Industrial IoT Market Size, Share, Trends and Forecast by Component, End User, and Region, 2026-2034

Industrial IoT Market Size, Share, Trends & Forecast (2026-2034)

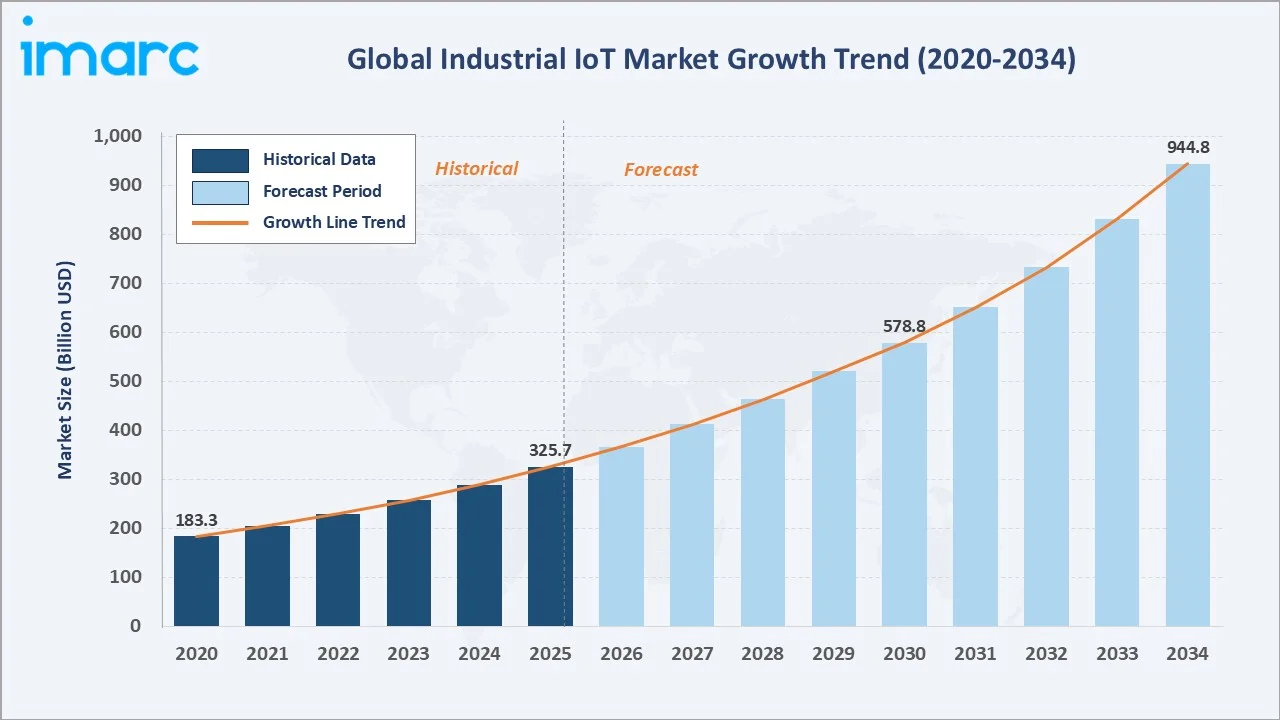

The Industrial IoT market was valued at USD 325.7 Billion in 2025 and is projected to reach USD 944.8 Billion by 2034, exhibiting a CAGR of 12.18% during 2026-2034. The rapid integration of connected devices, intelligent sensors, and real-time analytics into industrial operations is reshaping the manufacturing, energy, and transportation sectors worldwide.

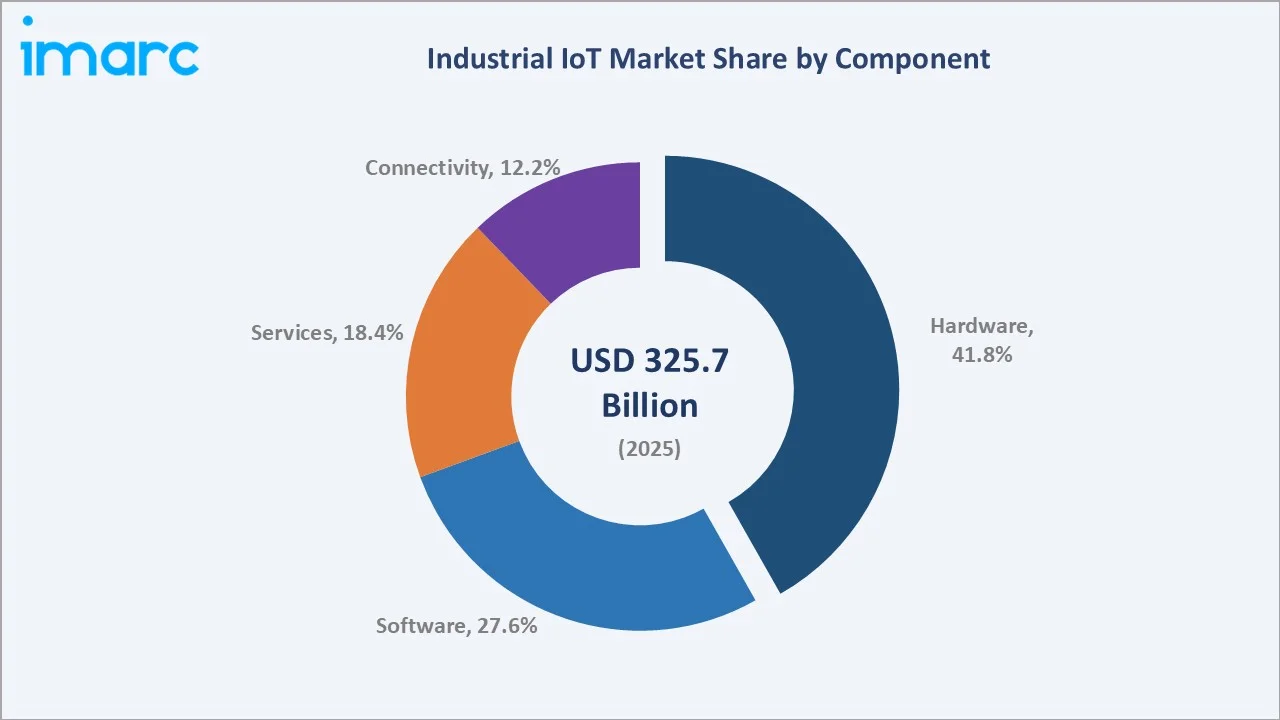

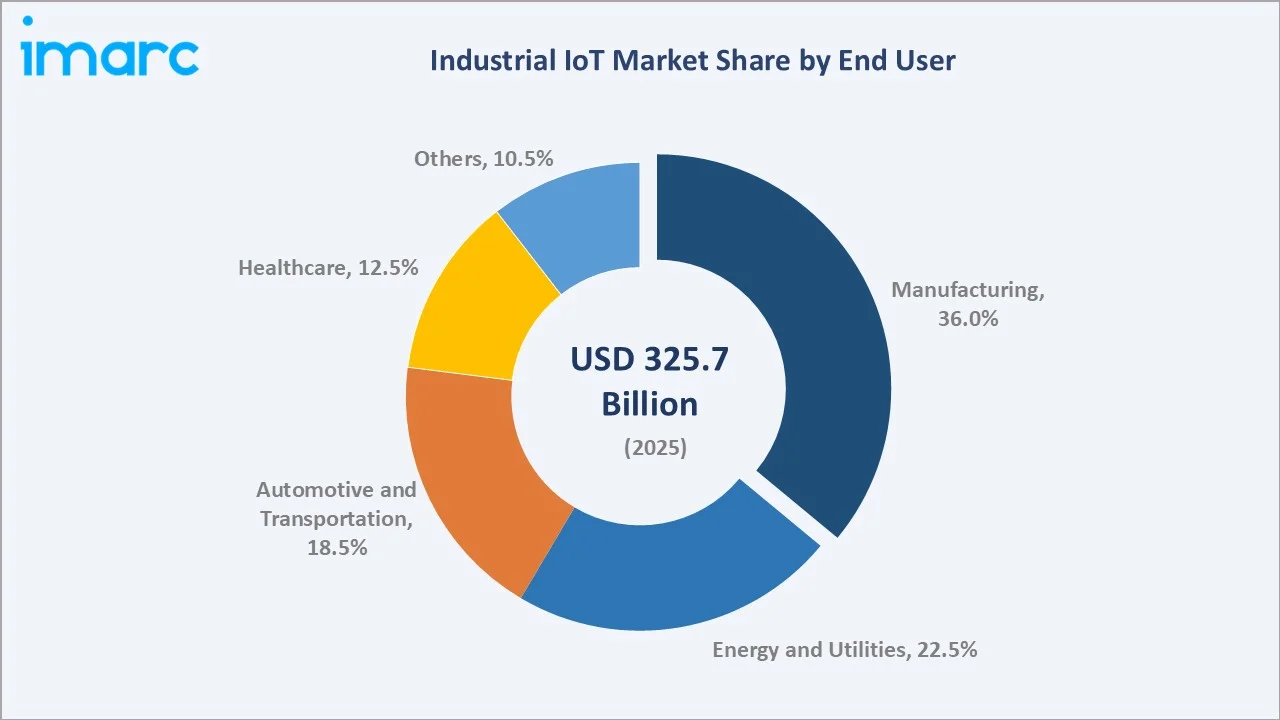

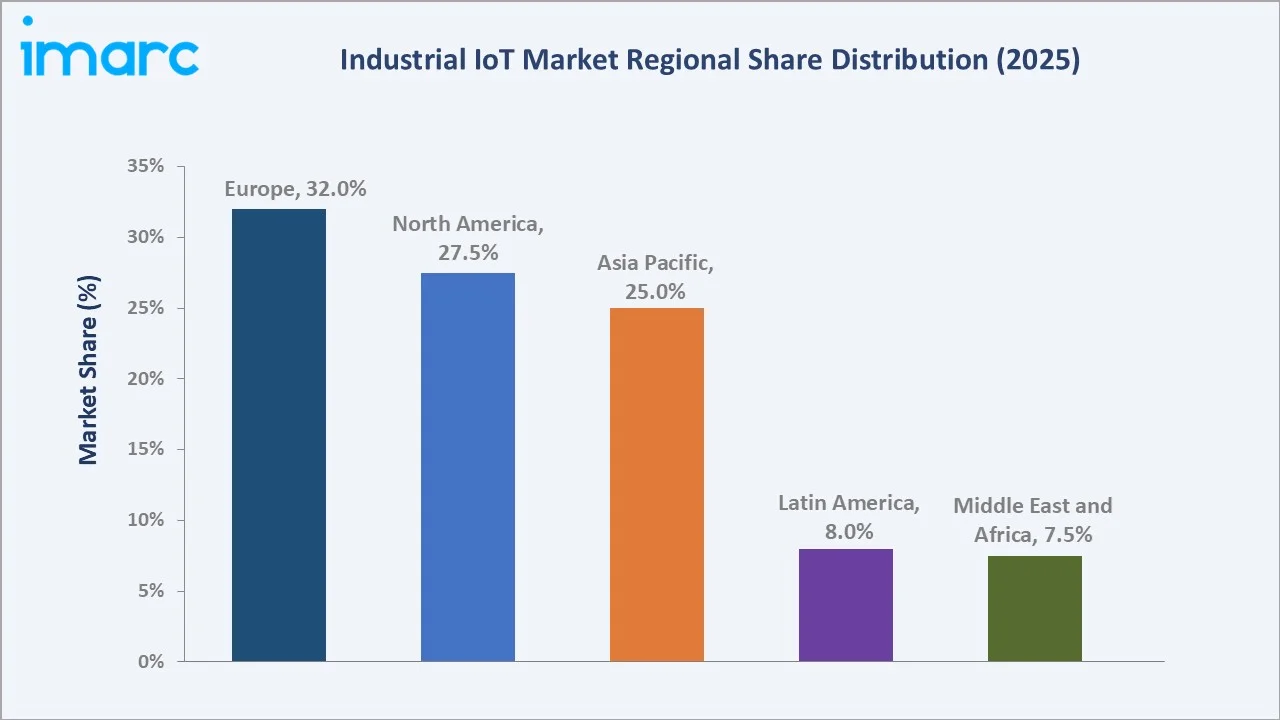

Hardware leads the component segment at 41.8%, manufacturing commands a 36.0% end user share, and Europe dominates regional contribution at 32.0% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 325.7 Billion |

|

Forecast Market Size (2034) |

USD 944.8 Billion |

|

CAGR (2026-2034) |

12.18% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (32.0%, 2025) |

|

Second Largest Region |

North America (27.5%, 2025) |

|

Leading Component |

Hardware (41.8%, 2025) |

|

Leading End-User |

Manufacturing (36.0%, 2025) |

The industrial IoT market expanded from USD 183.3 Billion in 2020 to USD 325.7 Billion in 2025, underpinned by Industry 4.0 initiatives, smart factory rollouts, and increasing demand for predictive maintenance solutions. Anchored at USD 578.8 Billion in 2030, the forecast to USD 944.8 Billion by 2034 reflects strong and sustained momentum driven by edge computing, AI integration, and expanding 5G-enabled industrial networks.

To get more information on this market, Request Sample

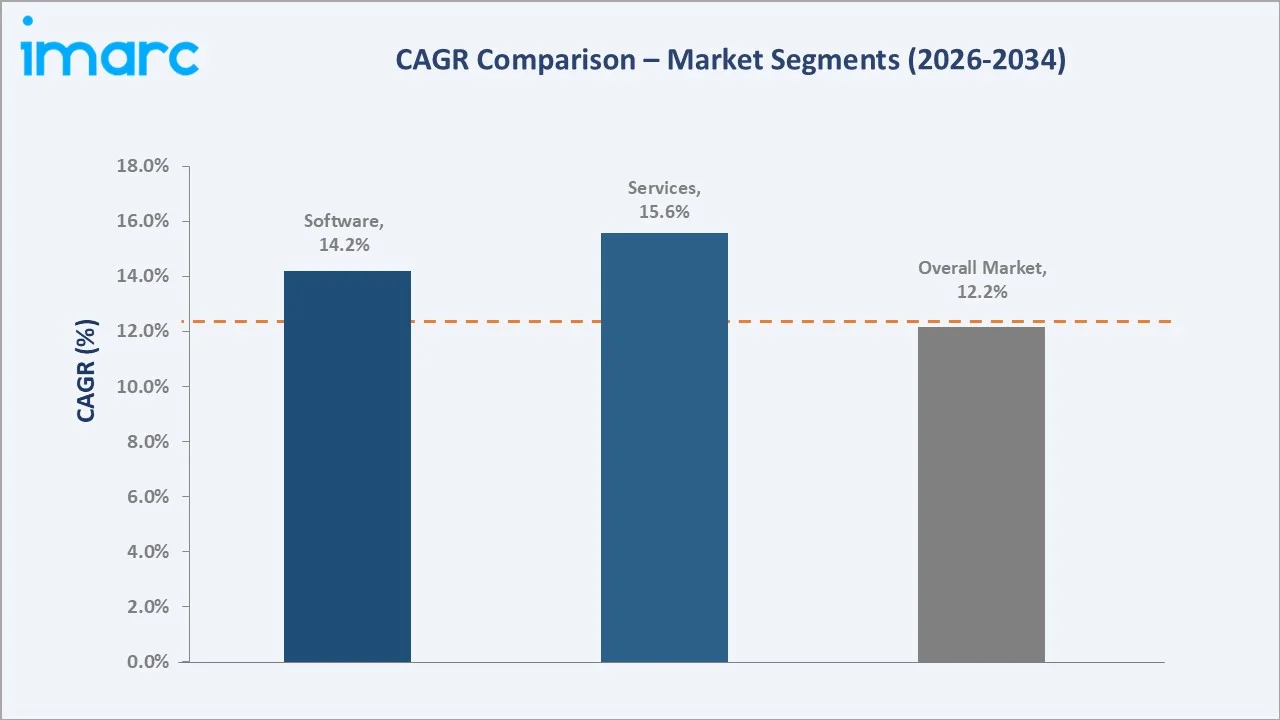

CAGR trajectories across component and end user sub-segments show software, services, and connectivity expanding faster than the overall 12.18% market CAGR, driven by platform adoption, managed services growth, and the rapid expansion of private industrial networks.

Executive Summary

The industrial IoT market is on a robust expansion path, growing from USD 183.3 Billion in 2020 to USD 944.8 Billion by 2034. Industrial enterprises are accelerating investment in connected sensors, edge gateways, and cloud-based analytics platforms to improve operational efficiency, reduce downtime, and enable data-driven decision-making. The convergence of IT and OT is driving broad adoption across the manufacturing, energy, automotive, and healthcare sectors.

Hardware leads at 41.8% in 2025, anchored by widespread deployment of sensors, controllers, and industrial gateways across factory floors and utility infrastructure. Manufacturing dominates the end user landscape at 36.0%, supported by smart factory programs and Industry 4.0 investments. As per IMARC Group, the global industry 4.0 market size reached USD 188.5 Billion in 2025. Europe commands the largest regional share at 32.0%, supported by a mature industrial base and strong government commitment to smart manufacturing.

Key Market Insights

|

Insight |

Data |

|

Leading Component |

Hardware – 41.8% share (2025) |

|

Second Largest Component |

Software – 27.6% share (2025) |

|

Leading End-User |

Manufacturing – 36.0% share (2025) |

|

Second Largest End-User |

Energy and Utilities – 22.5% share (2025) |

|

Leading Region |

Europe – 32.0% share (2025) |

|

Second Largest Region |

North America – 27.5% share (2025) |

|

Top Companies |

Siemens, Cisco Systems, Inc., Rockwell Automation, ABB, PTC |

Key Analytical Observations Expanding on the Data Above:

- Hardware dominance at 41.8% reflects the foundational role of physical devices, including sensors, actuators, gateways, and programmable logic controllers, in any Industrial IoT deployment. These components serve as the primary data-capture layer across industrial environments.

- Software at 27.6% captures the growing enterprise preference for cloud-based Industrial IoT platforms, analytics dashboards, and digital twin tools that convert raw operational data into actionable insights.

- Manufacturing leadership at 36.0% is driven by broad smart factory adoption, Industry 4.0 program rollouts, and the critical need for real-time process monitoring and predictive maintenance across complex production lines.

- Energy and utilities share at 22.5% reflects strong adoption of Industrial IoT solutions for smart grid management, asset performance monitoring, remote infrastructure supervision, and predictive maintenance of critical equipment. Utilities are increasingly deploying connected systems to improve operational reliability, energy efficiency, and grid resilience.

- Europe at 32.0% showcases an advanced industrial ecosystem, strong regulatory support for digital transformation, and mature adoption of connected manufacturing and energy systems across Germany, France, and the United Kingdom.

Industrial IoT Market Overview

Industrial IoT refers to the use of interconnected sensors, devices, machines, and software to collect, exchange, and analyze data for improving efficiency, productivity, and decision-making in industrial operations. Core application areas span smart manufacturing, predictive maintenance, remote asset monitoring, energy management, fleet tracking, and quality control across diverse end-user industries.

The ecosystem integrates hardware manufacturers, software platform providers, connectivity and network suppliers, system integrators, and end-user enterprises, collectively supported by cloud infrastructure, cybersecurity solutions, and professional services. Macroeconomic tailwinds, including government-backed Industry 4.0 programs, rising labor costs, and increasing energy efficiency mandates, are accelerating adoption across both developed and emerging industrial economies.

Market Dynamics

To evaluate market opportunities, Request Sample

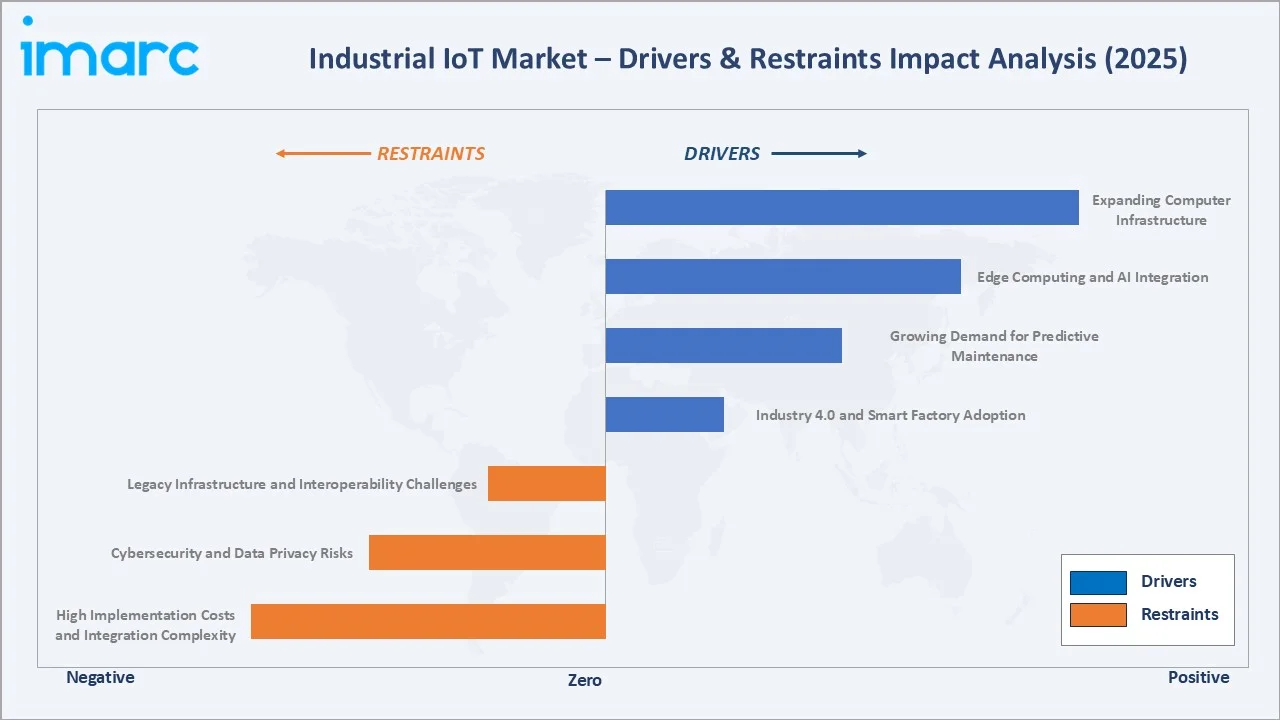

Market Drivers

- Industry 4.0 and Smart Factory Adoption: The widespread rollout of Industry 4.0 frameworks by governments and enterprises across Europe, North America, and Asia-Pacific is creating strong structural demand for Industrial IoT hardware, software, and connectivity infrastructure.

- Growing Demand for Predictive Maintenance: Rising demand for predictive and condition-based maintenance is driving rapid deployment of connected sensors and analytics platforms.

- Edge Computing and AI Integration: The integration of AI and edge computing into industrial environments is enabling faster, smarter, and more secure processing of operational data at the source. Reduced latency, lower bandwidth costs, and improved real-time decision-making are accelerating edge AI deployments across manufacturing, energy, and transportation sectors.

- Expanding Connectivity Infrastructure: Expansion of 5G networks and the decline in low-power wide-area networking (LPWAN) costs are lowering connectivity barriers for Industrial IoT deployments at scale, particularly in remote industrial sites, mines, and large outdoor infrastructure. As of January 2026, India became the 2nd largest 5G consumer with over 400 Million users worldwide.

Market Restraints

- High Implementation Costs and Integration Complexity: The complexity and cost of deploying Industrial IoT solutions, particularly when integrating with existing legacy OT infrastructure, remain a significant adoption barrier. Upfront hardware costs, system integration fees, and ongoing platform licensing can be prohibitive for small and medium-sized industrial enterprises with limited IT budgets.

- Cybersecurity and Data Privacy Risks: As industrial systems become more interconnected, the attack surface for cyber threats expands significantly. Concerns over ransomware attacks, unauthorized access to industrial control systems, and data security vulnerabilities can slow Industrial IoT adoption across critical industries.

- Legacy Infrastructure and Interoperability Challenges: A significant portion of industrial facilities operate on aging control systems and proprietary protocols that are difficult to integrate with modern Industrial IoT platforms. Retrofitting legacy equipment, managing OT/IT convergence, and ensuring backward compatibility require specialized expertise and extended deployment timelines.

Market Opportunities

- Sustainability and Energy Efficiency Programs: The global shift toward net-zero manufacturing and sustainable industrial operations is creating demand for Industrial IoT-powered energy management, emissions monitoring, and resource optimization solutions. Industrial operators are increasingly using connected systems to track energy consumption at the machine level and optimize usage in real time.

- Emerging Market Industrialization: Rapid industrialization across India, Southeast Asia, Latin America, and parts of Africa is generating new demand for scalable and affordable Industrial IoT solutions. Government-backed smart manufacturing programs and foreign direct investment in industrial infrastructure are accelerating deployment in previously underserved markets.

Market Challenges

- Shortage of Skilled Workforce: Many industrial organizations face a significant skills gap in deploying, managing, and optimizing Industrial IoT systems. The convergence of IT and OT disciplines requires specialized knowledge that is in short supply, slowing deployment timelines and increasing dependence on external system integrators.

- Standardization and Interoperability Gaps: The lack of universal Industrial IoT standards and the fragmented nature of industrial communication protocols complicate interoperability across multi-vendor deployments and increase integration costs.

Emerging Market Trends

1. Digital Twin Proliferation in Industrial Operations

Digital twin technology is becoming a central pillar of industrial IoT strategies. Manufacturers and utilities are deploying digital twins to simulate equipment behavior, optimize production schedules, and predict failures before they occur. Adoption is particularly strong in automotive, aerospace, and process industries.

2. Convergence of AI and Industrial IoT (AIoT)

The fusion of AI with industrial IoT infrastructure is enabling autonomous decision-making, self-optimizing production lines, and intelligent quality control. AI algorithms trained on sensor and process data allow systems to identify anomalies, recommend corrective actions, and adapt to changing conditions without human intervention.

3. Private 5G Networks for Industrial Environments

Industrial enterprises are increasingly deploying private 5G networks to support massive machine-type communication, ultra-reliable low-latency connections, and dense sensor deployments on factory floors and large-scale industrial sites. Private 5G offers deterministic performance, enhanced security, and greater control over network slicing compared to shared public networks.

4. OT/IT Convergence and Unified Data Architectures

The gradual convergence of OT and IT systems is enabling a unified data architecture that connects shopfloor sensors with enterprise applications, ERP systems, and supply chain platforms. This integration unlocks real-time operational intelligence and supports more agile and responsive industrial decision-making.

5. Industrial IoT-Enabled Predictive Quality and Zero-Defect Manufacturing

Real-time monitoring of production parameters, combined with machine learning (ML)-based defect detection, is enabling manufacturers to move from reactive quality inspection to predictive quality management. Connected vision systems, inline sensors, and AI models are identifying process deviations before defective parts are produced, reducing scrap rates and improving yield across high-precision manufacturing operations.

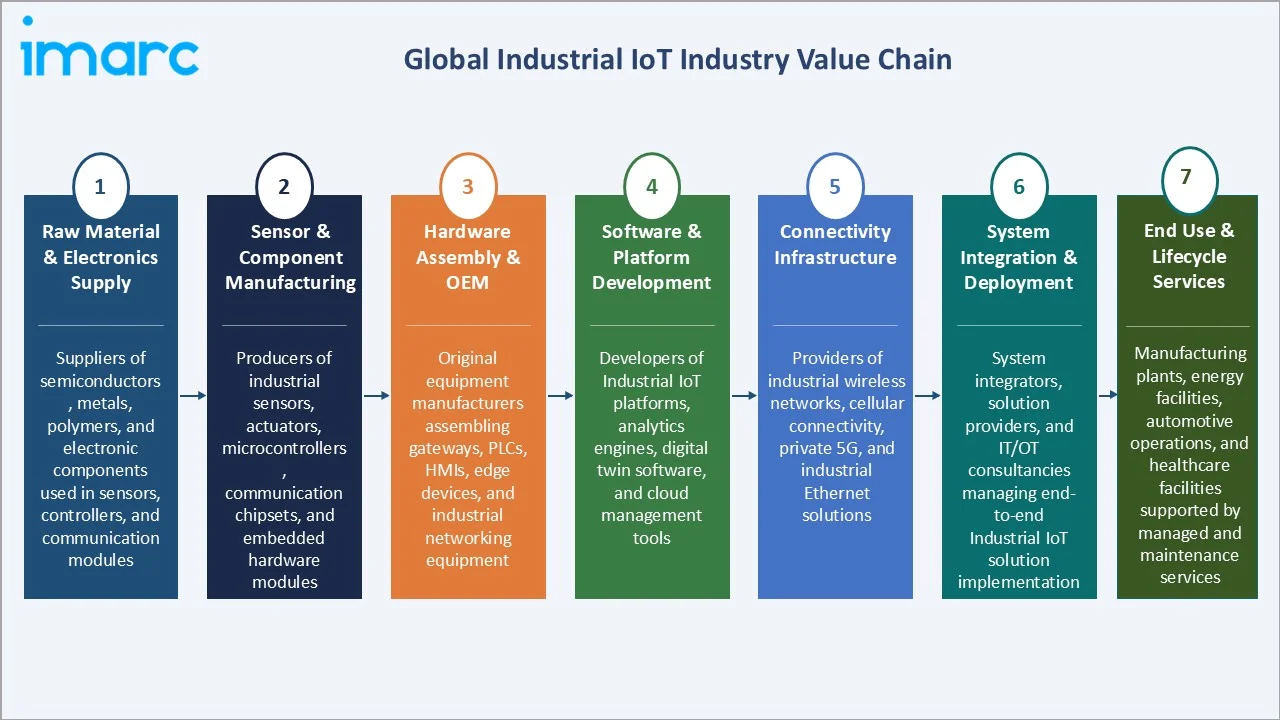

Industry Value Chain Analysis

The industrial IoT value chain spans seven stages, from raw material and component supply through end use deployment and lifecycle services. Platform software and system integration capture the highest value-add, while device manufacturing and connectivity provision form the foundational infrastructure layer.

|

Stage |

Key Players / Examples |

|

Raw Material & Electronics Supply |

Suppliers of semiconductors, metals, polymers, and electronic components used in sensors, controllers, and communication modules |

|

Sensor & Component Manufacturing |

Producers of industrial sensors, actuators, microcontrollers, communication chipsets, and embedded hardware modules |

|

Hardware Assembly & OEM |

Original equipment manufacturers assembling gateways, PLCs, HMIs, edge devices, and industrial networking equipment |

|

Software & Platform Development |

Developers of Industrial IoT platforms, analytics engines, digital twin software, and cloud management tools |

|

Connectivity Infrastructure |

Providers of industrial wireless networks, cellular connectivity, private 5G, and industrial Ethernet solutions |

|

System Integration & Deployment |

System integrators, solution providers, and IT/OT consultancies managing end-to-end Industrial IoT solution implementation |

|

End Use & Lifecycle Services |

Manufacturing plants, energy facilities, automotive operations, and healthcare facilities supported by managed and maintenance services |

Integrated solution providers that can deliver end-to-end Industrial IoT architecture hold a structural advantage over point-product suppliers. Cybersecurity and compliance capabilities are increasingly viewed as must-have competencies at every stage of the chain.

Technology Landscape in the Industrial IoT Industry

Sensor and Edge Device Innovation

Advances in MEMS-based sensors, low-power microcontrollers, and ruggedized industrial hardware are expanding the range of measurable parameters and deployment environments for Industrial IoT systems. Smart sensors with onboard processing capabilities reduce data transmission loads and enable real-time local decision-making at the device level.

Cloud and Edge Computing Platforms

Industrial cloud platforms provide scalable data ingestion, storage, and analytics capabilities for large Industrial IoT deployments. Complementary edge computing solutions process latency-sensitive data locally, reducing round-trip delays and enabling time-critical industrial control applications.

Connectivity and Industrial Networking

A diverse connectivity landscape, spanning industrial Ethernet, Wi-Fi 6, Bluetooth 5.0, LoRaWAN, NB-IoT, and private 5G, supports the range of data-rate, range, and latency requirements across different Industrial IoT use cases. Wireless technology adoption is accelerating as industrial-grade performance and reliability benchmarks are met.

Cybersecurity and Industrial Data Governance

Zero-trust security architectures, hardware-based root-of-trust, encrypted device communication, and AI-powered anomaly detection are becoming standard components of Industrial IoT security stacks. Regulatory compliance requirements are driving systematic adoption of security-by-design principles across Industrial IoT deployments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

41.8% |

2025 |

|

End-User |

Manufacturing |

36.0% |

2025 |

|

Region |

Europe |

32.0% |

2025 |

By Component

Hardware commands a 41.8% majority share in 2025, driven by the extensive physical deployment of industrial sensors, PLCs, edge gateways, HMIs, and industrial networking equipment. Nearly every Industrial IoT deployment requires a physical device layer, making hardware the foundational and highest-volume component category.

To access detailed market analysis, Request Sample

Software follows at 27.6%, supported by growing enterprise demand for Industrial IoT platforms, digital twin applications, SCADA modernization, and AI-powered analytics tools. The software segment is the fastest-growing component category, as enterprises move from hardware-centric deployments toward platform-driven intelligence.

By End-User

Manufacturing dominates with a 36.0% share in 2025, supported by the broad adoption of smart factory programs, real-time production monitoring, predictive maintenance platforms, and Industry 4.0 investments across discrete and process manufacturing industries globally.

Energy and utilities account for 22.5%, driven by grid modernization, smart metering, remote pipeline and substation monitoring, and demand response management systems.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

32.0% |

Advanced industrial base, strong manufacturing automation, and significant government investment in smart factory initiatives |

|

North America |

27.5% |

High adoption of Industry 4.0 technologies, strong IoT infrastructure, and large-scale manufacturing and energy sectors |

|

Asia-Pacific |

25.0% |

Rapid industrialization, expanding manufacturing output, growing smart factory deployments, and rising government support for digital transformation |

|

Latin America |

8.0% |

Growing industrial automation adoption, expanding energy and mining sectors, and increasing investment in connected infrastructure |

|

Middle East and Africa |

7.5% |

Rising oil and gas sector digitalization, gradual industrial modernization, and growing smart city and utility programs |

Europe at 32.0% in 2025 leads the market, anchored by its advanced manufacturing base in Germany, France, and Scandinavia, strong government support for digital industry programs, and mature adoption of Industry 4.0 frameworks.

North America at 27.5% is the second-largest region, driven by strong Industrial IoT adoption in automotive, aerospace, oil and gas, and large-scale manufacturing operations. High levels of enterprise IT investment, a robust cloud infrastructure ecosystem, and widespread cybersecurity maturity support continued growth across the United States and Canada.

Competitive Landscape

The industrial IoT market is moderately concentrated, with a small group of global technology leaders competing on platform breadth, integration capability, and vertical industry expertise, alongside a fragmented mid-tier of specialized hardware vendors, niche software providers, and regional system integrators. Competitive moats are built on installed customer bases, proprietary data networks, ecosystem partnerships, and cybersecurity credentials.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Siemens |

SIMATIC |

Leader |

Industrial automation, digital twin, and edge-to-cloud Industrial IoT platform leadership |

|

Cisco Systems, Inc. |

Cisco Industrial IoT |

Leader |

Industrial networking, OT/IT cybersecurity, and scalable Industrial IoT connectivity infrastructure |

|

Rockwell Automation |

FactoryTalk |

Challenger |

Smart manufacturing, industrial software, and integrated OT/IT solutions |

|

ABB |

ABB Ability Genix |

Challenger |

Electrification, process automation, and AI-driven digital solutions across manufacturing, energy, and infrastructure verticals |

|

PTC |

Vuforia |

Challenger |

AR-enabled industrial operations, product lifecycle management, and digital manufacturing |

Key players in the market include Siemens, Cisco Systems, Inc., Rockwell Automation, ABB, and PTC, among others.

Key Company Profiles

Siemens

Siemens is a global technology company with a comprehensive portfolio spanning industrial automation, digitalization, and smart infrastructure. The company plays a significant role in the Industrial IoT market through its connected industrial platforms, edge computing solutions, and data-driven automation technologies.

- Product Portfolio: A broad industrial technology portfolio encompassing the SIMATIC automation platform, digital twin solutions, and industrial edge computing products.

- Recent Development: In March 2025, Siemens revealed an expanded partnership with Microsoft regarding Siemens Xcelerator, the open digital business platform by Siemens, to ease the integration of IT and OT for corporate clients. Combining Siemens Industrial Edge with Microsoft Azure IoT Operations offers customers complementary solutions that facilitate an uninterrupted transfer of data from production lines to the edge and then to the cloud.

- Strategic Focus: End-to-end industrial digitalization through automation hardware, digital twin technology, and an open cloud-based industrial IoT platform ecosystem.

Cisco Systems, Inc.

Cisco Systems, Inc. is a global leader in networking and cybersecurity solutions with a significant presence in industrial IoT through its industrial networking hardware and OT security platforms, serving the manufacturing, energy, transportation, and public sector markets worldwide.

- Product Portfolio: Industrial networking switches, routers, and wireless access points for harsh environments.

- Recent Development: Cisco Systems, Inc. continues to actively invest in its industrial IoT portfolio, with ongoing product updates across industrial switching, OT security, and edge intelligence to support AI-ready industrial network deployments.

- Strategic Focus: Secure industrial connectivity, OT/IT network convergence, and scalable industrial IoT infrastructure through ruggedized networking hardware and OT cybersecurity solutions.

Rockwell Automation

Rockwell Automation is a leading provider of industrial automation and digital transformation solutions. Its integrated approach combines control systems, software, and industrial IoT capabilities to help enterprises improve productivity, operational resilience, and manufacturing efficiency.

- Product Portfolio: The FactoryTalk suite of industrial software, including analytics, MES, and remote monitoring.

- Recent Development: Rockwell Automation continues to invest in expanding its FactoryTalk software portfolio and smart manufacturing capabilities, integrating AI and cloud analytics tools to support digital transformation initiatives for industrial manufacturers.

- Strategic Focus: Smart manufacturing, OT/IT convergence, and integrated industrial software and automation solutions for process and discrete manufacturing industries.

Market Concentration Analysis

The industrial IoT market is moderately concentrated, with a small group of global technology leaders, including Siemens, Cisco Systems, Inc., Rockwell Automation, ABB, and PTC, holding a meaningful combined share of the platform, hardware, and services segments. A large and fragmented base of specialized hardware vendors, niche software providers, and regional system integrators competes for the balance of the market.

Barriers to competitive entry are significant and multi-layered. Building an enterprise-grade Industrial IoT platform requires sustained investment in cloud infrastructure, cybersecurity, protocol integration, and vertical industry expertise. Deep customer relationships, large installed bases of automation hardware, and established service organizations create powerful switching costs that reinforce the competitive position of established leaders.

Consolidation in the market is progressing through strategic acquisitions, technology partnerships, and ecosystem-building efforts. Major players are acquiring complementary capabilities in AI, digital twin software, edge computing, and industrial cybersecurity to offer more integrated solutions. Scale advantages in software development, global support infrastructure, and industry certifications further reinforce the position of established full-platform players.

Investment & Growth Opportunities

Fastest-Growing Segments

Software and services are expected to grow faster than the overall 12.18% market CAGR through 2034, driven by platform subscription models, managed Industrial IoT services, and enterprise demand for AI-powered analytics and digital twin applications. Connectivity is also a high-growth category as private 5G, industrial wireless, and LPWAN deployment scales rapidly across industrial environments.

Emerging Markets

Asia-Pacific is the highest-growth region through 2034, with China's manufacturing modernization, India's expanding industrial base, and ASEAN smart factory programs all driving accelerating Industrial IoT adoption. Latin America and the Middle East and Africa also represent meaningful incremental growth opportunities as industrial digitalization programs gain momentum in both regions.

Venture & Investment Trends

Investment activity in the industrial IoT space is concentrated in AI-powered analytics platforms, industrial cybersecurity, private 5G networks, digital twin software, and edge computing infrastructure. Sustainability-focused Industrial IoT applications, including carbon monitoring, energy optimization, and predictive environmental compliance tools, are attracting growing investor interest as industrial operators face increasing regulatory pressure on emissions and resource efficiency.

Future Market Outlook (2026-2034)

The industrial IoT market is forecast to expand from USD 325.7 Billion in 2025 to USD 944.8 Billion by 2034 at a CAGR of 12.18%, adding over USD 619 Billion in incremental market value over the forecast period.

Four structural forces will shape the industrial IoT market through 2034: the continued rollout of Industry 4.0 and smart manufacturing programs across developed and emerging economies; the maturation and convergence of AI, edge computing, and 5G connectivity into integrated industrial intelligence platforms; the accelerating OT/IT convergence driving unified operational data architectures; and the increasing prioritization of industrial cybersecurity as a mission-critical capability.

By 2034, the software and services segments are expected to account for a larger combined share of the market, reflecting the industry's shift from hardware-centric to platform-driven Industrial IoT architectures. Mature markets in Europe and North America will continue to be driven by technology refresh and platform expansion, while Asia-Pacific will provide the strongest incremental volume growth.

Research Methodology

Primary Research

Primary research included structured interviews and consultations with industrial technology vendors, Industrial IoT platform providers, system integrators, enterprise end users, and industry subject-matter experts, validating market sizing, segmentation analysis, regional dynamics, and competitive positioning across the forecast period.

Secondary Research

Secondary sources included company annual reports, investor presentations, press releases, government industrial digitalization program publications, industry association reports, trade publications covering industrial automation and IoT, patent filings, and regulatory documentation from relevant standards bodies.

Forecasting Models

Market forecasts were developed using a combination of top-down and bottom-up modeling, incorporating Industrial IoT device shipment data, platform revenue trends, industry capital expenditure patterns, and macroeconomic growth indicators. Scenario analysis addressed key risk factors including cybersecurity incidents, technology adoption pace, and macro-industrial investment cycles.

Industrial IoT Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Industrial IoT Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software, Services, Connectivity |

| End Users Covered | Manufacturing, Energy and Utilities, Automotive and Transportation, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Siemens, Cisco Systems, Inc., Rockwell Automation, ABB, PTC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, industrial IoT market forecasts, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the industrial IoT market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the industrial IoT industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Industrial IoT Market Report

The industrial IoT market was valued at USD 325.7 Billion in 2025, driven by accelerating adoption of connected devices, edge computing, and AI-powered analytics across manufacturing, energy, and transportation sectors.

The market is projected to grow at a 12.18% CAGR from 2026 to 2034, reaching USD 944.8 Billion, fueled by Industry 4.0 programs, smart factory investments, and expanding Industrial IoT platform adoption.

Hardware leads at 41.8% in 2025, reflecting the foundational role of sensors, gateways, PLCs, and edge devices as the primary data-capture and control layer across Industrial IoT deployments.

Manufacturing dominates at 36.0% in 2025, supported by smart factory programs, real-time production monitoring, and predictive maintenance platforms across discrete and process manufacturing industries.

Europe leads with a 32.0% share in 2025, anchored by an advanced industrial base, strong Industry 4.0 adoption, and robust government investment in manufacturing digitalization across the region.

Leading players include Siemens, Cisco Systems, Inc., Rockwell Automation, ABB, and PTC, among others.

Growth is driven by Industry 4.0 adoption, rising demand for predictive maintenance, edge AI integration, expanding 5G connectivity, and increasing enterprise investment in digital twin and smart manufacturing platforms.

High implementation costs, cybersecurity risks, legacy infrastructure integration challenges, interoperability gaps across industrial protocols, and a shortage of skilled OT/IT professionals constrain deployment pace.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade