Inflight Catering Market Size, Share, Trends and Forecast by Food Type, Flight Service Type, Aircraft Seating Class, and Region, 2026-2034

Inflight Catering Market Size, Share, Trends & Forecast (2026-2034)

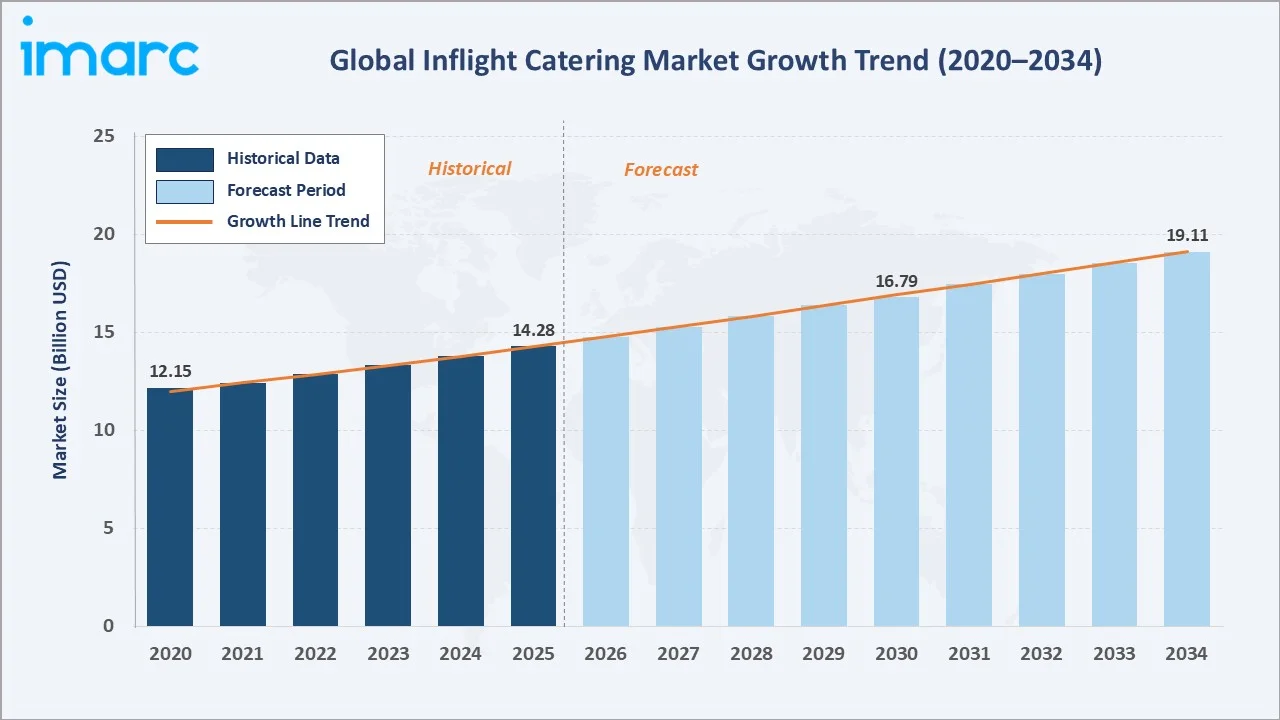

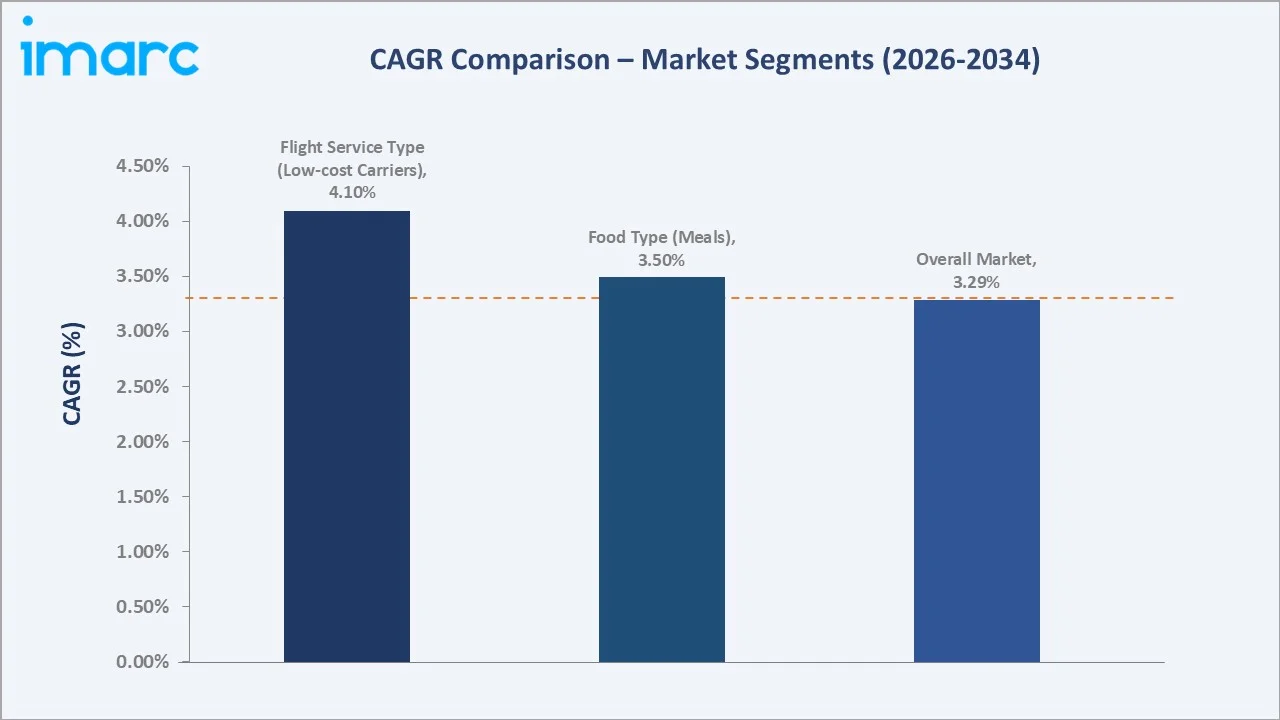

The global inflight catering market reached USD 14.28 Billion in 2025 and is projected to reach USD 19.11 Billion by 2034, growing at a CAGR of 3.29% during 2026-2034. The market is driven by the accelerating recovery of global air travel, rising passenger expectations for quality onboard dining, and the growing penetration of low-cost carriers expanding meal service offerings to drive competitive differentiation.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.28 Billion |

|

Forecast Market Size (2034) |

USD 19.11 Billion |

|

CAGR (2026-2034) |

3.29% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (31.6% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

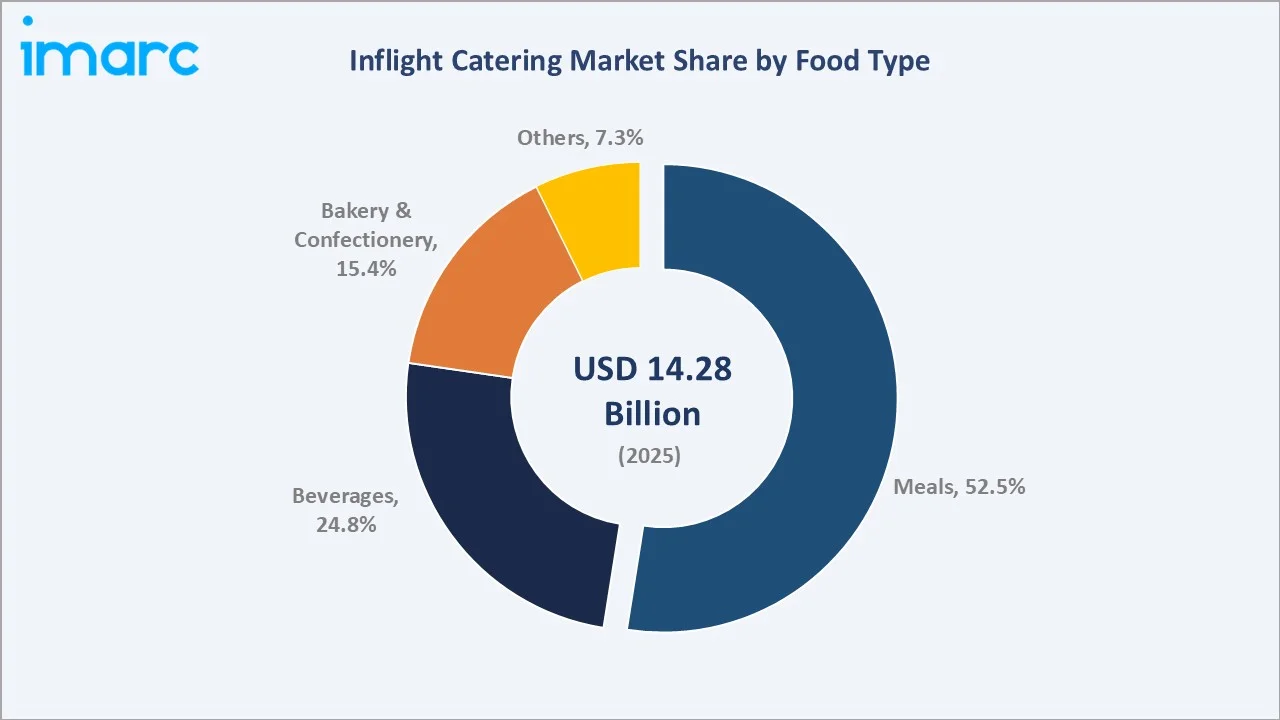

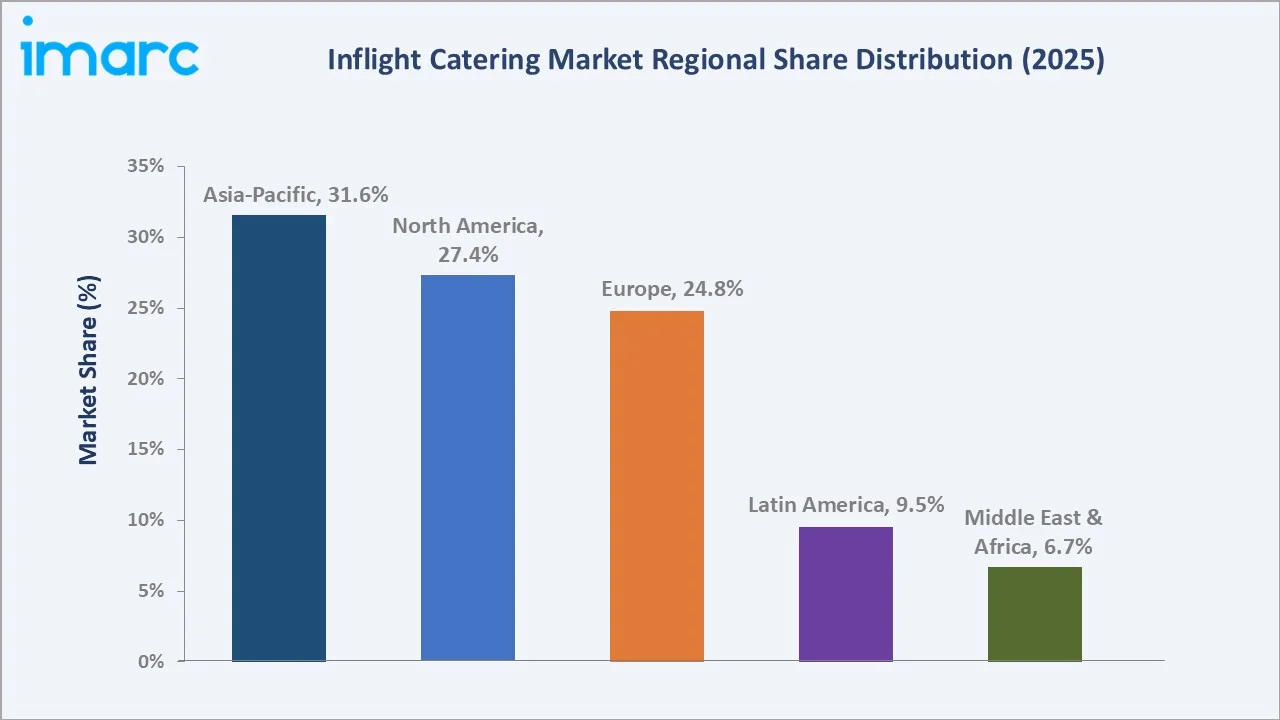

Asia-Pacific leads all regions with a 31.6% share in 2025, while the meals segment commands the largest share within the food type category at 52.5%. The inflight catering market growth is further supported by advancements in cold chain logistics, AI-driven food waste reduction, and the proliferation of customized dietary options catering to a globally diverse passenger base.

To get more information on this market, Request Sample

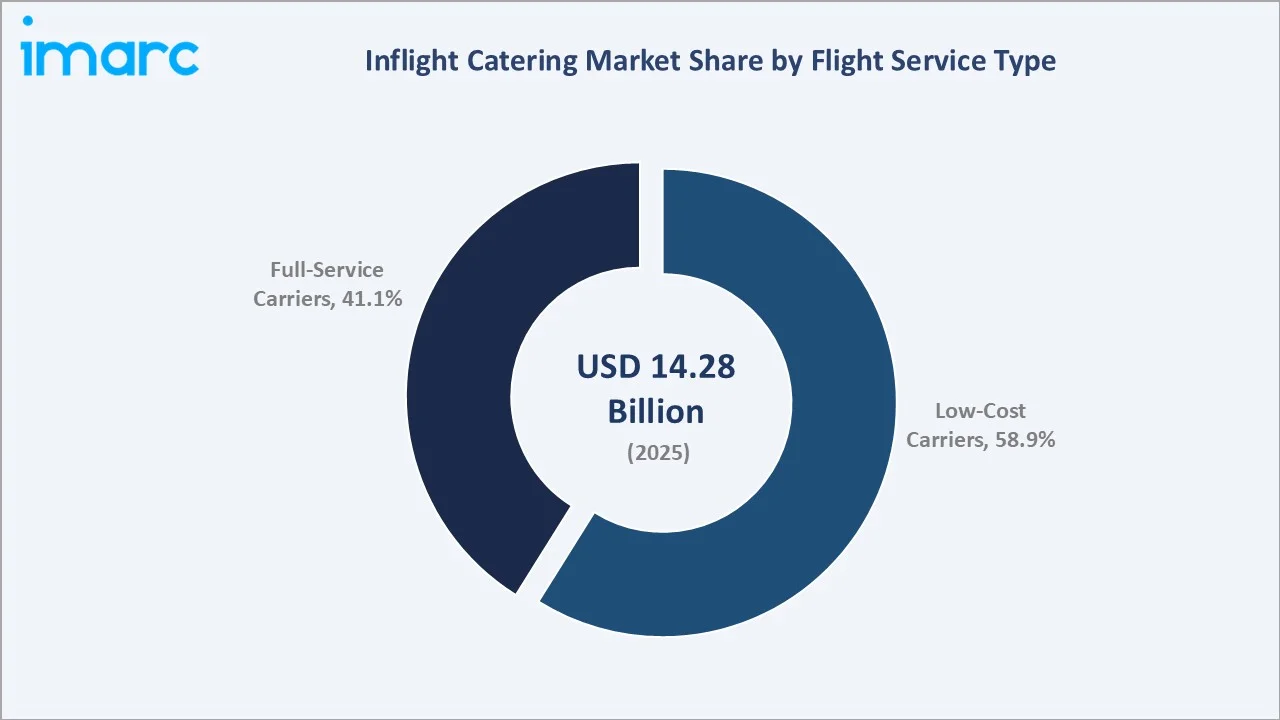

Low-cost carriers represent 58.9% of the market, reflecting their aggressive expansion of paid meal service programs. Inflight catering companies are increasingly investing in sustainable packaging, local ingredient sourcing, and AI-powered meal forecasting systems to improve cost efficiency and reduce food waste.

Executive Summary

The global inflight catering market is on a sustained expansion trajectory, supported by the recovery and growth of commercial aviation, rising per-capita income in emerging economies, and the increasing role of onboard dining as a passenger loyalty driver. The market reached USD 14.28 Billion in 2025 and is forecast to reach USD 19.11 Billion by 2034, reflecting a healthy CAGR of 3.29% across the forecast period.

Asia-Pacific leads globally, accounting for 31.6% of revenue in 2025, driven by exponential growth in passenger traffic across China, India, Indonesia, and Vietnam. North America contributes 27.4%, sustained by major airline networks and a strong premium cabin segment. Europe follows at 24.8%, with a focus on sustainability and gourmet dining initiatives.

Meals dominate the food type category at 52.5% in 2025, while low-cost carriers, now 58.9% of the market, continue to monetize onboard catering as an ancillary revenue channel. Leading operators, including gategroup, LSG Group, SATS Ltd., The Emirates Group, and DO & CO Aktiengesellschaft, continue to invest in digital food management, automation, and eco-compliant packaging systems.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Food Type) |

Meals – 52.5% share (2025) |

|

Largest Segment (Flight Service) |

Low-Cost Carriers – 58.9% (2025) |

|

Leading Region |

Asia-Pacific – 31.6% share (2025) |

|

Fastest Growing Region |

Asia-Pacific (air travel boom + fleet expansion) |

|

Top Companies |

gategroup, LSG Group, SATS Ltd., The Emirates Group, and DO & CO Aktiengesellschaft |

Key Analytical Observations:

- Meals account for 52.5% of the inflight catering market in 2025, preferred across all cabin classes due to passenger demand for cultural, dietary, and gourmet meal variety on medium and long-haul flights.

- Low-cost carriers represent 58.9% of the market in 2025, as airlines such as IndiGo, Ryanair, and AirAsia aggressively monetize onboard food as a key ancillary revenue source.

- Asia-Pacific holds 31.6% of global market revenue in 2025, led by China, India, and Southeast Asian markets, where passenger traffic is projected to double by the mid-2030s.

- Sustainable packaging and biodegradable meal containers are gaining rapid adoption, as 50% of cargo customers consider waste reduction in the supply chain a top priority, while over a third prioritize access to sustainable packaging options, according to the IATA Shipper Survey 2022.

- Inflight catering market trends indicate growing demand for AI-based meal forecasting, digital pre-ordering, and real-time cold chain monitoring, with airlines using customized AI platforms have reported waste reductions of 15 to 35 percent in the first year of implementation.

Global Inflight Catering Market Overview

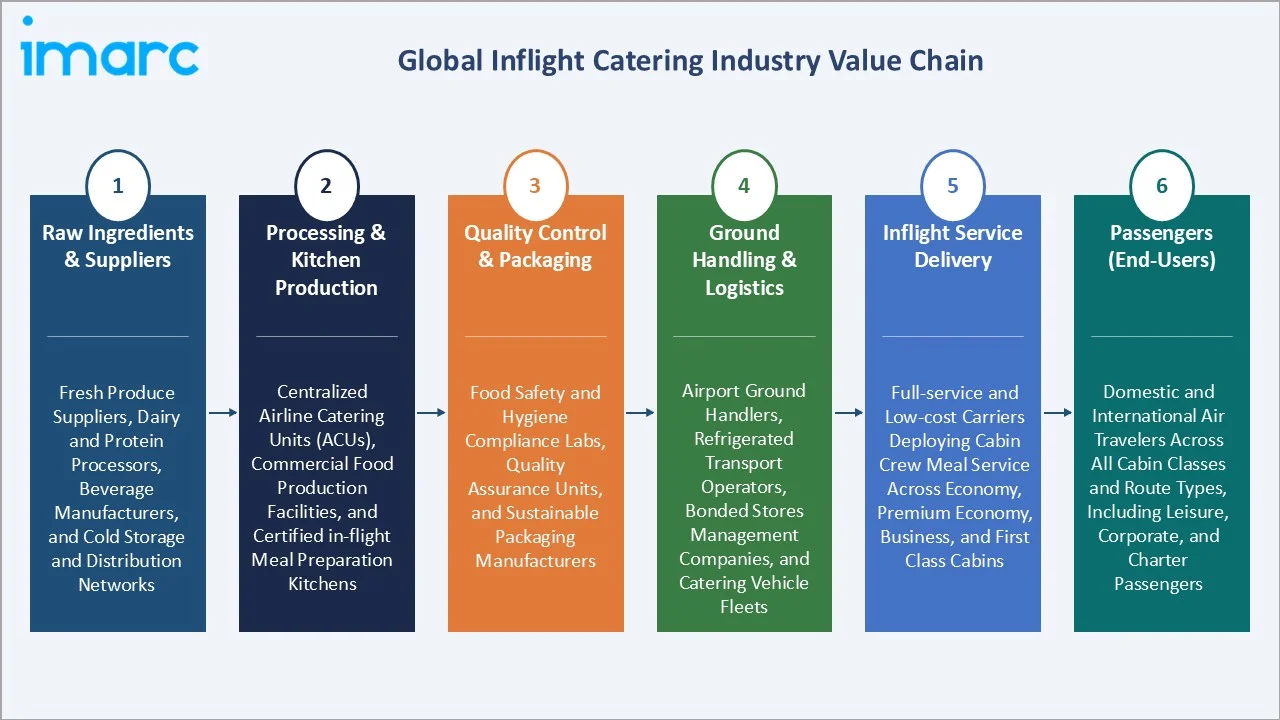

Inflight catering refers to the preparation, packaging, and delivery of food and beverages served to airline passengers during flight operations. Originating as a service differentiator for premium carriers in the mid-20th century, the sector has evolved into a sophisticated, logistics-intensive industry encompassing meal design, cold chain management, regulatory compliance, and waste reduction. The market ecosystem comprises raw food suppliers, centralized production kitchens, airline catering units (ACUs), ground handling logistics companies, and the airlines themselves as end-service deployers.

Macroeconomic growth in air passenger numbers, driven by expanding middle-class populations in Asia, Africa, and Latin America, is the primary catalyst for the inflight catering market forecast expansion. For 2026, the International Air Transport Association (IATA) Sustainability and Economics report projects a 4.9% year-on-year growth in passenger traffic (measured in RPK), driven by a 7.3% expansion in the Asia Pacific region, which is expected to directly increase catering meal volumes.

Market Dynamics

To evaluate market opportunities, Request Sample

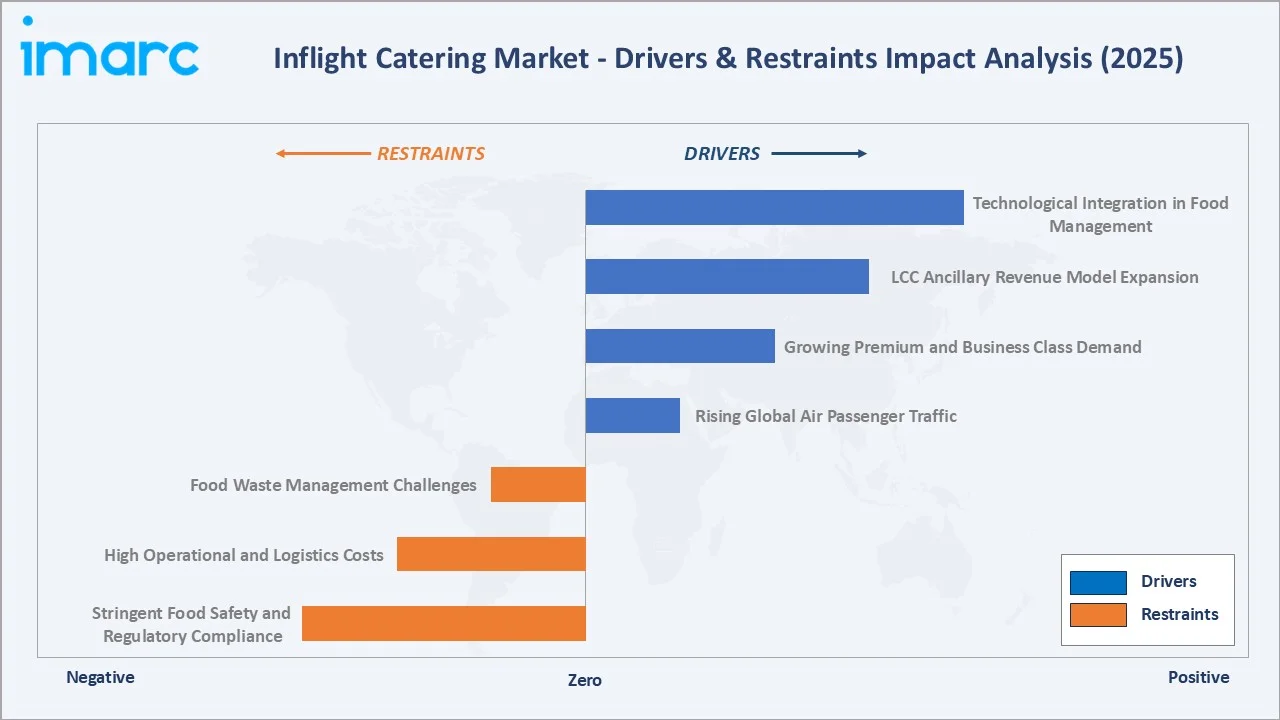

Market Drivers

- Rising Global Air Passenger Traffic: The IATA reported that as of the year-to-date (YTD) period ending October 2025, global passenger traffic has risen by 5.3% year-on-year, directly expanding the addressable volume for inflight meal services. Airlines across Asia-Pacific and the Middle East are adding new routes and increasing flight frequencies, creating sustained demand for catering capacity.

- Growing Premium and Business Class Demand: Rising corporate travel expenditure and affluent leisure traveler preferences are driving higher per-meal revenue opportunities. Meal costs can range from USD 60 to USD 80 per business class passenger, compared to USD 10 to USD 30 in economy, generating disproportionately high revenue for catering operators on long-haul routes.

- LCC Ancillary Revenue Model Expansion: Low-cost carriers are increasingly treating inflight catering as a profit center rather than a cost item. Pre-ordered meal programs, onboard retail menus, and airline brand food partnerships are expanding LCC catering revenues, with the segment contributing 58.9% of the global inflight catering market share in 2025.

- Technological Integration in Food Management: AI-based meal load optimization, RFID-enabled inventory tracking, and smart cold chain systems are improving catering efficiency and reducing waste. Airbus also noted that the Smart Catering platform could deliver double-digit reductions in preventable waste related to onboard food and beverage transportation.

Market Restraints

- Stringent Food Safety and Regulatory Compliance: Inflight food production must comply with HACCP, ISO 22000, and country-specific aviation food safety standards, increasing compliance costs for catering operators by an estimated 12–18% compared to conventional food service.

- High Operational and Logistics Costs: Centralized production kitchen infrastructure, specialized refrigerated transport fleets, and airport access fees represent significant fixed and variable cost burdens. Jet fuel price volatility indirectly impacts airline catering budgets, with carriers cutting catering costs during high-fuel-cost periods.

- Food Waste Management Challenges: The IATA and the Aviation Sustainability Forum (ASF) estimate that the global airline industry produces approximately 3.6 million tons of cabin and catering waste annually, based on data from 2024–2025, creating both cost and ESG compliance pressures.

Market Opportunities

- Expansion in Emerging Aviation Markets: The Indian government has set a target to develop 50 additional airports over the next five years and connect 120 new destinations within the next ten years. These regions offer greenfield investment opportunities for inflight catering operators, particularly around new international hub airports in India, Indonesia, and Nigeria.

- Sustainable Packaging and Eco-Catering Innovation: Airlines committing to net-zero carbon targets are partnering with catering operators to implement biodegradable packaging, locally sourced ingredients, and plant-based meal programs. Premium eco-catering is projected to represent a USD 1.8 billion market segment by 2030, driven by ESG procurement mandates among major carriers.

Market Challenges

- Supply Chain Disruptions: Ingredient price inflation, logistics bottlenecks, and geopolitical disruptions in key food-producing regions have materially increased raw material costs for catering operators. The post-pandemic supply chain normalization remains incomplete in several regions, limiting production capacity predictability.

- Talent and Workforce Constraints: Inflight catering is a labor-intensive operation requiring skilled food preparation, quality control, and logistics personnel. Staff shortages in airport catering hubs across Europe and North America are limiting production scalability, particularly during peak travel seasons.

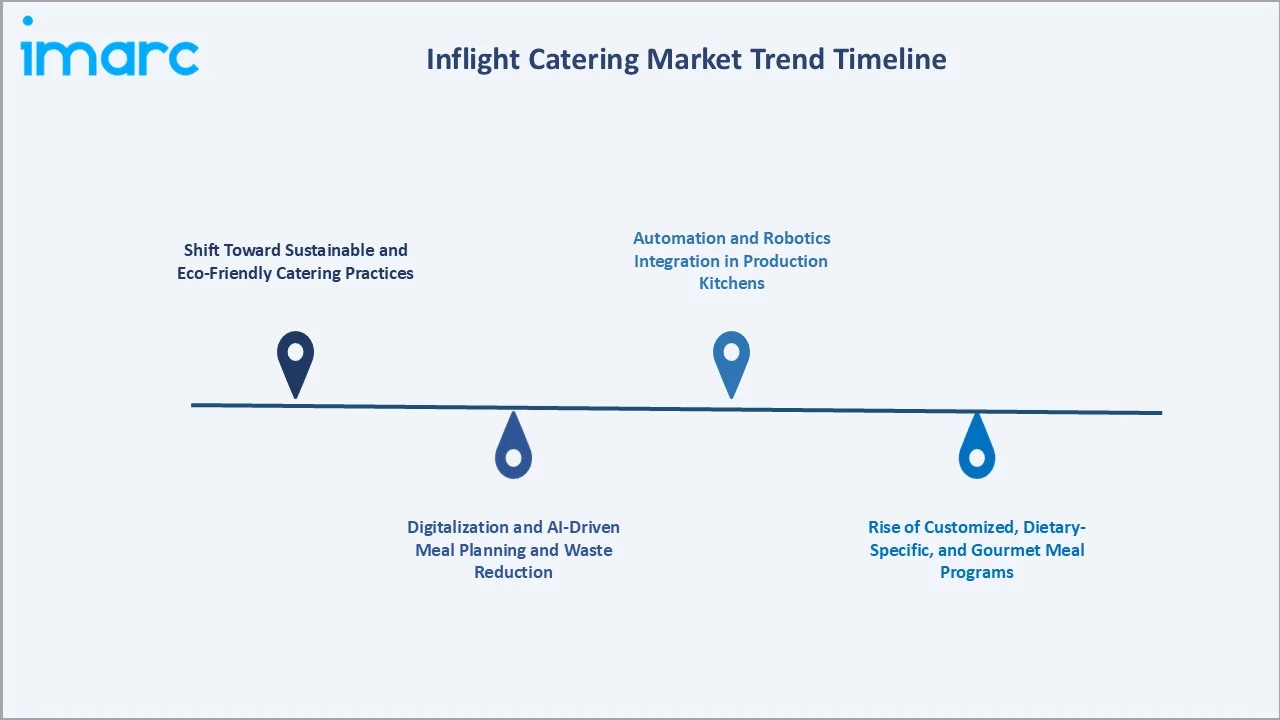

Emerging Market Trends

1. Shift Toward Sustainable and Eco-Friendly Catering Practices

According to IATA, many airlines are taking on the challenge of plastic pollution, with at least 40 airlines implementing single-use plastic product (SUPP) reduction and replacement programs, some of which began as early as 2018. Emirates Airlines saw a remarkable 40% rise in demand for plant-based cuisine, serving over 450,000 plant-based meals in 2023, a significant increase from the previous year.

2. Digitalization and AI-Driven Meal Planning and Waste Reduction

In 2025, Airbus tested its "Smart Catering" concept with Virgin Atlantic, using AI to track meal consumption and waste during live flights. After initial success in ground trials, the solution was deployed on A330 and A350 flights between London and key destinations for in-flight validation. In 2024, Virgin Atlantic said its Upper Class pre‑ordering system helped save about 310,000 entrées, roughly 86,000 kg of food, by reducing unnecessary meal preparation.

3. Rise of Customized, Dietary-Specific, and Gourmet Meal Programs

Emirates Airlines experienced a notable 40% rise in demand for plant-based cuisine, serving over 450,000 plant-based meals in 2023, a significant increase from the previous year. Regions such as Africa, Southeast Asia, and the Middle East have seen plant-based consumption outpace passenger volume growth. This shift is reflected in Emirates' extensive ‘vegan vault’ of over 300 chef-crafted recipes, showcasing a clear change in consumer preferences.

4. Automation and Robotics Integration in Production Kitchens

Robotic meal tray assembly lines, automated portioning machines, and computer vision-based quality inspection systems are being deployed by leading operators to improve throughput and consistency. Automation adoption is accelerating post-pandemic as the majority of Airline Catering Association members fast-tracked robotics investments to address social distancing requirements and labor availability constraints.

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Raw Ingredients & Suppliers |

Fresh produce suppliers, dairy and protein processors, beverage manufacturers, and cold storage and distribution networks |

|

Processing & Kitchen Production |

Centralized airline catering units (ACUs), commercial food production facilities, and certified in-flight meal preparation kitchens |

|

Quality Control & Packaging |

Food safety and hygiene compliance labs, quality assurance units, and sustainable packaging manufacturers |

|

Ground Handling & Logistics |

Airport ground handlers, refrigerated transport operators, bonded stores management companies, and catering vehicle fleets. |

|

Inflight Service Delivery |

Full-service and low-cost carriers deploying cabin crew meal service across economy, premium economy, business, and first class cabins |

|

Passengers (End-Users) |

Domestic and international air travelers across all cabin classes and route types, including leisure, corporate, and charter passengers |

Technology Landscape in the Inflight Catering Industry

AI and Predictive Meal Planning

Top technology providers, such as CHOOOSE and specialized aviation tech companies, are creating customized AI solutions that integrate with crew management, ground handling, and passenger data systems. Airlines that have adopted these platforms report waste reductions of 15 to 35 percent in the first year.

Advancing Data-Driven Catering Operations

In November 2025, Informatica partnered with Emirates Flight Catering (EKFC) to modernize its catering operations by deploying a cloud‑based Master Data Management (MDM) platform that unifies product, supplier, and customer data to boost efficiency and sustainability across its complex meal production processes. This collaboration enables EKFC to streamline stock control, improve supplier collaboration, and enhance traceability.

Digital Pre-Ordering and Passenger Experience Platforms

United Airlines introduced a new economy meal pre‑ordering system on longer flights (over ~1,190 miles), allowing passengers to select fresh entrees like burgers and sandwiches via the airline’s website or app from five days up to 24 hours before departure. This shift, which makes pre‑ordering the only way to buy fresh meals onboard in economy from March 1, aims to improve choice, streamline catering operations, and cut food waste by aligning meal preparation more closely with actual demand.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Food Type |

Meals |

52.5% |

2025 |

|

Flight Service Type |

Low-Cost Carriers |

58.9% |

2025 |

|

Aircraft Seating Class |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

31.6% |

2025 |

By Flight Service Type

Low-cost carriers dominate the inflight catering market with a 58.9% share in 2025. Their dominance reflects the structural transformation of global aviation, as carriers such as IndiGo, Ryanair, EasyJet, and AirAsia have turned onboard food and beverage into a high-margin ancillary revenue channel. LCCs sell pre-ordered and onboard food options at premium prices, generating per-passenger ancillary food revenues ranging from USD 8 to USD 35, depending on route length.

To access detailed market analysis, Request Sample

Full-service carriers hold a 41.1% share (2025), driven by their emphasis on complimentary multi-course meal services across all cabin classes. FSCs differentiate primarily through catering quality, with premium cabin meal programs serving as a key customer acquisition and retention tool. Airlines such as Singapore Airlines, Lufthansa, and Emirates deploy extensive resources toward fine-dining inflight programs, with per-seat catering budgets in first class exceeding USD 1,000 on select ultra-long-haul routes.

By Food Type

Meals lead the food type segment with a 52.5% share in 2025. Their dominance reflects the centrality of meal service to the inflight passenger experience on both medium and long-haul flights. Growing demand for special dietary meals, including halal, kosher, vegan, gluten-free, and diabetic-compliant options, is expanding the category’s addressable market and increasing average meal complexity and production costs.

Beverages account for 24.8% of the market in 2025, with alcoholic and premium non-alcoholic drink programs representing significant revenue for full-service carriers. Bakery and confectionery holds 15.4%, with packaged snack programs increasingly popular on short and medium-haul LCC routes.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

31.6% |

Air travel boom, fleet expansion, rising middle class |

|

North America |

27.4% |

Premium cabin demand, gourmet snack programs, and low-cost carrier growth |

|

Europe |

24.8% |

Sustainability mandates, premium dining programs, and business travel |

|

Latin America |

9.5% |

Rising aviation infrastructure, tourism growth, and new airline routes |

|

Middle East & Africa |

6.7% |

Hub airport expansion, premium long-haul catering, tourism |

Asia-Pacific’s market leadership (31.6%, 2025) reflects the region’s status as the world’s fastest-growing aviation market. China, India, Indonesia, Vietnam, and Thailand are collectively adding over 1,200 new commercial routes annually, driving proportional growth in inflight catering volumes. According to the Indian credit rating and research agency (ICRA), for FY2025(April 2024–March 2025), domestic air passenger traffic reached 1,653.8 lakh (165.38 million), marking a year-on-year growth of 7.6%, placing immense demand on airport-based catering infrastructure.

Competitive Landscape

The global inflight catering market exhibits a moderately consolidated structure. The top five operators, gategroup, LSG Group, SATS Ltd., The Emirates Group, and DO & CO Aktiengesellschaft, collectively hold approximately 45–52% of global market revenue in 2025.

|

Company |

Brand/ Platform/ Programs |

Market Position |

Core Strength |

|

gategroup |

gategourmet |

Market Leader |

World's largest independent inflight caterer; 300+ airline catering units across 60+ countries; AI Smart Kitchen initiative |

|

LSG Group |

LSG Sky Chefs |

Market Leader |

200+ customer service centers in 49 countries; ~550 million meals per year; Asia-Pacific expansion via acquisitions |

|

SATS Ltd. |

SATS |

Strong Challenger |

Asia-Pacific's leading aviation food solutions provider, Changi Airport hub, and WFS acquisition, strengthening global reach |

|

The Emirates Group |

Emirates Flight Catering |

Strong Challenger |

World's single largest inflight catering facility; 225,000+ meals/day at Dubai International Airport |

|

DO & CO Aktiengesellschaft |

DO & CO |

Challenger |

Premium gourmet specialist; first and business class focus; partnerships with top-tier international carriers |

The remaining market is served by regional specialists, airline-owned catering units, and boutique gourmet operators serving premium niche routes. Competitive differentiation is driven by operational scale, menu innovation capability, sustainability credentials, and technology integration in production management.

Key Company Profiles

gategroup

gategroup, headquartered in Glattbrugg, Switzerland, is the world’s largest independent provider of inflight catering services, operating from over 300 airline catering units in more than 68 countries.

- Product Portfolio: Full-spectrum catering services for economy, premium economy, business, and first class; retail-to-seat programs; special dietary meals; bonded store management.

- Recent Developments: In March 2026, gategroup announced an agreement to acquire a 75% stake in KLM Catering Services (KCS), forming a long-term strategic partnership with KLM Royal Dutch Airlines. The deal will redefine in-flight catering services for KLM at Amsterdam Airport Schiphol, with KLM retaining a 25% share.

- Strategic Focus: Digital transformation of production operations; sustainability certification across European units; Asia-Pacific capacity expansion.

LSG Group

LSG Group, headquartered in Neu-Isenburg, Germany, operates in 40+ countries with over 100+ customer service centers. The company serves more than 300 airlines globally and is among the largest catering operators by production volume, processing approximately 200 million meals per year.

- Product Portfolio: Airline meal production, cabin equipment management, onboard retail programs, and digital logistics solutions.

- Recent Developments: In April 2026, Bluspring Enterprises announced that Bluspring New Horizon Two agreed to acquire 100% of LSG Sky Chefs (India), marking its strategic entry into the aviation catering sector with an INR 129 crore deal. It gives it long‑term access to in‑flight catering facilities at Bengaluru Airport under a concession until 2039.

- Strategic Focus: Automation-led production efficiency; premium meal segment growth in Asia-Pacific; sustainable packaging compliance across EU operations.

SATS Ltd.

SATS Ltd., headquartered in Singapore, is the Asia-Pacific’s leading aviation food solutions and gateway services provider. Operating across 15+ countries with 200+ stations in the Asia-Pacific region, SATS serves over 60 airline partners from its centralized flight kitchen facilities at Changi Airport and other major hubs.

- Product Portfolio: Airline catering, inflight meal production, institutional food solutions, and perishables logistics.

- Recent Developments: In November 2025, SATS’ subsidiary TFK Corporation secured a three‑year inflight catering contract with Turkish Airlines, providing daily halal‑standard meal services for flights between Tokyo’s Narita and Haneda airports and Istanbul.

- Strategic Focus: Asia-Pacific market dominance; India market penetration; technology integration for digital pre-ordering and meal load optimization.

Market Concentration Analysis

The inflight catering market exhibits moderate-to-high concentration at the global level, with the top five operators accounting for approximately 45–52% of total revenue in 2025. However, significant fragmentation exists below the tier-one operators, particularly in regional and domestic airline catering in Asia, Latin America, and Africa, where airline-owned or government-affiliated catering units maintain strong positions.

Consolidation activity is accelerating, driven by the high capital requirements for airport catering facility investment, food safety certification costs, and the growing need for technology infrastructure investment. Between 2020 and 2024, six major M&A transactions reshaped the global catering competitive map, including SATS’ acquisition of WFS and various LSG Sky Chefs regional expansions.

Investment & Growth Opportunities

Fastest Growing Segments

Sustainable eco-catering (estimated CAGR of 5.8%), digital pre-ordering platforms (CAGR 7.2%), and AI-powered meal management systems (CAGR 8.5%) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable inflight catering sub-market of approximately USD 3.2 Billion by 2030.

Emerging Market Expansion

India, Indonesia, Vietnam, Nigeria, and Ethiopia collectively represent an incremental USD 2.1 Billion inflight catering opportunity by 2034, driven by airport infrastructure buildouts and rapid commercial aviation fleet expansion. Entry via joint ventures with national carriers, greenfield catering facility investments near new international airports, and alignment with government-backed aviation development programs are the preferred investment modalities for global operators.

Venture and Institutional Investment Trends

- Key investment themes include AI-based demand forecasting, robotics-enabled meal assembly systems, cold chain IoT platforms, and sustainable packaging material supply chains.

- Institutional investors and PE firms are increasingly targeting vertically integrated catering operators, consolidating kitchen production, logistics, onboard retail, and equipment management into unified platform companies.

- Strategic alliances between inflight caterers and airline loyalty program operators present a new monetization frontier for pre-order meal upselling and branded food partnerships.

Future Market Outlook (2026-2034)

The global inflight catering market is positioned for sustained, broad-based growth through 2034. From a base of USD 14.28 Billion in 2025, the market is projected to reach USD 19.11 Billion by 2034, representing total incremental value creation of approximately USD 4.83 Billion over the forecast decade, at a CAGR of 3.29%.

Three structural macro-themes underpin this trajectory: the global aviation passenger growth super-cycle; the premiumization of the passenger experience as airlines compete on service quality; and the digital transformation of catering production through AI, robotics, and IoT integration. Regulatory evolution will drive significant product and process innovation investment across the inflight catering value chain.

Operators that achieve scalable, technology-enabled, and sustainability-certified production capabilities by 2027 are well-positioned to capture a disproportionate share of new airline catering contract awards, particularly in Asia-Pacific and the Middle East, where fleet expansion is most aggressive. The inflight catering market forecast through 2034 strongly favors operators with diversified geographic footprints, premium meal capabilities, and demonstrated sustainability credentials.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including airline catering managers, procurement officers, ground handling specialists, airport authority representatives, and airline passenger experience teams across Asia-Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary research encompassed a systematic review of airline annual reports, IATA publications, national aviation authority databases, catering company corporate filings, industry publications (Aircraft Interiors International, AirlineTrends), and publicly available market intelligence.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating global passenger traffic growth indices, airline fleet expansion data, per-flight catering revenue benchmarks, and historical market evolution. A base-case CAGR of 3.29% reflects consensus analyst estimates validated against reported operator revenue growth rates.

Inflight Catering Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Food Types Covered | Meals, Bakery and Confectionary, Beverages, and Others |

| Flight Service Types Covered | Full-Service Carriers, Low-Cost Carriers |

| Aircraft Seating Classes Covered | Economy Class, Business Class, First Class |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | gategroup, LSG Group, SATS Ltd., The Emirates Group, DO & CO Aktiengesellschaft, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the inflight catering market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global inflight catering market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the inflight catering industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Inflight Catering Market Report

The global inflight catering market reached USD 14.28 Billion in 2025. It is projected to reach USD 19.11 Billion by 2034.

The inflight catering market is expected to grow at a CAGR of 3.29% during the forecast period from 2026 to 2034, supported by rising global air travel volumes and evolving passenger experience expectations.

Asia-Pacific leads the market with a 31.6% share in 2025, driven by exponential growth in commercial aviation across China, India, and Southeast Asia.

Meals dominate the food type segment with a 52.5% share in 2025, driven by rising passenger demand for quality, culturally adapted, and dietary-specific meal programs.

Low-cost carriers hold the largest share at 58.9% in 2025, reflecting their aggressive monetization of onboard food and beverage as a key ancillary revenue stream.

Key players include gategroup, LSG Group, SATS Ltd., The Emirates Group, and DO & CO Aktiengesellschaft, among others.

Key drivers include rising global air passenger traffic, growing premium cabin demand, LCC ancillary revenue program expansion, digitalization of food management systems, and increasing passenger preference for customized dietary meal options.

Key challenges include stringent food safety regulatory compliance, high operational and logistics costs, food waste management pressures, post-pandemic supply chain volatility, and workforce shortages at major airport catering hubs.

Expansion into emerging aviation markets such as India, Indonesia, and Sub-Saharan Africa, investment in AI and robotics-enabled kitchen automation, sustainable packaging supply chains, and digital pre-ordering platforms represent the highest-value growth opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)