Indian Pre-School/Childcare Market Size, Share, Trends and Forecast by Facility, Ownership, Age Group, Location, Major Cities, and Region, 2026-2034

Indian Pre-School/Childcare Market Summary:

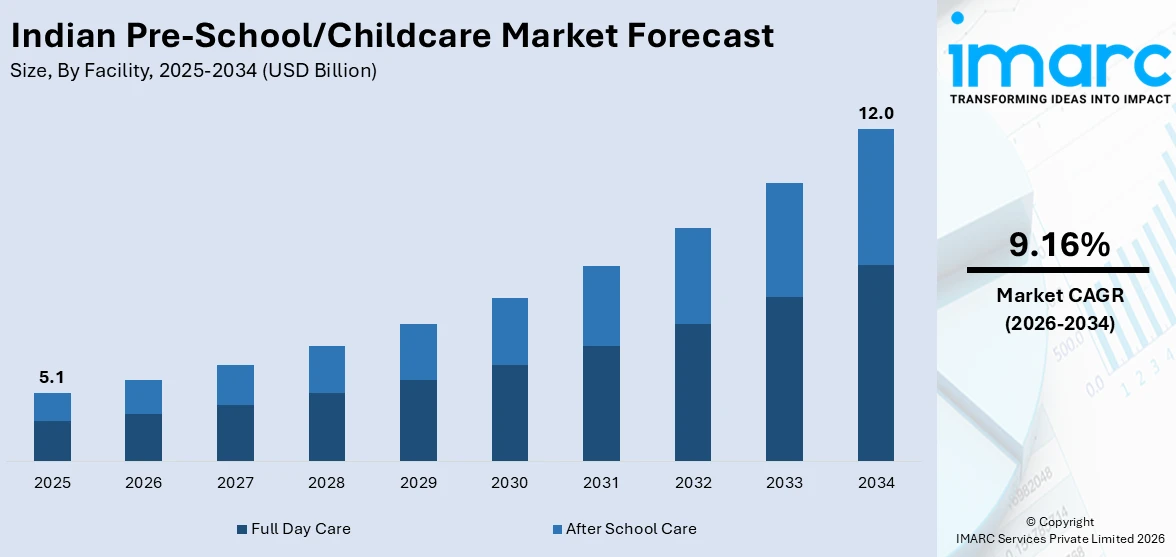

The Indian pre-school/childcare market size was valued at USD 5.1 Billion in 2025 and is projected to reach USD 12.0 Billion by 2034, growing at a compound annual growth rate of 9.16% from 2026-2034.

The market is driven by rising parental awareness, growing urbanization, increasing female workforce participation, and a cultural shift toward structured early learning environments. Expanding middle-class aspirations for quality foundational education, combined with supportive government initiatives promoting early childhood development, are accelerating sector growth. The convergence of demographic momentum and evolving parental priorities continues to strengthen demand, contributing significantly to the Indian pre-school/childcare market share.

Key Takeaways and Insights:

- By Facility: Full day care dominates the market with a share of 64.5% in 2025, driven by rising dual-income households demanding all-day supervised, structured childcare and learning solutions.

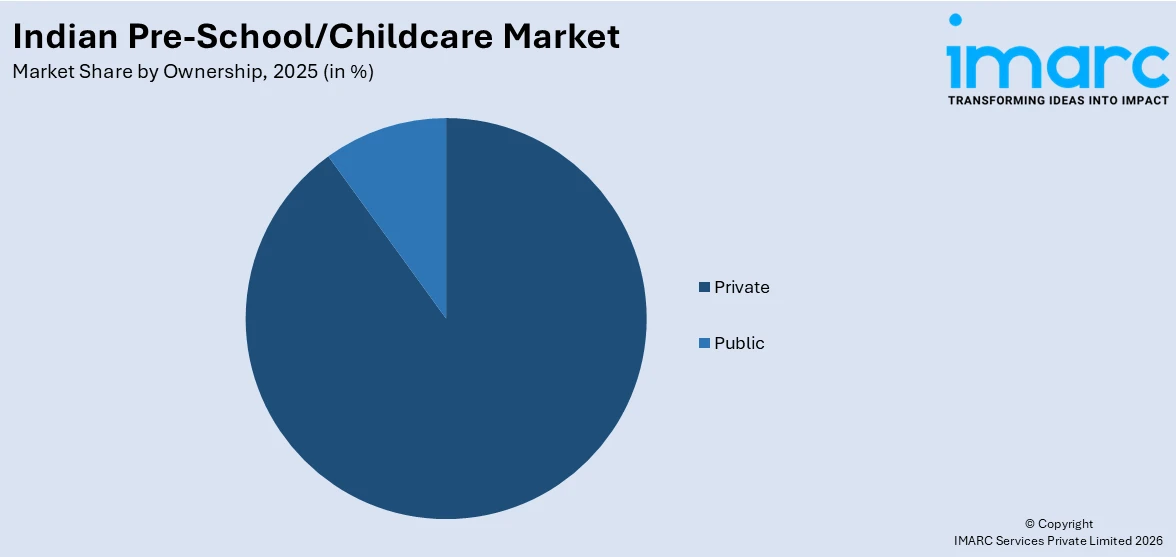

- By Ownership: Private leads the market with a share of 89.2% in 2025, owing to strong investor interest and parental preference for premium, innovative early education facilities.

- By Age Group: 2-4 years represents the largest segment with a market share of 48.5% in 2025, driven by growing recognition of this period as critical for foundational cognitive development.

- By Location: Standalone dominates the market with a share of 48.5% in 2025, owing to deep community trust, localized flexibility, and strong neighbourhood-level parental engagement.

- By Major Cities: Delhi-NCR represents the largest segment with a market share of 24.5% in 2025, driven by high population density, nuclear family growth, and concentrated working professional demand.

- By Region: North India leads the market with a share of 32.8% in 2025, owing to dense urban populations, rising disposable incomes, and strong parental emphasis on structured early education.

- Key Players: The Indian pre-school/childcare market features a dynamic mix of established organized chains and independent standalone operators competing across quality, curriculum, location, and affordability to capture a rapidly expanding base of early learners and growth-conscious investors. Some of the key players operating in the market include Kidzee, Bachpan Global, EuroKids, Tree House Education & Accessories Ltd., Shemrock Play School, Kangaroo Kids, Hello Kids, Little Millennium, and T.I.M.E. Kids.

To get more information on this market Request Sample

The Indian pre-school/childcare market is experiencing robust expansion underpinned by a confluence of demographic, socioeconomic, and policy-driven factors. Rising urbanization has created densely populated hubs where demand for structured early education is most intense, while growing female workforce participation has made professional childcare essential for millions of families across the country. In December 2025, HMI Learning, operator of the Happy Minds International pre‑school and daycare brand, secured strategic funding from Germany’s Klett Group to accelerate its expansion across India, reflecting strong investor confidence in the sector’s growth potential. A burgeoning middle class increasingly prioritizes academic readiness and holistic development, driving sustained demand for higher-quality preschool programs that go beyond conventional supervision. National policies emphasizing foundational literacy and numeracy have meaningfully elevated the importance of early childhood education within the broader national consciousness, encouraging both public and private investment.

Indian Pre-School/Childcare Market Trends:

Integration of Play-Based and Holistic Learning Approaches

Indian preschools are increasingly adopting play-based pedagogies that blend cognitive, emotional, and physical development. Influenced by globally recognized frameworks, operators are redesigning learning spaces to encourage creativity, problem-solving, and collaborative skills. In November 2024, Bachpan Play School launched “SPROUT,” India’s first preschool curriculum fully aligned with NEP 2020 and the National Curriculum Framework for Foundational Stage, emphasising activity‑ and play‑based learning across over 1200 branches nationwide. Parents today seek more than rote learning as they want environments where children develop curiosity and resilience. This shift has prompted curriculum overhauls, investment in specially trained educators, and redesigned infrastructure to support experiential learning as a cornerstone of the early childhood education journey across urban and semi-urban markets.

Technology-Enabled Parental Engagement and Classroom Delivery

Digital platforms and mobile applications are transforming how preschools communicate with parents, manage daily operations, and deliver supplementary learning content. Real-time updates on children's activities, progress tracking dashboards, and digital portfolios are becoming standard expectations among urban, tech-savvy parents. As per sources, preschools using childcare communication apps like Kiglee reported that parents save 30–90 minutes daily through real‑time updates and streamlined communication, boosting engagement and operational efficiency. These tools enhance transparency and trust between schools and families while streamlining administrative tasks such as attendance, fee collection, and event management.

Growing Demand for Structured Daycare and Extended-Hour Services

With dual-income households becoming the norm in urban India, demand for full-day and extended-hour childcare solutions has grown substantially. Modern preschools are expanding their service models to include nap routines, nutritious meal programs, and afternoon enrichment activities that accommodate parents' professional schedules. In January 2026, KLAY Harsha Icon in Hyderabad began offering extended daycare and full-day preschool services, providing structured routines, meals, and enrichment activities for working parents’ children. This evolution is reshaping facility design, staffing models, and pricing strategies. Operators are investing in safe, stimulating environments that balance supervision with learning, effectively blurring the line between traditional daycare and preschool education, creating a comprehensive early childhood development proposition.

Market Outlook 2026-2034:

The Indian pre-school/childcare market is poised for sustained revenue growth over the forecast period, supported by rising disposable incomes, expanding urbanization, and deepening parental commitment to quality early education. Government policy frameworks promoting foundational learning continue to strengthen both demand and investment confidence across the sector. Premium and technology-enabled offerings are expected to attract higher household spending, while growing female workforce participation sustains structural enrollment demand. The market presents a compelling long-term opportunity as organized operators and institutional investors recognize the enduring tailwinds shaping India's early childhood education landscape. The market generated a revenue of USD 5.1 Billion in 2025 and is projected to reach a revenue of USD 12.0 Billion by 2034, growing at a compound annual growth rate of 9.16% from 2026-2034.

Indian Pre-School/Childcare Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Facility |

Full Day Care |

64.5% |

|

Ownership |

Private |

89.2% |

|

Age Group |

2-4 Years |

48.5% |

|

Location |

Standalone |

48.5% |

|

Major Cities |

Delhi-NCR |

24.5% |

|

Region |

North India |

32.8% |

Facility Insights:

- Full Day Care

- After School Care

Full day care dominates with a market share of 64.5% of the total Indian pre-school/childcare market in 2025.

Full day care facilities have become the predominant service model in India's preschool landscape, driven by the widespread adoption of dual-income family structures in urban areas. As both parents enter the workforce, the need for reliable, structured, all-day supervision has intensified considerably. Full day care centers address this by offering comprehensive programs that combine learning activities, meals, recreational time, and nap schedules within a single managed environment. This integrated approach reduces the logistical burden on working parents while ensuring consistent developmental stimulation throughout the child's day.

The preeminence of the segment is also a reflection of a philosophical shift in the attitude of Indian parents, who now see the need for extended hours of preschooling as an opportunity for enrichment as opposed to mere childcare. In contemporary settings of full-day care, children are exposed to language, music, arts, and social interactions, which are now considered essential in the early developmental process of children. The operators of full-day care services are usually willing to spend more on infrastructure, staff-child ratios, and supplementary services like transportation and provision of meals, for which they charge a premium and make attractive business proposition for market players in search of long-term growth prospects.

Ownership Insights:

Access the comprehensive market breakdown Request Sample

- Public

- Private

Private leads with a share of 89.2% of the total Indian pre-school/childcare market in 2025.

Private ownership overwhelmingly shapes the Indian pre-school/childcare industry, reflecting the limited reach of government-run early education infrastructure and the strong entrepreneurial momentum within this sector. Private operators have led curriculum innovation, facility upgrades, and branded franchise expansion, establishing a competitive landscape that rewards quality and differentiation. In March 2025, Hello Kids Pre‑School Chain celebrated the opening of its 1,000 centre across India and Bangladesh, underscoring how private preschool brands are scaling rapidly through franchising and regional expansion. The flexibility inherent in private management enables rapid adaptation to parental preferences, regional language requirements, and evolving pedagogical trends, giving these operators a structural advantage over public alternatives in meeting the diverse demands of India's growing early learner population.

The high private ownership concentration also indicates significant investor confidence in the sector's long-term growth trajectory. Organized chains and individual entrepreneurs alike have identified early education as a recession-resilient business with recurring revenue and strong community trust. Access to private investment has enabled the adoption of digital learning tools, specially designed play spaces, and trained faculty, all of which command premium fees. As regulatory frameworks gradually mature, private-sector players are expected to further professionalize their offerings and consolidate market share across metropolitan and Tier-I cities.

Age Group Insights:

- Less Than 2 Years

- 2-4 Years

- 4-6 Years

- Above 6 Years

2-4 years exhibits a clear dominance with a 48.5% share of the total Indian pre-school/childcare market in 2025.

2-4 years represents the core target demographic for India's preschool sector, anchored in the scientific understanding that this period is among the most neurologically formative in a child's life. Early interventions during these years carry well-documented benefits for language acquisition, social adaptation, and cognitive development. Parents, increasingly aware of these developmental windows, are motivated to enroll their children in structured programs at younger ages, intensifying demand for facilities equipped with age-responsive curricula, appropriate safety infrastructure, and specially trained caregivers.

Beyond developmental science, this segment benefits from practical demand dynamics. Parents returning to work following maternity or paternity breaks typically seek childcare solutions for children within this age bracket, concentrating enrollment pressure on programs designed for this group. Preschool operators have responded by tailoring curriculum offerings, classroom environments, and caregiver training specifically for this age range. Specialized programs focusing on sensory learning, early literacy, and emotional regulation are growing in popularity, further reinforcing the commercial and educational primacy of this category within the broader market.

Location Insights:

- Standalone

- School Premises

- Office Premises

Standalone leads with a market share of 48.5% of the total Indian pre-school/childcare market in 2025.

Standalone dominates the location segment, reflecting the historical trajectory of India's early education sector, which developed largely through individual ownership and community-based operations. These centers benefit from deep neighborhood trust, personalized parental engagement, and operational agility. In Pune district alone, there were nearly 1,850 registered private pre‑primary centres in 2025, a mix of international branded chains and many small, standalone neighbourhood preschools serving local communities and working families. Unlike chain facilities bound by standardized formats, standalone operators can customize their offerings to meet the cultural, linguistic, and income-specific preferences of local communities.

Standalone facilities also appeal to operators due to lower franchise obligations, independent pricing power, and direct community relationships. Owners can rapidly adapt to local demand shifts, whether expanding hours, modifying curriculum, or adjusting fee structures, without institutional approval processes. For parents, standalone centers often offer greater proximity to home, familiar caregiver consistency, and perceived personalization of attention for their child. As India's urban population spreads into peripheral residential developments, standalone preschools continue to emerge as first-mover educational anchors in new neighborhoods.

Major Cities Insights:

- Delhi-NCR

- Bengaluru

- Hyderabad

- Chennai

- Mumbai

- Kolkata

- Rest of India

Delhi-NCR exhibits a clear dominance with a 24.5% share of the total Indian pre-school/childcare market in 2025.

Delhi-NCR commanding position in the major city segment stems from its combination of high population density, expanding nuclear family prevalence, and a concentration of working professionals demanding quality early education solutions. NCR encompasses a diverse economic geography ranging from established metropolitan zones to fast-growing satellite corridors, each generating strong demand for both premium and mid-market preschool options. The region's high proportion of dual-income households creates sustained structural demand for full-day childcare, making it one of the most commercially attractive urban markets for preschool operators across India.

The dense infrastructure established educational culture, and policy proximity to national early childhood development initiatives further reinforce Delhi-NCR's preschool market leadership. A culturally competitive parenting environment has made NCR parents among the earliest adopters of modern preschool methodologies, including international curricula and technology-enabled learning platforms. This demand sophistication has driven above-average investment in facility quality and educator training within the region, widening the gap between NCR's preschool ecosystem and those of smaller cities. Continued residential expansion in peripheral towns is expected to sustain enrollment growth.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India dominates with a market share of 32.8% of the total Indian pre-school/childcare market in 2025.

North India dominance in the preschool/childcare market is underpinned by a combination of population scale, rapid urbanization, and increasing parental investment in early education. The region is home to some of India's largest urban agglomerations, generating high absolute demand for childcare infrastructure. It has witnessed significant growth in organized preschool chains and branded franchise operations, reflecting improved access to investment capital and growing consumer sophistication. The presence of Delhi-NCR as the country's largest metropolitan economy further amplifies North India's commanding share within the national early childhood education market.

Cultural and demographic factors also contribute to North India's sustained market leadership. The region's relatively younger population profile, coupled with rising enrollment of women in the workforce, has created strong structural demand for professional childcare services. Middle-class families in North Indian cities increasingly regard early education as an investment in academic readiness rather than merely a childcare arrangement, driving willingness to pay for higher-quality organized programs. Government initiatives promoting early childhood development are progressively better implemented in North India's urban centers, creating a supportive environment for both demand growth and supply-side investment.

Market Dynamics:

Growth Drivers:

Why is the Indian Pre-School/Childcare Market Growing?

Rising Female Workforce Participation Driving Professional Childcare Demand

India's steadily growing female labor force participation has emerged as a powerful structural driver of preschool and childcare demand. As more women pursue professional careers across formal and informal sectors, dual-income households increasingly depend on organized childcare to fulfill both supervisory and developmental functions. As per sources, India’s female labour force participation rose to 41.7%, nearly doubling since 2017‑18, driven by initiatives like Mission Shakti and expanded maternity and childcare benefits. This shift has transformed preschool enrollment from an aspirational choice into a practical household necessity, expanding the addressable market significantly.

Government Policy Frameworks Supporting Early Childhood Development

Supportive government policy has meaningfully strengthened the foundations of India's preschool market by elevating early childhood education as a national developmental priority. Policy frameworks emphasizing foundational learning, structured curricula, and minimum quality benchmarks have encouraged greater parental confidence in organized preschool enrollment. Increased public investment in early childhood infrastructure and teacher training programs has also created a more favorable operating environment for private players. This policy momentum signals sustained governmental commitment to early education, reinforcing both consumer demand and institutional investment across the sector.

Urbanization and the Transition Toward Nuclear Family Structures

India's accelerating urbanization is fundamentally reshaping household dynamics in ways that directly fuel preschool demand. Migration to cities has eroded traditional joint family arrangements where extended relatives historically provided informal childcare, leaving nuclear households reliant on professional solutions. In May 2025, Indian preschool and daycare chain Footprints Childcare raised USD 7.5 million in Series A funding to expand its network of 175 centres across more than 25 cities, a move driven by rising urban parent demand for structured early education and childcare services near workplaces and residential hubs. This structural shift is most pronounced in fast-growing metropolitan regions where career mobility and population density are highest.

Market Restraints:

What Challenges the Indian Pre-School/Childcare Market is Facing?

Affordability Constraints Limiting Broader Market Penetration

Private preschools, which dominate the Indian market, often operate at price points that remain inaccessible for lower-income households despite strong aspirational demand for quality early education. The cumulative cost of childcare, encompassing tuition, transportation, uniforms, and ancillary charges, creates a significant financial burden for families in the informal economy, limiting addressable market penetration and leaving substantial unmet demand across economically underserved communities.

Shortage of Qualified Early Childhood Educators

The rapid expansion of the organized preschool sector has outpaced the availability of formally trained early childhood educators across India. Quality instruction requires specialized pedagogical training that existing teacher education pipelines have not yet scaled to adequately supply. This shortage constrains operators' ability to maintain consistent curriculum standards, restricts geographic expansion into smaller cities, and creates competitive labor pressure that elevates personnel costs for established preschool operators.

Fragmented Regulatory Framework Across States

India's preschool and childcare sector lack a unified national regulatory framework, with oversight responsibilities distributed unevenly across state governments, local bodies, and education ministries. This fragmentation produces inconsistent quality standards, licensing requirements, and safety norms across regions, complicating expansion strategies for organized operators. Regulatory ambiguity reduces investor confidence and operational predictability, collectively slowing the sector's formalization and long-term standardization.

Competitive Landscape:

The Indian pre-school/childcare market presents a heterogeneous competitive environment, characterized by the coexistence of organized branded chains, regional multi-city operators, and a large base of independent standalone facilities. Organized players compete on the basis of curriculum innovation, brand recognition, facility quality, and technology integration, while standalone operators leverage localized relationships, pricing flexibility, and community trust. The private sector commands an overwhelming share of the market, with competitive intensity concentrated in metropolitan regions where disposable incomes and parental aspirations are highest. Differentiation through internationally aligned pedagogies, digital learning tools, and extended service offerings has become a key battleground as operators seek to attract increasingly discerning urban parents willing to invest in premium early education solutions.

Some of the key players include:

- Kidzee

- Bachpan Global

- Eurokids

- Tree House Education & Accessories Ltd.

- Shemrock Play School

- Kangaroo Kids

- Hello Kids

- Little Millennium

- Podar Jumbo Kids

- T.I.M.E. Kids

Recent Developments:

- In January 2026, Alphabetz International Preschool celebrated a landmark year by inaugurating 60 new centers across 11 Indian states, including Telangana, Karnataka, and Andhra Pradesh. This expansion reflects strong franchise partner trust, operational excellence, and nationwide growth, reinforcing Alphabetz’s position as a leading provider of affordable, international-standard preschool education.

Indian Pre-School/Childcare Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Facilities Covered | Full Day Care, After School Care |

| Ownerships Covered | Public, Private |

| Age Groups Covered | Less Than 2 Years, 2-4 Years, 4-6 Years, Above 6 Years |

| Locations Covered | Standalone, School Premises, Office Premises |

| Major Cities Covered | Delhi-NCR, Bengaluru, Hyderabad, Chennai, Mumbai, Kolkata, Rest of India |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Kidzee, Bachpan Global, EuroKids, Tree House Education and Accessories Ltd., Shemrock Play School, Kangaroo Kids, Hello Kids, Little Millennium, Podar Jumbo Kids, T.I.M.E. Kids etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Pre-School/Childcare Market in India Report

The Indian pre-school/childcare market size was valued at USD 5.1 Billion in 2025.

The Indian pre-school/childcare market is expected to grow at a compound annual growth rate of 9.16% from 2026-2034 to reach USD 12.0 Billion by 2034.

Full day care held the largest Indian pre-school/childcare market share, driven by growing dual-income household prevalence in urban areas, sustained demand for all-day supervised childcare, and the appeal of integrated learning and care programs that meet parents' professional and developmental needs.

Key factors driving the Indian pre-school/childcare market include rising female workforce participation, government policy support through the National Education Policy, rapid urbanization reshaping household structures toward nuclear families requiring professional childcare and increasing parental awareness of early childhood developmental milestones and structured educational benefits.

Major challenges include affordability constraints limiting lower-income segment penetration, a shortage of formally qualified early childhood educators, fragmented state-level regulatory frameworks, inconsistent quality standards across regions, and limited organized childcare infrastructure in Tier-II cities and rural communities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)