Japan Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Region, 2026-2034

Japan Data Center Market Size, Share, Trends & Forecast (2026-2034)

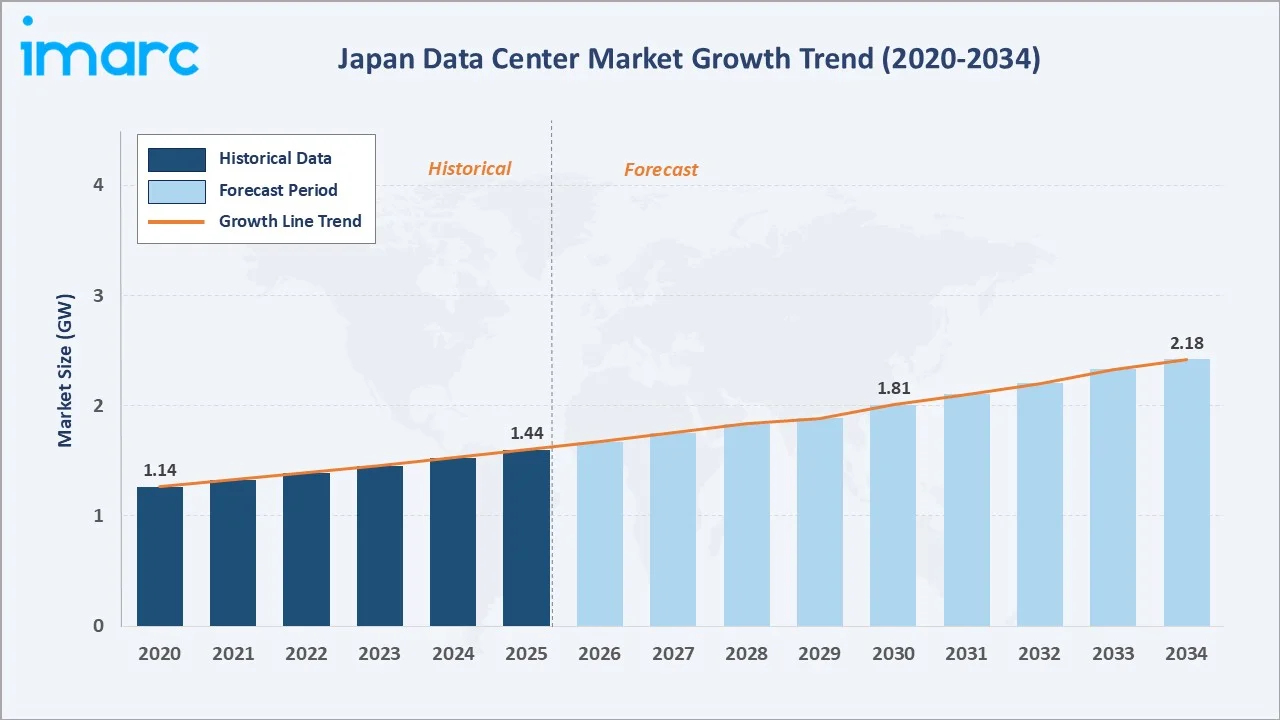

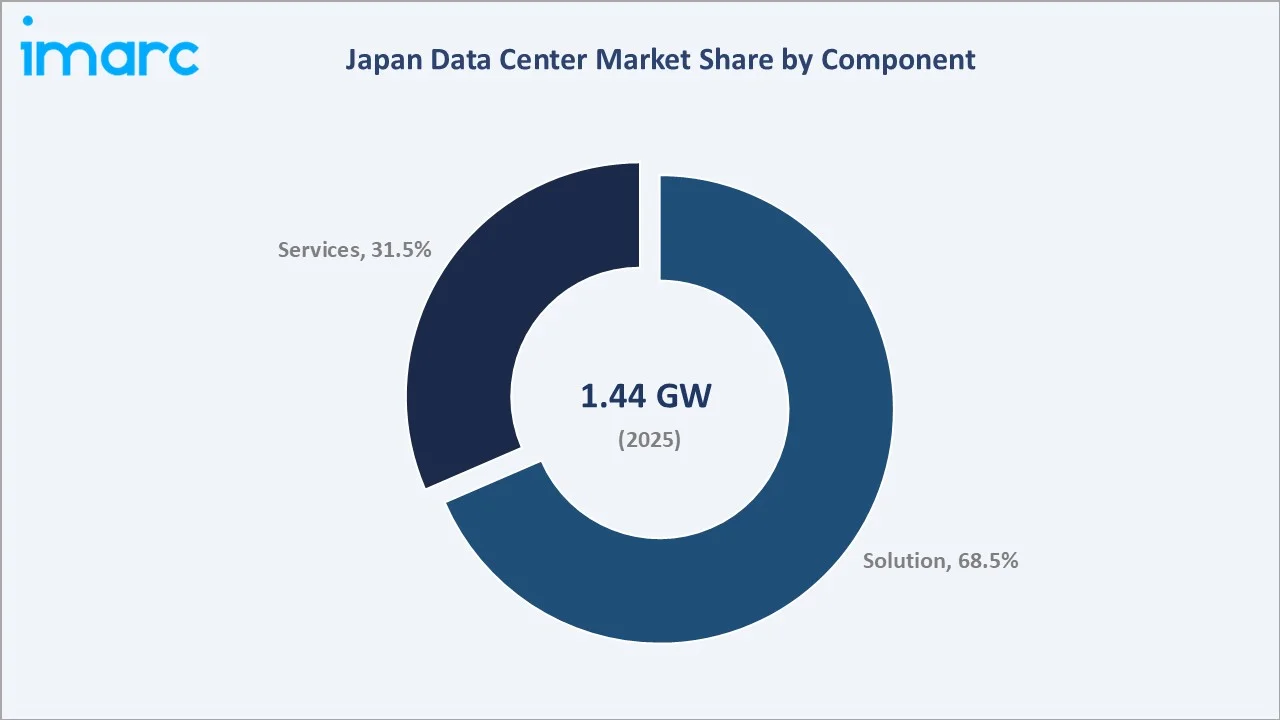

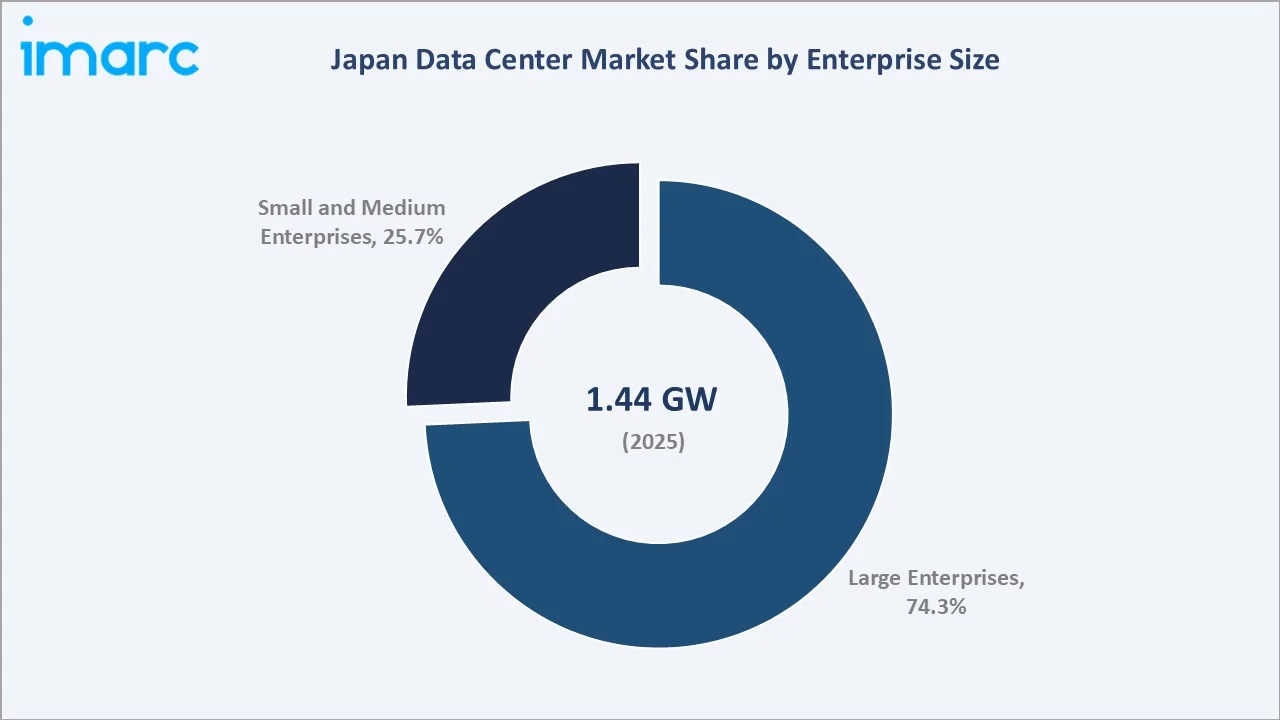

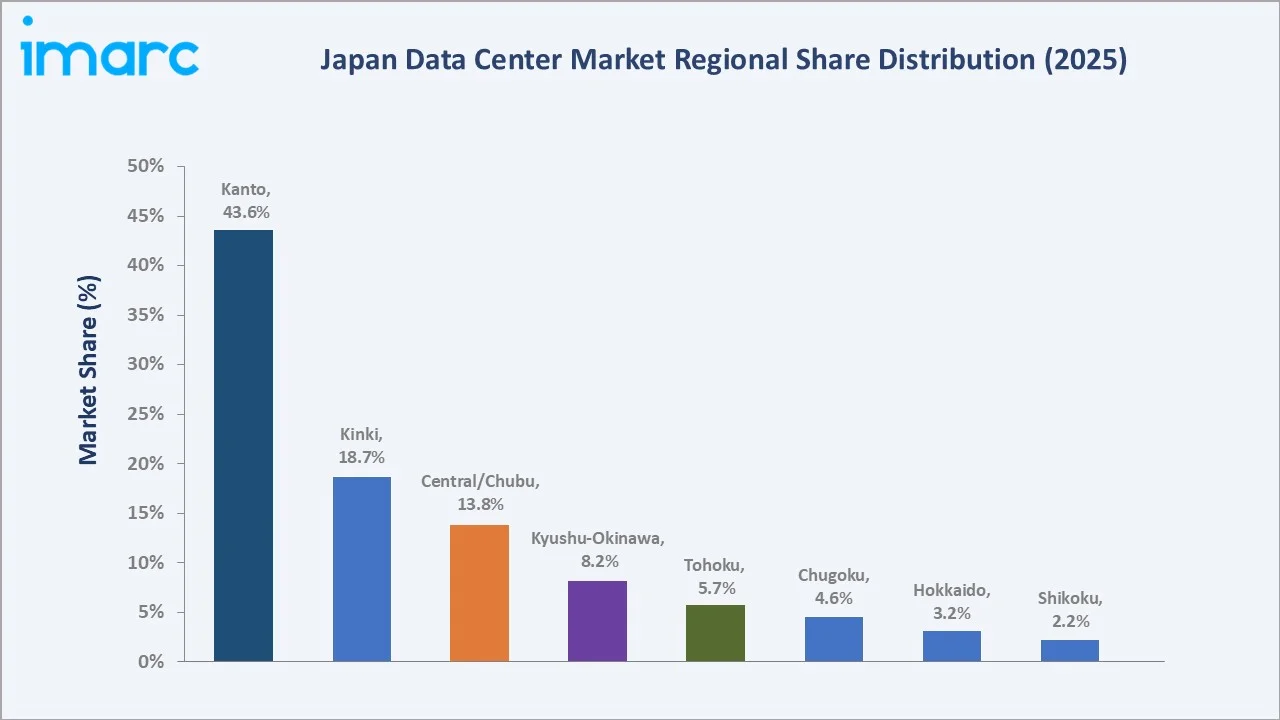

The Japan data center market reached 1.44 GW in 2025 and is projected to reach 2.18 GW by 2034, growing at a CAGR of 4.74% during 2026-2034. The market is driven by rising cloud adoption, AI workloads, 5G rollout, and enterprise digital transformation. Japan has 219 data centers as of March 2024, and its 10th global ranking highlights the country’s strong digital infrastructure base. Tight supply-demand conditions, especially in Greater Tokyo, along with a 51.0 trillion yen ICT industry, are driving continuous investments in new data center capacity. Solution leads component at 68.5%. Large enterprises lead in enterprise size at 74.3%. Kanto region leads at 43.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

1.44 GW |

|

Forecast Market Size (2034) |

2.18 GW |

|

CAGR (2026-2034) |

4.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Solution (68.5%, 2025) |

|

Dominant Enterprise Size |

Large Enterprises (74.3%, 2025) |

|

Leading Region |

Kanto Region (43.6%, 2025) |

The Japan data center market has shown steady expansion, increasing from 1.14 GW in 2020 to 1.44 GW in 2025. This growth reflects rising demand for cloud computing, colocation services, AI workloads, and enterprise digital transformation. The market is expected to reach 1.81 GW by 2030 as hyperscale operators continue expanding capacity. By 2034, it is forecast to grow further to 2.18 GW, supported by strong ICT infrastructure, 5G deployment, and growing data localization needs.

To get more information on this market, Request Sample

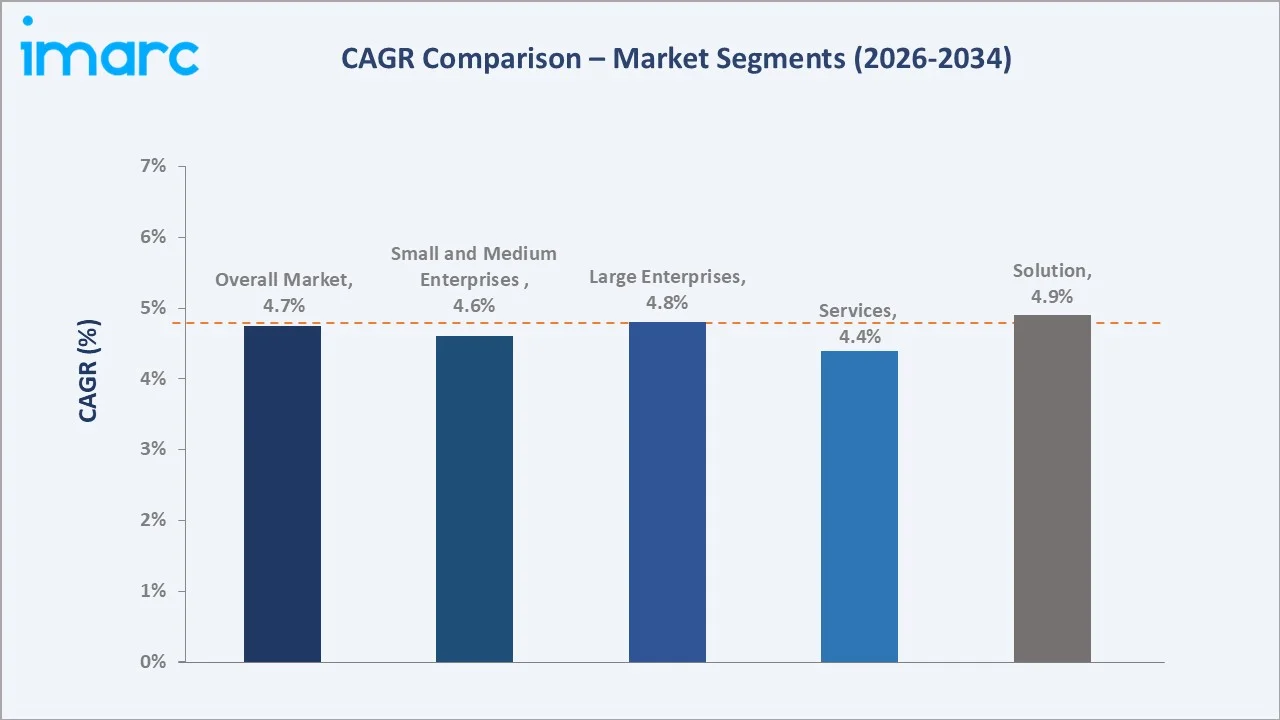

Solution component grows fastest at ~4.9% CAGR through AI GPU compute cluster, liquid cooling, and UPS power infrastructure investment. Large enterprises grow at ~4.8% CAGR through Japan megabank FSI and hyperscaler cloud colocation.

Executive Summary

The Japan data center market is expanding steadily, supported by rapid cloud adoption, AI workloads, 5G rollout, and enterprise digitization. Capacity growth is concentrated around Greater Tokyo and Osaka, where hyperscale and colocation demand remains strong. Tight supply conditions are encouraging new investments in high-density, energy-efficient facilities. Japan’s large ICT economy and strong connectivity ecosystem provide a solid foundation for long-term data center development. Growing demand for data security, low-latency services, and disaster-resilient infrastructure is further shaping market expansion. Solution at 68.5% leads through IT hardware infrastructure. Large enterprises at 74.3% lead through FSI and hyperscaler colocation. Kanto region leads at 43.6%.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Solution - 68.5% share (2025) |

|

Dominant Enterprise Size |

Large Enterprises - 74.3% market share (2025) |

|

Leading Region |

Kanto Region - 43.6% share (2025) |

|

Market Opportunity |

Green renewable energy DC; 5G edge computing; quantum computing APAC hub low-latency Japan |

Key Analytical Observations Supporting The Above Data:

- Solution at 68.5%: Solution dominates as enterprises prioritize integrated infrastructure, cloud, colocation, power, cooling, and security solutions to support AI, digital transformation, and mission-critical workloads.

- Large Enterprises at 74.3%: Large enterprises dominate due to their high-volume demand for secure, scalable, and reliable IT infrastructure. Their strong adoption of cloud, AI, big data, and disaster recovery solutions further drives data center capacity use.

- Kanto Region at 43.6%: Kanto Region dominates due to the concentration of Tokyo’s financial, technology, telecom, and enterprise demand. Strong connectivity, cloud adoption, and hyperscale investments further support its leading position.

Japan Data Center Market Overview

The Japan data center market encompasses hyperscale, colocation, enterprise, and edge facilities that support cloud computing, AI, telecom, financial services, and government workloads. It includes key infrastructure such as power systems, cooling solutions, networking, storage, security, and monitoring platforms. The market is concentrated in major digital hubs such as Kanto and Kansai due to strong connectivity and enterprise demand. Growth is driven by rising cloud migration, 5G adoption, data localization, and the need for secure, low-latency digital infrastructure. Macroeconomic factors include Japan’s large ICT sector, high enterprise digital spending, and steady cloud infrastructure investment. Urbanization, 5G rollout, AI adoption, and demand for energy-efficient infrastructure further support data center market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

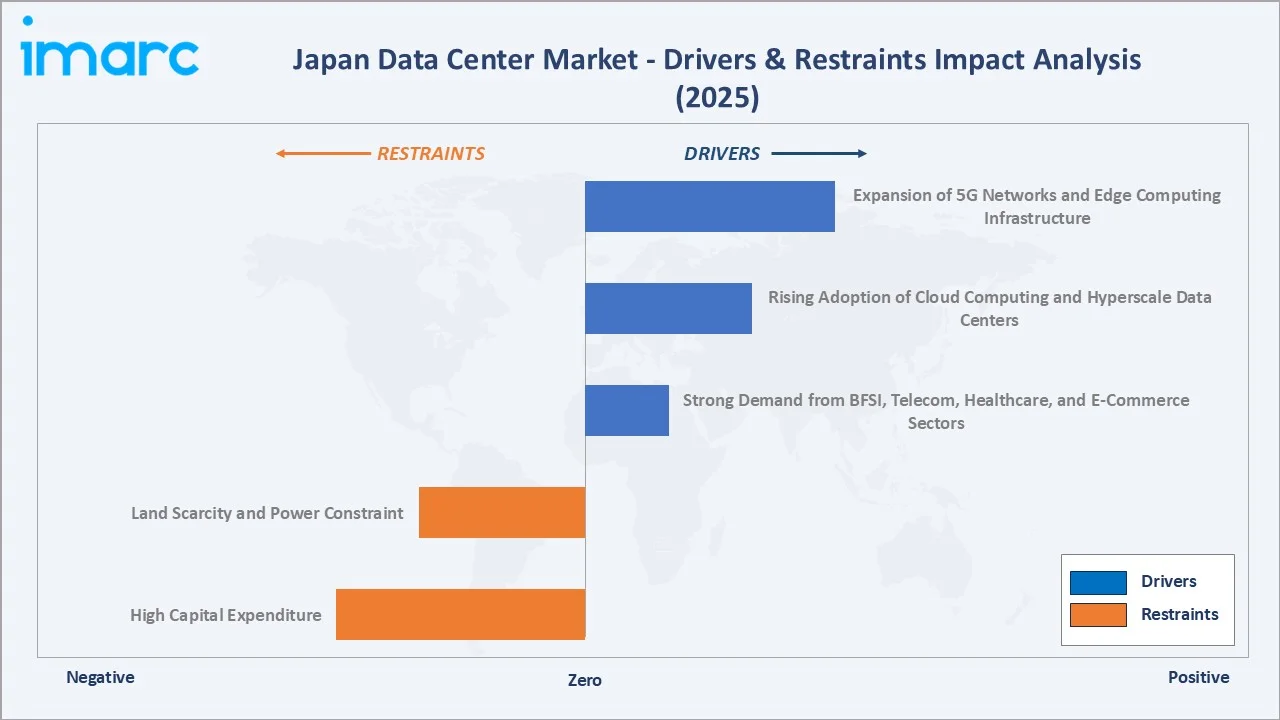

Market Drivers

- Expansion of 5G Networks and Edge Computing Infrastructure: Expansion of 5G networks and edge computing infrastructure is increasing demand for low-latency, high-speed data processing closer to end users. Fitch projects Japan will have around 45 million 4G subscriptions and over 151 million 5G subscriptions by 2029. As telecom operators, cloud providers, and enterprises deploy 5G-enabled applications, demand rises for distributed edge data centers. This supports real-time services such as autonomous systems, smart factories, IoT, gaming, and video streaming.

- Rising Adoption of Cloud Computing and Hyperscale Data Centers: Rising adoption of cloud computing and hyperscale data centers increasing demand for large-scale, secure, and high-capacity digital infrastructure. In June 2026, At Tokyo collaborated with Zadara to launch a sovereign AI cloud platform in Japan, hosted within At Tokyo’s data centers as the Zadara Cloud At Tokyo Region. The partnership will introduce ATBeX Edge Compute Powered by Zadara, an integrated edge cloud service combining compute, storage, and networking for AI workloads. The service will leverage At Tokyo’s ATBeX network fabric, which connects over 100 domestic and global network operators and cloud services, and is expected to be available from August 2026. This is accelerating investment in energy-efficient, high-density data centers across major hubs.

- Strong Demand from BFSI, Telecom, Healthcare, and E-Commerce Sectors: Strong demand from BFSI, telecom, healthcare, and e-commerce sectors is increasing the need for secure, scalable, and always-on digital infrastructure. Banks and insurers require resilient facilities for real-time transactions and compliance, while telecom firms need capacity for 5G and network services. Healthcare digitization and e-commerce growth are also generating large volumes of sensitive and high-speed data. This is boosting demand for colocation, cloud, backup, and disaster recovery data center services.

Market Restraints

- Land Scarcity and Power Constraint: Land scarcity and power constraints are limiting large-scale facility development in key hubs such as Tokyo and Osaka. High land costs, zoning restrictions, and limited space increase project expenses and delay expansion. At the same time, data centers require reliable, high-capacity electricity, but grid availability can be tight in dense urban areas. These constraints push operators to explore secondary locations, invest in efficient power systems, and carefully manage expansion plans.

- High Capital Expenditure: High capital expenditure hampers the market as operators must invest heavily in land, construction, power systems, cooling, security, and network infrastructure. Advanced facilities designed for AI, cloud, and hyperscale workloads require high-density equipment and energy-efficient technologies, increasing upfront costs. These expenses can delay project approvals and limit participation by smaller players. Rising financing, power, and construction costs further pressure profitability and slow capacity expansion.

Market Opportunities

- Expansion of GPU-Intensive Data Centers: The expansion of GPU-intensive data centers presents a significant opportunity as demand for AI, generative AI, machine learning, and high-performance computing continues to rise. Enterprises and hyperscale cloud providers are investing in advanced facilities equipped with high-density racks, liquid cooling, and powerful GPU clusters. As AI adoption accelerates across industries, demand for specialized GPU-enabled data centers is expected to increase substantially.

- Expansion of Next-Generation AI Data Centers: Expansion of next-generation AI data centers is an opportunity as enterprises require advanced infrastructure for generative AI, machine learning, automation, and high-performance computing. In April 2026, NTT DATA officially opened its Keihanna OSK11 Data Center in Kyoto, Japan. The next-generation, AI-ready facility uses advanced high-efficiency cooling and global engineering standards to support rising cloud and AI workload demand. Operated by NTT Global Data Centers, OSK11 strengthens digital infrastructure in the Kansai region, a rapidly growing data center hub in Japan. This opens opportunities for operators to offer premium colocation, sovereign AI cloud, and edge AI services.

Market Challenges

- Power Grid Constraints and Securing Reliable Electricity Supply: Power grid constraints and reliable electricity supply are major challenges as facilities require continuous, high-capacity power to support cloud, AI, and hyperscale workloads. Limited grid availability in dense hubs can delay new projects and increase connection costs. Rising power demand also makes energy procurement, backup systems, and redundancy planning more complex. Operators must invest in efficient power management, renewable energy sourcing, and resilient backup infrastructure to maintain uptime.

- Shortage of Skilled Data Center Engineering and Operations Talent: Shortage of skilled data center engineering and operations talent is challenging as advanced facilities require experts in power systems, cooling, networking, cybersecurity, and uptime management. As AI and hyperscale data centers expand, demand for specialized technicians and engineers is rising faster than talent availability. This can increase labor costs, delay commissioning, and affect operational efficiency. Operators may need to invest more in training, automation, and partnerships to maintain reliable 24/7 performance.

Emerging Market Trends

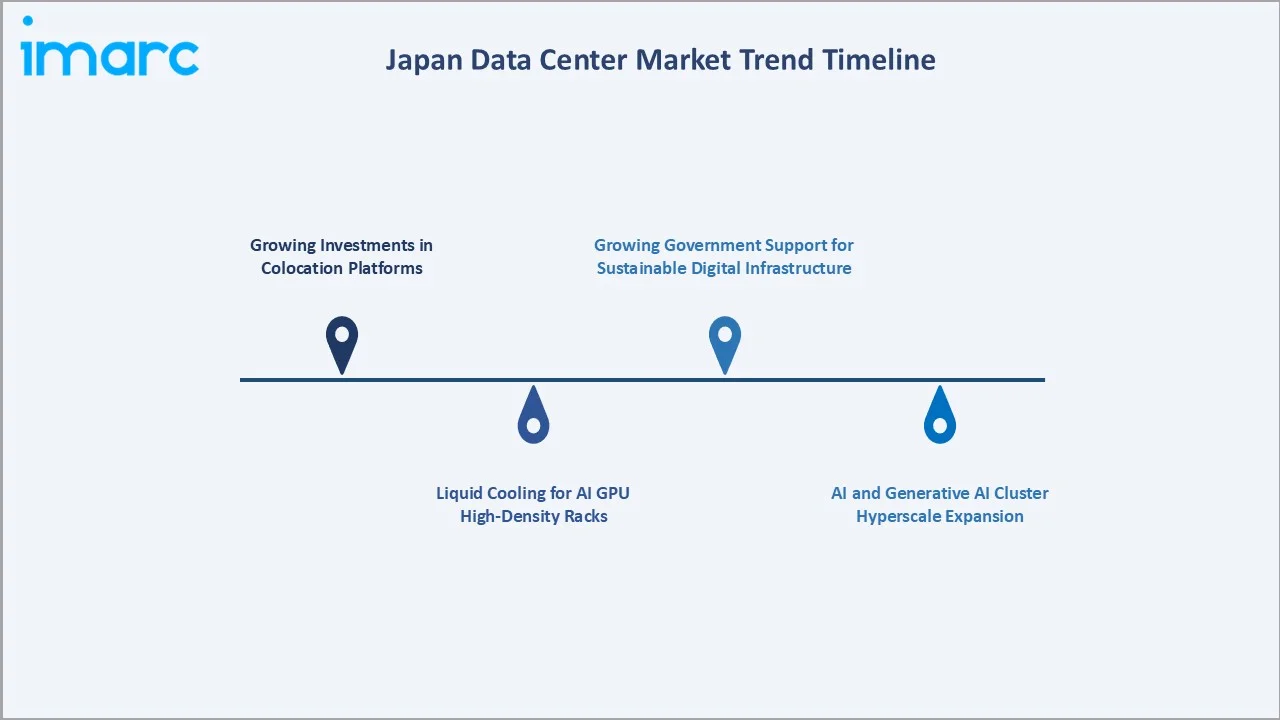

1. Growing Investments in Colocation Platforms

Growing investments in colocation platforms are emerging as infrastructure funds and global investors seek stable, long-term digital infrastructure assets. In June 2026, DigitalBridge Group and JEXI launched Nippon Gateway Infrastructure, a new colocation data center platform in Japan. The platform begins with former NEC data center assets in Greater Tokyo and Greater Osaka, including facilities in Kanagawa and Hyogo prefectures. NEC will remain the anchor customer, while the sites will also be opened to additional colocation clients. This trend is expanding colocation capacity across key hubs.

2. Liquid Cooling for AI GPU High-Density Racks

Liquid cooling for AI GPU high-density racks is emerging as AI and high-performance computing workloads generate significantly more heat than conventional servers. Operators are adopting direct-to-chip and immersion cooling technologies to improve thermal efficiency while reducing energy consumption. These advanced cooling systems enable higher rack densities, better performance, and lower power usage effectiveness (PUE). As AI-ready data centers expand, liquid cooling is becoming a critical requirement for next-generation infrastructure.

3. AI and Generative AI Cluster Hyperscale Expansion

AI and generative AI cluster hyperscale expansion is emerging as cloud providers and enterprises require massive computing capacity for model training, inference, automation, and data analytics. This is driving demand for hyperscale facilities with GPU clusters, high-density racks, advanced cooling, and resilient power systems. Operators are expanding AI-ready campuses in major hubs. The trend is also encouraging investment in sovereign AI cloud, edge AI, and sustainable high-performance data center infrastructure.

4. Growing Government Support for Sustainable Digital Infrastructure

Growing government support for sustainable digital infrastructure is emerging as Japan promotes low-carbon data center technologies and cleaner operations. Public-backed programmes are encouraging R&D, testing, and commercialization of energy-efficient cooling, power management, and emissions-reduction solutions. In May 2026, Japan introduced a government-backed programme to develop and test low-carbon technologies for data centres as digital infrastructure and generative AI demand increase. The initiative, led by the environment ministry with the Ministry of Internal Affairs and Communications, will support projects that reduce CO₂ emissions from data centres and related infrastructure. It aligns with Japan’s 2030, 2035, and 2040 emissions targets and its carbon neutrality goal for 2050. This is pushing operators to align new capacity expansion with national carbon-neutrality goals.

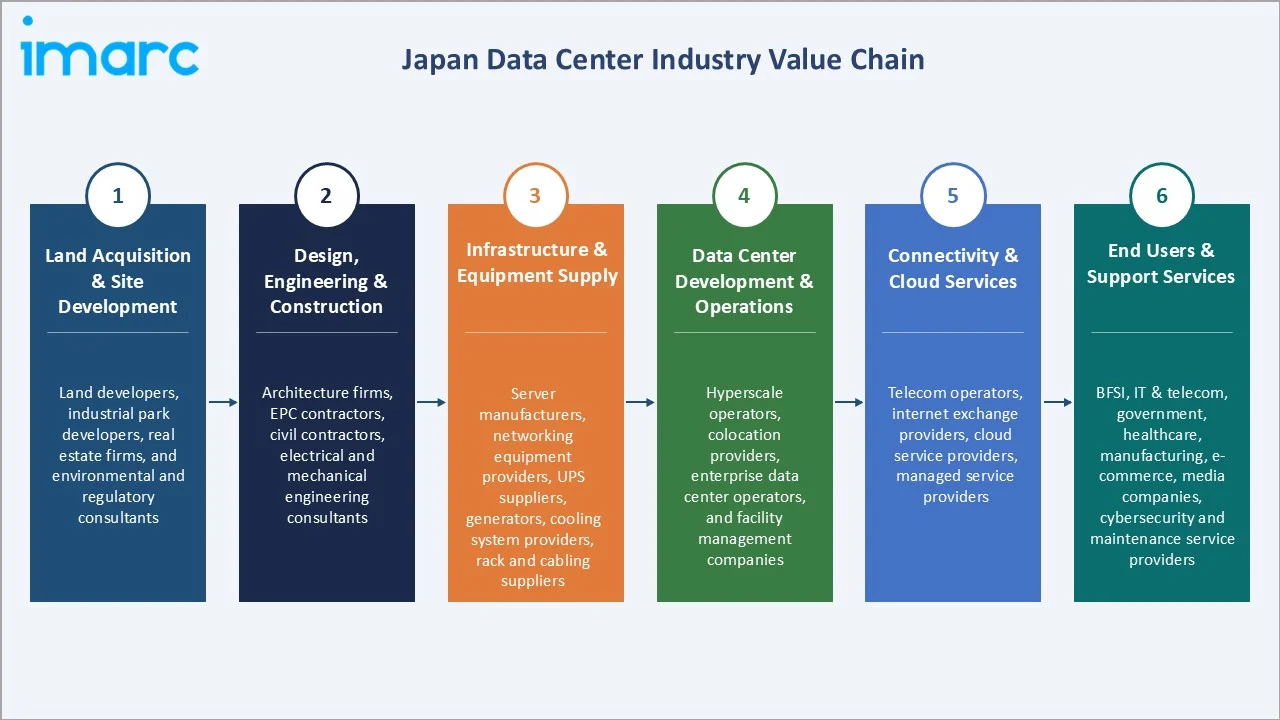

Industry Value Chain Analysis

The Japan data center value chain integrates land acquisition & site development, design, engineering & construction, infrastructure & equipment supply, data center development & operations, connectivity & cloud services, and end users & support services.

|

Stage |

Key Participants |

|

Land Acquisition & Site Development |

Land developers, industrial park developers, real estate firms, and environmental and regulatory consultants |

|

Design, Engineering & Construction |

Architecture firms, EPC contractors, civil contractors, electrical and mechanical engineering consultants |

|

Infrastructure & Equipment Supply |

Server manufacturers, networking equipment providers, UPS suppliers, generators, cooling system providers, rack and cabling suppliers |

|

Data Center Development & Operations |

Hyperscale operators, colocation providers, enterprise data center operators, and facility management companies |

|

Connectivity & Cloud Services |

Telecom operators, internet exchange providers, cloud service providers, and managed service providers |

|

End Users & Support Services |

BFSI, IT & telecom, government, healthcare, manufacturing, e-commerce, media companies, cybersecurity and maintenance service providers |

Data center development & operations is the most value-added stage in the Japan data center market, as it generates recurring revenue through colocation, cloud hosting, managed services, and infrastructure leasing. Operators create value by ensuring high uptime, security, energy efficiency, and scalability for mission-critical workloads. The growing adoption of AI, cloud computing, and hyperscale infrastructure further enhances profitability and long-term customer retention in this stage.

Technology Landscape in the Japan Data Center Industry

AI and Compute Technology

AI and compute technology are driving demand for GPU-intensive infrastructure, high-density server racks, and AI-optimized computing platforms. Data center operators are investing in advanced processors, accelerated computing, and high-speed networking to support generative AI, machine learning, and high-performance computing workloads. This is also accelerating the adoption of liquid cooling, intelligent workload management, and AI-ready hyperscale facilities. As AI deployment expands across industries, compute technology is becoming a key differentiator for next-generation data centers.

Hyperscale Data Center Technology

Hyperscale data center technology enables the development of large-scale, AI-ready campuses with modular and highly scalable designs. These facilities support hyperscale cloud providers and enterprise customers through high-density computing, resilient power infrastructure, and ultra-fast network connectivity. In April 2026, NTT DATA Group began developing the Tokyo TKY12 data center campus in Chiba Prefecture. The six-building hyperscale complex will provide around 200 MW of IT capacity and expand the Inzai-Shiroi data center cluster. Led by NTT Global Data Centers, the first phase is expected to start service in 2030 or later after utility power connections are completed, supporting rising cloud and AI infrastructure demand in Japan. Operators are adopting multi-building campus models to accommodate growing cloud, AI, and big data workloads while allowing phased capacity expansion.

Power and Cooling Technology

Power and cooling technology is shaping the Japan data center industry as operators focus on handling rising energy loads from cloud, AI, and hyperscale workloads. Advanced UPS systems, backup generators, intelligent power distribution, and renewable energy integration are becoming central to facility design. At the same time, liquid cooling, high-efficiency chillers, and thermal management systems are gaining importance for high-density racks. These technologies improve uptime, reduce energy consumption, and support sustainable data center expansion.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

68.5% |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Enterprise Size |

Large Enterprises |

74.3% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

43.6% |

2025 |

By Component

Solution leads at 68.5% (2025) through IT server infrastructure, storage systems, network infrastructure, UPS power systems, and cooling systems.

To access detailed market analysis, Request Sample

Services at 31.5% reflect colocation services, managed services, professional services, and cloud infrastructure services. Services grow at ~4.4% CAGR through growing managed outsourcing and hyperscaler cloud services adoption.

By Enterprise Size

Large enterprises lead at 74.3% (2025), due to their high demand for secure, scalable, and reliable digital infrastructure. Their growing use of cloud, AI, big data, and disaster recovery solutions drives strong data center capacity consumption.

Small and medium enterprises at 25.7% by increasingly adopting cloud computing, SaaS applications, and digital transformation solutions to improve operational efficiency. As many SMEs prefer colocation and managed hosting over building in-house IT infrastructure, demand for scalable and cost-effective data center services continues to grow.

Regional Market Insights

|

Region |

Share (2025) |

Key Japan Data Center Market Drivers & Characteristics |

|

Kanto Region |

43.6% |

Reflecting its position as the country's primary digital infrastructure hub. Strong demand from hyperscale cloud providers, financial institutions, internet exchanges, and enterprise customers. |

|

Kinki Region |

18.7% |

Growing investments in AI-ready facilities, enterprise colocation, and disaster recovery infrastructure are supporting sustained market growth. |

|

Central/Chubu Region |

13.8% |

Reflecting increasing demand from manufacturing, automotive, and industrial enterprises. Lower land costs and improved connectivity are attracting new hyperscale and enterprise data center developments. |

|

Kyushu-Okinawa Region |

8.2% |

Reflecting growing investments in regional cloud infrastructure and edge computing. Improved renewable energy availability and government initiatives are supporting future capacity expansion. |

|

Tohoku Region |

5.7% |

Reflecting rising demand for disaster recovery, backup facilities, and regional cloud deployments. |

|

Chugoku Region |

4.6% |

Reflecting steady enterprise digitalization and increasing demand for regional connectivity. |

|

Hokkaido Region |

3.2% |

The region's cooler climate offers natural cooling advantages that can improve energy efficiency and reduce operating costs. |

|

Shikoku Region |

2.2% |

Reflecting gradual growth in regional cloud adoption and enterprise IT modernization. |

Kanto's 43.6% dominance is driven by the concentration of hyperscale cloud providers, internet exchanges, financial institutions, and enterprise headquarters in Greater Tokyo. Kinki's 18.7% is supported by strong digital transformation, AI infrastructure investments, and disaster recovery deployments centered around Osaka.

Chubu's 13.8% is due to rising demand from manufacturing, automotive, and industrial enterprises. Kyushu-Okinawa's 8.2% is attracting investments in edge computing and renewable energy-powered facilities. Tohoku's 5.7%, Chugoku's 4.6%, Hokkaido's 3.2%, and Shikoku’s 2.2% are gradually expanding their presence, benefiting from lower land costs, improved connectivity, and growing regional cloud adoption.

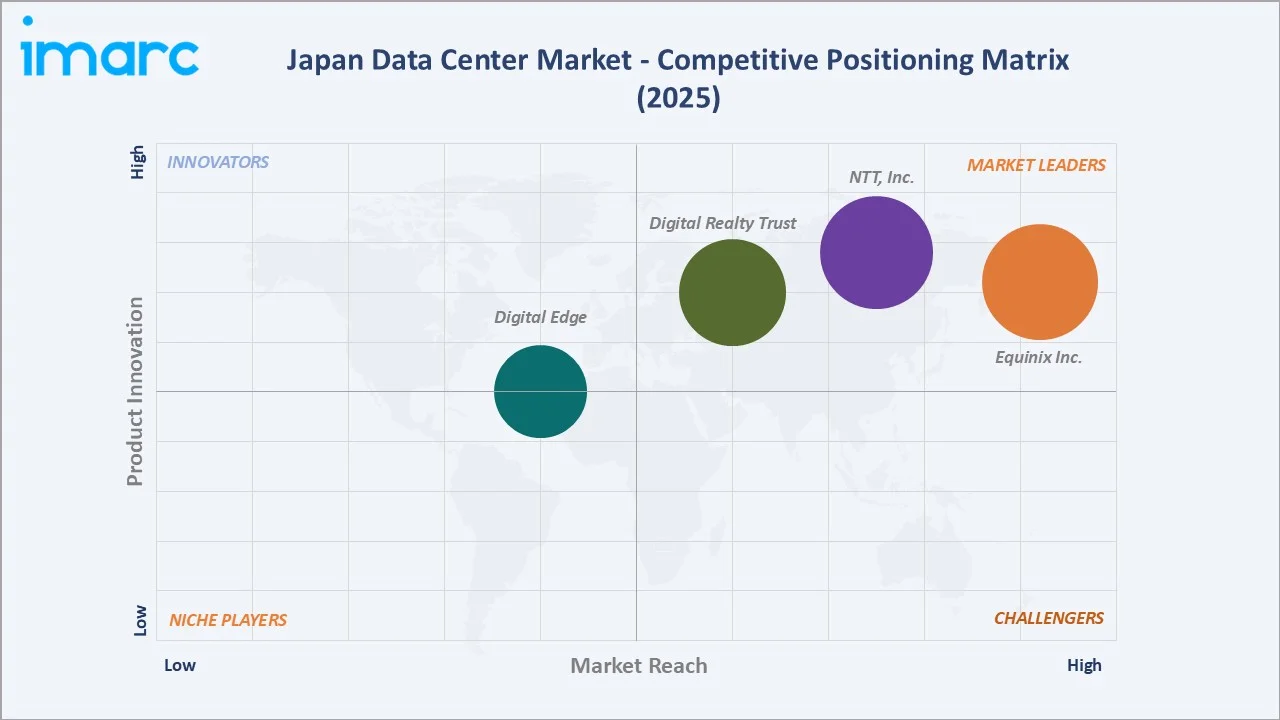

Competitive Landscape

The Japan data center market is moderately competitive, with global hyperscale, colocation, telecom, and cloud infrastructure providers expanding capacity. Key players focus on AI-ready campuses, high-density racks, renewable energy sourcing, and advanced cooling technologies. Competition is strongest in Greater Tokyo and Osaka due to connectivity, enterprise demand, and hyperscale cloud deployments.

|

Company |

Key Data Center Locations |

Market Position |

Core Strength |

|

Equinix Inc. |

Osaka, Tokyo |

Market Leader |

Equinix, Inc. serves as the digital infrastructure backbone in Japan, providing carrier-neutral colocation, cloud interconnection, and AI-ready infrastructure across Tokyo and Osaka. |

|

NTT, Inc. |

Osaka, Kyoto, Tokyo |

Market Leader |

NTT, Inc. acts as one of the primary builders, operators, and innovators of digital infrastructure in Japan, managing a vast network of carrier-neutral data centers. Their role centers around providing high-capacity, AI-ready infrastructure to support enterprise modernization, cloud computing, and advanced workloads. |

|

Digital Realty Trust |

Osaka, Tokyo |

Market Leader |

Digital Realty Trust’s role in Japan's data center market is primarily driven by MC Digital Realty, a successful 50/50 joint venture with Mitsubishi Corporation. This strategic alliance bridges Digital Realty's global data center platform with Mitsubishi’s local enterprise reach and real estate expertise. |

|

Digital Edge |

Osaka, Tokyo |

Established Player |

Digital Edge is a key player in Japan's rapidly growing data center market. Backed by Stonepeak, the Singapore-based firm rapidly established a major footprint in the Greater Tokyo and Osaka regions to support escalating cloud computing, AI, and IT infrastructure demands. |

Operators are also pursuing acquisitions, partnerships, and phased campus developments to secure capacity faster. Sustainability, uptime reliability, low latency, and scalable power availability remain key competitive differentiators.

Key Company Profiles

Equinix Inc.

Equinix Inc. is one of the leading digital infrastructure and colocation providers, with a strong presence in Japan through its data centers across Tokyo and Osaka. The company offers carrier-neutral colocation, interconnection, cloud connectivity, and digital infrastructure solutions to enterprises, cloud service providers, network operators, and financial institutions. Equinix serves as a key connectivity hub, enabling hybrid and multi-cloud deployments while supporting AI, edge computing, and digital transformation initiatives. Its continued investments in high-density, sustainable, and interconnected data center infrastructure reinforce its position as a major player in the Japan data center market.

- Key Data Center Locations: Osaka, Tokyo.

- Recent Developments: In June 2024, Equinix opened OS4x, its fourth data center in Osaka, Japan, under its hyperscale xScale platform. The facility expands the company’s Osaka capacity to serve cloud service providers with high power density, large-scale deployment capability, and flexible customization. OS4x is also equipped with chillers and piping in each data hall to support liquid cooling, including direct-to-chip cooling and rear-door heat exchangers.

- Strategic Focus: Centers on expanding carrier-neutral colocation, interconnection, and hybrid cloud connectivity across Tokyo and Osaka. The company emphasizes high-density, secure, and scalable digital infrastructure to support cloud, AI, fintech, enterprise, and network service demand.

NTT, Inc.

NTT, Inc. is one of the leading data center and digital infrastructure providers in Japan, operating through NTT Global Data Centers and related group companies. The company offers hyperscale, colocation, cloud connectivity, managed infrastructure, and enterprise IT solutions to domestic and international customers. In Japan, NTT has a strong presence across major data center hubs such as Tokyo, Kyoto, and Osaka, supported by its telecom backbone and enterprise customer base. Its facilities serve hyperscalers, cloud providers, financial institutions, telecom operators, and large enterprises.

- Key Data Center Locations: Osaka, Kyoto, Tokyo.

- Recent Developments: In April 2026, NTT DATA opened its Keihanna OSK11 Data Center in Kyoto, Japan. Designed as a next-generation, AI-ready facility, OSK11 incorporates advanced, high-efficiency cooling technologies and global engineering standards to support growing demand for cloud and AI workloads. The facility, operated by NTT Global Data Centers (GDC), strengthens digital infrastructure in the Kansai region, one of Japan's fastest growing data center markets.

- Strategic Focus: Centers on expanding hyperscale and AI-ready capacity across major hubs such as Tokyo and Osaka. The company is investing in large-scale campuses, high-capacity power infrastructure, advanced cooling, and resilient network connectivity to serve cloud providers, hyperscalers, and large enterprises.

Market Concentration Analysis

The Japan data center market is moderately concentrated. Large operators benefit from high capital strength, established connectivity ecosystems, and access to power and land in key hubs. Greater Tokyo and Osaka remain highly competitive, while secondary regions offer room for new entrants. Rising AI and hyperscale demand are encouraging consolidation, partnerships, and acquisition-led expansion. Smaller operators compete through niche colocation, edge facilities, and regional data center services.

Investment & Growth Opportunities

Highest Growth Segments

AI GPU hyperscale solution (~5.5% CAGR through AI cluster), government cloud services (~5% CAGR), Osaka-Kinki DR region (~5.2% CAGR), Hokkaido green cooling DC (~5.5% CAGR from growing base), liquid cooling technology (~6% CAGR), and Kyushu-Okinawa submarine cable hub (~5% CAGR) represent Japan DC highest-growth investment vectors through 2034.

Investment Themes

- AI GPU hyperscale data centers: Investments are accelerating in AI-ready hyperscale facilities equipped with GPU clusters, liquid cooling, and high-density power infrastructure to support generative AI, machine learning, and high-performance computing workloads.

- Green renewable energy data centers: Growing investments are focused on energy-efficient data centers powered by renewable energy, advanced cooling systems, and carbon reduction technologies to meet sustainability goals and Japan's carbon neutrality commitments.

Future Market Outlook (2026-2034)

The Japan data center market is projected to grow from 1.44 GW in 2025 to 2.18 GW by 2034, delivering a 4.74% CAGR over the forecast period through AI and generative AI GPU cluster hyperscale demand, green renewable energy DC expansion, 5G and edge computing low-latency, and Tokyo-Osaka APAC financial hub submarine cable hub. The market's anchor value of 1.81 GW in 2030 represents Japan DC at AI GPU mainstream and government cloud inflection.

Three structural forces define Japan data center growth through 2034: cloud migration, AI-driven compute demand, and sustainability-led infrastructure modernization. Rising adoption of hyperscale cloud, SaaS, and hybrid IT is increasing demand for large, scalable facilities. Generative AI and GPU-heavy workloads are pushing operators toward high-density racks, liquid cooling, and greater power capacity. At the same time, Japan’s carbon-neutrality goals are accelerating investment in renewable energy, efficient cooling, and low-carbon data center technologies.

Research Methodology

Primary Research

Primary research comprised interviews and discussions with data center operators, colocation providers, cloud service firms, telecom companies, EPC contractors, and equipment suppliers. It also included inputs from enterprise IT heads, facility managers, and industry consultants to validate demand trends, capacity expansion, pricing, and technology adoption across Japan.

Secondary Research

Secondary research encompassed the analysis of company annual reports, investor presentations, government publications, industry associations, regulatory documents, and data center operator announcements. It also included reviews of cloud provider updates, technology journals, market databases, trade publications, and credible news sources to assess market size, capacity additions, investment trends, and the competitive landscape in Japan.

Forecasting Models

Forecasting models incorporated time-series analysis, capacity expansion trends, cloud and AI adoption rates, and macroeconomic indicators to estimate future market growth. The forecasts also considered hyperscale investments, enterprise digital transformation, power availability, and regulatory developments. Multiple scenario analyses were applied to validate long-term demand and ensure robust market projections through 2034.

Japan Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GW |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Solution, Service |

| Types Covered | Colocation, Hyperscale, Edge, Others |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium Enterprises |

| End Users Covered | BFSI, IT And Telecom, Government, Energy and Utilities, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Equinix Inc., NTT Inc., Digital Realty Trust, Digital Edge, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan data center market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan data center market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Data Center Market Report

The Japan data center market reached 1.44 GW in 2025, driven by rising cloud adoption, AI and generative AI workloads, 5G expansion, and growing demand for secure digital infrastructure across BFSI, telecom, healthcare, e-commerce, and government sectors. Increasing hyperscale investments, edge computing needs, and sustainability-focused facility upgrades are further supporting market expansion.

The Japan data center market grows at 4.74% CAGR during 2026-2034, reaching 2.18 GW by 2034. The CAGR reflects AI GenAI GPU demand, APAC hub submarine cable, 5G MEC edge, and disaster recovery BCP structural demand.

Solution leads at 68.5% as enterprises increasingly require integrated services such as colocation, cloud connectivity, managed hosting, security, and infrastructure management. These solutions help customers scale digital operations without building and maintaining costly in-house data center facilities.

Large enterprises lead at 74.3% due to their substantial demand for high-performance computing, cloud infrastructure, AI workloads, and secure data storage. Their large IT budgets and ongoing digital transformation initiatives drive higher adoption of hyperscale and colocation data center services.

Kanto region leads at 43.6% due to Greater Tokyo’s strong concentration of cloud providers, financial institutions, telecom networks, and enterprise headquarters. Its superior connectivity, internet exchanges, and hyperscale investments make it the country’s primary digital infrastructure hub.

Leading companies include Equinix Inc., NTT, Inc., Digital Realty Trust, and Digital Edge, among others.

The market is projected to reach approximately 1.81 GW by 2030, reflecting steady expansion from rising cloud, AI, and enterprise digital infrastructure demand. Growth will be supported by hyperscale campus development, 5G expansion, and increased colocation adoption.

Three priority investment opportunities in the Japan data center market include the development of AI-ready hyperscale campuses equipped with GPU clusters and advanced liquid cooling systems to support generative AI workloads. Significant potential also exists in green and renewable energy-powered data centers, driven by carbon neutrality targets and demand for energy-efficient infrastructure. Additionally, edge and regional colocation facilities present attractive opportunities as 5G deployment, IoT adoption, and low-latency computing requirements expand beyond Tokyo and Osaka into secondary cities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)