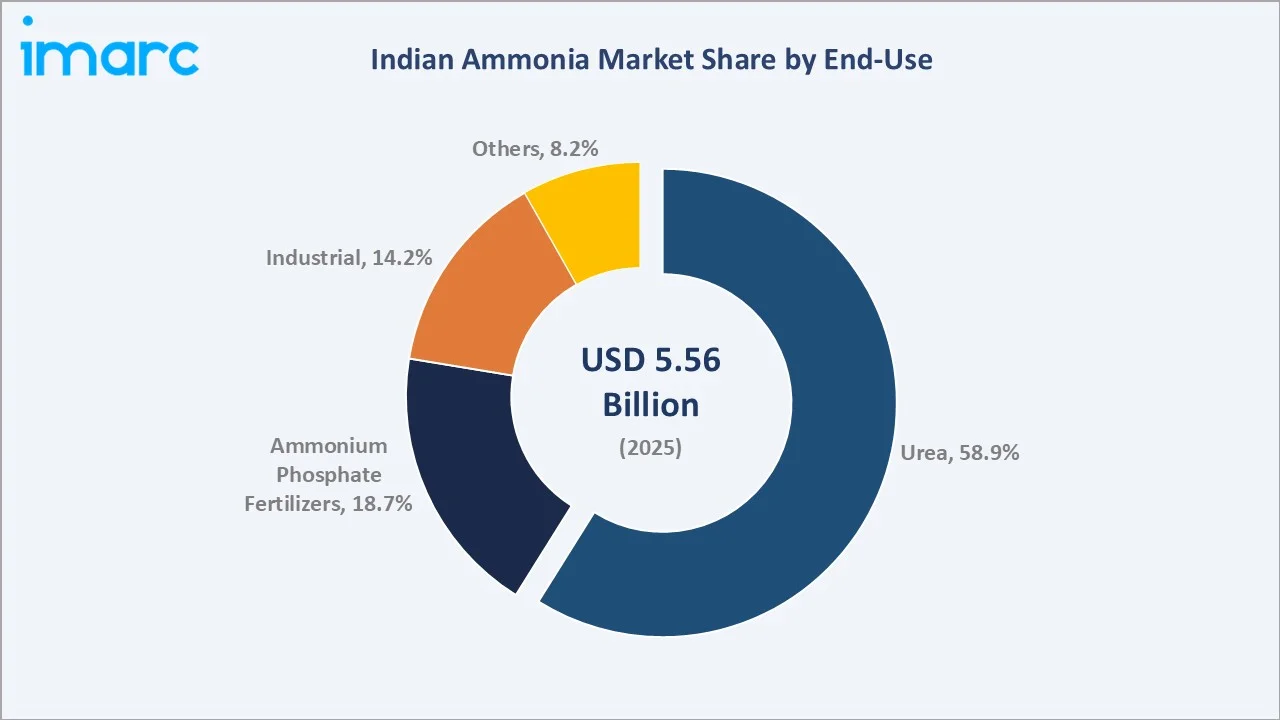

By End-Use

Urea leads the end-use segment with a 58.9% share in 2025, reflecting India's structural reliance on urea as the primary nitrogen fertilizer. In 2023–24, India achieved its highest-ever domestic urea production, surpassing 314 lakh metric tons (LMT), and consumes the majority of domestic ammonia output. The government's MRP cap and neem-coating mandates ensure near-inelastic urea demand, anchoring ammonia consumption in this segment through 2034.

Ammonium phosphate fertilizers at 18.7% represent the second-largest end-use, concentrated in Gujarat and Maharashtra's integrated fertilizer complexes. The industrial segment at 14.2% is the fastest-growing at ~1.5% CAGR, driven by HVAC refrigeration, ammonium nitrate for mining, textile effluent treatment, and pharmaceutical intermediates.

Regional Market Insights

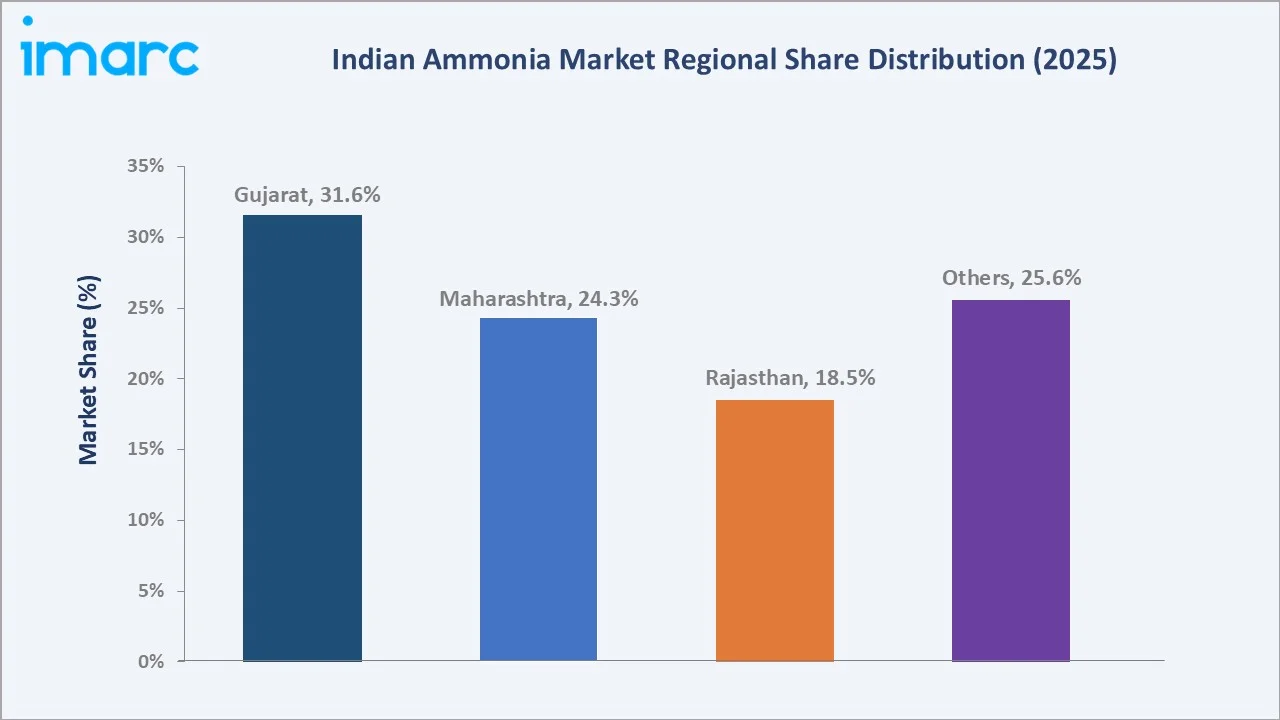

Gujarat's leadership at 31.6% in 2025 reflects the state's unrivalled concentration of ammonia production and consumption infrastructure. The Bharuch-Ankleshwar chemical corridor hosts GNFC's large-scale ammonia plant, GSFC's Vadodara complex, and IFFCO's Kalol unit, collectively accounting for approximately 35% of India's domestic ammonia production capacity. Gujarat's well-developed pipeline and storage infrastructure further consolidates its position.

|

State |

Share (2025) |

Key Growth Drivers |

|

Gujarat |

31.6% |

Dominant fertilizer industrial complex; strong pipeline infrastructure; chemical manufacturing demand |

|

Maharashtra |

24.3% |

Industrial ammonia demand from textiles and chemicals; growing cold chain refrigeration sector |

|

Rajasthan |

18.5% |

Expanding ammonia demand from mining (ammonium nitrate) and growing industrial base |

|

Others |

25.6% |

Distributed demand across Uttar Pradesh, Andhra Pradesh, Tamil Nadu |

Maharashtra at 24.3% is driven by RCFL's Trombay and Thal plants serving Mumbai's industrial and port ammonia demand, and the state's large industrial base consuming ammonia for refrigeration, water treatment, and chemical processing. Rajasthan at 18.5% is dominated by Chambal Fertilisers' Gadepan I, II & III, which together represent the largest private-sector urea manufacturing capacity in India.

Competitive Landscape

India's ammonia production market is moderately concentrated among government-supported cooperatives and public sector enterprises, with private sector participation through Chambal Fertilisers and Chemicals Limited. The top five producers (IFFCO, Gujarat Narmada Valley Fertilizers & Chemicals Limited, Chambal Fertilisers and Chemicals Limited, KRIBHCO, and Rashtriya Chemicals and Fertilizers Limited), collectively account for approximately 65–70% of domestic ammonia production capacity.

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

IFFCO |

IFFCO |

Market Leader |

Largest cooperative, multi-plant ammonia-urea complex; Phulpur, Aonla, Kalol facilities |

|

Gujarat Narmada Valley Fertilizers & Chemicals Limited |

GNFC |

Strong Challenger |

Bharuch plant, India's largest single-location ammonia producer; integrated chemicals and IT diversification |

|

Chambal Fertilisers and Chemicals Limited |

Uttam |

Strong Challenger |

Largest private urea producer; Gadepan I, II & III; strong rural distribution network |

|

KRIBHCO |

KRIBHCO |

Challenger |

Hazira, Gujarat, and Shahjahanpur, UP plants; cooperative model serving various primary cooperative societies |

|

Rashtriya Chemicals and Fertilizers Limited |

RCF |

Challenger |

Trombay (Mumbai) and Thal (Raigad) plants; diversified into specialty fertilizers and industrial chemicals |

Key Company Profiles

IFFCO

IFFCO, headquartered in New Delhi, is the world's largest fertilizer cooperative and India's largest ammonia producer. Operating through five ammonia-urea complexes at Phulpur (Uttar Pradesh), Aonla (Uttar Pradesh), Kalol (Gujarat), Kandla (Gujarat), and Paradeep (Odisha).

- Product Portfolio: Ammonia (anhydrous), urea, NPK complex fertilizers, nano-urea, nano-DAP, and agricultural input solutions.

- Recent Developments: In April 2024, IFFCO signed an MoU with ACME to purchase about 200,000 tons of green ammonia produced through renewable energy at ACME’s Gopalpur, Odisha facility. The ammonia will be used at IFFCO’s Paradeep and Kandla units to manufacture complex fertilizers, supporting India’s shift toward lower-carbon fertilizer production.

- Strategic Focus: Green ammonia integration; nano-fertilizer market development; cooperative supply chain digitalization; export of surplus ammonia and urea to Southeast Asia and Africa.

Gujarat Narmada Valley Fertilizers & Chemicals Limited

Gujarat Narmada Valley Fertilizers & Chemicals Limited, headquartered in Bharuch, Gujarat, is a joint venture of the Government of Gujarat and GSFC, operating India's one of the largest single-location ammonia plants at the Narmada Nagar complex. GNFC has diversified into industrial chemicals, TDI (toluene di-isocyanate), and IT services.

- Product Portfolio: Anhydrous ammonia, urea, ammonium nitrate solution (ANS), methanol, weak nitric acid, formic acid, and acetic acid.

- Recent Developments: In December 2025, GNFC awarded a INR 360 crore LEPC contract to Toyo Engineering India to install a new 480 MTPD / 163,200 MTPA Ammonium Nitrate-II plant. The project will use INCRO, Spain’s process technology and licensing, helping GNFC expand its ammonium nitrate production capacity by around 94%.

- Strategic Focus: Energy efficiency benchmarking; TDI and specialty chemical value-addition; blue ammonia feasibility; export-oriented ammonia production through Dahej port proximity.

Market Concentration Analysis

India's ammonia production market is moderately concentrated, with government-owned and cooperative enterprises dominating capacity. Public sector entities (IFFCO, Gujarat Narmada Valley Fertilizers & Chemicals Limited, KRIBHCO, and Rashtriya Chemicals and Fertilizers Limited) collectively control approximately 60–65% of domestic ammonia production capacity, with private sector participation through Chambal Fertilisers and Chemicals Limited(15%) providing limited competitive counterweight.

The growth percentage reflects a structurally stable but price-regulated market where competition occurs primarily on production efficiency, feedstock cost management, and government contract pricing rather than market-based competition. Green ammonia entrants including Hygenco Green Energies Pvt Ltd, Avaada, ACME, and Greenko will represent a distinct competitive tier by 2030–2034, potentially disrupting the existing market structure if green ammonia achieves cost competitiveness.

Investment & Growth Opportunities

Green Ammonia Export Market

India's renewable energy cost advantage positions it as a future globally competitive green ammonia producer. Japan, Germany, and South Korea have signed green ammonia offtake agreements with Indian developers. The export opportunity could mobilize USD 5–10 billion in capital investment in green ammonia production infrastructure by 2030.

Industrial Ammonia Diversification

Industrial applications (HVAC, ammonium nitrate for mining, pharmaceuticals, electronics) represent the fastest-growing ammonia end-use at ~1.5% CAGR, creating opportunities for smaller, decentralized aqueous ammonia production facilities serving industrial parks in Maharashtra, Tamil Nadu, and Karnataka without the logistical constraints of anhydrous ammonia transport.

Venture and Institutional Investment Trends

- India's INR 10,000 Crore viability gap funding scheme for green ammonia is catalyzing USD 2–3 Billion in private investment commitments from Avaada, ACME, Hygenco Green Energies Pvt Ltd, Greenko, and ReNew Power through 2026.

- Casale, Topsoe, Nel Hydrogen, and Siemens Energy are partnering with Indian developers to localize green ammonia technology, creating an ecosystem of electrolyzer manufacturing and ammonia synthesis technology supply that will support long-term cost reduction.

- World Bank and Asian Development Bank concessional financing for India's green hydrogen and ammonia transition is expected to provide USD 500+ Million in capital subsidy through multilateral green infrastructure lending programs through 2034.

Future Market Outlook (2026-2034)

India's ammonia market is expected to grow steadily from USD 5.56 Billion in 2025 to USD 5.99 Billion by 2034. This trajectory reflects a two-speed market: conventional grey ammonia consumption will remain near-flat as urea demand growth is modest and fertilizer pricing is government-controlled, while green ammonia production is expected to grow from a negligible base to approximately 1–2 million tons by 2034, adding incremental market value not fully captured in current forecasts.

The technology transition from grey to green and blue ammonia will be the defining structural shift through 2034. India's achievement of 5 million tons of green hydrogen by 2030 (which feeds directly into green ammonia synthesis) will be the key milestone determining whether India meets its green ammonia export ambitions and whether domestic industrial consumers of ammonia can access cost-competitive low-carbon alternatives.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including ammonia plant operators, Department of Fertilizers officials, natural gas suppliers (GAIL, GSPC), industrial ammonia consumers, and green ammonia technology developers across Gujarat, Maharashtra, Rajasthan, and Andhra Pradesh.

Secondary Research

Secondary research encompassed company annual reports, Department of Fertilizers' Annual Reports, FAI (Fertiliser Association of India) production data, GAIL gas allocation data, Ministry of Petroleum & Natural Gas statistics, Petroleum Planning and Analysis Cell (PPAC) LNG import data, and industry publications.

Forecasting Models

Market size estimations were derived using bottom-up forecasting incorporating plant-level production capacity, per-unit ammonia price trajectories (USD/ton), capacity utilization rates, and government pricing frameworks. A base-case growth percentage reflects the structural maturity of conventional ammonia demand validated against government subsidy allocation trends and demographic-driven food demand projections.

Indian Ammonia Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD, Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Physical Forms Covered | Anhydrous Ammonia, Aqueous Ammonia |

| End-Uses Covered | Urea, Ammonium Phosphate Fertilizers, Industrial, Others |

| States Covered | Gujarat, Maharashtra, Rajasthan, Others |

| Companies Covered | Chambal Fertilizers and Chemicals Ltd., GNFC (Gujarat Narmada Valley Fertilizers and Chemicals), IFFCO (Indian Farmers Fertilizer Cooperative Limited), KRIBHCO (Krishak Bharati Cooperative Limited), NFCL (Nagarjuna Fertilizers and Chemicals Limited), RCFL (Rashtriya Chemicals and Fertilizers Ltd) and Southern Petrochemicals Industries Limited (SPIC) |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Ammonia Market Report

The Indian ammonia market reached USD 5.56 Billion in 2025 and is projected to reach USD 5.99 Billion by 2034.

Anhydrous ammonia leads with a 72.6% share in 2025, reflecting its dominant use in large-scale urea and ammonium phosphate fertilizer production.

Urea leads the end-use segment with a 58.9% market share in 2025, anchored by India's structural dependency on urea as the primary nitrogen fertilizer under a government-administered subsidy and pricing framework.

Gujarat leads with a 31.6% state-wise share in 2025, driven by GNFC's Bharuch plant, GSFC's Vadodara complex, and IFFCO's Kalol unit concentrated in the Narmada-Surat chemical corridor.

The leading companies are IFFCO, Gujarat Narmada Valley Fertilizers & Chemicals Limited, Chambal Fertilisers and Chemicals Limited, KRIBHCO, and Rashtriya Chemicals and Fertilizers Limited, collectively dominating approximately 65–70% of domestic production capacity.

Green ammonia production for export (driven by PLI scheme and renewable energy cost advantages), industrial ammonia diversification, and plant modernization under the Amended Urea Policy represent the primary growth and investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)