IoT Security Market Size, Share, Trends and Forecast by Component, Security Type, Vertical, and Region, 2026-2034

Global IoT Security Market Size, Share, Trends & Forecast (2026-2034)

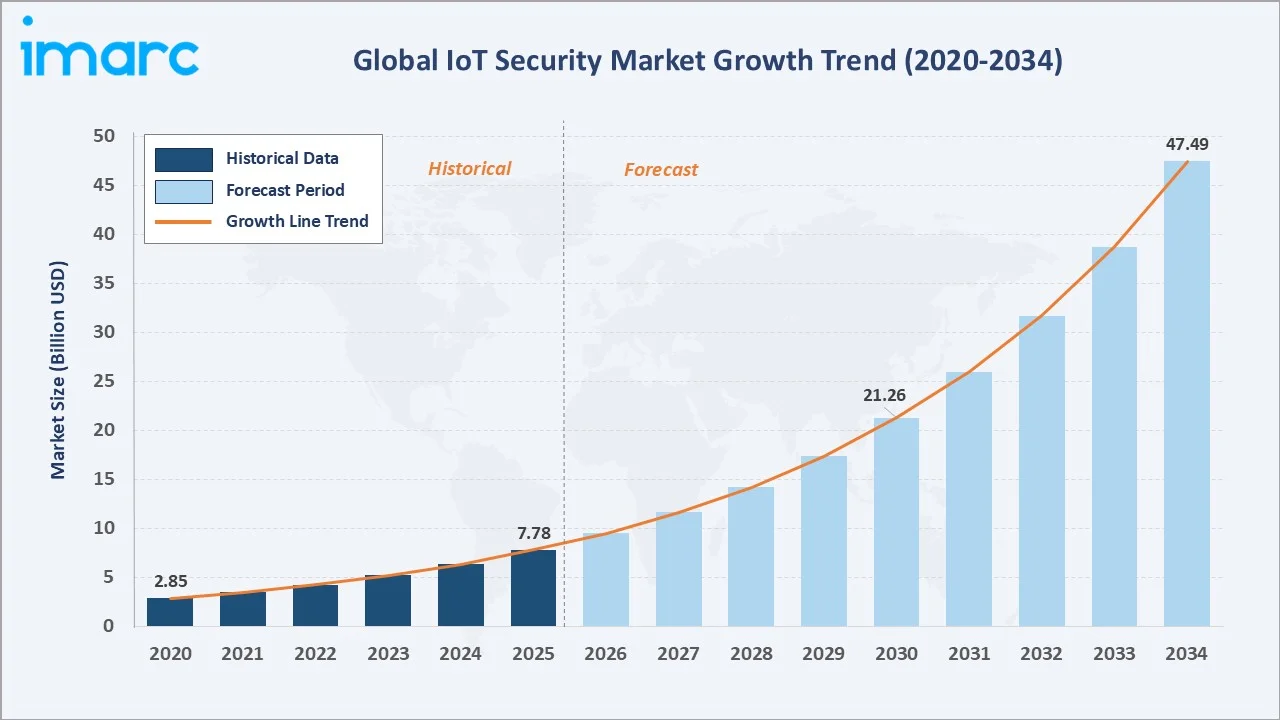

The global IoT security market size was valued at USD 7.78 Billion in 2025 and is projected to reach USD 47.49 Billion by 2034, exhibiting a CAGR of 22.25% during the forecast period 2026-2034. Rapid proliferation of connected devices, escalating cyberattack incidents, expanding cloud workloads, and stricter regulatory mandates are driving the IoT security market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.78 Billion |

|

Forecast Market Size (2034) |

USD 47.49 Billion |

|

CAGR (2026-2034) |

22.25% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

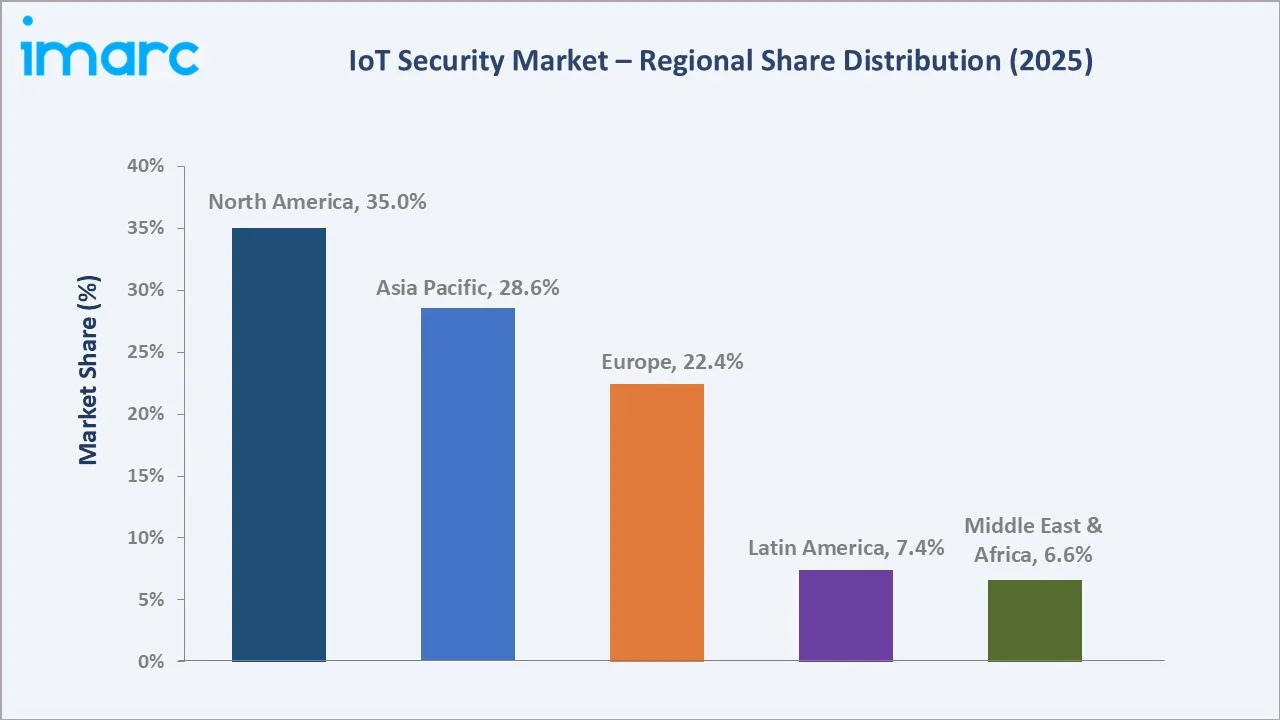

North America (35.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~24.1%) |

|

Leading Component |

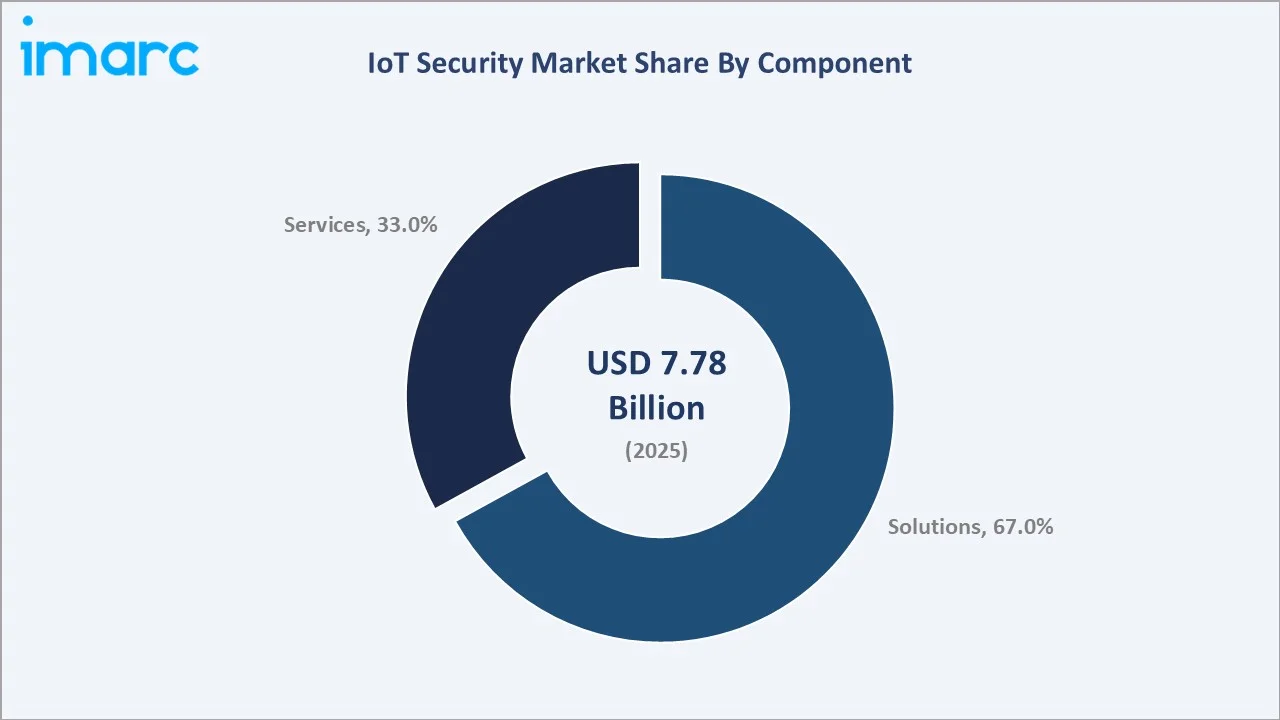

Solutions (67.0%, 2025) |

|

Leading Security Type |

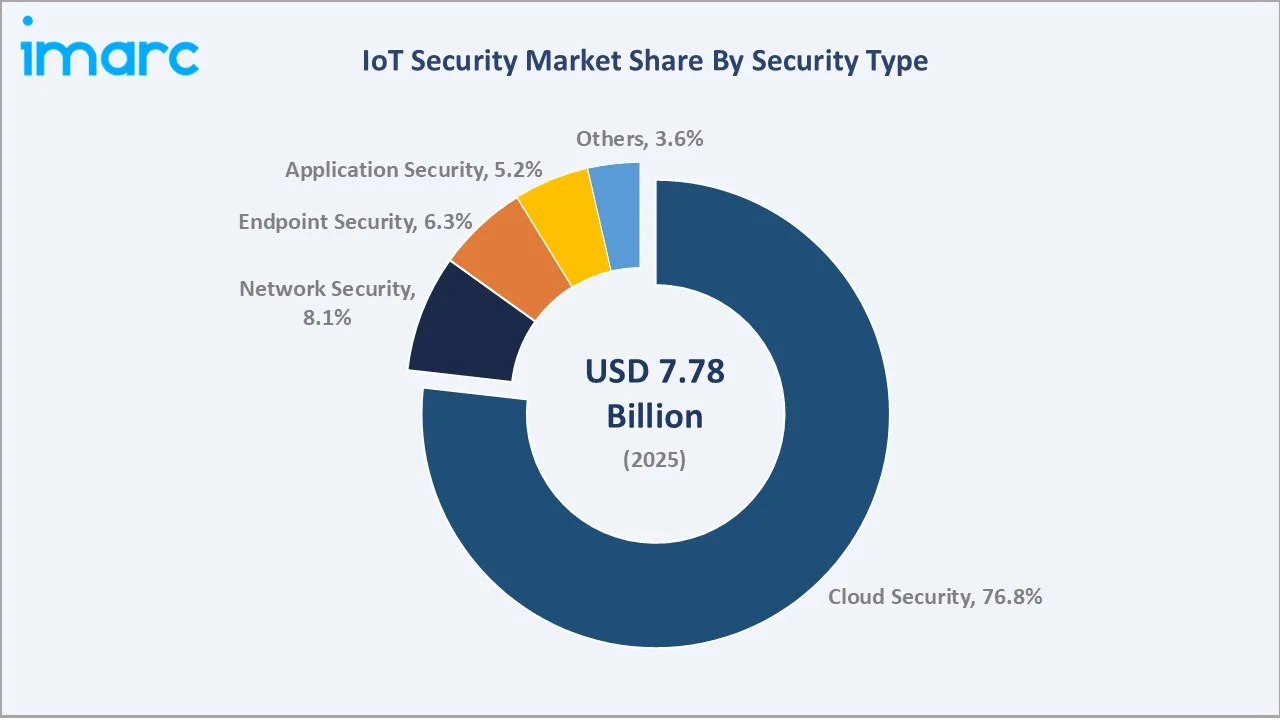

Cloud Security (76.8%, 2025) |

The global IoT security market growth trajectory from 2020 through 2034 shows sustained double-digit expansion, driven by accelerating device connectivity, enterprise digital transformation, and tightening cybersecurity legislation across both developed and emerging economies.

To get more information on this market, Request Sample

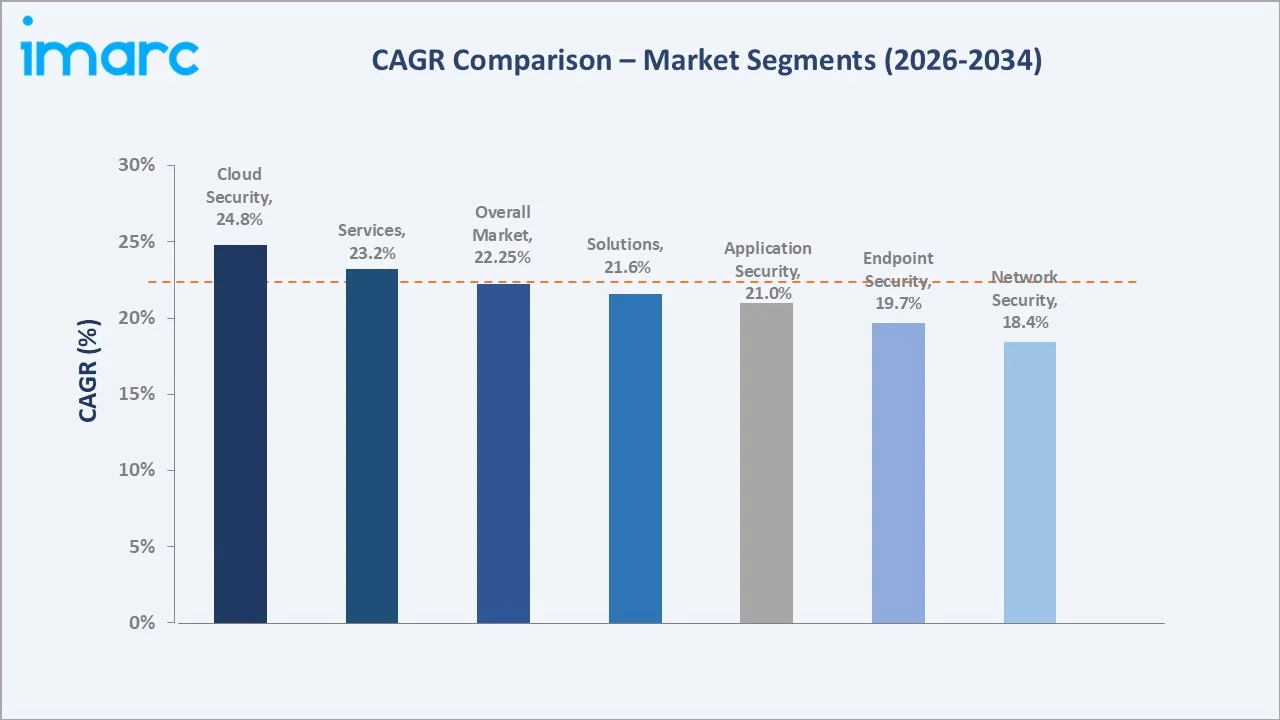

Segment-level CAGR comparisons show Cloud Security and Services leading growth rates within the broader IoT security market forecast through 2034, reflecting enterprise shifts to cloud-native architectures and managed security subscriptions.

Executive Summary

The global IoT security market is undergoing rapid expansion. Growth is driven by exponential device proliferation, rising cyber-threat severity, and regulatory mandates. Valued at USD 7.78 Billion in 2025, the market is forecast to reach USD 47.49 Billion by 2034 at a CAGR of 22.25%.

Solutions commands 67.0% share in 2025, anchored by endpoint protection platforms, identity modules, and IoT-aware firewalls. Services is propelled by managed detection, consulting, and integration engagements. Cloud Security represents 76.8% of demand by security type, while Network, Endpoint, and Application Security collectively account for approximately 19.6% in 2025.

North America leads with 35.0% global revenue share in 2025. Asia Pacific holds 28.6% and Europe 22.4%. The IoT security market outlook remains strongly positive as zero-trust adoption, AI-driven threat detection, and post-quantum cryptography readiness converge across enterprise, industrial, and consumer deployments.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Solutions – 67.0% share (2025) |

|

Second Component |

Services – 33.0% share (2025) |

|

Largest Security Type |

Cloud Security – 76.8% share (2025) |

|

Fastest Growing Security Type |

Cloud Security – ~24.8% CAGR (2026-2034) |

|

Leading Region |

North America – 35.0% revenue share (2025) |

|

Top Companies |

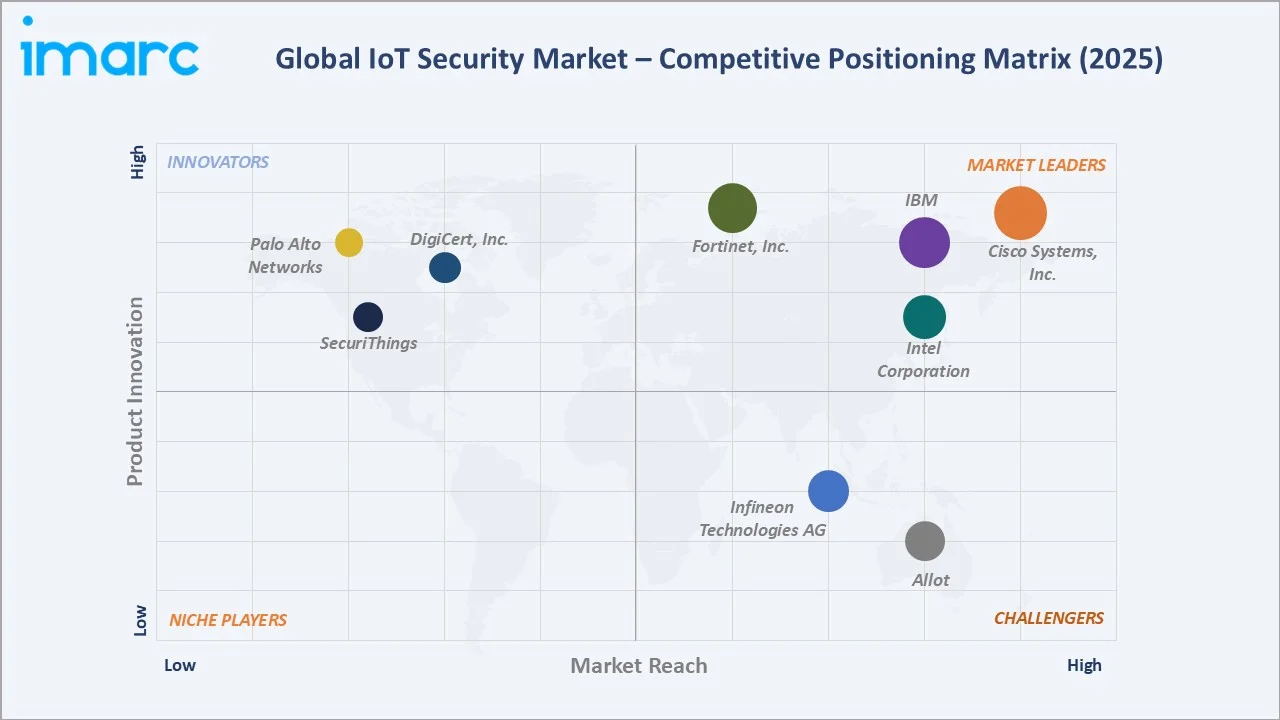

Cisco Systems, Inc., IBM, Intel Corporation Fortinet, Inc., Infineon Technologies AG, Allot, SecuriThings, DigiCert, Inc., Palo Alto Networks |

|

Connected IoT Device Base |

21.1 billion devices (2025) |

Key Analytical Observations Supporting The Above Data:

- Solutions' 67.0% dominance in 2025 reflects enterprise preference for integrated platforms that bundle device discovery, identity management, encryption, and runtime protection into a single pane of glass.

- Services' 33.0% share is underpinned by rising demand for managed detection and response, penetration testing, and compliance advisory as internal security teams struggle to scale alongside device growth.

- Cloud Security's 76.8% majority is driven by the migration of IoT workloads to hyperscaler platforms. AWS IoT Device Defender, Azure Defender for IoT, and Google Cloud IoT Core expansions are accelerating this concentration.

- North America's 35.0% global lead reflects early enterprise adoption, the U.S. IoT Cybersecurity Improvement Act of 2020, and large federal cybersecurity allocations exceeding USD 13 Billion in FY2025 appropriations.

- IoT attack surface expansion — connected devices surpassed 21.1 billion in 2025, with ransomware and firmware-level exploits growing sharply, pushing enterprises to embed security at the edge and throughout the device lifecycle.

- Regulatory acceleration — the EU Cyber Resilience Act (2024), U.S. FDA IoMT guidance, and Singapore's Cybersecurity Labelling Scheme are standardizing baseline IoT security requirements globally.

Global IoT Security Market Overview

IoT security encompasses the tools, processes, and services that protect connected devices, networks, data flows, and cloud endpoints across consumer, enterprise, and industrial environments. The market covers device identity and authentication, encryption, secure boot, firmware integrity, network segmentation, threat detection, and compliance management across heterogeneous hardware and protocols.

The industry sits at the convergence of cloud computing, AI-driven analytics, regulatory compliance, and connected-device economics. Growth is supported by macroeconomic drivers such as enterprise digitalization, Industry 4.0 capital expenditure, healthcare modernization, and smart-city infrastructure investment. Simultaneously, the market is undergoing a structural shift toward zero-trust architectures, edge-native protection, and automated security operations, which are redefining how organizations deploy and govern IoT at scale.

Market Dynamics

To evaluate market opportunities, Request Sample

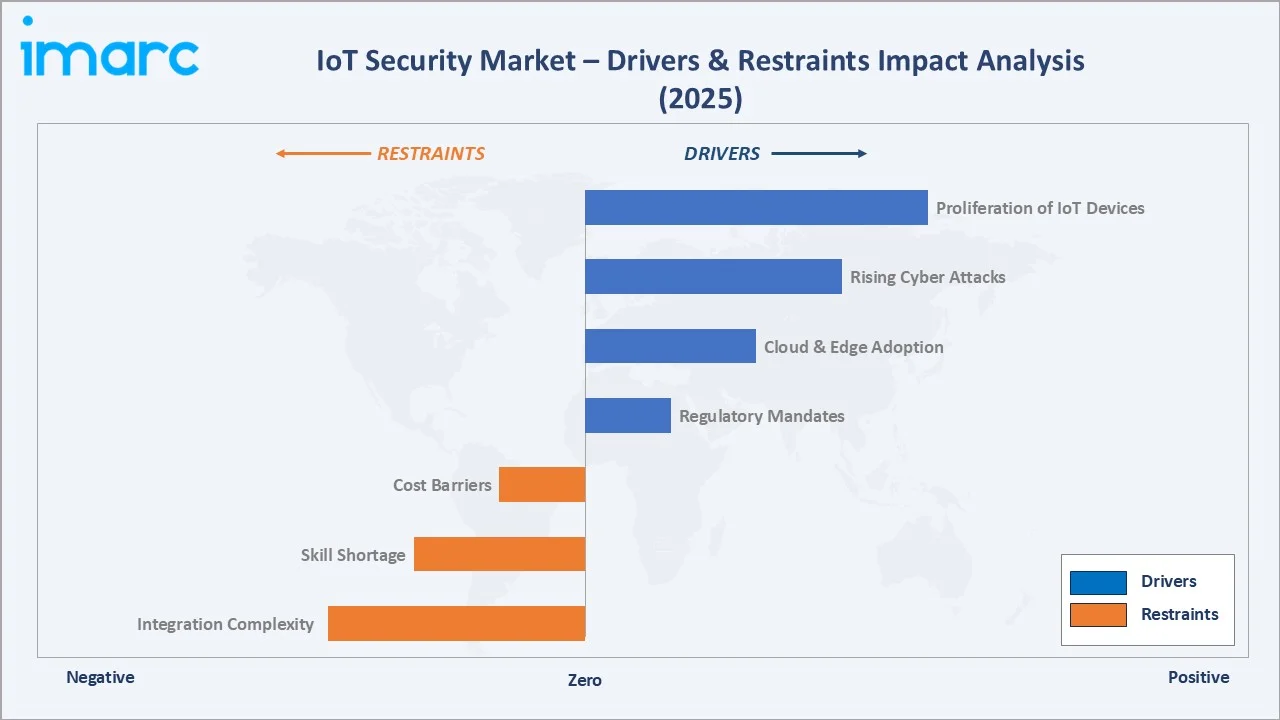

Market Drivers

- Proliferation of Connected Devices: In 2025, Number of connected IoT devices growing 14% to 21.1 billion globally according to IoT Analytics, with annual additions projected to exceed 6 billion units by 2030. Each unsecured endpoint multiplies the enterprise attack surface, driving structural demand for identity, encryption, and monitoring solutions.

- Rising Cyber-Attack Severity: IoT-targeted malware incidents grew more than 400% between 2023 and 2025, per SonicWall's 2025 threat report. High-profile events such as ransomware on industrial controllers and botnets leveraging unsecured cameras have pushed boardroom-level prioritization of IoT cybersecurity.

- Cloud and Edge Workload Adoption: Enterprise migration of IoT workloads to hyperscale cloud platforms is accelerating the growth of Cloud Security. A significant share of enterprise IoT data is expected to be processed at the edge or in the cloud in the coming years, necessitating the adoption of advanced protection architectures.

- Regulatory Mandates: The EU Cyber Resilience Act, the U.S. IoT Cybersecurity Improvement Act, and Singapore's Cybersecurity Labelling Scheme are standardizing baseline controls. In January 2025, the U.S. launched the U.S. Cyber Trust Mark program, creating further procurement pull for compliant devices.

Market Restraints

- Integration Complexity: Diverse IoT protocols and legacy OT systems complicate unified security deployment and extend project timelines.

- Cybersecurity Skill Shortage: ISC2 reported a global cybersecurity workforce gap of approximately 4.8 million professionals in 2024, limiting the pace at which enterprises can implement and operate IoT security programs.

- Cost Barriers for SMEs: Smaller enterprises face hardware refresh costs, subscription fees, and specialist service expenses that slow adoption relative to large-enterprise buyers.

Market Opportunities

- Zero-Trust IoT Architectures: Government and enterprise mandates for zero-trust network access are extending into IoT, creating greenfield demand for micro-segmentation, continuous authentication, and identity-based policy enforcement across device fleets.

- Industrial IoT and OT Convergence: Manufacturing, energy, and utilities operators are investing heavily in OT-aware security platforms. IIoT security spending is projected to grow significantly in the coming years, driven by pipeline, grid, and discrete manufacturing modernization programs.

- AI-Powered Threat Detection: Machine-learning models that baseline normal device behavior and flag anomalies are moving from pilots to production, with vendors bundling AI capabilities into standard subscriptions and expanding addressable pricing tiers.

Market Challenges

- Fragmented Standards Landscape: Overlapping certifications — ETSI EN 303 645, NIST IR 8425, and regional labelling schemes — force vendors into duplicative compliance efforts, raising go-to-market costs and slowing product rollout.

- Legacy Device Security Gaps: A large installed base of devices with limited compute, no firmware update path, and hard-coded credentials cannot be retrofitted, creating persistent risk that pushes organizations toward network-layer and compensating controls.

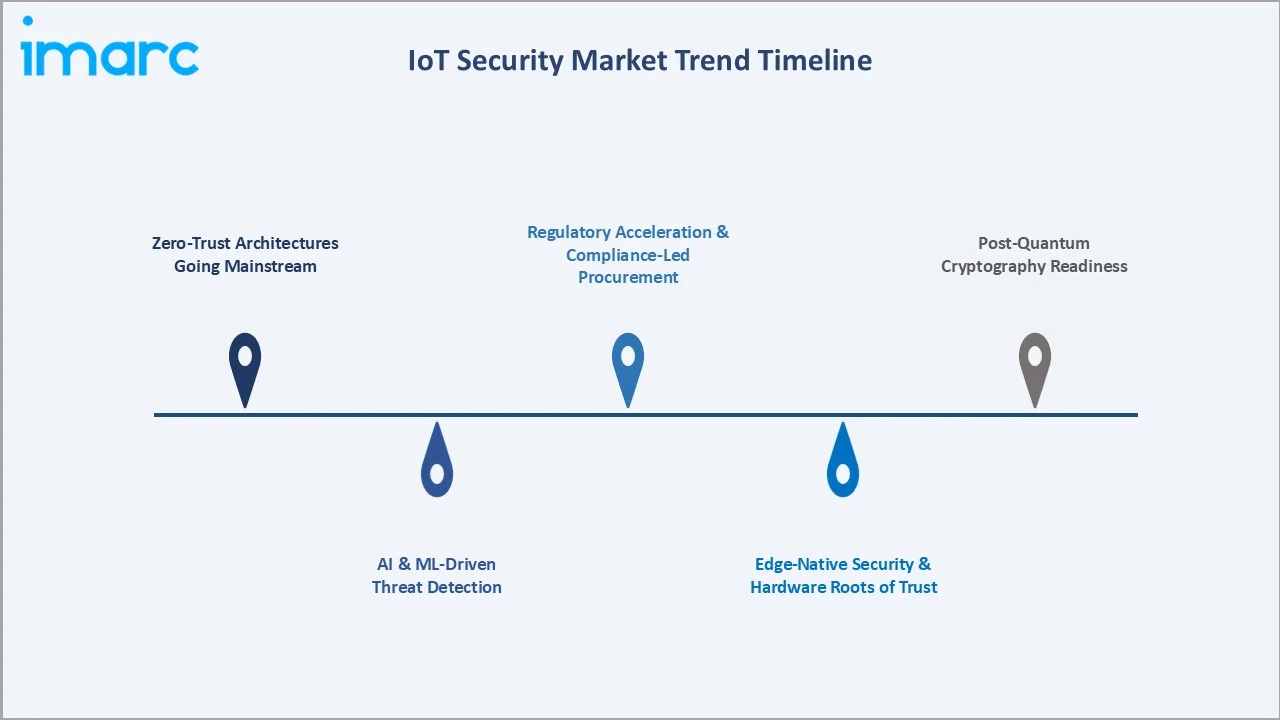

Emerging Market Trends

1. Zero-Trust Architectures Going Mainstream

Zero-trust frameworks are replacing perimeter-based models as the default posture for IoT deployments. Enterprises are adopting identity-centric access, continuous verification, and micro-segmentation to contain lateral movement. Regulators in the U.S. and EU are nudging critical infrastructure operators toward zero-trust baselines through 2028.

2. AI and Machine-Learning-Driven Threat Detection

AI-enabled security analytics are transitioning from add-ons to standard capabilities. Vendors embed behavioral baselining, anomaly detection, and automated response into IoT security platforms. This shift is reducing mean-time-to-detect for attacks on industrial controllers, medical devices, and connected vehicles.

3. Edge-Native Security and Hardware Roots of Trust

Security is moving closer to the device through hardware roots of trust, secure elements, and trusted execution environments. Chipmakers such as Intel, Infineon, and Arm are embedding cryptographic accelerators in IoT-grade silicon, enabling stronger identity, secure boot, and over-the-air update integrity at scale.

4. Regulatory Acceleration and Compliance-Led Procurement

Emerging regulations are reshaping procurement. The EU Cyber Resilience Act and the U.S. Cyber Trust Mark introduce mandatory security baselines and labelling. Buyers increasingly treat compliance certifications as table stakes, favoring vendors with pre-certified portfolios and clear vulnerability disclosure processes.

5. Post-Quantum Cryptography Readiness

With NIST finalizing post-quantum cryptography standards in 2024, IoT vendors are piloting quantum-safe key exchange and signature schemes. Early adopters in defense, finance, and critical infrastructure are planning hybrid deployments through 2030 to protect long-lifecycle devices from future quantum-capable adversaries.

Industry Value Chain Analysis

The global IoT security industry value chain spans six integrated stages from hardware components through end-user deployment. Each stage presents distinct competitive dynamics, margin profiles, and R&D investment intensity relevant to the overall IoT security market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Hardware Components |

Secure elements, trusted platform modules, cryptographic accelerators, IoT-grade MCUs |

|

Security Software |

Firmware protection, device identity, encryption libraries, endpoint agents – produced by platform vendors and specialist ISVs |

|

Platform Integration |

Unified IoT security platforms integrating discovery, monitoring, policy and response – Cisco Systems, Inc., IBM, Intel Corporation Fortinet, Inc., Infineon Technologies AG |

|

Deployment & Managed Services |

Systems integrators, MSSPs and MDR providers delivering design, rollout, SOC, and incident response services |

|

Compliance & Monitoring |

Continuous monitoring, audit, certification support aligned to NIST, ETSI EN 303 645, EU CRA, ISA/IEC 62443 |

|

End Users |

Enterprises and public bodies across manufacturing, energy & utilities, healthcare, transport, consumer electronics and government |

Platform integrators capture the highest strategic value by combining chips, software, analytics, and services into turnkey offerings. Meanwhile, managed security providers and cloud hyperscalers are reshaping distribution, enabling customers to consume IoT security as a subscription and shift from CapEx to OpEx models.

Technology Landscape in the IoT Security Industry

Device Identity and Hardware Roots of Trust

Hardware-anchored identity is becoming the foundation of modern IoT security. Secure elements, trusted platform modules, and physically unclonable functions are being embedded in IoT-grade silicon. Leading chipmakers are shipping pre-provisioned certificates at the fab, enabling automated onboarding, secure boot, and tamper resistance across device fleets.

Cloud-Native Security and Zero-Trust Enforcement

Cloud-delivered IoT security platforms are scaling rapidly, integrating device discovery, policy enforcement, and telemetry analytics. AWS IoT Device Defender, Azure Defender for IoT, and Google Cloud IoT Device Management are expanding breadth. Zero-trust frameworks are applied at the device and session level, replacing static network trust with continuous, identity-based verification.

AI-Driven Threat Detection and Response

Machine-learning models baseline normal device behavior, detect deviations, and initiate containment actions. Vendors now bundle AI capabilities into standard subscriptions, supporting anomaly detection across millions of endpoints. Automated playbooks reduce mean-time-to-respond, compensating for persistent cybersecurity workforce shortages.

Post-Quantum Cryptography and Next-Gen Encryption

Post-quantum algorithms standardized by NIST in 2024 are moving from labs into pilots. Hybrid schemes that combine classical and quantum-safe primitives are being tested for long-lifecycle assets in defense, finance, and critical infrastructure. Chipmakers are beginning to hardware-accelerate lattice-based algorithms in upcoming IoT silicon families.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solutions |

67.0% |

2025 |

|

Security Type |

Cloud Security |

76.8% |

2025 |

|

Vertical |

Energy and Utilities |

20.1% |

2025 |

|

Region |

North America |

35.0% |

2025 |

By Component

To access detailed market analysis, Request Sample

Solutions lead the global IoT security market component mix with a 67.0% share in 2025, translating to approximately USD 5.21 Billion in revenue. Demand is driven by enterprise adoption of unified IoT security platforms that consolidate device identity, encryption, firewall, and threat management into a single stack. Cloud-delivered subscription models are expanding average contract values, and bundled hardware-plus-software offerings from chipmakers are accelerating adoption in industrial and healthcare verticals.

By Security Type

Cloud Security is the dominant security type at 76.8% of global revenue in 2025, equivalent to approximately USD 5.97 Billion. Growth is underpinned by the migration of IoT workloads to AWS, Azure, and Google Cloud, coupled with adoption of cloud-native security posture management tools. The segment is forecast to advance at ~24.8% CAGR through 2034, reflecting multi-cloud IoT deployments and the embedding of security into hyperscaler IoT platforms.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

35.0% |

U.S. IoT Cybersecurity Improvement Act, federal cyber budgets exceeding USD 13 Billion (FY2025), U.S. Cyber Trust Mark (2025), zero-trust mandates |

|

Asia Pacific |

28.6% |

China smart manufacturing programs, India Smart Cities Mission, Japan IoT safety guidelines, Singapore Cybersecurity Labelling Scheme |

|

Europe |

22.4% |

EU Cyber Resilience Act (2024), NIS2 Directive, GDPR alignment, Industry 4.0 investment across Germany, France and the Nordics |

|

Latin America |

7.4% |

Brazil LGPD enforcement, Mexico manufacturing near-shoring, smart-utility rollouts across Chile and Colombia |

|

Middle East & Africa |

6.6% |

UAE National Cybersecurity Strategy, Saudi Arabia Vision 2030 smart-city projects (NEOM), South Africa POPIA compliance |

North America commands 35.0% global revenue share in 2025. The United States is the single most important national market, combining the world's largest enterprise cybersecurity spend with a deep vendor ecosystem. The U.S. IoT Cybersecurity Improvement Act and the launch of the U.S. Cyber Trust Mark in January 2025 are accelerating labelled-device procurement.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Cisco Systems, Inc. |

Cisco Cyber Vision, Secure Firewall, Talos |

Leader |

Deep OT visibility, networking + security integration, enterprise reach |

|

IBM |

QRadar, IBM Security Verify |

Leader |

AI-driven SIEM, identity platform, global services footprint |

|

Intel Corporation |

vPro |

Leader |

Silicon-level roots of trust, OEM partnerships, edge compute |

|

Fortinet, Inc. |

FortiGuard, FortiNAC, FortiGate |

Leader |

Integrated Security Fabric, OT/IoT segmentation, global channel |

|

Infineon Technologies AG |

OPTIGA Trust |

Challenger |

Secure MCU leadership, automotive & industrial silicon strength |

|

Allot |

NetworkSecure |

Challenger |

Carrier-grade IoT visibility and security-as-a-service for telcos |

|

SecuriThings |

Horizon IoTOps |

Emerging |

Physical security device management and automated compliance |

|

DigiCert, Inc. |

Mocana TrustCore |

Emerging |

Embedded device security, PKI for industrial and automotive |

|

Palo Alto Networks |

IoT Security |

Emerging |

AI-based device discovery and behavioral analytics |

The global IoT security market's competitive landscape is moderately fragmented, with global cybersecurity platform vendors competing alongside chip-level incumbents and specialist IoT-security pure-plays. Leading players compete on platform breadth, AI capabilities, compliance certifications, cloud integrations, and channel reach.

Key Company Profiles

Cisco Systems, Inc.

Cisco Systems Inc. is global technology company specializing in networking, cybersecurity, and digital communications solutions. Headquartered in San Jose, California, Cisco plays a central role in enabling internet infrastructure and enterprise connectivity worldwide.

- Product & Platform Portfolio: Cisco's IoT security portfolio spans Cisco Cyber Vision for OT visibility, Secure Firewall for network segmentation, Identity Services Engine (ISE) for device profiling, and Talos threat intelligence integrated across its Security Cloud.

- Recent Developments: In 2025, Cisco introduced major advancements in Industrial IoT security, highlighting the growing need to protect complex OT environments. The company unveiled AI-powered cybersecurity capabilities within its industrial networking portfolio, including enhanced visibility and automated threat detection through its Cyber Vision platform.

- Strategic Focus: Cisco Systems Inc’s strategy centers on converging networking and security under a single AI-driven platform, accelerating OT visibility in manufacturing and critical infrastructure, and extending zero-trust enforcement across hybrid IoT estates.

IBM

IBM is a global technology and consulting firm headquartered in Armonk, New York. Founded in 1911, IBM operates across cloud, AI, and cybersecurity, with IoT security delivered through IBM Security, IBM Consulting, and its hybrid cloud offerings.

- Product & Platform Portfolio: IBM's IoT security portfolio includes QRadar SIEM and XDR, MaaS360 for unified endpoint management, Guardium for data protection, and IBM Security Verify for identity and access. The portfolio is tightly integrated with IBM watsonx AI services.

- Recent Developments: In 2025, IBM has introduced new agentic AI-driven capabilities to strengthen IoT and enterprise security operations, focusing on automation and predictive threat intelligence. The company’s solution enables autonomous security operations by automating threat detection, investigation, and response, helping organizations address increasingly complex and persistent cyber threats.

- Strategic Focus: IBM's focus is on AI-driven security operations, regulated-industry solutions for healthcare and BFSI, and large-scale managed services engagements leveraging its global consulting footprint.

Intel Corporation

Intel Corporation is a global semiconductor company headquartered in Santa Clara, California. Founded in 1968, Intel is a leading supplier of compute silicon, including CPU, edge, and IoT-focused processor families, with a growing portfolio of hardware-level security capabilities.

- Product & Platform Portfolio: Intel's IoT security offerings include Intel vPro, Software Guard Extensions (SGX), Intel Secure Device Onboard (SDO) for zero-touch provisioning, and Trust Domain Extensions (TDX) for confidential computing across edge and cloud deployments.

- Recent Developments: In 2025, Intel unveiled major enhancements to its vPro platform, emphasizing stronger security for enterprise and IoT-connected environments. The updated platform integrates hardware-based security directly at the silicon level, enabling protection below the operating system and improving resilience against advanced cyber threats.

- Strategic Focus: Intel Corporation’s strategy emphasizes silicon-rooted security for edge and IoT, ecosystem partnerships with OEMs and cloud providers, and leadership in confidential computing to secure AI and IoT workloads end-to-end.

Market Concentration Analysis

The global IoT security market exhibits moderate fragmentation. The top five players - Cisco Systems, Inc., IBM, Intel Corporation, Fortinet, Inc., Infineon Technologies AG - collectively account for 32-38% of global market revenue in 2025.

The market is experiencing a bifurcated dynamic. Large platform vendors are consolidating capabilities through acquisitions and AI-led integration, while a vibrant group of specialist vendors continues to differentiate on vertical depth — for example, Armis in healthcare and manufacturing, or SecuriThings in physical security. Cloud hyperscalers are also encroaching on the stack with native IoT security services, intensifying competition across all pricing tiers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Cloud Security is the highest-growth security type at approximately 24.8% CAGR through 2034. Services is the fastest-growing component tier at 23.2% CAGR, driven by managed detection and response adoption. AI-powered threat analytics represents the premium technology growth lane, with enterprise subscriptions expanding rapidly as organizations replace legacy SIEMs with IoT-aware platforms.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by Smart Cities Mission deployments, enforcement of the Digital Personal Data Protection Act, and rapid enterprise cloud adoption. Southeast Asia's manufacturing base, GCC smart-city programs including NEOM, and Brazil's LGPD enforcement collectively create significant multi-year opportunities for vendors with localized delivery capabilities.

Venture and Strategic Investment Trends

Strategic acquisitions continue to reshape the landscape. Cisco completed its USD 28 Billion acquisition of Splunk in March 2024, strengthening integrated security operations. In 2024-2025, venture capital has concentrated on AI-driven IoT detection, OT/ICS security, confidential computing, and post-quantum cryptography readiness — the priority themes for corporate and financial investors through 2030.

Future Market Outlook (2026-2034)

The global IoT security market forecast projects rapid value expansion from USD 7.78 Billion in 2025 to USD 47.49 Billion by 2034 at a CAGR of 22.25%. North America will retain regional leadership on the back of federal cybersecurity investment, while Asia Pacific is expected to post the fastest growth at approximately 24.1% CAGR through 2034.

Three structural shifts will reshape the IoT security market through 2034. Zero-trust architectures will become the default for enterprise IoT deployments, making identity and continuous verification standard by 2028. AI-driven detection and automated response will transform security operations, reducing dependence on scarce cybersecurity talent. Meanwhile, post-quantum cryptography trials will mature into production rollouts in defense, finance, and critical infrastructure by 2030, safeguarding long-lifecycle IoT assets against future quantum-era threats.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with IoT security industry stakeholders, including CISOs and security architects at enterprise adopters, product leaders at platform vendors, channel executives at managed security service providers, and procurement leads at government agencies. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include IoT Analytics device installed-base reports, NIST and ENISA technical publications, U.S. federal cybersecurity appropriations records, EU Cyber Resilience Act and NIS2 documentation, ISC2 workforce studies, trade publications including Dark Reading, SC Magazine, and IoT World Today, and company annual reports and investor presentations.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating connected-device installed-base data, cybersecurity budget growth rates, regulatory milestone timelines, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic and regulatory uncertainty.

IoT Security Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solutions, Services |

| Security Types Covered | Network Security, Endpoint Security, Application Security, Cloud Security, Others |

| Verticals Covered | Energy and Utilities, Manufacturing, Automotive, Transport, Consumer Electronics, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others, Turkey, Saudi Arabia, Iran, United Arab Emirates, Others |

| Companies Covered | Cisco Systems, Inc., IBM, Intel Corporation, Fortinet, Inc., Infineon Technologies AG, Allot, SecuriThings, DigiCert, Inc., Palo Alto Networks, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, IoT security market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global IoT security market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the IoT security industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the IoT Security Market Report

The global IoT security market was valued at USD 7.78 Billion in 2025, driven by rapid device proliferation, escalating cyber threats, and tightening regulatory mandates across major economies worldwide.

The market is projected to reach USD 47.49 Billion by 2034, advancing at a CAGR of 22.25% during 2026-2034, supported by zero-trust adoption, AI-driven detection, and cloud migration.

Solutions lead the market with a 67.0% share in 2025, driven by enterprise adoption of integrated platforms that unify device identity, encryption, firewall, and threat-management capabilities.

Cloud Security holds the largest share at 76.8% in 2025, reflecting enterprise migration of IoT workloads to AWS, Azure, and Google Cloud and rapid uptake of cloud-native protection tools.

North America dominates with a 35.0% share in 2025, driven by federal cybersecurity spending, U.S. IoT legislation, and a deep enterprise and defense security vendor ecosystem.

Key drivers include exponential device proliferation, rising cyber-attack severity, cloud and edge adoption, zero-trust mandates, the EU Cyber Resilience Act, and the U.S. Cyber Trust Mark program.

Major players include Cisco Systems, Inc., IBM, Intel Corporation, Fortinet, Inc., Infineon Technologies AG, Allot, SecuriThings, DigiCert, Inc., and Palo Alto Networks.

Cloud Security is the fastest-growing segment, advancing at approximately 24.8% CAGR from 2026 to 2034, driven by hyperscaler integration, managed services, and scalable subscription economics.

Opportunities include zero-trust IoT platforms, OT and industrial IoT security, AI-powered threat detection, post-quantum cryptography readiness, and managed detection and response for mid-market buyers.

AI enables behavioral baselining, anomaly detection, and automated response at scale, reducing mean-time-to-detect and compensating for a cybersecurity workforce gap of roughly 4.8 million professionals in 2024.

Regulations such as the EU Cyber Resilience Act, NIS2 Directive, U.S. Cyber Trust Mark, and Singapore's labelling scheme are standardizing baseline controls and driving compliance-led procurement globally.

Asia Pacific is the fastest-growing region at approximately 24.1% CAGR through 2034, led by China's smart manufacturing, India's Smart Cities Mission, and tightening data-protection enforcement across the region.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)