Japan Car Rental Market Size, Share, Trends and Forecast by Booking Type, Rental Length, Vehicle Type, Application, End-User, and Region, 2026-2034

Japan Car Rental Market Size, Share, Trends & Forecast (2026-2034)

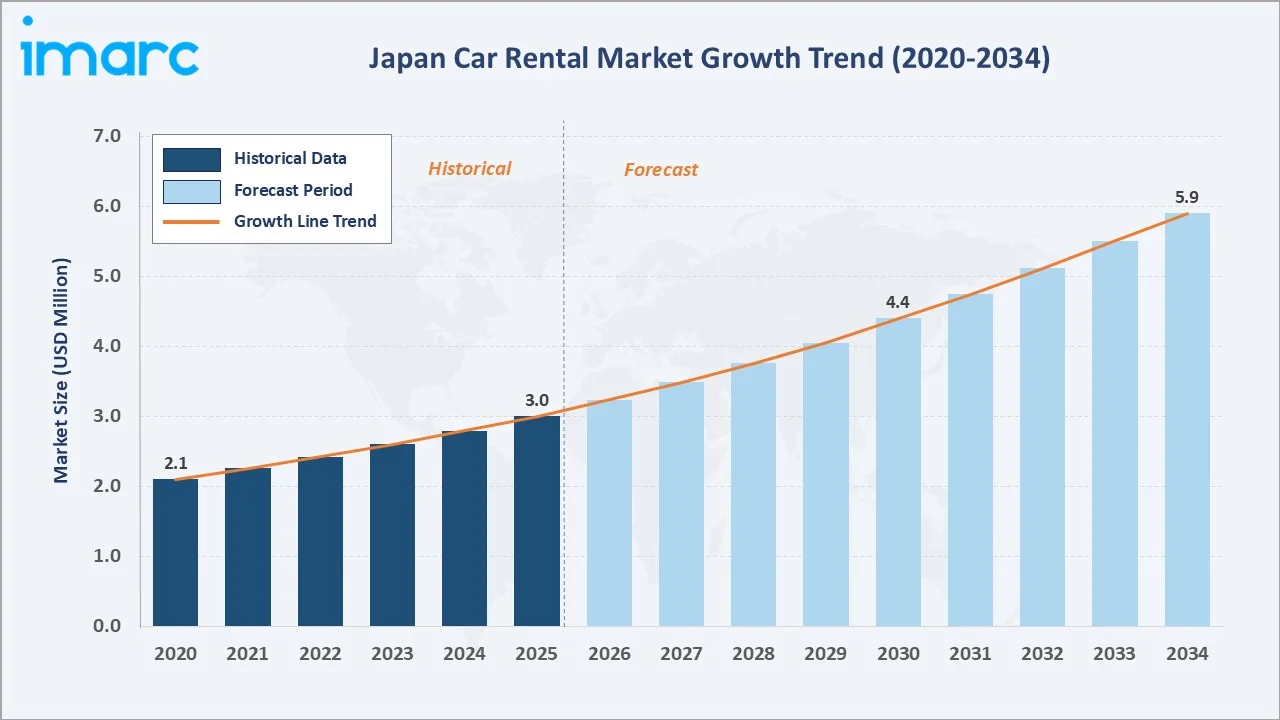

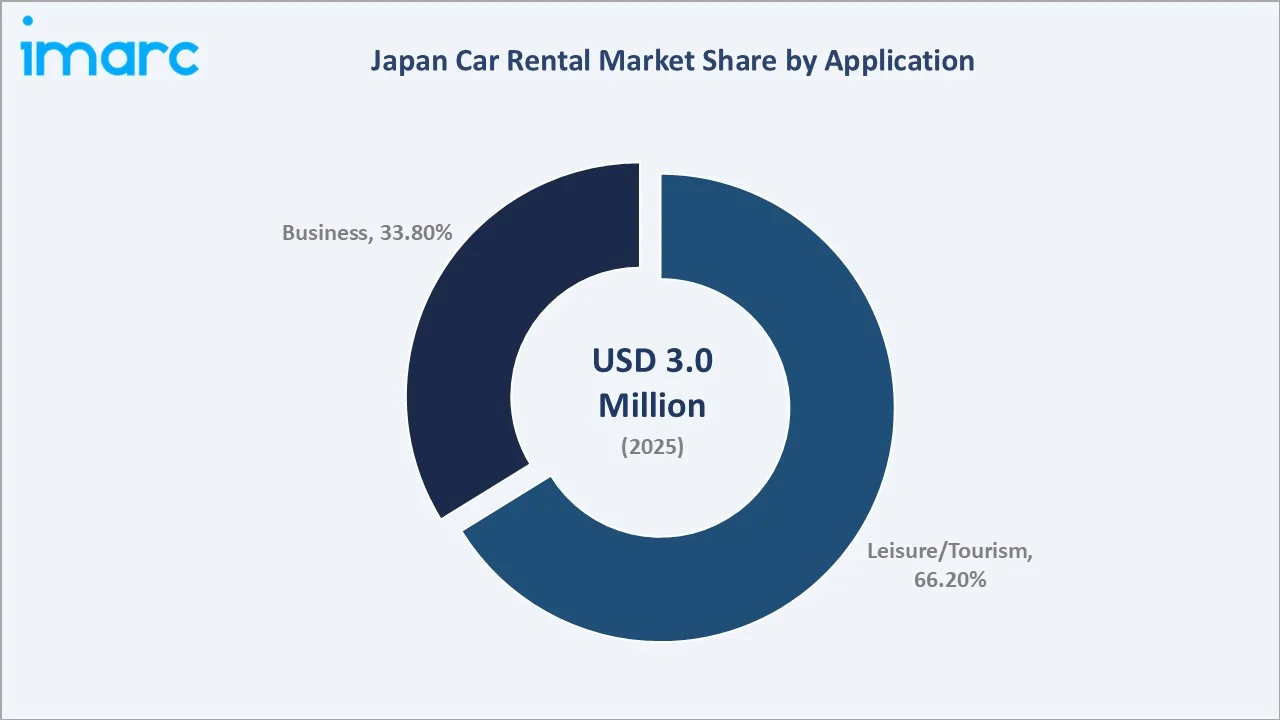

The Japan car rental market size reached USD 3.0 Million in 2025 and is projected to reach USD 5.9 Million by 2034, exhibiting a CAGR of 7.46% during 2026-2034. Robust tourism recovery, digital transformation of booking platforms, and rising shared-mobility preferences are the primary forces propelling market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.0 Million |

|

Forecast Market Size (2034) |

USD 5.9 Million |

|

CAGR (2026-2034) |

7.46% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Application |

Leisure/Tourism (66.2%, 2025) |

|

Leading End-User |

Self-Driven (71.5%, 2025) |

To get more information on this market, Request Sample

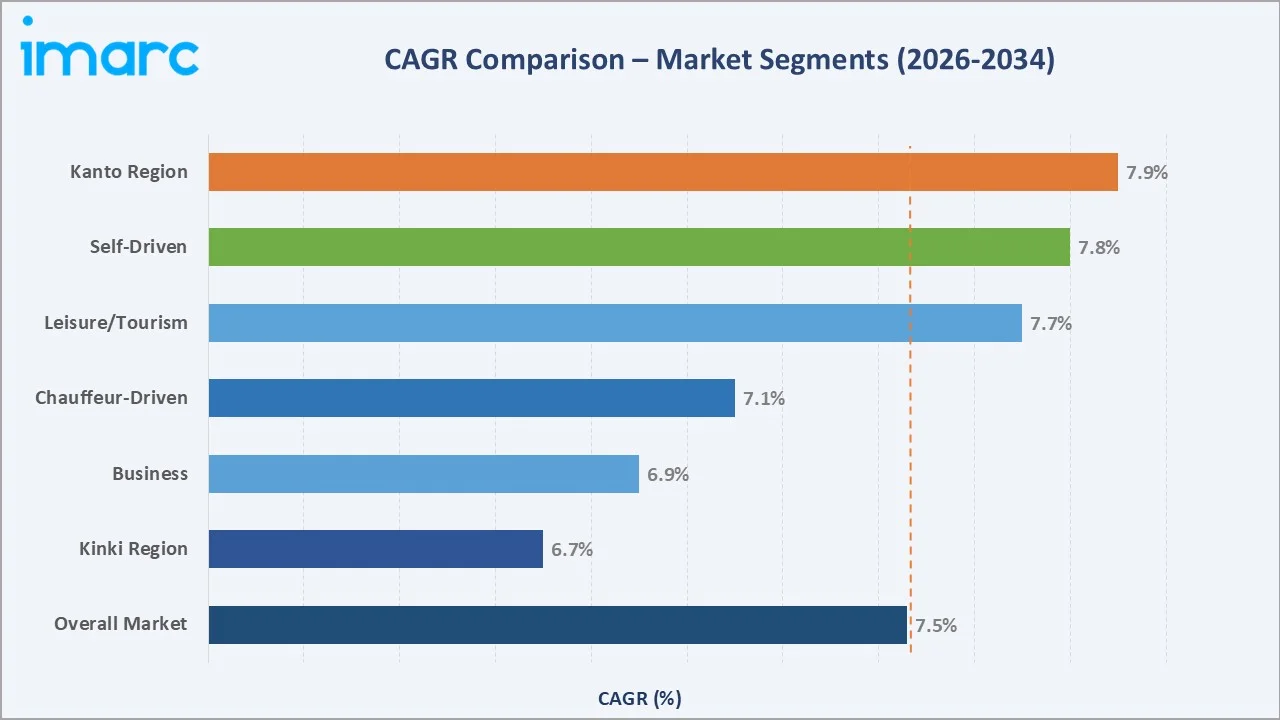

The CAGR trajectories across key application and end-user sub-segments, with Leisure/Tourism at ~8.1% CAGR and Self-Driven at ~7.8% CAGR, represent the fastest-growing sub-segments. Business and Chauffeur-Driven follow at 6.3% and 6.7% CAGR respectively, reflecting diversified demand drivers across the market.

Executive Summary

The Japan car rental market is on a sustained growth trajectory from USD 3.0 Million in 2025 to USD 5.9 Million by 2034. Car rental services, offering flexible personal mobility across leisure, corporate, and inbound tourism segments, are positioned as essential transport solutions across Japan's diverse prefectures and travel corridors.

Leisure/Tourism dominates application at 66.2% in 2025, driven by record inbound tourism with 33.1 million visitors recorded in 2023, domestic travel demand, and seasonal holiday travel. Business rental at 33.8% is supported by corporate fleet substitution and growing preference for flexible mobility-as-a-service arrangements.

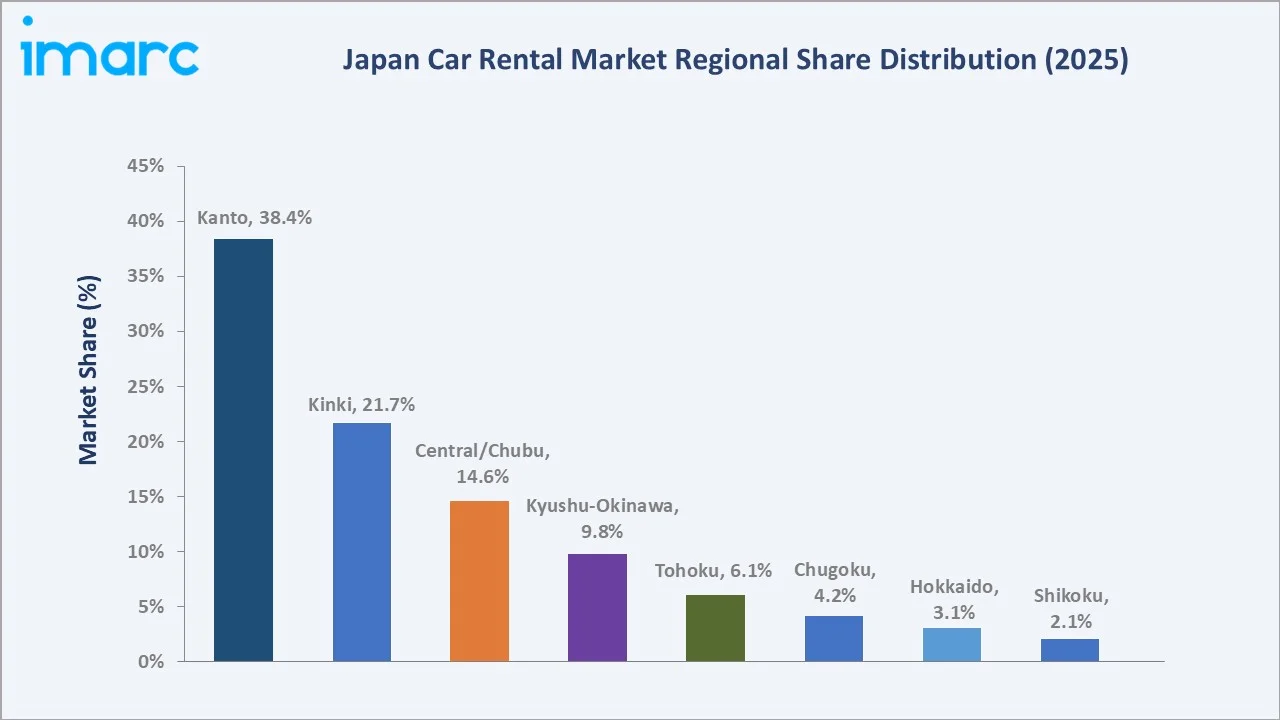

The Kanto Region dominates at 38.4% in 2025, anchored by Tokyo's major international airports and dense commercial activity. Kinki Region follows at 21.7%, leveraging the Osaka-Kyoto-Nara tourism circuit.

Self-Driven rentals account for 71.5% of end-user demand, reflecting Japan's well-maintained road infrastructure and GPS navigation availability across all vehicle classes.

Key Market Insights

|

Insight |

Data |

| Market Size (2025) |

USD 3.0 Million |

| Forecast Market Size (2034) |

USD 5.9 Million |

| CAGR (2026-2034) |

7.46% |

|

Leading Region |

Kanto Region (38.4%) |

| Leading Application | Leisure/Tourism (66.2%, 2025) |

| Leading End-User | Self-Driven (71.5%, 2025) |

Key Analytical Observations Supporting the Above Data:

- Leisure/Tourism application, with 66.2% in 2025, dominates because Japan's post-pandemic inbound tourism surge, 33.1 million visitors in 2023, has dramatically expanded rental demand from international travellers at Narita, Haneda, Kansai, and New Chitose international airports serving all major tourist entry points.

- Self-Driven end-user segment, with 71.5% in 2025, leads owing to Japan's extensive and well-maintained national road network, widespread multilingual GPS navigation in rental vehicles, and growing preference for independent itinerary flexibility among both domestic and inbound tourists.

- Kanto Region's 38.4% dominance in 2025 reflects Tokyo's status as Japan's largest business hub, its dual international airports handling the majority of inbound arrivals, and the highest concentration of corporate headquarters requiring business travel support across the Greater Tokyo Area.

- Kinki Region, with 21.7% in 2025, benefits from the Osaka-Kyoto-Nara-Kobe cultural tourism corridor attracting the highest concentration of inbound sightseeing travellers who prefer car rental for flexible temple and heritage itinerary coverage, further boosted by Osaka Expo 2025 international visitor influx.

Japan Car Rental Market Overview

Japan's car rental sector is a mature, technology-integrated mobility service industry supplying short-term and long-term vehicle access to leisure travellers, inbound tourists, domestic business travellers, and corporate fleet substitution clients across all 47 prefectures, served through airport counters, urban stations, and mobile digital booking platforms.

The Japan car rental ecosystem integrates vehicle OEMs, fleet management providers, insurance underwriters, digital reservation platforms, airport and rail hub operators, international booking aggregators including global distribution systems, and end-users spanning individual travellers, SME corporate accounts, and large enterprise fleet clients seeking fully managed mobility solutions.

Market Dynamics

To evaluate market opportunities, Request Sample

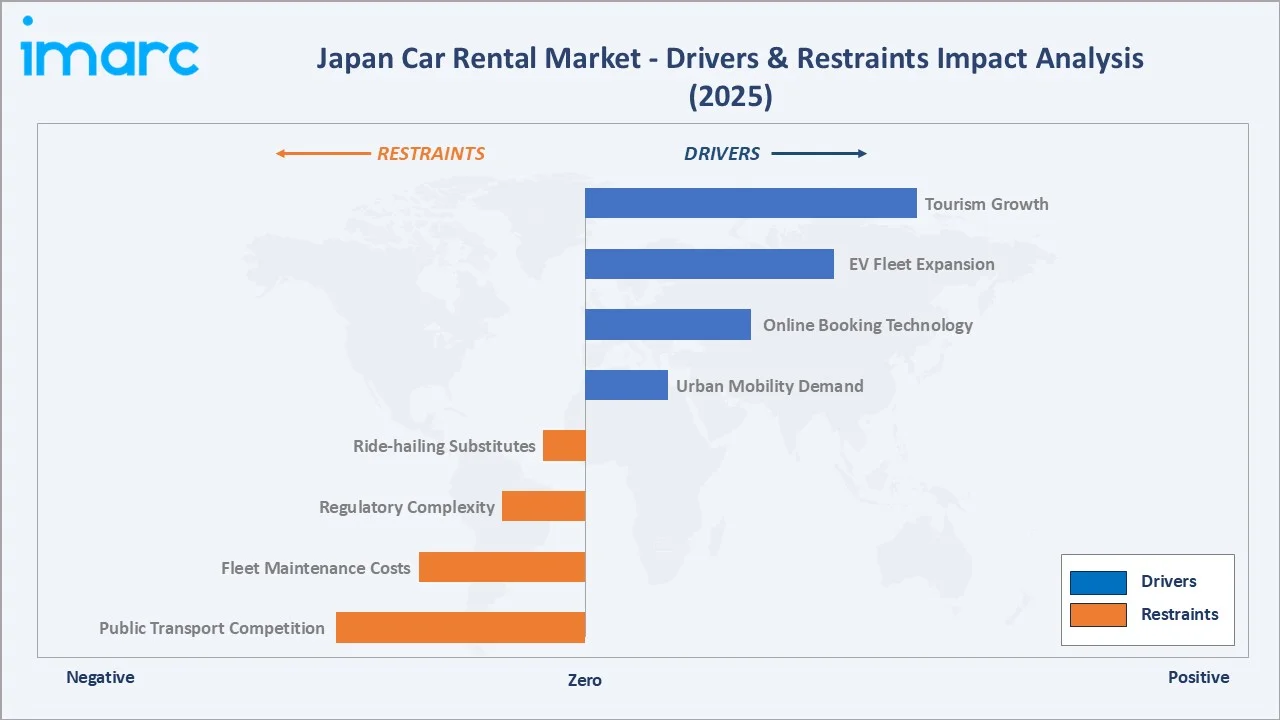

Market Drivers

- Inbound Tourism Expansion and Record International Visitor Volumes: Japan recorded 33.1 million inbound visitors in 2023 with government targets of 60 million by 2030 under the Tourism Vision for a Sustainable Nation strategy, generating substantial incremental car rental demand particularly in regional prefectures with limited public transport connectivity outside major metropolitan areas.

- Digital Platform Adoption and Mobile Booking Growth: Rising smartphone penetration and expanding in-app vehicle reservation capabilities from Toyota Mobility Service, Times Car, and international aggregators are enabling seamless booking, dynamic pricing, and contactless vehicle pickup, expanding addressable customer reach and repeat utilization across tourism and business segments.

- Corporate Mobility Transformation and Fleet Rationalization: Japanese corporations are progressively shifting from owned company car fleets toward subscription and rental models, reducing capital expenditure on vehicle depreciation. Toyota's Kinto One subscription service and competing corporate mobility platforms are accelerating this structural demand shift toward professionally managed rental fleets.

Market Restraints

- Aging Population and Declining Domestic Driving License Penetration: Japan's demographic transition, with 29.1% of the population aged 65 or above, progressively reduces the domestic driver pool. Elderly license surrender campaigns encouraged by road safety authorities are constraining the base of domestic self-driven rental customers, particularly in rural and suburban markets.

- Intense Competition from Ride-Hailing and Public Transport Alternatives: Japan's exceptional urban public transport network including Shinkansen bullet trains, dense subway systems, and expanding ride-hailing services reduces car rental necessity for short urban journeys, constraining demand in metropolitan centers compared to countries with less developed public transport infrastructure.

Market Opportunities

- EV Fleet Integration and Green Tourism Positioning: Japan's 2035 target to achieve 100% EV and electrified new vehicle sales creates substantial demand for EV rental fleets, enabling providers to position green car rental as a premium sustainable tourism product for environmentally conscious international visitors from European and North American markets seeking low-emission travel experiences.

- Rural and Regional Tourism Development Through Car Rental: Japan's rural tourism revitalization programs under the Destination Management Organization framework, targeting secondary prefectures in Tohoku, Shikoku, and Chugoku, create new demand centers where car rental represents the primary transport mode for visitors accessing off-the-beaten-path cultural and natural heritage attractions.

Market Challenges

- Vehicle Supply Constraints from Semiconductor Shortages and OEM Delivery Delays: Global semiconductor supply disruptions continuing through 2024–2025 have impacted new vehicle delivery timelines for fleet operators, constraining rental fleet expansion capacity precisely when demand is growing, creating fleet age management and customer satisfaction challenges for all major operators.

- Foreign Driver License Translation and International Visitor Navigation Complexity: Japan's requirement for International Driving Permits or official Japanese translation of foreign licenses creates administrative friction for inbound rental customers, particularly from non-Geneva Convention countries, limiting conversion rates from inbound visitors to actual car rental customers at airport counters.

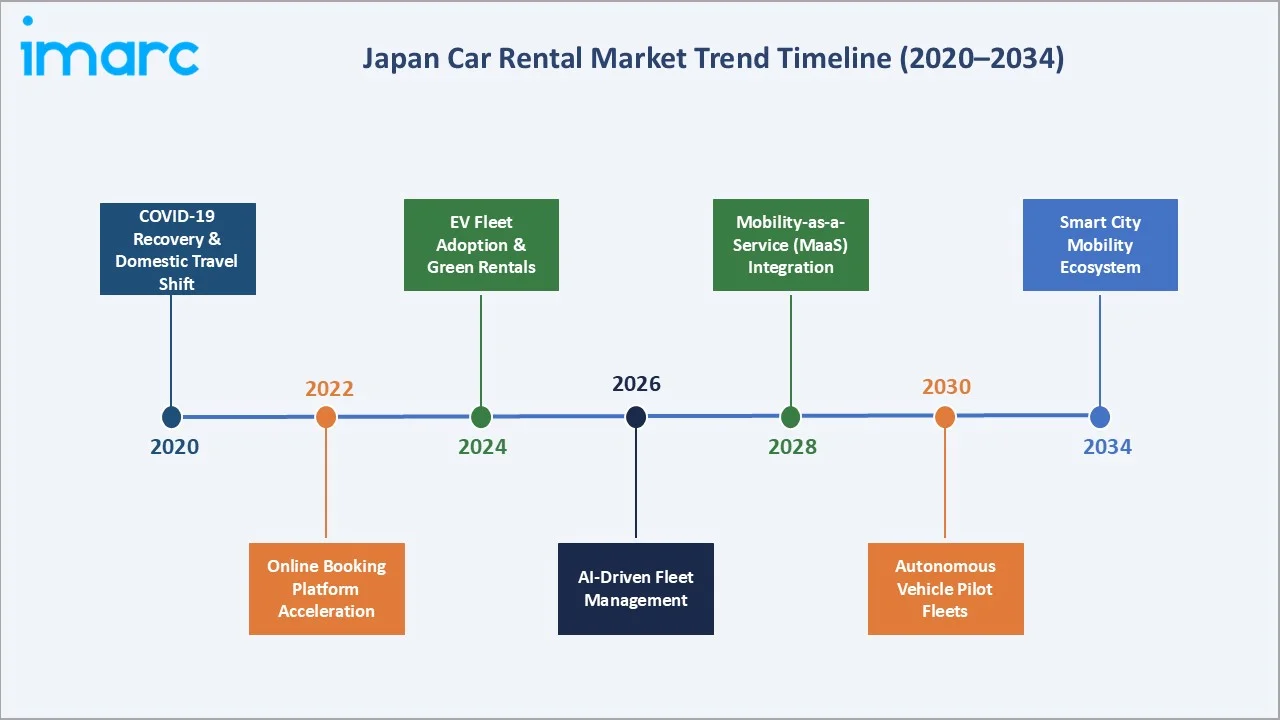

Emerging Market Trends

1. EV Fleet Electrification and Charging Infrastructure Integration

Japan's major rental operators are accelerating EV fleet adoption, integrating Toyota bZ4X and Nissan Ariya. Operators are partnering with charging network providers to ensure EV customers can plan long-distance itineraries with confidence, critical for tourist rental use cases across national parks and Japan's scenic coastal and mountain routes.

2. Contactless and Digital-First Rental Experience

Post-pandemic acceleration of contactless rental workflows including smartphone key access, fully digital check-in via QR verification, and AI-driven damage assessment photography is transforming customer experience. Nippon Rent-A-Car's app-based vehicle handover and Times Car's fully automated kiosk pickup represent the operational frontier of this digital transformation trend.

3. Integration with Multimodal Tourism Platforms

Car rental providers are integrating with Jalan, Rakuten Travel, and global OTA platforms to enable seamless bundled itineraries combining Shinkansen, accommodation, and regional car rental into single booking flows. This reduces booking friction for international visitors and increases rental attachment rates to hotel bookings across all major tourist destination regions of Japan.

4. Long-Term and Subscription Rental Growth from Corporate Accounts

Corporate demand is shifting from daily to monthly and annual subscription rental formats, driven by cost certainty, maintenance inclusion, and the desire to avoid vehicle ownership complexity. Toyota's Kinto One subscription and ORIX Auto's long-term plans are capturing fleet rationalization demand from mid-size enterprises seeking predictable mobility cost structures.

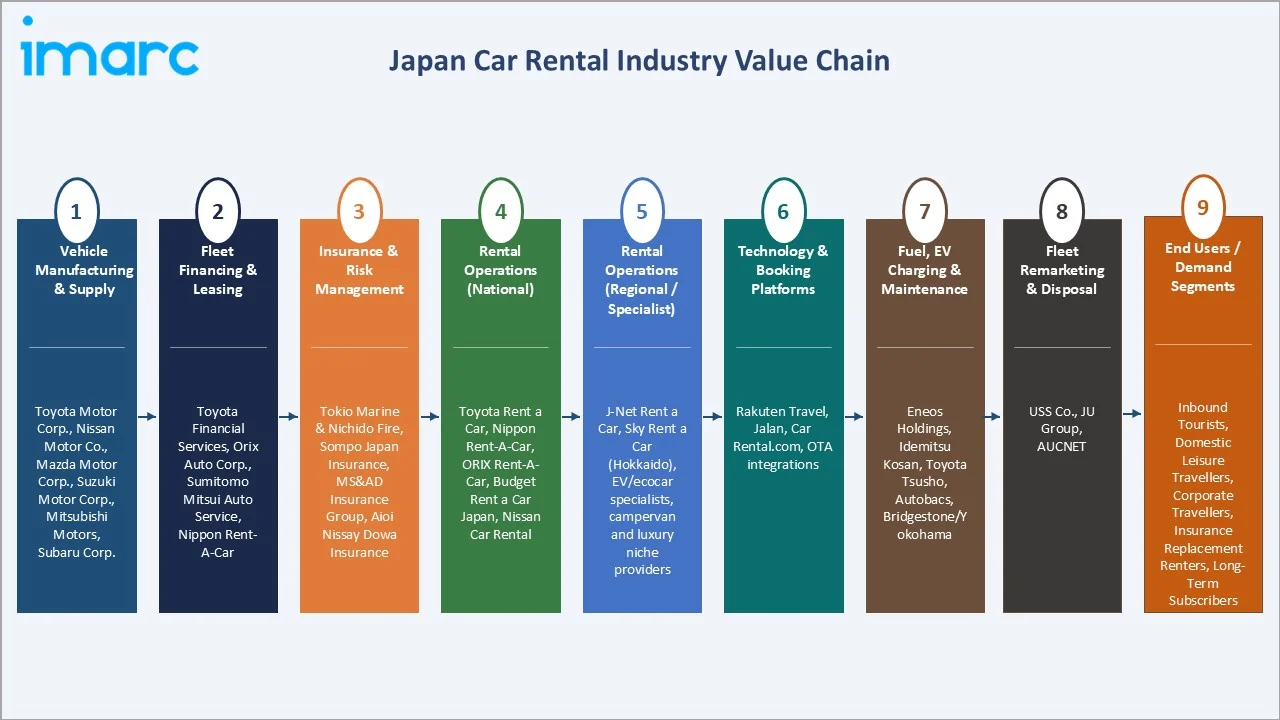

Industry Value Chain Analysis

The Japan car rental value chain spans six integrated stages from vehicle manufacturing through end-user mobility delivery. Fleet procurement and customer digital interface capture the highest margin concentration, while vehicle maintenance and cleaning logistics represent the highest operational cost intensity for rental operators.

|

Stage |

Key Activities / Examples |

| Vehicle Manufacturing & Supply | Toyota Motor Corp., Nissan Motor Co., Mazda Motor Corp., Suzuki Motor Corp., Mitsubishi Motors, Subaru Corp. |

|

Fleet Financing & Leasing |

Toyota Financial Services, Orix Auto Corp., Sumitomo Mitsui Auto Service, Nippon Rent-A-Car |

| Insurance & Risk Management | Tokio Marine & Nichido Fire, Sompo Japan Insurance, MS&AD Insurance Group, Aioi Nissay Dowa Insurance |

| Rental Operations (National) | Toyota Rent a Car, Nippon Rent-A-Car, ORIX Rent-A-Car, Budget Rent a Car Japan, Nissan Car Rental |

| Rental Operations (Regional / Specialist) | J-Net Rent a Car, Sky Rent a Car (Hokkaido), EV/eco-car specialists, campervan and luxury niche providers |

| Technology & Booking Platforms | Rakuten Travel, Tabirai Car Rental, Rentalcar.com, OTA integrations |

| Fuel, EV Charging & Maintenance | Eneos Holdings, Idemitsu Kosan, Toyota Tsusho, Autobacs, Bridgestone/Yokohama |

| Fleet Remarketing & Disposal | USS Co., JU Group, AUCNET |

| End Users / Demand Segments | Inbound tourists, domestic leisure travellers, corporate/business travellers, insurance replacement renters, long-term subscribers |

Vertically integrated operators such as Toyota Rent a Car, leveraging Toyota's manufacturing and dealer networks for fleet acquisition and replacement, maintain structural cost advantages over independent operators who procure through open market channels. ORIX Auto's financing and fleet management capabilities similarly enable below-market total cost of fleet ownership across its corporate client base.

Technology Landscape in the Japan Car Rental Industry

Connected Vehicle and Telematics Technology

Modern Japan car rental fleets increasingly feature factory-installed connected car systems enabling remote diagnostics, GPS tracking, mileage monitoring, and predictive maintenance scheduling. Toyota's T-Connect telematics platform and Nissan's NissanConnect system enable rental operators to manage fleet condition in real time, reducing unplanned breakdowns and improving fleet utilization rates across locations.

AI-Powered Dynamic Pricing and Revenue Management

Leading operators are deploying AI-driven revenue management systems that adjust rental pricing in real time based on demand forecasting, competitor rate monitoring, seasonal event calendars, and airport arrival data feeds. Dynamic pricing optimization enables operators to maximize revenue per available vehicle day while maintaining competitive positioning during peak tourism and corporate travel periods.

Digital Identity Verification and Automated Onboarding

AI-powered OCR and facial recognition systems for driver license verification, combined with digital rental agreements, are reducing counter processing time from 15 minutes to under 3 minutes per customer. Automated damage assessment using computer vision cameras integrated into vehicle return inspection bays enables objective, dispute-free condition recording across all vehicle handovers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Booking Type |

🔒 |

🔒 |

2025 |

|

Rental Length |

🔒 |

🔒 |

2025 |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

|

Application |

Leisure/Tourism |

66.2% |

2025 |

|

End-User |

Self-Driven |

71.5% |

2025 |

|

Region |

Kanto Region |

38.4% |

2025 |

By Application

Leisure/Tourism commands a 66.2% majority share in 2025, reflecting the structural dominance of inbound and domestic tourism as the primary driver of car rental demand in Japan. Airport pick-up rental, destination resort rental at Okinawa beach resorts, and rural prefecture sightseeing rental collectively represent the largest single demand block across all vehicle categories and booking channels.

To access detailed market analysis, Request Sample

Business application accounts for 33.8% in 2025, representing corporate travel substitution, executive transportation, and short-term project-based mobility from Japan's large enterprise and SME base. Business rental benefits from corporate fleet rationalization and the shift toward managed mobility programs replacing company car ownership models.

By End-User

Self-Driven end-user segment dominates at 71.5% in 2025, driven by Japan's exceptional road infrastructure, widespread GPS navigation in rental vehicles, and strong preference among both domestic and international tourists for independent travel flexibility. Motorway rest areas and scenic routes including Hokkaido's Blue Pond and Kyushu's Aso caldera road are major self-drive demand generators.

Chauffeur-Driven segment captures 28.5% in 2025, serving premium corporate executives, VIP inbound tourists, and high-net-worth domestic leisure travelers preferring professional driver services. The chauffeur-driven segment benefits from luxury tourism expansion, airport transfer services, and premium corporate event transportation demand across metropolitan markets.

Regional Market Insights

Japan's car rental demand is geographically distributed across eight distinct regions, each shaped by unique tourism profiles, infrastructure access patterns, and economic activity levels. The Kanto and Kinki regions collectively command over 60% of total market revenue, anchored by Japan's two largest international gateway airports and the country's most popular inbound tourist destinations.

Regional tourism diversification programs are progressively expanding rental demand into secondary prefectures including Tohoku, Chugoku, and Shikoku, where car rental remains the primary independent transport mode. The Kyushu-Okinawa region's leisure tourism concentration, particularly Okinawa's beach resort circuit, drives the highest leisure-to-business rental ratio of any region in Japan.

|

Region |

Share (2025) |

Key Growth Drivers |

| Kanto Region | 38.4% |

Tokyo airports; corporate demand; largest tourist hub in Japan |

| Kinki Region |

21.7% |

Osaka-Kyoto tourism; Kansai Airport; Expo 2025 visitor influx |

| Central/Chubu Region |

14.6%% |

Toyota City industrial demand; Central Alps scenic tourism |

| Kyushu-Okinawa Region |

9.8% |

Okinawa beach tourism; domestic leisure; hot spring resorts |

| Tohoku Region |

6.1% |

Rural sightseeing; regional infrastructure investment |

| Chugoku Region | 4.2% | Hiroshima heritage tourism; Sanin coastal drive routes |

| Hokkaido Region | 3.1% | Scenic drive tourism; lavender route; ski resort access |

| Shikoku Region | 2.1% | 88-temple pilgrimage circuit; rural coastal scenic routes |

The Kanto Region's 38.4% market dominance in 2025 is driven by Tokyo's position as Japan's largest business and tourism hub, served by Narita and Haneda international airports generating the highest volume of inbound tourist arrivals requiring rental vehicles for regional exploration beyond the capital's extensive transit network.

Kinki Region, with 21.7% in 2025, is experiencing tourism acceleration driven by Osaka's Expo 2025 preparations, expanded Kansai International Airport capacity, and the Kyoto-Nara cultural corridor's continued attraction of international visitors seeking flexible sightseeing itineraries beyond organized tour group schedules.

Competitive Landscape

The Japan car rental market is moderately concentrated at the national level, with Toyota Rent-a-Car and Nippon Rent-A-Car collectively commanding the majority of airport location market share. Regional operators and niche players compete on price, EV fleet modernity, and multilingual customer service for inbound tourist segments across Japan's diverse prefectural markets.

The competitive positioning of key Japan car rental market participants across national market presence and strategic investment dimensions in 2025 indicates market leadership of OEM-backed operators and the growing competitive challenge from digitally-native mobility platforms targeting urban and suburban demand segments.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

| Toyota Rent-a-Car | Short/long-term rental, EV fleet |

Leader |

National network leader; OEM integration; EV push |

| Nippon Rent-A-Car Service Inc. | Airport rental, corporate fleet |

Leader |

Airport dominance; multilingual inbound tourist service |

| Orix Auto Corporation | Long-term rental, fleet management, subscription plans |

Leader |

Fleet management leader; corporate subscriptions |

| Times Mobility Co., Ltd. | Car sharing, short-term rental, EV car sharing |

Leader |

Digital-first; Park24 synergy; urban mobility focus |

| OTS Transportation Service Co., Ltd (OTS Rent-a-Car) | Economy to SUV rental; Okinawa specialist; airport service |

Challenger |

Okinawa market leader; value pricing; leisure tourism |

| Idex Auto Japan Co., Ltd. (Budget Rent A Car Japan) | Economy and standard rental, online booking platform | Challenger | Value pricing; international brand recognition for tourists |

Key players include Toyota Rent-a-Car, Nippon Rent-A-Car Service Inc., Orix Auto Corporation, OTS Transportation Service Co., Ltd. (OTS Rent-a-Car), Times Mobility Co., Ltd., Idex Auto Japan Co., Ltd (Budget Rent A Car Japan), and others.

Key Company Profiles

Toyota Rent-a-Car

Toyota Rent a Car is Japan's largest car rental operator, running a nationwide network. Its vertical integration with Toyota's manufacturing and dealer network enables below-market fleet acquisition costs and the fastest adoption of new model introductions including BEV and hybrid vehicles.

- Product Portfolio: Compact to luxury vehicles, EV fleet including bZ4X, hybrid fleet

- Recent Developments: In July 2021, Toyota expanded access to its Booking Car cloud-based service across Japan through its dealer and rental network, following strong demand from corporate customers. The platform enables companies to digitally manage vehicle usage, streamline reservations, and optimize fleet operations.

- Strategic Focus: Toyota Rent a Car leverages Toyota group vertical integration to compete on fleet modernity, EV leadership, and national network density while expanding subscription and corporate mobility services through the Kinto platform across Japan.

Nippon Rent-A-Car Service Inc.

Nippon Rent-A-Car is Japan's second largest car rental company by airport location count, with strong presence at all major domestic and international airports. The company has historically led in multilingual inbound tourist services and maintains a comprehensive corporate account portfolio across major Japanese enterprises.

- Product Portfolio: Standard to premium vehicles, long-term rental, English and multilingual support for international customers

- Recent Developments: In April 2019, Enterprise Holdings partnered with Nippon Rent-A-Car to expand car rental services in Japan through a franchise agreement. The collaboration enables travelers to access Enterprise’s global brands across select Nippon airport locations in Japan, while also allowing Japanese customers to rent vehicles internationally through Enterprise’s worldwide network.

- Strategic Focus: Nippon Rent-A-Car differentiates on airport service excellence, multilingual customer capability, and corporate account depth, targeting the high-value inbound tourism and business travel segments with premium service reliability.

Orix Auto Corporation

Orix Auto Corporation operates with its brand ORIX Rent-A-Car, which is Japan's leading long-term and fleet rental specialist. ORIX Auto's fleet management expertise and financing capabilities distinguish it as the preferred partner for corporate fleet outsourcing.

- Product Portfolio: Long-term rental plans (1–5 years), fleet management services, maintenance inclusion packages, EV subscription plans

- Strategic Focus: ORIX Auto focuses on long-term and subscription rental growth, leveraging ORIX group's financial strength to offer competitive total-cost-of-ownership fleet packages to corporate customers undergoing vehicle ownership rationalization and decarbonization planning.

OTS Transportation Service Co., Ltd.

OTS Transportation Service Co., Ltd, which operates through, OTS Rent-a-Car, is Okinawa's leading car rental operator and one of Japan's most recognized leisure-focused rental brands, with primary operations at Naha Airport and across Okinawa's main and outer islands. The company targets domestic and international beach resort tourists requiring flexible island exploration vehicles.

- Product Portfolio: Economy to SUV rental, airport counter and hotel delivery, kei car and compact fleet

- Strategic Focus: OTS Car Rental focuses on Okinawa market leadership through unmatched local coverage, competitive leisure pricing, and seamless airport-to-resort service, targeting domestic holiday makers and inbound visitors to Japan's premier beach tourism destination.

Market Concentration Analysis

The Japan car rental market is moderately concentrated at the national level, with Toyota Rent a Car and Nippon Rent-A-Car together holding an estimated 45–55% combined market share at major airport locations. No single operator commands more than 35% of total national market revenue, reflecting competitive intensity across segments.

OEM-backed operators (Toyota Rent a Car) and diversified financial group operators (ORIX Auto) hold structural competitive advantages through fleet cost benefits and financing capabilities. Consolidation is progressing gradually as digitally capable platforms such as Times Mobility displace smaller regional operators in metropolitan and commuter belt markets.

Investment & Growth Opportunities

Fastest-Growing Segments

Leisure/Tourism rental at ~8.1% CAGR through 2034 is the highest-growth application segment, driven by Japan's inbound tourism target of 60 million visitors by 2030, regional tourism development programs, and expanding travel from Asian source markets including China's post-reopening outbound recovery toward Japanese destinations.

Emerging Markets

Regional prefectures in Tohoku, Chugoku, Shikoku, and Hokkaido represent the highest incremental growth opportunity for car rental expansion, as Japan's regional tourism diversification programs drive visitor flows toward secondary destinations where car rental is the primary, often only viable, independent transportation option for travellers seeking authentic rural Japanese experiences.

Venture & Investment Trends

Private mobility platforms and car sharing operators are attracting growth capital, with Times Mobility's digital-first model demonstrating the scalability of parking network integration strategies. EV fleet transition investment is emerging as a major capital allocation theme as operators position for green tourism premiumization and Japan's 2035 electrification mandate timelines.

Future Market Outlook (2026-2034)

The Japan car rental market is forecast to expand from USD 3.0 Million in 2025 to USD 5.9 Million by 2034 at a CAGR of 7.46%, adding USD 2.9 Million in incremental annual market value over the nine-year forecast period, driven by tourism expansion, EV fleet penetration, and corporate mobility transformation across all segments.

Three structural forces will most significantly shape the Japan car rental industry through 2034: electrification of rental fleets aligned with Japan's 2035 EV mandate, integration of car rental into multimodal tourism booking platforms, and acceleration of corporate fleet outsourcing replacing owned vehicle models with subscription and long-term rental contracts offering cost certainty and maintenance inclusion.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Japan car rental industry stakeholders including senior operations managers, corporate travel procurement managers, airport authority representatives, inbound tourism operators, and automotive OEM fleet sales teams, conducted in 2024–2025 across major Japanese cities and regional tourism centers.

Secondary Research

Key secondary sources include Japan Tourism Agency inbound visitor statistics, Japan Automobile Rental Association (JARA) fleet and revenue data, Ministry of Land, Infrastructure, Transport and Tourism road transport statistics, Japan Automobile Dealers Association new vehicle registration data, and corporate annual reports and investor presentations from major market participants.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating Japan GDP growth rates, inbound tourist arrival projections, domestic mobility behavior data, corporate fleet transition trends, and sensitivity analysis on EV adoption rate scenarios through 2034.

Japan Car Rental Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Booking Types Covered | Offline Booking, Online Booking |

| Rental Lengths Covered | Short Term, Long Term |

| Vehicle Types Covered | Luxury, Executive, Economy, SUVs, Others |

| Applications Covered | Leisure/Tourism, Business |

| End-Users Covered | Self-Driven, Chauffeur-Driven |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Toyota Rent-a-Car, Nippon Rent-A-Car Service Inc., Orix Auto Corporation, Times Mobility Co., Ltd., OTS Transportation Service Co., Ltd (OTS Rent-a-Car), Idex Auto Japan Co., Ltd. (Budget Rent A Car Japan), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan car rental market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan car rental market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan car rental industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Car Rental Market Report

The Japan car rental market reached USD 3.0 Million in 2025, reflecting post-pandemic tourism recovery, growing inbound visitor volumes, and expanding domestic shared mobility demand across leisure and business segments.

The market is projected to reach USD 5.9 Million by 2034, growing at a CAGR of 7.46% during 2026-2034, driven by tourism expansion, EV fleet transformation, corporate subscription growth, and digital platform adoption.

Leisure/Tourism leads with 66.2% application share in 2025, supported by Japan's record 33.1 million inbound visitors, extensive domestic leisure travel, and seasonal tourism demand at airports and resort destinations.

Self-Driven dominates at 71.5% in 2025, reflecting Japan's well-maintained road infrastructure, GPS navigation availability in rental vehicles, and strong preference among domestic and international tourists for independent travel flexibility.

The Kanto Region commands a dominant 38.4% market share in 2025, driven by Tokyo's dual international airports, the highest corporate activity concentration, and the largest inbound and domestic tourist arrival volumes in Japan.

Leisure/Tourism is the fastest-growing application at ~8.1% CAGR through 2034, driven by Japan's inbound tourism growth target of 60 million visitors by 2030 and regional tourism diversification programs expanding rental demand.

Leading companies include Toyota Rent-a-Car, Nippon Rent-A-Car Service Inc., Orix Auto Corporation, OTS Transportation Service Co., Ltd. (OTS Rent-a-Car), Times Mobility Co., Ltd., Idex Auto Japan Co., Ltd (Budget Rent A Car Japan), and others.

Key drivers include inbound tourism expansion, digital platform and mobile booking growth, corporate fleet rationalization, EV tourism positioning, and multimodal travel integration across Shinkansen and air travel connections.

EV fleet integration is a transformative growth driver, enabling operators to serve Japan's green tourism premium segment. Toyota bZ4X, and Nissan Leaf are progressively replacing petrol fleet vehicles at major airport rental locations.

Leisure rental is driven by airport pick-up, scenic route exploration, and inbound tourist itineraries, typically shorter term and price-sensitive. Business rental serves corporate travel, executive transportation, and long-term fleet substitution.

Kanto dominates through Tokyo's Narita and Haneda airport gateway volumes, Japan's highest concentration of corporate headquarters requiring business travel support, and the largest domestic and inbound tourist base accessing regional Japan from the capital.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)