Indian Sports and Fitness Goods Market Size, Share, Trends and Forecast by Product Type, Fitness Goods, Cardiovascular Training Goods, End Use, and Region, 2026-2034

Indian Sports and Fitness Goods Market Summary:

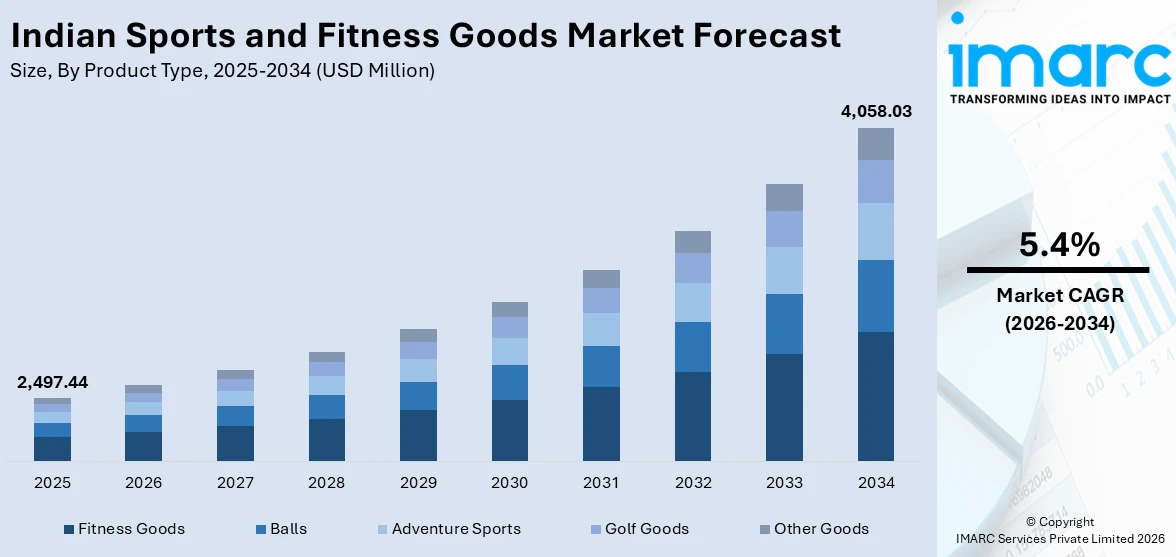

The Indian sports and fitness goods market size was valued at USD 2,497.44 Million in 2025 and is projected to reach USD 4,058.03 Million by 2034, growing at a compound annual growth rate of 5.4% from 2026-2034.

The Indian sports and fitness goods market is advancing steadily as the country embraces a cultural shift toward health consciousness and active living. Rapid urbanization and growing disposable incomes are empowering a broader consumer base to invest in quality sports and fitness products. Government-backed programs such as the Khelo India initiative and the Fit India Movement are fostering grassroots sports participation and strengthening the demand ecosystem for sports goods. India's commercial fitness sector has been expanding rapidly and is expected to witness significant growth over the coming years, reflecting a robust expansion in fitness-related spending across both organized and unorganized channels. The proliferation of fitness centers across tier-2 and tier-3 cities, coupled with rising home fitness adoption and technological innovations in smart equipment, is creating diverse demand channels. Social media influence, celebrity endorsements, and e-commerce accessibility are further accelerating consumer engagement, strengthening the Indian sports and fitness goods market share.

Key Takeaways and Insights:

- By Product Type: Fitness goods dominate the market with a share of 38.5% in 2025, owing to the growing emphasis on cardiovascular health and strength training among urban and semi-urban populations. Rising gym memberships and increasing adoption of home fitness solutions are fueling the market expansion.

- By Fitness Goods: Cardiovascular training goods lead the market with a share of 56.0% in 2025, driven by heightened consumer awareness about heart health and the widespread popularity of treadmills, stationary bikes, and elliptical trainers across health clubs and home settings.

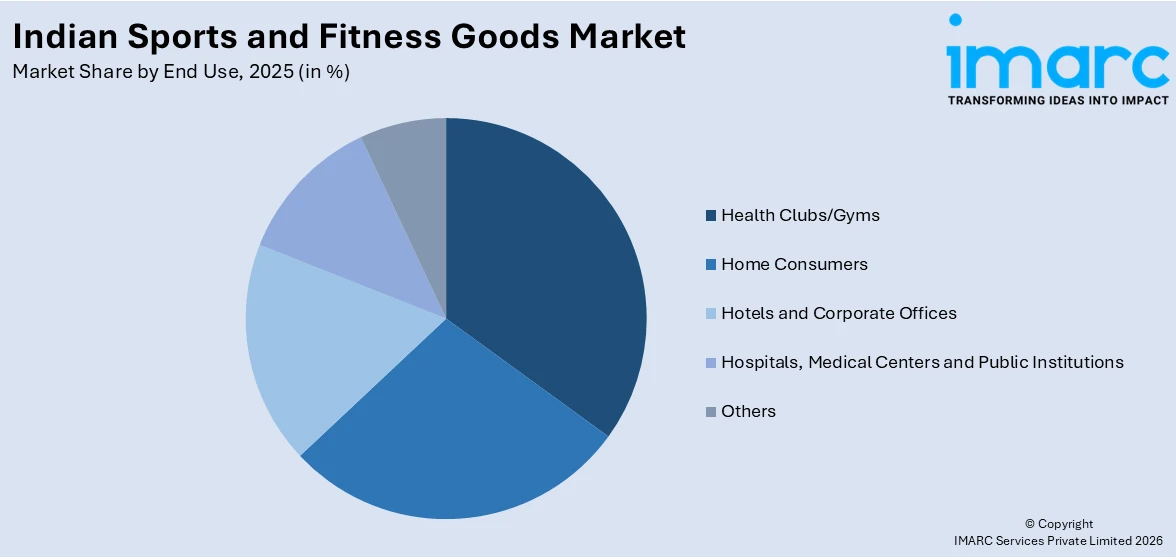

- By End Use: Health clubs/gyms represent the biggest segment with a market share of 34.2% in 2025, reflecting the rapid expansion of organized fitness facilities and franchise-driven gym chains that are penetrating new markets across Indian metropolitan and emerging urban areas.

- By Region: West and Central India is the largest region with 31.5% share in 2025, driven by concentration of major commercial fitness hubs in Mumbai and Pune, higher consumer spending power, and strong presence of sports goods manufacturing and distribution networks.

- Key Players: Key players drive the Indian sports and fitness goods market by diversifying product portfolios, investing in manufacturing innovation, expanding distribution networks, and strengthening brand visibility through strategic partnerships and endorsements to capture growing demand across diverse consumer segments. Some of the key players operating in the market include Bhalla International, Cosco (India) Limited, Nivia Sports (Freewill Sports Pvt Ltd), Sanspareils Greenlands Pvt. Ltd., and Sareen Sports Industries Private Limited.

To get more information of this market Request Sample

Indian Sports and Fitness Goods Market Trends:

Rapid expansion of organized fitness facilities

India’s organized fitness sector is experiencing unprecedented growth as domestic and international gym franchises scale their operations across major cities and emerging urban centers. For instance, in February 2025, Crunch Fitness signed a master franchise agreement to open a minimum of 75 gym locations across India, marking its first physical presence in South Asia. The entry of premium and boutique fitness formats is driving demand for high-quality sports and fitness equipment. Rising disposable incomes, increasing awareness about preventive healthcare, and the growing influence of fitness culture are contributing to Indian sports and fitness goods market growth.

Integration of digital technologies in fitness equipment

The convergence of digital innovation and fitness is reshaping the Indian sports and fitness goods landscape. Smart fitness equipment featuring artificial intelligence-driven coaching, real-time performance tracking, and mobile app connectivity is gaining traction among tech-savvy consumers. The growing demand for personalized workout experiences and interactive feedback is encouraging manufacturers to embed advanced digital features in cardiovascular and strength training equipment. Wearable device integration and virtual coaching platforms are further enhancing consumer engagement, enabling users to monitor progress and optimize routines seamlessly. This technological transformation is driving premiumization and broadening the appeal of connected fitness solutions across demographics.

Growing adoption of home fitness solutions

Home fitness adoption is accelerating across urban India as consumers prioritize convenience, hygiene, and flexibility in their exercise routines. The shift toward remote work and fast-paced urban lifestyles is encouraging individuals to set up personal workout spaces at home. Manufacturers are responding by developing space-saving, foldable, and multi-functional equipment that caters to the growing segment of home consumers seeking professional-grade fitness experiences. The increasing availability of affordable yet feature-rich home workout products through e-commerce platforms is further democratizing access, enabling consumers across income segments to maintain consistent fitness regimens without relying on commercial gym facilities.

Market Outlook 2026-2034:

India’s sports and fitness goods market is positioned for sustained expansion, underpinned by favorable demographic trends, policy momentum, and evolving consumer preferences toward health and wellness. The market generated a revenue of USD 2,497.44 Million in 2025 and is projected to reach a revenue of USD 4,058.03 Million by 2034, growing at a compound annual growth rate of 5.4% from 2026-2034. Increasing government investments in sports infrastructure, the proliferation of fitness facilities beyond metropolitan regions, and the rising penetration of smart and connected fitness technologies are expected to drive robust demand. Growing youth participation in organized sports, expanding e-commerce channels, and deepening corporate wellness programs are further anticipated to broaden market accessibility and create new revenue streams across diverse product categories and consumer segments.

Indian Sports and Fitness Goods Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Fitness Goods |

38.5% |

|

Fitness Goods |

Cardiovascular Training Goods |

56.0% |

|

End Use |

Health Clubs/Gyms |

34.2% |

|

Region |

West and Central India |

31.5% |

Product Type Insights:

- Balls

- Fitness Goods

- Adventure Sports

- Golf Goods

- Other Goods

Fitness goods dominate with a share of 38.5% of the total Indian sports and fitness goods market in 2025.

Fitness goods represent the most prominent product category in the Indian sports and fitness goods market, driven by the expanding network of gyms, health clubs, and boutique studios across the country. Cardiovascular training equipment such as treadmills, stationary bikes, and elliptical trainers, along with strength training products like dumbbells and resistance bands, constitute the core of this segment. Rising health awareness, the growing prevalence of lifestyle diseases, and the aspiration for active living among India's increasingly urbanized population are sustaining robust demand for fitness goods across commercial and residential settings.

The segment is further bolstered by the growing home fitness trend, as urban consumers seek convenient and space-efficient workout solutions tailored to apartment-style living. Manufacturers are developing compact, foldable, and multi-functional equipment designed to meet the needs of space-constrained households. The integration of digital features such as Bluetooth connectivity, calorie tracking, and virtual coaching into fitness equipment is enhancing consumer engagement, broadening product appeal across age groups, and driving premiumization within the fitness goods category.

Fitness Goods Insights:

- Cardiovascular Training Goods

- Strength Training Goods

Cardiovascular training goods lead with a share of 56.0% of the total Indian sports and fitness goods market in 2025.

Cardiovascular training goods hold the largest share within the fitness goods category, driven by their critical role in promoting heart health, weight management, and overall physical endurance. Treadmills remain the most sought-after cardiovascular equipment owing to their versatility and suitability for indoor use regardless of weather conditions. Stationary bikes, elliptical trainers, and rowing machines complement the category by offering low-impact, joint-friendly alternatives that appeal to a wide demographic, including aging populations and rehabilitation-focused consumers across both commercial and home environments.

The segment is gaining further traction from technological innovation and the expansion of connected fitness ecosystems that offer personalized training experiences. The growing preference for smart cardiovascular equipment with interactive displays, heart rate monitoring, and app integration is driving premiumization within this segment and supporting sustained revenue growth. Manufacturers are increasingly embedding artificial intelligence-driven coaching, real-time performance analytics, and virtual workout programs into cardiovascular machines, transforming them from traditional exercise tools into comprehensive digital wellness platforms that enhance user motivation and retention.

Cardiovascular Training Goods Insights:

- Treadmills

- Stationary Bikes

- Rowing Machines

- Ellipticals

- Others

Treadmills are the most popular cardiovascular training equipment in India, offering versatile indoor walking, jogging, and running options. Their demand is sustained by urban consumers seeking weather-proof cardio solutions and fitness-conscious working professionals prioritizing convenient home exercise routines. The introduction of foldable and motorized variants with smart displays, incline adjustments, and heart rate monitoring features is further broadening their appeal among home users and commercial fitness facilities seeking durable, technology-enhanced cardio equipment.

Stationary bikes are gaining popularity due to their low-impact nature and suitability for users of all age groups. The rising demand for connected cycling experiences and compact home fitness solutions is driving adoption among urban consumers and fitness enthusiasts. Recumbent, upright, and air bike variants cater to diverse fitness goals, from rehabilitation and fat burning to endurance training, while Bluetooth-enabled models offering virtual cycling programs and calorie tracking are attracting a growing base of digitally engaged consumers.

Rowing machines are emerging as a favored full-body cardiovascular option in Indian fitness facilities, combining upper and lower body engagement. Their growing adoption reflects increasing consumer preference for comprehensive, calorie-efficient workout solutions. The equipment targets multiple muscle groups including the back, arms, core, and legs in a single session, making it attractive for time-conscious consumers. Fitness centers and boutique studios are increasingly incorporating rowing machines into their equipment portfolios to diversify workout offerings.

Elliptical trainers provide a low-impact, joint-friendly cardiovascular workout that appeals to users recovering from injuries and older fitness enthusiasts. Their versatility and ability to engage multiple muscle groups simultaneously support their growing demand. The smooth gliding motion minimizes stress on knees, hips, and ankles while delivering effective aerobic conditioning, making them a preferred choice in rehabilitation centers, corporate wellness facilities, and home gyms where users seek gentle yet comprehensive cardiovascular training options.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Health Clubs/Gyms

- Home Consumers

- Hotels and Corporate Offices

- Hospitals, Medical Centers and Public Institutions

- Others

Health clubs/gyms hold the largest share at 34.2% of the total Indian sports and fitness goods market in 2025.

Health clubs and gyms constitute the leading end-use segment in the Indian sports and fitness goods market, reflecting the rapid proliferation of organized fitness facilities across the country. The segment benefits from rising consumer preference for structured workout environments, group fitness classes, and access to professional-grade equipment. Franchise-driven gym chains are expanding aggressively into tier-2 and tier-3 cities, driving demand for a comprehensive range of cardiovascular, strength training, and functional fitness equipment that meets diverse consumer expectations and professional standards.

The entry of international fitness brands is further energizing the segment and elevating equipment procurement standards across the country. Global gym franchises are bringing world-class amenities, innovative class formats, and premium equipment configurations to the Indian market, raising consumer expectations and competitive benchmarks. Boutique fitness studios focusing on specialized formats such as high-intensity interval training, Pilates, and CrossFit are also contributing to heightened equipment demand across premium and specialized categories, creating diversified revenue opportunities for sports and fitness goods manufacturers and distributors.

Regional Insights:

- West and Central India

- North India

- South India

- East India

West and Central India accounts for the highest revenue share of 31.5% of the total Indian sports and fitness goods market in 2025.

Due to the concentration of important commercial and financial hubs in Mumbai, Pune, and Ahmedabad, which support a dense network of upscale fitness facilities, sporting goods merchants, and manufacturing facilities, West and Central India dominates the regional market landscape. Higher consumer purchasing capacity and a strong fitness culture that promotes investment in both home and commercial fitness equipment are advantageous to the area. The region's dominant position in the market is further reinforced by the existence of established sports goods distribution networks and robust retail infrastructure.

The region’s leadership is further strengthened by the entry and expansion of global sporting goods and fitness brands. For instance, in November 2025, Decathlon reopened its expanded flagship outlet in Whitefield, Bengaluru, unveiling a redesigned 60,000 square-foot format that stands as the brand’s largest store in India. The growing popularity of boutique fitness studios, corporate wellness initiatives, and e-commerce channels within this region is creating diversified demand for sports and fitness goods across product categories.

Market Dynamics:

Growth Drivers:

Why is the Indian Sports and Fitness Goods Market Growing?

Government-led sports infrastructure and fitness promotion initiatives

Through historic legislative actions and major budgetary expenditures, the Indian government has greatly increased its commitment to sports development and fitness promotion. With the introduction of Khelo Bharat Niti, the old national sports policy framework has been replaced, marking the most extensive reorganization of India's sports scene in more than 20 years. Funding for the Ministry of Youth Affairs and Sports has been steadily boosted by the government, with funds specifically allocated to the Khelo India Programme to assist competitive sports platforms, athlete development, and grassroots talent identification. In order to improve grassroots athlete routes, the program has made it easier for many new sports infrastructure projects to be approved and for Khelo India Centers to be established at the district level around the nation. These significant investments are establishing a solid basis for sports participation and generating a steady demand for fitness products and sports equipment nationwide. In addition to strengthening the culture of physical exercise and promoting wider consumer involvement with sports and wellness products, the Fit India Movement continues to advance mass fitness as a national public movement.

Rising health awareness and increasing prevalence of lifestyle diseases

Indian consumers are prioritizing regular physical activity and fitness due to the rising burden of lifestyle-related health issues like obesity, diabetes, cardiovascular disease, and hypertension. Spending on sports and fitness products has increased due to increased health consciousness, especially after the worldwide pandemic. India's fitness facility membership base has been continuously growing, and industry forecasts show substantial development potential because penetration rates are still significantly lower than those of other countries. The demand for commercial and personal fitness equipment is growing as people of all ages become more aware of the health advantages of exercise. Consumer incentive to purchase sports and fitness products is further strengthened by the increasing impact of fitness-focused social media content and celebrity endorsements. Corporate wellness initiatives are also becoming more popular, as more businesses incorporate fitness benefits into employee wellness plans. This opens up new markets for high-quality sports and fitness products.

Expansion of organized fitness ecosystems and global brand investments

New demand channels for sports and fitness equipment are being created by the quick growth of foreign sporting goods merchants, boutique studios, and organized fitness chains throughout India. International companies are investing large sums of money in the Indian market, demonstrating their strong belief in the country's potential for long-term growth. To take advantage of India's expanding customer base, top multinational sporting goods retailers are expanding their retail locations, investing in local production capabilities, and improving digital commerce platforms. Concurrently, the country's equipment procurement is rising due to the franchise-driven growth of multinational gym chains, as new facilities need to be fully equipped with functional fitness, strength training, and cardiovascular equipment. This confluence of manufacturing investments, retail expansion, and fitness facility growth is expanding consumer access to high-quality sports and fitness items and fostering a favorable ecology for long-term market development. Brands are now able to reach customers outside of typical metropolitan regions because to the growing use of e-commerce platforms and quick-commerce delivery strategies.

Market Restraints:

What Challenges the Indian Sports and Fitness Goods Market is Facing?

High cost of premium fitness equipment

One major obstacle to wider market acceptance in India is the high cost of sophisticated, high-end exercise equipment. Although there is a growing desire for technologically advanced items, a significant portion of price-conscious consumers, especially in tier-2 and tier-3 cities, cannot afford them due to high initial expenditures and continuing maintenance costs. Penetration beyond wealthy metropolitan groups is further hampered by the lack of structured financing choices and low knowledge of affordable alternatives.

Low fitness penetration and awareness in smaller markets

Fitness facility membership penetration in India is still very low when compared to worldwide standards, despite notable increase in metropolitan areas. This suggests both enormous unrealized potential and ongoing accessibility issues. In semi-urban and rural locations, a significant section of the population does not have sufficient access to organized fitness centers, sports facilities, and high-quality equipment. The market's potential for growth is nevertheless limited by low awareness of the advantages of regular exercise and poor sports facilities outside of large cities.

Competition from unorganized and low-cost alternatives

A sizable unorganized sector made up of regional producers selling inexpensive, unbranded items puts pressure on the Indian sports and fitness goods market. These substitutes draw in budget-conscious customers, but they frequently sacrifice requirements for durability, quality, and safety. For organized organizations looking to set consistent quality standards and foster brand loyalty across a variety of consumer categories, the fragmented nature of the domestic manufacturing industry presents difficulties.

Competitive Landscape:

The market for sports and fitness products in India is competitive, with both well-known local producers and foreign companies growing their market share. In order to meet the increasing demand in urban and emerging markets, market players are concentrating on product innovation, technology integration, and distribution network growth. Key competitive strategies influencing the industry include investments in local manufacturing capabilities, franchise agreements, and strategic collaborations. Brands are able to access larger consumer bases and improve customer engagement through digital marketing tactics and individualized products because to the growing influence of e-commerce platforms and direct-to-consumer channels.

Some of the key players include:

- Bhalla International

- Cosco (India) Limited

- Nivia Sports (Freewill Sports Pvt Ltd)

- Sanspareils Greenlands Pvt. Ltd.

- Sareen Sports Industries Private Limited

Indian Sports and Fitness Goods Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Balls, Fitness Goods, Adventure Sports, Golf Goods, Other Goods |

| Fitness Goods Covered | Cardiovascular Training Goods, Strength Training Goods |

| Cardiovascular Training Goods Covered | Treadmills, Stationary Bikes, Rowing Machines, Ellipticals, Others |

| End-Uses Covered | Health Clubs/Gyms, Home Consumers, Hotels and Corporate Offices, Hospitals, Medical Centers and Public Institutions, Others |

| Region Covered | West and Central India, North India, South India, East India |

| Companies Covered | Bhalla International, Cosco (India) Limited, Nivia Sports (Freewill Sports Pvt Ltd), Sanspareils Greenlands Pvt. Ltd., Sareen Sports Industries Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Sports and Fitness Goods Market Report

The Indian sports and fitness goods market size was valued at USD 2,497.44 Million in 2025.

The Indian sports and fitness goods market is expected to grow at a compound annual growth rate of 5.4% from 2026-2034 to reach USD 4,058.03 Million by 2034.

Fitness goods dominated the market with a share of 38.5%, driven by the expanding network of gyms and health clubs, rising health awareness, growing adoption of home fitness solutions, and increasing consumer preference for cardiovascular and strength training equipment.

Key factors driving the Indian sports and fitness goods market include government sports infrastructure investments, rising health consciousness, expanding organized fitness ecosystems, growing home fitness adoption, increasing disposable incomes, and technological advancements in smart fitness equipment.

Major challenges include high costs of premium fitness equipment, low fitness penetration in smaller cities and rural areas, competition from unorganized low-cost manufacturers, limited consumer awareness about quality standards, and inadequate sports infrastructure outside metropolitan regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)