Interior Car Accessories Market Size, Share, Trends and Forecast by Type, Vehicle Type, Distribution Channel, and Region, 2026-2034

Interior Car Accessories Market Size and Share:

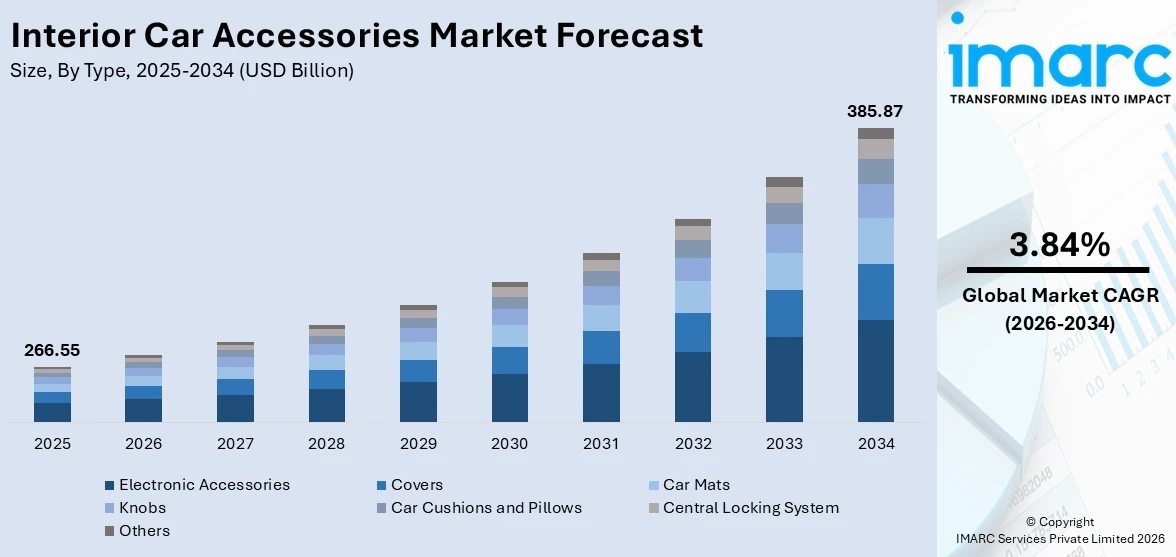

The global interior car accessories market size was valued at USD 266.55 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 385.87 Billion by 2034, exhibiting a CAGR of 3.84% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 37.5% in 2025. The region benefits from a rapidly expanding automotive sector, rising middle-class incomes fueling vehicle ownership, and the growing preference for personalized vehicle interiors across densely populated urban centers in developing nations, which collectively reinforce the interior car accessories market share.

The rising inclination among vehicle owners toward enhancing cabin comfort, aesthetics, and functionality is a primary factor propelling the interior car accessories market growth globally. The proliferation of advanced infotainment systems, touchscreen displays, wireless charging modules, and smart connectivity features in modern automobiles has significantly elevated the demand for electronic interior accessories. Additionally, the expanding vehicle parc across both developed and developing regions creates a sustained replacement and upgrade cycle for products such as seat covers, floor mats, cushions, and knobs. The growing emphasis on vehicle personalization, driven by shifting consumer lifestyles and social media influence, further amplifies spending on aftermarket interior components. Favorable economic conditions in several countries have also increased disposable incomes, enabling a broader consumer base to invest in premium interior accessories that improve driving convenience and overall vehicle appeal.

The United States has emerged as a major region in the interior car accessories market owing to many factors. This aging fleet drives consistent replacement demand for interior components such as seat covers, floor mats, and electronic upgrades. Furthermore, a strong culture of vehicle customization and personalization among consumers fuels spending on aftermarket interior accessories. The expansion of e-commerce platforms and dedicated automotive parts retailers has simplified access to a wide range of products. Growing interest in technology-integrated accessories, including wireless phone chargers, advanced dash cameras, and ambient lighting kits, continues to strengthen consumer engagement with the market.

To get more information on this market Request Sample

Interior Car Accessories Market Trends:

Rising Smart Technology Integration

The rapid integration of smart technology into vehicle cabins is reshaping the demand landscape for interior accessories. Modern consumers increasingly expect seamless digital connectivity, voice-controlled infotainment, wireless device charging, and advanced navigation features as standard elements of their driving experience. This evolution has elevated the role of electronic interior components, transforming them from optional add-ons into essential cabin features. Automakers and aftermarket suppliers are responding with products that incorporate artificial intelligence, augmented reality head-up displays, and multi-device synchronization capabilities. The transition toward electrified powertrains has further accelerated technology adoption in vehicle interiors, as electric vehicles often feature digitally native cabin architectures. For instance, in 2025, hybrid-electric vehicles captured 34.5% of the total EU new car market, becoming the most preferred powertrain option among European buyers. This shift toward technologically advanced powertrains directly elevates consumer expectations for sophisticated interior digital accessories and connectivity-enabled components across all price segments.

Growing Sustainability in Interior Materials

Sustainability has become a defining factor in the development and selection of vehicle interior accessories, reflecting the broader interior car accessories market outlook across the industry. Manufacturers are increasingly adopting recycled plastics, bio-based polymers, organic textiles, and responsibly sourced leather alternatives to produce seat covers, floor mats, dashboard trims, and cushioning materials. Consumer awareness regarding environmental impact has heightened demand for products that minimize ecological footprints without compromising quality or aesthetics. Regulatory frameworks in major markets are also mandating the reduction of volatile organic compounds and hazardous substances in automotive interior components, pushing suppliers toward cleaner formulations. For instance, India's total electric vehicle registrations reached 1.97 million units in fiscal year 2024-25, reflecting a 16.9% increase over the previous year. This accelerating electrification trend reinforces the demand for sustainably manufactured interior accessories that align with the eco-conscious ethos of electric vehicle ownership and broader environmental stewardship across the automotive supply chain.

Expanding Aftermarket E-Commerce Channels

The expansion of digital retail platforms is fundamentally transforming how consumers discover, evaluate, and purchase vehicle interior accessories, shaping the interior car accessories market forecast positively. E-commerce channels now offer extensive product catalogs, detailed specifications, customer reviews, and competitive pricing that empower buyers to make informed purchasing decisions from their homes or mobile devices. The convenience of doorstep delivery, easy returns, and subscription-based maintenance kits has attracted a growing base of digitally savvy consumers who prefer online shopping over traditional brick-and-mortar outlets. Social media marketing and influencer partnerships have further amplified product visibility and brand awareness across global audiences. The growing availability of virtual try-on tools, augmented reality previews, and detailed installation tutorials on digital platforms has reduced purchase hesitation and improved consumer confidence in selecting interior accessories online. Additionally, marketplace aggregators and dedicated automotive parts portals enable seamless price comparisons across multiple brands and sellers, fostering a highly competitive retail environment that benefits consumers through better value propositions. This digital transformation of the aftermarket retail landscape continues to lower entry barriers for new suppliers while expanding the overall addressable consumer base for vehicle interior products globally.

Interior Car Accessories Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global interior car accessories market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, vehicle type, and distribution channel.

Analysis by Type:

- Covers

- Car Mats

- Knobs

- Electronic Accessories

- Car Cushions and Pillows

- Central Locking System

- Others

Electronic accessories hold 32.0% of the market share. Electronic interior accessories encompass a broad range of products including infotainment systems, navigation units, touchscreen displays, wireless charging modules, Bluetooth connectivity solutions, dash cameras, and ambient lighting kits that collectively enhance the driving experience. The dominance of this segment is attributed to the escalating consumer demand for in-vehicle digital connectivity, entertainment, and convenience features that mirror the technology integration prevalent in daily life. As vehicles increasingly serve as mobile digital environments, the need for advanced electronic components has grown substantially across all vehicle categories. The proliferation of smartphone integration technologies, voice-activated controls, and real-time navigation systems continues to drive consumer spending on electronic interior upgrades. This segment benefits from continuous innovation cycles that introduce products with improved functionality, sleeker designs, and greater compatibility with evolving vehicle architectures.

Analysis by Vehicle Type:

- Mini

- Hatchback

- Sedan

- SUV/MUV

- Sports-Car

- Others

Mini and hatchback leads the market with a share of 30.5%. Mini and hatchback vehicles represent a significant consumer base for interior car accessories due to their widespread popularity in urban commuting environments across global markets. These compact vehicle categories are favored for their affordability, fuel efficiency, and maneuverability in congested city traffic, attracting a broad demographic of first-time buyers, young professionals, and budget-conscious families. Vehicle owners in this segment frequently seek interior accessories that maximize cabin functionality within limited spatial dimensions, including compact organizers, custom-fit floor mats, ergonomic seat cushions, and space-efficient electronic accessories. The growing global urbanization trend continues to sustain demand for smaller vehicles, which directly supports the aftermarket for interior customization products tailored to compact cabin layouts and the specific comfort enhancement preferences of their owners.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Aftermarket

- OEM

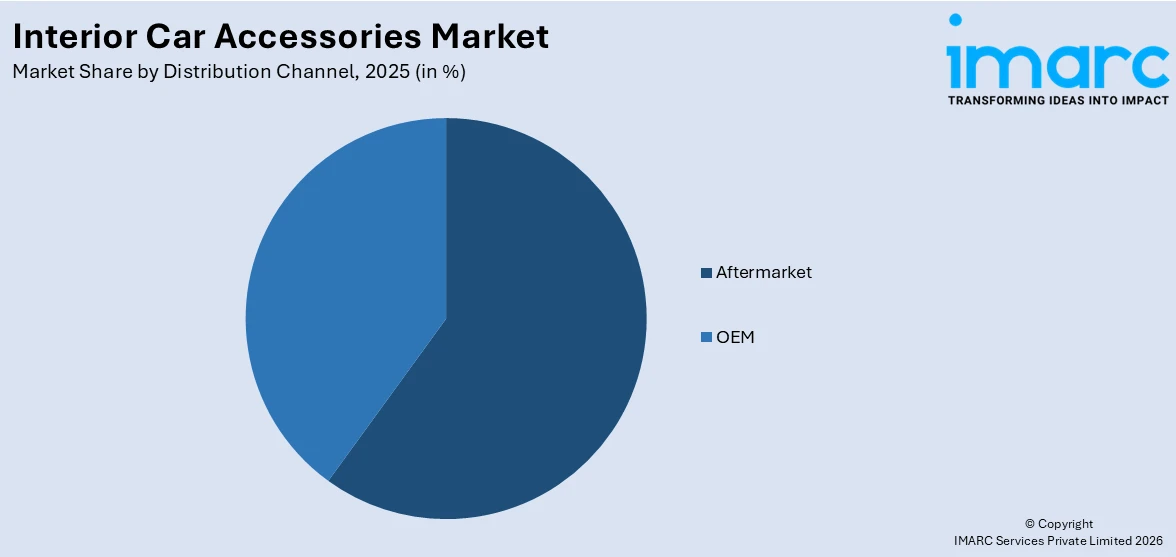

Aftermarket dominates the market, with a share of 59.0%. The aftermarket distribution channel maintains its dominant position through extensive product availability, competitive pricing, and the flexibility to cater to diverse consumer preferences that original equipment offerings often cannot fully address. Vehicle owners increasingly turn to aftermarket channels for interior upgrades, replacement components, and personalization products that allow them to customize cabin aesthetics and functionality according to individual tastes. The rapid expansion of e-commerce platforms, specialty automotive retailers, and dedicated accessory outlets has broadened consumer access to an extensive range of interior products spanning seat covers, floor mats, electronic accessories, and comfort enhancers. The do-it-yourself culture among vehicle enthusiasts, combined with growing awareness of product options through digital marketing and online reviews, further strengthens the aftermarket ecosystem and sustains its leading position in the distribution landscape.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific, accounting for 37.5% of the share, enjoys the leading position in the market. The dominance of the region is ensured by the high level of automotive production, the rising rates of vehicle ownership, and the increase in disposable income of the burgeoning middle-class population of the nations included in the region, such as China, India, Japan, South Korea, Indonesia, and Australia. The high level of original equipment manufacturing and the established base of original equipment suppliers ensure the availability of interior car accessories. The trend of urbanization in the region ensures the sustained demand for compact and mid-segment vehicles, which would require interior car accessories. The initiatives taken by the governments of the nations included in the region in the automotive industry ensure the dominance of the region as the primary driver of the interior car accessories industry globally.

Key Regional Takeaways:

North America Interior Car Accessories Market Analysis

The North America interior car accessories market benefits from a mature automotive ecosystem characterized by high vehicle ownership rates, strong consumer spending power, and a deeply embedded culture of vehicle personalization. The region's expansive highway infrastructure and reliance on personal automobiles for daily commuting sustain continuous demand for interior comfort and convenience accessories including seat covers, floor mats, electronic gadgets, and organizational products. Additionally, the growing popularity of sport utility vehicles and pickup trucks has expanded the addressable product range for interior accessories designed to accommodate larger cabin spaces. The increasing penetration of connected vehicle technologies and advanced infotainment systems creates further opportunities for aftermarket electronic accessory suppliers to serve a technology-receptive consumer base across both urban and suburban markets throughout the region.

United States Interior Car Accessories Market Analysis

The United States maintains its position as the dominant contributor to the North American interior car accessories market, driven by the world's largest light-duty vehicle fleet and a consumer landscape that strongly favors vehicle customization and interior upgrades. The country's extensive network of automotive parts retailers, specialty accessory shops, and e-commerce platforms provides consumers with unmatched product accessibility and choice, fueling the interior car accessories market trends across diverse product categories. The growing average age of vehicles on American roads drives a robust replacement market for wear-prone interior components, including floor mats, seat covers, and dashboard accessories. Furthermore, the expanding electric vehicle segment introduces new accessory categories designed to complement digitally integrated cabin environments. Consumer preferences for premium materials, technology-enhanced accessories, and branded interior products continue to strengthen spending in the aftermarket channel.

Europe Interior Car Accessories Market Analysis

Europe represents a significant market for interior car accessories, driven by the region's established automotive manufacturing heritage, stringent quality standards, and discerning consumer preferences for premium interior products. The transition toward electrified powertrains and technologically advanced vehicle cabins is reshaping accessory demand across the continent, with increasing focus on digital integration, sustainable materials, and ergonomic design principles. In 2025, battery-electric car registrations across the European Union reached approximately 1.88 million units, capturing 17.4% of the total new car market. This rapid electrification elevates demand for interior accessories compatible with the distinctive cabin architectures of electric vehicles, including wireless charging solutions, ambient lighting, and minimalist dashboard organizers. Germany, France, the United Kingdom, Italy, and Spain collectively account for the majority of regional demand, supported by strong purchasing power and a well-developed aftermarket infrastructure. Regulatory emphasis on vehicle safety and interior material standards further encourages accessory innovation and quality improvement across the value chain.

Asia-Pacific Interior Car Accessories Market Analysis

Asia Pacific continues to lead global demand for interior car accessories, supported by rapid vehicle ownership growth, expanding urbanization, and rising disposable incomes across its diverse economies. India's passenger vehicle domestic sales reached a record 4.3 million units during fiscal year 2024-25, reflecting the deepening automotive penetration that drives accessory consumption across the subcontinent. China remains the world's largest automobile market, sustaining massive demand for both original equipment and aftermarket interior products. Southeast Asian nations, including Indonesia and Thailand, are emerging as important growth centers due to expanding middle-class populations and increasing automotive manufacturing activity. The region's well-established e-commerce ecosystem further accelerates consumer access to a broad spectrum of interior accessory products, enabling rural and semi-urban markets to participate in the aftermarket upgrade cycle alongside metropolitan consumers.

Latin America Interior Car Accessories Market Analysis

Latin America presents growing opportunities for the interior car accessories market, driven by expanding vehicle fleets, urbanization trends, and improving economic conditions across major economies. Brazil and Mexico serve as the region's primary automotive markets, with increasing consumer interest in vehicle personalization and cabin comfort enhancements supporting aftermarket accessory demand. The growing penetration of e-commerce platforms across the region has broadened consumer access to a diverse range of interior products previously limited to physical retail channels. Government incentives supporting local automotive manufacturing and assembly operations further stimulate the domestic supply of interior components and accessories for regional consumers.

Middle East and Africa Interior Car Accessories Market Analysis

The Middle East and Africa region is witnessing gradual expansion in the interior car accessories market, supported by increasing vehicle ownership, infrastructure development, and rising consumer spending in Gulf Cooperation Council nations. Premium vehicle demand in countries such as the United Arab Emirates, Saudi Arabia, and Qatar drives interest in high-quality interior accessories including leather seat covers, advanced electronic systems, and luxury cabin enhancements. Across the broader African continent, the expanding used vehicle market and improving road infrastructure create emerging demand for replacement interior components. Growing urbanization and the expansion of organized retail and digital commerce channels are gradually improving product accessibility for consumers across the region.

Competitive Landscape:

The competitive scenario for the interior car accessories market can be identified as the presence of established players, regional players, and new digital players competing in various categories. Some of the prominent players in the market are focusing on the development of new products with the incorporation of latest technologies, which can be achieved through the development of new products with the incorporation of latest technologies, sustainable practices, and the development of new products with the incorporation of latest technologies. Strategic partnerships between the original equipment manufacturers and the interior car accessories manufacturers can be identified, which can allow the interior car accessories manufacturers to integrate the products with the new vehicle configurations. Expansion strategies, such as mergers, acquisitions, and expansion, can be identified as the prominent strategies for the growth of the market, particularly for the players operating in the markets with high growth rates.

The report provides a comprehensive analysis of the competitive landscape in the interior car accessories market with detailed profiles of all major companies, including:

- Car Mate Mfg Co. Ltd.

- Classic Soft Trim Inc

- Covercraft Industries

- Grupo Antolin

- Lloyd Mats

- O'Reilly Auto Parts Corporate

- Pecca Group Berhad

- Pep Boys

Latest News and Developments:

- In September 2025, Grupo Antolin inaugurated new manufacturing plants in Indonesia and Thailand, reinforcing its commitment to expanding production capacity across the Asia-Pacific region. The new facilities emphasize sustainable manufacturing practices, incorporating recycled materials and energy-efficient processes into the production of interior automotive components designed for regional and global vehicle programs.

Interior Car Accessories Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Covers, Car Mats, Knobs, Electronic Accessories, Car Cushions and Pillows, Central Locking System, Others |

| Vehicle Types Covered | Mini, Hatchback, Sedan, SUV/MUV, Sports-Car, Others |

| Distribution Channels Covered | Aftermarket, OEM |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Car Mate Mfg Co. Ltd., Classic Soft Trim Inc, Covercraft Industries, Grupo Antolin, Lloyd Mats, O'Reilly Auto Parts Corporate, Pecca Group Berhad, Pep Boys, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the interior car accessories market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global interior car accessories market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the interior car accessories industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Interior Car Accessories Market Report

The interior car accessories market was valued at USD 266.55 Billion in 2025.

The interior car accessories market is projected to exhibit a CAGR of 3.84% during 2026-2034, reaching a value of USD 385.87 Billion by 2034.

The key factors driving the interior car accessories market include the rising consumer inclination toward vehicle personalization and cabin comfort enhancement, growing integration of smart technology and digital connectivity in modern vehicles, expanding e-commerce distribution channels, increasing adoption of sustainable interior materials, and the expanding global vehicle fleet driving replacement and upgrade demand.

Asia Pacific currently dominates the interior car accessories market, accounting for a share of 37.5%. The region benefits from a massive automotive production base, rapidly rising vehicle ownership driven by expanding middle-class populations, strong aftermarket infrastructure, and the growing consumer preference for personalized vehicle interiors.

Some of the major players in the interior car accessories market include Car Mate Mfg Co. Ltd., Classic Soft Trim Inc, Covercraft Industries, Grupo Antolin, Lloyd Mats, O'Reilly Auto Parts Corporate, Pecca Group Berhad, Pep Boys, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)