Intraoperative Imaging Market Size, Share, Trends and Forecast by Product, Application, End Use, and Region, 2026-2034

Intraoperative Imaging Market Size, Share, Trends & Forecast (2026-2034)

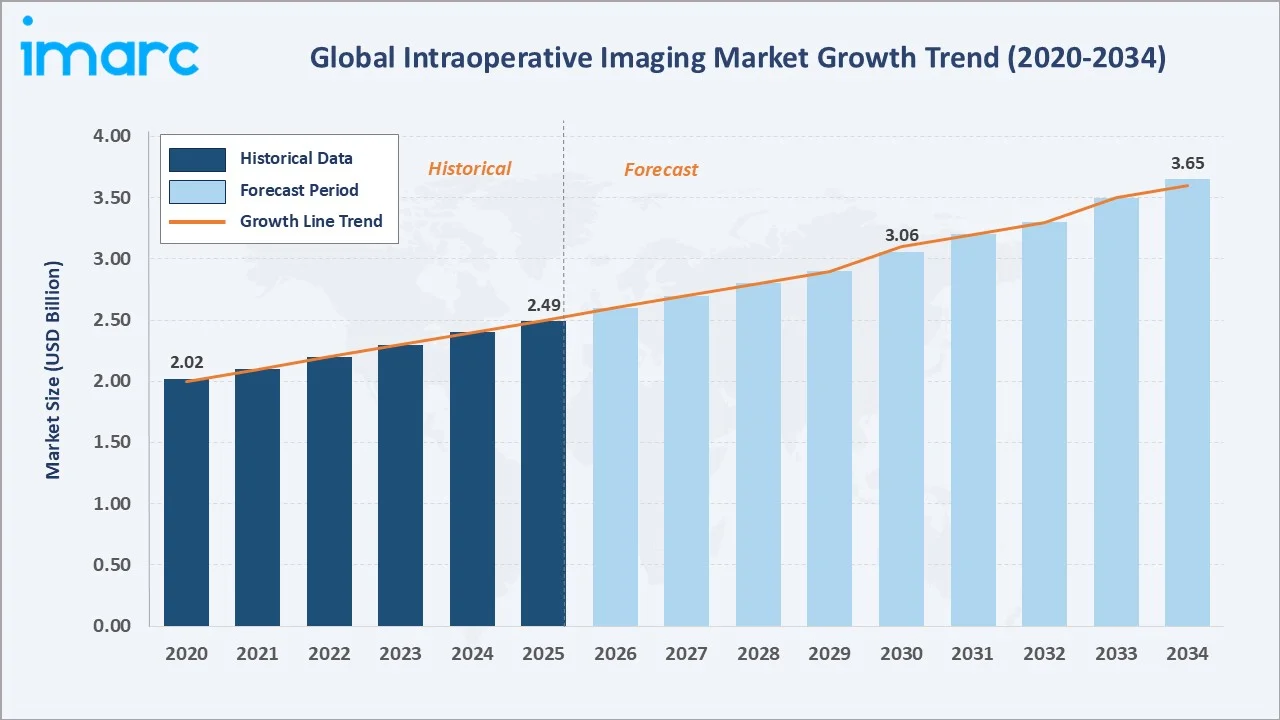

The global intraoperative imaging market reached USD 2.49 Billion in 2025 and is projected to reach USD 3.65 Billion by 2034, growing at a CAGR of 4.22% during 2026-2034. The escalating need for precision in complex surgeries, rising incidence rates of neurological, orthopedic, and cardiovascular conditions, growing emphasis on patient-centric care, and continual technological advancements in image-guided surgical platforms are the key market growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.49 Billion |

|

Forecast Market Size (2034) |

USD 3.65 Billion |

|

CAGR (2026-2034) |

4.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

Advanced imaging modalities such as intraoperative MRI, CT, ultrasound, and fluorescence imaging are increasingly used across neurosurgery, oncology, and cardiovascular procedures. Rapid technological innovations, growing adoption of minimally invasive surgeries, and the need for enhanced intraoperative guidance are driving investments and market expansion globally.

To get more information on this market, Request Sample

The intraoperative imaging market is underpinned by rising global surgical volumes driven by aging demographics, technological convergence between imaging modalities and robotic surgical platforms, and expanding healthcare infrastructure in Asia-Pacific and Latin America. These forces collectively sustain a consistent growth trajectory through the forecast horizon.

Executive Summary

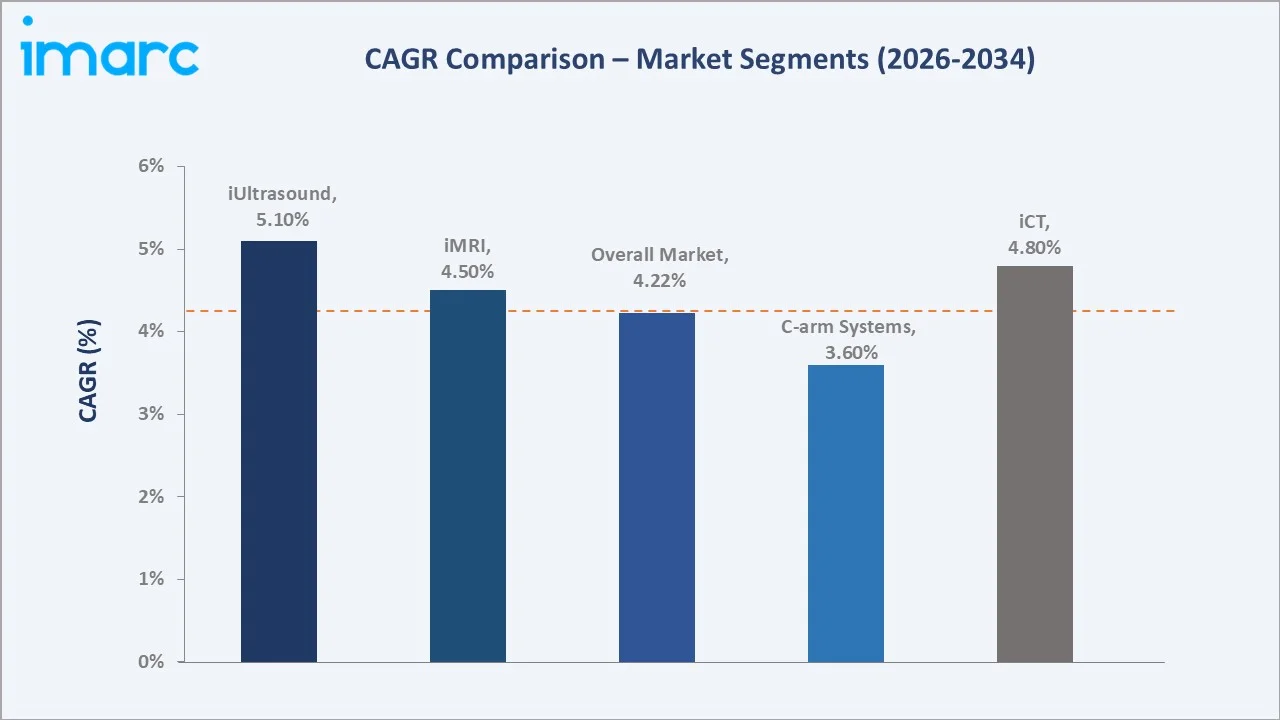

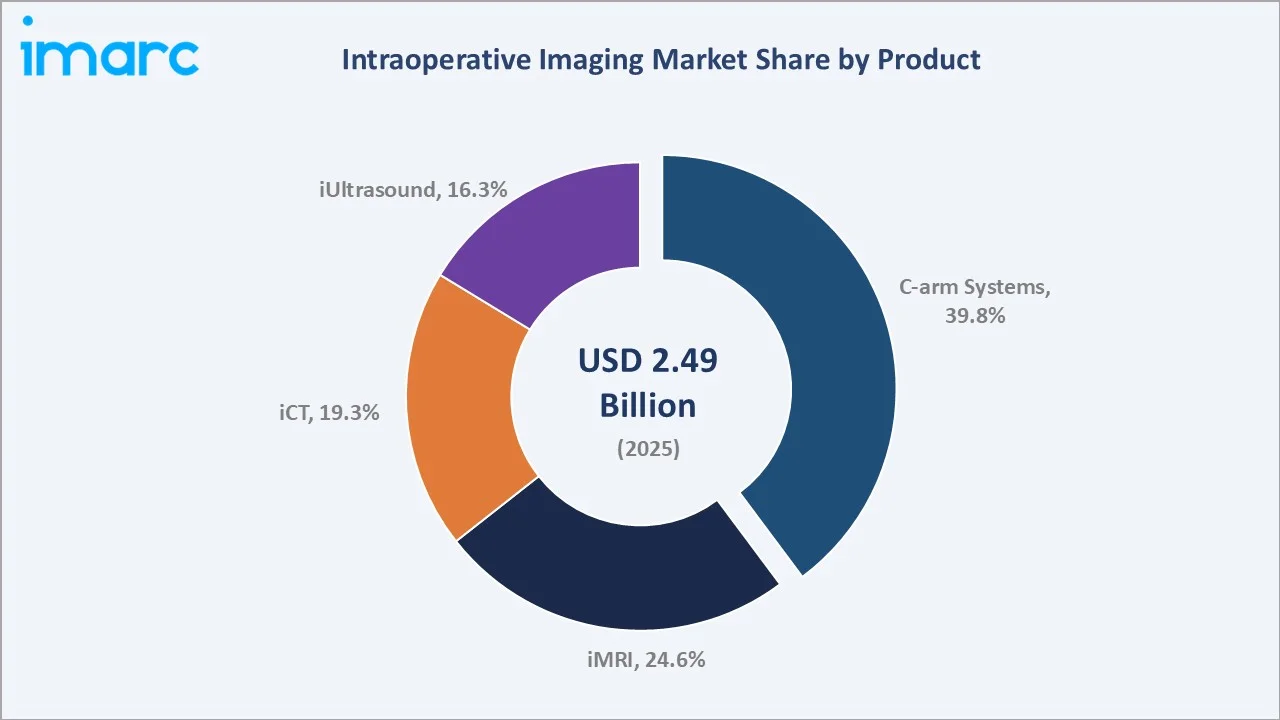

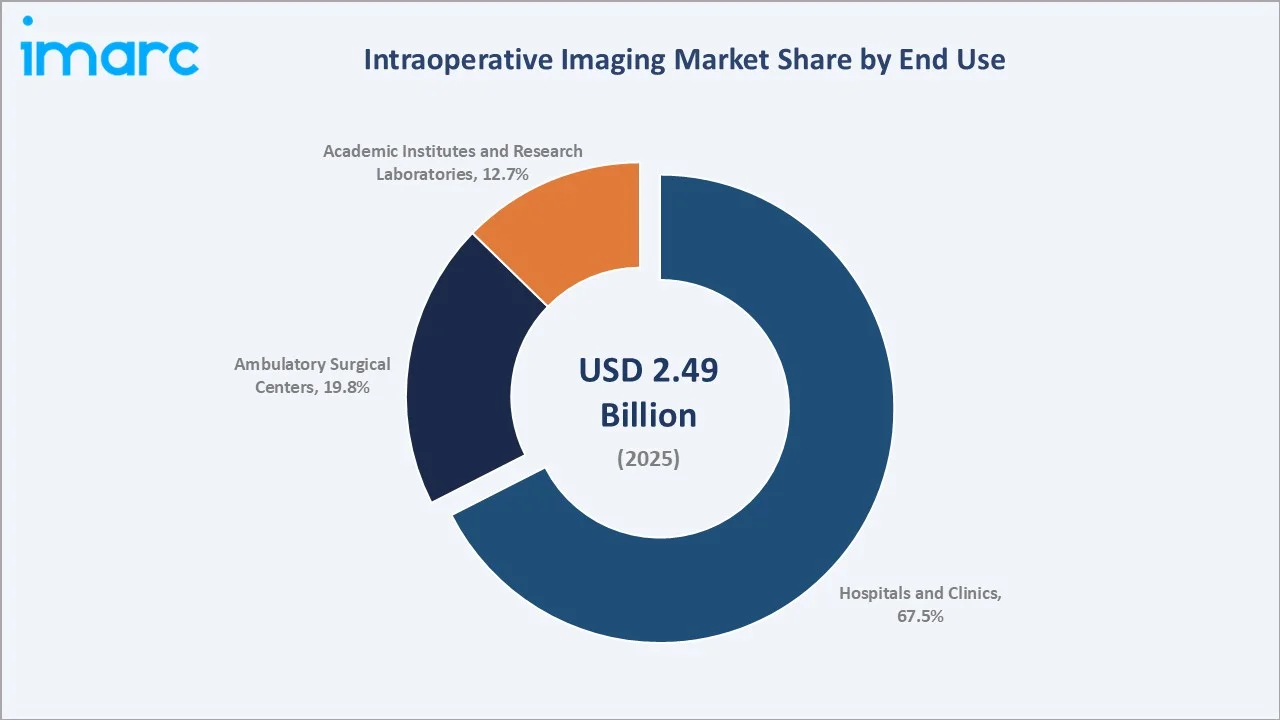

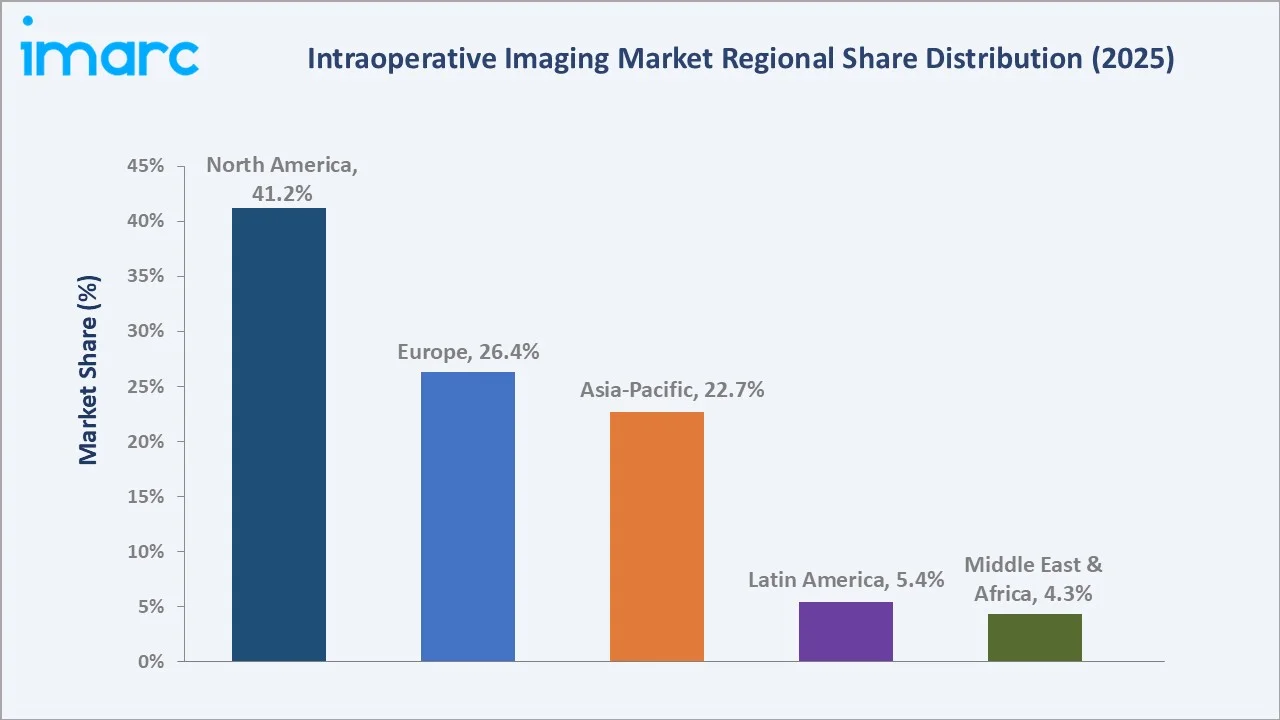

The global intraoperative imaging market was valued at USD 2.49 Billion in 2025 and is forecast to reach USD 3.65 Billion by 2034 at a CAGR of 4.22%. C-arm systems lead product segmentation at 39.8%, followed by iMRI at 24.6%, iCT at 19.3%, and iUltrasound at 16.3%. Hospitals and clinics dominate end-use at 67.5%. North America leads regionally at 41.2%, anchored by the advanced United States surgical infrastructure, robust reimbursement frameworks, and high imaging technology adoption.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

C-arm Systems – 39.8% share (2025) |

|

Fastest Growing Product |

iUltrasound – ~5.1% CAGR (2026-2034) |

|

Largest End-Use Segment |

Hospitals and Clinics – 67.5% share (2025) |

|

Fastest Growing End Use |

Ambulatory Surgical Centers – ~5.8% CAGR |

|

Leading Region |

North America – 41.2% share (2025) |

|

Top Companies |

GE HealthCare, Siemens, Medtronic, Koninklijke Philips N.V., ATON GmbH |

Key Analytical Observations For 2025:

- C-arm Systems (39.8%): Broad clinical utility across orthopedic, cardiovascular, urological, and spinal disciplines, combined with relative cost efficiency versus iMRI/iCT installations, drives dominant share. AI-assisted fluoroscopy and 3D reconstruction sustain replacement demand within existing installed bases.

- iMRI (24.6%): Indispensable in high-precision neurosurgical procedures for real-time soft-tissue contrast imaging during tumor resection and deep brain stimulation, commanding premium pricing concentrated at major academic medical centers.

- Hospitals and Clinics (67.5%): Primary setting for complex multi-disciplinary procedures requiring dedicated hybrid operating room infrastructure and multi-modality imaging procurement contracts.

- North America (41.2%): Advanced surgical infrastructure density, comprehensive Medicare/Medicaid and private insurance reimbursement for image-guided procedures, and a highly innovation-receptive hospital procurement culture.

Intraoperative Imaging Market Overview

Intraoperative imaging encompasses real-time use of advanced imaging technologies during surgical procedures to provide continuous anatomical visualization. The global market spans four principal modalities: C-arm fluoroscopy, intraoperative MRI (iMRI), intraoperative CT (iCT), and intraoperative ultrasound (iUltrasound), serving neurosurgery, orthopedics, cardiovascular surgery, oncological resection, and spine procedures.

Macroeconomic drivers include the global aging of populations generating increased surgical demand, the World Health Organization estimate of over 300 million surgical procedures performed annually, and government healthcare investment programs in China, India, Brazil, and Gulf states accelerating hospital modernization. The intraoperative imaging market forecast reflects these structural dynamics sustaining above-average demand through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

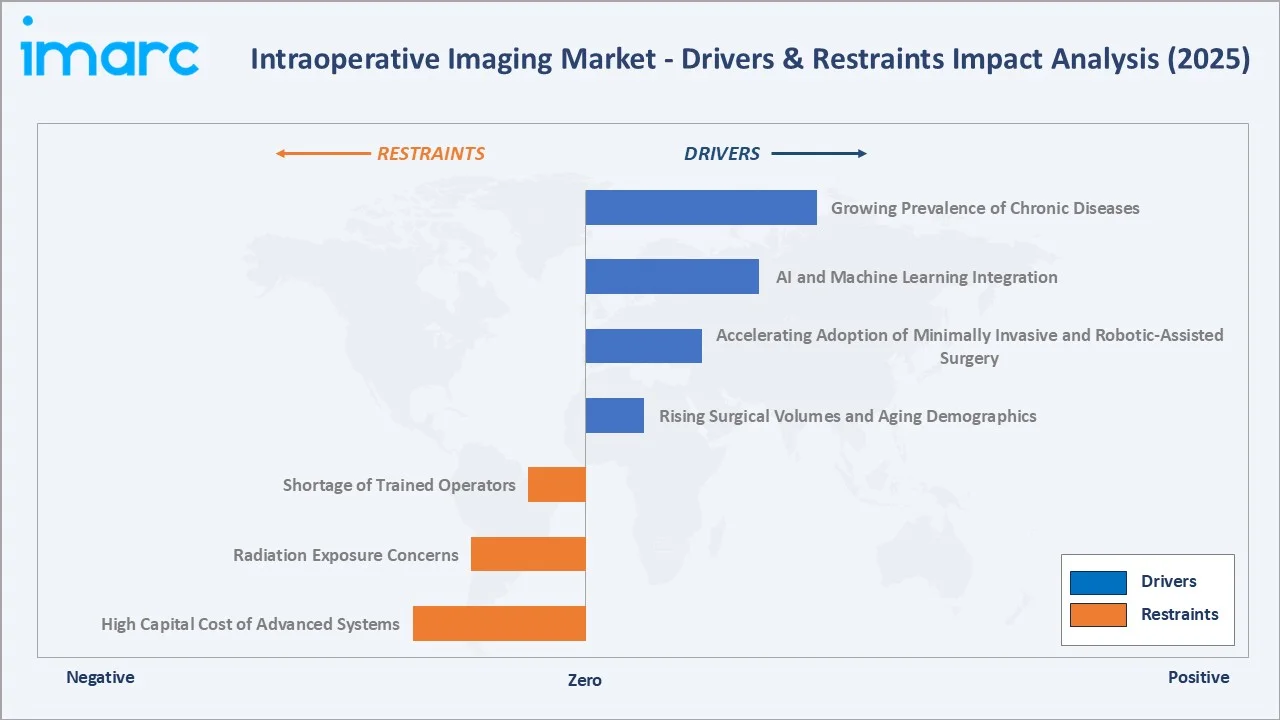

Market Drivers

- Rising Surgical Volumes and Aging Demographics: The global population of individuals aged 60 and above is expected to rise from 1.1 billion in 2023 to 1.4 billion by 2030. This is generating sustained demand for orthopedic joint replacements, neurosurgical interventions, and cardiovascular procedures, each relying increasingly on real-time imaging guidance.

- Accelerating Adoption of Minimally Invasive and Robotic-Assisted Surgery: Minimally invasive techniques require continuous high-resolution imaging guidance to compensate for reduced tactile feedback, making intraoperative imaging an indispensable procedural tool.

- AI and Machine Learning Integration: AI-assisted robotic surgeries have shown a 25% reduction in operative time and a 30% decrease in intraoperative complications compared with traditional manual procedures. Embedding AI-powered image enhancement and automated anatomical segmentation into imaging systems is substantially improving clinical utility and driving upgrade procurement cycles.

- Growing Prevalence of Chronic Diseases: Rising global incidence of neurological disorders, spinal conditions, cardiovascular disease, and cancer directly expands the surgical procedure base relying on intraoperative imaging. Approximately 90% of the United States’ USD 4.9 trillion annual health care spending is directed toward individuals with chronic and mental health conditions.

Market Restraints

- High Capital Cost of Advanced Systems: iMRI systems require USD 2.5–6 Million per installation inclusive of facility shielding, while iCT costs USD 1–5 Million, representing significant barriers for community hospitals in emerging economies.

- Radiation Exposure Concerns: Extended fluoroscopic procedures expose surgical teams to cumulative radiation doses, adding workflow complexity and prompting shifts toward non-ionizing modalities in specific clinical contexts.

- Shortage of Trained Operators: Effective utilization of advanced iMRI and AI-enabled C-arms requires specialized training, and the global shortage of trained operators constrains adoption in healthcare systems with limited specialist programs.

Market Opportunities

- Expansion of Ambulatory Surgical Centers: Rapid proliferation of ASCs as the preferred setting for elective procedures is creating substantial demand for portable, space-efficient imaging systems.

- AI-Powered Imaging Platforms: AI integration is enabling imaging systems to perform tumor margin assessment, navigation accuracy verification, and real-time implant positioning, expanding clinical application and revenue opportunity per system.

- Healthcare Infrastructure in Asia-Pacific and Latin America: Government-led hospital construction programs in China, India, and Brazil are creating large-scale procurement opportunities for intraoperative imaging equipment.

Market Challenges

- Complex Regulatory Compliance: Medical imaging devices require rigorous approval processes across FDA, EU MDR, CDSCO, and NMPA, necessitating substantial investment and extending time-to-market for new system launches.

- Supply Chain Disruptions: Flat-panel detectors, high-power X-ray generators, and gradient coils rely on concentrated global supply chains, and geopolitical disruptions can adversely impact manufacturing timelines.

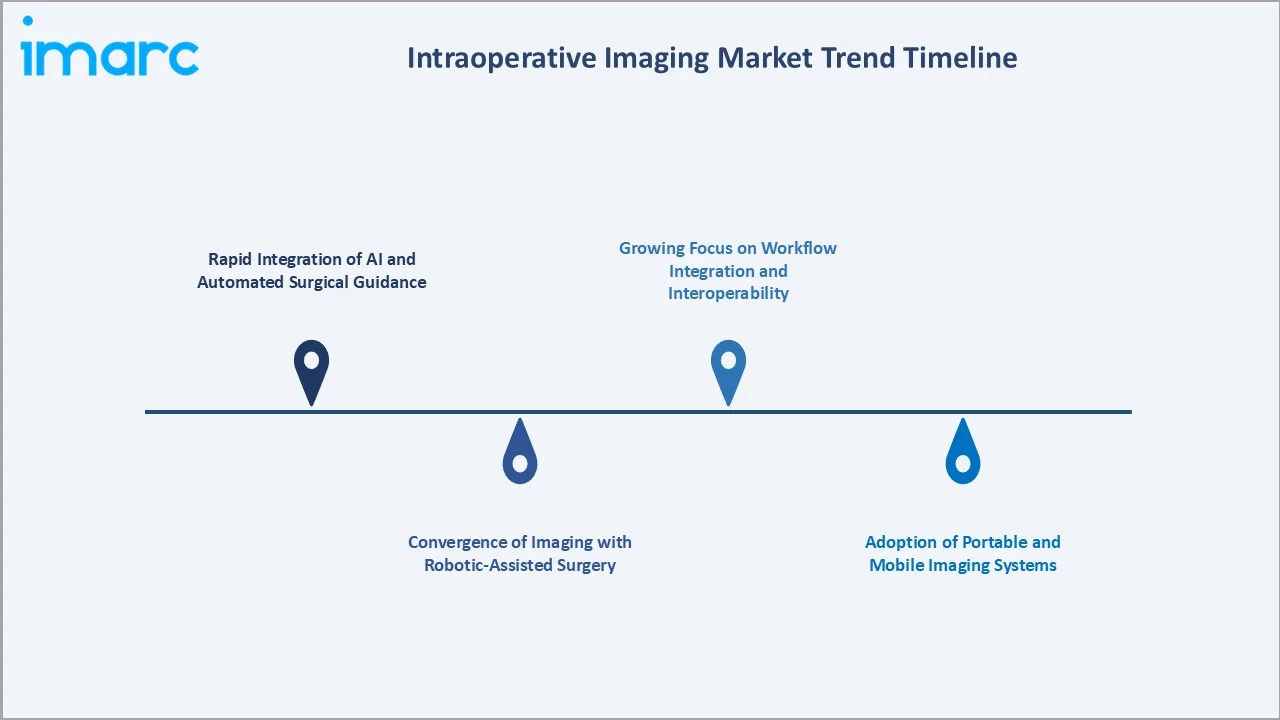

Emerging Market Trends

1. Rapid Integration of AI and Automated Surgical Guidance

In November 2025, Siemens Healthineers AG introduced Optiq AI, an AI-powered imaging chain for its latest interventional systems, designed to deliver high-quality, low-dose images in real time for complex image-guided procedures across cardiology, radiology, and minimally invasive surgery. Approximately 45% of manufacturers launched AI-enabled imaging systems between 2023 and 2025.

2. Convergence of Imaging with Robotic-Assisted Surgery

In September 2025, AiM Medical Robotics Inc. secured USD 8.1 million in Series A financing led by IQ Capital and 1540 Ventures to accelerate development of its MRI‑compatible robotic neurosurgery platform toward first‑in‑human trials. The technology integrates real‑time intraoperative MRI with robotic guidance for precise cranial procedures such as lead placement, biopsies, and targeted therapeutic delivery, aiming to improve safety and accuracy.

3. Adoption of Portable and Mobile Imaging Systems

In November 2024, GE HealthCare unveiled new clinical applications for its OEC 3D mobile C‑arm portfolio, expanding imaging uses beyond traditional orthopedic and trauma procedures to include advanced interventional and airway imaging workflows. The enhancements aim to improve intraoperative imaging quality, versatility, and workflow efficiency across procedures such as bronchoscopy, neuro‑spine, and other minimally invasive interventions.

4. Growing Focus on Workflow Integration and Interoperability

Healthcare providers are prioritizing seamless integration of intraoperative imaging with hospital information systems, EHR, and PACS. Growing adoption of DICOM and HL7 standards enables real-time transmission of intraoperative images to remote specialists. This integration trend is generating additional SaaS imaging analytics and post-procedure image management revenue streams for vendors.

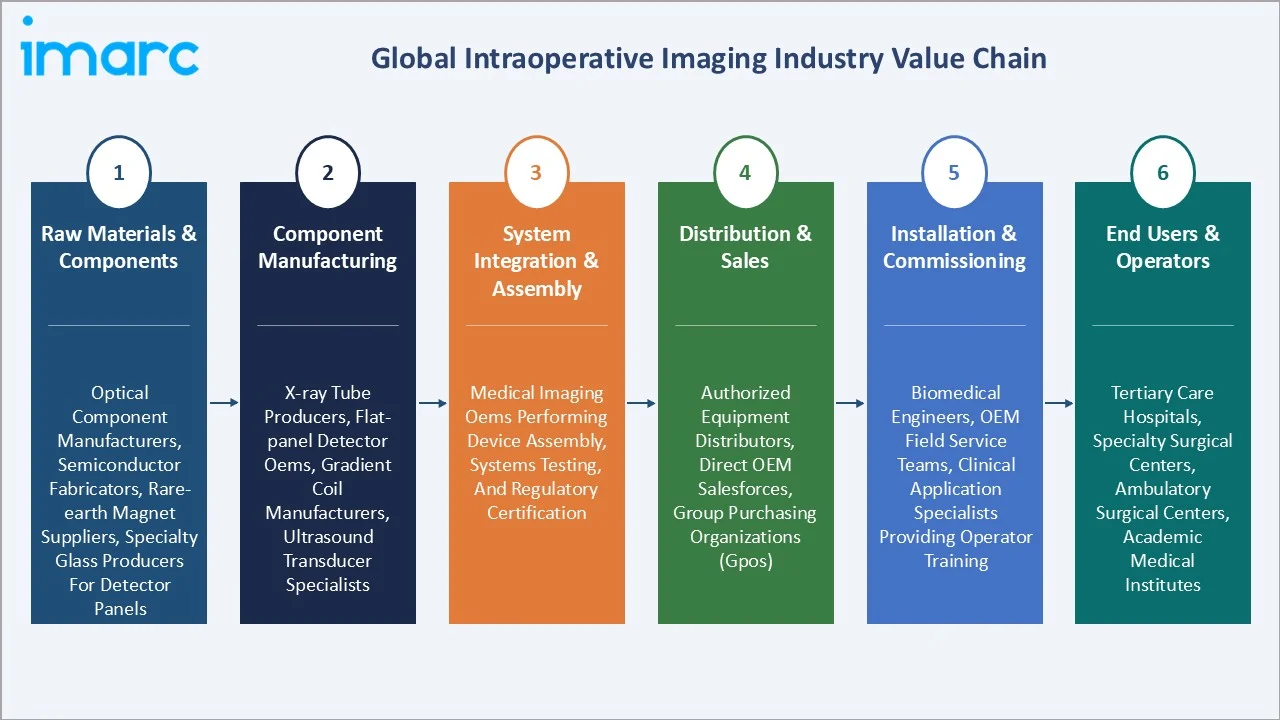

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Optical component manufacturers, semiconductor fabricators, rare-earth magnet suppliers, specialty glass producers for detector panels |

|

Component Manufacturing |

X-ray tube producers, flat-panel detector OEMs, gradient coil manufacturers, ultrasound transducer specialists |

|

System Integration & Assembly |

Medical imaging OEMs performing device assembly, systems testing, and regulatory certification |

|

Distribution & Sales |

Authorized equipment distributors, direct OEM salesforces, group purchasing organizations (GPOs) |

|

Installation & Commissioning |

Biomedical engineers, OEM field service teams, clinical application specialists providing operator training |

|

End Users & Operators |

Tertiary care hospitals, specialty surgical centers, ambulatory surgical centers, academic medical institutes |

Technology Landscape in the Intraoperative Imaging Industry

C-arm Fluoroscopy Systems

C-arm fluoroscopy systems form the technological backbone of the global intraoperative imaging market, offering real-time X-ray imaging across a wide range of surgical applications including orthopedics, spine, cardiovascular, and urology. Modern C-arm platforms incorporate flat-panel digital detectors, 3D cone-beam CT reconstruction capabilities, and AI-assisted image enhancement algorithms that substantially improve diagnostic image quality while reducing radiation dose.

Intraoperative MRI (iMRI) Systems

Intraoperative MRI systems represent the premium segment of the market, providing superior soft-tissue contrast and multi-planar imaging capability essential for neurosurgical procedures. The primary technical challenge for iMRI is compatibility with surgical instrumentation, requiring MRI-conditional anesthesia, monitoring, and surgical tool sets, concentrating adoption in high-volume academic medical centers and specialized neurosurgical hospitals.

Intraoperative CT (iCT) Systems

Intraoperative CT systems provide high-resolution cross-sectional imaging during surgery, enabling surgeons to verify implant positioning, assess surgical margins, and confirm procedural outcomes before wound closure. The O-arm platform from Medtronic has become the reference technology for intraoperative spinal and orthopedic CT imaging, providing both 2D fluoroscopy and 3D CT functionality from a single motorized platform.

Intraoperative Ultrasound (iUltrasound) Systems

Intraoperative ultrasound systems represent the fastest-growing product segment, benefiting from continued advances in transducer miniaturization, image quality improvement, and AI-assisted interpretation. The integration of AI-powered automated target delineation with iUltrasound is substantially reducing operator skill dependency, broadening adoption into clinical settings beyond specialized neurosurgical centers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

C-arm Systems |

39.8% |

2025 |

|

End Use |

Hospitals and Clinics |

67.5% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

North America |

41.2% |

2025 |

By Product

C-arm systems dominate at 39.8% share in 2025. Their versatility across orthopedic, cardiovascular, urological, and spinal disciplines combined with established clinical evidence sustains replacement demand within existing installed bases.

To access detailed market analysis, Request Sample

iMRI at 24.6% holds premium positioning in neurosurgery, delivering unmatched soft-tissue contrast for tumor margin delineation, deep brain stimulation placement, and epilepsy resection procedures. iCT at 19.3% provides cross-sectional imaging for spinal navigation and orthopedic implant verification, with the Medtronic O-arm establishing the clinical standard.

By End Use

Hospitals and clinics command 67.5% share in 2025 as the primary setting for complex surgical procedures requiring dedicated hybrid operating room infrastructure. Ambulatory surgical centers represent 19.8%, the fastest-growing end-use segment driven by migration of elective procedures to outpatient settings.

Academic Institutes and Research Laboratories at 12.7% constitute a strategically important segment that drives early adoption of prototype imaging modalities, augmented reality overlays, and AI-assisted navigation systems, creating a pipeline for commercial diffusion of innovations into mainstream hospital procurement cycles over subsequent years.

Regional Market Insights

North America's market leadership at 41.2% in 2025 reflects advanced surgical infrastructure, comprehensive reimbursement, and concentration of leading medical imaging technology developers anchored by the United States healthcare system.

Asia-Pacific at 22.7% is the most dynamic growth geography. China's hospital construction program, India's Ayushman Bharat investment expanding specialist surgical access, and mature technology-intensive markets in Japan and South Korea maintaining premium imaging system adoption drive above-average regional CAGR.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

41.2% |

Advanced hospital infrastructure, robust reimbursement for image-guided procedures, and concentration of leading imaging technology innovators |

|

Europe |

26.4% |

Strong public health expenditure, leading medical device manufacturers, rising neurosurgery and orthopedic volumes |

|

Asia-Pacific |

22.7% |

Rapid hospital construction in China and India, government healthcare investment, rising surgical volumes, and expanding specialist care access |

|

Latin America |

5.4% |

Growing healthcare budgets, expansion of private hospital chains, rising chronic disease burden, and minimally invasive procedure adoption |

|

Middle East & Africa |

4.3% |

Government-led healthcare modernization in Gulf states, growth of specialized surgical centers, and medical tourism driving premium procurement |

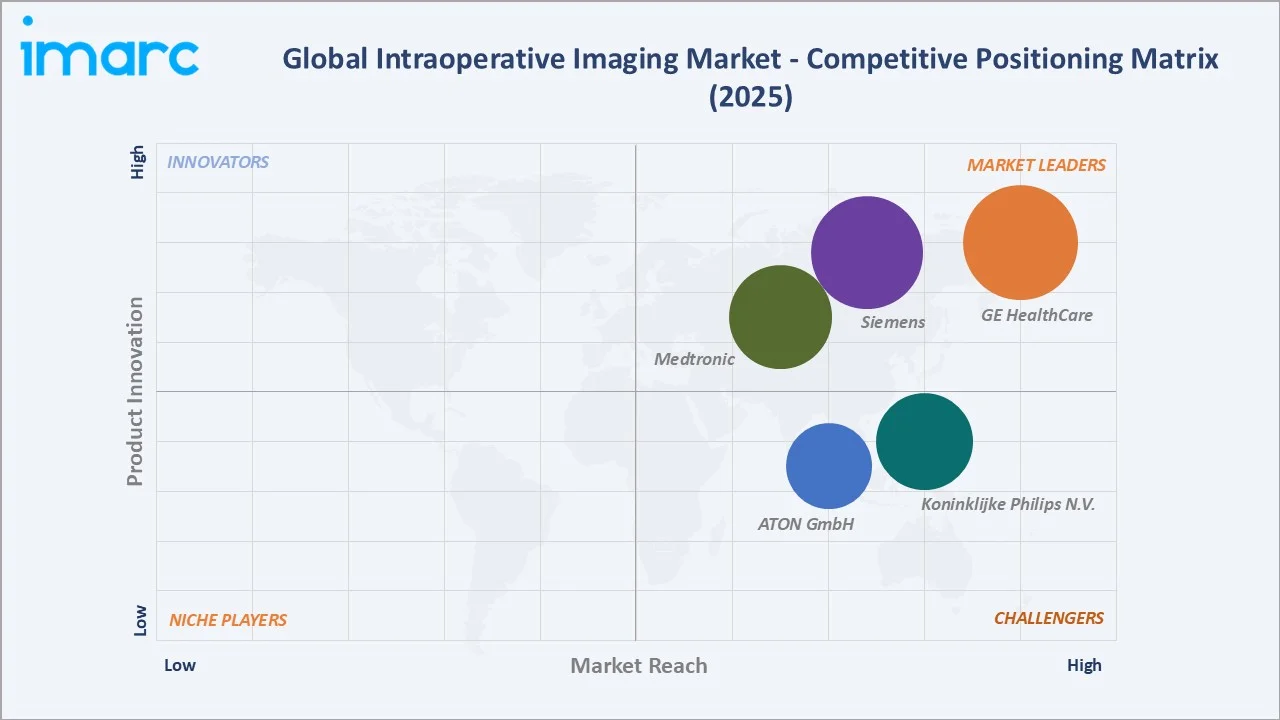

Competitive Landscape

The global intraoperative imaging market exhibits moderate concentration, with GE HealthCare, Siemens, Medtronic, Koninklijke Philips N.V., and ATON GmbH collectively holding approximately 54–58% of total global revenue in 2025. Geographic expansion into high-growth Asia-Pacific and Middle East markets is intensifying, with vendors investing in distribution partnerships and regional manufacturing facilities to capture incremental market share.

| Company Name | Brands/Products | Market Position | Core Strength |

|---|---|---|---|

| GE HealthCare | OEC, Optima, bkFusion, bkActiv, bk3000, bk5000 | Market Leader | Broad C-arm portfolio, AI fluoroscopy innovation, global service network |

| Siemens | MAGNETOM, ARTIS, Cios, Nexaris, SOMATOM | Market Leader | iMRI leadership, AI hybrid OR solutions, advanced 3D imaging |

| Medtronic | O-arm, StealthStation, Mazor | Market Leader | Intraoperative CT navigation, spine surgery leadership |

| Koninklijke Philips N.V. | Azurion, Ingenia, Zenition | Strong Challenger | Cardiovascular imaging, hybrid cathlab integration, AI workflow tools |

| ATON GmbH | Ziehm Vision RFD, Ziehm Solo FD | Strong Challenger | Operating as Ziehm Imaging GmbH, mobile C-arm specialists, orthopedic focus, compact system design |

Market leadership in intraoperative imaging is being actively contested through distinct competitive strategies. First, vendors are pursuing vertical integration across imaging hardware, surgical navigation software, and robotic surgery platforms. Second, AI-driven differentiation is emerging as the primary non-price competitive battleground, with vendors competing on the depth of clinical workflow automation, image enhancement algorithms, and real-time analytics.

Key Company Profiles

GE HealthCare

GE HealthCare is the global leader in intraoperative C-arm imaging systems. Its OEC series C-arms are the benchmark platform for orthopedic and vascular intraoperative fluoroscopy, deployed across the world.

- Product Portfolio: OEC Elite CFD C-arm, Optima IGS series, bkFusion, bkActiv, bk3000, and bk5000.

- Recent Developments: In April 2026, GE HealthCare announced a digital integration between its bkActiv intraoperative ultrasound system and the Medtronic Stealth AXiS surgical navigation system, enabling real‑time ultrasound imaging to be incorporated directly into surgical navigation workflows during cranial procedures.

- Strategic Focus: AI-driven image quality enhancement; expanding portable C-arm share in ASCs; strengthening software recurring revenue.

Siemens

Siemens operates Siemens Healthineers AG as a subsidiary, which is a global leader in medical imaging with a comprehensive intraoperative portfolio spanning iMRI, hybrid OR imaging, and AI-enabled surgical visualization.

- Product Portfolio: MAGNETOM, ARTIS pheno robotic angiography, ARTIS icono hybrid OR system, Cios, Nexaris, and SOMATOM.

- Recent Developments: In March 2024, Siemens Healthineers AG announced FDA clearance of the CIARTIC Move, a self‑driving mobile C‑arm that automates 2D fluoroscopy and 3D cone‑beam CT imaging to speed and standardize intraoperative imaging workflows.

- Strategic Focus: Expanding iMRI accessibility to mid-tier academic centers; AI surgical visualization platform development; hybrid OR robotic integration.

Medtronic

Medtronic is a global healthcare technology leader. The O-arm Surgical Imaging System and StealthStation navigation platform represent the industry standard for intraoperative spinal and orthopedic imaging guidance.

- Product Portfolio: O-arm Surgical Imaging System (2D/3D iCT), StealthStation S8 surgical navigation, Stealth AXiS surgical system, and Mazor X robotic spinal system.

- Recent Developments: In March 2026, Medtronic announced that the U.S. FDA has cleared the Stealth AXiS surgical system for use in cranial and ear, nose, and throat (ENT) procedures, expanding its indication beyond spine surgery and uniting surgical planning, navigation, and robotics for greater precision and real‑time insights.

- Strategic Focus: Deepening imaging-navigation integration in robotic spine surgery; expanding O-arm into emerging markets; AI-based implant positioning.

Market Concentration Analysis

The global intraoperative imaging market exhibits moderate concentration, with the top five global vendors holding approximately 54–58% of total revenue in 2025. Consolidation is driven by strategic acquisition of AI software capabilities and robotic surgery integration competencies by established imaging hardware incumbents.

AI-native entrants focusing on software-only imaging enhancement represent an emerging competitive pressure that large OEMs are countering through internal R&D investment and targeted acquisitions.

Investment and Growth Opportunities

Fastest Growing Segments

iUltrasound (~5.1% CAGR), AI-enabled imaging software platforms (~12–15% CAGR), portable mobile C-arm systems for ASCs (~6.5% CAGR), and robotic surgery-integrated imaging systems (~8% CAGR) represent the highest-growth investment vectors through 2034.

Together, these sub-categories address a combined addressable market of approximately USD 1.8 Billion by 2030, offering attractive entry points for both incumbent vendors expanding portfolios and new entrants with AI-native software capabilities.

Emerging Market Expansion

China, India, Brazil, and the Gulf Cooperation Council collectively represent an incremental USD 500+ Million intraoperative imaging opportunity beyond North America and Europe by 2034. Entry strategies include local manufacturing partnerships to meet domestic content requirements, tiered product strategies offering cost-optimized system variants alongside premium platforms, and direct engagement with government hospital procurement programs.

Venture and Institutional Investment Trends

- AI-powered surgical imaging analytics startups are attracting significant venture investment, with multiple companies raising Series B and C rounds focused on computer vision-based real-time tissue classification, tumor margin delineation, and implant positioning verification during intraoperative procedures.

- Strategic partnerships between imaging OEMs and robotic surgery platform developers are intensifying, creating joint commercialization agreements that bundle imaging and navigation into unified surgical suite solutions sold under multi-year service contracts.

- Imaging-as-a-Service models are emerging where vendors retain system ownership and charge hospitals on a per-procedure basis, reducing capital expenditure barriers and generating recurring revenue streams that command premium total contract values over equipment purchase alternatives.

Future Market Outlook (2026-2034)

The global intraoperative imaging market is positioned for sustained, consistent growth through 2034. From a base of USD 2.49 Billion in 2025, the market is projected to reach USD 3.65 Billion by 2034, representing total incremental value creation of USD 1.16 Billion at a CAGR of 4.22%. This growth is structurally supported by multi-year surgical volume expansion, technology upgrade cycles across existing installed bases, and geographic market penetration across emerging healthcare economies.

The technology transition from conventional C-arm fluoroscopy toward AI-enhanced, multi-modality, and robotic-integrated imaging solutions will define the market composition by 2034. C-arm systems' share is projected to moderate slightly as iUltrasound and integrated robotic imaging systems capture incremental share from new procedure categories.

AI-powered imaging analytics software will represent the fastest-growing revenue component, transitioning from a hardware-bundled feature to a standalone recurring revenue stream. The convergence of intraoperative imaging with augmented reality surgical overlays represents a frontier innovation that could create an entirely new market sub-segment beyond current forecast assumptions through the latter portion of the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants during 2024–2025, including surgical department heads, biomedical procurement specialists, imaging system vendors, and institutional investors across North America, Europe, and Asia-Pacific, validating market sizing assumptions and technology adoption timelines.

Secondary Research

Secondary research encompassed vendor annual reports, FDA 510(k) clearance databases, EU MDR technical documentation, medical device trade publications, academic surgical journals, and institutional investor research on medtech equipment manufacturers.

Forecasting Models

Market size estimations derived using top-down and bottom-up forecasting incorporating procedure volume data by surgical specialty, imaging penetration rates by procedure type and geography, average selling price trajectories, and vendor revenue disclosures. Base-case CAGR of 4.22% reflects consensus estimates validated against announced hospital capital expenditure pipelines through 2034.

Intraoperative Imaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | iCT, iMRI, iUltrasound, C-arm systems |

| Applications Covered | Neurosurgery, Orthopedic Surgery, ENT Surgery, Oncology Surgery, Trauma Surgery/Emergency Room, Cardiovascular, Others |

| End Uses Covered | Hospitals And Clinics, Ambulatory Surgical Centers, Academic Institutes and Research Laboratories |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | GE HealthCare, Siemens, Medtronic, Koninklijke Philips N.V., ATON GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the intraoperative imaging market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global intraoperative imaging market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the intraoperative imaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Intraoperative Imaging Market Report

The global intraoperative imaging market reached USD 2.49 Billion in 2025.

The market is projected to grow at a CAGR of 4.22%, reaching USD 3.65 Billion by 2034.

Key drivers include rising global surgical volumes, accelerating adoption of minimally invasive and robotic-assisted surgery, AI integration in imaging platforms, and growing chronic disease prevalence requiring surgical intervention.

C-arm systems dominate with a 39.8% share in 2025, owing to clinical versatility across orthopedic, cardiovascular, and spinal disciplines.

iUltrasound is the fastest-growing segment at approximately ~5.1% CAGR during 2026–2034, driven by miniaturization advances and AI-enabled image interpretation.

Hospitals and clinics lead with a 67.5% share in 2025, serving as the primary setting for complex surgical procedures.

North America dominates at 41.2% in 2025, driven by advanced hospital infrastructure, comprehensive reimbursement, and high AI-enabled imaging technology adoption.

Asia-Pacific at 22.7% is the fastest-growing region, driven by hospital construction in China, India's healthcare investment, and rising surgical procedure volumes.

Major players include GE HealthCare, Siemens, Medtronic, Koninklijke Philips N.V., and ATON GmbH.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)