Indoor Farming Market Size, Share, Trends and Forecast by Facility Type, Crop Type, Component, Growing System, and Region, 2026-2034

Indoor Farming Market Size, Share, Trends & Forecast (2026-2034)

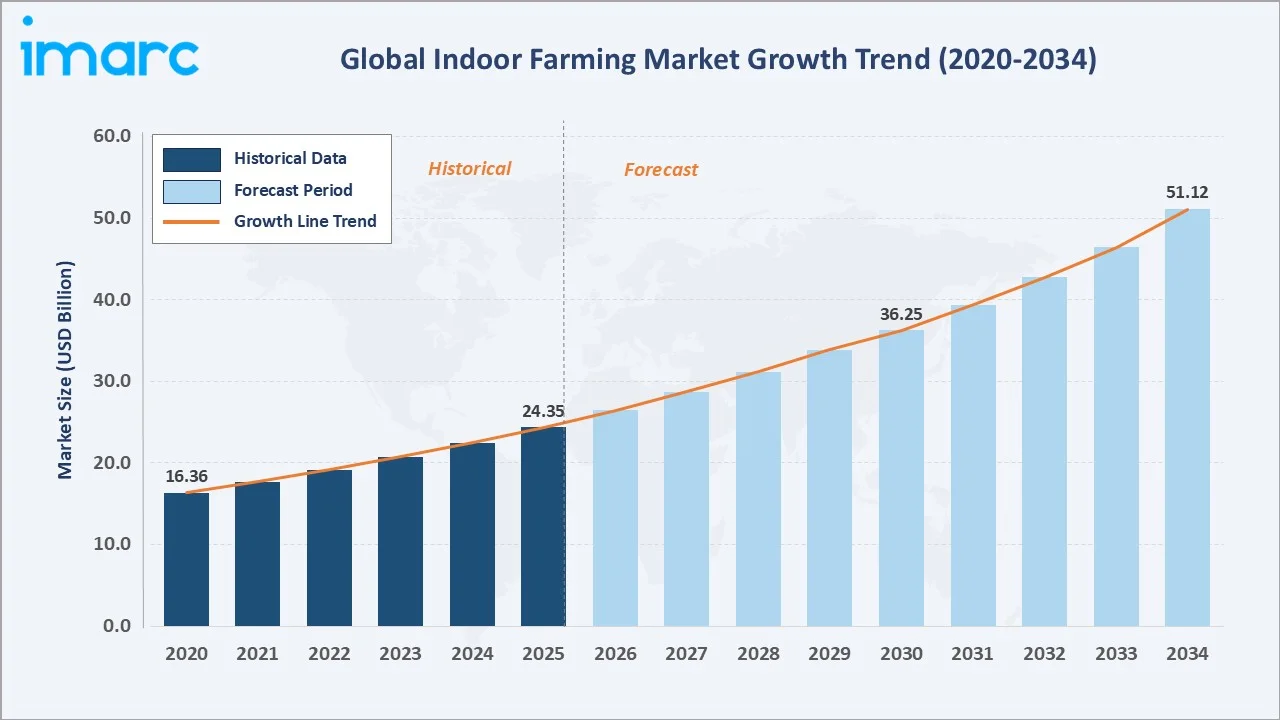

The global indoor farming market reached USD 24.35 Billion in 2025 and is projected to reach USD 51.12 Billion by 2034, growing at a CAGR of 8.28% during 2026-2034. Rising demand for pesticide-free locally grown produce, rapid advancements in controlled-environment agriculture (CEA) technologies, including AI, IoT, and LED lighting, and strong government mandates for sustainable food production are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.35 Billion |

|

Forecast Market Size (2034) |

USD 51.12 Billion |

|

CAGR (2026-2034) |

8.28% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.9% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

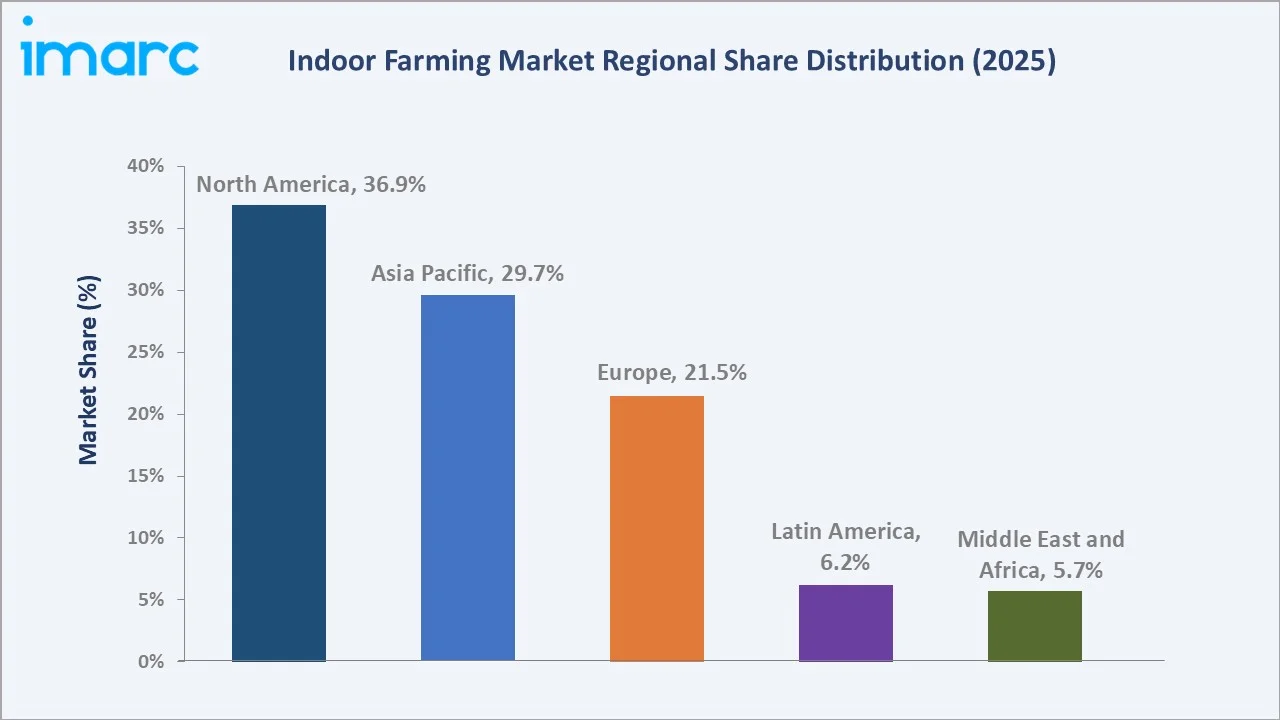

North America dominates, holding a 36.9% market share in 2025, while the greenhouse segment leads facility-type demand at 47.0%. Hardware components remain dominant with an 89.2% share. Indoor farming leverages controlled environments to enable year-round hydroponics with up to 95% less water use than conventional field agriculture, making it critical for food security in water-scarce and land-constrained regions.

To get more information on this market, Request Sample

With applications spanning greenhouse cultivation, vertical indoor farms, container farms, and deep water culture systems, the market is expected to continue expanding, supported by innovations in precision agriculture technologies and the increasing urgency of food security investment globally.

Executive Summary

The global indoor farming market is on a sustained growth path, underpinned by accelerating food security concerns, declining arable land, and rapid investment in precision CEA technologies. The market grew from USD 16.36 Billion in 2020 to USD 24.35 Billion in 2025. This expansion trajectory is projected to continue through 2034, with the market expected to more than double to USD 51.12 Billion, driven by structural demand from urbanizing populations and technology-enabled yield improvements.

North America leads globally with a 36.9% revenue share in 2025, driven by over 2,000 vertical farms in the United States, sustained venture capital investment exceeding USD 1.8 Billion cumulatively, and USDA specialty crop grant programs. Asia Pacific, at 29.7%, represents the fastest-growing opportunity, with Japan operating 300+ certified plant factories and China integrating indoor farming into its national food security framework.

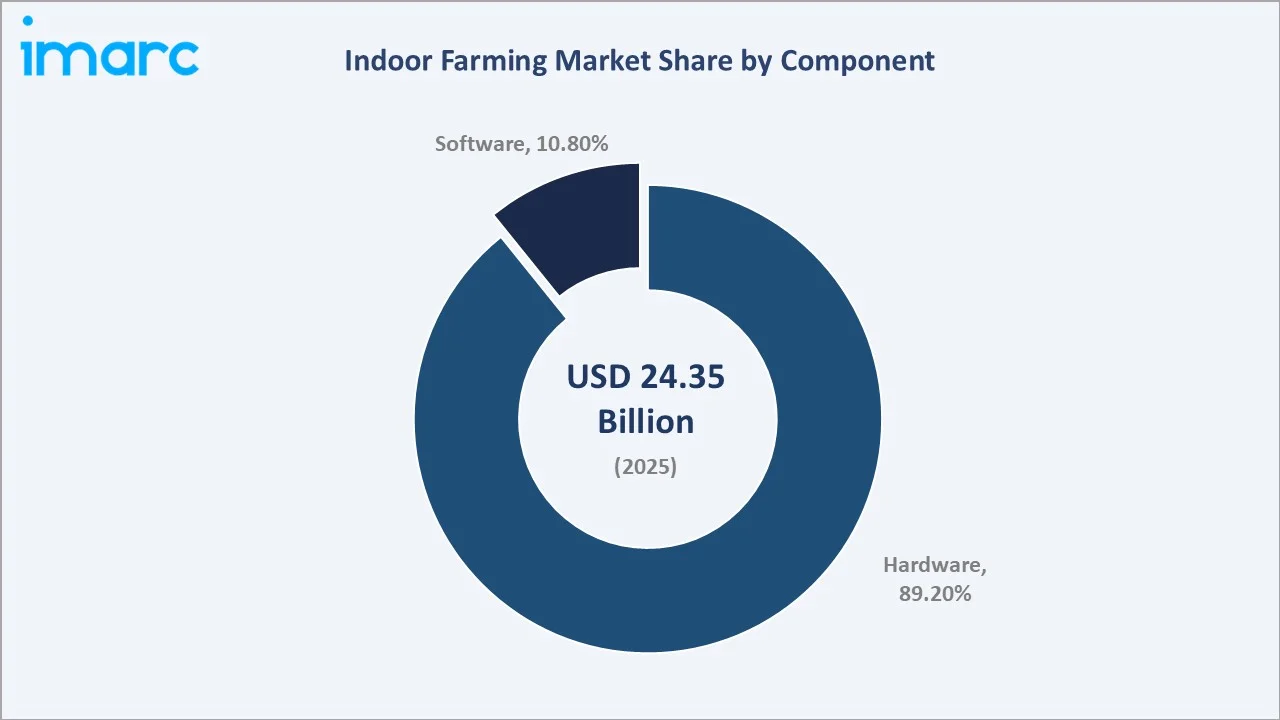

Greenhouse facilities command the largest share at 47.0%, benefitting from lower capital requirements and natural light supplementation. Hardware components account for 89.2% of the component market, reflecting significant expenditure on LED grow lights, HVAC systems, and automated nutrient delivery.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Facility Type) |

Greenhouse – 47.0% share (2025) |

|

Largest Segment (Component) |

Hardware – 89.2% share (2025) |

|

Leading Region |

North America – 36.9% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (food security + urbanization mandates) |

|

Top Companies |

Gotham Greens, 80 Acres Farms, Oishii, Plenty Unlimited Inc., UrbanKisaan Inc. |

|

Market Opportunity |

Vertical farm expansion in urban Asia Pacific and the Middle East is projected at USD 3–5 Billion by 2030 |

Key Analytical Observations Supporting The Above Data:

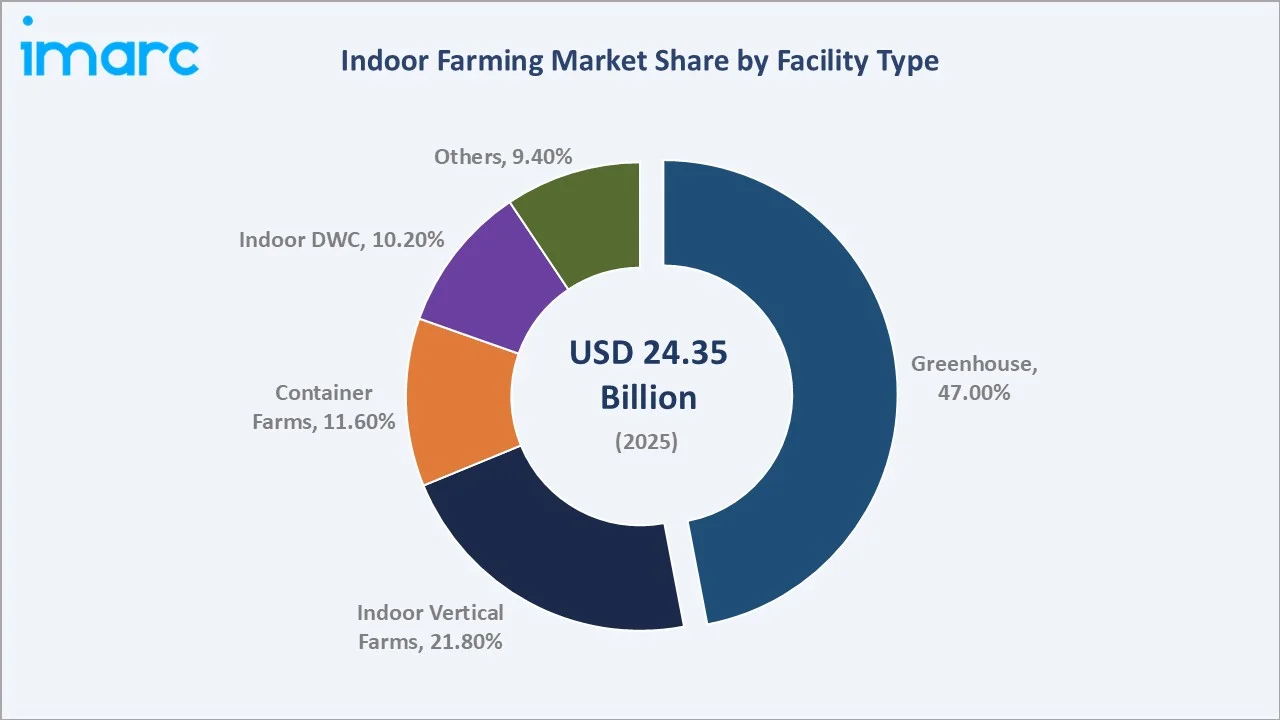

- Greenhouse facilities hold 47.0% of the market in 2025 (equivalent to approximately USD 11.44 Billion), preferred for their cost-efficiency, natural light utilization, and proven scalability across temperate climates in North America and Europe.

- Indoor vertical farms, commanding 21.8% share (approx. USD 5.31 Billion), are the fastest-growing facility sub-segment. Fourteen indoor and vertical farming companies have secured over USD 100 million in venture funding in 2023.

- Hardware dominates the component segment at 89.2% (approx. USD 21.72 Billion in 2025), driven by significant capital expenditure on LED grow lighting systems, HVAC and climate control equipment, and hydroponic racking structures critical for CEA operations.

- North America holds 36.9% regional share with the U.S. accounting for over 82% of the regional total, supported by water scarcity regulations in California and Arizona compelling fresh produce growers to adopt recirculating hydroponic systems.

- Asia Pacific is expanding at an estimated 10.2% CAGR driven by Japan's 300+ plant factories, China's 14th Five-Year Plan for smart greenhouse expansion, and South Korea's USD 300 Million investment in vertical farm research centers since 2020.

Global Indoor Farming Market Overview

Indoor farming refers to the cultivation of crops within enclosed, controlled-environment structures that regulate temperature, humidity, light spectrum, CO2 concentration, and nutrient delivery independent of external weather conditions. Originating from Dutch greenhouse practices and Japanese plant factory research in the late 20th century, its application has expanded to encompass residential food production, commercial leafy green cultivation, and pharmaceutical-grade botanical production.

Macroeconomic factors, including the degradation of approximately 33% of global agricultural land (FAO, 2023), climate change-induced weather volatility impacting yield predictability, rapid urbanization concentrating over 55% of the global population in cities, and escalating consumer preference for pesticide-free produce, are primary growth catalysts.

Market Dynamics

To evaluate market opportunities, Request Sample

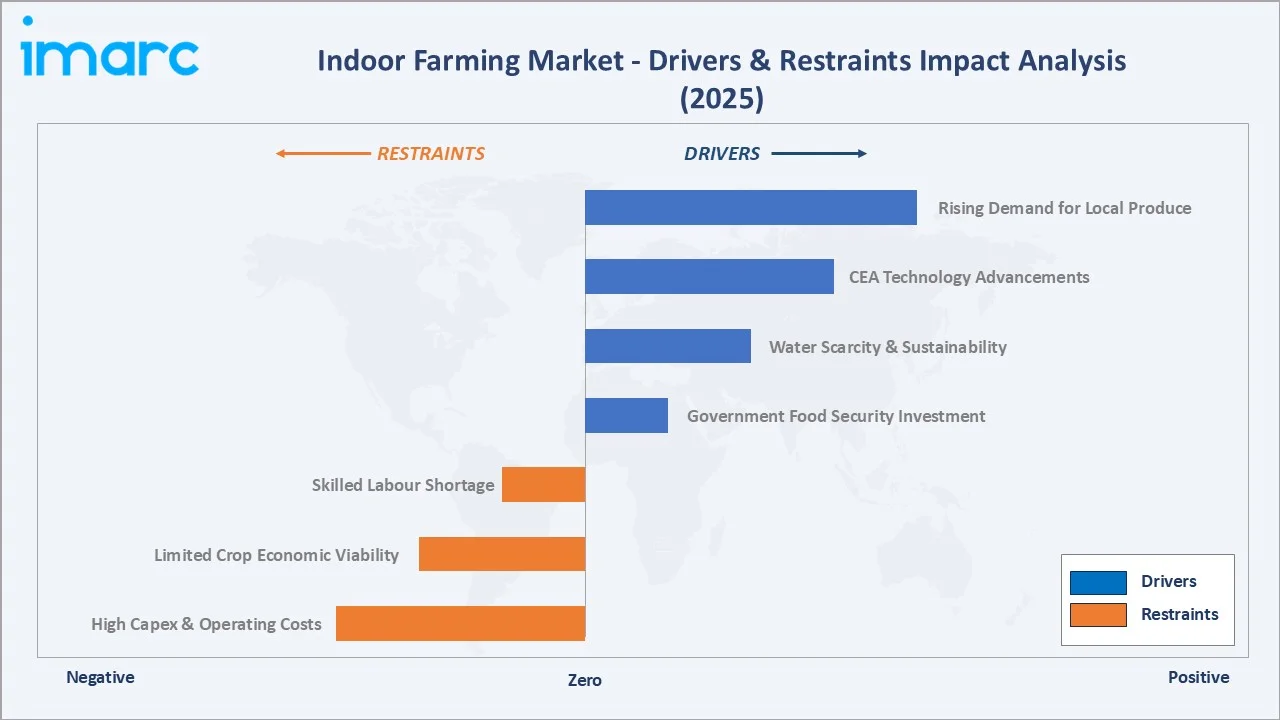

Market Drivers

- Growing Demand for Locally Sourced, Pesticide-Free Produce: Consumer preference surveys indicate 75% of shoppers are willing to pay a premium for locally grown produce. Indoor farms positioned near metropolitan areas reduce cold-chain costs, post-harvest losses, and food miles, while enabling year-round delivery of certified pesticide-free leafy greens, herbs, and tomatoes.

- Technological Advancements in CEA Systems: Next-generation LED grow lights now achieve photosynthetic photon flux densities (PPFD) of 1,200+ µmol/m²/s with 70% energy efficiency gains over legacy HPS lamps.

- Water Scarcity and Sustainability Mandates: Hydroponic systems consume 90–95% less water than conventional field agriculture. Regions facing acute water stress, including the Middle East, California, and Australia, are mandating water-efficient cultivation, accelerating indoor farming adoption as a compliance-driven imperative for commercial growers.

- Government Food Security Investment Programs: Singapore's SGD 200 Million '30 by 30' initiative, the UAE's Ministry of Climate Change indoor farming grants, Japan's Plant Factory Consortium public subsidies, and USDA specialty crop grants collectively represent over USD 2 Billion in government-backed indoor farming development globally through 2030.

These drivers reinforce a self-sustaining growth cycle, technology cost reductions drive commercial viability, which attracts institutional capital, which accelerates technology improvements, which further expands the addressable crop range and geographic markets for indoor farming solutions.

Market Restraints

- High Capital Expenditure and Operating Costs: Indoor vertical farm setup costs range from USD 10 Million to USD 100 Million per acre-equivalent, compared to USD 50,000–100,000 for conventional greenhouse structures. Energy-intensive artificial lighting accounts for up to 30% of total operating costs, constraining profitability margins for all but the highest-value crop categories.

- Limited Crop Economic Viability: Current indoor farming economics are viable primarily for leafy greens, herbs, microgreens, and premium produce such as strawberries and tomatoes. Staple caloric crops, wheat, rice, and maize, remain economically unviable indoors, limiting the sector's contribution to resolving global food security at scale.

- Skilled Labor and Operational Complexity: Operating advanced indoor farms requires rare interdisciplinary skill sets spanning agronomy, data science, mechanical engineering, and food safety compliance.

Market Opportunities

- Expansion into Protein and Medicinal Crops: Early-stage pilots in indoor algae cultivation for high-protein supplement markets, pharmaceutical-grade cannabis in regulated jurisdictions, and nutraceutical herb production represent multi-billion-dollar adjacencies anticipated to unlock over the 2026–2034 forecast period as regulatory frameworks evolve.

- Smart Farm-as-a-Service Business Models: Technology providers are commercializing subscription-based modular farm units for supermarkets and food service operators, lowering the capex barrier and democratizing indoor farming access beyond well-capitalized large operators.

Market Challenges

- Consumer Price Sensitivity: Premium pricing of indoor-grown produce, typically 20–50% above conventionally farmed equivalents, creates adoption barriers in price-sensitive markets. Achieving cost parity through technology efficiency gains remains the sector's central commercial challenge over the forecast horizon.

- Energy Transition Dependency: The environmental case for indoor farming is materially weakened in grids reliant on fossil fuels. Operators in regions without access to renewable energy face both elevated cost structures and growing scrutiny from ESG-aligned institutional investors and retail procurement teams applying carbon footprint criteria.

Emerging Market Trends

1. AI-Driven Precision Cultivation

Artificial intelligence and machine learning platforms are enabling autonomous optimization of light spectra, nutrient concentration, temperature, and CO2 parameters in real time. AeroFarms' proprietary AI system demonstrated a 390x yield improvement per square foot over conventional field farming.

2. Vertical Integration and Direct Retail Partnerships

Gotham Greens supplies Whole Foods Market, Target, and Walmart across 40+ U.S. states, securing premium shelf placement and predictable revenue. This direct-to-retail model is compressing farm-to-shelf cycles to under 24 hours for metropolitan consumers and reshaping fresh produce supply chain economics.

3. Renewable Energy Co-location

Leading operators are co-locating indoor farms with solar arrays and wind installations to offset electricity costs and reduce carbon footprints. AppHarvest's 2.6 million sq ft Kentucky facility operated on collected rainwater and solar-supplemented energy, targeting carbon-neutral production by 2026. This trend is accelerating in Europe, where green electricity access is rapidly expanding.

4. Modular Container Farm Deployments in Remote Regions

Modular shipping-container farms are being deployed in remote arctic, desert, and conflict-affected zones where traditional agriculture is climatically infeasible. Installations by Saudi Arabian desert complexes and military base supply chains are demonstrating the facility type's strategic relevance beyond urban food retail.

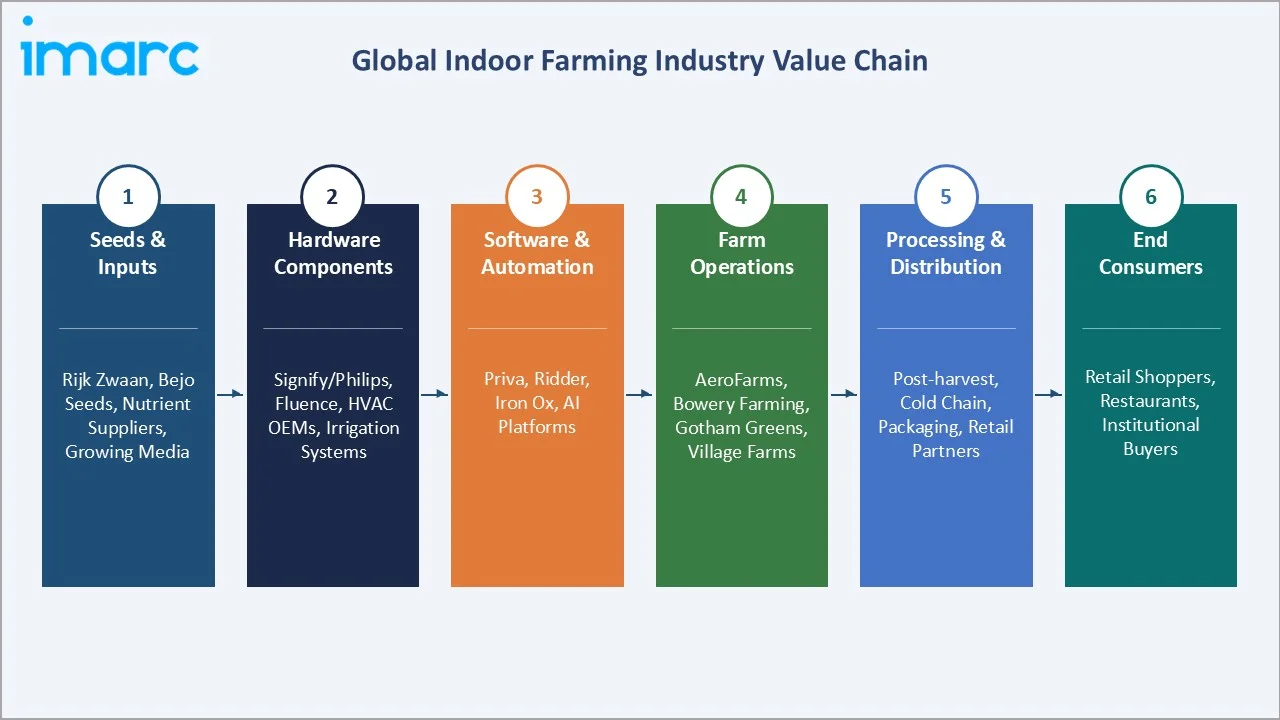

Industry Value Chain Analysis

The indoor farming value chain spans seed and input sourcing through end-consumer delivery, with each stage populated by specialized operators whose performance directly influences crop yield, product quality, food safety compliance, and farm economics.

|

Stage |

Key Players / Examples |

|

Raw Materials & Seeds |

Rijk Zwaan, Bejo Seeds; nutrient solution providers; growing media manufacturers (rockwool, coco coir); water treatment providers |

|

Hardware Components |

LED grow light manufacturers (Signify/Philips); HVAC and climate control OEMs; hydroponic rack and structure fabricators; irrigation system suppliers |

|

Software & Automation |

Farm management software developers (Priva, Ridder); IoT sensor providers; AI analytics platforms; robotics integrators |

|

Farm Operations |

Greenhouse operators (Gotham Greens); vertical farm operators; container farm operators; indoor DWC operators |

|

Processing & Packaging |

Post-harvest washing, trimming, and drying lines; modified atmosphere and clamshell packaging; cold-chain logistics operators; food safety testing laboratories |

|

Distribution & Retail |

Foodservice distributors; direct retail partnerships (Whole Foods, Walmart, Target); e-commerce platforms; subscription box services (Hungry Root) |

|

End Consumers |

Urban retail grocery shoppers; premium restaurant chains; institutional buyers (hospitals, schools, corporate campuses, military catering) |

Technology Landscape in the Indoor Farming Industry

Advanced LED Photonics

Philips Horticulture (Signify)’s GreenPower LED interlighting delivers targeted light spectra at 50% lower energy consumption versus legacy HPS installations. Full-spectrum and tunable LED systems now support differentiated light recipes for root development, vegetative expansion, and fruit set, enabling operators to accelerate crop cycles by 15–20%.

Hydroponic, Aeroponic, and Aquaponic Innovations

Next-generation aeroponic systems developed by AeroFarms mist plant roots with nutrient solutions in 50-micron droplets, reducing water usage by 95% relative to soil farming and enabling harvest cycles 30–40% faster than conventional hydroponics. Deep water culture (DWC) system refinements have improved dissolved oxygen delivery, increasing leafy green yields by 15–20%. Aquaponic integrations combining fish and plant cultivation are generating dual-revenue streams for specialist indoor operators.

Automation and Robotics

Iron Ox, a California‑based ag‑tech startup, developed one of the world’s first fully autonomous indoor farms where AI‑driven robots grow, move, monitor, and help harvest leafy greens and herbs in a hydroponic system, aiming to increase local production, reduce transport distances, and address labor shortages in agriculture.

IoT-Enabled Climate Intelligence

Quantified Sensor Technology has expanded its platform‑agnostic precision greenhouse monitoring by enabling its wireless sensor systems to integrate directly with the widely used Priva One climate control platform, allowing growers to view detailed micro‑ and macro‑climate data in one place and improve water, nutrient, and labor efficiency without switching systems.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Facility Type | Greenhouse | 47.0% | 2025 |

| Crop Type | Fruits, Vegetables, and Herbs | 96.5% | 2025 |

| Component | Hardware | 89.2% | 2025 |

| Growing System | Soil-based | 41.6% | 2025 |

| Region | North America | 36.9% | 2025 |

By Facility Type

Greenhouse facilities dominate the facility-type segment with a 47.0% share in 2025, equivalent to approximately USD 11.44 Billion. Their lower capital requirements, typically USD 20–50 per square foot versus USD 150–250 for vertical farms, combined with natural sunlight supplementation, make greenhouses the preferred choice for medium-to-large-scale operators across North America and Europe.

To access detailed market analysis, Request Sample

Indoor vertical farms hold 21.8% share and are the fastest-growing sub-segment. Their ability to stack growing layers 10–20 high enables land-use efficiency 100x greater than conventional fields, making them uniquely viable in land-scarce urban environments. Container farms at 11.6% offer rapid deployment flexibility, gaining traction in defense, hospitality, and remote mining camp supply chains.

By Component

Hardware commands 89.2% of the component market, reflecting the capital-intensive nature of indoor farming infrastructure. LED grow light systems represent the single largest hardware category, accounting for an estimated 28–32% of total hardware expenditure. HVAC and climate control systems follow at approximately 22% of hardware spend, essential for maintaining precise temperature and humidity bands critical for consistent crop quality.

Software at 10.8% (approx. USD 2.63 Billion) is growing at an accelerated pace, supported by cloud-based farm management platforms, computer vision systems for automated pest and disease detection, and predictive analytics for yield optimization.

Regional Market Insights

North America's market leadership (36.9%, 2025) reflects the combination of a mature CEA investment ecosystem, significant retail infrastructure alignment, and acute water conservation drivers across the western U.S. Over 2,000 commercial indoor farms operated in the U.S. as of 2024, with fresh produce shortfalls caused by droughts in California and Arizona accelerating grower transitions to recirculating hydroponic systems. Canada's British Columbia greenhouse cluster, among the world's largest, contributes materially to regional revenue.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

North America |

36.9% |

High CEA investment, retail partnerships, USDA programs, water scarcity |

USDA specialty crop grants; state water conservation mandates |

|

Asia Pacific |

29.7% |

Food security mandates, urban farming policies, and plant factory networks |

National food self-sufficiency targets; Plant Factory subsidies |

|

Europe |

21.5% |

EU Farm-to-Fork strategy, Dutch greenhouse cluster, premium organic demand |

EU Farm-to-Fork 25% organic target by 2030 |

|

Latin America |

6.2% |

Expanding urban middle class, climate variability driving CEA adoption |

Limited formal regulation; nascent government support |

|

Middle East & Africa |

5.7% |

Food import reduction goals, UAE/Saudi Vision 2030, desert farming imperatives |

Vision 2030 food security mandates; halal compliance |

Asia Pacific is the highest-growth region, with the agriculture ministry reporting that the number of plant factories in Japan has increased from 93 in March 2011 to 432 in February 2024. China's 14th Five-Year Plan explicitly targets smart greenhouse expansion across Northern provinces for food self-sufficiency, with state-funded pilot farms operating in Beijing, Shanghai, and Chengdu.

Competitive Landscape

The global indoor farming market exhibits a fragmented competitive structure, with no single operator commanding more than 8–10% of global revenues. Gotham Greens, 80 Acres Farms, Oishii, Plenty Unlimited Inc., and UrbanKisaan Inc. collectively hold approximately 22–27% of the market in 2025. Competitive intensity is highest in the U.S. vertical farm segment, where well-capitalized operators compete on proprietary grow technology, retail distribution reach, and cost-per-kilogram of produce.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Gotham Greens |

Gotham Greens |

Strong Challenger |

13 facilities across the U.S.; distribution in all 50 states; direct Whole Foods, Walmart & Target supply |

|

80 Acres Farms |

80 Acres Farms / Soli Organic |

Market Leader – Vertical |

Merged with Soli Organic in August 2025; projected first-year revenues approaching $200 million; serving 17,000+ retail locations |

|

Oishii |

Oishii |

Premium Niche Leader |

Raised USD 150M Series B in 2024; 237,500 sq ft strawberry vertical farm; premium pricing strategy at Whole Foods. |

|

Plenty Unlimited Inc. |

Plenty |

Challenger / Niche Player |

Proprietary indoor vertical farming technology platform capable of up to 350x more yield per acre than conventional farms |

|

UrbanKisaan Inc. |

UrbanKisaan |

Challenger / Niche Player |

Hydroponic vertical farming platform growing 50+ crop varieties using 95% less water with 30% higher crop yield than traditional methods |

Key Company Profiles

Plenty Unlimited Inc.

Plenty Unlimited Inc. is an indoor vertical farming technology company that has spent over a decade developing indoor agricultural technologies. The company is headquartered in Laramie, Wyoming, and operates a research and development center alongside its commercial strawberry farm in Richmond, Virginia.

- Product Portfolio: Driscoll's Plenty Sweet strawberries, grown locally in the Richmond vertical farm and available at Walmart stores across the Baltimore-to-D.C. corridor.

- Recent Developments: The company is advancing the development of the world's largest vertical farming research center in Laramie, Wyoming, focusing on food ingredients and pharmaceuticals..

- Strategic Focus: Plenty is solely focused on strawberries, expanding growing capacity at the Richmond farm, and pursuing opportunities to license and sell its proprietary vertical strawberry farming technology to new locations globally.

UrbanKisaan Inc.

UrbanKisaan Inc. is a Hyderabad-based agri-tech company founded in 2017, reshaping food production through hydroponic and vertical farming technologies. The company employs nutrient-rich water-based growing systems that drastically reduce reliance on traditional agricultural resources.

- Product Portfolio: A range of 50+ pesticide-free crops, including leafy greens, herbs, and salad vegetables grown across 30 vertical farms in and around Hyderabad, distributed via Swiggy, Zomato, and Dunzo.

- Recent Developments: In August 2023, NKK Investments partnered with UrbanKisaan to expand hydroponic and vertical farming operations into Saudi Arabia, the UAE, and Oman.

- Strategic Focus: UrbanKisaan is focused on building local farms using advanced hydroponic systems and its Speed Breeding Program to enhance crop quality and accelerate growth cycles.

Gotham Greens

Gotham Greens is a pioneering U.S. urban greenhouse company and operates 13 climate-controlled greenhouses in nine U.S. states, including New York, Illinois, Rhode Island, Maryland, Virginia, Colorado, California, Georgia, and Texas.

- Product Portfolio: Greenhouse-grown salad greens, and premium salad dressings, herbs (multiple varieties), dips, pesto sauces, and cooking sauces.

- Recent Developments: Gotham Greens' products are available in more than 6,500 retail locations across all 50 states; and have around 13 greenhouses.

- Strategic Focus: Urban greenhouse network expansion into new major metropolitan markets; food service and institutional buyer channel development.

Market Concentration Analysis

The indoor farming market reflects a fragmented competitive structure at both the technology and operations levels. The top five commercial operators collectively hold approximately 22–27% of global revenues in 2025, representing a low-to-moderate concentration ratio consistent with an industry still in formative stages of commercial consolidation.

A long tail of hundreds of regional greenhouse operators, small-scale vertical farm start-ups, and technology suppliers maintains market diversity across geographies and facility types. Consolidation dynamics are accelerating in the vertical farm sub-segment following high-profile funding rounds and restructurings in 2022–2023 that rationalized over-capitalized entrants.

Surviving scaled operators are deepening competitive moats through proprietary grow technology IP, long-term retail supply contracts, and geographic farm network density advantages. The greenhouse segment remains more fragmented, dominated by independent operators in the Netherlands, Canada, and the U.S.

Investment & Growth Opportunities

Fastest Growing Segments

Vertical farm technology licensing (estimated CAGR 12–15%), smart farm-as-a-service platforms (16–18% CAGR), and container farm deployments in remote/arid regions (10–12% CAGR) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable market of approximately USD 8–10 Billion, accessible at lower capital intensity than direct farm ownership.

Emerging Market Expansion

The Middle East and Asia Pacific collectively represent an incremental USD 3–5 Billion indoor farming opportunity by 2030. Entry through joint ventures with local agri-technology developers, alignment with government food security procurement mandates, and technology transfer agreements offer accretive pathways for international operators and investors seeking exposure to high-growth emerging market CEA deployment.

Venture and Institutional Investment Trends

- Key investment themes include AI-powered crop management software, energy-efficient LED photonics, robotic transplanting and harvesting equipment, and blockchain-enabled farm-to-retail traceability platforms.

- Institutional and private equity capital is increasingly targeting vertical integration plays, consolidating grow technology IP, commercial farm operations, distribution logistics, and retail brand ownership into single platform companies capable of commanding premium valuations.

Future Market Outlook (2026-2034)

The global indoor farming market is positioned for sustained, broad-based growth through 2034. From a base of USD 24.35 Billion in 2025, the market is projected to reach USD 51.12 Billion by 2034, representing total incremental value creation of over USD 26 Billion over nine years, at a CAGR of 8.28%.

Technology evolution, particularly continued LED cost deflation projected at 40% through 2030, green electricity access expansion reducing energy cost burdens, and AI-driven yield optimization scaling commercially, will materially narrow the operating cost gap between indoor farms and conventional agriculture. As economics improve, the total addressable crop range will expand beyond current leafy greens and herbs to encompass tomatoes, peppers, berries, and eventually higher-calorie crops.

Long-term, the market's trajectory is tied to three structural macro-themes: urbanization (creating space-constrained markets where controlled-environment agriculture is often the only commercially viable fresh produce option), climate change (intensifying weather volatility and water scarcity mandates driving institutional adoption), and rising global consumer demand for transparent, sustainable, and locally produced food supply chains.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including indoor farm operators, CEA technology vendors, retail category managers, agri-investment analysts, and regulatory specialists across North America, Europe, and Asia Pacific. Primary data collection focused on market size validation, competitive positioning, technology adoption timelines, and investment intent across all covered geographies.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, regulatory filings, USDA National Agricultural Statistics Service data, Japanese Ministry of Agriculture plant factory census data, industry databases (Euromonitor, IBISWorld), and trade publications (CEA Investor, Indoor Ag-Con, Vertical Farm Daily). Patent databases, including the USPTO and EPO, were reviewed for technology landscape mapping.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, urbanization rates, food security investment indices, technology cost curve projections, and historical market evolution data from 2020 to 2025. All segment-level forecasts were independently validated through demand-side buyer surveys and supply-side operator capacity planning data.

Indoor Farming Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Facility Types Covered | Greenhouse, Indoor Vertical Farms, Container Farms, Indoor Deep Water Culture, Others |

| Crop Types Covered |

|

| Components Covered |

|

| Growing Systems Covered | Aeroponics, Hydroponics, Aquaponics, Soil-Based, Hybrid |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Netherlands, Germany, United Kingdom, France, Italy, China, Japan, Singapore, South Korea, Brazil, Mexico |

| Companies Covered | Gotham Greens, 80 Acres Farms, Oishii, Plenty Unlimited Inc., UrbanKisaan Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the indoor farming market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global indoor farming market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the indoor farming industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Indoor Farming Market Report

The global indoor farming market reached USD 24.35 Billion in 2025. It is projected to reach USD 51.12 Billion by 2034.

The indoor farming market is expected to grow at a CAGR of 8.28% during the forecast period from 2026 to 2034, supported by consistent demand growth from food security, sustainability, and technology advancement drivers.

North America leads the market with a 36.9% revenue share in 2025, driven by a mature CEA investment ecosystem, extensive retail distribution partnerships, and water scarcity regulations in western U.S. states compelling grower adoption of indoor hydroponic systems.

Greenhouse facilities dominate the market with a 47.0% share in 2025, valued at approximately USD 11.44 Billion. Their dominance is driven by lower capital intensity, natural light supplementation economics, and proven scalability for high-volume tomato, cucumber, and pepper production.

The hardware segment holds the largest component share at 89.2% in 2025, driven by significant capital expenditure on LED grow lighting systems, HVAC and climate control equipment, and hydroponic racking and structural components.

Key players include Gotham Greens, 80 Acres Farms, Oishii, Plenty Unlimited Inc., and UrbanKisaan Inc.

Asia Pacific growth is driven by Japan's 300+ certified plant factory network, China's 14th Five-Year Plan smart greenhouse expansion targets, South Korea's USD 300 Million vertical farm R&D investment, and government food self-sufficiency mandates across Singapore, Japan, and South Korea.

Key challenges include high capital and operating expenditure, limited crop economic viability beyond premium produce categories, energy intensity constraints in fossil-fuel-reliant grids, and a global shortage of skilled interdisciplinary operators capable of managing advanced CEA facilities.

High-growth investment opportunities include vertical farm technology licensing, AI-powered farm management software platforms, smart farm-as-a-service subscription models, container farm deployments in arid regions, and Middle East and Asia Pacific greenfield CEA project pipelines.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)