India Paper Cups Market Size, Share, Trends and Forecast by Cup Type, Wall Type, Cup Size, Application, End User, and States, 2026-2034

India Paper Cups Market Summary:

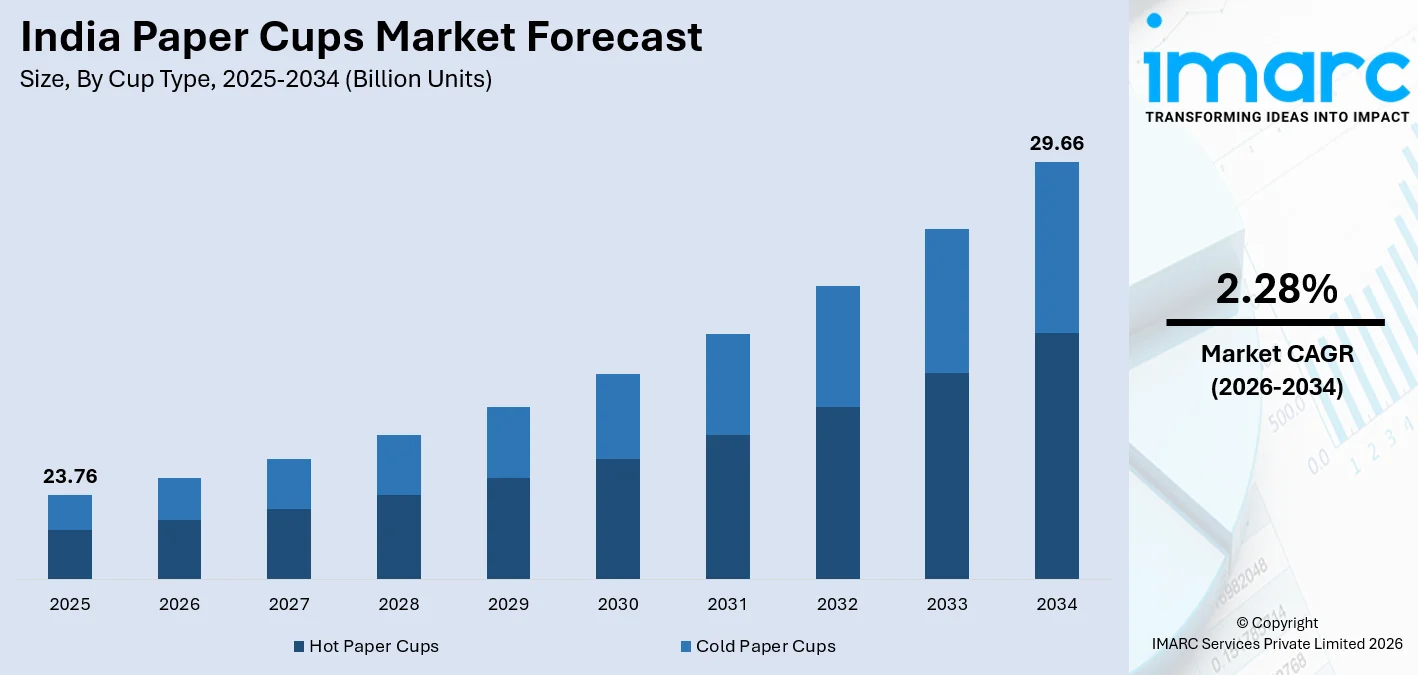

The India paper cups market size reached 23.76 Billion Units in 2025 and is projected to reach 29.66 Billion Units by 2034, growing at a compound annual growth rate of 2.28% from 2026-2034.

India's paper cups market is gaining steady momentum as consumers, foodservice operators, and institutions shift away from plastic-based alternatives toward eco-friendly and biodegradable packaging solutions. Supportive government regulations banning single-use plastics, the rapid expansion of coffee shops and quick-service restaurant (QSR) chains, and rising demand for on-the-go beverage consumption are reinforcing this transition. Increased urbanization, growing disposable incomes, and heightened hygiene awareness continue to shape market expansion, driving the India paper cups market share.

Key Takeaways and Insights:

- By Cup Type: Hot paper cups dominates the market with a share of 66.3% in 2025, driven by the country's deep-rooted tea and coffee culture and widespread usage across foodservice establishments.

- By Wall Type: Single wall paper cups leads the market with a share of 51.5% in 2025, preferred for their cost-efficiency and wide application in institutional, commercial, and casual settings.

- By Cup Size: Medium represents the largest segment with a market share of 45.8% in 2025, reflecting widespread adoption for standard beverage servings across cafes, QSRs, and offices.

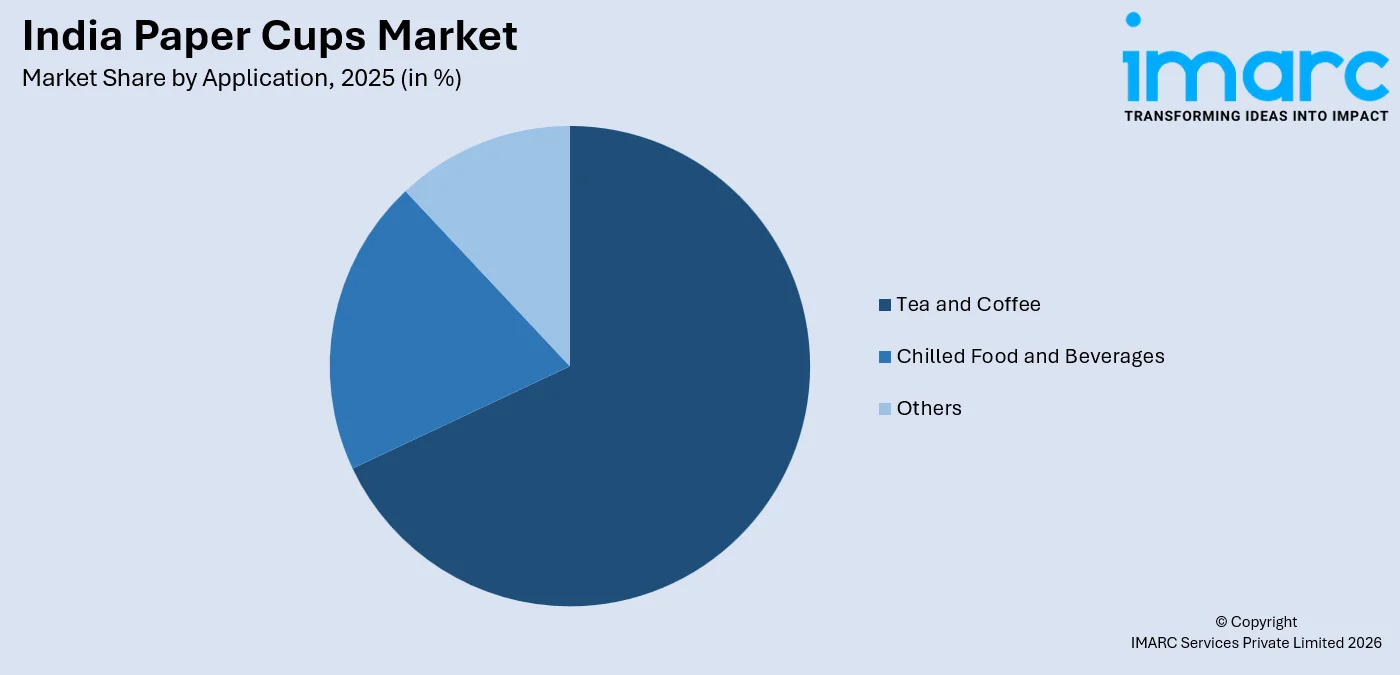

- By Application: Tea and coffee dominates the market with a share of 68.0% in 2025, supported by India's massive beverage culture spanning urban and rural areas.

- By End User: Coffee/tea shops lead the market with a share of 29.5% in 2025, driven by the rapid proliferation of branded and independent café chains across Indian cities.

- By States: Maharashtra dominates the market with a share of 18.5% in 2025, driven by its large urban population, thriving foodservice sector, and significant presence of paper cup manufacturers.

- Key Players: The India paper cups market is highly competitive, with manufacturers focusing on product innovation, expanding production capacities, and introducing compostable and eco-friendly product lines to meet evolving consumer expectations and regulatory requirements. Some of the companies operating in the market include Leetha Group, Sri Lakshmi Polypack, Octane Ecowares Pvt Ltd, Plus Paper Foodpac Limited, Neeyog Packaging, Swan International, Manohar International Private Limited (MIPL), Greenware Revolution, Vecchio Industries, Hyper Pack Pvt. Ltd., Valpack Solutions Private Ltd., Ashima Paper Products, World Star Packaging Industry, Paricott India Papercup Pvt. Ltd., etc.

To get more information on this market Request Sample

The India paper cups market is advancing steadily as environmental consciousness, regulatory momentum, and evolving consumer lifestyles collectively strengthen demand across the country. In December 2025, WSCS India reported rapid growth in its paper cutlery segment and expanded its sustainable packaging portfolio, including paper cups, to cater to global QSR and retail brands as sustainability commitments intensified. Government-led restrictions on single-use plastics have accelerated the transition toward biodegradable and paper-based packaging among foodservice operators and institutions alike. The rapid growth of organized quick-service restaurants, cloud kitchens, and coffee shop chains has made disposable paper cups a standardized packaging solution for beverage delivery and takeaway. Meanwhile, manufacturers are increasingly investing in barrier coating innovations, digital printing capabilities, and compostable product formats to align with rising urban sustainability expectations.

India Paper Cups Market Trends:

Rising Shift Toward Compostable and Biodegradable Paper Cups

India's paper cups market is experiencing a structural shift toward compostable and biodegradable formats as environmental regulations tighten and consumer preferences evolve. In February 2025, Bengaluru‑based startup Aecoz reported that its biodegradable packaging solutions, targeting the foodservice and hospitality sectors, have helped save an estimated 400,000 kg of plastic from continued use, underscoring the growing commercial traction for plant‑based alternatives. Growing awareness about plastic pollution has accelerated adoption of bagasse, PLA, and bamboo-based cup materials across foodservice and institutional segments. Rising willingness among consumers to pay a premium for sustainable brands is encouraging manufacturers to expand eco-friendly product lines, reinforcing compostable and biodegradable formats as increasingly mainstream packaging alternatives throughout the country.

Expansion of Organized Foodservice and Digital Delivery Channels

The proliferation of organized quick-service restaurants, cloud kitchens, and digital food delivery platforms is significantly driving paper cup volumes across India. For instance, homegrown chain Barista Coffee announced in January 2026 plans to expand its network to 800–900 outlets, especially in tier‑II and tier‑III towns, to tap into growing coffee consumption outside major metros. Urban consumers' growing preference for coffee, tea, and cold beverages ordered through delivery aggregators and branded cafes has made standardized disposable packaging essential. This India paper cups market growth trajectory is further reinforced by the continued expansion of coffee shop chains into tier-2 and tier-3 cities, broadening the geographic footprint of paper cup demand nationwide.

Technological Advancements and Customization in Manufacturing

Technology innovation in paper cup manufacturing is reshaping the market by improving product functionality and commercial appeal. For example, Smart Planet Technologies launched a new biodegradable barrier coating for paper cups in January 2025 called EarthCoating, which has already been applied in over 3 billion cups and enhances compostability while remaining compatible with standard recycling systems. Enhanced barrier coatings, double-wall insulation systems, and leak-proof constructions are becoming standard features, while digital printing technologies enable businesses to brand cups as effective marketing tools. Automated manufacturing lines are reducing operational costs and improving consistency, allowing both large-scale and regional players to scale production efficiently and meet the increasingly diverse quality and customization requirements of modern foodservice operators.

Market Outlook 2026-2034:

India's paper cups market is poised for sustained growth through the forecast period, supported by regulatory momentum against single-use plastics, rapid urban expansion, and the continued proliferation of coffee shops and organized foodservice chains. Innovation in eco-friendly and compostable products, rising demand for branded and customized packaging, and the expansion of modern retail and digital food delivery ecosystems are expected to drive incremental volume growth. These converging forces are creating value-added opportunities across the paper cups value chain, positioning the market for a competitive and sustainability-focused future. The market size was estimated at 23.76 Billion Units in 2025 and is expected to reach 29.66 Billion Units by 2034, reflecting a compound annual growth rate of 2.28% over the forecast period 2026-2034.

India Paper Cups Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Cup Type |

Hot Paper Cups |

66.3% |

|

Wall Type |

Single Wall Paper Cups |

51.5% |

|

Cup Size |

Medium |

45.8% |

|

Application |

Tea and Coffee |

68.0% |

|

End User |

Coffee/Tea Shops |

29.5% |

|

States |

Maharashtra |

18.5% |

Cup Type Insights:

- Hot Paper Cups

- Cold Paper Cups

Hot paper cups dominates with a market share of 66.3% of the total India paper cups market in 2025.

Hot paper cups dominate India's paper cups market, reflecting the country's deeply ingrained tea and coffee consumption culture that spans urban cafes, roadside stalls, corporate offices, and institutional settings alike. These cups are engineered to withstand high temperatures while maintaining structural integrity and preventing heat transfer, making them the preferred disposable packaging choice across diverse foodservice environments. Manufacturers are increasingly developing biodegradable and PE-free coated variants to address both performance requirements and growing sustainability expectations among eco-conscious consumers and operators.

Cold paper cups are experiencing rising demand driven by growing consumption of chilled beverages, smoothies, cold-brew coffee, and juices across cafes, QSRs, and quick-commerce delivery platforms. The segment is expanding as branded foodservice chains diversify their beverage menus to include premium cold drink formats, requiring cups that combine leak-proof performance with aesthetic appeal. Customization opportunities through digital printing and branded designs are further encouraging operators to invest in cold cup formats as part of their overall packaging and brand visibility strategies.

Wall Type Insights:

- Single Wall Paper Cups

- Double Wall Paper Cups

- Triple Wall Paper Cups

The single wall paper cups leads with a share of 51.5% of the total India paper cups market in 2025.

Single wall paper cups lead India's paper cups market, driven by their cost efficiency, lightweight construction, and suitability for high-volume institutional and commercial applications. For example, Chemline, a Delhi‑based coatings and adhesives company, recently showcased its new range of water‑based barrier‑coated paper cup stocks at Pamex 2026. The range is designed to improve recyclability by eliminating conventional polyethylene-based liners and to enhance performance for single-wall cups. These cups require fewer input materials during production, resulting in lower manufacturing costs that make them an accessible and practical choice for offices, educational institutions, catering services, and large-scale public events where cost management is a consistent operational priority. Their wide availability through organized distribution channels and e-commerce platforms has reinforced their dominant position across both urban and semi-urban consumption environments.

Double wall paper cups represent a fast-growing alternative, favored in premium beverage applications at branded cafes and upscale restaurants where insulation and heat retention are critical performance attributes. Their two-layer construction provides enhanced protection for users handling hot beverages and supports a more refined consumer experience aligned with the expectations of aspirational café audiences. Triple wall paper cups serve specialized high-temperature applications, offering maximum structural strength and insulation for premium hot beverages primarily within sophisticated foodservice and hospitality environments.

Cup Size Insights:

- Small

- Medium

- Large

The medium dominates with a market share of 45.8% of the total India paper cups market in 2025.

Medium-sized paper cups dominate India's market by aligning with standard beverage volumes served across the country's broad and diverse foodservice spectrum, including cafes, quick-service restaurants, offices, and social gatherings. Their capacity strikes an effective balance between cost efficiency and serving convenience, catering to the most commonly consumed portions of tea, coffee, and cold beverages. Standardization of medium cup formats across major foodservice chains has further cemented their widespread adoption, as uniform sizing supports operational efficiency in both beverage preparation and delivery across high-volume commercial settings.

Small cups continue to play a foundational role in traditional Indian tea-serving culture, particularly within standalone roadside stalls and high-volume institutional settings where single-serve, economical packaging is the dominant requirement. Large cups are gaining growing momentum alongside the expansion of premium cold beverage formats and supersized serving trends within fast-food chains, cinema halls, and outdoor entertainment venues, where consumers increasingly seek value through extended portions and convenient portable packaging that complements modern on-the-go lifestyle preferences.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Tea and Coffee

- Chilled Food and Beverages

- Others

The tea and coffee leads with a share of 68.0% of the total India paper cups market in 2025.

Tea and coffee represent the dominant application for paper cups in India, reflecting a consumption culture that is deeply embedded across every demographic, geography, and occasion in the country. The rapid formalization of this consumption through organized coffee shop chains, QSRs, corporate cafeterias, and cloud kitchen platforms has translated traditional beverage habits into structured, recurring demand for standardized disposable packaging. Increasing premiumization of hot beverage offerings and growing café culture among younger urban consumers are further deepening the role of paper cups within the tea and coffee application segment.

Chilled food and beverages form a steadily growing application segment, propelled by rising consumption of cold-brew coffee, flavored smoothies, soft drinks, and frozen dessert servings across cafes, dessert parlors, and quick-service restaurants. Seasonal demand patterns and expanding cold beverage menus at organized food chains are creating new volume opportunities within this segment. Others encompasses healthcare, institutional, and event-based applications, generating consistent and predictable demand from hospitals, corporate campuses, and large public gatherings where hygiene, convenience, and single-use practicality remain paramount procurement priorities.

End User Insights:

- Coffee/Tea Shops

- Fast Foods Shops/ QSRS

- Offices, Educational Institutes and Multiplexes

- Supermarket (Food Courts)

- Others

The coffee/tea shops dominates with a market share of 29.5% of the total India paper cups market in 2025.

Coffee and tea shops represent the leading end-user segment in India's paper cups market, shaped by the country's accelerating café culture and expanding presence of both domestic and international beverage chains. The segment is driven by rising aspirational preferences among urban millennials and Gen Z consumers who view café experiences as social and lifestyle expressions rather than simple refreshment stops. The rapid proliferation of branded café concepts across metropolitan and emerging urban markets is generating sustained and growing demand for standardized, aesthetically appealing, and customized paper cups tailored to each brand's identity.

Fast food shops and QSRs constitute a significant and fast-expanding end-user base, supported by aggressive outlet expansion across tier-one, tier-two, and tier-three cities driven by rising consumer appetite for convenient, affordable dining experiences. Offices, educational institutes, and multiplexes represent a stable institutional demand source for paper cups across cafeterias, vending stations, and daily hydration points. Supermarket food courts are an emerging consumption channel fueled by organized retail expansion and rising mall culture, while others, including healthcare facilities, catering services, and event operators, maintain consistent volumes through hygiene-driven, single-use packaging requirements.

States Insights:

- Maharashtra

- Uttar Pradesh

- Tamil Nadu

- West Bengal

- Gujarat

- Others

Maharashtra exhibits a clear dominance with a 18.5% share of the total India paper cups market in 2025.

Maharashtra commands the largest share of India's paper cups market, underpinned by its highly urbanized population, thriving foodservice ecosystem, and concentration of commercial and industrial activity. Mumbai, Pune, and Nagpur serve as key demand centers, collectively hosting a dense network of cafes, QSRs, hotels, hospitals, and corporate offices that generate significant and ongoing paper cup consumption. The state's role as India's financial and commercial capital supports a large institutional segment, including multinational corporations and organized food courts, with consistent and large-scale paper cup procurement requirements throughout the year.

Uttar Pradesh is a rapidly growing market driven by its large population base and expanding tier-two and tier-three urban centers, with a growing network of foodservice establishments supporting steady volume growth. Tamil Nadu benefits from a strong tea culture and a robust foodservice sector anchored by Chennai's dense commercial activity. West Bengal, centered on Kolkata, drives eastern India demand through entrenched beverage habits and an expanding café presence. Gujarat's industrially active cities generate demand through organized food courts and corporate campuses, while the remaining states increasingly contribute as coffee chains and QSR networks penetrate newer geographies.

Market Dynamics:

Growth Drivers:

Why is the India Paper Cups Market Growing?

Government Regulations Banning Single-Use Plastics

India's regulatory environment has become one of the most significant structural drivers of paper cup demand. Government-enforced bans on single-use plastic items, including cups, plates, straws, and cutlery, were implemented under the Plastic Waste Management (Amendment) Rules, 2021. These rules prohibited the manufacture, import, stocking, distribution, sale, and use of identified single-use plastic items from July 1, 2022, prompting foodservice operators to shift toward compliant alternatives such as paper-based cups. Compliance with plastic restrictions has become a strategic business necessity, accelerating large-scale substitution toward biodegradable and recyclable paper cups. State-level enforcement mechanisms and rising penalties for non-compliance are further incentivizing both manufacturers and end-users to commit to sustainable packaging transitions.

Rapid Expansion of Coffee Shops and QSR Networks

The accelerating proliferation of organized coffee shop chains and quick-service restaurants across India represents one of the most dynamic demand drivers for paper cups. India’s homegrown specialty brand Third Wave Coffee Roasters celebrated the opening of its 200th café in December 2025 and is targeting further expansion to about 300 outlets by 2026, signalling sustained growth in branded coffee consumption across both metropolitan and emerging urban markets. The rapid growth of domestic and international café brands, alongside the emergence of tea-centric concepts, is expanding the geographic footprint of branded beverage consumption into tier-two and tier-three cities. Each new outlet generates sustained demand for standardized and branded paper cups, directly translating network expansion into proportional volume growth and reinforcing paper cups as an indispensable component of organized foodservice operations nationwide.

Urbanization and Growth of On-the-Go Beverage Culture

India's rapid urbanization, accompanied by shifts in consumer lifestyles, rising disposable incomes, and evolving food consumption habits, is a foundational driver of paper cup market growth. Expanding foodservice infrastructure across urban and peri-urban areas is broadening the addressable consumer base for disposable beverage packaging. In March 2026, both Swiggy and Zomato reported significant increases in gross order value and monthly active users, with Swiggy’s gross order value growing over 20% year‑on‑year and total orders rising sharply, reflecting strong demand for delivered meals and beverages that frequently involve disposable packaging. Online food delivery platforms have normalized takeaway and home delivery of hot and cold beverages, creating a structural demand channel for paper cups. Busy urban lifestyles and growing preference for convenient, single-serve packaging solutions continue to reinforce sustained demand growth across the country.

Market Restraints:

What Challenges the India Paper Cups Market is Facing?

High Production Costs for Eco-Friendly Paper Cups

The development and production of biodegradable and compostable paper cups involve significantly higher raw material and manufacturing costs compared to conventional plastic-lined alternatives. Premium substrates such as PLA-coated and bagasse-based materials, along with advanced barrier technologies, increase input costs and restrict adoption among price-sensitive buyers. This cost differential creates a barrier to widespread market penetration, particularly in small foodservice businesses and rural institutional segments that prioritize cost over sustainability credentials, slowing the transition to eco-friendly formats.

Limited Consumer Awareness in Tier-2 and Tier-3 Markets

While metro cities demonstrate strong adoption of eco-friendly paper cups, consumer awareness regarding the benefits and proper disposal of compostable and biodegradable variants remains limited in smaller towns and rural areas. This awareness gap slows market penetration into emerging geographic segments, where low-cost plastic alternatives continue to dominate. Inconsistent enforcement of plastic bans at the local level further reduces motivation for end users to transition to premium paper cup formats, restraining the pace of market conversion in these high-population regions.

Competition from Low-Cost Conventional Alternatives

The India paper cups market faces persistent pricing pressure from low-cost, conventional plastic-lined disposable cups that remain widely available across unorganized trade channels. Manufacturers of budget paper cups compete aggressively on price, creating downside pressure on margins for premium and sustainable product manufacturers. Inconsistent quality standards and the absence of uniform certification requirements across the industry can also undermine consumer confidence, complicating differentiation for compliant manufacturers and limiting premiumization in price-sensitive market segments.

Competitive Landscape:

The India paper cups market is moderately fragmented, with a mix of organized national players and smaller regional manufacturers competing across volume and premium product categories. Leading manufacturers are investing in capacity expansions, digital printing technologies, and eco-friendly product lines to strengthen their competitive positioning. Market players are differentiating through product customization, compostable material adoption, and direct supply partnerships with organized QSR and coffee shop chains, enabling them to capture growing demand from branded foodservice operators. Regional players continue to compete primarily on cost efficiency and localized distribution reach, serving price-sensitive institutional and small-scale commercial end users across diverse geographies.

- Leetha Group

- Sri Lakshmi Polypack

- Octane Ecowares Pvt Ltd

- Plus Paper Foodpac Limited

- Neeyog Packaging

- Swan International

- Manohar International Private Limited (MIPL)

- Greenware Revolution

- Vecchio Industries

- Hyper Pack Pvt. Ltd.

- Valpack Solutions Private Ltd.

- Ashima Paper Products

- World Star Packaging Industry

- Paricott India Papercup Pvt. Ltd.

Recent Developments:

- In November 2025, A Kerala‑based entrepreneur Athul Krishna founded a paper cup business named Choodu that makes instant tea/coffee cups and is planning expansion in 2026. This venture has gained attention locally for improving paper cup manufacturing methods.

India Paper Cups Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Crore, Billion Units |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Cup Types Covered | Hot Paper Cups, Cold Paper Cups |

| Wall Types Covered | Single Wall Paper Cups, Double Wall Paper Cups, Triple Wall Paper Cups |

| Cup Sizes Covered | Small, Medium, Large |

| Applications Covered | Tea and Coffee, Chilled Food and Beverages, Others |

| End Users Covered | Coffee/Tea Shops, Fast Foods Shops/ QSRS, Offices, Educational Institutes and Multiplexes, Supermarket (Food Courts), Others |

| States Covered | Maharashtra, Uttar Pradesh, Tamil Nadu, West Bengal, Gujarat, Others |

| Companies Covered | Leetha Group, Sri Lakshmi Polypack, Octane Ecowares Pvt Ltd, Plus Paper Foodpac Limited, Neeyog Packaging, Swan International, Manohar International Private Limited (MIPL), Greenware Revolution, Vecchio Industries, Hyper Pack Pvt. Ltd., Valpack Solutions Pvt. Ltd., Ashima Paper Products, World Star Packaging Industry and Paricott India Papercup Pvt. Ltd. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Paper Cups Market Report

The India paper cups market reached a volume of 23.76 Billion Units in 2025.

The India paper cups market is expected to grow at a compound annual growth rate of 2.28% from 2026-2034 to reach 29.66 Billion Units by 2034.

Hot paper cups, holding the largest share of 66.3%, remain integral to India's paper cups demand, driven by the country's deep-rooted tea and coffee culture and widespread use across cafes, QSRs, offices, and institutional settings across the country.

Key factors driving the India paper cups market include government regulations banning single-use plastics, rapid expansion of coffee shop and QSR chains, urbanization-driven on-the-go beverage consumption, rising demand for eco-friendly packaging, and growth in digital food delivery platforms.

Major challenges include high production costs for biodegradable paper cups, limited consumer awareness in smaller markets, competition from low-cost conventional alternatives, and inconsistent enforcement of single-use plastic bans across different regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)