Indian Frozen Foods Market Size, Share, Trends and Forecast by Product Type, 2026-2034

Indian Frozen Foods Market Size and Share (2026-2034)

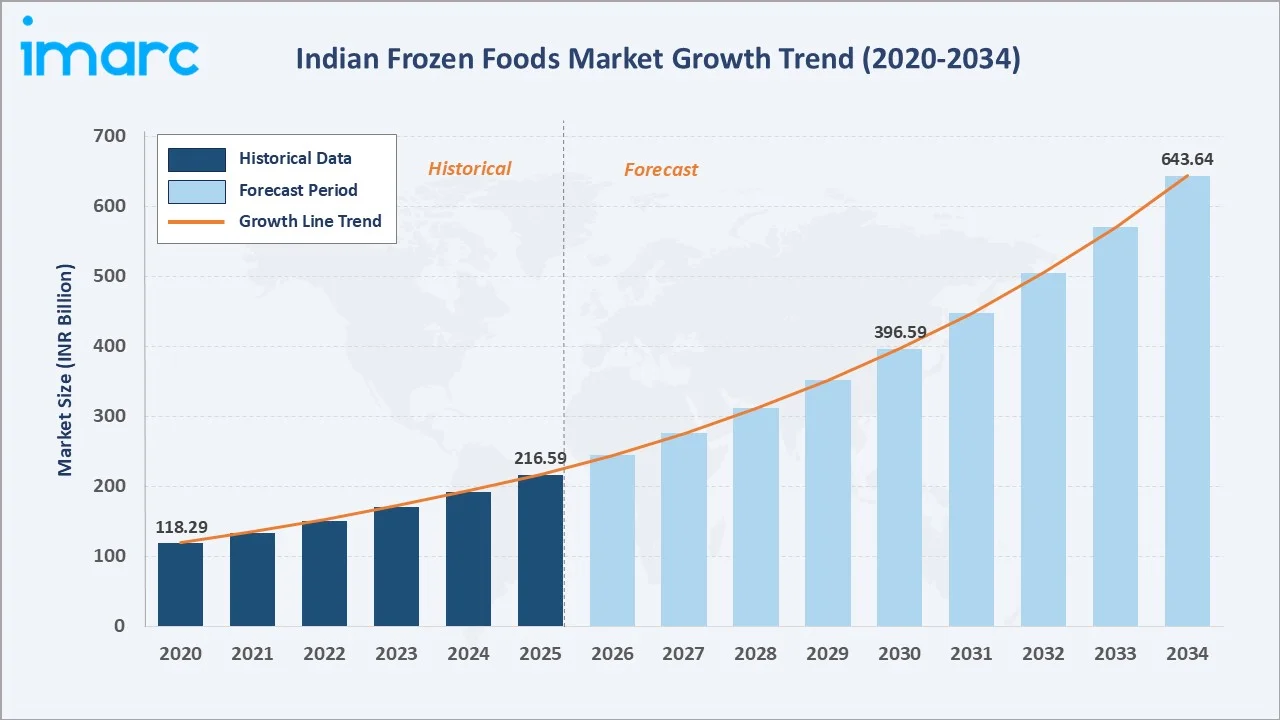

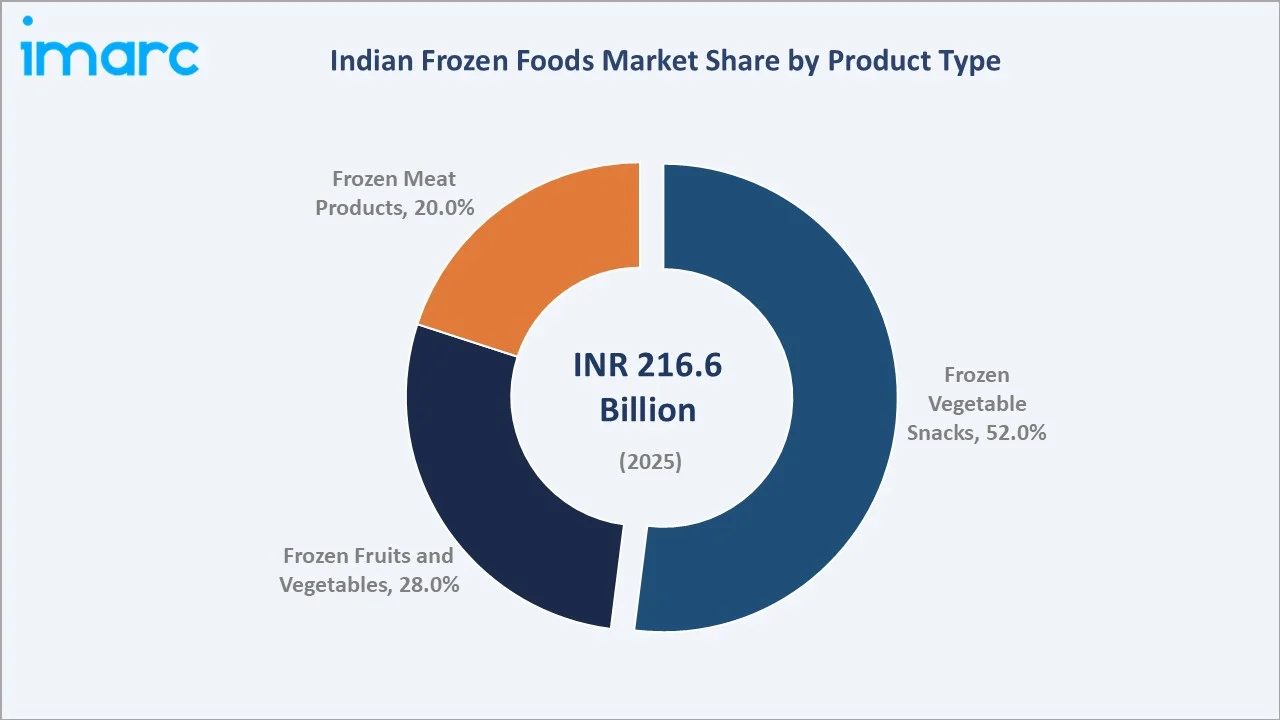

The Indian frozen foods market size was valued at INR 216.59 Billion in 2025 and is projected to reach INR 643.64 Billion by 2034, exhibiting a CAGR of 12.86% during the forecast period 2026-2034. Rapid urban transformation in consumer eating habits, rising disposable incomes, and significant improvements in cold chain infrastructure are driving the Indian frozen foods market growth. Frozen Vegetable Snacks lead the product type segment at 52.0% in 2025, while North India commands approximately 32% of national revenue, the country's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 216.59 Billion |

|

Forecast Market Size (2034) |

INR 643.64 Billion |

|

CAGR (2026-2034) |

12.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Product Segment |

Frozen Vegetable Snacks (52.0%, 2025) |

To get more information on this market, Request Sample

Executive Summary

The Indian frozen foods market is undergoing a fundamental transformation driven by accelerating urbanisation, improving cold chain infrastructure, rising dual-income households, and rapid digitisation of food retail through quick-commerce platforms. Valued at INR 216.59 Billion in 2025, the market is forecast to reach INR 643.64 Billion by 2034 at a CAGR of 12.86%. The Pradhan Mantri Kisan SAMPADA Yojana approved 372 integrated cold chain projects generating over 2.23 lakh jobs and 38 million metric tons of additional cold storage capacity — a transformational infrastructure push directly catalysing the Indian frozen foods market outlook across the country's diverse geographies.

Frozen Vegetable Snacks command the dominant product-type share at 52.0% in 2025, reflecting India's evolving health consciousness and plant-based snacking momentum. Frozen Fruits and Vegetables follow at 28.0%, benefiting from export-led demand and growing modern retail penetration, while Frozen Meat Products account for 20.0%, driven by rising protein consumption among urban middle-class households.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Frozen Vegetable Snacks – 52.0% share (2025) |

|

Second Largest Segment |

Frozen Fruits & Vegetables – 28.0% share (2025) |

|

Third Largest Segment |

Frozen Meat Products – 20.0% share (2025) |

|

Top Companies |

McCain India, Mother Dairy Safal, Venky's, Sumeru, Godrej Tyson |

Key Analytical Observations Supporting the Above Data:

- Frozen Vegetable Snacks' 52.0% dominance reflects India's deep-rooted vegetarian food culture, health-forward snacking trends, and widespread popularity of frozen potato-based products across QSR and household channels.

- Frozen Fruits & Vegetables at 28.0% are anchored by growing export demand — India exported 17,81,602 MT of seafood worth ₹60,523.89 crore in 2023–24 — and rising adoption in organised food service and modern retail.

- North India's regional leadership reflects India's largest food processing industrial clusters in Punjab, Haryana, and Uttar Pradesh, combined with the NCR's dense urban consumer base and deep modern trade penetration.

Indian Frozen Foods Market Overview

Frozen foods encompass a broad range of products preserved through rapid freezing technologies — individual quick freezing (IQF), blast freezing, and plate freezing — that extend shelf life, maintain nutritional quality, and deliver convenience across diverse consumer segments. The Indian frozen foods market encompasses frozen vegetable snacks (French fries, nuggets, aloo tikki, bites and wedges), frozen fruits and vegetables (green peas, corn, mixed vegetables, tropical fruits), and frozen meat products (poultry, seafood, and processed meat formats).

Applications span urban and semi-urban households seeking convenient meal solutions, food service establishments (HoReCa), institutional buyers including hospitals and corporate canteens, and the export-oriented seafood and processed vegetable sector. India's geographic diversity — northern wheat-belt agricultural surplus, southern vegetable-growing clusters, and coastal seafood belts — creates a structurally advantaged raw material base. Macroeconomic enablers include India's urban population reaching approximately 36% of total population, rising GDP per capita enabling premium food expenditure, and the PMKSY programme establishing 37 million metric tons of cold storage capacity nationally by 2024.

Market Dynamics

To evaluate market opportunities, Request Sample

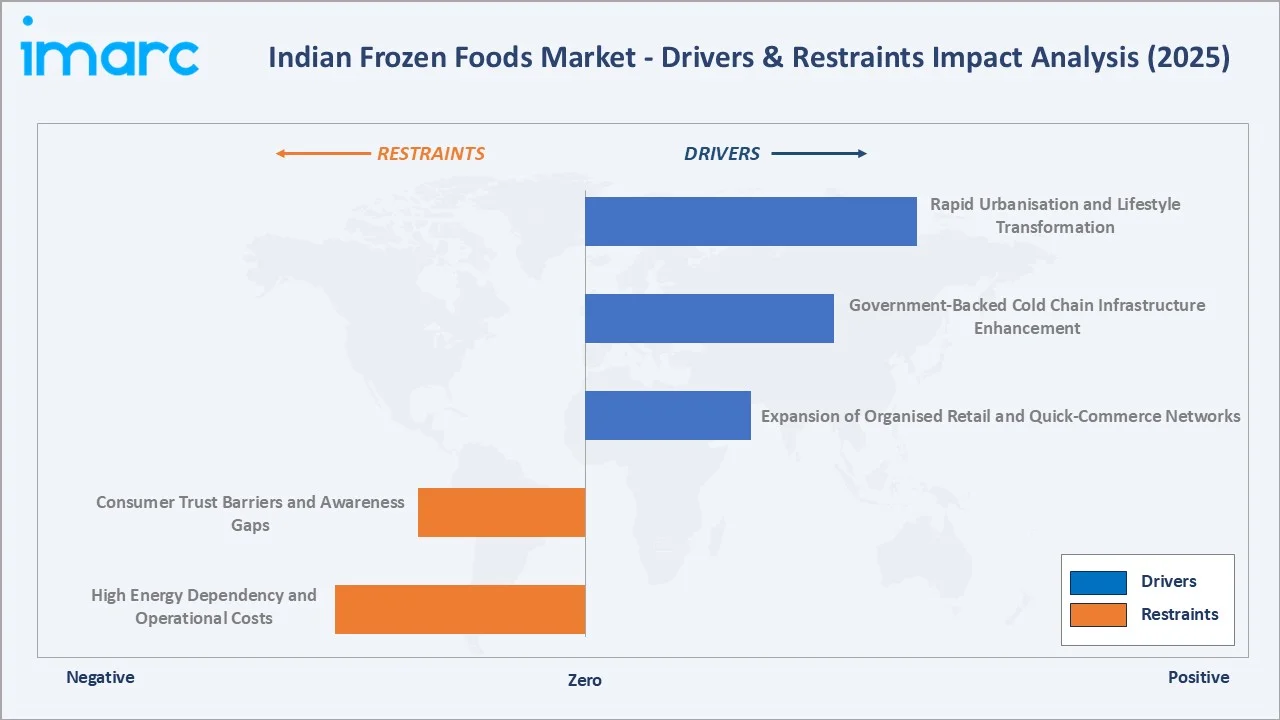

Market Drivers

- Rapid Urbanisation and Lifestyle Transformation: India's urban population, representing approximately 36% of total population in 2025, has created unprecedented demand for convenient meal solutions. Nuclear family formation, rising female workforce participation, and demanding professional schedules are converting frozen foods from a niche segment into a mainstream daily consumption category across Tier-I and Tier-II cities nationally.

- Government-Backed Cold Chain Infrastructure Enhancement: The Pradhan Mantri Kisan SAMPADA Yojana's Integrated Cold Chain and Value Addition Infrastructure Scheme approved 372 projects creating over 38 million metric tons of cold storage capacity and 2.23 lakh jobs. Ministry of Food Processing Industries subsidies and GST rationalization for food processors have stimulated supply-side investment, enabling broader geographic penetration of frozen products.

- Expansion of Organised Retail and Quick-Commerce Networks: Modern retail formats operated by Reliance Retail and D-Mart drive frozen food visibility through dedicated freezer sections. Blinkit targeted 1,000 dark stores by end-FY25 while operating 639 stores as of June 2024, with Swiggy Instamart and Big Basket aggressively expanding 10–30 minute cold-chain-enabled delivery capabilities across major Indian cities.

Market Restraints

- High Energy Dependency and Operational Costs: Frozen storage maintained below -18°C requires approximately 69.4 kWh per cubic meter annually, creating substantial operating cost pressures. Cold chain logistics representing 30–40% of total frozen food operating costs compress margins, particularly for mid-size regional processors competing against multinationals with greater economies of scale.

- Consumer Trust Barriers and Awareness Gaps: Significant rural and semi-urban consumer segments continue to exhibit preference for fresh produce over frozen alternatives, driven by cultural practices, scepticism regarding preservatives, and limited cold chain exposure. Sustained investment in consumer education and transparent food labelling is required to overcome these adoption barriers.

Market Opportunities

- Plant-Based and Health-Focused Frozen Product Innovation: India's vegan food market is projected by IMARC Group to reach USD 3,823.93 Million by 2034, creating substantial opportunity for processors to expand into millet-based nuggets, plant-based meat alternatives, and protein-enriched frozen snacks tailored to health-conscious urban consumers seeking nutritious convenience food options.

- Export Market Expansion in Frozen Vegetables and Seafood: India's seafood export — 17,81,602 MT valued at ₹60,523.89 crore (USD 7.38 billion) in 2023–24 — demonstrates competitive positioning as a global frozen food exporter. Expanding IQF vegetable processing capacity targeting Europe, the Middle East, and the United States represents significant revenue diversification potential for Indian processors.

Market Challenges

- Cold Chain Fragmentation and Last-Mile Logistics: India's cold chain infrastructure remains fragmented in rural geographies, with inadequate refrigerated transport connectivity creating temperature excursion risks that constrain market expansion beyond urban centres and represent the critical bottleneck requiring public-private investment collaboration.

- Regulatory Compliance Complexity: FSSAI's evolving product standards, mandatory labelling requirements, and category-specific compliance obligations create ongoing cost burdens for frozen food manufacturers, particularly smaller regional processors lacking dedicated regulatory affairs capabilities across product categories.

Emerging Market Trends

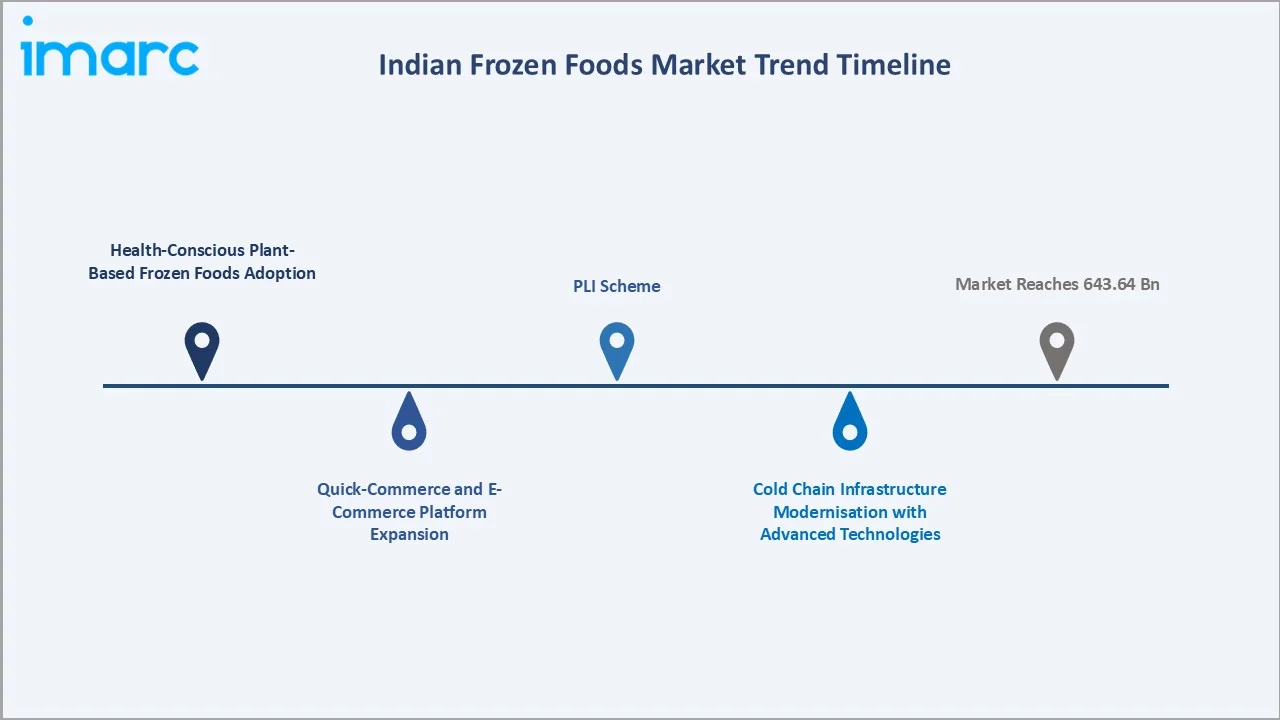

1. Health-Conscious Plant-Based Frozen Foods Adoption

Consumer preferences across urban India are shifting markedly toward nutritious, plant-based frozen alternatives as health and wellness awareness intensifies. Major food processors are launching products incorporating protein-rich, gluten-free, and organic ingredients specifically tailored to Indian palates. The plant-based frozen snack category is gaining momentum with millet-based nuggets and vegetable meat alternatives entering organised retail and quick-commerce channels. This transformation reflects growing awareness of environmental sustainability driving plant-rich dietary adoption, while social media-driven foodie culture expands consumer exposure to diverse, health-forward frozen options. IMARC Group projects the India vegan food market will reach USD 3,823.93 Million by 2034, validating the substantial growth trajectory for plant-based frozen food innovation through the forecast period as consumer health consciousness becomes a mainstream product development driver shaping the Indian frozen foods market trends for years ahead.

2. Quick-Commerce and E-Commerce Platform Expansion

Digital retail channels are fundamentally reshaping frozen food accessibility through cold-chain-enabled last-mile delivery networks maintaining product integrity during 10–30 minute delivery windows. Blinkit targeted 1,000 dark stores by end-FY25, while Swiggy Instamart and Big Basket aggressively expand micro-fulfilment infrastructure in Tier-I and Tier-II cities. Online grocery platforms reported substantial frozen food order growth during 2024, with particular demand intensity for frozen snacks and bakery categories. Quick-commerce operators leverage real-time temperature monitoring, IoT-enabled inventory management, and expanding dark store networks to make frozen foods viable for impulse purchase occasions previously dominated by ambient food categories. This channel transformation represents the most disruptive distribution evolution reshaping the Indian frozen foods market forecast trajectory, driving incremental volume growth and new consumer acquisition across India's diverse urban geography through 2034.

3. Cold Chain Infrastructure Modernisation with Advanced Technologies

Technological advancement in India's cold chain logistics is fundamentally transforming market economics by ensuring product quality, extending shelf life, and enabling broader geographic penetration. Cold storage capacity reached over 37 million metric tons nationally by 2024, supported by IoT-based temperature monitoring, GPS-enabled refrigerated transport tracking, and automated multi-temperature warehousing. State-of-the-art facilities are enhancing delivery efficiency while maintaining optimal cold chain conditions throughout the supply network. Advanced packaging technologies including modified atmosphere packaging and temperature-indicator smart labels are enhancing consumer confidence in frozen product safety, creating a virtuous cycle of trust-building and consumption growth that underpins the long-term Indian frozen foods market growth trajectory through the forecast period to 2034.

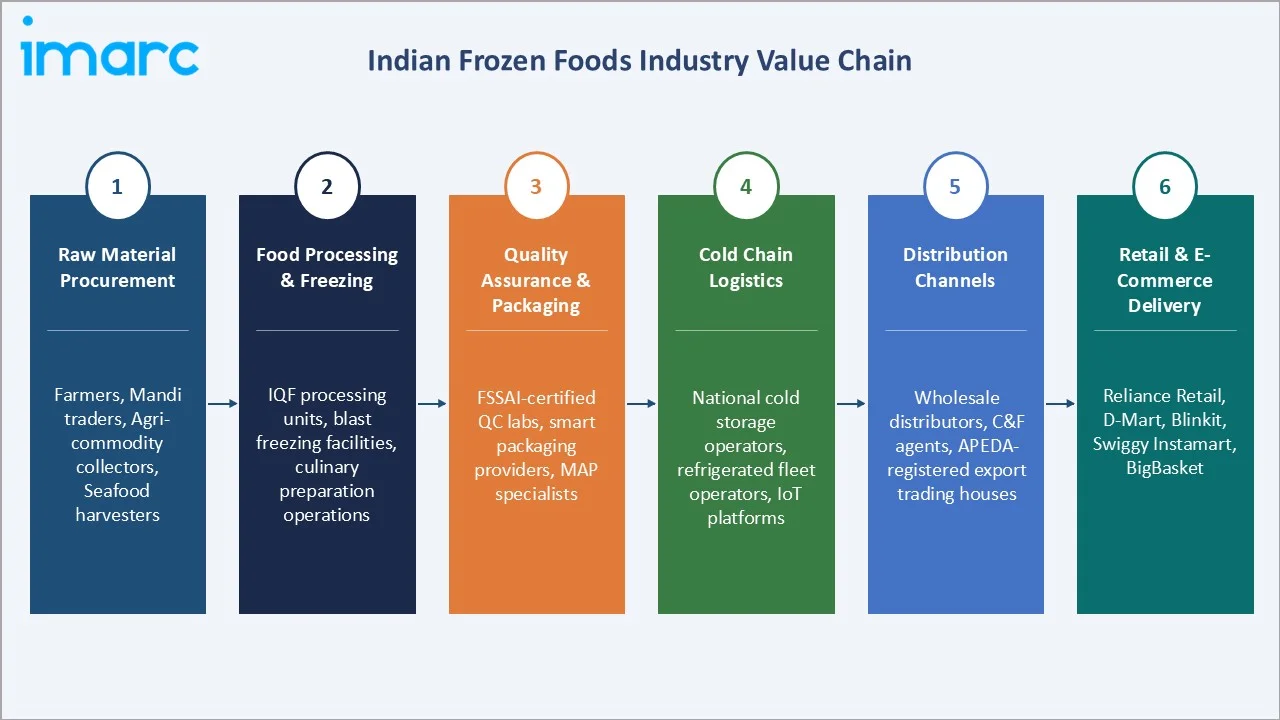

Industry Value Chain Analysis

The Indian frozen foods value chain spans six integrated stages from agricultural raw material procurement through end-consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and cold chain investment requirements critical to the health of the overall market ecosystem.

|

Stage |

Key Players / Examples |

|

Raw Material Procurement |

Farmers, Mandi traders, Agri-commodity collectors, Seafood harvesters (coastal states) |

|

Food Processing & Freezing |

IQF processing units, blast freezing facilities, culinary preparation and blending operations |

|

Quality Assurance & Packaging |

FSSAI-certified QC labs, smart packaging providers, modified atmosphere packaging specialists |

|

Cold Chain Logistics |

National cold storage operators (NCCDs), refrigerated fleet operators, IoT temperature monitoring platforms |

|

Distribution Channels |

Wholesale distributors, C&F agents, APEDA-registered export trading houses |

|

Retail & E-Commerce Delivery |

Supermarkets (Reliance Retail, D-Mart), quick-commerce (Blinkit, Swiggy Instamart), BigBasket, food service distributors |

Food processors and cold chain logistics operators occupy the highest strategic value positions in the Indian frozen foods value chain. IQF and blast-freezing technology operators differentiate on quality, throughput, and product consistency, while cold chain providers determine geographic reach and market accessibility of frozen products. IoT-enabled temperature monitoring at every node represents the critical technology investment underpinning consumer trust and FSSAI regulatory compliance across the national supply network.

Technology Landscape in the Indian Frozen Foods Industry

Individual Quick Freezing (IQF) Technology Leadership

IQF technology represents the gold standard for premium frozen vegetable, fruit, and meat products, freezing individual pieces at ultra-low temperatures of -35°C to -40°C within 30 minutes to preserve cellular structure, colour, nutritional content, and natural texture. Indian processors are increasingly investing in continuous IQF tunnel freezers replacing older batch-processing blast freezers, reducing energy consumption by 20–30% while improving throughput and product quality consistency. IQF adoption is directly enabling premium product positioning and export market competitiveness for Indian frozen food manufacturers targeting quality-sensitive European and Middle Eastern consumers seeking superior nutritional integrity.

Cold Chain Digitisation and IoT Integration

Real-time IoT-based temperature monitoring across cold storage and refrigerated transport networks is transforming supply chain reliability and FSSAI compliance capabilities. GPS-enabled refrigerated vehicle tracking, automated cold room temperature logging, and cloud-based cold chain analytics platforms provide end-to-end visibility from processing facility to retail shelf. National Centre for Cold Chain Development (NCCD) programmes are promoting IoT adoption through subsidy frameworks that accelerate technology uptake among mid-size cold chain operators, reducing spoilage rates and strengthening product safety assurances across India's geographically diverse distribution network.

Smart Packaging Innovations

Advanced packaging technologies are enhancing both product quality preservation and consumer engagement in the Indian frozen foods market. Modified atmosphere packaging (MAP) extending shelf life by displacing oxygen with protective gas blends, microwave-safe convenience packaging enabling direct-from-pack cooking, and temperature-indicator labels providing consumer-visible quality assurance are gaining adoption across premium product tiers. Bio-based and recyclable packaging materials are emerging as strategic priorities among brands targeting sustainability-conscious urban consumers, aligning frozen food product innovation with broader environmental responsibility objectives increasingly valued by India's millennial and Gen-Z consumer cohorts.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Frozen Vegetable Snacks |

52% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Frozen Vegetable Snacks command a leading 52.0% market share in 2025, underpinned by India's predominantly vegetarian food culture, intensifying health and wellness trends, and the deep popularity of potato-based frozen snacks across all income segments. The category encompasses French fries, nuggets, aloo tikki, bites, wedges, and smileys — products with universal appeal across household, quick-service restaurant, and institutional food service channels. Product innovation incorporating protein-rich ingredients, millet bases, and reduced-sodium formulations is expanding the health-conscious consumer segment within this leading category, driving premiumisation and higher average selling prices across modern retail and quick-commerce platforms.

Frozen Fruits and Vegetables hold a 28.0% market share in 2025, supported by growing export demand for green peas, corn, and mixed vegetables, rising adoption in food service, and expanding modern retail availability. The segment benefits from India's diverse agricultural production base and government-supported processing infrastructure.

Frozen Meat Products account for 20.0%, driven by rising protein consumption awareness, expanding poultry and seafood processing capacity, and increasing acceptance of frozen meat formats among non-vegetarian consumer households in South and East India, supported by improving cold chain reach and branded product availability.

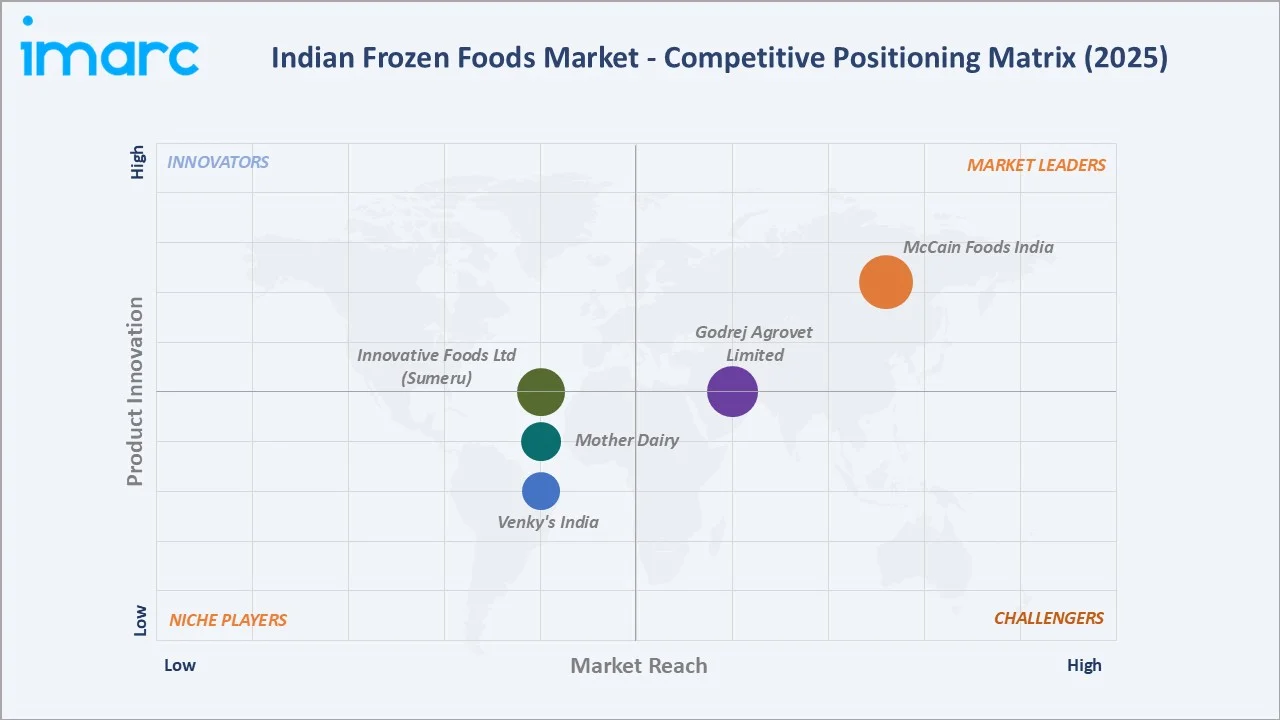

Competitive Landscape

|

Company Name |

Key Brand / Product |

Market Position |

Core Strength |

|

McCain Foods (India) Private Limited |

McCain French Fries, Aloo Tikki, Smileys |

Leader |

Premium frozen potato; QSR supply chain; global IQF platform |

|

Mother Dairy Fruit & Vegetable Pvt. Ltd. |

Safal Frozen Vegetables & Peas |

Leader |

Pan-India brand trust; cooperative sourcing; cold chain network |

|

Venky's India |

Venky's Frozen Poultry Products |

Leader |

Vertical integration in poultry; South & West India strength |

|

Innovative Foods Ltd (Sumeru) |

Sumeru Frozen Seafood & Vegetables |

Challenger |

Seafood processing expertise; HoReCa distribution; export focus |

|

Godrej Agrovet Limited |

Yummiez Frozen Snacks & Chicken |

Challenger |

Modern retail distribution; brand investment; product innovation |

Key Company Profiles

McCain Foods (India) Private Limited

McCain India, the Indian subsidiary of McCain Foods Limited (Canada), is the dominant player in the Indian frozen potato snacks segment, supplying both retail consumers and quick-service restaurant chains across north and south India. McCain's vertically integrated operations — from contract potato farming in Gujarat, Punjab, and Karnataka to IQF processing, cold chain distribution, and retail branded sales — provide unmatched cost and quality control in the premium frozen snacks segment.

- Product Portfolio: French fries, aloo tikki, bites, wedges, smileys, hash browns, and plant-based frozen snacks.

- Strategic Focus: QSR channel leadership, retail brand premiumisation, sustainable potato sourcing, and expansion of plant-based offerings for health-conscious urban consumers seeking nutritious frozen snacking alternatives.

- Recent Developments: In September 2025, McCain Foods announced plans to set up Madhya Pradesh’s largest food processing plant with a total investment of INR 4,000 crore (USD 480 million), aimed at strengthening the state’s industrial and agricultural ecosystem.

The project will be developed in three phases, with Phase 1 attracting INR 1,500–1,800 crore, followed by Phase 2 and Phase 3 investments of INR 1,000 crore each.

Mother Dairy Fruit & Vegetable Pvt. Ltd.

Mother Dairy's Safal brand is India's most trusted frozen vegetable brand, leveraging a cooperative-backed sourcing model procuring directly from farmer producer organisations across Punjab, Haryana, and Himachal Pradesh for frozen peas, corn, mixed vegetables, and tropical fruits distributed nationally.

- Product Portfolio: Frozen peas, corn, mixed vegetables, spinach, and a range of frozen fruits targeting modern retail and e-commerce channels across India.

- Strategic Focus: Pan-India cold chain distribution strengthening, cooperative farmer integration, e-commerce channel expansion, and premium organic frozen vegetable range development for health-conscious urban families.

- Recent Developments: In March 2025, Mother Dairy announced an investment of around Rs 600 crore to set up two new fruit and vegetable processing plants in Gujarat and Andhra Pradesh, strengthening its food processing footprint. The company will allocate over Rs 400 crore for a facility at Itola near Baroda, Gujarat, with construction expected to be completed within two years.

Godrej Agrovet Limited

Godrej Tyson Foods, a joint venture between Godrej Agrovet and Tyson Foods (USA), markets the Yummiez brand of frozen snacks, chicken products, and ready-to-cook items targeting modern retail, e-commerce, and food service channels with branded, innovation-driven product launches appealing to India's millennial and Gen-Z consumer cohorts seeking convenient premium frozen food options.

- Product Portfolio: Frozen chicken nuggets, tenders, kebabs, burger patties, and vegetarian frozen snacks under the Yummiez brand with an expanding SKU range.

- Strategic Focus: Brand investment in modern trade and digital channels, product innovation targeting Gen-Z and millennial consumers, and expansion of value-added chicken product ranges across India's growing organised food retail network.

- Recent Developments: In February 2024, Godrej Yummiez, a brand of frozen ready-to-cook products from Godrej Tyson Foods Limited (GTFL) expanded its non-veg portfolio with the launch of Yummiez Crispy Fried Chicken and Yummiez Crispy Chicken Bites, strengthening its ready-to-cook offerings in India.

Market Concentration Analysis

The Indian frozen foods market exhibits moderate-to-high competitive concentration among the top five to six nationally distributed brands, with McCain India, Mother Dairy Safal, and Venky's collectively accounting for an estimated 45–55% of organised market revenue in 2025. The market operates across three distinct competitive tiers: (1) multinational corporations with global technology platforms and premium product positioning; (2) domestic vertically integrated processors with cooperative or farmer-linked supply chains; and (3) regional specialists serving specific export, halal, or geographic segments.

Quick-commerce platform growth is accelerating premiumisation by enabling branded players to reach consumers previously served only by unorganised traders, gradually shifting market concentration toward organised players. The entry of retail private-label frozen food ranges by Reliance Retail and BigBasket adds a competitive dynamic combining scale distribution with price-point accessibility targeting value-seeking urban consumers while maintaining modern retail quality standards.

Investment & Growth Opportunities

Fastest-Growing Segments

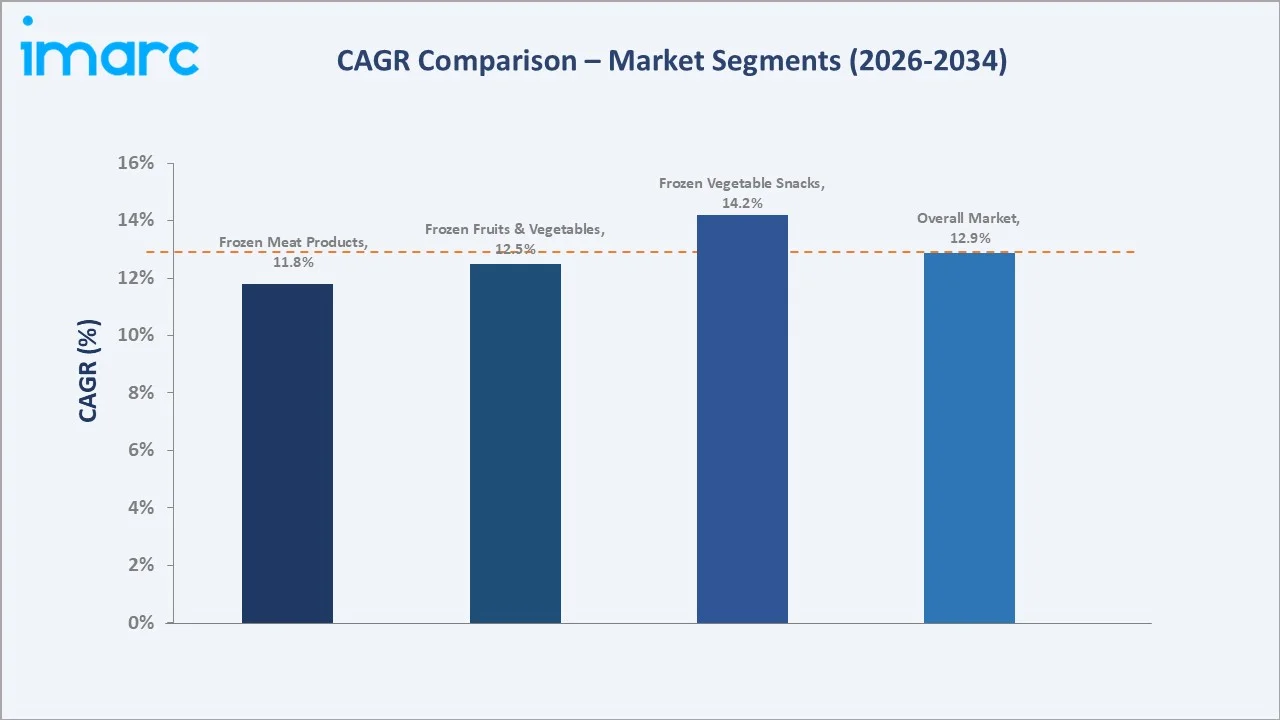

Frozen Vegetable Snacks remain the highest-volume growth product segment at an estimated 14.2% CAGR, driven by plant-based product innovation, expanding QSR chain volumes, and rising health-conscious snacking demand from India's 300 million-strong urban consumer market actively seeking nutritious convenience food solutions at competitive price points.

Emerging Market Expansion

Plant-based and health-positioned frozen foods represent the highest-potential product innovation frontier, with millet-based frozen snacks, protein-enriched vegetable products, and certified organic frozen ranges attracting premium pricing and high consumer engagement. Export market expansion in frozen vegetables and seafood — leveraging India's cost-competitive agricultural processing base — offers diversified revenue growth for processors investing in IQF technology, HACCP certification, and EU and US market regulatory compliance capabilities.

Investment & Private Capital Trends

India's food processing sector attracted significant investment, with the Production Linked Incentive (PLI) scheme allocating INR 10,900 crore to incentivise processing capacity expansion and export promotion. Private equity interest in cold chain infrastructure, IoT-enabled logistics platforms, and D2C frozen food brands is increasing, reflecting investor recognition of the long-term structural growth opportunity as urbanisation, modern retail penetration, and digital commerce continue their multi-decade expansion trajectories across India's rapidly evolving consumer economy.

Future Market Outlook (2026-2034)

The Indian frozen foods market forecast projects sustained value expansion from INR 216.59 Billion in 2025 to INR 643.64 Billion by 2034 at a CAGR of 12.86%, representing a near-tripling of market value over the forecast period. This growth trajectory is underpinned by three interconnected structural forces: accelerating urbanisation adding an estimated 100 million new urban residents to India's cities by 2034; continuing cold chain infrastructure investment improving geographic reach and reliability; and rapid digital commerce adoption transforming frozen food purchasing behaviour across demographic segments.

Three market evolution themes are likely to define the Indian frozen foods landscape through 2034. First, product innovation driven by health, sustainability, and premiumisation will reshape category value — plant-based frozen snacks, organic certified frozen vegetables, and functional frozen meal solutions will command higher average selling prices and attract aspirational urban consumers. Second, quick-commerce platforms achieving nationwide Tier-II city coverage by 2027–2028 will unlock hundreds of millions of potential new frozen food consumers previously excluded by cold chain access limitations, fundamentally expanding the addressable market.

By 2034, the Indian frozen foods industry is forecast to have completed its transition from a metropolitan niche category to a nationally distributed, digitally enabled, health-conscious mainstream food segment. The competitive landscape will be shaped by global multinational technology leadership, domestic vertically integrated cooperative processors, and innovative D2C digital-native frozen food brands from India's startup ecosystem targeting Gen-Z consumers with premium, sustainably positioned frozen food propositions across physical and digital retail channels.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024–2025 with Indian frozen foods industry stakeholders including product and marketing directors at leading frozen food manufacturers, cold chain infrastructure operators, quick-commerce platform category managers, modern retail buyers, food service procurement heads, and institutional investors in India's food technology sector. Primary insights validated market sizing, segmentation estimates, distribution channel dynamics, and competitive positioning assessments across all product categories.

Secondary Research

Secondary sources include Ministry of Food Processing Industries (MoFPI) PMKSY scheme documentation, APEDA seafood and agricultural export statistics, FSSAI regulatory publications, National Centre for Cold Chain Development (NCCD) infrastructure reports, IMARC Group proprietary market databases, company annual reports and investor presentations, and trade publications including FnB News India, Food Business News, and Progressive Grocer India covering India's evolving frozen food category landscape.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating India GDP growth rates, urban population expansion projections, household consumption expenditure data, cold chain infrastructure capacity growth, and historical frozen food category evolution patterns across comparable emerging market economies. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty and infrastructure development variability through the 2026–2034 forecast period.

Indian Frozen Foods Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Frozen Vegetable Snacks, Frozen Fruits and Vegetables, Frozen Meat Products |

| Companies Covered | McCain Foods (India) Private Limited, Mother Dairy Fruit & Vegetable Pvt. Ltd., Venky's India, Innovative Foods Ltd (Sumeru), Godrej Agrovet Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Frozen Foods Market Report

The Indian frozen foods market was valued at INR 216.59 Billion in 2025.

The Indian frozen foods market is projected to exhibit a CAGR of 12.86% during 2026-2034, reaching a value of INR 643.64 Billion by 2034, driven by urbanisation, cold chain modernisation, and rapid digital commerce expansion.

Key drivers include rapid urbanisation creating demand for convenient meal solutions, government-backed cold chain infrastructure expansion under PMKSY, proliferating organised retail and quick-commerce networks, rising disposable incomes enabling premium frozen product adoption, and growing health consciousness driving plant-based frozen food innovation across urban India.

Frozen Vegetable Snacks currently dominate the Indian frozen foods market, accounting for a 52.0% share in 2025, driven by India's vegetarian food culture, health-conscious snacking trends, and the widespread popularity of frozen potato-based and vegetable-based products across all consumer segments.

Some of the major players in the Indian frozen foods market include McCain India Pvt Limited, Mother Dairy Fruit and Vegetable (Safal), Venky's (India) Limited, Innovative Foods Limited (Sumeru), and Godrej Tyson Foods Limited.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)