Indian Vaccine Market Size, Share, Trends and Forecast by Monovalent and Combined Vaccines, 2026-2034

Indian Vaccine Market Size, Share, Trends & Forecast (2026-2034)

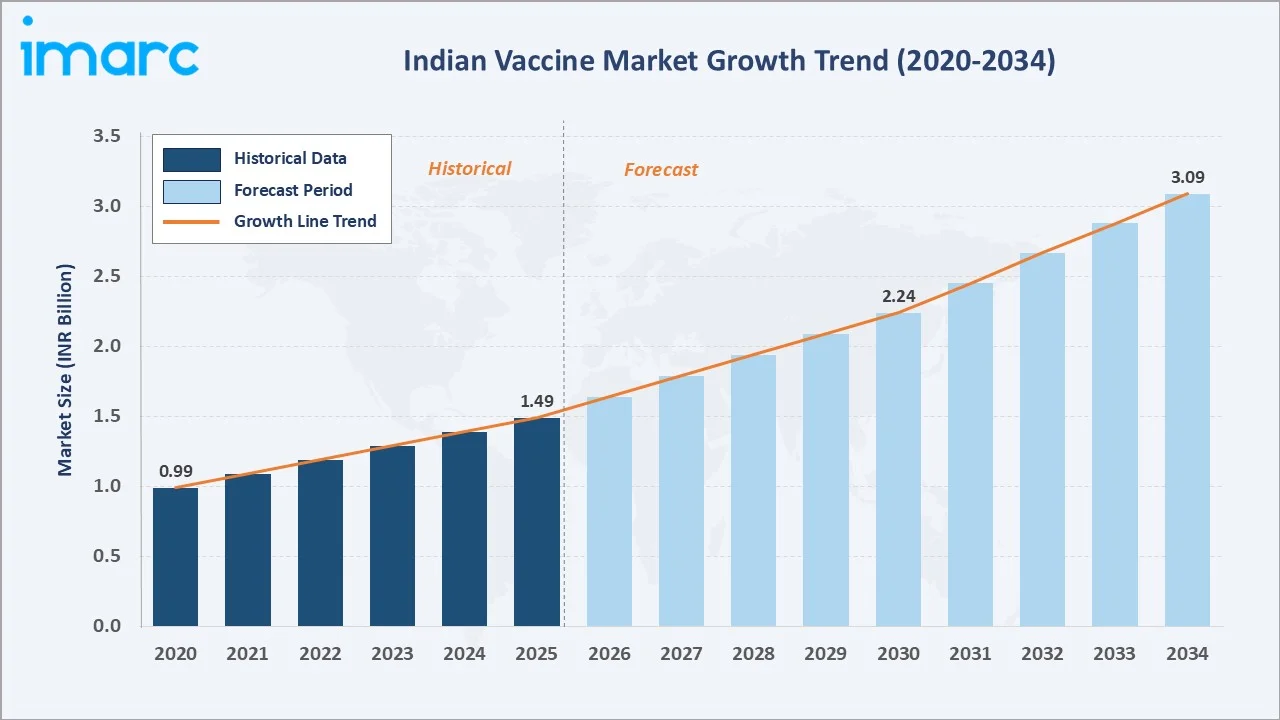

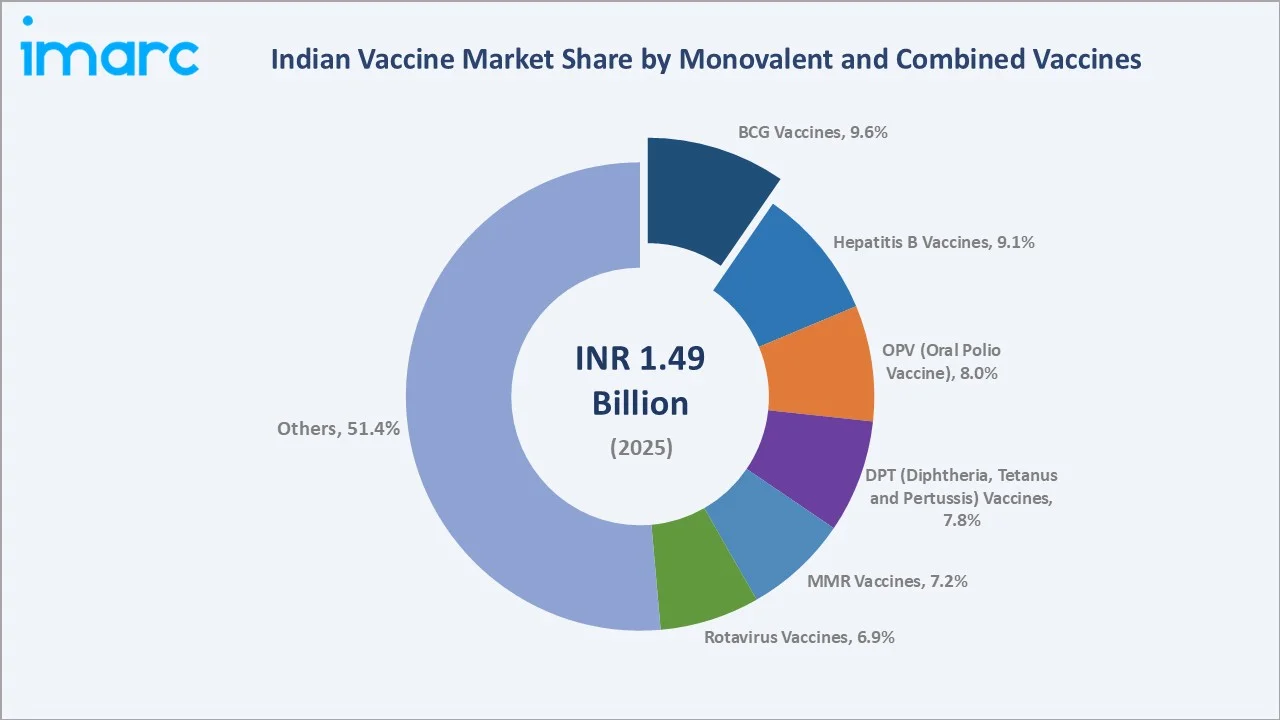

The Indian vaccine market was valued at INR 1.49 Billion in 2025 and is projected to reach INR 3.09 Billion by 2034, exhibiting a CAGR of 8.45% during 2026-2034. Government-led expansion of immunization coverage, rising awareness of preventable diseases, surging pediatric and adult vaccination uptake, and active private sector participation are the primary factors shaping market growth.

BCG vaccines lead the monovalent and combined vaccines segment at 9.6% in 2025, driven by widespread newborn immunization programs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 1.49 Billion |

|

Forecast Market Size (2034) |

INR 3.09 Billion |

|

CAGR (2026-2034) |

8.45% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Monovalent and Combined Vaccines |

BCG Vaccines (9.6%, 2025) |

|

Second Largest Monovalent and Combined Vaccines |

Hepatitis B Vaccines (9.1%, 2025) |

The Indian vaccine market expanded from INR 0.99 Billion in 2020 to INR 1.49 Billion in 2025, reflecting steady progress driven by widening immunization coverage, increasing government health expenditure, and rising acceptance of newer vaccines in both the public and private sectors. The market is anchored at INR 2.24 Billion in 2030, with the forecast to INR 3.09 Billion by 2034 supported by introduction of novel vaccines, adult immunization programs, and continuous cold chain infrastructure development.

To get more information on this market, Request Sample

CAGR trajectories across the monovalent and combined vaccines segment show newer sub-types, such as HPV vaccines, rotavirus vaccines, and pneumococcal vaccines expanding faster than the overall 8.45% market CAGR, driven by rising disease awareness, government inclusion in national programs, and growing private sector adoption.

Executive Summary

The Indian vaccine market is on a robust growth trajectory, expanding from INR 0.99 Billion in 2020 to INR 3.09 Billion by 2034. The market has evolved from a largely public-sector-driven immunization framework to a diversified ecosystem that encompasses government programs, private healthcare providers, and multinational vaccine manufacturers. Strong institutional support, coupled with expanding cold chain infrastructure, has significantly improved vaccine reach across urban and rural geographies.

BCG vaccines dominate the monovalent and combined vaccines segment at 9.6% in 2025, driven by their inclusion in national immunization programs. Their critical role in preventing severe forms of tuberculosis among infants and young children supports sustained demand across both developed and emerging healthcare systems. In March 2025, Karnataka Health Minister Dinesh Gundu Rao initiated an adult BCG vaccination program to enhance tuberculosis prevention efforts in the state.

Key Market Insights

|

Insight |

Data |

|

Leading Monovalent and Combined Vaccines |

BCG Vaccines - 9.6% share (2025) |

|

Second Largest Monovalent and Combined Vaccines |

Hepatitis B Vaccines - 9.1% share (2025) |

|

Top Companies |

Cyrus Poonawalla Group, Bharat Biotech, Biological E Limited, Panacea Biotec, Sanofi |

Key Analytical Observations Expanding on the Data Above:

- BCG vaccines at 9.6% remain the single largest sub-type within the monovalent and combined vaccines segment in 2025, reflecting India's continued reliance on BCG as a cornerstone of national tuberculosis prevention. The ‘Adult BCG Vaccination Study’ was initiated by MoHFW and the Indian Council of Medical Research in January 2024 to vaccinate at-risk adults with the BCG vaccine, track the resulting changes in reported TB cases, and assess the vaccine's effectiveness. The research was being conducted using an innovative digital health platform, TB-WIN, created by MoHFW with technical assistance from UNDP.

- Hepatitis B vaccines at 9.1% maintain strong second-position share driven by the birth-dose administration mandate and the national program's multi-dose schedule, ensuring consistent demand across both government and private healthcare channels.

Indian Vaccine Market Overview

Vaccines are biological preparations that provide active acquired immunity against specific infectious diseases by stimulating the immune system to recognize and combat pathogens. The Indian vaccine market encompasses a broad spectrum of products classified under a single segment — monovalent and combined vaccines — spanning products targeting single disease agents as well as multi-antigen formulations offering combined protection in one dose.

The Indian vaccine ecosystem integrates domestic manufacturers, multinational pharmaceutical companies, government procurement agencies, regulatory authorities, cold chain infrastructure providers, healthcare delivery networks, and international development partners. Together, these stakeholders enable the production, procurement, distribution, and administration of vaccines across India's vast and diverse geography.

Market Dynamics

To evaluate market opportunities, Request Sample

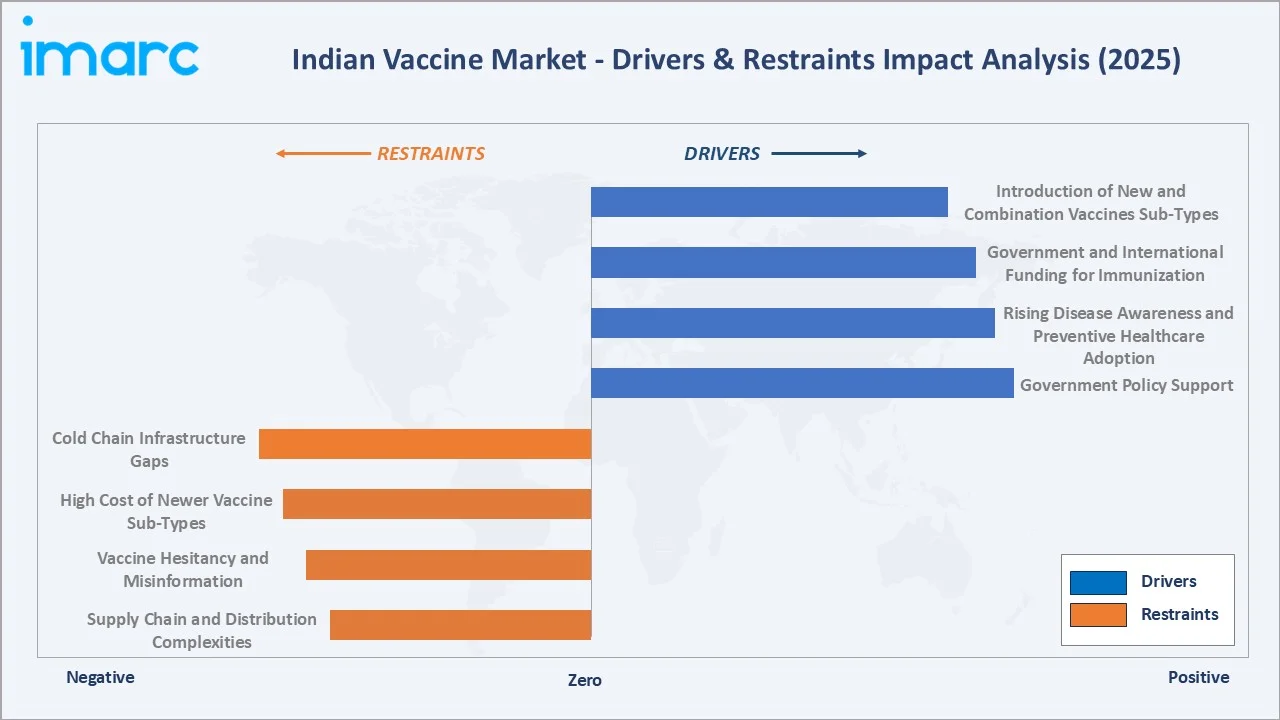

Market Drivers

- Government Policy Support: India's national immunization initiatives provide free vaccination coverage to infants, young children, and pregnant women, creating a large and dependable institutional demand base. Continuous expansion of immunization schedules and broader healthcare outreach programs further stimulate growth within the monovalent and combined vaccines segment.

- Rising Disease Awareness and Preventive Healthcare Adoption: Growing health literacy among urban and semi-urban populations is driving voluntary vaccination for diseases, such as typhoid, influenza, cervical cancer, and hepatitis A. In 2026, the Government of India initiated a nationwide HPV vaccination drive for girls aged 14 to safeguard against cervical cancer, along with an indigenous tetanus-diphtheria (Td) vaccine.

- Government and International Funding for Immunization: Significant financial support from international agencies continues to fund vaccine procurement and delivery infrastructure, ensuring sustained coverage across lower-income states and reducing out-of-pocket vaccination costs for families.

- Introduction of New and Combination Vaccine Sub-Types: Ongoing expansion of national immunization schedules to include newer vaccine categories continues to create additional demand within the segment. Combination vaccines that reduce the number of injections and simplify immunization schedules are increasingly preferred by both public healthcare programs and private providers, supporting broader adoption and coverage.

Market Restraints

- Cold Chain Infrastructure Gaps: India's extensive cold chain network, while significantly improved, continues to face challenges in last-mile connectivity in hilly, remote, and tribal areas. Temperature excursion incidents can compromise vaccine efficacy and result in wastage, adding to cost burdens for both government and private operators.

- High Cost of Newer Vaccine Sub-Types: Newer sub-types within the monovalent and combined vaccines segment, such as HPV, dengue, and pneumococcal vaccines, carry significantly higher price points compared to traditional formulations. This can limit adoption in price-sensitive markets and healthcare settings.

- Vaccine Hesitancy and Misinformation: Misinformation about vaccine safety, particularly in rural and semi-urban areas, continues to impede full immunization coverage. Cultural and religious resistance in certain communities remains a persistent challenge for frontline health workers.

- Supply Chain and Distribution Complexities: Vaccine distribution across India's complex federal health system involves multiple layers of coordination, resulting in logistical inefficiencies, stockouts in some regions, and overstocking in others.

Market Opportunities

- Adult Immunization Programs: The nascent adult immunization market in India presents a significant untapped opportunity, particularly for influenza, pneumococcal, hepatitis A and B, and HPV sub-types. Growing physician recommendation rates and corporate wellness programs are gradually shifting adult vaccine acceptance.

- Private Sector and Travel Vaccination Expansion: Rising outbound international travel, increasing corporate health programs, and proliferation of private vaccination centers are expanding the addressable market for premium and specialty sub-types, including rabies, meningococcal, and Japanese encephalitis vaccines.

Market Challenges

- Intense Price Competition and Tender-Driven Procurement: Government vaccine procurement through tenders at lowest-bid pricing creates margin pressure for manufacturers, particularly for established sub-types. This dynamic can discourage investment in domestic production capacity for lower-margin products.

- Regulatory Timelines and Approvals: Lengthy regulatory approval pathways for new vaccine sub-types in India, while necessary for safety assurance, can delay introduction of newer products and create competitive disadvantage relative to markets with faster approval mechanisms.

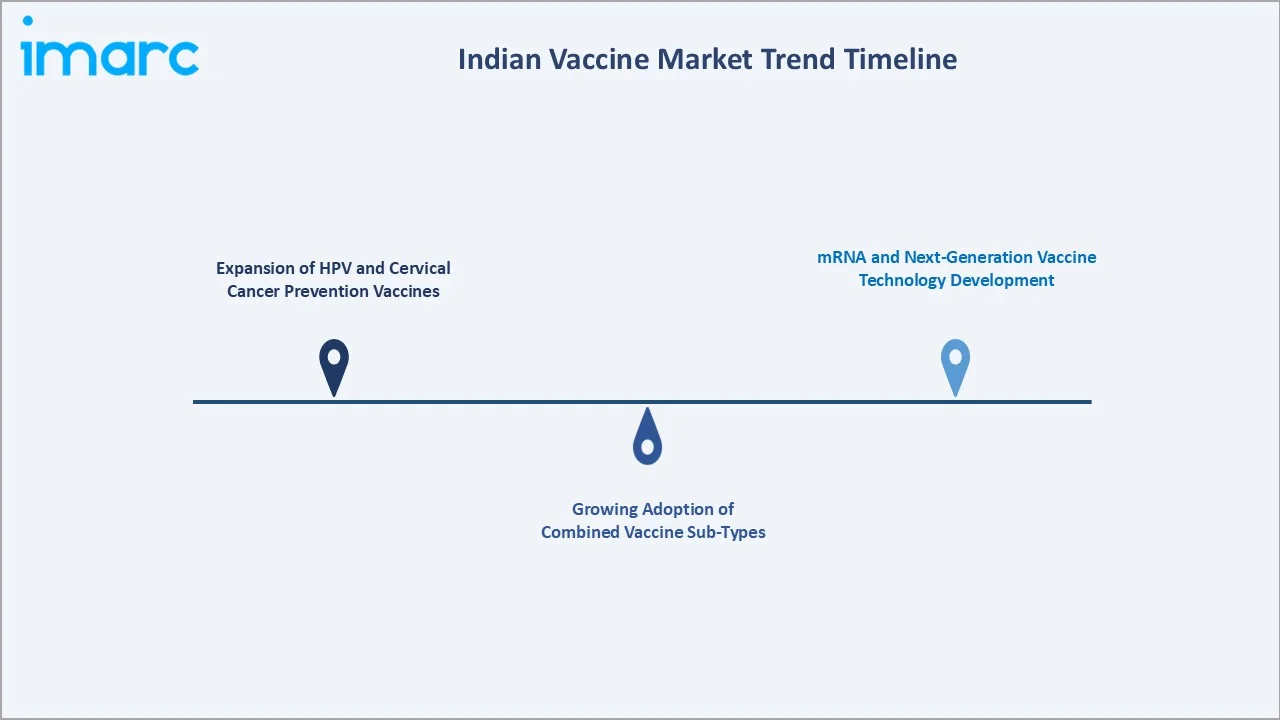

Emerging Market Trends

1. Expansion of HPV and Cervical Cancer Prevention Vaccines

HPV vaccines are witnessing growing adoption in India due to increasing awareness of cervical cancer prevention and expanding immunization initiatives. Improved accessibility, supportive healthcare policies, and greater focus on preventive healthcare are expected to drive sustained growth of this vaccine sub-type through 2034.

2. Growing Adoption of Combined Vaccine Sub-Types

Hexavalent and pentavalent combined sub-types, which protect against diphtheria, tetanus, pertussis, hepatitis B, haemophilus influenzae type b, and polio in a single injection, are increasingly preferred by state immunization programs to reduce caregiver burden and improve schedule compliance.

3. mRNA and Next-Generation Vaccine Technology Development

India's domestic biotechnology industry is actively developing next-generation vaccine platforms, including mRNA technology. In 2023, India's inaugural mRNA vaccine was created utilizing indigenous platform technology by Gennova, backed financially by the Department of Biotechnology (DBT) and the Biotechnology Industry Research Assistance Council (BIRAC). Several domestic players are investing in mRNA vaccine infrastructure for future pandemic preparedness and endemic disease management.

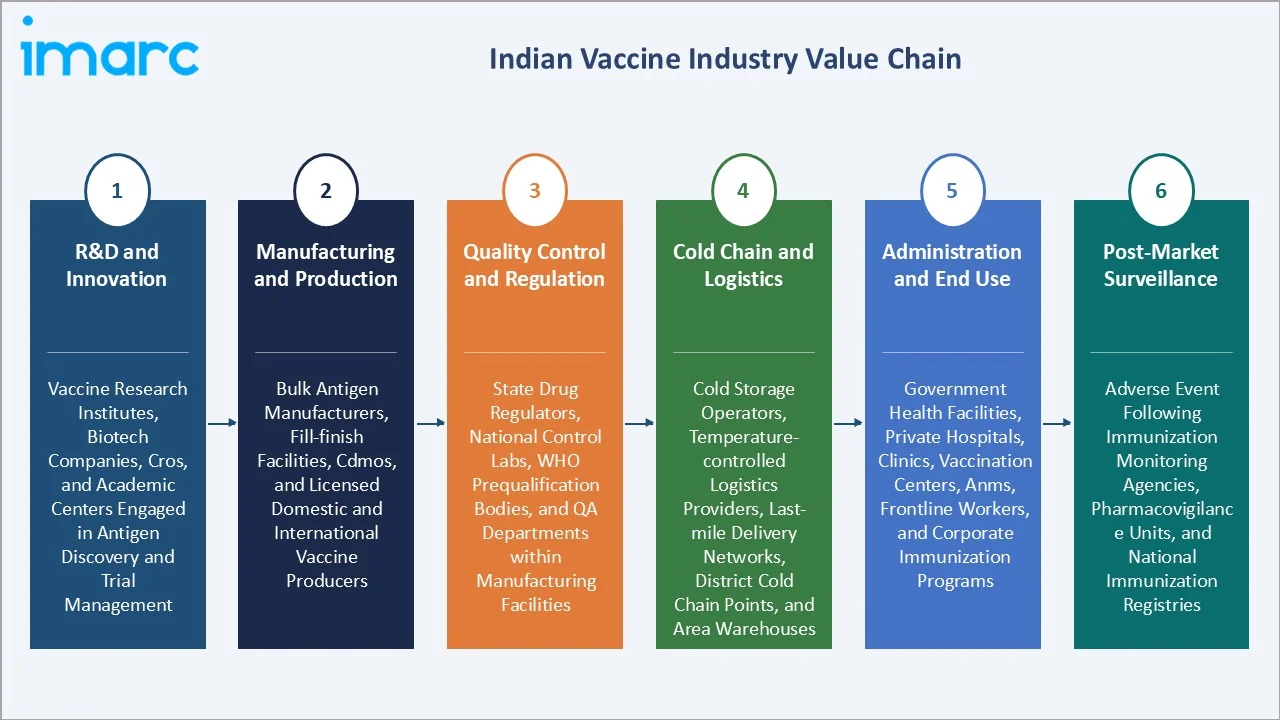

Industry Value Chain Analysis

The Indian vaccine value chain spans six stages from research and development through post-market surveillance and lifecycle management. Manufacturing and cold chain logistics capture the highest value-add in the domestic context, while regulatory compliance and pharmacovigilance capabilities increasingly determine sustainable competitive position for both domestic and international players.

|

Stage |

Key Players / Examples |

|

R&D & Innovation |

Vaccine research institutes, biotech companies, clinical research organizations, and academic collaboration centers engaged in antigen discovery and trial management |

|

Manufacturing & Production |

Bulk antigen manufacturers, fill-finish facilities, contract development and manufacturing organizations, and licensed domestic and international vaccine producers |

|

Quality Control & Regulation |

State drug regulators, national control laboratories, WHO prequalification bodies, and quality assurance departments within manufacturing facilities |

|

Cold Chain & Logistics |

Cold storage operators, temperature-controlled logistics providers, last-mile vaccine delivery networks, district cold chain points, and area warehouses |

|

Administration & End Use |

Government health facilities, private hospitals, clinics, vaccination centers, ANMs and frontline health workers, and school and corporate immunization programs |

|

Post-Market Surveillance |

Adverse event following immunization monitoring agencies, pharmacovigilance units, national immunization registries, and real-world vaccine effectiveness tracking bodies |

Vertically integrated domestic players with proprietary manufacturing capabilities, established regulatory relationships, and government supply agreements are positioned to capture greater value than those dependent on technology licensing or third-party contract manufacturing.

Technology Landscape in the Indian Vaccine Industry

Live Attenuated and Inactivated Vaccine Platforms

Conventional live attenuated platforms continue to dominate the Indian market due to their proven safety profiles, established manufacturing processes, and cost-effectiveness at scale. Inactivated vaccines, including inactivated poliovirus vaccine and whole-cell pertussis formulations, provide alternatives for immune-compromised populations.

Recombinant and Subunit Vaccine Technologies

Recombinant antigen-based vaccines, particularly for hepatitis B, HPV, and typhoid, have gained significant traction in both public and private markets. India is a global leader in recombinant hepatitis B vaccine production, with domestic manufacturers supplying affordable formulations to developing countries worldwide.

mRNA and Viral Vector Platforms

mRNA and viral vector technologies are gaining attention within the Indian vaccine industry, as manufacturers expand capabilities for next-generation vaccine development. Investments in research infrastructure, technology partnerships, and pandemic preparedness initiatives are supporting the gradual adoption of these advanced platforms for both emerging infectious diseases and future immunization programs.

Market Segmentation Analysis

The report covers the following segment:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Monovalent and Combined Vaccines |

BCG Vaccines |

9.6% |

2025 |

By Monovalent and Combined Vaccines

BCG vaccines command the largest sub-type share at 9.6%, underpinned by universal birth-dose policy and consistent institutional demand under the national immunization schedule. Their established role in tuberculosis prevention ensures stable procurement and sustained uptake across public healthcare facilities.

To access detailed market analysis, Request Sample

Hepatitis B vaccines at 9.1% rank second, supported by the multi-dose birth schedule and strong private sector use. Continued emphasis on early-life immunization and prevention of chronic liver disease further sustains demand for this vaccine category.

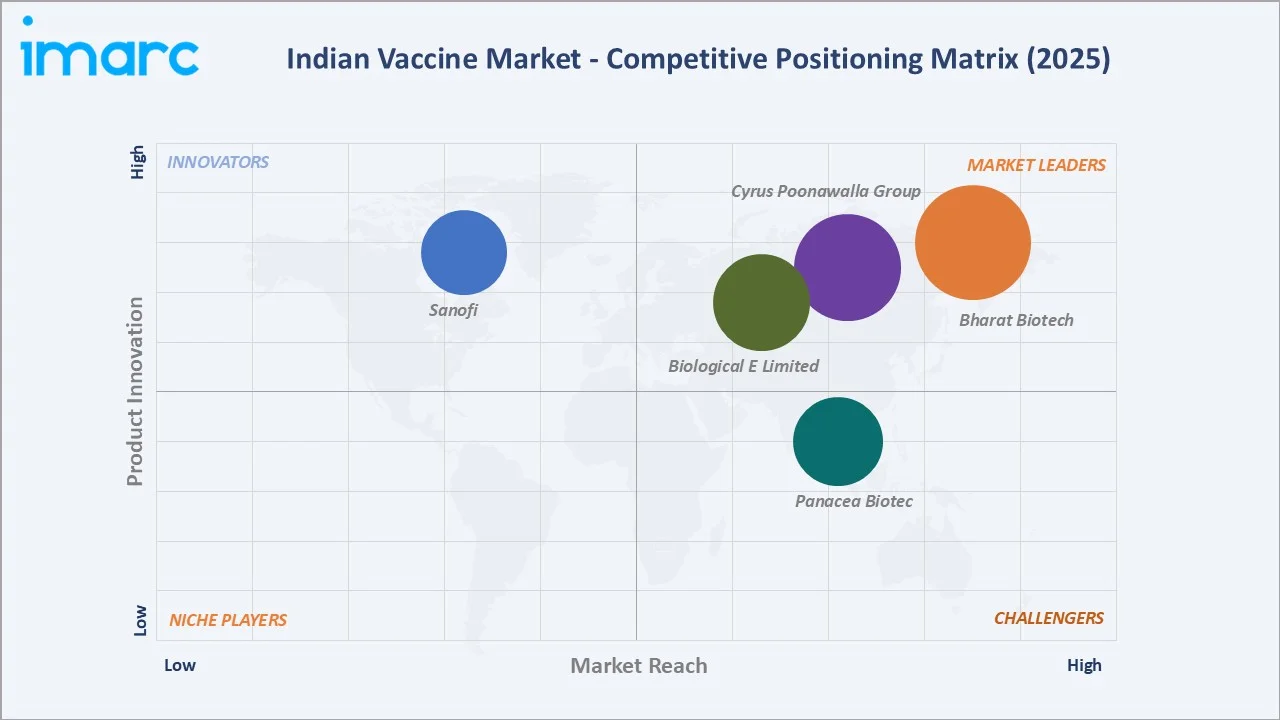

Competitive Landscape

The Indian vaccine market is moderately concentrated at the manufacturing level, with a small number of large domestic producers commanding substantial share of government procurement. Brand strength, regulatory track record, manufacturing scale, and established government supply relationships form the key competitive moats. The private market is more fragmented, with multinational brands competing alongside domestic manufacturers across the monovalent and combined vaccines segment.

|

Company Name |

Key Brand / Product |

Position |

Strategic Focus |

|

Cyrus Poonawalla Group |

CERVAVAC |

Leader |

Large-scale manufacturing, global supply and domestic immunization programs |

|

Bharat Biotech |

ROTAVAC 5D, Typbar TCV |

Leader |

Indigenous innovation, domestic and emerging market penetration |

|

Biological E Limited |

PNEUBEVAX 14, nOPV2 |

Leader |

Combination vaccines, government supply, and international expansion |

|

Panacea Biotec |

EasySix |

Challenger |

Pediatric combination vaccines and cost-effective government and UN agency supply |

|

Sanofi |

HEXAXIM |

Innovator |

Multinational portfolio of combination and influenza vaccines in the private market |

Key players include Cyrus Poonawalla Group, Bharat Biotech, Biological E Limited, Panacea Biotec, and Sanofi, among others.

Key Company Profiles

Cyrus Poonawalla Group

Cyrus Poonawalla Group is a diversified Indian conglomerate headquartered in Pune, Maharashtra. Its flagship subsidiary, Serum Institute of India, is the world's leading vaccine manufacturer by volume and a cornerstone supplier to global immunization programs. The group has built its leadership position over decades through a focus on affordable, high-quality biological products.

- Product Portfolio: The group offers a broad portfolio of vaccines covering a wide range of infectious and vaccine-preventable diseases for pediatric and adult populations.

- Recent Development: Serum Institute of India became the first company to submit a WHO prequalification dossier for CERVAVAC in June 2025.

- Strategic Focus: Large-scale manufacturing, global supply partnerships, and domestic immunization programs.

Bharat Biotech

Bharat Biotech is a leading Indian biotechnology company headquartered in Hyderabad, Telangana, with a strong track record in developing and manufacturing innovative vaccines. The company operates multiple WHO-prequalified manufacturing facilities and is known for bringing several world-first vaccine products to market.

- Product Portfolio: The company offers a diversified portfolio of vaccines addressing multiple vaccine-preventable diseases across pediatric and adult immunization segments.

- Recent Development: Bharat Biotech continues to expand its portfolio and manufacturing capabilities, with active supply agreements with global health agencies for its core vaccine products.

- Strategic Focus: Indigenous vaccine innovation, domestic and emerging market penetration.

Biological E Limited

Biological E Limited is one of India's oldest biopharmaceutical companies, headquartered in Hyderabad, Telangana. The firm holds multiple WHO-prequalified vaccine products, supplying to UN agencies, national immunization programs, and global markets.

- Product Portfolio: The company offers a range of vaccines covering several vaccine-preventable diseases, with products supplied to domestic and international immunization programs.

- Recent Development: Biological E Limited continues to expand its combination vaccine manufacturing capacity and is pursuing WHO prequalification for additional products for supply to UNICEF and Gavi-supported programs.

- Strategic Focus: Combination vaccines, government supply, and international expansion.

Market Concentration Analysis

The Indian vaccine market is moderately concentrated at the manufacturing level. The top three domestic manufacturers — Cyrus Poonawalla Group, Bharat Biotech, and Biological E Limited — account for the majority of government procurement volumes. Their combined manufacturing capacity and established government relationships create significant structural advantages.

Barriers to entry are high, particularly for government supply, including WHO prequalification requirements, large capital investment for manufacturing infrastructure, stringent quality compliance, long regulatory approval timelines, and the need for established institutional relationships. These factors favor well-capitalized incumbents with proven track records.

Consolidation is accelerating through strategic partnerships between domestic manufacturers and international biotechnology firms, particularly for technology transfer in mRNA and next-generation platforms. The private vaccination market is more fragmented, with multinational brands competing on product differentiation, acellular pertussis formulations, and physician relationships.

Investment & Growth Opportunities

Fastest-Growing Sub-Types

HPV vaccines represent the fastest-growing sub-type within the monovalent and combined vaccines segment, driven by government inclusion in the national program and large-scale awareness campaigns targeting adolescent girls. Pneumococcal vaccines and rotavirus vaccines are also expanding rapidly as state programs extend coverage.

Emerging Markets

Adult immunization represents the largest untapped growth opportunity in the Indian vaccine market. Pneumococcal vaccines and hepatitis vaccines for adult populations are significantly underpenetrated relative to global benchmarks. Corporate wellness programs, travel vaccination clinics, and physician-led awareness are creating emerging demand channels across urban markets.

Venture & Investment Trends

Investment is focused on mRNA vaccine manufacturing infrastructure, vaccine cold chain modernization through IoT and digital tracking, and next-generation combination vaccine formulation development. Government initiatives are channeling institutional capital toward domestic vaccine research and manufacturing self-sufficiency.

Future Market Outlook (2026-2034)

The Indian vaccine market is forecast to expand from INR 1.49 Billion in 2025 to INR 3.09 Billion by 2034 at a CAGR of 8.45%, adding approximately INR 1.60 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: continued expansion of the national immunization schedule to include newer sub-types within the monovalent and combined vaccines segment; the rise of adult and adolescent immunization programs; deepening penetration of the private vaccination market driven by rising incomes and health awareness; and ongoing investment in domestic manufacturing technology for next-generation vaccine platforms.

By 2034, the Indian vaccine market is expected to reflect a more balanced public-private participation model, with newer sub-types, including HPV and mRNA-based products, collectively accounting for a significantly higher share of overall market value. Regulatory modernization, digital immunization infrastructure, and cold chain advancement are expected to further enable broader geographic reach and improved vaccination outcomes.

Research Methodology

Primary Research

Primary research included structured interviews with vaccine manufacturers, national immunization program officials, pediatricians and private practitioners, cold chain logistics providers, and regulatory specialists. These inputs validated market sizing, segment dynamics, and competitive positioning across the monovalent and combined vaccines segment.

Secondary Research

Secondary sources included Ministry of Health and Family Welfare publications, National Health Mission data, CDSCO regulatory approvals, WHO and UNICEF immunization program reports, Gavi supply data, annual reports and investor presentations from listed vaccine companies, and trade association publications from the Organization of Pharmaceutical Producers of India.

Forecasting Models

Market forecasts used top-down and bottom-up models combining national immunization schedule dose counts, government procurement data, private sector sales estimates, price trends, and new vaccine introduction scenarios. Scenario analysis addressed policy pace, price evolution, and international supply dynamics.

Indian Vaccine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million, INR Billion |

|

Scope of the Report

|

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Monovalent and Combined Vaccines Covered | BCG, HIB, Influenza, Varicella, Typhoid, Japanese Encephalitis, Measles, Tetanus Toxoid, Hepatitis A, Rubella, Diphtheria, Tetanus, and Pertussis (DPT), Oral Polio Vaccine (OPV), MMR, Rotavirus, Hepatitis B, Pneumococcal, Meningococcal, Rabies, HPV, Hexavalent, Dengue vaccines |

| Companies Covered | Cyrus Poonawalla Group, Bharat Biotech, Biological E Limited, Panacea Biotec, Sanofi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Vaccine Market Report

The Indian vaccine market was valued at INR 1.49 Billion in 2025, driven by government immunization programs, rising disease awareness, and growing private sector vaccination uptake across urban and semi-urban geographies.

The market is projected to grow at 8.45% CAGR from 2026 to 2034, reaching INR 3.09 Billion, supported by new vaccine sub-type introductions, adult immunization expansion, and increasing private sector penetration.

BCG vaccines lead with 9.6% share in 2025, fueled by sustained government procurement programs. Their critical role in tuberculosis prevention ensures consistent demand across public healthcare facilities nationwide.

Key drivers include rising preventive healthcare awareness, government and international funding, introduction of new sub-types, and India's large pediatric population base.

Leading players include Cyrus Poonawalla Group, Bharat Biotech, Biological E Limited, Panacea Biotec, and Sanofi.

Key challenges include cold chain infrastructure gaps in remote areas, high cost of newer sub-types limiting private adoption, vaccine hesitancy in certain communities, and regulatory complexity in introducing new formulations.

HPV vaccine demand is rising steadily in India, driven by increasing awareness of cervical cancer prevention, expanding immunization initiatives, and improving vaccine accessibility. Greater emphasis on adolescent vaccination and preventive healthcare is expected to support strong growth in demand over the coming years.

Key investment opportunities include adult immunization program expansion, mRNA and next-generation vaccine manufacturing infrastructure, cold chain modernization, and digital immunization record infrastructure. Government policy support and international funding make these segments attractive for long-term investment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)