Indian Sorbitol Market Size, Share, Trends and Forecast by Application, Feedstock, Type and Distribution Channel, 2026-2034

Indian Sorbitol Market Size, Share, Trends & Forecast (2026-2034)

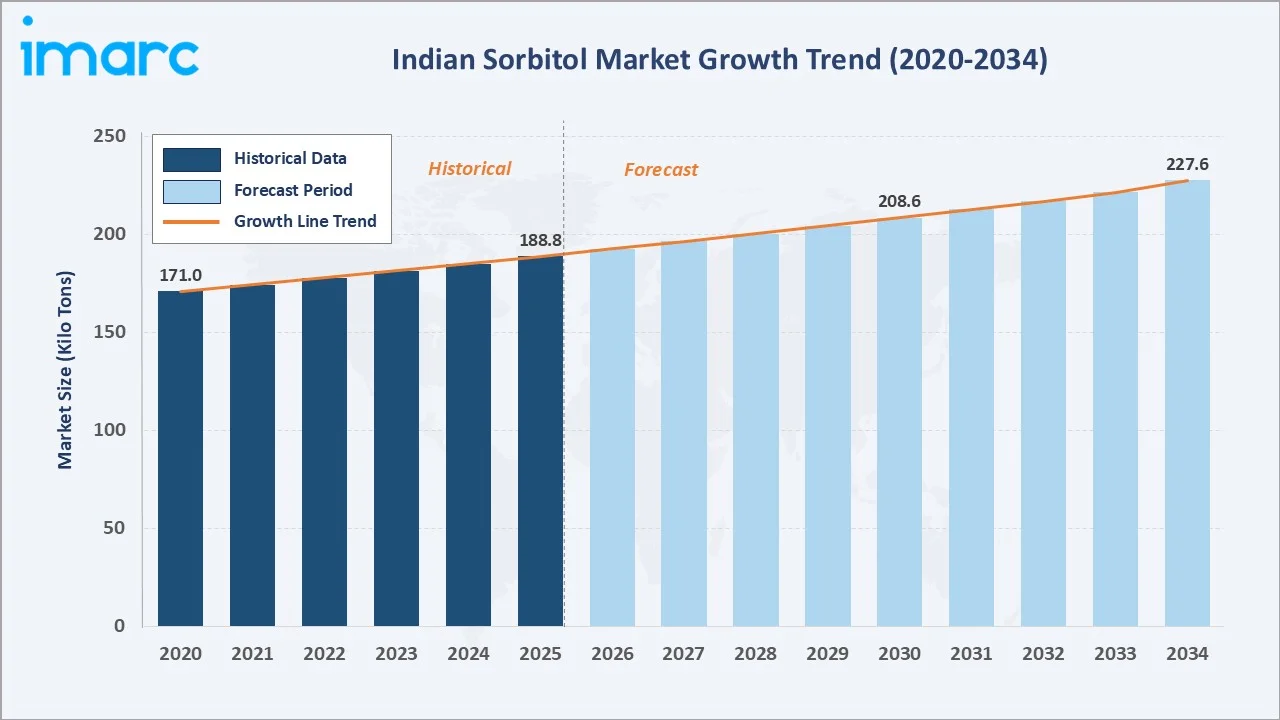

The Indian sorbitol market reached 188.8 Kilo Tons in 2025 and is projected to reach 227.6 Kilo Tons by 2034, growing at a CAGR of 2.01% during 2026-2034. Market growth is driven by expanding pharmaceutical excipient demand, the growing sugar-free food and confectionery sector, rising oral care product consumption, and increasing export competitiveness of Indian sorbitol producers in global markets.

Market Snapshot

|

Metric |

Value |

|

Market Volume (2025) |

188.8 Kilo Tons |

|

Forecast Market Volume (2034) |

227.6 Kilo Tons |

|

CAGR (2026-2034) |

2.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

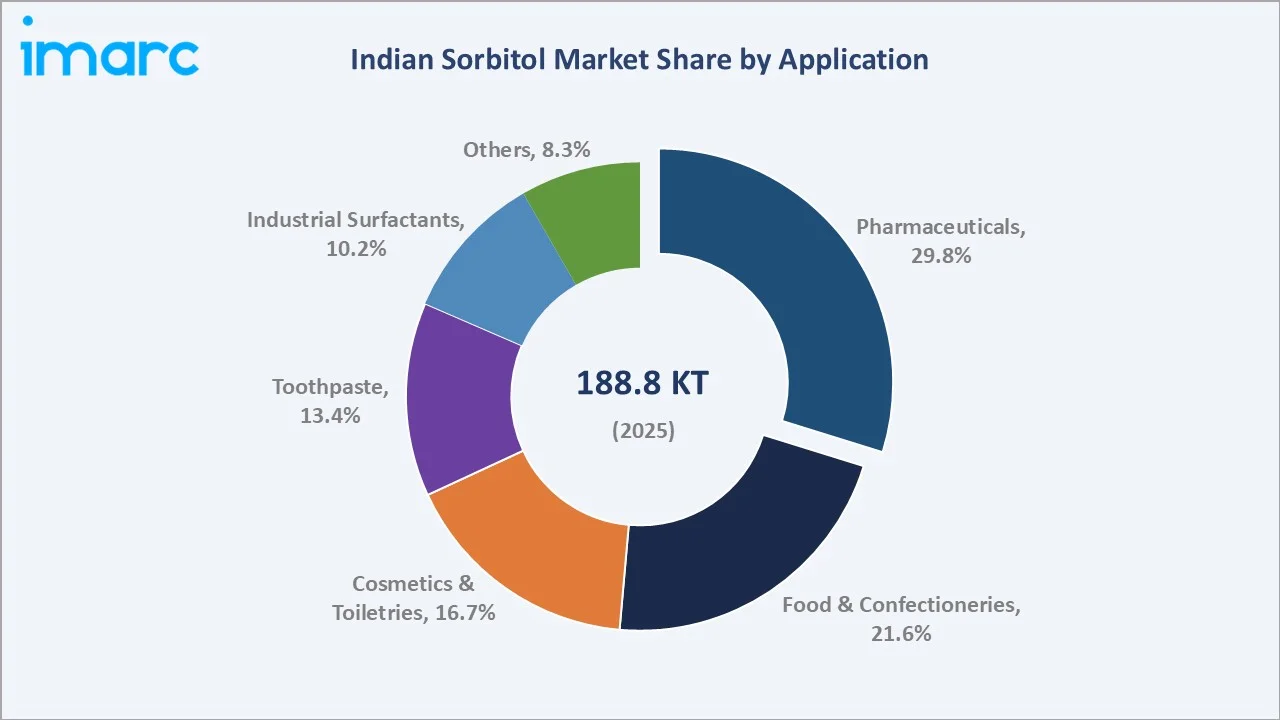

Pharmaceuticals' 29.8% application dominance reflects sorbitol's critical role as a tablet excipient, syrup sweetener, and humectant in a rapidly growing Indian pharmaceutical industry that is both serving domestic demand and expanding its global generic drug export footprint.

To get more information on this market, Request Sample

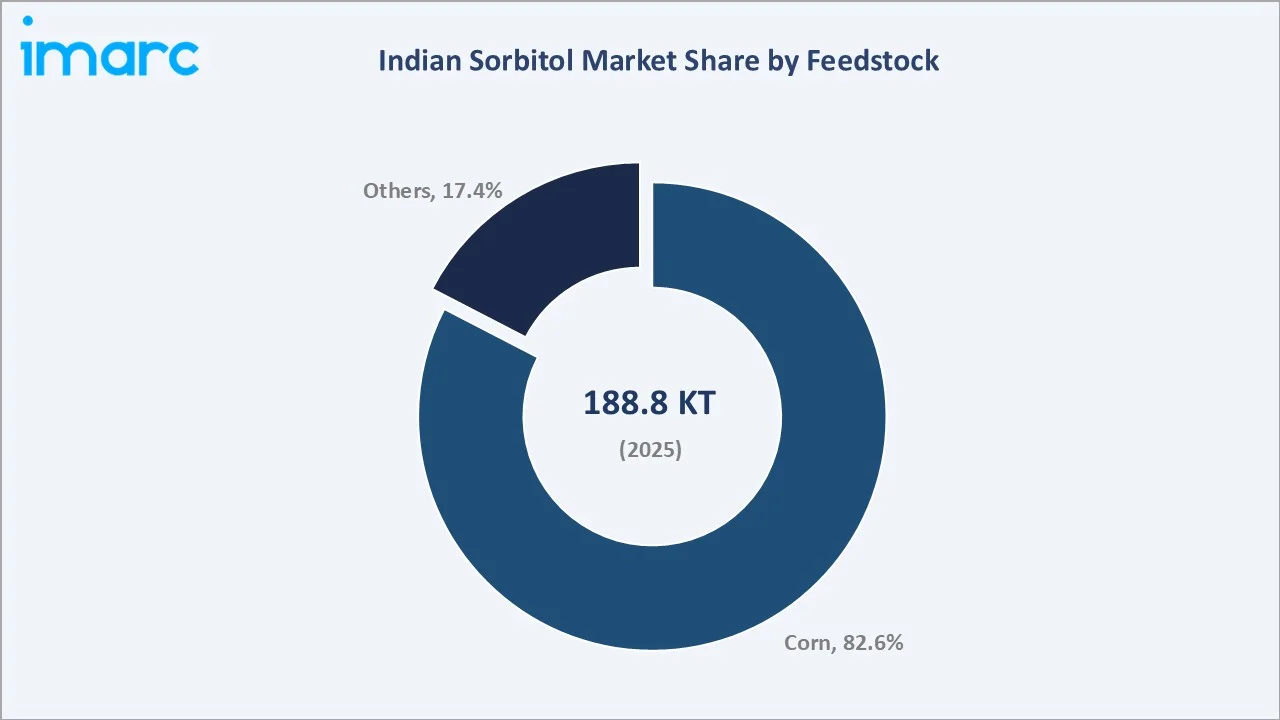

Corn feedstock's 82.6% share reflects the mature corn wet milling infrastructure in India that efficiently converts corn starch to glucose and subsequently to sorbitol via catalytic hydrogenation.

Executive Summary

The Indian sorbitol market is characterized by steady volume growth underpinned by structurally expanding demand from pharmaceuticals, processed foods, oral care, and industrial applications. From 188.8 Kilo Tons in 2025, the market will reach 227.6 Kilo Tons by 2034, adding 38.8 Kilo Tons at a 2.01% CAGR.

Pharmaceuticals lead applications at 29.8% in 2025, where sorbitol serves as a non-cariogenic sweetener in paediatric syrups, a tablet binder and diluent, a laxative API in constipation formulations, and a humectant in topical drug vehicles. Corn-derived sorbitol at 82.6% dominates feedstock, produced through starch extraction, enzymatic glucose conversion, and high-pressure catalytic hydrogenation at manufacturing facilities concentrated in Gujarat, Uttar Pradesh, and Punjab.

Key players, including Gulshan Polyols Ltd., Gujarat Ambuja Exports Limited, Kasyap Sweetners Private Limited, The Sukhjit Starch & Chemicals Ltd., and Gayatri Bio Organics Ltd. compete through production scale, product purity grade range, pharmaceutical certification credentials, and export market access across over 50 countries.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Pharmaceuticals – 29.8% share (2025) |

|

Second Application |

Food & Confectioneries – 21.6% |

|

Largest Feedstock |

Corn – 82.6% share (2025) |

|

Alternative Feedstock |

Others – 17.4% |

|

Top Companies |

Gulshan Polyols Ltd., Gujarat Ambuja Exports Limited, Kasyap Sweetners Private Limited, The Sukhjit Starch & Chemicals Ltd., Gayatri Bio Organics Ltd. |

Key Analytical Observations:

- Pharmaceuticals at 29.8% (2025) is the largest and fastest-growing application segment for Indian sorbitol. Sorbitol serves multiple functions in pharmaceutical formulations: as a sweetening and flavoring agent in paediatric and geriatric liquid formulations, as a binder, filler, and diluent in direct compression tablet manufacturing, as a laxative active pharmaceutical ingredient (API) in osmotic laxative formulations, and as a stabilizer in protein and vaccine formulations.

- Food and confectioneries at 21.6% (2025) serve the growing sugar-free, reduced-calorie, and diabetic-friendly product segments across biscuits, chocolates, chewing gums, mints, hard candies, and functional confectionery.

- Corn feedstock at 82.6% (2025) is dominant because corn starch is the most cost-efficient and consistent-quality raw material for industrial sorbitol production in India. Indian corn availability at competitive prices supports cost-competitive sorbitol manufacturing for both domestic supply and export markets.

- Industrial surfactants at 10.2% (2025) represent a chemically important application where sorbitol is the precursor for sorbitan esters and polysorbates, non-ionic emulsifiers widely used in pharmaceutical, food, and cosmetic formulations.

Indian Sorbitol Market Overview

Sorbitol is a sugar alcohol produced industrially through the catalytic hydrogenation of glucose derived from corn starch or other carbohydrate feedstocks. With a molar mass of 182.17 g/mol, 60% relative sweetness versus sucrose, low glycaemic index, and multifunctional physical properties, sorbitol serves as a versatile ingredient across pharmaceuticals, food and beverages, personal care, and industrial chemical applications.

India is the second-largest producer of sorbitol, accounting for 19.73% of global output. Supported by its expanding starch processing industry and emphasis on export-oriented manufacturing, the country supplies sorbitol to regional pharmaceutical and oral care industries while meeting growing demand from international markets.

Market Dynamics

To evaluate market opportunities, Request Sample

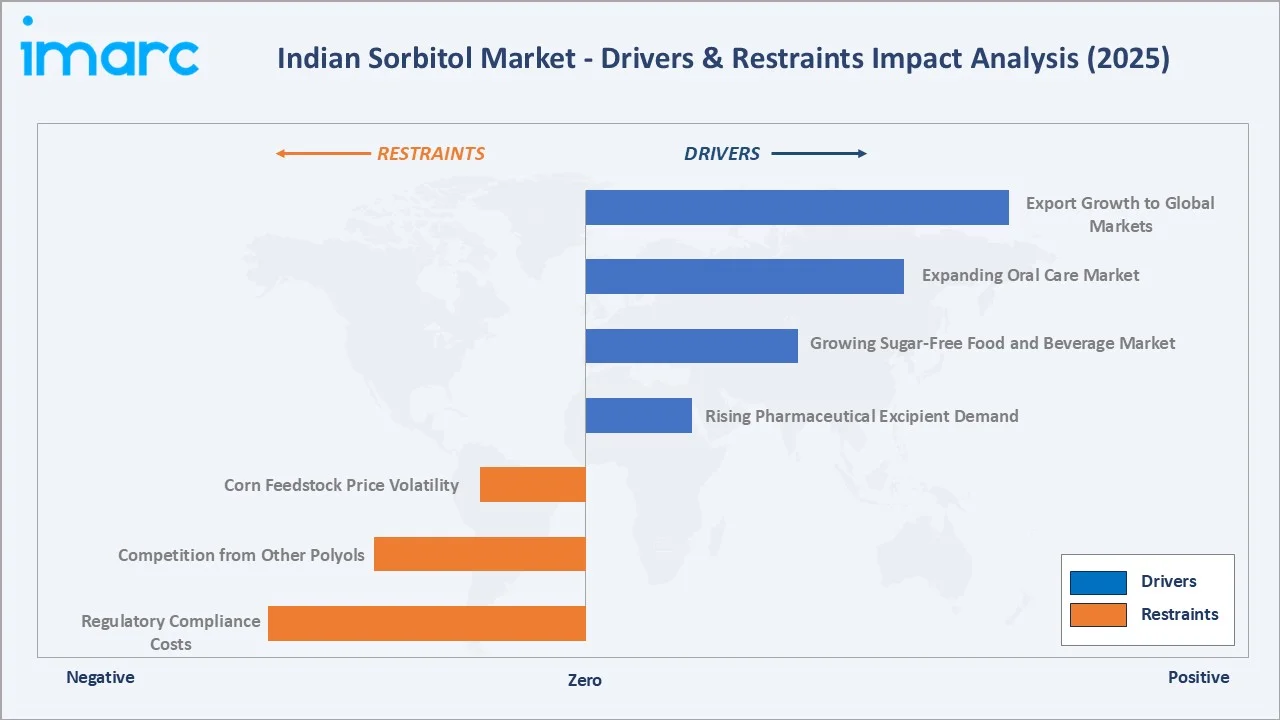

Market Drivers

- Rising Pharmaceutical Excipient Demand: India's pharmaceutical industry is the world's largest producer of generic drugs by volume, manufacturing approximately 20% of global generic medicine supply. The industry's growth at 8–10% annually generates increasing demand for pharmaceutical-grade sorbitol as a multi-functional excipient.

- Growing Sugar-Free Food and Beverage Market: India's rapidly growing diabetic and health-conscious consumer population is expected to drive the sugar-free and reduced-calorie food and beverage market at 8.84% during 2026-2034. Sorbitol-containing products, including sugar-free chewing gum, chocolates, mints, and low-calorie confectionery, are growing their shelf presence in modern retail and e-commerce channels.

- Expanding Oral Care Market: India's oral care market is projected to grow at 4.15% during 2026-2034, driven by rising dental hygiene awareness, increasing toothpaste penetration in rural markets, and premiumization toward whitening, sensitivity, and natural ingredient toothpaste variants.

- Export Growth to Global Markets: Competitive corn feedstock costs, improving product quality and certification standards, and growing international buyer awareness of Indian sorbitol suppliers are driving export market development.

Market Restraints

- Corn Feedstock Price Volatility: Corn prices are subject to global commodity price fluctuations driven by weather patterns, crop yields, energy price impacts on corn-ethanol demand, and international commodity speculation.

- Competition from Other Polyols: Sorbitol competes with other polyol sweeteners, including maltitol, xylitol, mannitol, and erythritol, in food and pharmaceutical applications. Xylitol's superior dental health claims give it a marketing advantage in premium oral care and confectionery.

- Regulatory Compliance Costs: Meeting the multiple pharmacopoeia standards required for pharmaceutical-grade sorbitol, food-grade specifications, and export market certification requirements requires significant investment in analytical laboratory infrastructure, quality management systems, and regulatory affairs capabilities.

Market Opportunities

- Pharmaceutical Grade Sorbitol Premiumization: The development and commercialization of ultra-high-purity sorbitol grades represents a premium value-addition opportunity for Indian sorbitol producers. These functional excipient grades command 3–5 times the commodity sorbitol solution price and serve the fast-growing oral solid dosage (OSD) pharmaceutical manufacturing market in India and globally.

- Downstream Sorbitan Ester and Polysorbate Production: Integrated downstream processing of sorbitol to sorbitan esters and polysorbates converts a commodity sorbitol value chain into a specialty emulsifier value chain.

- Bio-Based and Non-GMO Sorbitol Premium Segment: Growing demand in European and North American markets for certified non-GMO and bio-based sorbitol represents a premium market segment accessible to Indian producers.

Market Challenges

- Import Competition from China and Indonesia: Indian sorbitol producers face competitive pressure from large-scale Chinese and Indonesian sorbitol exporters in domestic and third-country export markets. China's massive integrated corn processing infrastructure and Indonesia's cassava-based sorbitol provide significant scale cost advantages.

- Limited Awareness of Advanced Sorbitol Applications: Beyond conventional liquid sorbitol solution, many Indian industrial buyers are not aware of advanced sorbitol product forms that could provide superior functional performance in their formulations.

Emerging Market Trends

1. Gulshan Polyols 250 KLPD Ethanol Plant and Sorbitol Expansion

In June 2024, Gulshan Polyols commenced commercial operations of a 250 KLPD grain-based ethanol plant in Assam, India, representing a strategic diversification into biofuels while leveraging its existing grain processing infrastructure. The expansion signals Gulshan's integrated grain processing capability that underpins its sorbitol manufacturing cost base.

2. Expansion of Domestic Sorbitol Manufacturing Capacity

In February 2024, Gujarat Ambuja Exports commissioned a 100 tons-per-day sorbitol unit at its existing facility in Hubli, Karnataka. The addition increased the company’s cumulative sorbitol manufacturing capacity to 500 tons per day across four locations, positioning it as one of India’s largest sorbitol manufacturers.

3. Non-GMO and Clean-Label Sorbitol Certification Growth

European food and cosmetic manufacturers are increasingly mandating non-GMO and clean-label certified ingredients in their supply chains. Indian sorbitol producers sourcing from identity-preserved non-GMO corn suppliers in India are pursuing ISCC, ProTerra, and Non-GMO Project Verified certification to access premium European export market buyers.

4. Sorbitol in Functional Food and Nutraceutical Applications

India's growing functional food, nutraceutical, and sports nutrition market is creating new sorbitol demand in applications such as sugar-free energy bars, vitamin gummies, protein chews, and prebiotic fiber supplements, where sorbitol's combined sweetening, humectancy, and prebiotic properties provide multi-functional value.

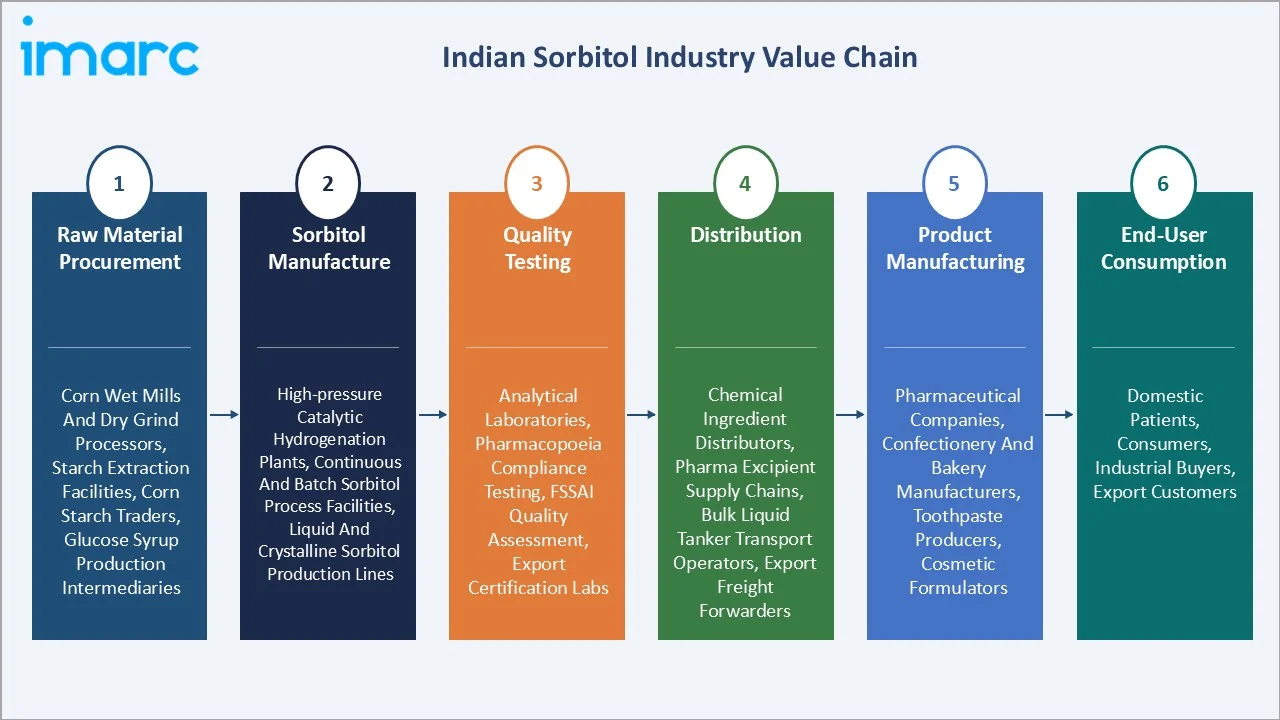

Industry Value Chain Analysis

The Indian sorbitol value chain is vertically integrated at major manufacturers, spanning corn procurement through starch processing, sorbitol manufacturing, quality certification, and multi-sector distribution.

|

Stage |

Key Players / Examples |

|

Raw Material Procurement |

Corn wet mills and dry grind processors, starch extraction facilities, corn starch traders, glucose syrup production intermediaries |

|

Sorbitol Manufacture |

High-pressure catalytic hydrogenation plants, continuous and batch sorbitol process facilities, liquid and crystalline sorbitol production lines |

|

Quality Testing |

Analytical laboratories, pharmacopoeia compliance testing, FSSAI quality assessment, export certification labs |

|

Distribution |

Chemical ingredient distributors, pharma excipient supply chains, bulk liquid tanker transport operators, export freight forwarders |

|

Product Manufacturing |

Pharmaceutical companies, confectionery and bakery manufacturers, toothpaste producers, cosmetic formulators |

|

End-User Consumption |

Domestic patients, consumers, industrial buyers, export customers |

Technology Landscape in the Indian Sorbitol Industry

Catalytic Hydrogenation Technology

Indian sorbitol production uses continuous or batch high-pressure catalytic hydrogenation of glucose using Raney nickel or supported ruthenium catalysts at 100–150 bar hydrogen pressure and 130–150°C. Modern continuous hydrogenation plants achieve 95%+ sorbitol yield from glucose input with stable catalyst activity over multi-year operating cycles, enabled by catalyst regeneration programs.

Purification and Crystallization Technology

Pharmaceutical-grade and crystalline sorbitol production requires multi-stage purification, including activated carbon decolorization, ion exchange demineralization, membrane ultrafiltration, and vacuum evaporation concentration to achieve 70% liquid sorbitol solution specification. Crystalline sorbitol production requires controlled cooling crystallization from concentrated sorbitol solution, seeding, crystal growth management, and fluidized bed drying to achieve free-flowing crystalline particle specifications.

Quality Management and Certification Systems

Leading Indian sorbitol producers have established comprehensive quality management systems aligned with pharmaceutical GMP, food safety, and export market requirements. Many companies maintain ISO 9001:2015, FSSC 22000 food safety, GMP (WHO-cGMP), and multiple pharmacopoeia-grade compliance for their pharmaceutical-grade sorbitol products.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Pharmaceuticals |

29.8% |

2025 |

|

Feedstock |

Corn |

82.6% |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

By Application

Pharmaceuticals lead at 29.8% in 2025. Sorbitol's pharmaceutical utility spans liquid formulations, solid dosage forms, and osmotic laxative formulations. India's pharmaceutical industry generates an estimated 50,000–60,000 tons of annual sorbitol demand and is growing at the fastest rate among all application segments.

To access detailed market analysis, Request Sample

Food and confectioneries at 21.6% serve sugar-free and diabetic product categories. Cosmetics and toiletries at 16.7% use sorbitol as a skin conditioning humectant in moisturizers, lotions, and shampoos. Toothpaste at 13.4% uses sorbitol as a functional humectant, texturizer, and sweetener, a significant and stable demand pool as India's oral care market continues penetrating rural and semi-urban populations.

By Feedstock

Corn feedstock dominates at 82.6% in 2025, reflecting India's mature corn processing industry and the feedstock's technical advantages, high and consistent starch content, established corn wet milling infrastructure, and competitive procurement supply chains across Madhya Pradesh, Bihar, Karnataka, and Telangana producing states.

Others at 17.4% include wheat starch-based sorbitol, cassava/tapioca starch-based sorbitol for specific applications, and sugarcane molasses-derived glucose as an alternative feedstock in South Indian production facilities.

Competitive Landscape

The Indian sorbitol market is moderately concentrated, with Gulshan Polyols Ltd. and Gujarat Ambuja Exports Limited together accounting for approximately 55–65% of domestic production capacity.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

Gulshan Polyols Ltd. |

Gulshan Polyols |

Market Leader |

One of India's largest sorbitol producers, an integrated corn-to-polyols value chain with pharma-grade certification |

|

Gujarat Ambuja Exports Limited |

Gujarat Ambuja Exports Limited (GAEL) |

Market Leader |

India's largest corn processor with integrated sorbitol production, large-scale low-cost manufacturing, broad domestic and export market coverage |

|

Kasyap Sweetners Private Limited |

Kasyap Sweetners |

Strong Challenger |

Multi-polyol product range, pharmaceutical and food grade specialization, broad industry application coverage, established customer relationships |

|

The Sukhjit Starch & Chemicals Ltd. |

Sukhjit |

Challenger |

Corn/maize-based starch processor, offers pharmaceutical and food-grade sorbitol |

|

Gayatri Bio Organics Ltd |

Gayatri |

Challenger |

South India sorbitol production, pharma, and food grade capabilities, export market development |

Kasyap Sweetners Private Limited, The Sukhjit Starch & Chemicals Ltd., and Gayatri Bio Organics Ltd., serve specific regional markets and export segments, while smaller producers address niche pharmaceutical and specialty grades.

Key Company Profiles

Gulshan Polyols Ltd.

Gulshan Polyols Ltd. is one of India's largest sorbitol manufacturers. The company operates a fully integrated corn-to-polyols manufacturing complex producing sorbitol, maltitol, dextrose, and corn starch-based ingredients.

- Product Portfolio: NC, BP Crystalline and Non-Crystalline grades of Sorbitol (D-Glucitol)

- Recent Developments: In January 2025, Gulshan Polyols Ltd. resumed operations and production at its Goalpara, Assam plant after a temporary shutdown for investigations following an incident at the facility. The plant supports the company’s production of Sorbitol-70%, a starch derivative used in oral care, cosmetics, pharmaceuticals, vitamin C, and food products.

- Strategic Focus: Pharmaceutical-grade sorbitol market leadership, export market expansion, downstream maltitol and polyol derivative development, and integrated grain-to-chemical value chain optimization.

Gujarat Ambuja Exports Limited

Gujarat Ambuja Exports Limited is one of India's largest corn processors and a major sorbitol producer, leveraging its large-scale integrated corn wet milling infrastructure across multiple facilities.

- Product Portfolio: Sorbitol 70% Solution

- Recent Developments: In October 2024, Gujarat Ambuja Exports Limited’s Udham Singh Nagar, Uttarakhand facility received EXCiPACT GMP certification from SGS as a pharmaceutical excipient supplier. The certification covers the manufacture of Sorbitol 70% for pharmaceutical applications, reinforcing the company’s compliance with recognized good manufacturing practice requirements.

- Strategic Focus: Scale-based cost leadership in sorbitol and corn derivatives, geographic market expansion in Southeast Asia and the Middle East, food and pharma dual-market certification maintenance, and by-product valorization to improve overall production economics.

Market Concentration Analysis

The Indian sorbitol market is moderately concentrated. Gulshan Polyols Ltd. and Gujarat Ambuja Exports Limited together hold approximately 55–65% of domestic production capacity. The top five producers collectively account for approximately 80–85% of domestic production, with a long tail of smaller regional producers serving local market segments.

The concentration level is higher in pharmaceutical-grade sorbitol, where certification requirements limit the producer universe to companies with GMP-qualified manufacturing and NABL-accredited analytical capabilities.

Investment & Growth Opportunities

Fastest Growing Segments

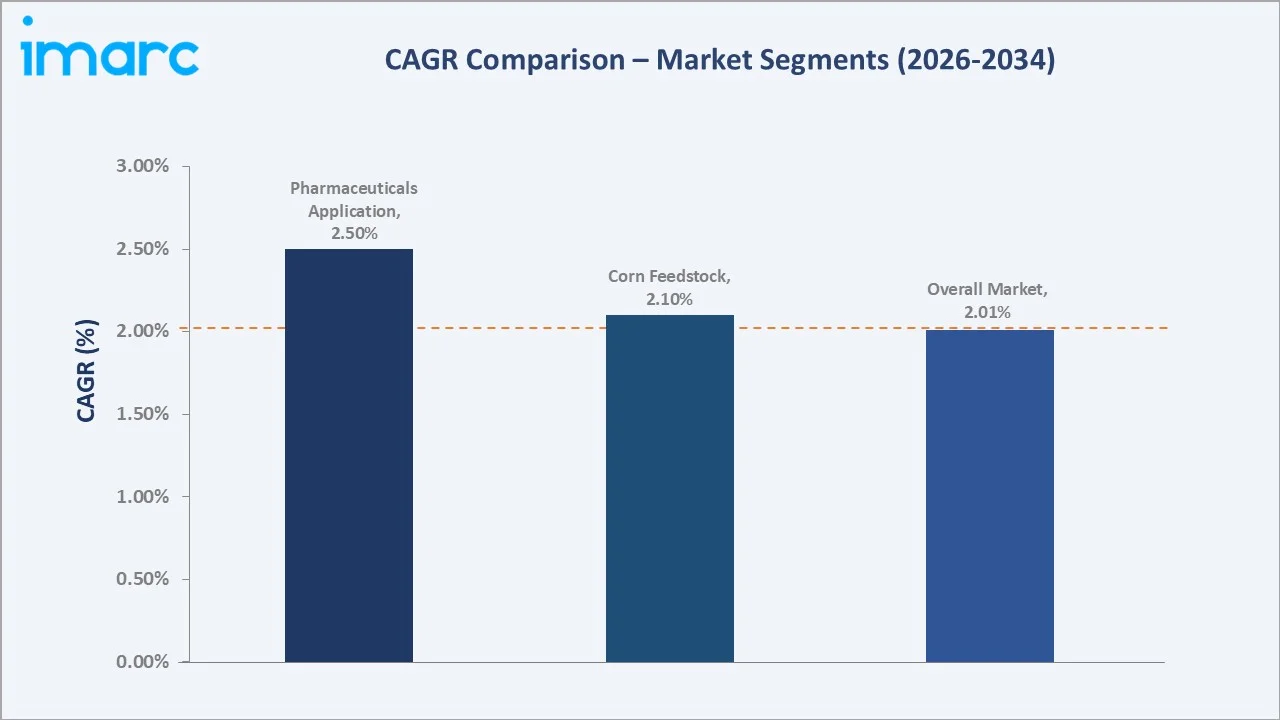

Pharmaceutical-grade sorbitol (~2.50% CAGR), crystalline direct compression sorbitol excipients, polysorbate derivatives, and non-GMO certified export sorbitol represent the highest-value growth opportunities through 2034, collectively addressing a combined incremental market of approximately 20+ Kilo Tons by 2034.

Emerging Market Expansion

Africa represents the fastest-growing export market for Indian sorbitol, with rapidly expanding pharmaceutical manufacturing in Nigeria, Kenya, South Africa, and Egypt creating structured demand for IP/BP-certified sorbitol excipients. Indian sorbitol's competitive pricing and WHO-GMP manufacturing credentials position it as the preferred supply source for African pharma excipient buyers.

Venture and Institutional Investment Trends

- Indian sorbitol manufacturers are attracting institutional investment for capacity expansion and pharmaceutical grade upgrade projects, supported by the PLI (Production Linked Incentive) scheme for API and pharma excipient manufacturing that incentivizes domestic supply chain development.

- Downstream investment in sorbitan ester and polysorbate manufacturing, converting sorbitol into high-value specialty emulsifiers, is a capital allocation priority for producers seeking to capture 10–20× value multiplication per kg of sorbitol feedstock.

Future Market Outlook (2026-2034)

The Indian sorbitol market will reach 227.6 Kilo Tons by 2034 from 188.8 Kilo Tons in 2025, adding 38.8 Kilo Tons at a 2.01% CAGR. Growth will be broad-based across pharmaceutical, food, oral care, and industrial applications, with pharmaceutical-grade premium market development being the key value driver above the volume growth rate.

India's sorbitol export volume is expected to continue growing at 10%+ annually, driven by expanding African pharmaceutical manufacturing, Southeast Asian food industry development, and Middle Eastern cosmetic manufacturing growth. Pharmaceutical-grade and crystalline sorbitol will command a growing share of total market value as Indian producers invest in advanced purification and crystallization capabilities to compete in premium excipient markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 65 industry participants in 2024–2025, including sorbitol manufacturers, pharmaceutical excipient buyers, food industry procurement teams, chemical distributors, and industry analysts across Gujarat, Uttar Pradesh, Maharashtra, and Punjab. Expert input validated market sizing, application adoption trends, and production capacity data.

Secondary Research

Secondary research encompassed manufacturer annual reports, MCA company filings, Directorate General of Commercial Intelligence and Statistics, FSSAI regulatory data, pharmacopoeia standards documents, and trade publications, including Chemical Engineering World, Pharma Horizons, and Food Ingredients First.

Forecasting Models

Market volume estimations used bottom-up forecasting incorporating domestic production capacity by manufacturer, application segment demand growth assumptions, import-export balance data, and end-user industry growth rates. A base-case CAGR of 2.01% reflects consensus validated against manufacturer volume disclosures and industry association production estimates.

Indian Sorbitol Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Kilo Tons |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Pharmaceuticals, Cosmetics and Toiletries, Toothpaste, Food and Confectioneries, Industrial Surfactants, Others |

| Feedstocks Covered | Corn, Others |

| Types Covered | Liquid Sorbitol, Crystal Sorbitol |

| Distribution Channels Covered | Distributors, Manufacturers |

| Companies Covered | Gulshan Polyols Ltd., Gujarat Ambuja Exports Limited, Kasyap Sweetners Private Limited, The Sukhjit Starch & Chemicals Ltd., Gayatri Bio Organics Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Indian sorbitol market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Indian sorbitol market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Indian sorbitol industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Indian Sorbitol Market Report

The market reached 188.8 Kilo Tons in 2025 and is projected to reach 227.6 Kilo Tons by 2034 at a 2.01% CAGR.

Pharmaceuticals lead with a 29.8% share in 2025, driven by sorbitol's critical role as a tablet excipient, liquid formulation sweetener, and osmotic laxative active in India's large generic drug industry.

Corn dominates at 82.6% in 2025, supported by India's mature corn wet milling infrastructure, competitive corn prices, and by-product valorization advantages of integrated corn processing.

Gulshan Polyols Ltd., Gujarat Ambuja Exports Limited, Kasyap Sweetners Private Limited, The Sukhjit Starch & Chemicals Ltd., and Gayatri Bio Organics Ltd., are some of the leading players in the market.

Rising pharmaceutical excipient demand, growing sugar-free food market, expanding oral care market, and increasing export competitiveness of Indian sorbitol producers are the primary drivers.

Gujarat (Gujarat Ambuja Exports Limited) and Uttar Pradesh (Gulshan Polyols Ltd.) are the dominant production states, with Punjab (Sukhjit Starch), Maharashtra, and others contributing additional capacity.

Corn feedstock price volatility, competition from Chinese and Indonesian producers, regulatory compliance costs, and competition from alternative polyols are key challenges.

Downstream processing of sorbitol into sorbitan esters and polysorbates offers 10–20× value multiplication per kg of sorbitol input, representing a high-return diversification opportunity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade