Insurance Third Party Administrator Market Size, Share, Trends and Forecast by Insurance Type and Region, 2026-2034

Global Insurance Third Party Administrator Market Size, Share, Trends & Forecast (2026-2034)

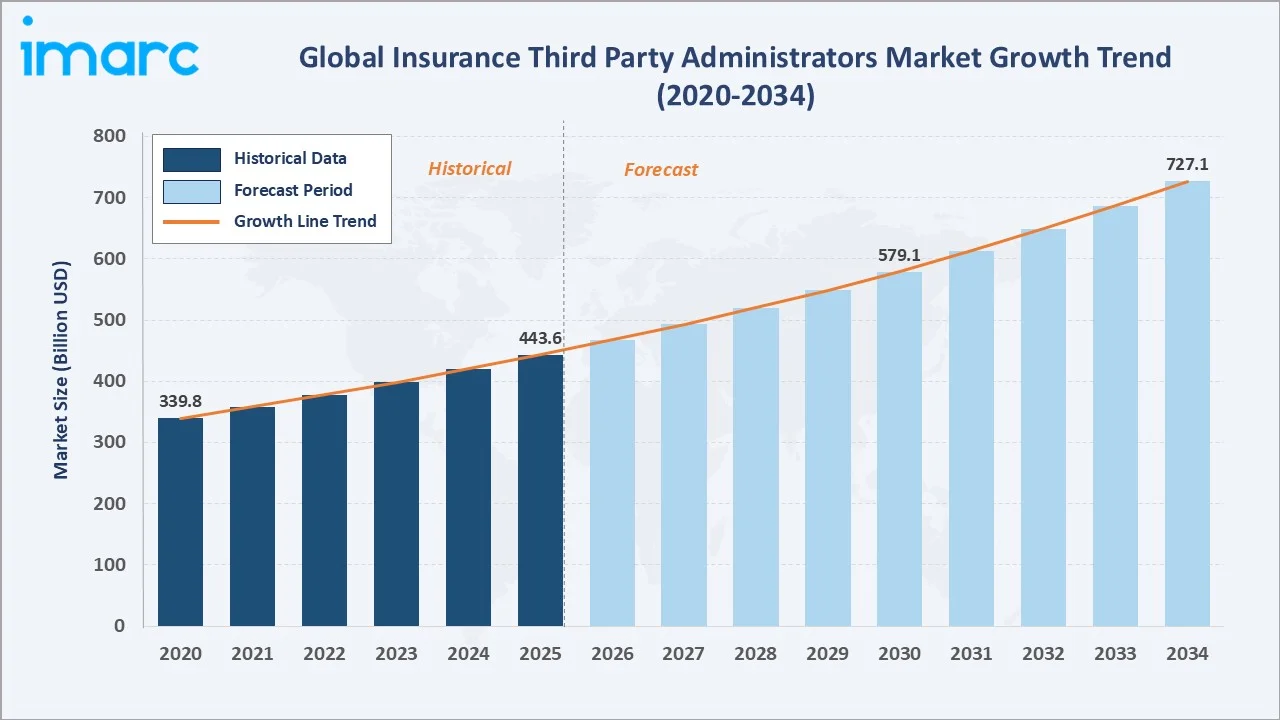

The Global Insurance third party administrator market reached a value of USD 443.6 Billion in 2025 and is projected to reach USD 727.1 Billion by 2034. The market is expected to register a CAGR of 5.48% during 2026-2034. Growth is driven by rising healthcare claims, expanding self-insured employer base, regulatory complexity, and rapid digital claims automation. Health insurance led the insurance type segment with 46.3% share in 2025. North America dominated with 38.7% global revenue share in 2025, supported by the country's mature self-funded health plan ecosystem and large commercial liability market. The insurance Third Party Administrator market trends point toward AI-led claims processing and embedded insurance services through 2034.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 443.6 Billion |

|

Forecast Market Size (2034) |

USD 727.1 Billion |

|

CAGR (2026-2034) |

5.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

North America (38.7%) |

|

Fastest Growing Region |

Asia Pacific (~7.2% CAGR) |

|

Leading Insurance Type (2025) |

Health Insurance (46.3%) |

|

Top Companies |

Sedgwick, Crawford & Company, Gallagher Bassett, Optum (United Health Group), ESIS (Chubb Limited). |

The insurance Third Party Administrator market growth trajectory from 2020 through 2034 shows a sustained expansion path. Market value grew from USD 339.8 Billion in 2020 to USD 443.6 Billion in 2025, supported by post-pandemic claims volumes.

Forecast values reflect strong demand from health insurance and retirement administration through 2030. The market is expected to add over USD 280 Billion in value by 2034, anchored by rising self-insured employer adoption.

To get more information on this market, Request Sample

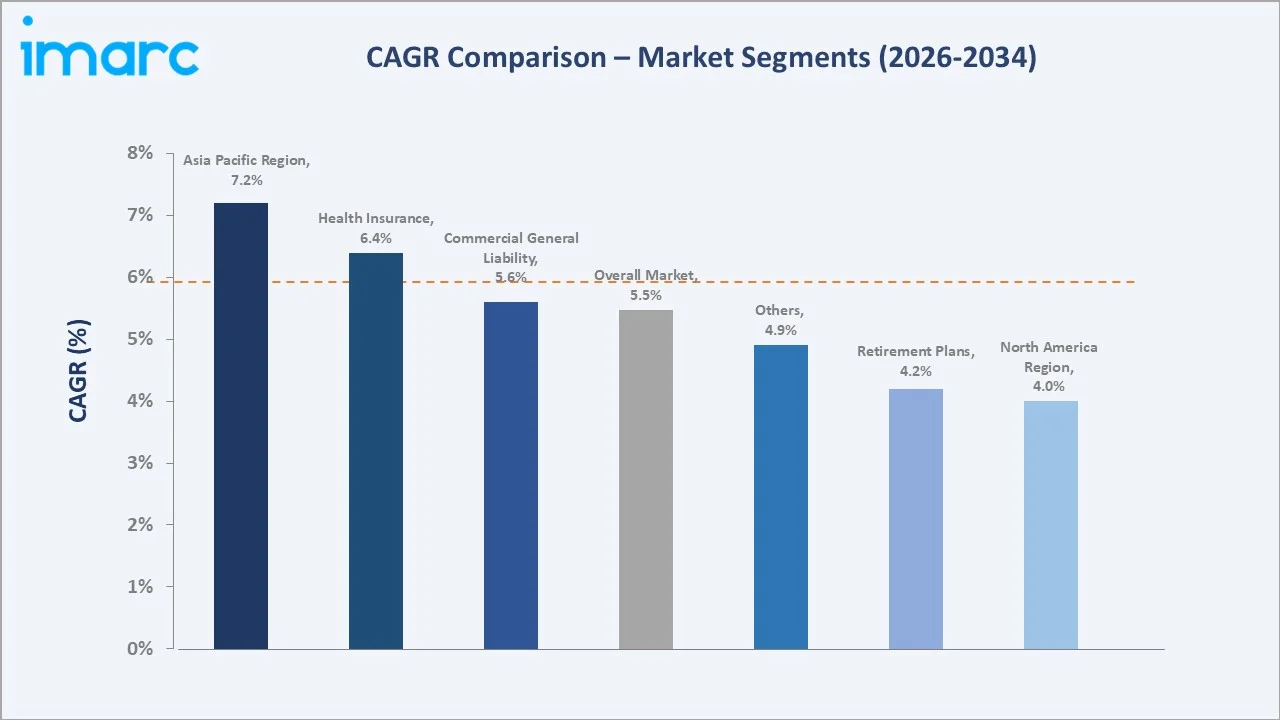

Segment-level CAGR comparisons highlight Asia Pacific and health insurance administration as the fastest-growing categories. Both outpace the overall 5.48% benchmark through 2034.

Executive Summary

The global insurance Third Party Administrator market size stood at USD 443.6 Billion in 2025 and is forecast to reach USD 727.1 Billion by 2034. The insurance Third Party Administrator market growth reflects a CAGR of 5.48% over 2026-2034, anchored by rising healthcare claims and outsourcing demand.

Health insurance accounted for 46.3% of total Third-Party Administrator revenue in 2025, supported by the United States' self-funded employer health plans covering over 153 million Americans. Retirement plans held 24.8%, while commercial general liability insurance captured 17.6%. Digital transformation, AI-driven claims processing, and embedded insurance services are reshaping the operating model.

North America led with 38.7% global revenue share in 2025. Europe held 26.2% and Asia Pacific 21.5%. The insurance Third Party Administrator market outlook remains strong as employers embrace outsourcing, regulators tighten compliance, and insurers offload non-core operations. Asia Pacific is the fastest growing region, driven by India and China's expanding health insurance penetration.

Key Market Insights

|

Insight |

Data |

|

Largest Insurance Type |

Health Insurance - 46.3% share (2025) |

|

Second Insurance Type |

Retirement Plans - 24.8% share (2025) |

|

Third Insurance Type |

Commercial General Liability - 17.6% share (2025) |

|

Leading Region |

North America - 38.7% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific - ~7.2% CAGR (2026-2034) |

|

Top Companies |

Sedgwick, Crawford & Company, Gallagher Bassett, Optum, ESIS, Davies Group |

|

Self-Insured Coverage (US) |

153+ million members (2025) |

Key Analytical Observations Supporting the Above Data:

- Health Insurance dominance: Health insurance held 46.3% of insurance Third Party Administrator revenue in 2025. US self-funded employer plans covering over 153 million members anchor the segment.

- Retirement Plans share: Retirement plans accounted for 24.8% in 2025. Pension administration outsourcing is expanding as defined-contribution plan assets surpassed USD 11 trillion in the United States in 2025.

- North America leadership: North America commanded 38.7% global revenue share in 2025. The United States hosts the world's largest self-insured employer base and the most mature commercial liability claims market.

- Asia Pacific acceleration: Asia Pacific grew at an estimated 7.2% CAGR through 2030. India's Ayushman Bharat scheme covering 500+ million beneficiaries and China's commercial health insurance growth fuel demand.

- Digital claims automation: Over 60% of Third-Party Administrators deployed AI or RPA tools in claims handling by 2025. Straight-through processing rates exceeded 35% for routine health claims.

- Top company consolidation: Sedgwick, Crawford & Company, and Gallagher Bassett together held an estimated 25-30% of global Third-Party Administrator revenue in 2025, reinforcing scale advantages.

Global Insurance Third Party Administrator Market Overview

Insurance third party administrators handle claims processing, premium collection, benefits administration, and compliance reporting for insurance carriers, employers, and self-insured organizations. They operate as outsourced operating partners across health, retirement, commercial liability, and specialty insurance lines.

The Third-Party Administrator industry sits at the intersection of insurance distribution, technology, and regulatory compliance. It is shaped by macroeconomic factors such as healthcare cost inflation, aging populations, employer benefits trends, and digital transformation. Workforce shortages in claims adjustment and rising data privacy regulations further influence demand.

The market spans full-service generalist Third-Party Administrators serving multiple lines, specialist administrators focused on workers' compensation or pension plans, and technology-led entrants offering API-first claims platforms. Strategic alignment between insurers, brokers, and Third-Party Administrators is intensifying through 2034.

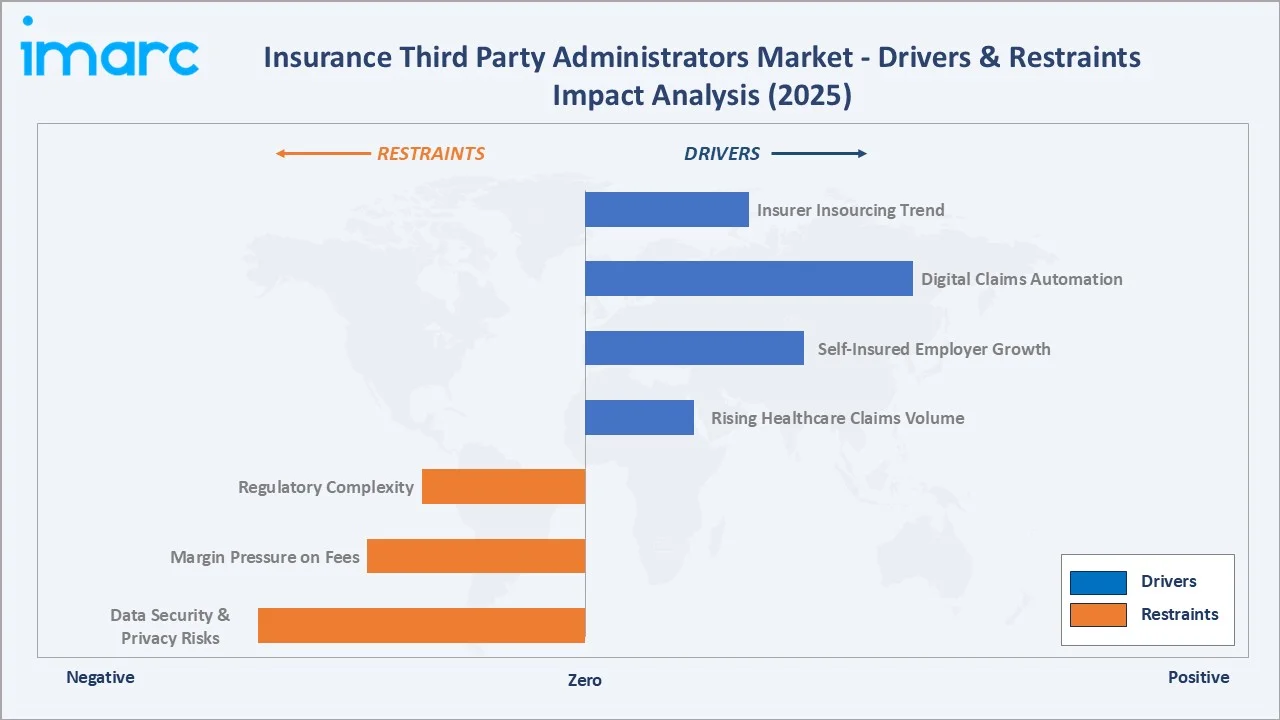

Market Dynamics

The insurance Third Party Administrator market is shaped by a balance of growth drivers and structural restraints. The chart below summarizes the relative impact weight of each force in 2025.

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Healthcare Claims Volume: United States national health expenditure crossed USD 5 trillion in 2024, lifting claims volumes for Third Party Administrators handling self-insured employer plans. Health insurance held the largest Third-Party Administrator share at 46.3% in 2025.

- Self-Insured Employer Growth: Over 65% of US workers with employer health coverage were enrolled in self-funded plans in 2024. Employers continue to outsource administration to specialized Third Party Administrators to control costs.

- Digital Claims Automation: AI, machine learning, and robotic process automation cut average health claims handling time by 25-35% across leading Third-Party Administrators in 2025. Investment in InsurTech platforms is accelerating.

- Regulatory Complexity: Compliance with HIPAA, ERISA, GDPR, and emerging AI governance rules creates demand for specialized administrative expertise. Compliance-led outsourcing rose meaningfully through 2025.

Demand drivers reflect the structural shift of insurance operations toward outsourcing and digital services. The combined pressure of cost containment, scale economics, and regulatory burden continues to define the insurance Third Party Administrator market growth path through 2034.

Market Restraints

- Data Security and Privacy Risks: Third Party Insurance Administrators process sensitive health and financial records. Cyber breach incidents in the US insurance sector rose nearly 19% year-on-year in 2024, lifting compliance and insurance costs.

- Margin Pressure on Fees: Carrier consolidation and procurement-led negotiation compressed Third Party Administrator margins by 100-150 basis points between 2022 and 2025, especially in commoditized health claims processing.

- Insurer Insourcing Trend: Some carriers are bringing claims operations back in-house to capture data and customer experience. This selective insourcing trend limits Third Party Administrator growth in specific niches.

Market Opportunities

- Embedded Insurance Administration: Embedded insurance offerings via fintech, retail, and travel platforms are projected to grow at over 25% annually through 2030. Third Party Administrators supplying back-end administration for these programs gain significant volume.

- Cyber Insurance Third Party Administrator Services: Global cyber insurance premiums approached USD 15 billion in 2024 and are projected to grow exponentially by 2030. Specialized Third Party Administrators handling cyber claims and incident response represent a high-growth niche.

- Asia Pacific Health Coverage Expansion: Government programs such as India's Ayushman Bharat covering over 500 million beneficiaries and China's growing commercial health market open large addressable opportunities for regional Third-Party Administrator players.

Market Challenges

- Talent Shortage in Claims Adjustment: The US Bureau of Labor Statistics projected a decline in adjuster employment through 2030. Third Party Administrators face wage inflation and longer hiring cycles for licensed claims professionals in 2025.

- Legacy Technology Modernization: Many Third-Party Administrators still operate legacy claims platforms. Migration to cloud-native core systems requires multi-year investments and disrupts day-to-day client service.

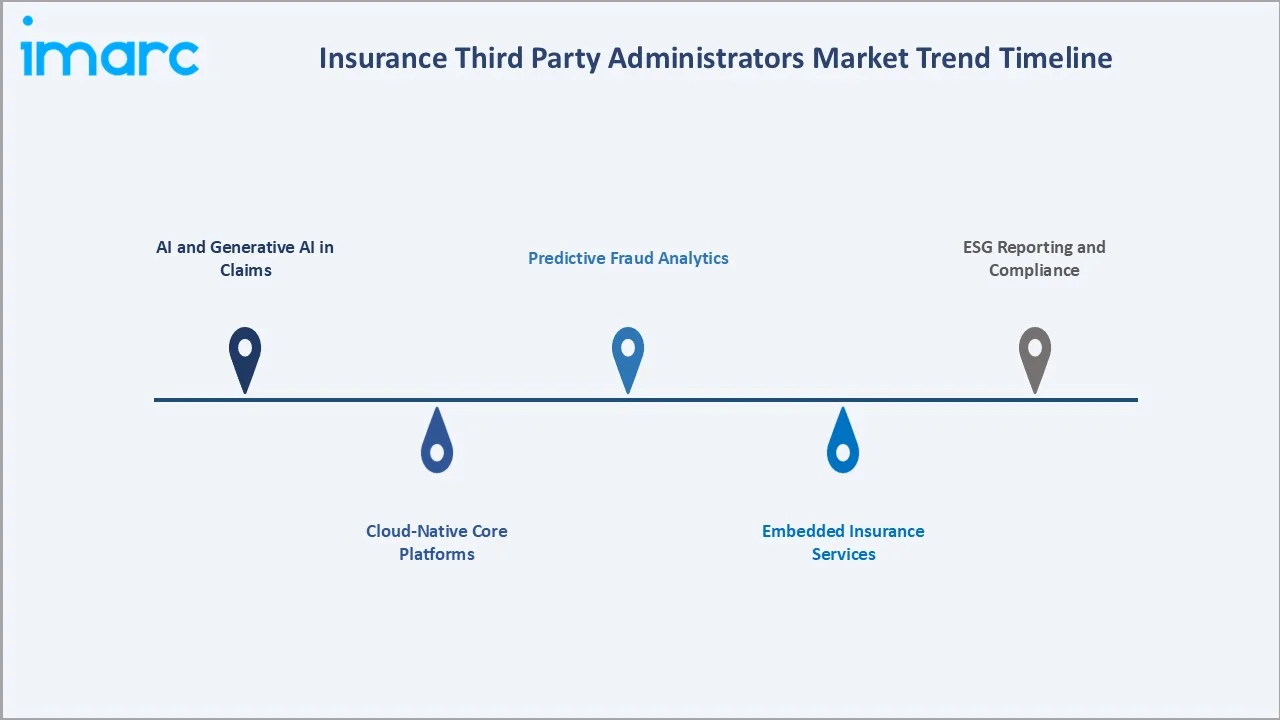

Emerging Market Trends

AI and Generative AI in Claims

Generative AI tools are reshaping claims triage, fraud detection, and customer correspondence. Leading Third Party Administrators reported 20-30% productivity gains in claims handling pilots run during 2024-2025.

Cloud-Native Core Platforms

Third Party Administrators are migrating from legacy mainframes to cloud-native cores from Guidewire, Duck Creek, and Sapiens. Third Party Administrators are rapidly transitioning to cloud-based platforms, which accounted for nearly half of technology deployments in 2025, with adoption expected to accelerate as insurers prioritize scalability and real-time processing.

Embedded Insurance Services

Embedded insurance distribution through retail, fintech, and mobility platforms is creating new Third Party Administrator service categories. Embedded gross written premiums are forecast to exceed USD 700 billion globally by 2030.

Predictive Fraud Analytics

Insurance claims fraud costs the global industry over USD 60 billion annually. Third Party Administrators are deploying machine learning fraud engines, with leading vendors reporting improvement in fraud detection rates.

ESG Reporting and Compliance

Insurers face rising disclosure requirements under EU Sustainable Finance Regulation and SEC climate rules. Third Party Administrators are expanding ESG data capture, beneficiary outreach, and reporting capabilities through 2025.

Industry Value Chain Analysis

The insurance Third Party Administrator value chain spans six integrated stages from policy intake through member services. Each stage presents distinct technology, compliance, and competitive dynamics.

|

Value Chain Stage |

Key Participants / Description |

|

Policy Intake |

Insurance carriers, brokers, and digital distribution platforms onboarding new policies into Third Party Administrator systems |

|

Premium Administration |

Premium calculation, billing, collection, and remittance across health, retirement, and commercial lines |

|

Claims Processing |

First notice of loss intake, eligibility checks, documentation handling, and claims registration |

|

Adjudication & Payments |

Claims investigation, settlement decisioning, provider/beneficiary payments, and recovery |

|

Reporting & Compliance |

HIPAA, ERISA, GDPR reporting, regulatory filings, audit trails, and ESG-related disclosures |

|

Member Services |

Beneficiary communication, dispute resolution, digital portals, and call center support |

Third Party Administrators that integrate digital claims processing with strong compliance and member-experience capabilities capture the highest economic value. Cloud-native and AI-led players are reshaping competitive positioning across all six stages through 2034.

Technology Landscape in the Insurance Third Party Administrator Industry

Artificial Intelligence and Machine Learning

AI-led claims triage, document review, and fraud scoring have become standard. Leading Third Party Administrators report productivity gains and improvement in fraud detection rates from machine learning deployments in 2025.

Cloud-Native Core Platforms

Modern claims and policy administration platforms from Guidewire, Duck Creek, and Sapiens dominate cloud migration. Adoption among top 50 global Third-Party Administrators rose by 2025, accelerating deployment cycles.

Robotic Process Automation

RPA bots handle routine data entry, eligibility verification, and provider payments. Straight-through processing rates exceeded for routine health claims among leading Third-Party Administrators in 2025, lowering unit costs.

Cybersecurity and Data Privacy

With cyber breaches in US insurance rising year-on-year in 2024, Third Party Administrators are investing in zero-trust architectures, encryption, and continuous monitoring to protect HIPAA and GDPR-regulated data.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

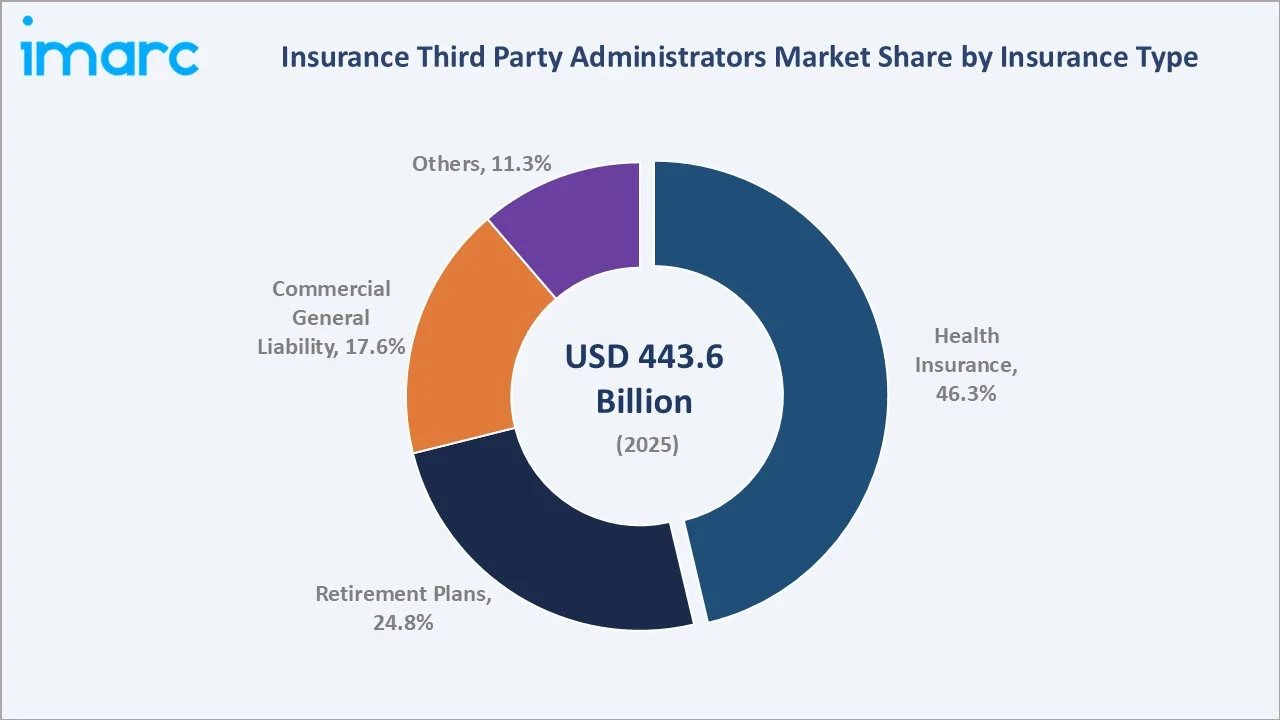

| Insurance Type | Health Insurance | 46.3% |

2025 |

|

Region |

North America |

38.7% |

2025 |

By Insurance Type

|

Insurance Type |

Share (2025) |

Key Insight |

|

Health Insurance |

46.3% |

Anchored by US self-funded employer plans covering 153+ million members |

|

Retirement Plans |

24.8% |

Pension administration outsourcing across DC plans worth USD 11+ trillion (US, 2024) |

|

Commercial General Liability |

17.6% |

Workers' comp and commercial liability claims; Sedgwick and Gallagher Bassett lead |

|

Others |

11.3% |

Travel, cyber, life, and specialty insurance administration |

Health insurance led the insurance Third Party Administrator market share in 2025 with 46.3%. The dominance reflects the United States' self-insured employer base, where employers offload claims and benefits administration to Third Party Administrators to manage cost and complexity.

To access detailed market analysis, Request Sample

Retirement plans accounted for 24.8% in 2025, supported by an aging workforce and pension administration outsourcing. Commercial general liability captured 17.6%, while specialty lines such as cyber, travel, and life insurance contributed the remaining 11.3% share.

The pie chart confirms health insurance's structural lead. The non-health categories together account for 53.7% of the insurance Third Party Administrator market size in 2025, leaving meaningful headroom for retirement and commercial growth through 2034.

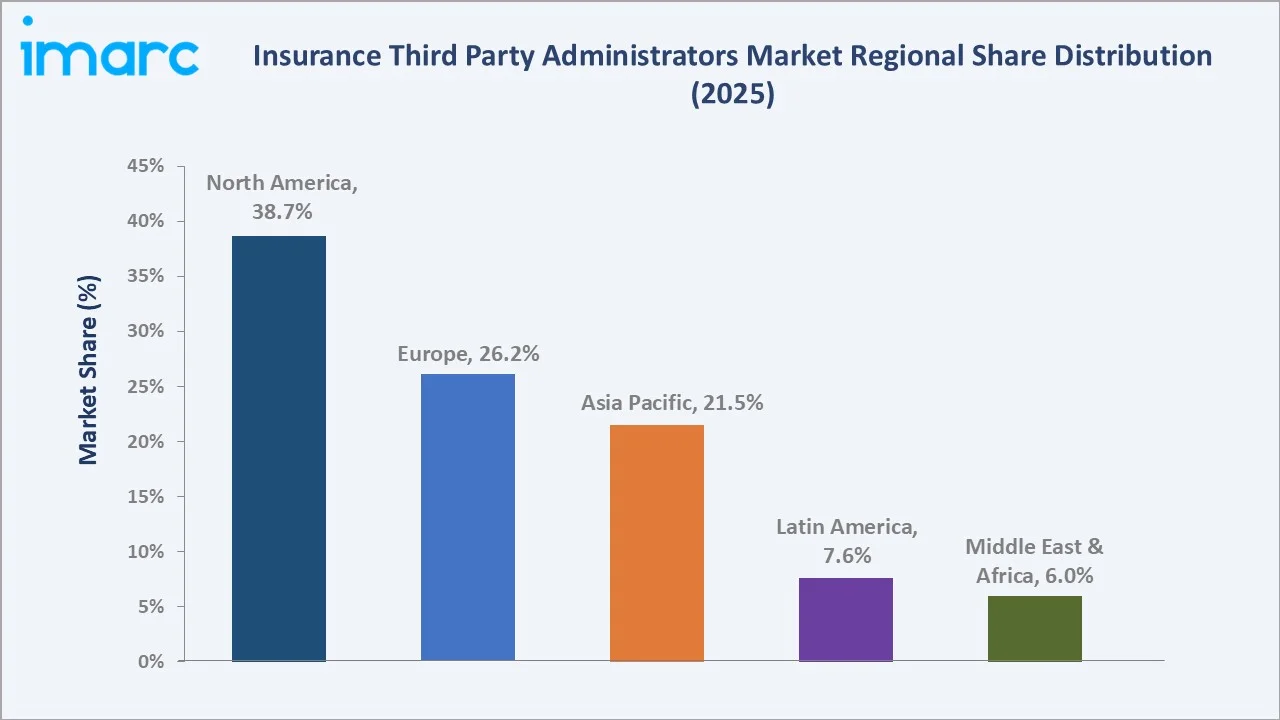

Regional Market Insights

Insurance Third Party Administrator demand is geographically concentrated in mature insurance markets. North America leads, while Asia Pacific emerges as the fastest growing region, backed by health insurance penetration in India and China.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.7% |

US self-insured employer plans, mature commercial liability, ERISA compliance, large pension assets |

|

Europe |

26.2% |

GDPR-driven outsourcing, UK and German pension administration, EU Solvency II reporting |

|

Asia Pacific |

21.5% |

India's Ayushman Bharat (500M+ beneficiaries), China's commercial health, Japan's pension reforms |

|

Latin America |

7.6% |

Brazil/Mexico health insurance growth, expanding middle-class coverage, regulatory modernization |

|

Middle East and Africa |

6.0% |

GCC mandatory health insurance, South Africa retirement administration, expat coverage |

North America's 38.7% share in 2025 reflects the United States' world-leading self-insured market, with over 65% of insured workers covered under self-funded employer plans. Canada's expanding pension administration market also contributes to regional dominance.

Asia Pacific's 21.5% share is anchored by India's Ayushman Bharat scheme covering 500+ million beneficiaries and China's commercial health insurance expansion. The region is the fastest growing at an estimated 7.2% CAGR through 2030.

Europe's 26.2% reflects mature retirement administration in the UK and Germany, alongside GDPR-driven compliance demand. Latin America (7.6%) and Middle East & Africa (6.0%) show moderate but rising activity tied to regulatory modernization in 2025.

Regional analysis underscores the geographic concentration of demand. North America and Europe together accounted for 64.9% of global insurance Third Party Administrator revenue in 2025, shaping competitive priorities and investment flows.

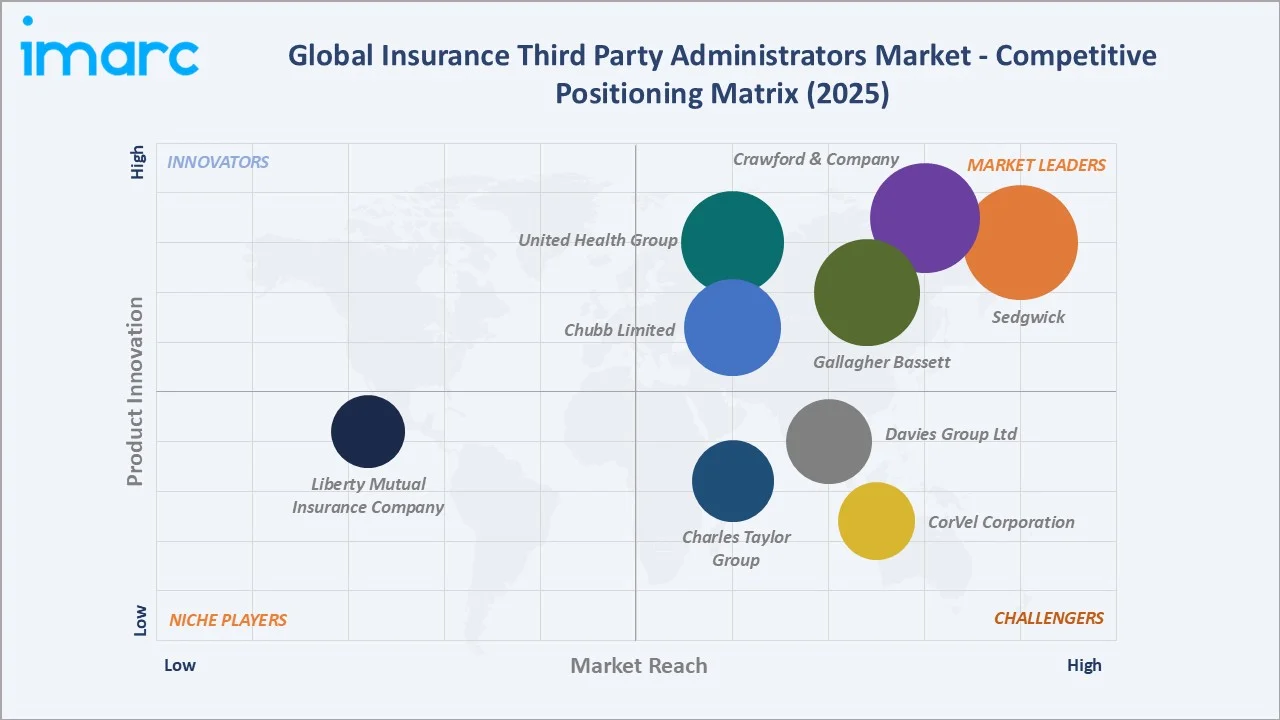

Competitive Landscape

The global insurance Third Party Administrator market is moderately consolidated. Global majors hold significant share, while regional and specialist players serve niche segments such as cyber, workers' compensation, and pension administration.

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Sedgwick |

Sedgwick, York Risk |

Leader |

Workers' comp, casualty, broad global footprint |

|

Crawford & Company |

Crawford, Broadspire |

Leader |

Property and casualty Third Party Administrator, global claims network |

|

Gallagher Bassett |

Gallagher Bassett |

Leader |

Commercial liability, US public sector, technology-led |

|

United Health Group |

Optum |

Leader |

Health insurance administration, US self-funded plans |

|

Chubb Limited |

ESIS |

Leader |

Commercial casualty Third Party Administrator, global multinational accounts |

|

Davies Group Ltd |

Davies |

Challenger |

UK and EU Third Party Administrator, claims and adjusting services |

|

CorVel Corporation |

CorVel |

Challenger |

Workers' comp, technology-driven medical bill review |

|

Charles Taylor Group |

Charles Taylor |

Challenger |

Marine, aviation, specialty insurance Third Party Administrator services |

|

Liberty Mutual Insurance Company |

Helmsman Management Services |

Emerging |

Workers' comp, multi-line claims for US employers |

The top three players, Sedgwick, Crawford & Company, and Gallagher Bassett, together held an estimated 25-30% of global insurance Third Party Administrator revenue in 2025. UnitedHealth's Optum and Chubb's ESIS strengthen the leadership tier in health and commercial lines respectively.

The matrix groups players by geographic reach and service innovation breadth. Leaders combine global footprint with broad service portfolios, while challengers and emerging firms target specific lines or geographies through 2034.

Key Company Profiles

Sedgwick

- Company Overview: Sedgwick is a global leader in claims management, loss adjusting, and risk management solutions. Headquartered in Memphis, Tennessee, the firm operates in 80+ countries with over 33,000 colleagues.

- Service Portfolio: Workers' compensation, casualty, property, marine, benefits, and disability claims administration; loss adjusting; managed care services.

- Recent Developments: Sedgwick launched its Global Specialty platform in 2026, a dedicated solution designed to manage large and complex claims across sectors such as marine, energy, and other technical risk categories. The platform is centered in London with additional hubs across Asia, the Middle East, and the Americas, and is supported by over 100 specialist loss adjusters, reflecting a strategic investment to expand capabilities and address rising complexity in global claims.

- Strategic Focus: Technology-led claims handling, AI-powered triage, expanding into specialty risk such as cyber and ESG-related liability.

Crawford & Company

- Company Overview: Crawford & Company is one of the world's largest publicly listed independent providers of claims management and outsourcing solutions. The firm operates across 70+ countries serving carriers, brokers, and corporates.

- Service Portfolio: Broadspire Third Party Administrator services, loss adjusting, third-party administration, contractor connection, and managed care for property, casualty, and specialty insurance lines.

- Recent Developments: Crawford & Company undertook a major organizational restructuring in 2025, including ~$14 million in restructuring costs, aimed at improving operational efficiency, profitability, and business processes. As part of this shift, the company is realigning its business into three core segments—U.S. Operations, Broadspire, and International Operations—effective January 2026, to create a more streamlined, client-centric structure.

- Strategic Focus: Global claims network, technology-enabled adjusting, and specialty Third Party Administrator services across complex commercial accounts.

Gallagher Bassett

- Company Overview: Gallagher Bassett is the global Third Party Administrator arm of Arthur J. Gallagher & Co. The firm provides risk management and claims solutions across multiple lines for corporates, public entities, and insurers.

- Service Portfolio: Workers' compensation, general liability, auto, property, professional liability, and specialty risk claims management with strong analytics tools.

- Recent Developments: Gallagher Bassett acquired Reck & Co. GmbH, a Germany-based marine and transportation claims specialist, to strengthen its global marine and transit claims management offering and expand its footprint across Europe.

- Strategic Focus: Public sector and large commercial leadership, technology-driven decision support, and international expansion in Europe and Asia Pacific.

Market Concentration Analysis

The global insurance Third Party Administrator market exhibits moderate fragmentation. Global majors lead in share, while regional and specialist players cover niche segments and underserved geographies.

- Top 5 share: The top five players, Sedgwick, Crawford & Company, Gallagher Bassett, Optum (United Health Group), ESIS (Chubb Limited), collectively accounted for 35-42% of global insurance Third Party Administrator revenue in 2025.

- Fragmentation level: The remaining 58-65% is distributed among Davies Group, CorVel, Charles Taylor, Helmsman, regional specialists, and a long tail of country-level Third Party Administrators across Asia Pacific and Latin America.

- Consolidation trends: M&A activity remained robust in 2024-2025. Private equity capital continued backing platform consolidations, especially in workers' compensation and health Third Party Administrator.

- Bifurcated competition: Premium tier consolidation focuses on global scale and AI capabilities. Mid-market and specialty Third Party Administrators are differentiating through niche expertise in cyber, ESG, and embedded insurance.

Investment & Growth Opportunities

Fastest-Growing Segments

Health insurance administration is the highest-growth segment at 6.4% CAGR through 2030, supported by US self-insured plan expansion. Cyber insurance Third Party Administrator services represent a premium growth opportunity.

Emerging Market Expansion

India is the highest-potential emerging market, driven by Ayushman Bharat covering 500+ million beneficiaries and rapid private health insurance growth. Southeast Asia, GCC mandatory health insurance regimes, and Brazil's expanding middle class also represent significant volume opportunities.

Venture and Strategic Investment Trends

Strategic acquisitions and InsurTech investments are reshaping the competitive landscape. Private equity capital is backing platform plays in workers' compensation, health, and specialty Third Party Administrator. Investments in AI claims engines, cloud-native cores, and embedded insurance APIs are the primary capital deployment areas through 2034.

Future Market Outlook (2026-2034)

The global insurance Third Party Administrator market forecast projects steady value expansion from USD 443.6 Billion in 2025 to USD 727.1 Billion by 2034 at a CAGR of 5.48%. North America will retain leadership while Asia Pacific accelerates structurally through health insurance penetration.

Three key shifts will reshape the insurance Third Party Administrator market through 2034. First, generative AI will automate over 50% of routine claims processing by 2030. Second, embedded insurance will create new Third Party Administrator service categories tied to retail, fintech, and mobility ecosystems. Third, cyber and ESG-related Third Party Administrator services will become a meaningful revenue line for specialist players.

Regional dynamics will continue to evolve. Asia Pacific is forecast to lift its share from 21.5% in 2025 toward 25-26% by 2034, while North America gradually moderates to 35-36% as international markets catch up. Mature markets will see consolidation; emerging markets will see capacity build-out.

Research Methodology

Primary Research

Primary research included structured interviews with Third Party Administrator executives, insurance carrier procurement leaders, broker risk consultants, and self-insured employer benefits managers. Over 35 expert interviews supported demand-side validation in 2024-2025.

Secondary Research

Secondary sources include insurance regulator filings, NAIC reports, US Department of Labor data, OECD pension statistics, AM Best reports, company annual reports, and trade publications such as Insurance Journal, Claims Magazine, and Risk & Insurance.

Forecasting Models

Market sizing and growth projections used a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, healthcare expenditure data, insurance premium volumes, and pension assets. Scenario analyses (base, optimistic, conservative) accounted for macroeconomic uncertainty.

Data Validation

Data underwent triangulation across primary, secondary, and proprietary sources. Cross-checks against insurance premium volumes, claims expenditure data, and Third-Party Administrator company filings improved estimate confidence intervals to within ±3%.

Insurance Third Party Administrator Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Insurance Types Covered | Health Insurance, Retirement Plans, Commercial General Liability Insurance, Others |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Sedgwick, Crawford & Company, Gallagher Bassett, United Health Group, Chubb Limited, Davies Group Ltd, CorVel Corporation, Charles Taylor Group, Liberty Mutual Insurance Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the insurance third party administrator market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global insurance third party administrator market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the insurance third party administrator industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Insurance Third Party Administrator Market Report

The global insurance Third Party Administrator market reached USD 443.6 Billion in 2025, supported by rising healthcare claims, self-insured employer growth, and outsourcing of claims and benefits administration.

The market is projected to reach USD 727.1 Billion by 2034, growing at a CAGR of 5.48% during 2026-2034, supported by digital claims automation and embedded insurance expansion.

Health insurance leads with 46.3% share in 2025, anchored by US self-funded employer plans covering over 153 million members and rising healthcare cost containment needs.

North America dominates with 38.7% share in 2025. The United States hosts the world's largest self-insured employer base and most mature commercial liability claims market.

Asia Pacific is the fastest growing region at an estimated 7.2% CAGR through 2030, driven by India's Ayushman Bharat scheme and China's commercial health insurance growth.

Key drivers include rising healthcare claims volume, self-insured employer expansion, digital and AI claims automation, regulatory complexity around HIPAA, ERISA, and GDPR compliance.

Major players include Sedgwick, Crawford & Company, Gallagher Bassett, United Health Group, Chubb Limited, Davies Group Ltd, CorVel Corporation, Charles Taylor Group, Liberty Mutual Insurance Company.

AI and generative AI claims automation, cloud-native core platforms, robotic process automation, predictive fraud analytics, and zero-trust cybersecurity are reshaping Third Party Administrator operations through 2034.

Restraints include data security risks, margin pressure on fees, insurer insourcing of select operations, and shortages of licensed claims adjusters across mature markets.

Opportunities include cyber insurance Third Party Administrator services, embedded insurance administration, Asia Pacific health expansion, AI claims engines, and ESG reporting capabilities for global carriers.

Digital transformation is automating over 35% of routine claims, lifting productivity by 20-35%, and enabling cloud-native core platforms among 55%+ of top global Third Party Administrators by 2025.

Third Party Administrators administer benefits, process claims, manage compliance, and operate member services for self-insured employers, who covered over 65% of US insured workers in 2024.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)