Insomnia Market Size, Share, Trends and Forecast by Therapy Type, Drug Class, Distribution Channel, and Region, 2026-2034

Insomnia Market Size and Share:

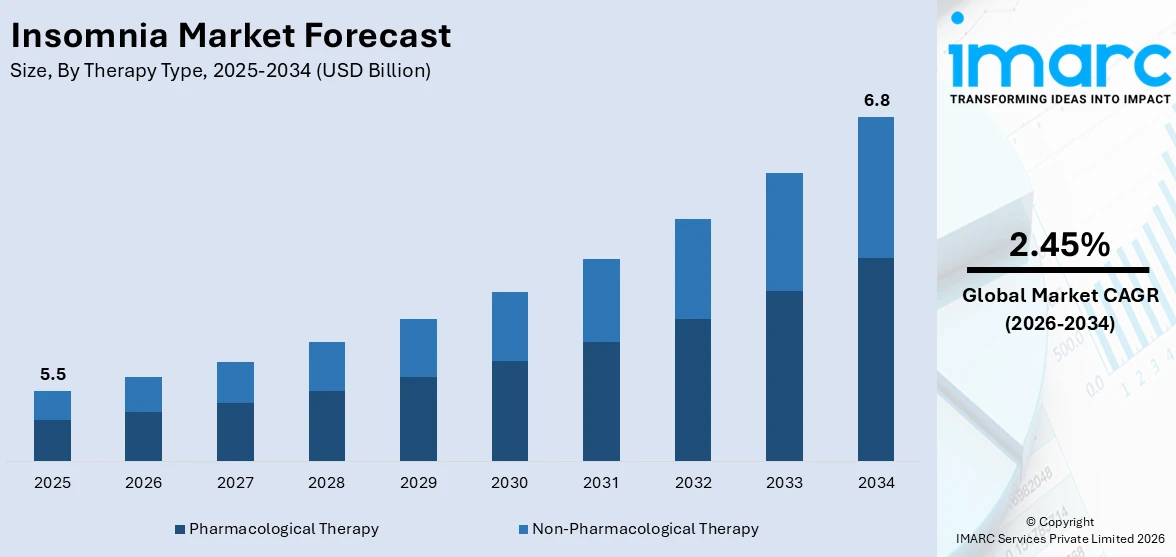

The global insomnia market size was valued at USD 5.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 6.8 Billion by 2034, exhibiting a CAGR of 2.45% during 2026-2034. North America currently dominates the market, holding a significant market share of over 36.4% in 2025. Increasing prevalence due to modern lifestyles and stress, advancements in diagnostic technologies enhancing accuracy, robust research into novel therapies, rising healthcare expenditures, integration of digital health solutions, strategic industry collaborations, and growing consumer preference for non-pharmacological treatments are some of the factors bolstering the market growth. In addition to this, advanced healthcare, high sleep disorder prevalence, and adoption of innovative treatments are further increasing the insomnia market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 5.5 Billion |

|

Market Forecast in 2034

|

USD 6.8 Billion |

| Market Growth Rate (2026-2034) | 2.45% |

The key drivers in the insomnia market are increasing prevalence of sleep disorders due to modern lifestyles, stress, and aging populations. Advances in diagnostic technologies improve accuracy while research into novel therapies is increasing the treatment options. Increasing healthcare expenditures and the adoption of digital health solutions including sleep-tracking apps and telemedicine are fueling growth in the market. For instance, in March 2024, Emma Up launched by Emma - The Sleep Company is an innovative AI sleep coaching app featuring sound-based sleep tracking. It offers personalized insights to tackle sleep issues addressing over 73% of users' desire for better sleep quality. Consumer demand for non-pharmacological treatments like cognitive behavioral therapy for insomnia and government initiatives are also creating a positive insomnia market outlook across the world.

To get more information on this market Request Sample

The key drivers in the United States insomnia market are the high prevalence of sleep disorders associated with stress, sedentary lifestyles and aging populations. Increased awareness of the importance of sleep health and its impact on overall well-being is driving demand for effective treatments. Advances in diagnostic tools and therapeutic options including digital health technologies like sleep apps and telemedicine further represent some of the key insomnia market trends in the country. For instance, in October 2024, SleepScore Labs launched Sleep.AI the first evidence-based AI platform for sleep health utilizing over 500 million hours of sleep data and insights from 230+ studies. Increasing non-pharmacological treatments especially cognitive behavioral therapy for insomnia are gaining momentum among consumers. Moreover, extensive research investments, increasing healthcare expenses and supportive insurance policies also fuel the U.S. market for insomnia.

Insomnia Market Trends:

Rising Prevalence of Stress, Anxiety, and Mental Health Disorders

The growing incidence of stress, anxiety, and mental health disorders is positively influencing the market. The findings from the American Psychiatric Association's yearly mental health survey for 2024 indicated that US adults experienced heightened anxiety. In 2024, 43% of adults reported feeling more anxious compared to 2023, an increase from 37% in 2023 and 32% in 2022. Modern lifestyles marked by work pressure, digital distractions, and social challenges have led to widespread sleep disturbances. Chronic stress affects hormonal balance and disrupts sleep-wake cycles, resulting in insomnia among both adults and adolescents. Moreover, anxiety and depression often coexist with sleep disorders, increasing the demand for medical interventions. The growing societal awareness around mental well-being has encouraged more individuals to seek professional help, boosting prescriptions for sleep medications and therapies. Pharmaceutical companies are developing safer, non-addictive drugs and cognitive behavioral treatments tailored for stress-related insomnia. As mental health challenges continue to escalate globally, the growing interconnection between psychological wellness and sleep health remains a central factor driving the market expansion.

Growing Aging Population and Higher Risk of Sleep Disorders

The expanding global aging population is significantly contributing to the growth of the insomnia market. As per the WHO, by the year 2030, one in every six individuals will be 60 years old or more across the globe. Older adults are more prone to sleep disturbances due to age-related physiological changes, chronic illnesses, and medication side effects. Conditions, such as arthritis, cardiovascular diseases, and neurological disorders, often interfere with normal sleep patterns. Additionally, melatonin production decreases with age, making it harder for elderly individuals to maintain regular sleep cycles. With longer life expectancy and rising healthcare awareness, more seniors are seeking medical assistance for sleep-related problems. This demographic shift is creating the growing demand for prescription medications, behavioral therapies, and natural sleep aids. Healthcare providers are focusing on holistic sleep management approaches tailored to elderly needs, making age-related sleep disorders one of the key factors driving the market forward.

Increasing Adoption of Digital Lifestyles and Screen Exposure

The growing dependence on digital devices and prolonged screen exposure is offering a favorable market outlook. As per industry reports, by Q3 2024, users globally aged 16 to 64 typically spent 6 hours and 38 minutes each day engaged with screens on different devices. The blue light released by smartphones, tablets, and computers inhibits melatonin secretion, disrupting natural sleep cycles and making it harder to fall asleep. Remote working trends, late-night entertainment, and social media usage have intensified this problem across all age groups. The constant connectivity and overstimulation also contribute to cognitive alertness, preventing adequate rest. As awareness about digital-induced sleep disruption is growing, consumers are turning to sleep aids, mobile applications, and therapies to improve rest quality. Pharmaceutical and wellness companies are addressing this modern lifestyle issue through melatonin-based supplements, behavioral therapies, and mindfulness programs. The continuous expansion of screen-driven lifestyles ensures steady demand for insomnia treatments across both clinical and consumer wellness markets.

Insomnia Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on the therapy type, drug class, and distribution channel.

Analysis by Therapy Type:

- Non-Pharmacological Therapy

- Hypnotherapy

- Cognitive Behavioral Therapy

- Medical Devices

- Others

- Pharmacological Therapy

- Prescription Sleep Aids

- Over-The-Counter Sleep Aids

The pharmacological therapy segment is driven by the increasing demand for effective treatments targeting insomnia's physiological mechanisms and symptomatology. Pharmaceutical innovations aimed at developing medications with improved efficacy and safety profiles play a crucial role in expanding this segment. Research into novel drug formulations and delivery methods, including sustained-release formulations and combination therapies, enhances treatment options. Moreover, the rising prevalence of insomnia globally, exacerbated by lifestyle changes and stressors, amplifies the need for pharmacological interventions that can efficiently address sleep disturbances. Strategic collaborations between pharmaceutical companies and research institutions accelerate drug development processes, driving market competitiveness. Regulatory approvals for new drugs and treatment modalities also stimulate segment growth by expanding market access and enhancing patient trust in therapeutic efficacy.

Analysis by Drug Class:

- Antidepressants

- Melatonin Antagonist

- Benzodiazepines

- Nonbenzodiazepines

- Orexin Antagonist

- Others

Benzodiazepines leads the market with around 28.9% of market share in 2025. The benzodiazepines segment is driven by the increasing demand for effective anxiolytics and sedatives across various medical and psychiatric conditions. Benzodiazepines are favored for their rapid onset of action and efficacy in managing anxiety disorders, insomnia, seizures, and muscle spasms, thereby sustaining their prominence in clinical practice. Moreover, the rising prevalence of anxiety disorders globally, compounded by lifestyle stressors and mental health awareness, fuels insomnia market growth. Additionally, the segment benefits from ongoing research and development efforts aimed at improving drug formulations to minimize side effects and enhance patient compliance. Regulatory approvals for new indications and formulations also bolster market expansion, ensuring broader accessibility and application in diverse healthcare settings. Furthermore, the aging population, particularly in developed regions, contributes significantly as older adults seek treatments for anxiety-related disorders and sleep disturbances.

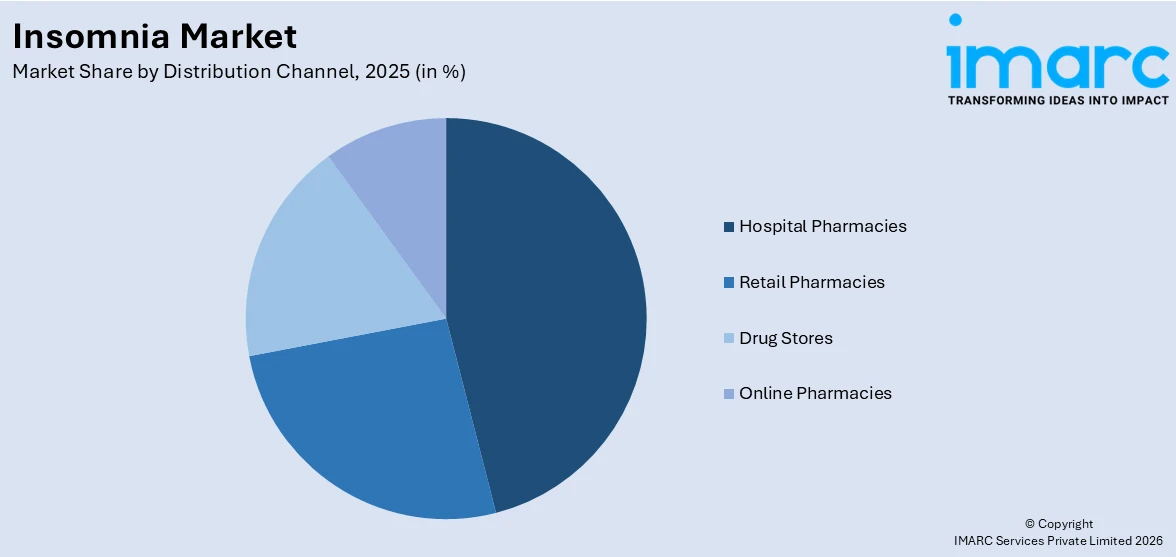

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Hospital Pharmacies

- Retail Pharmacies

- Drug Stores

- Online Pharmacies

The hospital pharmacies segment is driven by the increasing demand for specialized pharmaceutical services within healthcare facilities. These pharmacies play a crucial role in ensuring seamless medication management and distribution within hospitals, catering to inpatient and outpatient needs efficiently. Key drivers include the rising prevalence of chronic diseases requiring complex treatment regimens, which necessitate close coordination between healthcare providers and pharmacists. Additionally, advancements in hospital pharmacy automation and inventory management systems enhance operational efficiency and patient safety.

The retail pharmacies segment is driven by the increasing accessibility and convenience of healthcare services at local community settings. These pharmacies serve as accessible points of care (POC) for routine medication needs, preventive health screenings, and over-the-counter (OTC) products, catering directly to consumer demand. Key drivers include demographic trends such as aging populations requiring ongoing medication management and a shift towards self-care and wellness. Retail pharmacies also benefit from expanding healthcare insurance coverage and regulatory reforms promoting pharmacist-provided clinical services, enhancing their role in primary healthcare delivery.

The drug stores segment is driven by the increasing consumer preference for one-stop shopping experiences that combine pharmaceutical products with convenience goods. These stores offer a wide range of healthcare products, including prescription medications, over-the-counter treatments, and personal care items, appealing to consumers seeking convenience and affordability. Key drivers include strategic partnerships with healthcare providers and pharmaceutical manufacturers, which enhance product offerings and service delivery. Drug stores also benefit from location-based advantages in high-traffic areas and promotional strategies that promote health and wellness solutions.

The online pharmacies segment is driven by the increasing adoption of digital health solutions and e-commerce platforms, facilitating convenient access to medications and healthcare products. These pharmacies offer a diverse range of prescription drugs, over-the-counter medications, and health supplements, often at competitive prices and with home delivery options. Key drivers include the growing consumer demand for telemedicine services, which integrate online consultations with prescription fulfillment, enhancing accessibility and patient convenience. Online pharmacies also benefit from regulatory frameworks supporting virtual healthcare delivery and secure online transactions, ensuring patient safety and data privacy.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 36.4%. The North America regional market is driven by the increasing awareness and diagnosis of insomnia disorders, supported by robust healthcare infrastructure and diagnostic capabilities. The region's high prevalence of lifestyle-related factors such as stress, irregular work hours, and sedentary lifestyles contribute significantly to the rising incidence of sleep disorders. Moreover, the growing elderly population in North America, characterized by a higher susceptibility to insomnia, further propels insomnia market demand. Advances in medical research and technology within the region continuously enhance diagnostic accuracy and treatment efficacy, fostering innovation in therapeutic approaches. Additionally, the proactive regulatory environment and favourable reimbursement policies stimulate market growth by facilitating quicker approvals and broader patient access to treatment options. Collaborative efforts between healthcare providers, pharmaceutical companies, and research institutions drive the development of novel therapies and personalized medicine approaches tailored to address specific patient needs.

Key Regional Takeaways:

United States Insomnia Market Analysis

The United States holds 80.00% of the market share in North America. The United States insomnia market is driven by high stress exposure, demanding work schedules, and lifestyle habits that disrupt sleep cycles across various age groups. Rising mental health burdens, particularly anxiety disorders, occupational burnout, and mood instability, have significantly increased the number of individuals seeking treatment for chronic and acute insomnia. Widespread use of electronic devices, long hours on digital screens, and dependence on mobile-based entertainment late at night are major behavioral drivers, fueling sleep disruption. The country’s rapidly aging population is contributing strongly to the market expansion, as seniors frequently experience sleep fragmentation due to chronic illnesses, medication side effects, or neurocognitive decline. The US healthcare system’s emphasis on specialized sleep medicine is encouraging growth in sleep labs, polysomnography services, behavioral therapy programs, and telehealth platforms offering digital cognitive behavioral therapy for insomnia (CBT-I). In addition, increasing awareness campaigns around sleep hygiene, productivity loss due to sleep deprivation, and benefits of early intervention are boosting treatment uptake. The pharmaceutical sector plays a central role, supported by extensive research and development activities (R&D) for safer hypnotics, prolonged-release melatonin, orexin receptor antagonists, and non-addictive formulations tailored for long-term use. The health and wellness sector is also stimulating demand through wearable sleep trackers, app-based monitoring solutions, and nutraceutical products, appealing to consumers seeking natural alternatives. As per the IMARC Group, the United States health and wellness market is set to attain USD 1,560 Billion by 2033, exhibiting a CAGR of 5.8% from 2025-2033.

Europe Insomnia Market Analysis

The Europe insomnia market is driven by rising mental health issues, increasing workplace stress, and lifestyle routines that heighten sleep disturbances across both urban and rural populations. The growing awareness about the long-term cognitive and physical effects of poor sleep is encouraging more individuals to seek professional help, expanding demand for behavioral therapies, prescription medicines, and OTC sleep aids. An aging demographic plays a major role, as insomnia prevalence rises with age due to chronic illnesses, pain conditions, and neurological disorders. As per the report published by Age UK, in 2024, there were 22 Million people aged over 50 in England, equivalent to two in five of the total population. Europe’s strong regulatory focus on safe and clinically supported treatments is motivating the adoption of non-addictive sleep medications and structured psychological programs like CBT-I. Digital health adoption, including sleep-tracking wearables, mobile apps, and remote therapeutic programs, is gaining traction, as younger consumers are looking for technology-enabled solutions. Additionally, lifestyle factors, such as increased screen exposure, longer working hours, and urban noise pollution, contribute to sleep disruption, further supporting treatment demand.

Asia-Pacific Insomnia Market Analysis

The Asia-Pacific insomnia market is driven by rising stress levels, rapid urbanization, and increasingly demanding work schedules that disrupt sleep patterns across diverse age groups. The growing academic pressure among younger populations and high professional workloads among adults are contributing significantly to insomnia prevalence. Awareness about mental health and sleep quality is improving, encouraging more individuals to explore medical consultations, digital therapeutic tools, and OTC supplements. In October 2025, Go Spiritual, a prominent spiritual organization, initiated a groundbreaking mental health awareness campaign in India on World Mental Health Day. Rooted in the theme ‘Harmony in Mind and Soul, this initiative tackled the growing crisis of mental health challenges, suicides, and social pressures by integrating spiritual insights with contemporary mental health approaches. The region’s expanding middle class and increasing healthcare access support broader adoption of sleep aids, including herbal remedies, melatonin products, and prescription treatments. Technology use, especially late-night screen exposure, is also a major behavioral factor elevating sleep disturbances. Additionally, aging populations in countries like Japan, South Korea, and China are further boosting the demand.

Latin America Insomnia Market Analysis

The Latin America insomnia market is driven by rising stress, socioeconomic pressures, and increasing mental health concerns that disrupt sleep across different communities. The growing urbanization, long commutes, and extended work hours are contributing to poor sleep hygiene and higher demand for treatment options. Awareness about sleep disorders is gradually improving, encouraging interest in both pharmaceutical therapies and natural supplements. Expanding access to healthcare services and digital wellness tools also supports diagnosis and management. Additionally, lifestyle changes, increased screen usage, and an aging population are propelling the market growth in the region.

Middle East and Africa Insomnia Market Analysis

The Middle East and Africa insomnia market is driven by lifestyle stress, changing work cultures, and environmental factors, such as heat and irregular sleep routines that affect overall rest quality. Rising mental health awareness and better recognition of sleep disorders are encouraging more individuals to seek treatment. Urbanization, late-night technology use, and shift-based employment contribute to widespread sleep disruption. Improving healthcare infrastructure and the growing availability of sleep clinics, medications, and wellness supplements are supporting the market expansion. Additionally, aging population and chronic disease prevalence are driving the demand for insomnia-related solutions.

Competitive Landscape:

Key players in the insomnia market are actively engaged in a variety of strategic initiatives aimed at enhancing their market position and meeting evolving consumer demands. These initiatives include ongoing R&D efforts focused on discovering and developing new pharmacological treatments and therapies tailored to address different types and severities of insomnia. Additionally, players are investing in advanced diagnostic technologies to improve the accuracy of insomnia diagnosis, thereby enabling more personalized treatment approaches. Collaborations with healthcare providers and academic institutions are also common, facilitating the exchange of knowledge and the development of innovative treatment protocols. Furthermore, there is a growing emphasis on the integration of digital health solutions and telemedicine platforms to expand access to insomnia care and improve patient outcomes through remote monitoring and support services. Players are also navigating regulatory landscapes to secure approvals for new products and indications, ensuring compliance with evolving healthcare regulations. Market leaders are increasingly focused on sustainability and social responsibility initiatives, aligning their business strategies with broader environmental and community health goals.

The report provides a comprehensive analysis of the competitive landscape in the insomnia market with detailed profiles of all major companies, including:

- Aurobindo Pharma USA

- Eisai Inc.

- Idorsia Pharmaceuticals, Ltd

- Mallinckrodt Pharmaceuticals

- Merck & Co., Inc

- Neurim Pharmaceuticals LTD

- Pfizer Inc

- Sanofi S.A.

Latest News and Developments:

- September 2025: Johnson & Johnson revealed findings from the Phase 3 MDD3005 26-week clinical trial assessing the effectiveness and safety of seltorexant versus quetiapine extended release (XR) as an add-on therapy in adults and older patients suffering from major depressive disorder (MDD) with insomnia symptoms. Patients receiving seltorexant had significantly fewer side effects compared to those on quetiapine XR, and a higher number of patients completed the 26-week study duration.

- July 2024: Neurim Pharmaceuticals announced that they received a positive CHMP opinion for Slenyto® (Pediatric Prolonged-Release Melatonin) to treat insomnia in children with neurogenetic disorders, expanding its indication to benefit more patients.

- June 2024: Merck & Co revealed that their trial for the insomnia medication suvorexant demonstrated continued effectiveness over a 12-month period in a late-stage study, making it the first sleep aid trial to last a full year.

- July 2023: Astellas Pharma announced a significant collaboration with Pfizer to advance the combination therapy of PADCEV™ (enfortumab vedotin) with KEYTRUDA® (pembrolizumab) for the first-line treatment of advanced urothelial cancer. This therapy has shown promise in improving overall and progression-free survival compared to standard platinum-containing chemotherapy.

- June 2022: Merck launched the Merck Digital Sciences Studio (MDSS) to support early-stage biomedical startups. This initiative aims to foster innovation in drug discovery and development by providing startups with investment, access to Azure Cloud computing, and collaboration opportunities with Merck scientists. MDSS will prioritize startups developing AI and ML applications, offering resources and expertise to accelerate their technologies.

Insomnia Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Therapy Types Covered |

|

| Drug Classes Covered | Antidepressants, Melatonin Antagonist, Benzodiazepines, Nonbenzodiazepines, Orexin Antagonist, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Drug Stores, Online Pharmacies |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Aurobindo Pharma USA, Eisai Inc., Idorsia Pharmaceuticals, Ltd, Mallinckrodt Pharmaceuticals, Merck & Co., Inc, Neurim Pharmaceuticals LTD, Pfizer Inc, Sanofi S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the insomnia market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global insomnia market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the insomnia industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Insomnia Market Report

The insomnia market was valued at USD 5.5 Billion in 2025.

The insomnia market is projected to exhibit a CAGR of 2.45% during 2026-2034, reaching a value of USD 6.8 Billion by 2034.

Greater public awareness, supported by healthcare campaigns and easier access to medical advice, is encouraging more individuals to seek diagnosis and treatment. The aging population also plays a major role, as older adults experience higher rates of sleep disturbances linked to health conditions and medication use. Advancements in sleep-related research, wearable sleep trackers, and digital therapeutic apps are expanding non-pharmacological treatment options.

North America currently dominates the insomnia market, accounting for a share of 36.4%. The North America insomnia market is primarily driven by the rising awareness and diagnosis of insomnia disorders, supported by advanced healthcare infrastructure and diagnostic capabilities. Other factors, such as high prevalence of lifestyle-related factors including stress, irregular work hours, and sedentary lifestyles, along with the growing elderly population, are creating a positive insomnia market outlook across the region.

Some of the major players in the insomnia market include Aurobindo Pharma USA, Eisai Inc., Idorsia Pharmaceuticals, Ltd, Mallinckrodt Pharmaceuticals, Merck & Co., Inc, Neurim Pharmaceuticals LTD, Pfizer Inc, Sanofi S.A., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade