ISOBUS Component Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

ISOBUS Component Market Size, Share, Trends & Forecast (2026-2034)

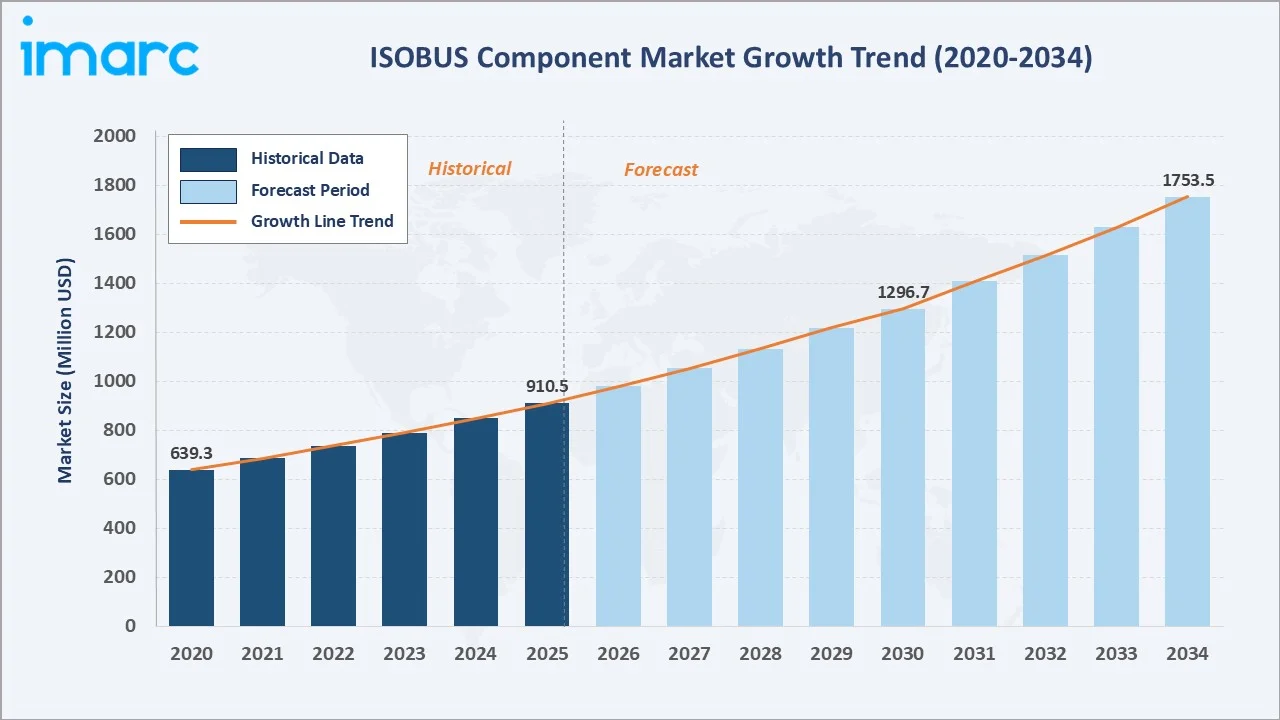

The ISOBUS component market reached a value of USD 910.5 Million in 2025 and is projected to reach USD 1,753.5 Million by 2034, expanding at a CAGR of 7.33% during 2026-2034. Market expansion is anchored by the rising adoption of precision agriculture and the growing demand for cross-manufacturer interoperability across mixed equipment fleets.

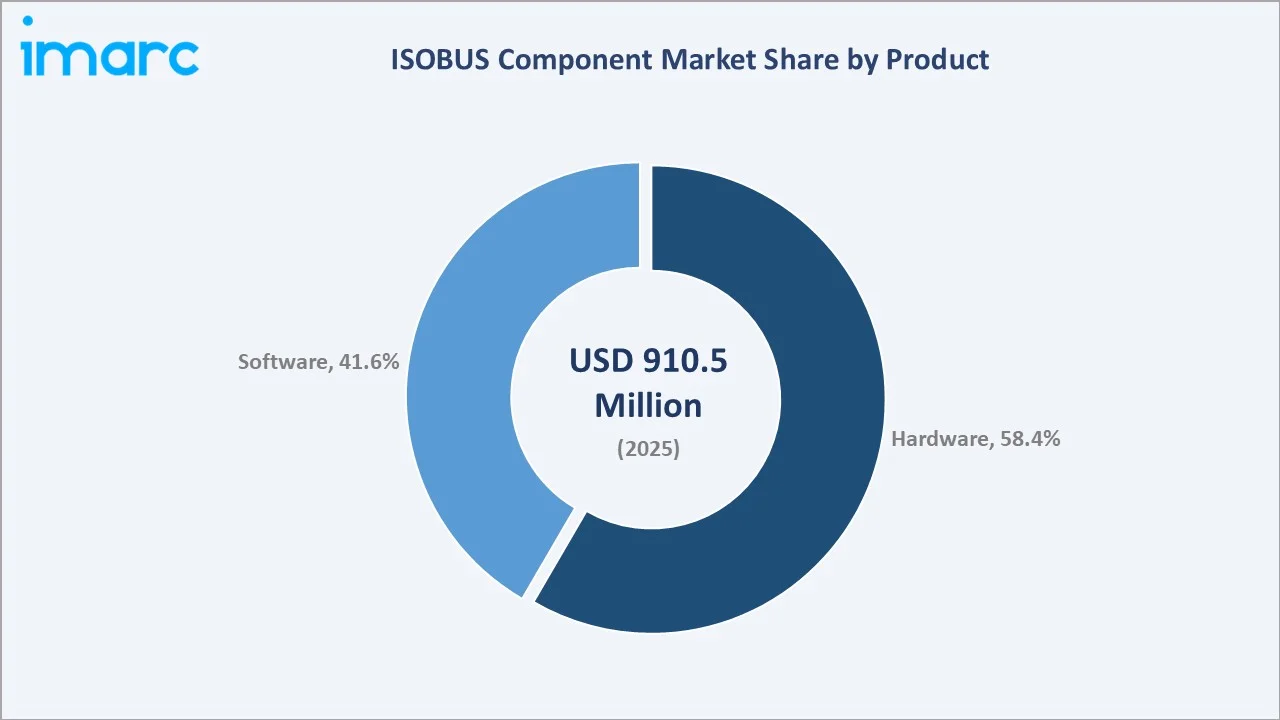

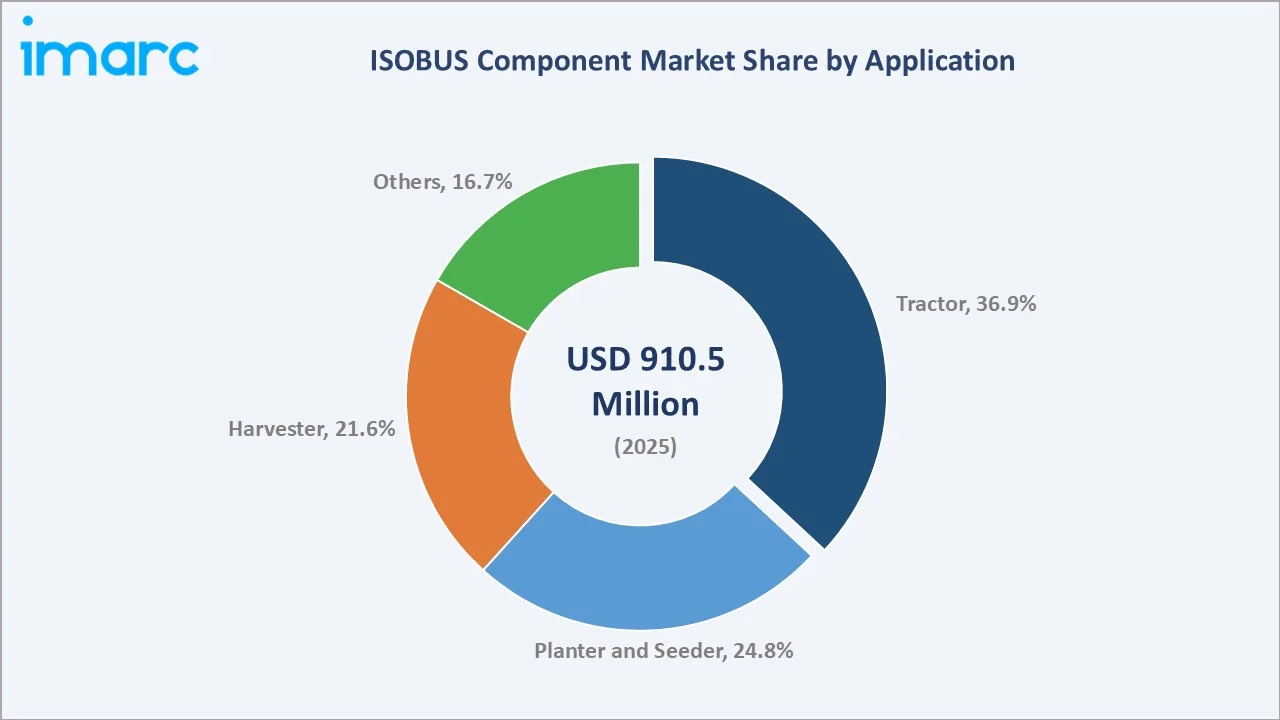

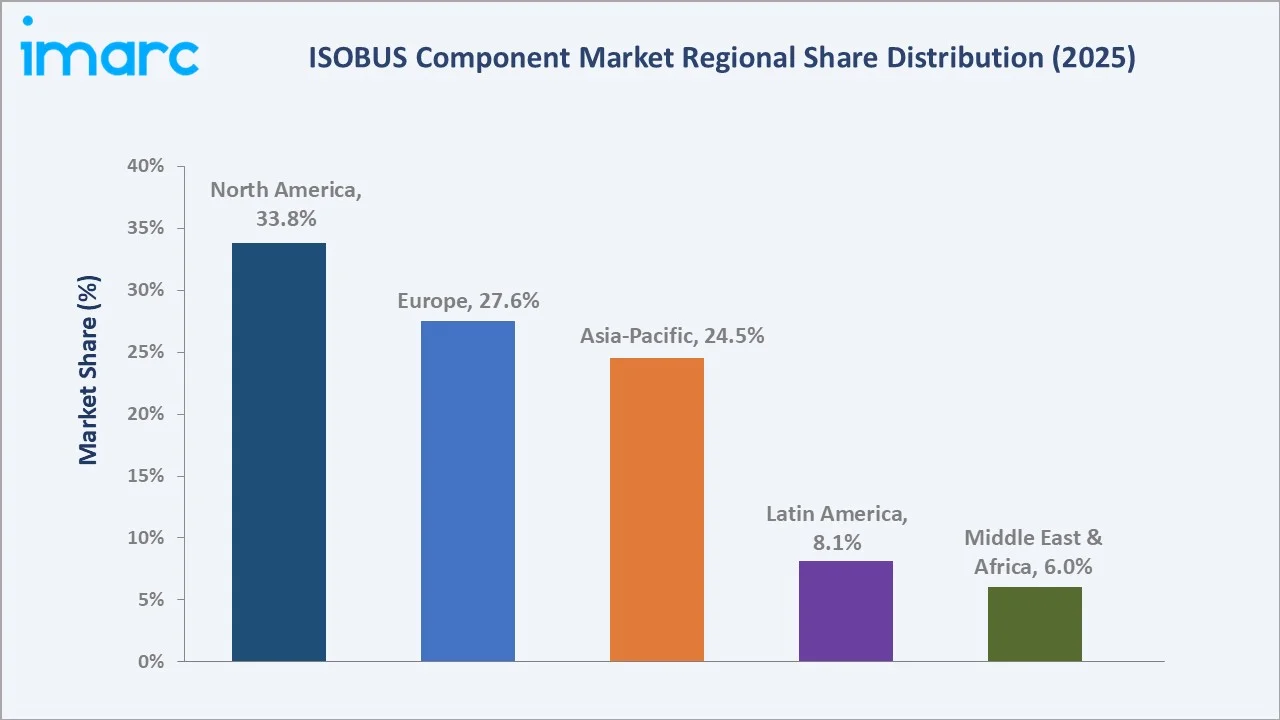

Hardware leads the product segment at 58.4%, tractor dominates the application segment at 36.9%, and North America commands the largest regional share at 33.8% in 2025.

Market Snapshot

|

Report Attribute |

Details |

|

Market Size (2025) |

USD 910.5 Million |

|

Market Forecast Size (2034) |

USD 1,753.5 Million |

|

CAGR (2026-2034) |

7.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (33.8%, 2025) |

|

Second Largest Region |

Europe (27.6%, 2025) |

|

Leading Product |

Hardware (58.4%, 2025) |

|

Leading Application |

Tractor (36.9%, 2025) |

The market has advanced steadily from USD 639.3 Million in 2020 through the historical period, supported by the electronification of farm machinery and the widespread integration of plug-and-play implement control. The trajectory below illustrates both the realized growth and the forecast outlook through 2034.

To get more information on this market, Request Sample

Growth rates vary meaningfully across product, application, and regional categories. Software and Asia-Pacific are modeled to outpace the overall 7.33% market CAGR, while established hardware categories grow at a more measured pace.

Executive Summary

The ISOBUS component market is on a strong growth path from USD 639.3 Million in 2020 to USD 1,753.5 Million by 2034. The ISOBUS component market is transitioning from an early standardization phase into a mature interoperability ecosystem in which compatibility across brands is an expectation rather than a differentiator. Demand is propelled by farm consolidation, labor scarcity, and the economic imperative to extract more value from each field operation through data-driven decision-making.

Hardware remains the revenue backbone of the market with a share of 58.4%, reflecting the capital intensity of displays, controllers, and connectivity modules. Tractor at 36.9% commands the application segment, driven by rising adoption of precision agriculture technologies, autonomous guidance systems, and smart fleet management solutions across large agricultural operations. As per IMARC Group, the global precision agriculture market size was valued at USD 10.2 Billion in 2025. Geographically, North America at 33.8% anchors demand on the strength of large-scale mechanized farming, high penetration of advanced agricultural technologies, and sustained investment in connected farm equipment infrastructure.

Key Market Insights

|

Insight |

Finding |

|

Leading Product |

Hardware – 58.4% share, (2025) |

|

Second Largest Product |

Software – 41.6% share, (2025) |

|

Leading Application |

Tractor – 36.9% share, (2025) |

|

Second Largest Application |

Planter and Seeder – 24.8% share, (2025) |

|

Leading Region |

North America – 33.8% share, (2025) |

|

Second Largest Region |

Europe – 27.6% share, (2025) |

|

Top Companies |

Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation |

Key Analytical Observations from the Study Include the Following:

- Hardware leadership at 58.4% dominates market value generation, as displays, terminals, electronic control units, and connectivity modules form the core infrastructure of ISOBUS-enabled farm equipment and represent the most capital-intensive component of deployment.

- Software at 41.6% benefits from rising demand for task controllers, variable rate application, section control, and cloud-based farm management platforms that improve interoperability and operational efficiency.

- Tractor at 36.9% share leads the application segment because tractors function as the primary communication hub within ISOBUS architecture, enabling integration between implements, displays, and precision farming systems during field operations.

- Planter and seeder at 24.8% share gains traction through increasing adoption of precision seeding technologies, automated row control, and variable rate planting systems focused on improving crop yield optimization and input efficiency.

- North America at 33.8% dominates regional demand, supported by high agricultural mechanization, strong penetration of precision farming technologies, and widespread OEM adoption of standardized electronic communication systems across commercial farms.

ISOBUS Component Market Overview

The ISOBUS component market sits at the intersection of agricultural machinery, electronics, and data services. At its core, ISOBUS provides a standardized communication backbone so that a single in-cab terminal can recognize and control any compliant implement, eliminating the need for proprietary, brand-specific controllers. This plug-and-play philosophy has reshaped how equipment is specified, sold, and serviced.

The market ecosystem spans component manufacturers, original equipment manufacturers (OEMs), software developers, dealers, and end use farmers, each connected through the shared standard. Component suppliers provide the displays, control units, and connectors; OEMs integrate these into machinery; software providers layer on agronomic and management capabilities; and dealers translate the technology into field-ready solutions for growers.

Market Dynamics

To evaluate market opportunities, Request Sample

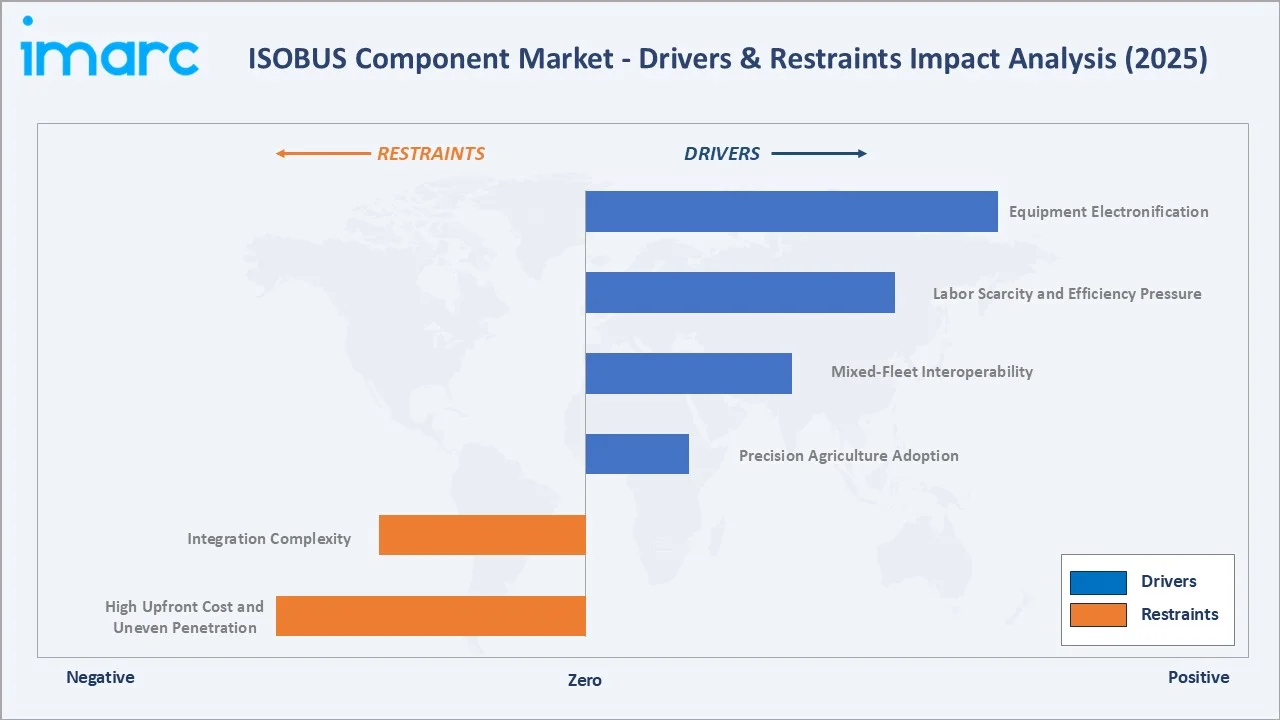

Market Drivers

- Precision Agriculture Adoption: Auto-steer and guidance technologies have moved from novelty to mainstream practice. Growing demand for operational efficiency, reduced input wastage, and real-time field data monitoring is accelerating the integration of connected and automated farming equipment across large-scale agricultural operations.

- Mixed-Fleet Interoperability: Farmers increasingly operate machinery from multiple brands, making cross-manufacturer compatibility a purchasing priority and reinforcing demand for certified ISOBUS components.

- Labor Scarcity and Efficiency Pressure: Persistent shortages of skilled farm labor push growers toward automation, section control, and variable-rate application, all of which depend on ISOBUS connectivity. In 2024, it was estimated that there were 2.4 Million available agricultural positions in the United States, with 56% of farmers indicating a lack of labor, as stated in FTI Consulting’s report from June 2025.

- Equipment Electronification: The steady increase in electronic content per machine expands the addressable value of displays, controllers, and wiring harnesses across the equipment lifecycle.

Market Restraints

- High Upfront Cost and Uneven Penetration: Advanced guidance and connectivity carry significant capital cost, and adoption remains concentrated among larger operations. Smaller farms continue to face adoption barriers due to the substantial investment required for advanced precision agriculture hardware and connectivity systems.

- Integration Complexity: Despite standardization, achieving seamless compatibility across older equipment, varied software versions, and certified functionalities can require technical expertise that smaller operations lack.

Market Opportunities

- Retrofit and Aftermarket Solutions: A large installed base of pre-ISOBUS machinery represents a substantial opportunity for retrofit terminals and adapter kits that extend modern connectivity to legacy fleets.

- Emerging-Market Mechanization: Rising farm mechanization across Asia-Pacific and Latin America opens new demand pools as growers leapfrog directly to standardized, connected equipment.

Market Challenges

- Certification and Version Fragmentation: Keeping pace with evolving certified functionalities and ensuring consistent behavior across brands remains an ongoing technical challenge for the ecosystem.

- Data Ownership and Security: As connectivity deepens, questions around data ownership, privacy, and cybersecurity introduce friction that suppliers and OEMs must actively manage.

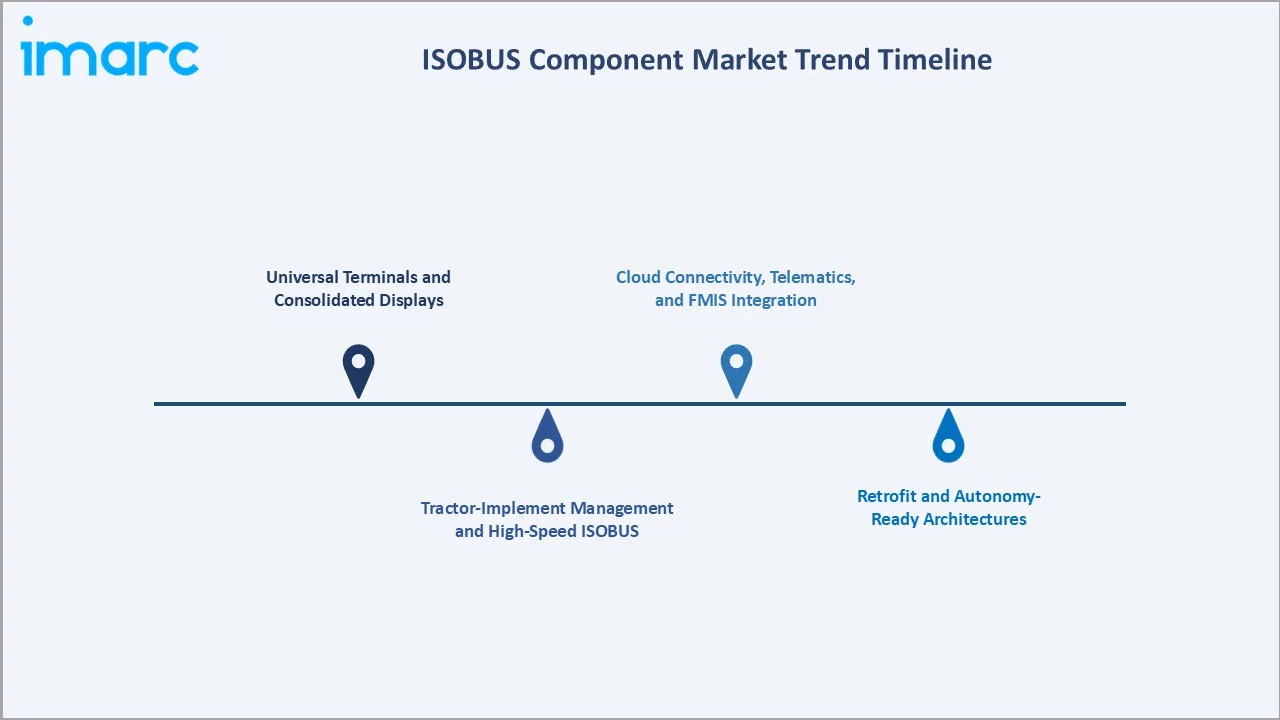

Emerging Market Trends

1. Universal terminals and consolidated displays

Manufacturers are consolidating multiple proprietary screens into a single, larger universal terminal capable of running any compliant implement. This reduces cab clutter, simplifies operator training, and reinforces the value of standardized hardware as the central control surface in the machine.

2. Tractor-implement management and high-speed ISOBUS

Tractor Implement Management (TIM) allows a compliant implement to command certain tractor functions, such as speed and hydraulics, enabling closed-loop automation in the field. However, increasing volumes of sensor and control data are creating network bandwidth limitations, prompting ongoing industry efforts to develop higher-capacity communication infrastructure for next-generation precision farming applications.

3. Cloud connectivity, telematics, and FMIS integration

Components are increasingly linked to telematics gateways and farm management information systems, so that task data, prescriptions, and machine performance flow automatically between the field and the office. This connectivity transforms the terminal from a control device into a node in a broader digital agronomy platform.

4. Retrofit and autonomy-ready architectures

Suppliers are designing components that are both backward-compatible with existing fleets and forward-compatible with autonomous operation. Retrofit-friendly terminals and modular control units allow growers to adopt advanced capabilities incrementally while preparing for driverless and supervised-autonomy workflows.

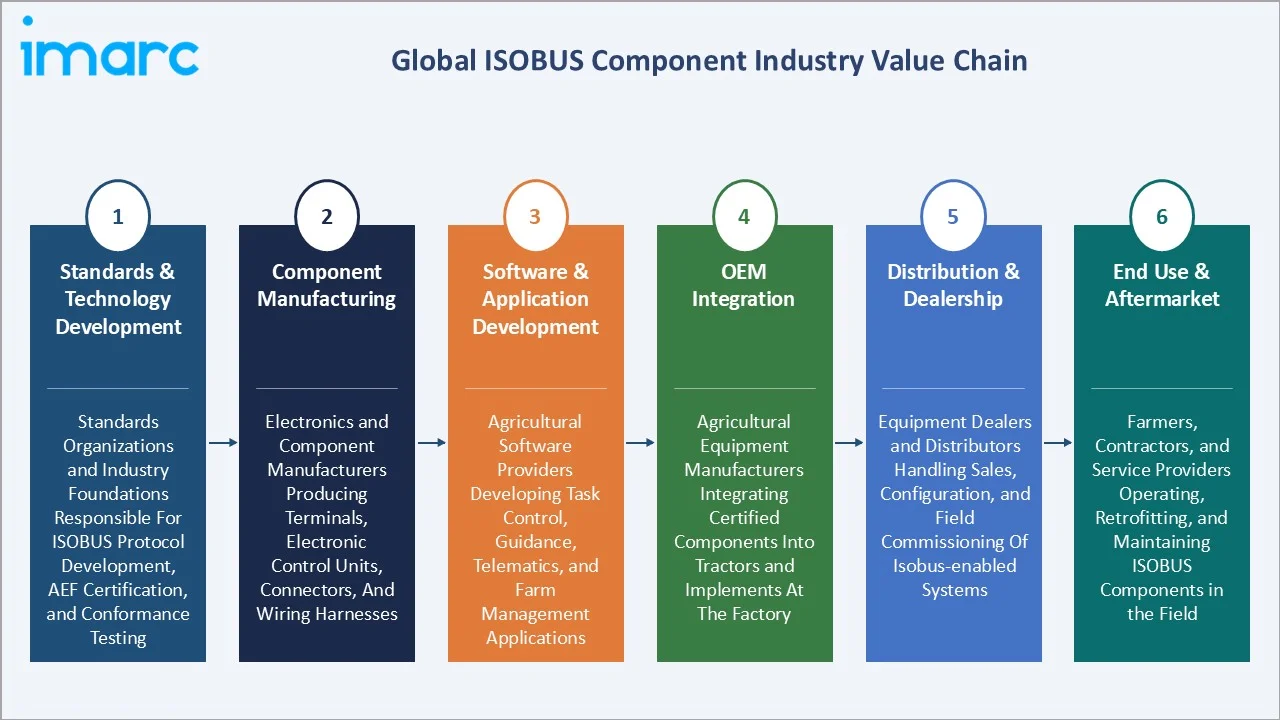

Industry Value Chain Analysis

The ISOBUS component value chain spans from underlying electronics and standards development through to in-field deployment and aftermarket support. Each stage adds distinct value.

|

Stage |

Key Players / Examples |

|

Standards & Technology Development |

Standards organizations and industry foundations responsible for ISOBUS protocol development, AEF certification, and conformance testing that define cross-brand compatibility |

|

Component Manufacturing |

Electronics and component manufacturers producing terminals, electronic control units, connectors, and wiring harnesses that form the physical ISOBUS layer |

|

Software & Application Development |

Agricultural software providers developing task control, guidance, telematics, and farm management applications that run on standardized hardware |

|

OEM Integration |

Agricultural equipment manufacturers integrating certified components into tractors and implements at the factory |

|

Distribution & Dealership |

Equipment dealers and distributors handling sales, configuration, and field commissioning of ISOBUS-enabled systems |

|

End Use & Aftermarket |

Farmers, contractors, and service providers operating, retrofitting, and maintaining ISOBUS components in the field |

Vertically integrated manufacturers achieve stronger interoperability, software compatibility, and system reliability by developing tractors, implements, displays, and ISOBUS control systems within unified product ecosystems, reducing integration complexity and dependency on third-party electronic and connectivity suppliers.

Technology Landscape in the ISOBUS Component Industry

Virtual terminals and universal displays

The virtual terminal is the operator-facing heart of the ISOBUS system, rendering the control interface of any connected implement on a standardized display. Modern universal terminals offer high-resolution touchscreens, faster processors, and the ability to manage guidance, section control, and implement settings from a single screen.

Electronic control units and task controllers

Electronic control units execute implement-level logic, while task controllers coordinate functions such as automatic section control and variable-rate application against field prescriptions. Together they translate operator intent and digital prescriptions into precise mechanical action.

Connectivity, harnesses, and the physical layer

The physical layer comprises the connectors, in-cab and implement wiring harnesses, and the CAN-based network that carry power and data between tractor and implement. Standardized connectors are central to the plug-and-play promise that defines ISOBUS.

Software, guidance, and data management

The software layer encompasses guidance and auto-steer, task management, telematics, and integration with farm management information systems. This layer is the primary vehicle for ongoing innovation, extending the capability of installed hardware over time.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Hardware |

58.4% |

2025 |

|

Application |

Tractor |

36.9% |

2025 |

|

Region |

North America |

33.8% |

2025 |

By Product

Hardware accounts for 58.4% of the market in 2025, encompassing displays, terminals, electronic control units, connectors, and wiring harnesses. Its leadership reflects the capital-intensive, foundational nature of these physical components, which are required for every ISOBUS deployment regardless of the software layered on top.

To access detailed market analysis, Request Sample

Software represents 41.6% of the market in 2025 and is the faster-growing product category. It spans guidance and task-control applications, section and rate control, and farm management integration. Because software can be updated and extended without replacing hardware, it increasingly carries the differentiation and recurring-value potential within the ecosystem.

By Application

Tractor leads with 36.9% of the market in 2025, as it hosts the universal terminal and serves as the central power and control hub for connected implements. Growing adoption of precision farming technologies and automated field operations continues to strengthen demand for ISOBUS-enabled tractor platforms across modern agricultural operations.

Planter and seeder account for 24.8%, driven by demand for precise seed placement, automatic section control, and variable-rate seeding. Increasing focus on improving crop yield consistency and reducing input wastage is further accelerating the adoption of digitally connected planting equipment.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

33.8% |

Large-scale mechanized farming, high precision-agriculture adoption, established dealer networks |

|

Europe |

27.6% |

Strong standardization culture, sustainability regulation, dense equipment manufacturing base |

|

Asia-Pacific |

24.5% |

Rising farm mechanization, government support for modernization, expanding equipment demand |

|

Latin America |

8.1% |

Growth in large-scale commercial agriculture and row-crop production |

|

Middle East and Africa |

6.0% |

Gradual mechanization and investment in agricultural productivity |

North America leads regional demand at 33.8%, underpinned by large average farm sizes and mature adoption of guidance and connectivity. Strong presence of advanced agricultural equipment manufacturers and widespread integration of precision farming technologies continue to support regional market expansion.

Europe at 27.6% is supported by strong adoption of smart farming technologies, increasing focus on equipment interoperability, and regulatory emphasis on precision agriculture practices across the region.

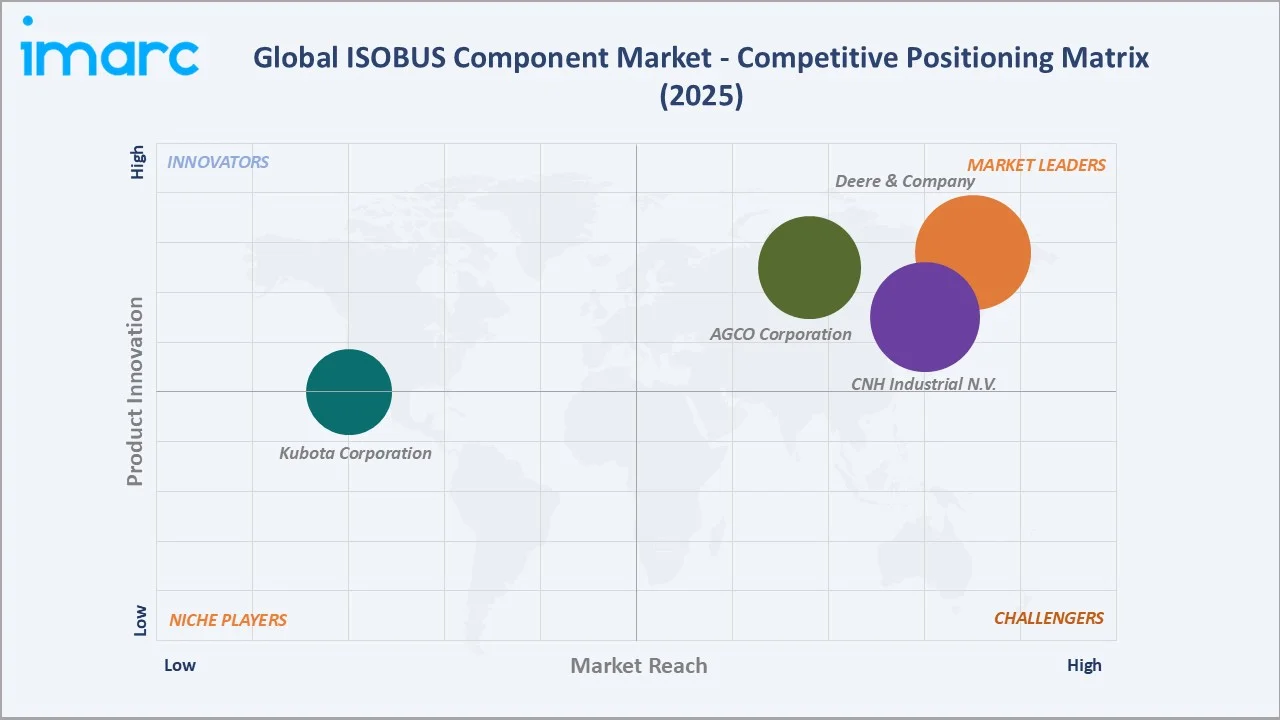

Competitive Landscape

The ISOBUS component market is moderately consolidated, with leadership held by large manufacturers that combine proprietary terminals, guidance, and connectivity into integrated ecosystems. Specialist precision-agriculture firms compete alongside them, often supplying brand-agnostic displays and retrofit solutions.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Deere & Company |

John Deere G5 Plus Universal Display |

Leader |

Integrated hardware-software ecosystems and connected services |

|

CNH Industrial N.V. |

Case IH AFS Pro 1200 |

Leader |

Precision platforms across multiple equipment brands |

|

AGCO Corporation |

FendtONE |

Leader |

Mixed-fleet precision agriculture and retrofit solutions |

|

Kubota Corporation |

Tellus 1200 |

Emerging |

Implement-focused terminals and task control |

Key players include Deere & Company, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation.

Key Company Profiles

Deere & Company

Deere & Company, operating under the John Deere brand, is one of the world's leading manufacturers of agricultural machinery and precision-agriculture technology, with an integrated approach that spans equipment, in-cab displays, guidance, and connected digital services.

- Product Portfolio: The company offers a comprehensive range of ISOBUS-compatible terminals, guidance receivers, telematics gateways, and farm management software that function together as a connected precision-agriculture ecosystem.

- Recent Developments: The company has strengthened its ISOBUS-enabled precision agriculture ecosystem through the introduction of enhanced display technologies, improved machine connectivity features, and expanded automation functionalities designed to support seamless implement integration and data-driven farm operations.

- Strategic Focus: The company focuses on integrated hardware-software ecosystems, automation, and recurring value from connected services.

AGCO Corporation

AGCO Corporation is a global manufacturer and distributor of agricultural machinery and precision-agriculture technology, serving farmers through a portfolio of equipment brands and smart-farming solutions.

- Product Portfolio: Its offering includes ISOBUS-compatible terminals, guidance and section-control systems, and farm management tools designed to operate across mixed equipment fleets.

- Recent Developments: The company has continued to invest in mixed-fleet, brand-agnostic precision-agriculture technology, expanding its retrofit and factory-fit solutions and strengthening its digital farming portfolio.

- Strategic Focus: AGCO Corporation concentrates on mixed-fleet precision agriculture and retrofit solutions that extend across equipment from multiple manufacturers.

Kubota Corporation

Kubota Corporation is a global agricultural and machinery manufacturer that, through its group companies, offers ISOBUS terminals and implement-control solutions for precision farming.

- Product Portfolio: Its portfolio includes universal ISOBUS terminals and task-control software that enable precise implement management and integration across compatible tractors and machinery.

- Recent Developments: The company has continued to develop its universal ISOBUS terminal range and implement-control software, reinforcing its precision-farming capabilities for mixed-fleet operations.

- Strategic Focus: The firm focuses on implement-focused terminals and task-control solutions that simplify precise field operations.

Market Concentration Analysis

The ISOBUS component market is moderately concentrated. A small group of large, fully integrated equipment manufacturers commands the majority of value through proprietary terminals, guidance, and connected-service ecosystems. These leaders benefit from scale, established dealer networks, and the ability to bundle hardware with software and data services.

Barriers to entry include compliance with ISOBUS communication standards, extensive cross-brand compatibility testing, and the technical expertise required to develop reliable electronic control units, displays, connectors, and communication modules for agricultural equipment integration. Established suppliers also benefit from long-term OEM partnerships and strong distribution networks within the agricultural machinery industry.

Consolidation is increasing through partnerships and acquisitions focused on precision agriculture software, connectivity technologies, and smart implement control solutions that strengthen integrated ISOBUS ecosystems. Scale advantages in component manufacturing, embedded software development, and aftermarket technical support continue to reinforce the market position of established ISOBUS component manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

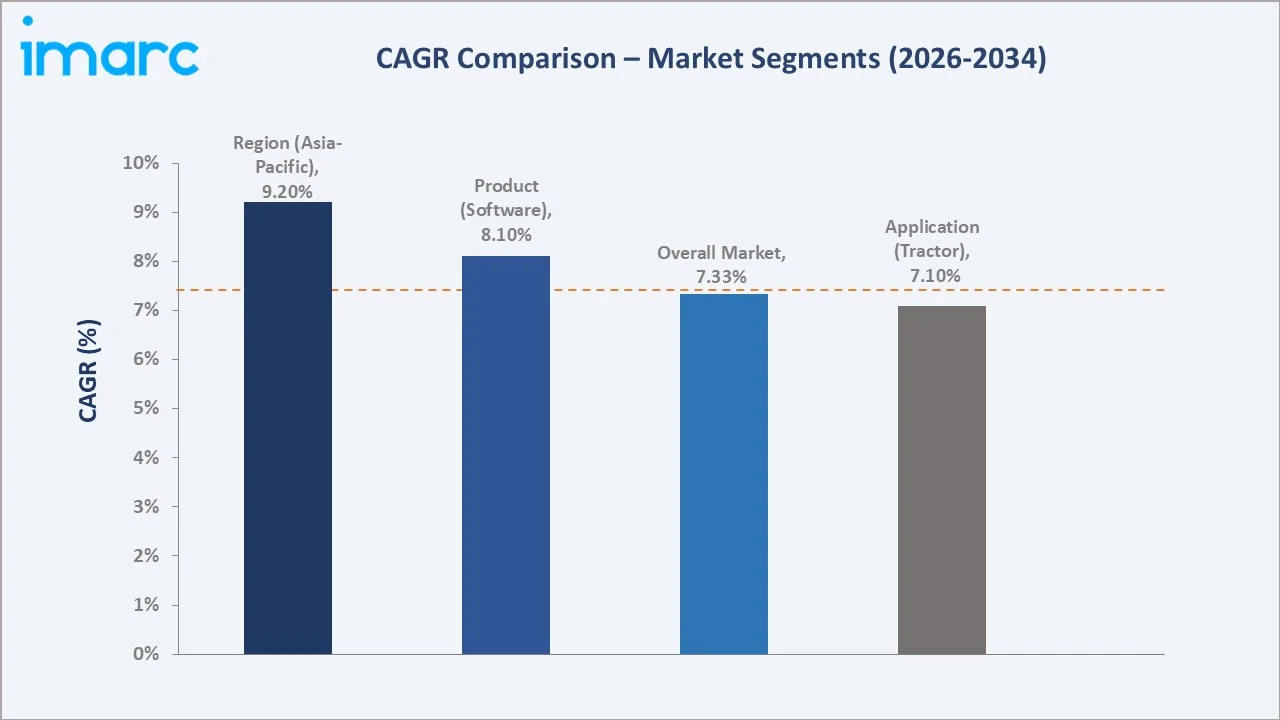

Software is the fastest-growing product segment, expanding at an estimated 8.10% CAGR against the overall market's 7.33% through 2034, as recurring, update-driven value from task control, guidance, and data management outpaces hardware. Among applications, planter and seeder represent the fastest-growing category at an estimated 7.60% CAGR, driven by demand for precise seed placement, automatic section control, and variable-rate seeding.

Emerging Markets

Asia-Pacific is the highest-growth region, expanding at an estimated 9.20% CAGR as farm mechanization accelerates across major agricultural economies and government modernization initiatives broaden equipment demand. Latin America at 8.1% and the Middle East and Africa at 6.0% represent the largest untapped opportunities, where the growth of commercial row-crop agriculture and rising investment in productivity are drawing standardized, connected components into newly mechanizing fleets.

Venture & Investment Trends

Investment is concentrating in retrofit and aftermarket solutions that extend modern connectivity to the large installed base of pre-ISOBUS machinery, and in software and data services that generate recurring value through telematics and farm management integration. Capital is also flowing toward autonomy-ready architectures and higher-bandwidth connectivity, positioning early movers to capture the next wave of in-field automation.

Future Market Outlook (2026-2034)

The ISOBUS component market is forecast to expand from USD 910.5 Million in 2025 to USD 1,753.5 Million by 2034 at a CAGR of 7.33%, adding roughly USD 843 Million in incremental annual market value over the forecast period.

Several forces will shape the market through 2034: software and data services outgrowing hardware as recurring value accrues from task control and telematics; autonomy-ready components moving from pilot to mainstream; higher-bandwidth ISOBUS enabling more sophisticated tractor-implement automation; and broadening farm mechanization across emerging regions.

By 2034, ISOBUS compatibility will be a baseline expectation rather than a differentiator across new equipment in leading markets, and integrated ecosystems combining certified hardware, software, and connected services will capture the bulk of growth. Asia-Pacific and Latin America will broaden demand as they mechanize, while North America and Europe continue to anchor the market.

Research Methodology

Primary Research

Primary research included interviews with senior product managers at agricultural equipment manufacturers and component suppliers, precision-agriculture dealers, agronomists, and farmers operating mixed fleets, validating market sizing, segmentation, regional shares, and adoption trends.

Secondary Research

Secondary sources included the ISO 11783 standard documentation, Agricultural Industry Electronics Foundation (AEF) materials and the AEF ISOBUS database, United States Department of Agriculture statistics, company annual reports and regulatory filings, product literature, and reputable industry news sources.

Forecasting Models

Market forecasts used a combination of top-down and bottom-up models, drawing on the installed base of machinery, electronic content per machine, adoption and penetration rates, equipment replacement cycles, and regional mechanization trends. Scenario analysis addressed variation in adoption rates and equipment costs.

ISOBUS Component Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Applications Covered | Tractor, Planter and Seeder, Harvester, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ISOBUS component market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global ISOBUS component market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ISOBUS component industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the ISOBUS Component Market Research Report Report

The ISOBUS component market reached a value of USD 910.5 Million in 2025, supported by rising precision-agriculture adoption and growing demand for cross-manufacturer interoperability across mixed equipment fleets.

The market is projected to reach USD 1,753.5 Million by 2034, expanding at a compound annual growth rate of 7.33% over the forecast period from 2026 to 2034.

Hardware leads the product segment with a 58.4% share in 2025, comprising displays, terminals, electronic control units, and connectors, while software accounts for the remaining 41.6%.

Tractor dominates with a 36.9% share in 2025, fueled by increasing adoption of precision farming technologies, automated implement control systems, and the growing role of tractors as the primary connectivity and communication hub within ISOBUS-enabled agricultural operations.

North America holds the largest share at 33.8% in 2025, supported by large-scale mechanized farming and high adoption of guidance and connectivity technologies.

Key players include Deere & Company, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation.

The principal drivers are rising precision-agriculture adoption, demand for mixed-fleet interoperability, labor scarcity that pushes automation, and the increasing electronic content of agricultural machinery.

Key challenges include keeping pace with evolving certification and version fragmentation across brands, integration complexity for legacy and mixed fleets, high upfront equipment cost, and emerging concerns around data ownership and cybersecurity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)