India Cold Chain Market Size, Share, Trends and Forecast by Segment, Product, Sector, Organised and Unorganised, and States, 2026-2034

India Cold Chain Market Size, Share, Trends & Forecast (2026-2034)

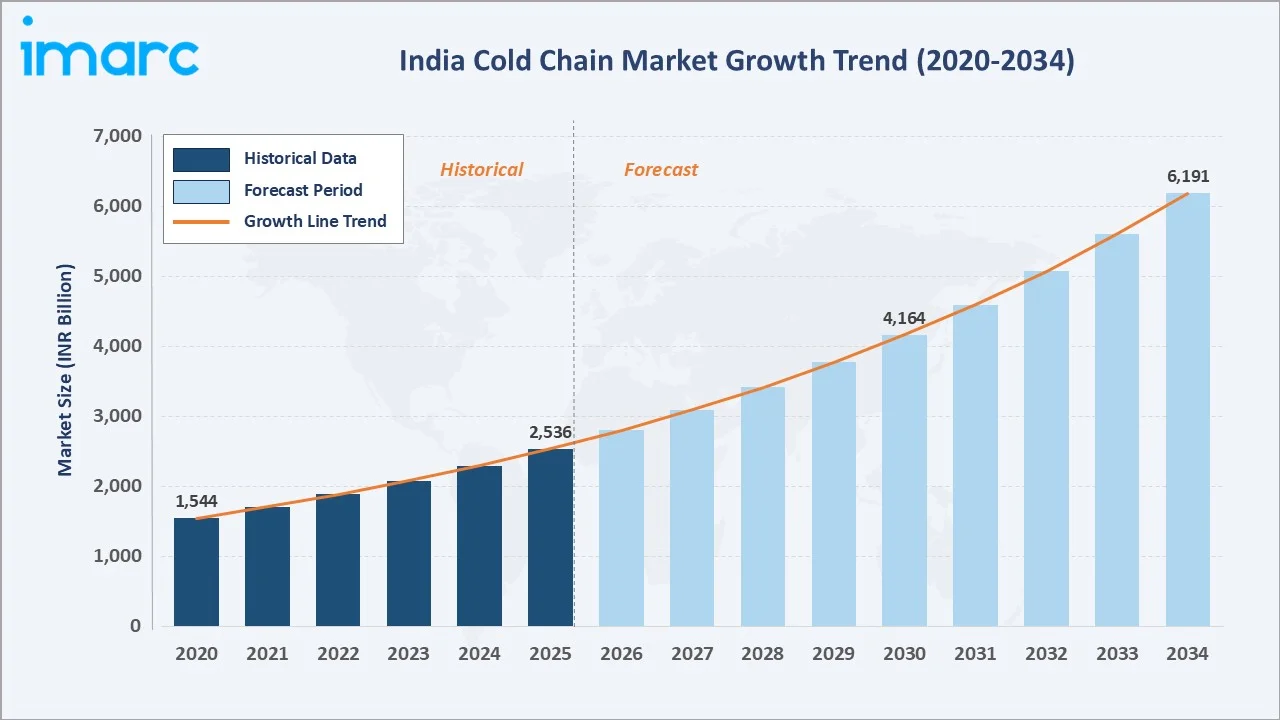

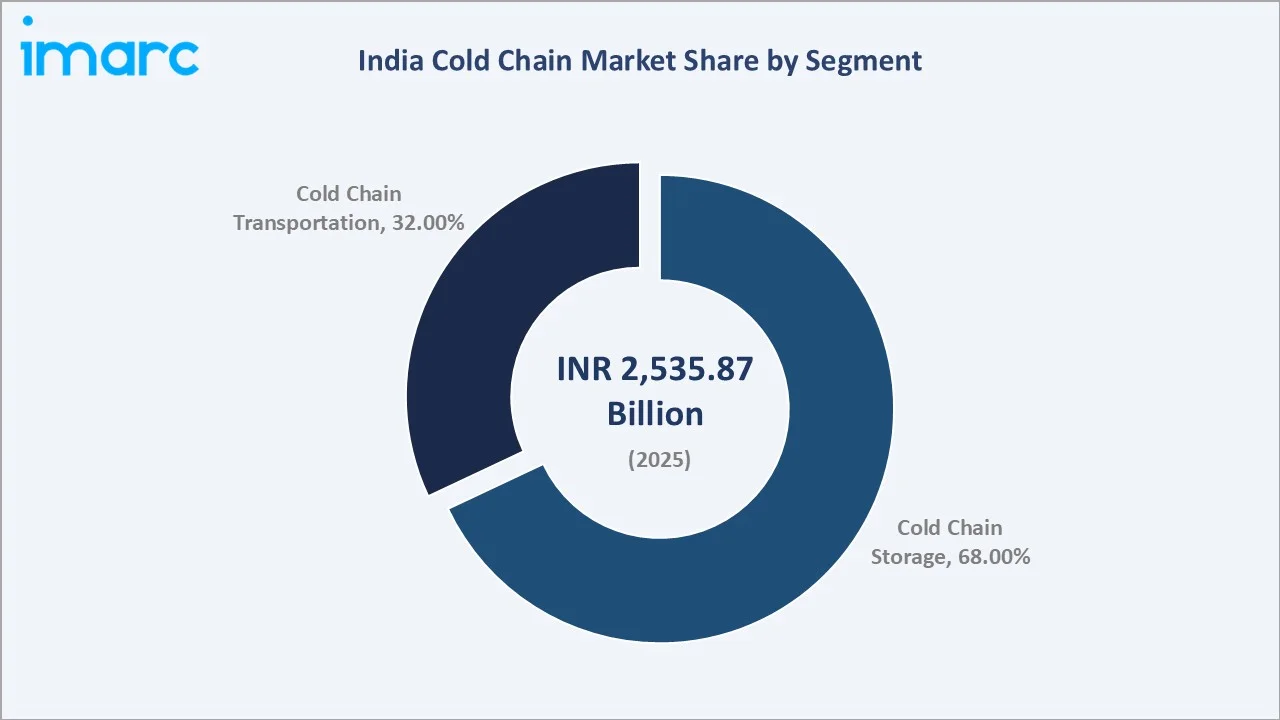

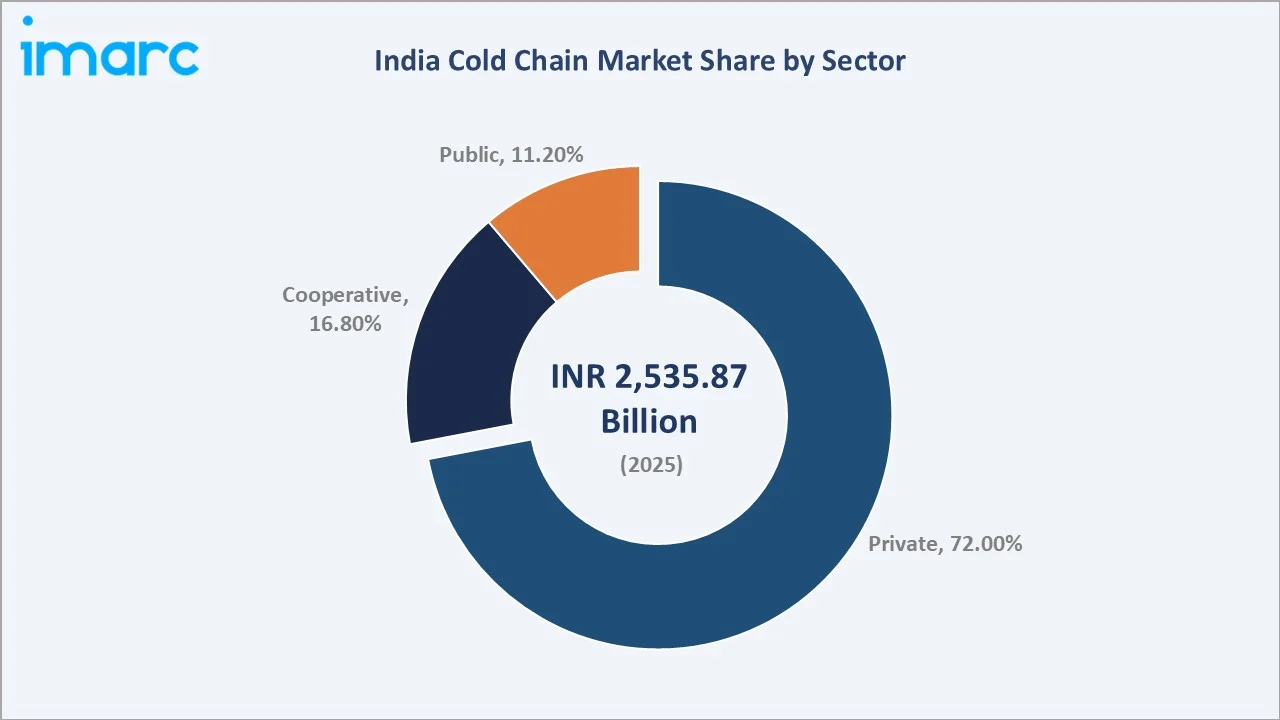

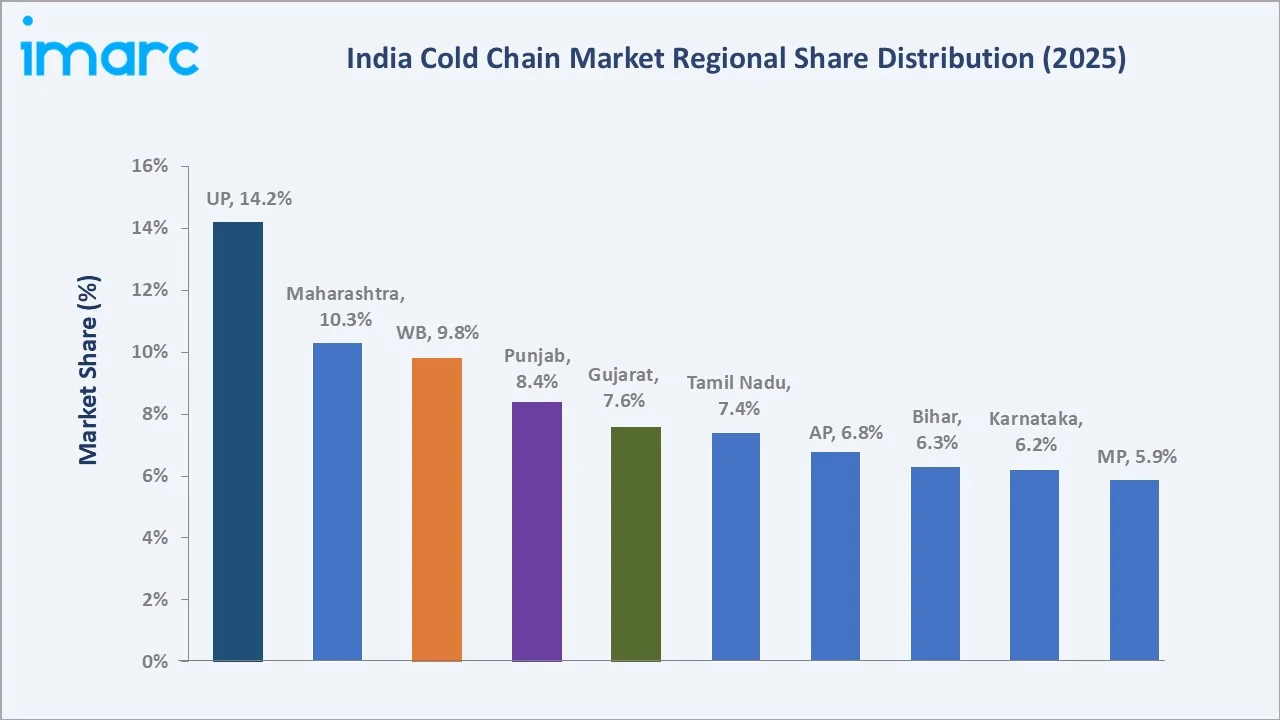

The India cold chain market was valued at INR 2,535.87 Billion in 2025 and is estimated to reach INR 2,800.4 Billion in 2026. The market is further projected to grow INR 6,190.91 Billion by 2034, expanding at a robust CAGR of 10.43% during the forecast period 2026-2034. This growth trajectory is driven by surging demand from organized food retail, pharmaceutical logistics, and government-backed infrastructure initiatives such as PM Kisan SAMPADA Yojana. Cold chain storage dominates with a 68.0% segment share (2025), while the private sector leads with 72.0% of total market revenue. Uttar Pradesh and Maharashtra emerge as the most significant state-level contributors, collectively representing 24.5% of market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 2,535.87 Billion |

|

Forecast Market Size (2034) |

INR 6,190.91 Billion |

|

CAGR (2026-2034) |

10.43% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Largest State |

Uttar Pradesh (14.2% share, 2025) |

|

Fastest Growing Segment |

Cold Chain Transportation (CAGR 11.2%) |

The India cold chain market growth trajectory from 2020 through 2034 contrasts the steady historical base against a steeply accelerating forecast curve shaped by infrastructure investment, government subsidy programmes, and surging demand from food processing, pharmaceutical, and e-grocery sectors.

To get more information on this market, Request Sample

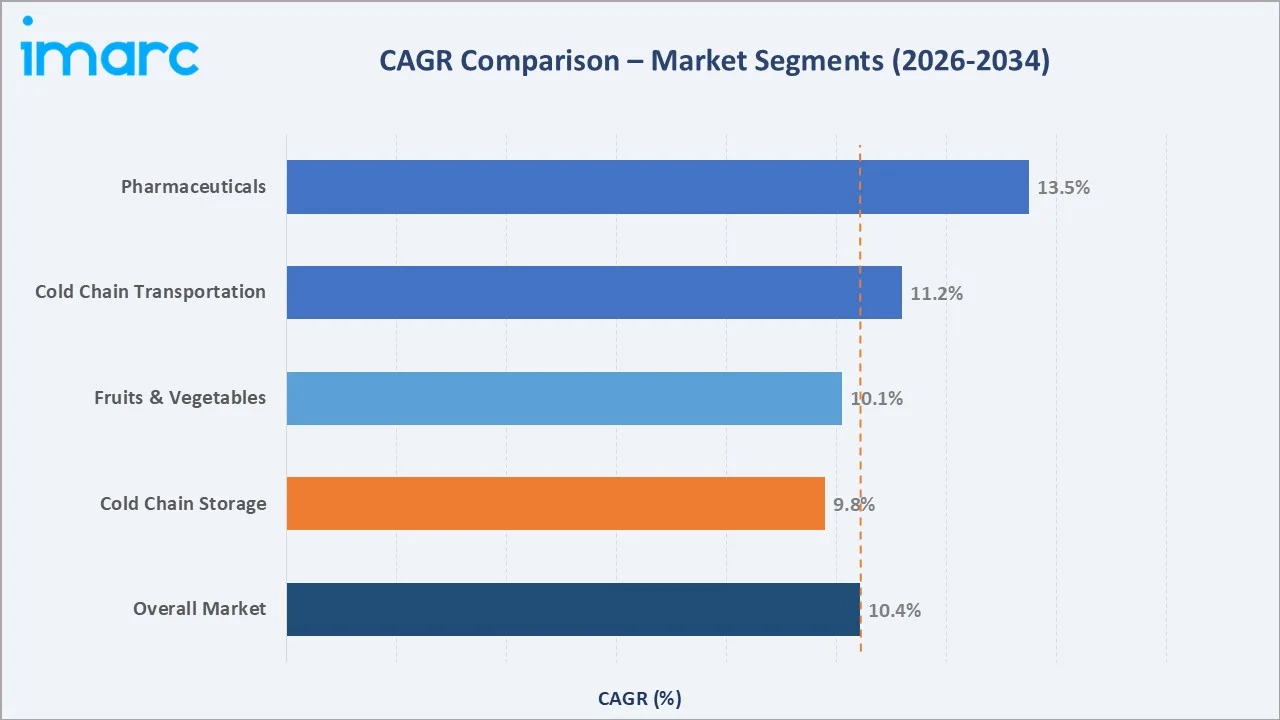

The CAGR comparisons across key segments and technology sub-categories, revealing IoT-enabled cold chain solutions and e-grocery last-mile logistics as the standout highest-growth categories within the India cold chain industry analysis through 2034.

Executive Summary

The India cold chain market is entering a high-growth phase underpinned by transformative shifts across food consumption, pharmaceutical logistics, and e-commerce delivery infrastructure. Valued at INR 2,535.87 Billion in 2025, the market is on a strong trajectory to reach INR 6,190.91 Billion by 2034, a CAGR of 10.43%. Key growth catalysts include government policy support through the PM Kisan SAMPADA Yojana, increasing organized food retail penetration, and rising pharmaceutical cold chain requirements driven by vaccine distribution mandates.

Cold chain storage commands the dominant segment position with 68.0% of total market revenue (2025), supported by rapid warehouse infrastructure expansion across key agricultural states. The private sector leads with a 72.0% share, reflecting sustained capital investments by organized logistics players. E-commerce grocery delivery, growing at 28.4% annually (2025), is a significant emerging demand vector for last-mile cold chain solutions.

State-level analysis reveals Uttar Pradesh (14.2% share), Maharashtra (10.3%), and West Bengal (9.8%) as the three dominant markets in 2025, collectively contributing 34.3% of national cold chain revenues. The pharmaceutical cold chain sub-segment is growing at an estimated 13.5% CAGR (2026–2034), driven by biologics, biosimilars, and vaccine distribution requirements.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Cold Chain Storage - 68.0% share (2025) |

|

Leading Sector |

Private - 72.0% share (2025) |

|

Largest State Market |

Uttar Pradesh - 14.2% revenue share (2025) |

|

Fastest Growing Segment |

Cold Chain Transportation - CAGR 11.2% (2026-2034) |

|

Top Companies |

Snowman Logistics, Delhivery, Mahindra Logistics, Concor Air, AFL |

|

Market Opportunity |

Pharma cold chain projected at INR 620 Billion by 2034 |

Key Analytical Observations Supporting the Above Data:

- Cold chain storage leads with 68.0% share (2025), driven by extensive multi-purpose warehouse development and growing demand for temperature-controlled preservation facilities across agricultural and pharmaceutical sectors.

- The private sector commands 72.0% of market revenues (2025), bolstered by strong private capital investment in modern logistics infrastructure supported by government subsidy schemes under ICCVAI.

- Uttar Pradesh contributes 14.2% of national cold chain revenues (2025), establishing itself as the country's largest state-level market due to its high agricultural output and growing organized cold storage capacity.

- Cold chain transportation is the fastest growing segment at 11.2% CAGR (2026-2034), driven by e-commerce grocery delivery growth (28.4% annually) and expanding last-mile reefer fleet deployment.

India Cold Chain Market Overview

The India cold chain industry constitutes a critical segment within the country's broader logistics and supply chain ecosystem, encompassing temperature-controlled storage, refrigerated transportation, and integrated end-to-end cold chain management services. India's cold chain infrastructure, comprising approximately 8,698 cold storage units as of May 2024, provides a total capacity of 395 lakh metric tonne, forms the backbone of the nation's perishable food preservation network.

The sector's ecosystem spans from farm-gate pre-cooling and pack-house operations to multi-temperature warehousing, reefer transport, and last-mile distribution to urban consumers. Macroeconomic drivers, including rapid urbanization, rising middle-class disposable incomes, and the proliferation of organized retail formats are reshaping consumer demand for temperature-sensitive product categories. Government policy support through MOFPI, NHB, and NABARD-linked schemes provides substantial financial incentives for cold chain infrastructure creation, particularly in under-penetrated states.

Market Dynamics

To evaluate market opportunities, Request Sample

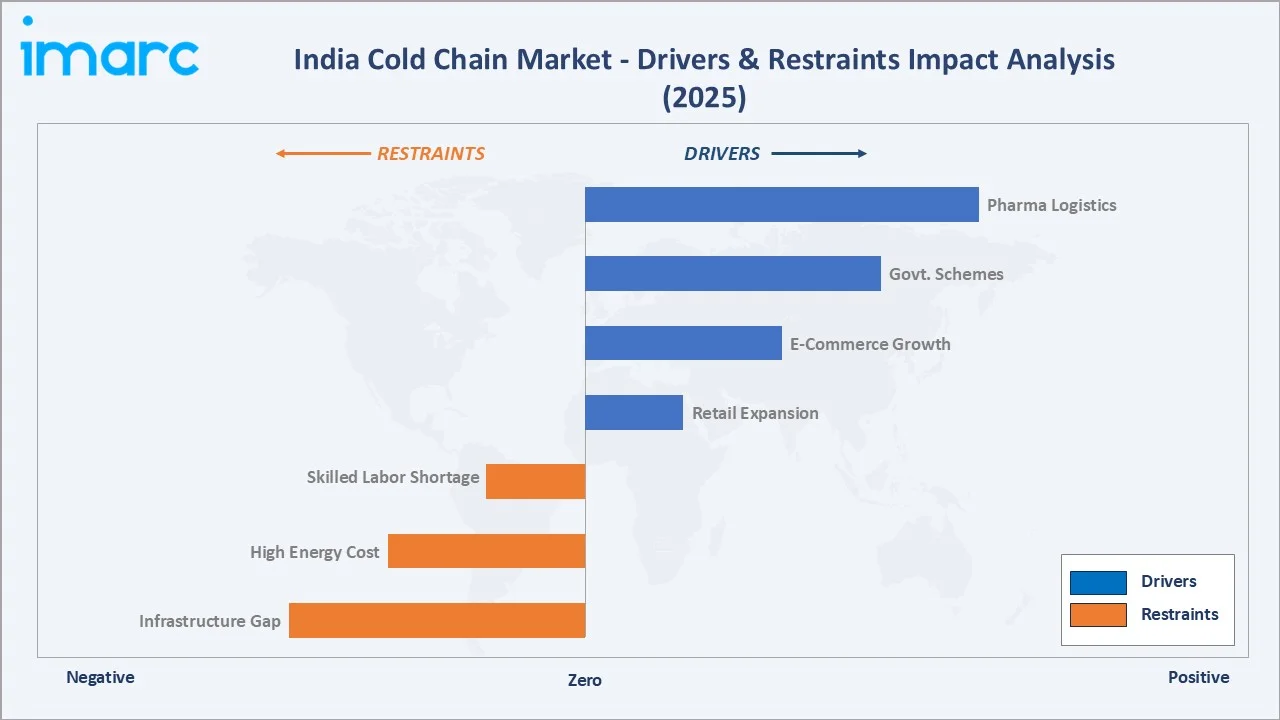

Market Drivers

- Rising E-Commerce Food Delivery: India's e-commerce grocery sector is growing with platforms like Blinkit, Zepto, and Swiggy Instamart creating high-frequency demand for temperature-controlled last-mile logistics, directly driving cold chain transportation investment.

- Pharmaceutical Sector Expansion: India's pharmaceutical exports reached US$ 27.9 Billion in FY2024, with vaccine distribution under the Universal Immunization Programme covering 26 million newborns annually, creating non-negotiable demand for GDP-compliant cold chain infrastructure.

- Government Policy Support: The PM Kisan SAMPADA Yojana allocated ₹ 630 Crore for food processing and cold chain infrastructure for the financial year 2024-25 .

- Organized Retail Penetration: Every 1% increase in organized retail penetration translates to an estimated INR 45–60 Billion in incremental cold chain demand.

Market Restraints

- High Energy and Operational Costs: Electricity costs represent 10% of total operational expenses for cold chain operators, significantly impacting profitability, particularly for smaller facilities.

- Infrastructure Gaps in Tier-2 and Tier-3 Markets: Over 60% of India's cold chain capacity is concentrated in 10 major states (2025), leaving significant under-penetrated geographies with minimal temperature-controlled infrastructure, constraining market reach and limiting agricultural loss reduction.

Market Opportunities

- Multi-Commodity Facility Development: The shift from single-commodity cold storage to multi-temperature warehousing presents a significant efficiency opportunity.

- Solar-Powered Cold Storage: India issued comprehensive guidelines for solar-powered cold storage in 2025. With solar energy costs declining 89% between 2010 and 2023, solar-integrated cold storage offers 30–40% energy cost reduction, enabling viable operations in off-grid agricultural regions.

- Export-Oriented Cold Chain Infrastructure: India's agricultural export target requires significant cold chain investment at ports and export processing zones, representing an incremental infrastructure opportunity through 2030.

Market Challenges

- Skilled Workforce Shortage: Cold chain operations require specialized technical expertise in refrigeration engineering, GDP compliance, and temperature monitoring, skills in short supply across India.

- Regulatory Complexity: Compliance with FSSAI food safety standards, WHO-GDP guidelines for pharmaceutical cold chains, and state-level licensing requirements creates operational complexity, particularly for multi-state logistics operators managing diverse product categories.

Emerging Market Trends

1. IoT-Enabled Real-Time Temperature Monitoring

Advanced sensor networks and IoT platforms are transforming cold chain visibility. In September 2025, Tag-N-Trac's AI and IoT tracking reduced pharmaceutical shipment excursions from 1.93% to 0.3%. Real-time monitoring reduces temperature deviations by up to 68%, directly improving product quality compliance and reducing wastage across the cold chain network.

2. Multi-Temperature Warehousing Adoption

Operators are shifting from single-commodity to versatile multi-temperature facilities handling frozen (-18°C), chilled (0-4°C), and ambient conditions simultaneously. Swisslog's AutoStore Multi-Temperature Solution features 9,500 bins for chilled storage and 5,500 bins for ambient storage, with an initial phase of 6,500 bins.

3. Solar-Powered Cold Storage Expansion

India issued comprehensive solar cold storage guidelines in 2025, accelerating energy-efficient infrastructure investment. Solar-integrated cold storage reduces operational energy costs by 30-40% and enables deployment in areas with unreliable grid connectivity, unlocking cold chain access for over 65% of India's agricultural hinterland.

4. Blockchain-Enabled Supply Chain Traceability

Blockchain traceability is gaining adoption for pharmaceutical and high-value agricultural product cold chains, providing immutable temperature logs from origin to destination.

5. AI-Driven Logistics Optimization

Artificial intelligence is reshaping route optimization, demand forecasting, and capacity utilization for cold chain operators. AI-driven platforms have demonstrated a reduction in empty run rates for reefer trucks and improvement in warehouse utilization for operators who have deployed predictive analytics tools in their operations.

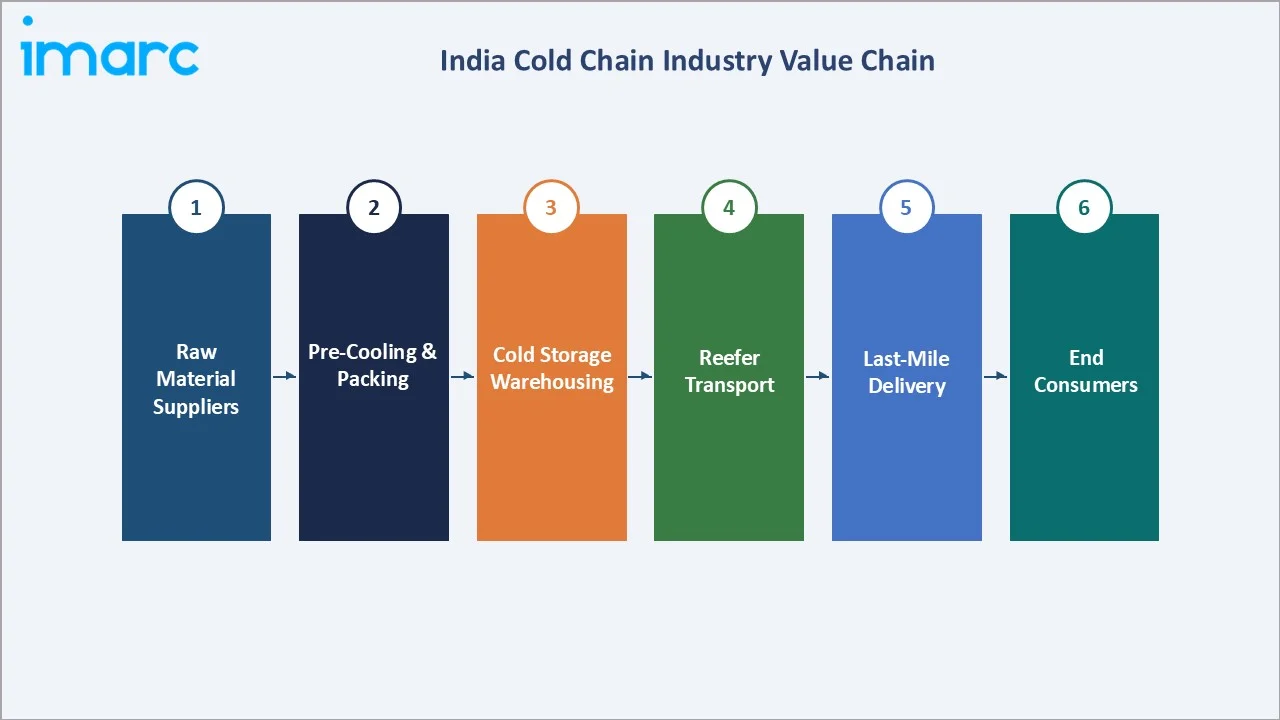

Industry Value Chain Analysis

The India cold chain industry value chain spans multiple interconnected stages from agricultural production and procurement to end-consumer delivery. Each stage requires specialized infrastructure, technology, and expertise to maintain product temperature integrity and ensure compliance with quality standards.

|

Stage |

Key Players / Examples |

|

Raw Material / Farm Gate |

Farmers, FPOs, horticulture cooperatives; pre-cooling units & pack houses |

|

Processing & Packaging |

Food processors (Amul, ITC, Mother Dairy), pharmaceutical manufacturers (Sun Pharma, Cipla) |

|

Cold Storage / Warehousing |

Snowman Logistics, Riviera Cold Storage, ColdEx, Kelvin Cold Chain, NCCD-registered facilities |

|

Reefer Transportation |

AFL, Radhakrishna Foodsland, Concor Air, Mahindra Logistics, TCI Supply Chain, VRL Logistics |

|

Distribution & Retail |

Reliance Retail, DMart, Big Bazaar, e-commerce (Blinkit, Swiggy Instamart, Zepto) |

|

Last-Mile / End Consumer |

Direct-to-consumer delivery platforms, pharmacies (Apollo, MedPlus), household consumers |

Technology Landscape in the India Cold Chain Industry

Refrigeration and Energy Technology

Advanced refrigeration systems using low-GWP (Global Warming Potential) refrigerants such as R-290 (propane), CO2, and ammonia are replacing legacy HFC-based systems in compliance with India's Cooling Action Plan.

IoT, AI, and Digital Platforms

IoT sensor networks deployed across cold chain facilities provide continuous temperature, humidity, and vibration monitoring with sub-second data transmission frequencies. AI-driven demand forecasting reduces inventory carrying costs by 15-25% for cold chain operators serving organized food retail clients. Digital cold chain management platforms, including INAPH (e-Gopala) for dairy and NHB-linked horticulture platforms, are standardizing data capture and enabling regulatory compliance verification across the supply network.

Automated Storage and Retrieval Systems (ASRS)

Automated cold storage facilities with ASRS technology improve throughput capacity by 40-60% compared to manual operations while reducing labor costs by 35-45%. The ICCVAI Scheme provides financial assistance for ASRS adoption in integrated multi-temperature cold chain complexes.

Sustainability and Green Cold Chain

Solar photovoltaic integration for cold storage reduces energy consumption costs by 30-40% and qualifies for accelerated depreciation benefits under Indian tax regulations. The GRIHA rating system for green cold storage buildings is gaining adoption among premium logistics operators.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Segment |

Cold Chain Storage |

68.0% |

2025 |

|

Product |

Fruits and Vegetables |

37.0% |

2025 |

|

Sector |

Private |

72.0% |

2025 |

|

Organised and Unorganised |

Unorganised |

80.0% |

2025 |

|

States |

Uttar Pradesh |

14.2% |

2025 |

By Segment

Cold chain storage leads the Indian market with a commanding 68.0% revenue share in 2025, encompassing multi-purpose warehousing, controlled atmosphere facilities, and pharmaceutical-grade storage units. The segment benefits from government infrastructure grants, rising private investment, and structural demand from organized food retail expansion.

To access detailed market analysis, Request Sample

Cold chain storage's dominance reflects the infrastructure-first development stage of India's cold chain ecosystem. Automated storage and retrieval systems, multi-temperature capabilities, and controlled atmosphere technology are increasingly being incorporated into new cold storage facilities, enhancing revenue per unit and driving segment value growth beyond mere capacity expansion.

By Sector

The private sector commands 72.0% of India's cold chain market revenues in 2025, reflecting sustained capital investment by organized logistics operators supported by government subsidy schemes and growing institutional demand. The cooperative sector holds 16.8% share in 2025, primarily serving dairy and agricultural cooperative networks including Amul's extensive cold chain infrastructure. The public sector contributes 11.2% of revenues, with government-owned cold storage facilities concentrated in agricultural states under National Horticulture Board and FCI programs.

The cooperative sector’s 16.8% share (2025) reflects the significant cold chain infrastructure operated by dairy cooperatives across states, including Gujarat, Rajasthan, and Andhra Pradesh. Amul's cold chain network alone encompasses high chilling centers with a combined processing of 447,000 litres of milk daily from 2.12 million farmers across 1,200 cooperatives, representing a significant institutional cold chain asset base.

Regional Market Insights (State-Level Analysis)

Uttar Pradesh's 14.2% market leadership (2025) reflects its dual advantage as India's most populous state and largest agricultural producer, with cold chain demand spanning potatoes (30% of national output), onions, and horticultural commodities. The state benefits from proximity to the national capital region's consumption base and is a priority investment destination under MOFPI's cold chain infrastructure scheme.

|

State |

Share (2025) |

Key Growth Drivers |

Strategic Positioning |

Major Operators |

|

Uttar Pradesh |

14.2% |

Horticulture & Agri Logistics |

Largest potato producer; extensive horticulture base; Agra-Lucknow corridor logistics |

Snowman, ColdEx, CCCL, local operators |

|

Maharashtra |

10.3% |

Pharma + Organized Retail |

Largest organized retail hub; Pune pharma cluster; JNPT Mumbai port cold chain; Nashik grapes export belt |

Mahindra Logistics, AFL Pvt. Ltd., Radhakrishna Foodland |

|

West Bengal |

9.8% |

Fish & Seafood Exports |

Major fish & seafood producer; Kolkata cold chain hub; Hooghly potato belt; Bangladesh export linkages |

Balaji Cold Chain, VRL Logistics, local fish processors |

|

Punjab |

8.4% |

Grain, Dairy & Horticulture |

Largest wheat/grain producer; Amul partner dairy cold chain; developing potato & horticulture export infrastructure |

Local cooperatives, Agri logistics firms, Amul distribution |

|

Gujarat |

7.6% |

Dairy & Port Cold Chain |

Amul GCMMF dairy cold chain backbone; Kandla and Mundra port cold storage; organized F&B manufacturing cluster |

Amul, GCMMF, Delhivery, Gujarat Cooperative |

|

Tamil Nadu |

7.4% |

Seafood + Pharma Exports |

Export-oriented horticulture; Chennai pharma manufacturing cluster; cold storage modernization under NHM schemes |

Snowman Logistics, ColdStar, local export operators |

|

Andhra Pradesh |

6.8% |

Aquaculture & Mango Belt |

Largest aquaculture exporter; Chittoor mango and tomato belt; Hyderabad pharma manufacturing cold chain |

Snowman Logistics, local aquaculture operators |

|

Bihar |

6.3% |

Horticulture & Litchi |

Large potato and Litchi production state; government cold storage expansion; NABARD-funded facility development |

NABARD-funded facilities, PMKSY beneficiary operators |

|

Karnataka |

6.2% |

Tech Logistics & Horticulture |

Flower and vegetable exports; Bangalore tech-driven processed food demand; pharma cold chain; Kolar tomato belt |

Delhivery, Mahindra Logistics, local operators |

|

Madhya Pradesh |

5.9% |

Agri + Pharma |

Indore pharma hub cold chain; soybean and wheat processing; PM Kisan SAMPADA scheme major beneficiary state |

Local warehouse operators, Indore pharma logistics firms |

|

Haryana |

5.7% |

Dairy & Vegetable Belt |

NCR proximity driving processed food demand; Amul distribution hub; Sonipat vegetable cold chain corridor |

Local dairy cooperatives, NCR-linked 3PL operators |

|

Rajasthan |

5.1% |

Milk & Spices |

RCDF dairy cold chain; Jodhpur and Jaipur spice processing cold chain; solar cold storage adoption leader |

RCDF, local operators, solar cold storage start-ups |

|

Orissa |

4.2% |

Seafood & Aquaculture |

Chilika lake aquaculture cold chain; Paradip port export cold chain; growing private investment in storage capacity |

Regional operators, Paradip port cold chain firms |

|

Chhattisgarh |

3.4% |

Paddy & Poultry |

Poultry cold chain; rice and vegetable storage; lowest cold chain penetration nationally with high growth potential |

State FCI warehouses, local poultry operators |

|

Others |

8.7% |

Multi-State Emerging |

Includes Jharkhand, NE states, J&K horticulture, and Union Territories; nascent cold chain markets with high growth trajectory |

Regional and state-specific logistics operators |

Maharashtra's 10.3% share (2025) reflects its position as India's economic capital, a convergence of organized retail, pharmaceutical manufacturing, and export-oriented food processing creating multi-vector cold chain demand. The Mumbai-Pune corridor hosts over 40% of India's pharmaceutical manufacturing capacity , generating premium-priced GDP-compliant cold chain requirements.

Competitive Landscape

The India cold chain market exhibits a fragmented competitive structure, with the top five organized players collectively accounting for approximately 18-22% of total market revenues in 2025. The remainder is distributed among thousands of regional cold storage operators, cooperative-owned facilities, and small-scale reefer transport providers.

|

Company Name |

Brand/Network Name |

Market Position |

Core Strength |

|

Snowman Logistics Ltd. |

Snowman |

Market Leader |

Largest organized cold chain network; 40+ facilities; pharmaceutical & food expertise |

|

Mahindra Logistics Ltd. |

Mahindra Logistics |

Strong Challenger |

Integrated 3PL with temperature-controlled capabilities; organized food retail clients |

|

Delhivery Ltd. |

Delhivery |

Fast Challenger |

Technology-first approach; pan-India reach; e-commerce cold chain specialization |

|

Container Corporation of India |

CONCOR |

Established Player |

Government-backed; cold container logistics; multi-modal transport infrastructure |

|

AFL (Agri Fresh Logistics) |

AFL |

Sector Specialist |

Agri-focused cold chain; farm-to-fork solutions; export-oriented infrastructure |

|

Radhakrishna Foodsland |

RK Foodsland |

Regional Leader |

QSR and organized food retail cold chain; Mumbai and western India strength |

|

Riviera Cold Storage |

Riviera |

Emerging Player |

Modern automated facilities; multi-temperature capabilities; western India focus |

Organized players are differentiating through technology investment, multi-temperature capability, and integrated end-to-end service offerings.

Key Company Profiles

Snowman Logistics Limited

Snowman Logistics is India's prominent organized cold chain logistics company, operating a network of 40+ temperature-controlled facilities with a combined capacity exceeding 130,000 pallet positions across 15+ cities as of 2025.

- Product Portfolio: Multi-temperature cold storage (frozen, chilled, ambient); reefer transport; cold chain packaging and value-added services; pharmaceutical GDP-compliant warehousing.

- Recent Developments: In October 2025, Snowman Logistics announced the commencement of construction of a new temperature-controlled warehouse facility in Pune.

- Strategic Focus: Geographic expansion into Tier-2 cities; pharmaceutical cold chain capacity investment; digital platform development for real-time supply chain visibility.

Mahindra Logistics Limited

Mahindra Logistics (MLL) is one of India's leading 3PL providers offering integrated supply chain solutions including temperature-controlled logistics for food, pharmaceutical, and FMCG clients.

- Product Portfolio: Reefer trucking, cold chain warehousing, integrated 3PL services, pharmaceutical cold chain, e-commerce fulfilment with temperature control.

- Recent Developments: Partnered with Flipkart for grocery cold chain fulfilment; expanded EV reefer fleet.

- Strategic Focus: Technology integration through MLL digital platform; expansion of cold chain service portfolio; sustainable logistics with EV fleet and solar-powered warehouses.

Delhivery Limited

Delhivery is India's leading technology-enabled logistics provider with an emerging cold chain capability catering to e-commerce and quick-commerce grocery delivery.

- Product Portfolio: Cold chain last-mile delivery; reefer express freight; temperature-controlled fulfillment centers; cold storage integrated with D2C brand fulfilment.

- Recent Developments: In February 2026, Delhivery Limited partnered with electric mobility startup RIDEV (ANV Web Ventures Pvt Ltd) to deploy 150 high-performance electric vehicles (EVs).

- Strategic Focus: Technology-driven cold chain scaling; hyperlocal delivery infrastructure investment; B2B pharmaceutical cold chain entry.

Market Concentration Analysis

The India cold chain market exhibits low-to-moderate concentration at the organized sector level, with the top five organized players collectively accounting for approximately 18-22% of total national market revenues in 2025. This concentration level is significantly lower than comparable cold chain markets in developed economies such as the US and Europe, reflecting India's market development stage.

In contrast, the organized segment commands premium pricing, typically 25-35% above unorganized equivalents, due to multi-temperature capability, technology integration, and service quality differentiation.

Consolidation trends are accelerating, with an estimated 12–15 significant M&A transactions or strategic partnerships expected annually through 2034 as organized players acquire regional operators to expand geographic coverage.

Investment & Growth Opportunities

Fastest Growing Segments

Pharmaceutical cold chain (CAGR 13.5%), cold chain transportation (CAGR 11.2%), and multi-temperature warehousing (CAGR 12.1%) represent the three highest-growth investment vectors in the India cold chain market through 2034. These segments collectively address a total addressable market, supported by regulatory mandates, e-commerce growth, and export infrastructure requirements.

Emerging Market Opportunities

Tier-2 and Tier-3 city cold chain infrastructure presents the most compelling geographic investment opportunity, with an estimated 34% of India's agricultural output still lacking adequate cold chain access. Bihar, Odisha, Jharkhand, and Northeastern states represent under-penetrated markets with growing government infrastructure commitment. Solar-powered cold storage, enabled by comprehensive guidelines issued in 2025, unlocks investment opportunities in off-grid agricultural regions previously unviable for cold storage deployment.

Venture Investment Trends

Key investment themes include AI-driven cold chain management platforms, automated multi-temperature warehousing, EV reefer fleet deployment, and agri-tech integrated cold chain solutions connecting farmers directly to organized retail supply chains.

- Government subsidy capture: PM Kisan SAMPADA Yojana grants of up to INR 10 Crore per ICCVAI-eligible project offer attractive co-investment opportunities for private sector operators building multi-temperature integrated cold chain complexes.

- Pharmaceutical cold chain premium: GDP-compliant pharmaceutical cold chain facilities command 35–50% premium pricing over standard food-grade cold storage, offering superior unit economics for specialized operators.

Future Market Outlook (2026-2034)

The India cold chain market is positioned for sustained high-growth expansion through 2034, anchored by government policy commitment, structural demographic demand drivers, and accelerating private capital investment. From a base of INR 2,535.87 Billion in 2025, the market is forecast to reach INR 6,190.91 Billion by 2034, representing absolute incremental value addition of INR 3,655.04 Billion over the nine-year forecast horizon.

Technological disruptions, including AI-driven route optimization, automated multi-temperature warehousing, IoT-enabled real-time monitoring, and blockchain-based traceability, are expected to materially reduce cold chain spoilage rates from the current 15–18% level to below 8% by 2030.

The pharmaceutical cold chain sub-segment is projected to become the highest-value product category by 2032, surpassing fruits and vegetables in revenue contribution, driven by biosimilar launches, expanding vaccine programs, and biopharmaceutical logistics requirements.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 180 industry participants, comprising cold chain logistics executives, pharmaceutical supply chain managers, organized food retail procurement heads, government officials from MOFPI and NHB, and end-user manufacturers across food, pharmaceutical, and FMCG sectors in India during 2024–2025.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, NCCD data, NHB cold storage surveys, APEDA export statistics, Ministry of Food Processing Industries publications, industry databases, and trade publications including Cold Chain India, Food Technology magazine, and Logistics Insider. Over 300 secondary sources were reviewed and triangulated for data accuracy.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, organized retail penetration trends, pharmaceutical sector CAGR projections, agricultural output data, and government infrastructure spending commitments. Scenario analysis across base, optimistic, and conservative cases was performed to account for policy uncertainty and macroeconomic risk factors.

India Cold Chain Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion, Million Metric Tons |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Segments Covered | Cold Chain Storage, Cold Chain Transportation |

| Products Covered | Fruits and Vegetables, Meat and Fish, Dairy Products, Healthcare Products |

| Sectors Covered | Private, Cooperative, Public |

| Organised and Unorganised Covered | Organised, Unorganised |

| States Covered | Uttar Pradesh, West Bengal, Punjab, Gujarat, Bihar, Andhra Pradesh, Madhya Pradesh, Maharashtra, Karnataka, Haryana, Chhattisgarh, Rajasthan, Orissa, Tamil Nadu, Others |

| Companies Covered | Snowman Logistics Ltd., Mahindra Logistics Ltd., Delhivery Ltd., Container Corporation of India, AFL (Agri Fresh Logistics), Radhakrishna Foodsland, Riviera Cold Storage, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Cold Chain Market Report

The India cold chain market was valued at INR 2,535.87 Billion in 2025 and is projected to reach INR 6,190.91 Billion by 2034.

The India cold chain market is projected to grow at a robust CAGR of 10.43% during the forecast period from 2026-2034, reflecting strong structural demand from multiple end-use sectors.

Cold chain storage dominates with a 68.0% revenue share in 2025, supported by extensive warehousing infrastructure development and growing demand for temperature-controlled preservation across food and pharmaceutical sectors.

Uttar Pradesh holds the largest state-level share at 14.2% in 2025, driven by high agricultural output, extensive potato and horticulture production, and growing organized cold storage infrastructure in the NCR and Agra-Lucknow corridor.

Key drivers include rising e-commerce grocery delivery (28.4% annual growth), pharmaceutical sector expansion, government PM Kisan SAMPADA Yojana investment, and increasing organized retail penetration driving temperature-controlled infrastructure demand.

The private sector holds 72.0% of market revenue in 2025, driving modern cold chain infrastructure investment, technology adoption, and multi-temperature facility development supported by government subsidy incentives under ICCVAI.

Leading companies include Snowman Logistics, Mahindra Logistics, Delhivery, Container Corporation of India (CONCOR), AFL (Agri Fresh Logistics), Radhakrishna Foodsland, and Riviera Cold Storage.

The pharmaceutical cold chain sub-segment grows at an estimated 13.5% CAGR from 2026-2034, driven by biologics, biosimilar launches, vaccine distribution under Universal Immunization Programme, and India's pharmaceutical export expansion.

IoT real-time monitoring, AI-driven route optimization, automated storage systems, and solar-powered cold storage are transforming efficiency. IoT adoption reduced pharmaceutical excursions from 1.93% to 0.3% in 2025pilot deployments.

Key challenges include fragmented unorganized sector (80% of capacity), high energy costs (35–45% of operational expenses), skilled workforce deficit of 45,000 professionals, and inadequate last-mile infrastructure in rural geographies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)