Indian Fertilizer Market Size, Share, Trends and Forecast by Product Type, Segment, Formulation, Application, and Region, 2026-2034

Indian Fertilizer Market Size, Share, Trends & Forecast (2026-2034)

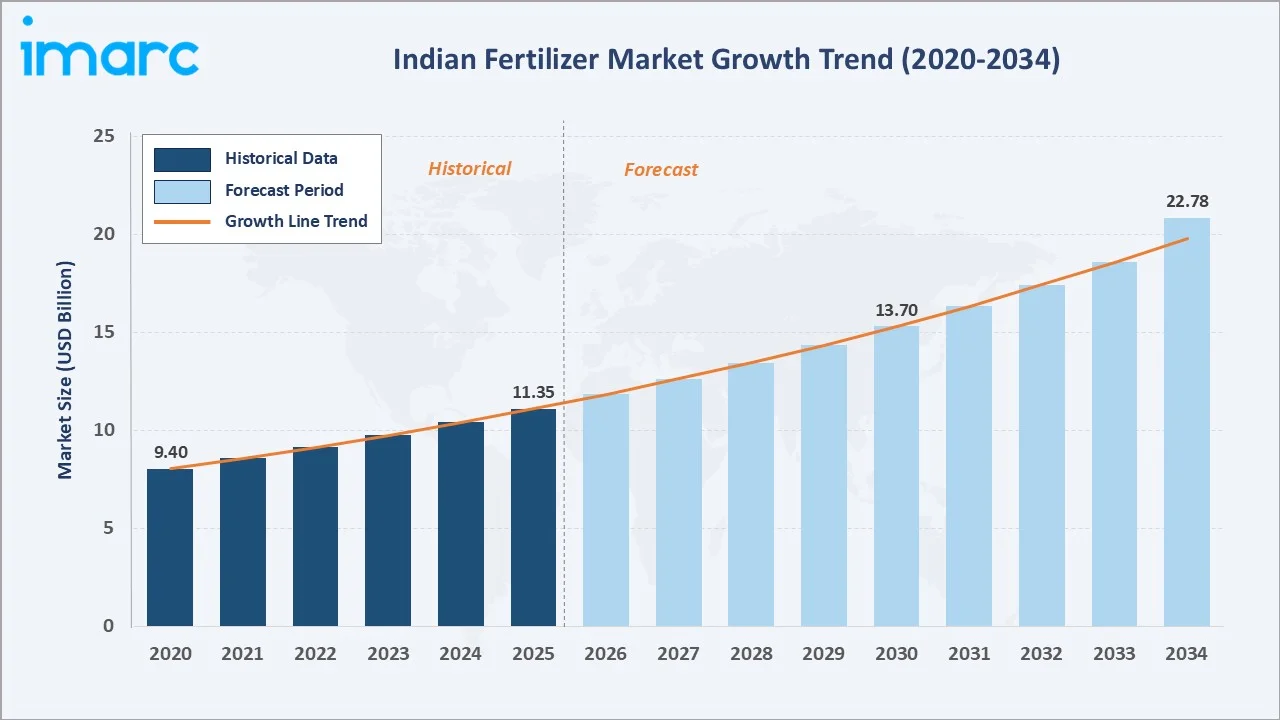

The Indian fertilizer market size was valued at USD 11.35 Billion in 2025 and is projected to reach USD 22.78 Billion by 2034, growing at a CAGR of 3.84% during 2026-2034. Rising food demand, robust government subsidy support, and accelerating adoption of nano and biofertilizer technologies are the primary growth drivers shaping India's fertilizer landscape.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.35 Billion |

|

Forecast Market Size (2034) |

USD 22.78 Billion |

|

CAGR (2026-2034) |

3.84% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (33.0% share, 2025) |

|

Fastest Growing Region |

South India |

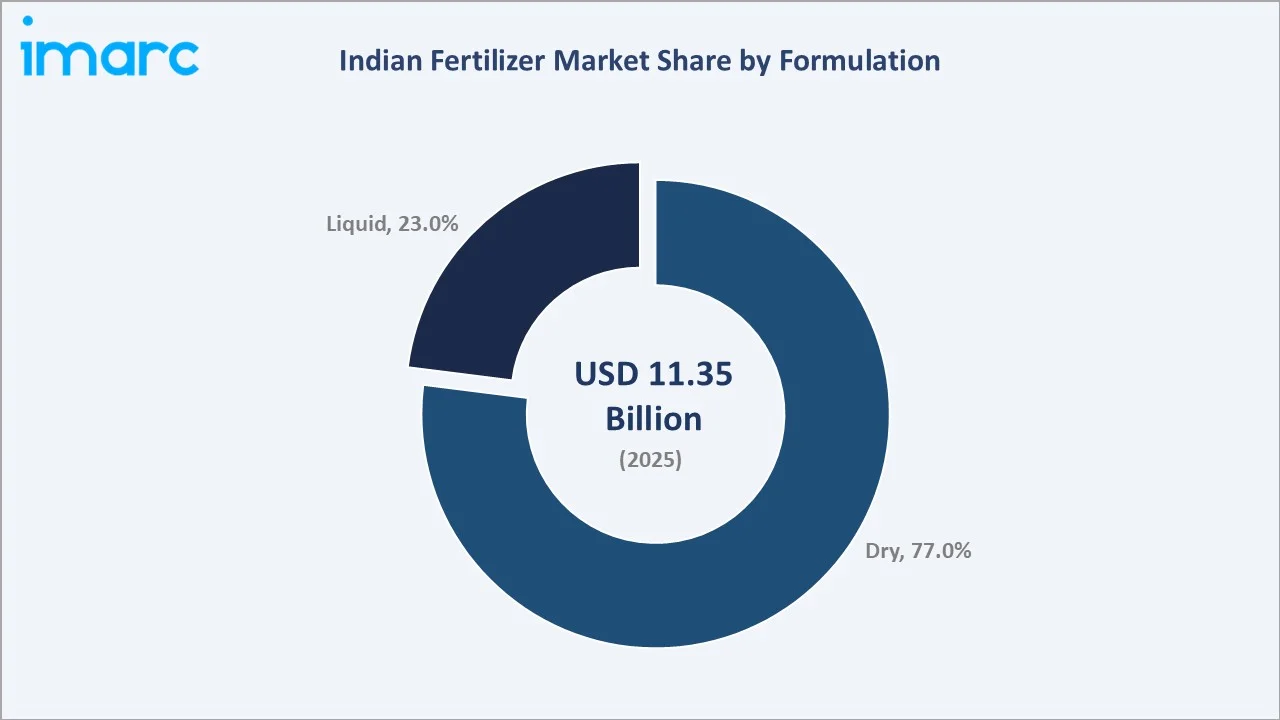

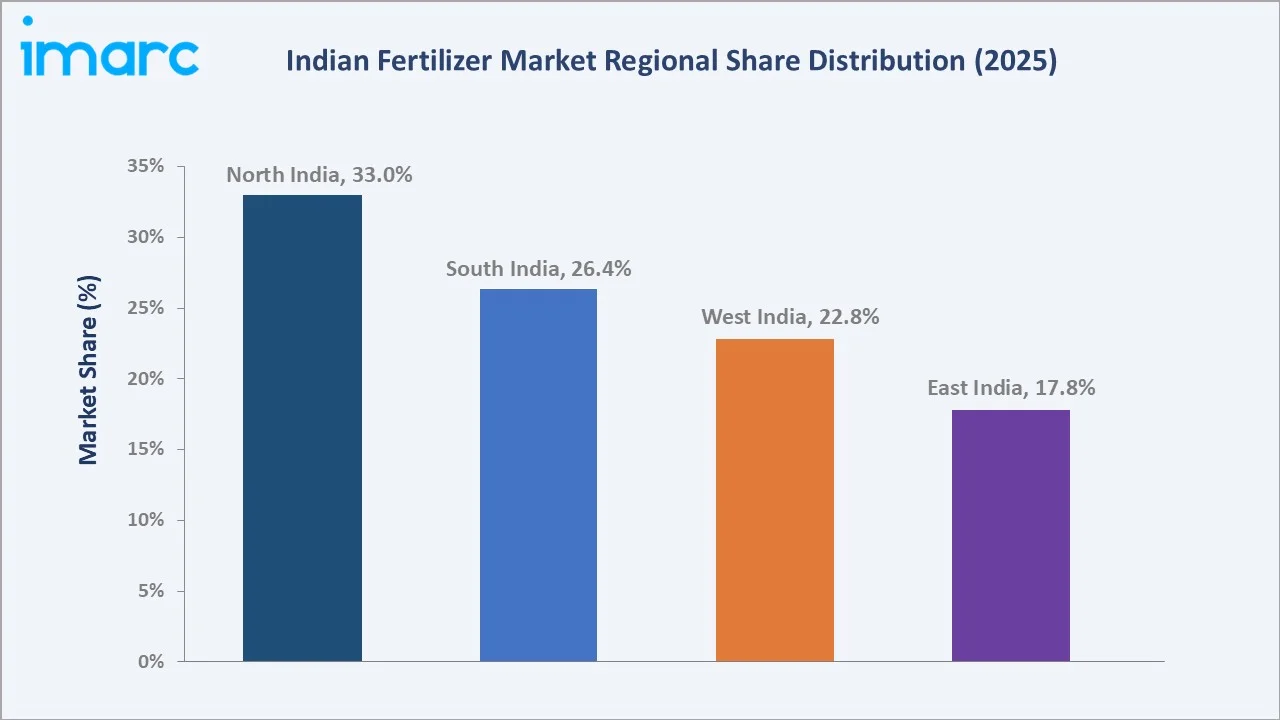

North India dominates with a 33.0% market share in 2025, driven by intensive cereal-based farming in Punjab, Haryana, and Uttar Pradesh. Chemical fertilizers command 83.0% of product-type demand, while dry formulations lead at 77.0%. India's status as the world's second-largest fertilizer consumer, combined with the government's Nutrient-Based Subsidy (NBS) framework and PM-PRANAM policy, underpins the market's steady growth trajectory through 2034.

To get more information on this market, Request Sample

With applications spanning grains and cereals, oilseeds, fruits and vegetables, and horticulture, and a growing portfolio of nano-fertilizers, biofertilizers, and water-soluble specialty inputs, the Indian fertilizer market forecast reflects sustained expansion driven by structural food security imperatives and agricultural modernization.

Executive Summary

The Indian fertilizer market is on a sustained growth path, supported by population-driven food demand, government subsidy architecture, and rapid technological innovation in nutrient delivery systems. The market reached USD 11.35 Billion in 2025 and is forecast to reach USD 22.78 Billion by 2034, reflecting a steady CAGR of 3.84% over the forecast period.

North India leads regionally with a 33.0% revenue share in 2025, anchored by the intensive cereal-farming belt of Punjab, Haryana, and Uttar Pradesh, where paddy and wheat cultivation drives substantial urea and DAP consumption. South India, at 26.4%, is the fastest-growing region, supported by expanding horticulture and cash crop cultivation. West India accounts for 22.8%, while East India holds 17.8%, with the latter showing strong growth potential driven by expanding irrigation and government input-support programs.

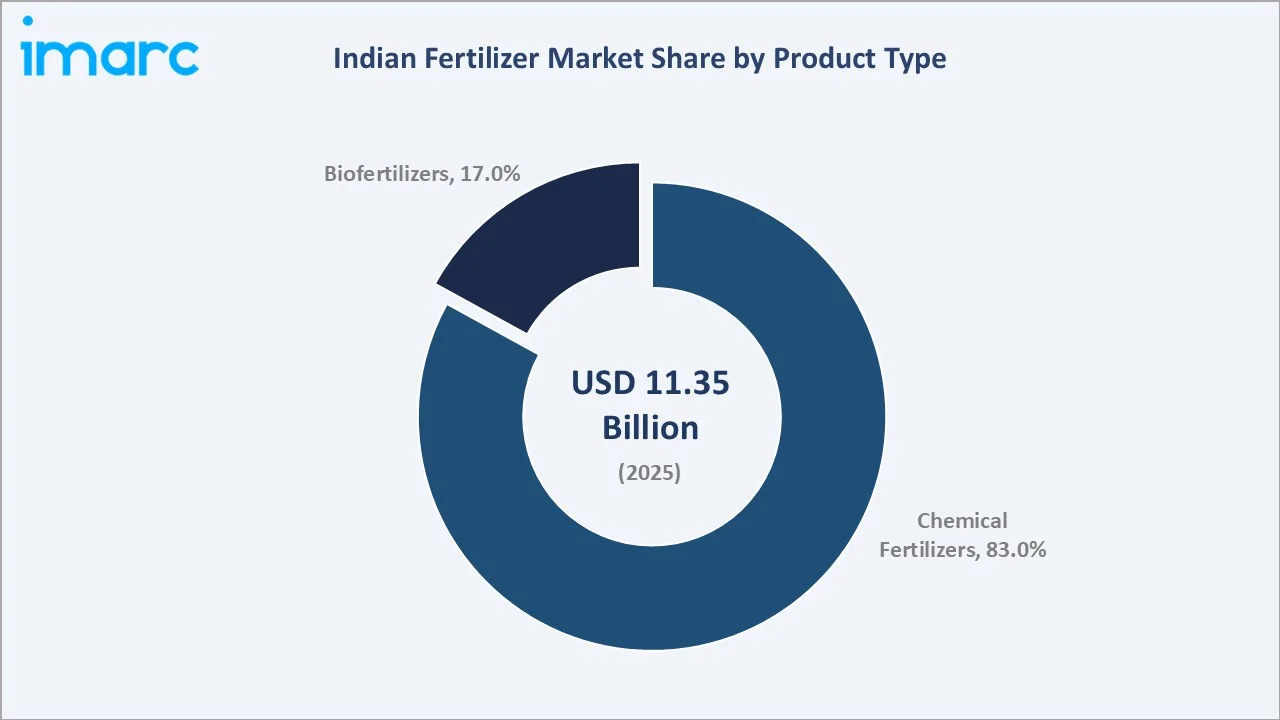

Chemical fertilizers dominate product demand at 83.0% in 2025, reflecting their established role in crop nutrition and government-subsidized affordability. Biofertilizers, at 17.0%, are growing rapidly as sustainability mandates and the National Mission on Natural Farming accelerate adoption. Key players, including IFFCO, Chambal Fertilisers and Chemicals Limited, Rashtriya Chemicals and Fertilizers Limited, National Fertilizers Limited, and DFPCL., continue to invest in nano-fertilizer manufacturing, specialty product portfolios, and distribution network expansion to capture incremental market share.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Chemical Fertilizers – 83.0% share (2025) |

|

Largest Segment (Formulation) |

Dry – 77.0% share (2025) |

|

Leading Region |

North India – 33.0% revenue share (2025) |

|

Fastest Growing Region |

South India (horticulture + cash crops expansion) |

|

Market Opportunity |

Nano-fertilizer market projected at CAGR 4.28% through 2034 |

|

Policy Driver |

PM-PRANAM & National Mission on Natural Farming (INR 2,481 Cr) |

Key Analytical Observations Supporting the Above Data:

- Chemical fertilizers account for 83.0% of the Indian fertilizer market in 2025, driven by widespread use across staple crop cultivation, affordability through government subsidies, and the ability to deliver instant, predictable nutrient outcomes for urea, DAP, and complex NPK formulations.

- Dry formulations dominate at 77.0% in 2025 due to ease of storage, handling, and application across India's diverse agro-climatic zones, extended shelf life, and compatibility with existing farm mechanization equipment and distribution infrastructure.

- North India holds 33.0% of the domestic fertilizer market in 2025, driven by intensive cropping patterns in the Indo-Gangetic Plain, where wheat-paddy rotation demands high fertilizer inputs across 33.4 million hectares of agricultural land.

- South India at 26.4% is the fastest-growing region, with Karnataka, Tamil Nadu, and Andhra Pradesh's expanding horticulture, coffee, and sugarcane cultivation driving demand for specialty NPK and biofertilizer products beyond conventional urea.

- Biofertilizers at 17.0% are growing rapidly, supported by the government's National Mission on Natural Farming (INR 2,481 crore), PM-PRANAM policy rewarding states that reduce chemical fertilizer consumption, and IFFCO's nano-fertilizer Mahaabhiyan across 800 villages.

Indian Fertilizer Market Overview

The Indian fertilizer market encompasses the production, distribution, and consumption of chemical fertilizers, biofertilizers, nano-fertilizers, and specialty nutrient inputs used across farming, horticulture, and gardening segments. India is the world's second-largest fertilizer consumer, with agriculture contributing approximately 17–18% to GDP and employing 42% of the national workforce.

Macroeconomic drivers include India's population of 1.45 billion, creating structural food security imperatives, a total cropped area of 219.16 million hectares with significant productivity improvement potential, and the government's Deep Direct Benefit Transfer (DBT) subsidy mechanism ensuring farmer access to subsidized nutrients.

Market Dynamics

To evaluate market opportunities, Request Sample

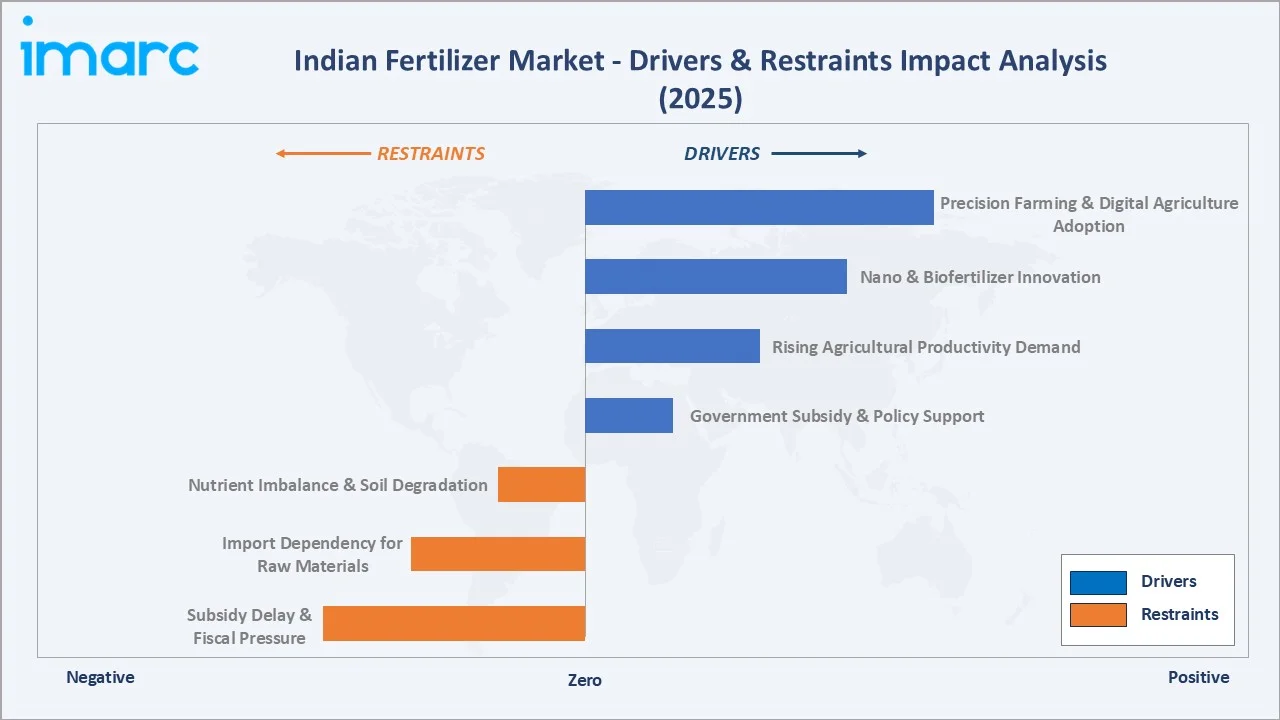

Market Drivers

- Government Subsidy and Policy Support: India's fertilizer subsidy budget reached approximately INR 1.64 trillion in 2024–25, ensuring that urea and NBS-covered fertilizers remain affordable for farmers. The DBT mechanism directly transfers subsidy benefits to certified retailers, reducing diversion and improving nutrient access for smallholder farmers across all states.

- Rising Agricultural Productivity Demand: India’s foodgrain production is projected to reach around 368 million tonnes by 2030–31, driven by continued growth in agricultural output and rising demand, according to a recent report.

- Nano and Biofertilizer Innovation: IFFCO launched the Nano Fertilizer Usage Promotion Mahaabhiyan covering 200 model nano village clusters across 800 villages, offering farmers a 25% subsidy on Nano Urea Plus, Nano DAP, and Sagarika.

- Precision Farming and Digital Agriculture Adoption: Soil Health Card program rollouts, drone-based fertilizer application, and IoT-enabled soil monitoring are optimizing fertilizer use efficiency. Digital agronomy platforms providing crop-specific nutrient recommendations are improving application precision and reducing wasteful over-fertilization across India's diverse farm size categories.

These drivers reinforce a self-sustaining growth cycle, government subsidies maintain accessibility, innovation improves efficiency, and productivity demand sustains consumption growth that justifies continued policy investment across the fertilizer ecosystem.

Market Restraints

- Nutrient Imbalance and Soil Degradation: Heavy subsidization of urea has historically skewed India's N:P:K ratio to as high as 8:3:1, causing long-term soil health deterioration across the Indo-Gangetic Plain. Correcting this imbalance requires sustained policy and behavioral change that constrains near-term urea volume growth while promoting balanced nutrition inputs.

- Import Dependency for Raw Materials: India imports approximately 80% of its phosphoric acid and potash requirements, exposing the market to global commodity price volatility and geopolitical supply disruptions. Raw material cost inflation passes through to manufacturer margins and subsidy outflows, creating fiscal pressure on the government's support architecture.

- Subsidy Delay and Fiscal Pressure: Delays in subsidy reimbursements from the government to fertilizer manufacturers create working capital stress for companies, particularly smaller private manufacturers. Fiscal consolidation pressures periodically constrain subsidy budgets, creating uncertainty in pricing and distribution planning for the sector.

Market Opportunities

- Indigenous Water-Soluble Fertilizer Technology: In August 2025, India's Ministry of Mines successfully developed its first indigenous water-soluble fertilizer technology after seven years of research, using domestic raw materials. This breakthrough could transform India from a specialty fertilizer importer into a potential global exporter of high-value water-soluble formulations, creating a new manufacturing and export opportunity.

- Biofertilizer and Natural Farming Expansion: The Government of India's INR 2,481 crore National Mission on Natural Farming (NMNF) targets 750,000 hectares and 10 million farmers, creating sustained demand for biofertilizers and organic nutrient inputs. The PM-PRANAM policy financially incentivizes states to shift consumption from conventional to alternative fertilizers, expanding the biofertilizer addressable market.

- Horticulture and Specialty Crop Demand: India's horticulture production exceeding 351.92 million tons annually, combined with growing export demand for fruits and vegetables, is driving adoption of specialty NPK blends, micronutrient formulations, and water-soluble fertilizers tailored to high-value crop requirements.

Market Challenges

- Distribution and Last-Mile Access: Reaching fertilizers to India's 100+ million smallholder farmers across 640,000 villages requires extensive distribution infrastructure. Cold-chain requirements for biofertilizers and short shelf-life constraints for certain liquid formulations add logistical complexity and cost to rural distribution networks.

- Farmer Awareness and Technology Adoption: Transitioning farmers from established urea-heavy application practices to balanced nutrient management, nano-fertilizers, and biofertilizers requires sustained agronomic extension and demonstration programs. Low digital literacy in rural areas limits the penetration of precision farming platforms among the smallholder farmer majority.

Emerging Market Trends

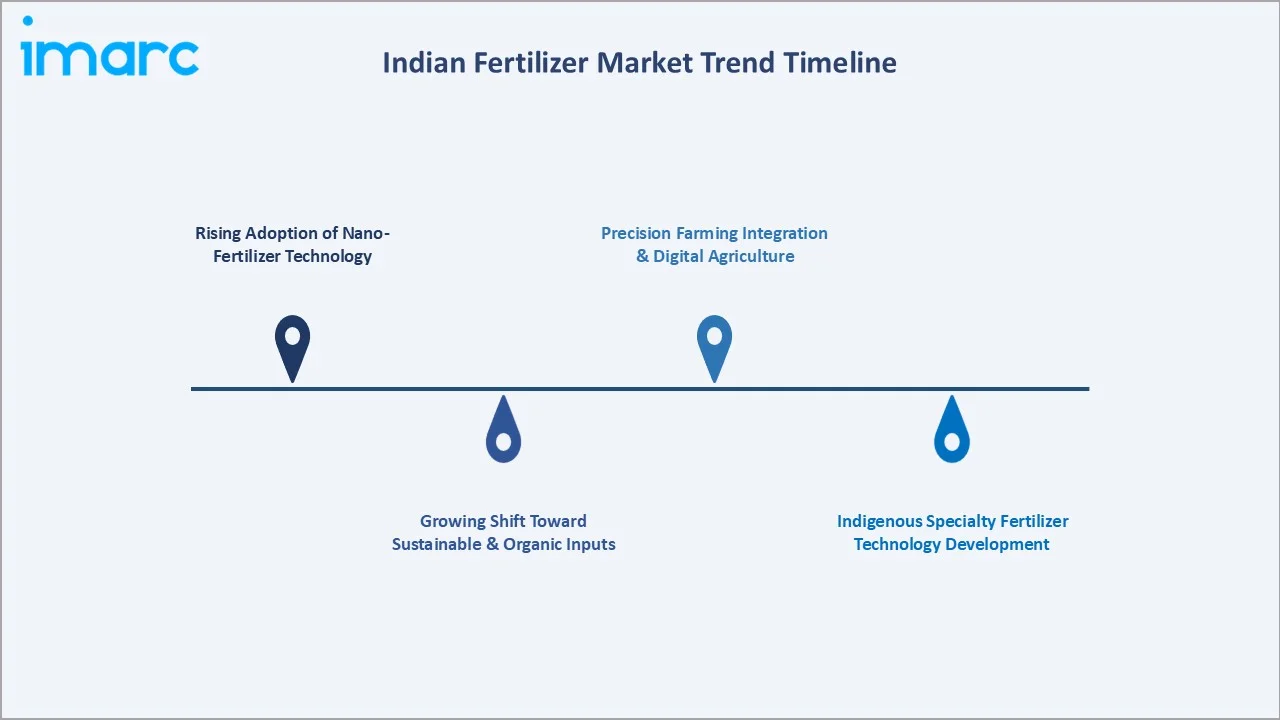

1. Rising Adoption of Nano-Fertilizer Technology

In May 2025, IFFCO expanded production by launching two new Nano DAP Liquid plants in Uttar Pradesh, churning 2 lakh bottles daily from each facility. The government is scaling nano-liquid fertilizer production to 13 plants by 2025. In December 2024, IFFCO developed Nano NPK nutrients and sought regulatory approval.

2. Growing Shift Toward Sustainable and Organic Inputs

In 2025, the Government of India launched the INR 2,481 crore National Mission on Natural Farming (NMNF) to promote eco-friendly practices across 750,000 hectares, benefiting 10 million farmers by reducing dependence on synthetic inputs and improving soil health. The PM-PRANAM policy creates financial incentives for states to reduce chemical fertilizer consumption.

3. Indigenous Specialty Fertilizer Technology Development

In August 2025, the Ministry of Mines successfully developed India's first water-soluble fertilizer technology after seven years of research, utilizing domestic raw materials. This breakthrough positions India to potentially transition from a net importer to an exporter of high-value specialty fertilizers on the global market.

4. Precision Farming Integration and Digital Agriculture

Drone-based precision fertilizer spraying is expanding rapidly, particularly for foliar application of nano-fertilizers and liquid formulations on high-value horticulture crops. IoT-enabled soil monitoring and digital agronomy platforms are being combined with satellite imagery to create variable-rate fertilizer application systems.

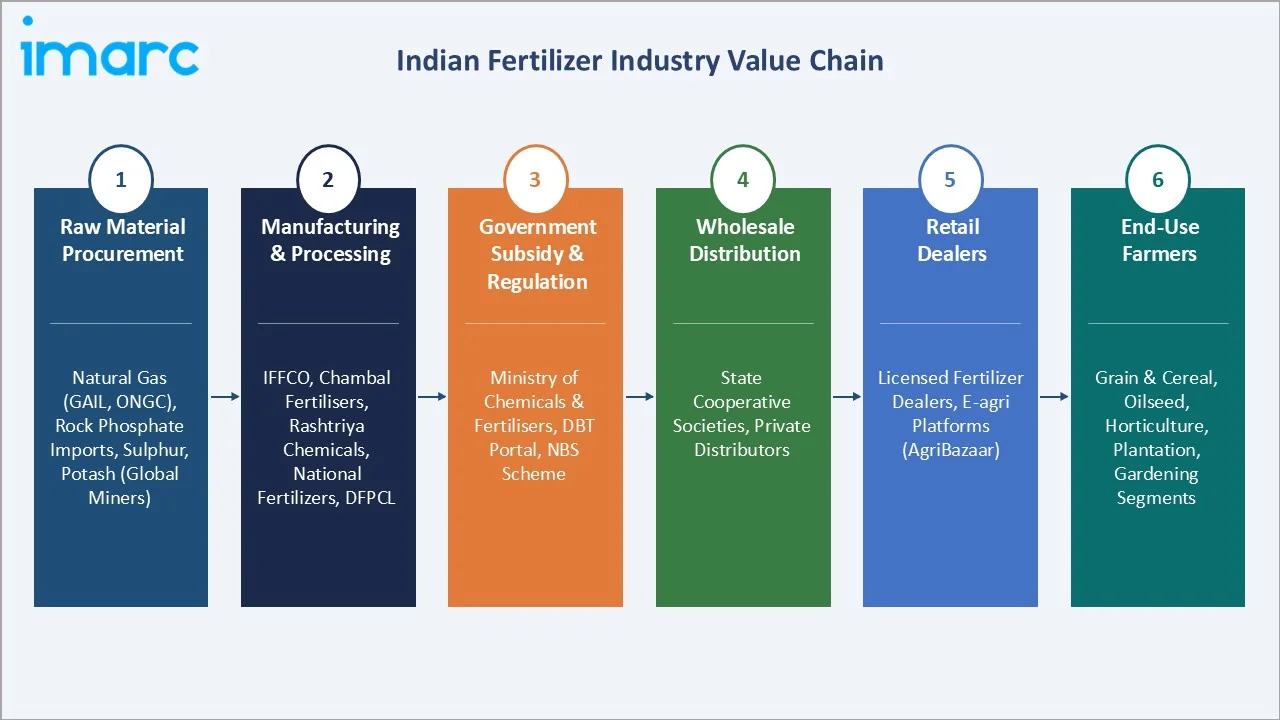

Industry Value Chain Analysis

The Indian fertilizer value chain spans raw material procurement through farm-level nutrient application, with each stage influenced by government policy, global commodity markets, and domestic agricultural demand patterns.

|

Stage |

Key Players / Examples |

|

Raw Material Procurement |

Natural gas (GAIL, ONGC), rock phosphate imports, sulphur, potash (global miners) |

|

Manufacturing & Processing |

IFFCO, Chambal Fertilisers and Chemicals Limited, Rashtriya Chemicals and Fertilizers Limited, National Fertilizers Limited, and DFPCL. |

|

Government Subsidy & Regulation |

Ministry of Chemicals & Fertilisers, DBT portal, NBS scheme administration |

|

Wholesale Distribution |

State cooperative societies, private distributors |

|

Retail Dealers |

Licensed fertilizer dealers, e-agri platforms (AgriBazaar) |

|

End-Use Farmers |

Grain & cereal, oilseed, horticulture, plantation, and gardening segments |

Technology Landscape in the Indian Fertilizer Industry

Nano-Fertilizer Production Technology

IFFCO's Nano Urea and Nano DAP plants use proprietary nano-particle synthesis technology that creates nutrient particles of 20–50 nanometers for superior foliar absorption. The technology enables a single 500ml bottle of Nano Urea to replace one bag of conventional urea for certain applications, reducing transportation costs and environmental load.

Water-Soluble and Controlled-Release Formulations

In August 2025, India's Ministry of Mines completed development of indigenous water-soluble fertilizer technology using domestic raw materials, potentially enabling India to reduce specialty fertilizer imports. Controlled-release fertilizers using polymer coatings and slow-release mechanisms are gaining adoption in horticulture and high-value crop segments.

Biofertilizer and Microbial Technology

Advanced biofertilizer formulations incorporating microbial consortia are being commercialized for improved soil health and crop nutrition. Coromandel International partnered with IFDC through a strategic research agreement to drive innovation and sustainability in fertilizer development in India. The collaboration focuses on developing next-generation fertilizers to improve nutrient efficiency, boost crop productivity, and reduce environmental impact.

Digital Soil Health and Precision Application Technology

India's Soil Health Card program has issued over 220 million cards providing crop-specific nutrient recommendations based on soil analysis. Integration of these recommendations with drone-based variable-rate fertilizer applicators and IoT soil monitoring sensors is creating precision nutrient management systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Chemical Fertilizers |

83.0% |

2025 |

|

Segment |

Urea |

40.0% |

2025 |

|

Formulation |

Dry |

77.0% |

2025 |

|

Application |

Farming |

95.0% |

2025 |

|

Region |

North India |

33.0% |

2025 |

By Product Type

Chemical fertilizers dominate the product-type segment with an 83.0% share in 2025. Their dominance reflects established use in staple crop cultivation, government subsidy support maintaining affordability, and the ability to deliver instant, predictable nutrient outcomes for productivity-focused farmers.

To access detailed market analysis, Request Sample

Biofertilizers represent 17.0% of the product-type segment in 2025, growing at a higher rate than the overall market due to government initiatives. It includes the National Mission on Natural Farming and the PM-PRANAM policy, incentivize adoption.

By Formulation

Dry formulations lead the market with a 77.0% share in 2025, reflecting the established supply chain infrastructure optimized for granular, powder, and prilled fertilizer formats. Dry formulations benefit from longer shelf life, ease of handling and storage in rural environments, compatibility with broadcast spreaders and mechanical applicators, and minimal cold-chain requirements that simplify last-mile rural distribution.

Liquid formulations hold a 23.0% share in 2025 and are the fastest-growing segment, driven by the rapid adoption of nano-liquid fertilizers (Nano Urea and Nano DAP), liquid biofertilizers, and water-soluble specialty inputs for fertigation and foliar application.

Regional Market Insights

North India's market leadership (33.0%, 2025) reflects the unmatched agricultural intensity of the Indo-Gangetic Plain, where Punjab, Haryana, and Uttar Pradesh together account for a disproportionate share of India's wheat, paddy, and sugarcane production. These states maintain the highest per-hectare fertilizer application rates nationally, with paddy and wheat cultivation driving year-round demand for urea, DAP, and NPK complexes across two to three cropping seasons annually.

|

Region |

Share (2025) |

Key Growth Drivers |

Key Characteristics |

|

North India |

33.0% |

Intensive cereal farming; wheat-paddy rotation; high urea demand |

Punjab, Haryana, UP: Indo-Gangetic Plain dominates national wheat production |

|

South India |

26.4% |

Horticulture expansion; cash crops; specialty fertilizer adoption |

Karnataka, TN, AP: coffee, banana, cotton drive specialty NPK demand |

|

West India |

22.8% |

Sugarcane, cotton, soybean farming; specialty inputs growth |

Maharashtra, Gujarat, MP: diversified cropping; drip irrigation fertigation |

|

East India |

17.8% |

Rice cultivation; growing irrigation coverage; policy expansion |

WB, Odisha, Bihar: paddy dominance; under-served distribution opportunity |

South India is the fastest-growing region at 26.4%, driven by Karnataka's coffee and horticulture sectors, Andhra Pradesh's and Telangana's expanding aquaculture-adjacent vegetable production, and Tamil Nadu's banana and sugarcane cultivation, driving demand for specialty water-soluble formulations and liquid biofertilizers.

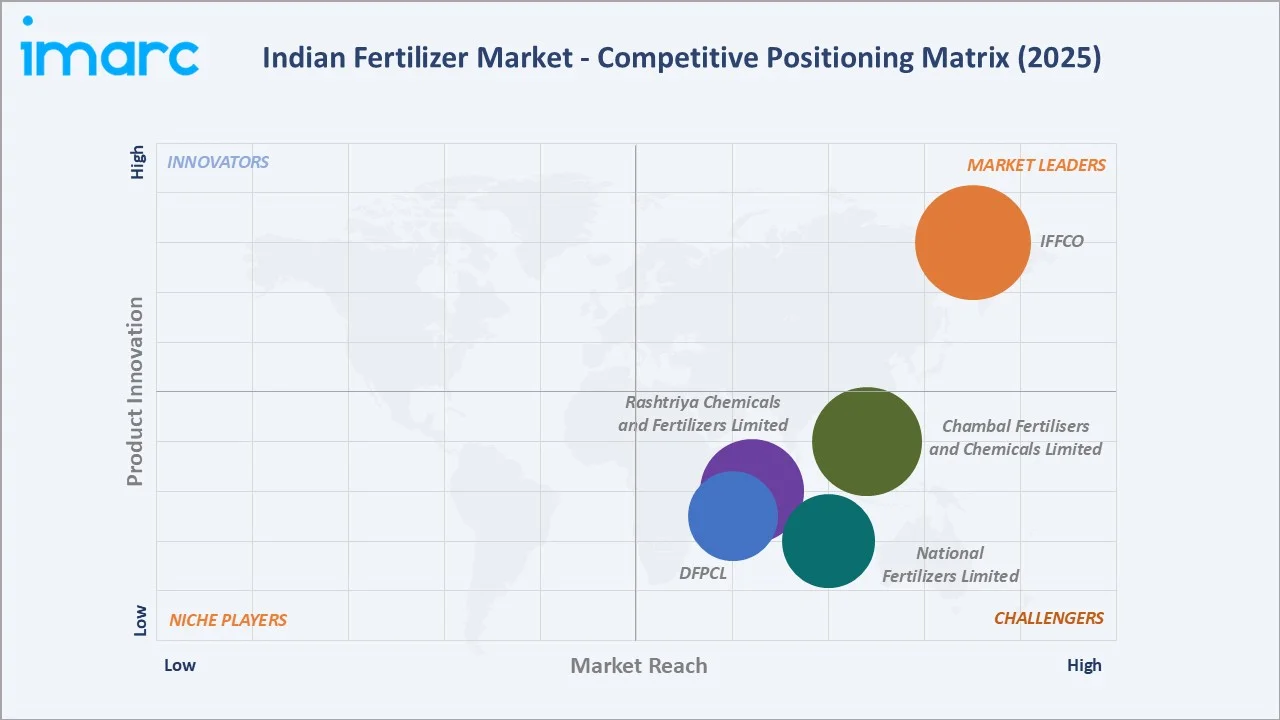

Competitive Landscape

The Indian fertilizer market exhibits a moderately concentrated competitive structure with a blend of government-owned enterprises, cooperative societies, and private manufacturers. State-owned entities and cooperatives, including IFFCO, Rashtriya Chemicals and Fertilizers Limited, National Fertilizers Limited, leverage policy backing and extensive dealer networks.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

IFFCO |

IFFCO / Nano Urea |

Market Leader |

2nd largest cooperative; nano-fertilizer innovation leader; 1k+ village network |

|

Chambal Fertilisers and Chemicals Limited |

Uttam Veer |

Strong Challenger |

Urea leader in North India; strong farmer relationship and distribution network |

|

Rashtriya Chemicals and Fertilizers Limited |

Ujjwala / Suphala |

Strong Challenger |

State-owned; cost-efficient urea and complex fertilizer manufacturing in Maharashtra |

|

National Fertilizers Limited |

Kisan |

Challenger |

Government enterprise; urea specialization; North India dealer network strength |

|

DFPCL |

Mahadhan |

Challenger |

Technical ammonium nitrate; specialty NPK; Maharashtra and South India presence |

Private manufacturers, including Chambal Fertilisers and Chemicals Limited and DFPCL., compete through operational efficiency, specialty product portfolios, and geographic market focus. The top six players collectively account for an estimated 55–60% of domestic market revenue in 2025.

Key Company Profiles

IFFCO

IFFCO is the 2nd largest cooperative, headquartered in New Delhi, operating multiple manufacturing complexes across India and holding a dominant position in urea and DAP distribution through its cooperative network of over 36,000 member primary agricultural cooperative societies.

- Product Portfolio: Urea, DAP, NPK complexes, Nano Urea, Nano DAP, liquid biofertilizers, and nano micronutrients, including Nano Zinc and Nano Copper products.

- Recent Developments: In October 2023, IFFCO launched the world’s first Nano DAP (liquid) plant in Kalol, Gujarat, with a production capacity of 2 lakh 500 ml bottles per day, each equivalent to a conventional 45 kg DAP bag.

- Strategic Focus: Nano-fertilizer manufacturing scale-up; biofertilizer product expansion; cooperative digital platform development; export market entry for nano products.

National Fertilizers Limited

National Fertilizers Limited is a Central Public Sector Enterprise under the Ministry of Chemicals and Fertilizers, headquartered in Noida. It operates five gas-based Ammonia-Urea plants viz Nangal & Bathinda in Punjab, Panipat in Haryana, and two plants at Vijaipur (Madhya Pradesh), and a Bio-fertilizers plant in Vijaipur. The company is a significant urea and neem-coated urea producer serving North India's agricultural markets.

- Product Portfolio: Urea, neem-coated urea (Kisan Urea), and agricultural inputs marketed under the Kisan brands.

- Recent Developments: In April 2025, National Fertilizers Limited announced participation in a joint venture to establish the Namrup IV Fertilizer Plant (Ammonia-Urea Complex) in Assam, holding 18% equity stake to expand northeastern India production capacity.

- Strategic Focus: Capacity expansion in northeastern India; neem-coated urea growth; energy efficiency improvement; sustainability-aligned manufacturing.

Chambal Fertilisers and Chemicals Limited

Chambal Fertilisers, is one of India's largest private urea manufacturers, with its registered office is at Gadepan, Kota, Rajasthan; its corporate office is at Jasola, New Delhi. The company is a leading fertilizer brand across the northern and central Indian agricultural belt.

- Product Portfolio: Urea (Uttam Veer Urea), DAP, complex NPK fertilizers, specialty fertilizers, and agri-inputs including seeds and crop protection products under the Uttam brand.

- Recent Developments: Expanded specialty fertilizer and biofertilizer product lines to meet growing demand for balanced nutrient inputs.

- Strategic Focus: Urea production efficiency leadership; specialty fertilizer portfolio expansion; North India farmer relationship deepening through direct digital marketing.

Market Concentration Analysis

The Indian fertilizer market exhibits moderate-to-high concentration at the manufacturing level, with state-owned enterprises and IFFCO holding structural advantages through policy alignment, subsidy access, and distribution network scale. The top six manufacturers, IFFCO, Chambal Fertilisers and Chemicals Limited, Rashtriya Chemicals and Fertilizers Limited, National Fertilizers Limited, and DFPCL., collectively account for approximately 55–60% of domestic market revenue in 2025.

Consolidation activity is influenced by government disinvestment policy, cooperative restructuring, and private equity interest in specialty fertilizer segments. The specialty fertilizer segment, encompassing water-soluble, controlled-release, and biofertilizer products, is more fragmented and innovation-driven, attracting new entrants. The February 2025 National Fertilizers Limited joint venture for the Namrup IV plant and December 2025 Oil India-Assam government fertilizer plant formation signal ongoing capacity investment that will shape the competitive map through the forecast period.

Investment & Growth Opportunities

Fastest Growing Segments

Nano-fertilizers (CAGR 4.28% through 2034), liquid biofertilizers (CAGR ~8%), and specialty water-soluble formulations represent the three highest-growth investment vectors through 2034. Together, these premium segments address an incremental market opportunity of approximately INR 180–220 Billion by 2030, driven by government policy mandates, precision farming adoption, and farmer willingness to pay for demonstrably higher efficiency products.

Emerging Market Expansion

East India and Central India represent the most under-penetrated domestic geographies, with Bihar, Jharkhand, and Chhattisgarh showing strong growth potential as irrigation coverage expands and government agricultural input programs intensify. The INR 2,481 crore National Mission on Natural Farming creates co-investment opportunities for biofertilizer manufacturers in states transitioning toward natural farming. The Namrup IV Assam plant and Assam Valley Fertilizer initiative signal Northeast India as an emerging manufacturing and distribution growth zone.

Venture and Institutional Investment Trends

- Key investment themes include indigenous water-soluble fertilizer technology commercialization, nano-fertilizer manufacturing capacity expansion, biofertilizer product portfolio development, and digital agronomy platform integration with precision nutrient delivery.

- The government's AVGC-analogous agricultural input modernization budget and NBS policy framework create predictable policy-backed demand for innovative fertilizer products, reducing investment risk for specialty formulation manufacturers.

Future Market Outlook (2026-2034)

The Indian fertilizer market is positioned for steady, policy-supported growth through 2034. From a base of USD 11.35 Billion in 2025, the market is projected to reach USD 22.78 Billion by 2034, representing total incremental value creation of approximately USD 412.3 Billion over the forecast decade.

Policy evolution, particularly the operationalization of the National Mission on Natural Farming and the NBS framework's continued shift toward balanced nutrient application, will drive significant product portfolio transformation. Manufacturers achieving commercially viable biofertilizer and nano-fertilizer portfolios with government subsidy integration by 2026 are positioned to capture a disproportionate share of incremental market revenue.

Long-term, the Indian fertilizer market trends are tied to three structural macro-themes: food security imperatives requiring sustained productivity growth from finite arable land, sustainability transition mandating reduced chemical nutrient intensity and adoption of biological alternatives, and digital agriculture infrastructure enabling precision nutrient management at scale.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with industry participants in 2024–2025, including fertilizer manufacturers, agricultural cooperative officials, government subsidy administrators, fertilizer dealers, agricultural extension officers, and end-user farmers across North, South, West, and East India.

Secondary Research

Secondary research encompassed a systematic review of Ministry of Chemicals and Fertilizers publications, Fertiliser Association of India data, Department of Agriculture crop production statistics, NBS policy documentation, industry databases, and trade publications. Key sources included government annual reports on fertilizer subsidy outflows, IFFCO cooperative publications, and specialized agricultural input market analytics.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating agricultural GDP growth rates, cropped area expansion, per-hectare fertilizer consumption trends, and government subsidy policy trajectories. A base-case CAGR of 3.84% reflects consensus analyst estimates validated against reported manufacturer revenue growth and government fertilizer offtake data.

Indian Fertilizer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | USD Billion, 000’ Metric Tons |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Chemical Fertilizers, Biofertilizers |

| Segments Covered | Complex Fertilizers, DAP, MOP, Urea, SSP, Others |

| Formulations Covered | Liquid, Dry |

| Applications Covered |

|

| Regions Covered | East India, North India, South India, West India |

| Companies Covered | IFFCO, Chambal Fertilisers and Chemicals Limited, Rashtriya Chemicals and Fertilizers Limited, National Fertilizers Limited, DFPCL, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Fertilizer Market Report

The Indian fertilizer market size was valued at USD 11.35 Billion in 2025. It is projected to reach USD 22.78 Billion by 2034, growing at a CAGR of 3.84% during the forecast period of 2026-2034.

The Indian fertilizer market is expected to grow at a CAGR of 3.84% during the forecast period from 2026-2034, supported by government subsidy programs, rising agricultural productivity demands, nano and biofertilizer innovation, and precision farming adoption.

North India leads the market with a 33.0% revenue share in 2025, driven by the intensive cereal-farming belt of the Indo-Gangetic Plain across Punjab, Haryana, and Uttar Pradesh, where wheat-paddy rotation sustains high per-hectare fertilizer application across multiple cropping seasons.

Chemical fertilizers dominate the product-type segment with an 83.0% share in 2025. Their dominance is driven by government subsidy support, widespread use in staple crop cultivation, and ability to deliver instant, predictable nutrient results across diverse agro-climatic conditions.

Dry formulations lead the market at 77.0% in 2025, preferred for ease of storage, handling, and broad compatibility with existing distribution infrastructure and farm mechanization equipment across India's diverse agricultural geographies.

Key drivers include government subsidy programs, rising food security demand requiring higher agricultural productivity, nano-fertilizer innovation by IFFCO and Coromandel, precision farming adoption, the National Mission on Natural Farming, and indigenous water-soluble fertilizer technology development.

Key players include IFFCO, Chambal Fertilisers and Chemicals Limited, Rashtriya Chemicals and Fertilizers Limited, National Fertilizers Limited, and DFPCL.

Key challenges include nutrient imbalance and soil degradation from urea-heavy application patterns, import dependency for phosphoric acid and potash raw materials, subsidy payment delays creating manufacturer working capital pressure, last-mile distribution complexity for biofertilizers, and farmer behavioral transition barriers toward balanced nutrient management.

Significant opportunities exist in nano-fertilizer manufacturing capacity expansion, biofertilizer and organic input product development, indigenous water-soluble fertilizer technology commercialization, digital precision farming platform integration, and specialty fertilizer distribution in under-penetrated East India and Northeast India geographies through the forecast period.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)