Indian Pasta Market Size, Share, Trends and Forecast by Type, Raw Material, Distribution Channel, Cuisine, and Region, 2026-2034

Indian Pasta Market Summary:

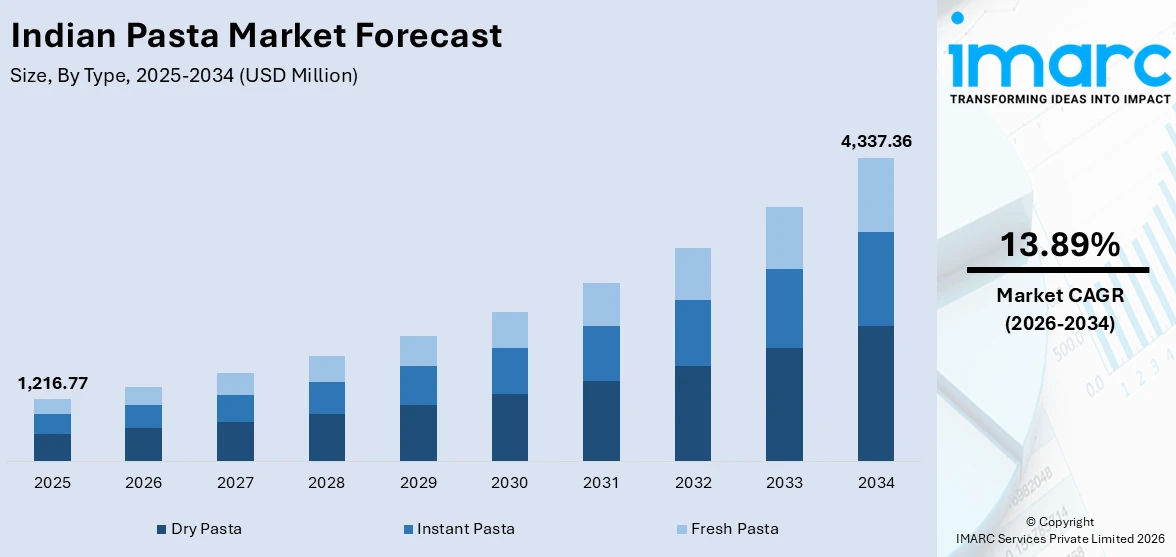

The Indian pasta market size was valued at USD 1,216.77 Million in 2025 and is projected to reach USD 4,337.36 Million by 2034, growing at a compound annual growth rate of 13.89% from 2026-2034.

The Indian pasta market is expanding rapidly as urbanization, evolving dietary preferences, and rising disposable incomes drive consumer demand for convenient and versatile meal options. Growing acceptance of Italian cuisine among younger demographics, increasing penetration of organized retail, and the proliferation of quick-service restaurants serving pasta-based dishes are reshaping consumption patterns, positioning pasta as an increasingly mainstream staple across Indian households.

Key Takeaways and Insights:

- By Type: Dry pasta dominates the market with a share of 63.5% in 2025, owing to its extended shelf life, ease of preparation, and widespread availability across retail and institutional channels. Growing preference for pantry-friendly staples and cost-effective meal solutions is fueling demand expansion.

- By Raw Material: Semolina leads the market with a share of 42.8% in 2025, driven by its superior gluten content that ensures optimal pasta texture and shape retention during cooking. Traditional consumer familiarity with semolina-based products and abundant domestic wheat supply reinforces its dominance.

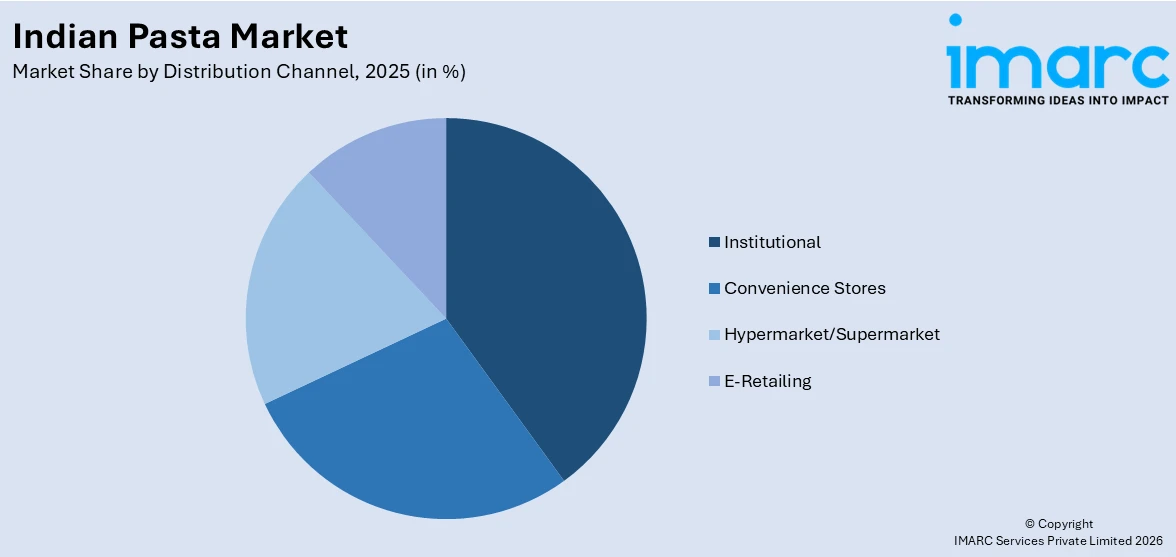

- By Distribution Channel: Institutional represents the largest segment with a market share of 34.2% in 2025, reflecting strong demand from restaurants, hotels, cafeterias, and catering establishments that integrate pasta into their core menus as consumer preference for Italian cuisine accelerates nationwide.

- By Cuisine: White sauce pasta holds the market with a share of 41.5% in 2025, owing to its creamy flavor profile and widespread appeal among urban consumers seeking indulgent yet approachable Italian-style dishes at restaurants and quick-service outlets.

- By Region: Maharashtra exhibits a clear dominance with 14.5% share in 2025, driven by the concentration of urban population centers in Mumbai and Pune, high penetration of organized food service outlets, and strong consumer adoption of Western dining formats across the state.

- Key Players: Key players drive the Indian pasta market by expanding product portfolios, introducing healthier multigrain and fortified variants, strengthening nationwide distribution networks, and investing in marketing and innovation. Their partnerships with quick-service restaurants and e-commerce platforms boost awareness, accelerate adoption, and ensure consistent product availability across diverse consumer segments. Some of the key players operating in the industry are Nestle India Limited, ITC Limited, Bambino Agro Industries Limited, Del Monte and MTR Foods Private Limited.

To get more information on this market Request Sample

The Indian pasta market is witnessing robust expansion driven by fundamental shifts in consumer lifestyles, eating habits, and food accessibility. Rapid urbanization, rising dual-income households, and increasingly hectic work schedules are propelling demand for convenient, ready-to-cook meal solutions, with pasta emerging as a preferred choice among young professionals, students, and families. The growing westernization of Indian diets, coupled with the expanding footprint of Italian restaurants, cafes, and quick-service chains, has significantly elevated pasta consumption across metropolitan and tier-two cities. Furthermore, the proliferation of e-commerce platforms and quick-commerce services is making diverse pasta products accessible to consumers in smaller towns and semi-urban markets. Health-conscious consumers are increasingly embracing whole wheat, multigrain, and protein-enriched pasta variants, broadening the market’s appeal and driving Indian pasta market share.

Indian Pasta Market Trends:

Rising Demand for Health-Focused Pasta Variants

Nutritious pasta substitutes are becoming more and more popular among Indian consumers; whole wheat, multigrain, gluten-free, and protein-enriched varieties are particularly popular. The change is a reflection of larger wellness trends that are changing how packaged food is consumed in urban and semi-urban regions. For instance, in September 2024, Modi Naturals launched its Oleev Kitchen multigrain pasta range, combining chickpea, jowar, brown rice, and durum wheat to offer a high-protein, fiber-rich alternative free from refined flour. This transition toward healthier formulations is encouraging both established and emerging brands to invest in product innovation, supporting Indian pasta market growth.

Proliferation of Fusion Pasta Cuisine Across Food Service Channels

The integration of Indian flavors into Italian pasta formats is reshaping the food service landscape, as restaurants, cafes, and quick-service chains create distinctive fusion offerings such as tandoori pasta, masala penne, and butter chicken spaghetti. This trend caters to consumers seeking familiar flavors in international formats. The growing expansion of dedicated pasta-focused dining chains and casual Italian restaurants into new cities reflects rising investor confidence in fusion cuisine, broadening pasta consumption beyond traditional metropolitan markets into emerging urban corridors across India.

Expansion of Quick-Commerce and E-Retailing Channels

The rapid growth of online grocery platforms and quick-commerce services is transforming how Indian consumers access pasta products, enabling delivery within minutes across major urban centers. Platforms are offering extensive pasta assortments alongside complementary sauces and ingredients, encouraging trial and repeat purchases. The convenience of doorstep delivery, coupled with attractive discounts and bundled meal solutions, is accelerating consumer adoption and democratizing pasta access beyond traditional retail channels into smaller towns and semi-urban markets.

Market Outlook 2026-2034:

The Indian market for pasta is likely to witness steady growth in the upcoming years, driven by the changing lifestyle and consumption patterns of the populace in India. Additionally, the rising standard of living and penetration of organized retail and foodservice chains in India are also likely to have a positive impact on the market in the upcoming years. Furthermore, the rising health-consciousness among the populace in India and the increasing acceptance of pasta as a part of their regular consumption patterns are likely to remain major growth accelerators in the upcoming years. These factors are likely to ensure steady growth in the market in India in the upcoming years. The market generated a revenue of USD 1,216.77 Million in 2025 and is projected to reach a revenue of USD 4,337.36 Million by 2034, growing at a compound annual growth rate of 13.89% from 2026-2034.

Indian Pasta Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Dry Pasta |

63.5% |

|

Raw Material |

Semolina |

42.8% |

|

Distribution Channel |

Institutional |

34.2% |

|

Cuisine |

White Sauce Pasta |

41.5% |

|

Region |

Maharashtra |

14.5% |

Type Insights:

- Dry Pasta

- Instant Pasta

- Fresh Pasta

Dry pasta dominates with a market share of 63.5% of the total Indian pasta market in 2025.

Dry pasta continues to be the preferred format among Indian consumers owing to its extended shelf life, convenient storage, and affordability. The segment benefits from its versatility, as it can be prepared in numerous ways and pairs well with both traditional Italian and Indian fusion sauces. Widely stocked across supermarkets, convenience stores, and kirana shops, dry pasta has achieved deep market penetration. The availability of diverse shapes such as penne, fusilli, spaghetti, and macaroni in economy-friendly pack sizes has further expanded its consumer base, particularly among budget-conscious households and students.

The institutional channel significantly contributes to dry pasta demand, as restaurants, hotels, and catering companies favor it for its consistency, cost-effectiveness, and ease of bulk preparation. The growing presence of Italian dining formats and quick-service restaurants across India has accelerated institutional procurement of dry pasta. The expansion of organized food service operations into tier-two and tier-three cities is further strengthening this demand, as pasta-based dishes become a staple offering across casual dining chains, cloud kitchens, and multi-cuisine outlets catering to an increasingly cosmopolitan consumer base nationwide.

Raw Material Insights:

- Semolina

- Refined Flour

- Durum Wheat

- Others

Semolina leads the market with a share of 42.8% of the total Indian pasta market in 2025.

Semolina remains the predominant raw material in Indian pasta manufacturing due to its superior gluten content, which ensures firm texture, optimal shape retention, and consistent cooking quality. Derived from durum wheat through milling and purification, semolina produces pasta that meets consumer expectations for an authentic al dente experience. Indian consumers are traditionally familiar with semolina through its widespread use in products such as rava and sooji, which helps lower adoption barriers for semolina-based pasta products across diverse demographic groups and regions.

India's strong domestic wheat production infrastructure supports the sustained availability of semolina for pasta manufacturing. The country's robust agricultural output, with durum wheat varieties cultivated extensively in states like Madhya Pradesh and Rajasthan, contributes directly to the semolina supply chain. Major pasta manufacturers leverage this domestic raw material base to maintain competitive pricing while ensuring product quality, positioning semolina-based pasta as both an affordable and nutritionally appealing option for mass-market consumers across diverse regional markets.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Institutional

- Convenience Stores

- Hypermarket/Supermarket

- E-Retailing

Institutional represents the largest segment with a 34.2% share of the total Indian pasta market in 2025.

The institutional distribution channel encompasses restaurants, hotels, cafeterias, catering services, and commercial kitchens that procure pasta in bulk for menu preparation. The rapid expansion of Italy-inspired dining concepts, casual dining chains, and quick-service restaurants across Indian cities has created a sustained pipeline of institutional demand. Pasta has become a core menu item at many food service establishments, valued for its versatility, fast preparation, and broad customer appeal across vegetarian and non-vegetarian diners alike.

The food service sector continues to evolve as operators integrate pasta into diverse culinary formats, from standalone Italian restaurants to multi-cuisine outlets and cloud kitchens. The aggressive expansion of organized dining chains and delivery-focused kitchens into metropolitan and smaller cities is broadening the reach of pasta-based menu offerings to new consumer segments. This sustained growth of food service infrastructure, coupled with rising consumer demand for convenient and versatile dining options, ensures that institutional channels remain the primary distribution pathway for pasta products in India.

Cuisine Insights:

- White Sauce Pasta

- Red Sauce Pasta

- Mix Sauce Pasta

White sauce pasta holds the largest share at 41.5% of the total Indian pasta market in 2025.

White sauce pasta maintains its leading position in the cuisine segment due to its rich, creamy flavor profile that resonates strongly with Indian consumers, particularly in urban areas. The béchamel-based preparation offers a mild, indulgent taste that appeals across age groups, from children to adults, making it a frequent choice at restaurants, cafes, and home kitchens alike. The versatility of white sauce pasta as a base for various additions, including mushrooms, corn, paneer, and grilled vegetables, enhances its popularity among vegetarian consumers who constitute a significant portion of the Indian market.

The growing presence of Italian-themed cafes and casual dining outlets in metro and tier-two cities has further reinforced the prominence of white sauce pasta as a core menu offering. Food service operators increasingly customize white sauce pasta with locally inspired ingredients and spice profiles to cater to regional palates, driving repeat consumption. Additionally, the availability of ready-to-use white sauce pasta kits and instant preparation formats in retail and e-commerce channels has simplified home preparation, encouraging trial among first-time consumers and expanding the category’s household penetration across India.

Regional Insights:

- Uttar Pradesh

- Delhi

- Maharashtra

- Gujarat

- Karnataka

- Tamil Nadu

- Others

Maharashtra exhibits a clear dominance in the market with a 14.5% share of the total Indian pasta market in 2025.

Maharashtra is the largest market for the Indian pasta industry, primarily because the state houses the largest urban agglomerations of India, namely Mumbai, Pune, and Nagpur. The presence of a large number of restaurants with a strong presence of Italian cuisine is also a significant factor for the demand for pasta products in the state. Additionally, the presence of a large young working-age population with a strong affinity for Western cuisine is a significant factor for the demand for pasta products in the state.

The state also holds the advantages of well-developed organized retail networks and advanced e-commerce logistics to ensure widespread availability of different varieties of pasta from multiple brands to consumers. The state’s food processing industry also supports the manufacturing industry for making pasta products, with proximity to major raw material sourcing regions. Additionally, the rise of quick-commerce platforms with large dark store networks in the Mumbai and Pune metropolitan areas has helped improve the availability of pasta products to consumers, allowing for impulse buys due to their ability to deliver products in minutes.

Market Dynamics:

Growth Drivers:

Why is the Indian Pasta Market Growing?

Rapid Urbanization and Evolving Consumer Lifestyles

India’s accelerating urbanization is fundamentally transforming food consumption patterns, with an increasing proportion of the population gravitating toward convenient, ready-to-cook meal solutions. The expansion of urban centers, rising dual-income households, and increasingly demanding work schedules are creating a structural shift away from time-intensive traditional cooking toward faster meal preparation formats. Pasta, with its ease of preparation and versatile pairing options, aligns perfectly with the needs of time-pressed urban consumers seeking quick yet satisfying meals. The growing young working population in cities is particularly receptive to Western food influences, fueling adoption of pasta as a regular household staple. This demographic shift is complemented by the expansion of food delivery platforms that make pasta dishes readily accessible. This digital accessibility continues to accelerate pasta consumption across urban and semi-urban markets.

Expanding Quick-Service Restaurant and Food Service Infrastructure

The rapid proliferation of quick-service restaurants, casual dining chains, and cloud kitchens across India is creating significant demand for pasta products through institutional channels. As these food service formats expand beyond metropolitan areas into tier-two and tier-three cities, they bring pasta-based menu offerings to new consumer segments who may not have previously encountered such products. The competitive pricing strategies employed by these outlets make pasta meals accessible to a broader income demographic. Major food service operators are increasingly incorporating pasta into their core menus, recognizing its appeal as a customizable, high-margin item with broad consumer acceptance. For example, Pasta Street, one of India’s dedicated Italian dining chains, expanded to its eighth Bengaluru location in December 2024 and subsequently opened its first outlet in Delhi, with plans for five additional locations across the Delhi-NCR region. Such expansions reflect the growing investor confidence in pasta-focused dining formats and their role in driving market growth.

Growing Health Consciousness and Product Innovation

Rising health awareness among Indian consumers is driving demand for innovative, nutritionally enhanced pasta products that offer functional benefits beyond basic sustenance. Manufacturers are responding by introducing whole wheat, multigrain, high-protein, and gluten-free pasta variants that cater to fitness-conscious consumers, individuals with dietary restrictions, and parents seeking healthier meal options for their families. This trend toward health-forward products is broadening the market’s consumer base beyond traditional pasta enthusiasts. The entry of health-focused brands into the pasta category is intensifying product innovation and expanding shelf space in retail outlets. For instance, WickedGüd, a health-oriented noodle and pasta brand, raised INR 20 Crore in December 2025, having achieved threefold revenue growth over the preceding twelve months and expanded its presence to over 5,000 retail stores nationwide. The brand’s success demonstrates the commercial viability of better-for-you pasta products in the Indian market, encouraging further innovation and investment in the health-focused segment.

Market Restraints:

What Challenges the Indian Pasta Market is Facing?

Strong Competition from Traditional Staple Foods

Pasta faces formidable competition from deeply entrenched staple foods such as rice, roti, and traditional Indian bread varieties that have been integral to Indian diets for centuries. These culturally rooted alternatives are perceived as more filling, affordable, and nutritionally complete by a large proportion of the population. Overcoming these deeply established dietary preferences requires sustained marketing investment, product localization, and competitive pricing strategies that can position pasta as a viable everyday alternative rather than an occasional indulgence.

Price Sensitivity in Rural and Semi-Urban Markets

A significant proportion of Indian consumers, particularly in rural and semi-urban areas, remain highly price-sensitive when it comes to packaged food purchases. Branded pasta products are often priced higher than traditional alternatives, limiting adoption among lower-income demographics. The premium associated with imported brands and health-focused variants further restricts market penetration in price-conscious segments, requiring manufacturers to develop affordable pack sizes and value-oriented product lines to expand their consumer reach.

Limited Awareness and Distribution in Smaller Towns

Despite growing urbanization, pasta awareness and availability remain limited in many smaller towns and rural regions across India. Inadequate cold chain logistics for fresh and frozen pasta variants, sparse organized retail presence, and limited consumer familiarity with pasta preparation methods constrain market expansion in these areas. Overcoming these distribution and awareness gaps requires investment in last-mile supply chain infrastructure, localized marketing campaigns, and partnerships with regional retailers to build sustained market presence beyond established urban corridors.

Competitive Landscape:

The Indian pasta market has been witnessing a highly competitive market scenario with the presence of both domestic and international brands. Companies are trying to compete in the market through product diversification, health innovation, pricing strategies, and expansion of distribution networks. Strategic partnerships are also facilitating companies to expand their market reach. Companies are trying to compete with each other through celebrity endorsements, online marketing campaigns, and participation in popular platforms. Companies are trying to differentiate their brands from their competitors through taste innovation and regional flavors.

Some of the key players operative in the industry include:

- Nestle India Limited

- ITC Limited

- Bambino Agro Industries Limited

- Del Monte

- MTR Foods Private Limited

Indian Pasta Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD, ‘000 Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Dry Pasta, Instant Pasta, Fresh Pasta |

| Raw Materials Covered | Semolina, Refined Flour, Durum Wheat, Others |

| Distribution Channels Covered | Institutional, Convenience Stores, Hypermarket/Supermarket, E-Retailing |

| Cuisines Covered | White Sauce Pasta, Red Sauce Pasta, Mix Sauce Pasta |

| States Covered | Uttar Pradesh, Delhi, Maharashtra, Gujarat, Karnataka, Tamil Nadu, Others |

| Companies Covered | Nestlé, ITC, Bambino, MTR, Del Monte |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Pasta Market Report

The Indian pasta market size was valued at USD 1,216.77 Million in 2025.

The Indian pasta market is expected to grow at a compound annual growth rate of 13.89% from 2026-2034 to reach USD 4,337.36 Million by 2034.

Dry pasta dominated the market with a share of 63.5%, driven by its extended shelf life, affordable pricing, versatile preparation options, and widespread availability across retail and institutional channels throughout India.

Key factors driving the Indian pasta market include rapid urbanization, rising disposable incomes, growing acceptance of Western cuisines, expanding food service infrastructure, increasing health consciousness, and the proliferation of e-commerce distribution channels.

Major challenges include strong competition from traditional staple foods, price sensitivity in rural and semi-urban markets, limited awareness and distribution in smaller towns, fluctuating raw material costs, and the need for sustained consumer education about pasta preparation methods.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade