Japan Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

Japan Diabetes Market Size, Share, Trends & Forecast (2026-2034)

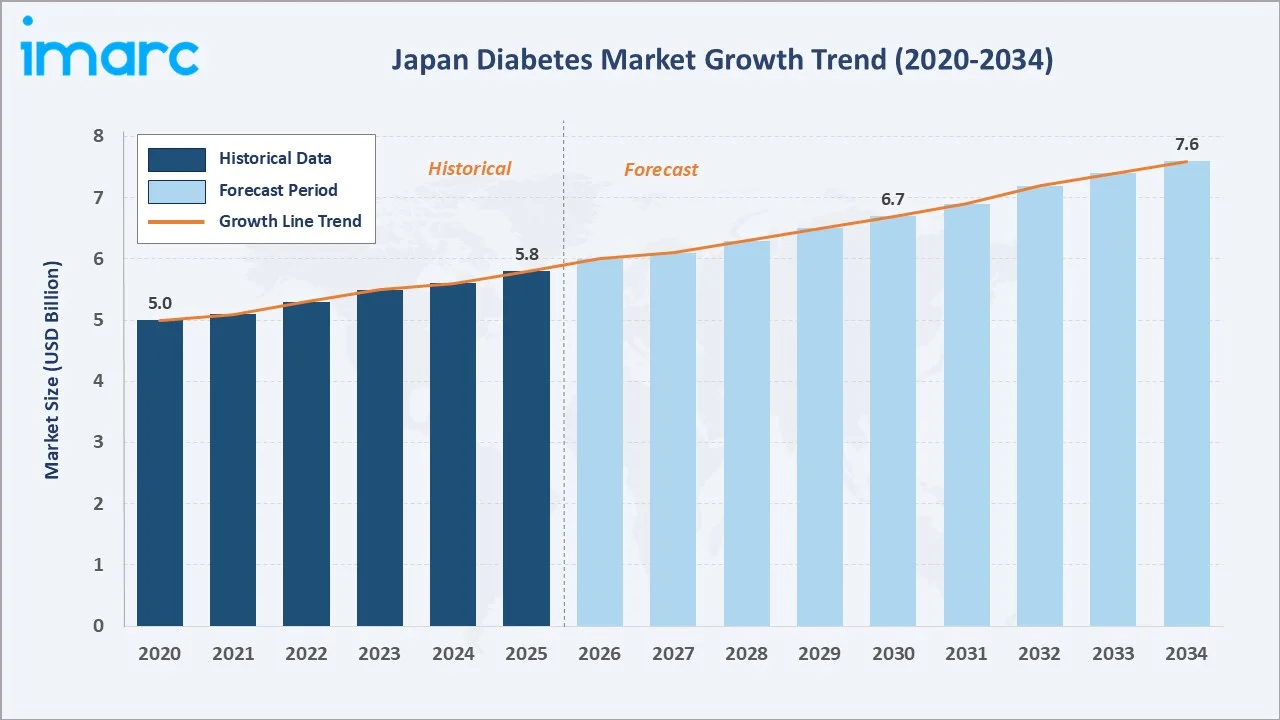

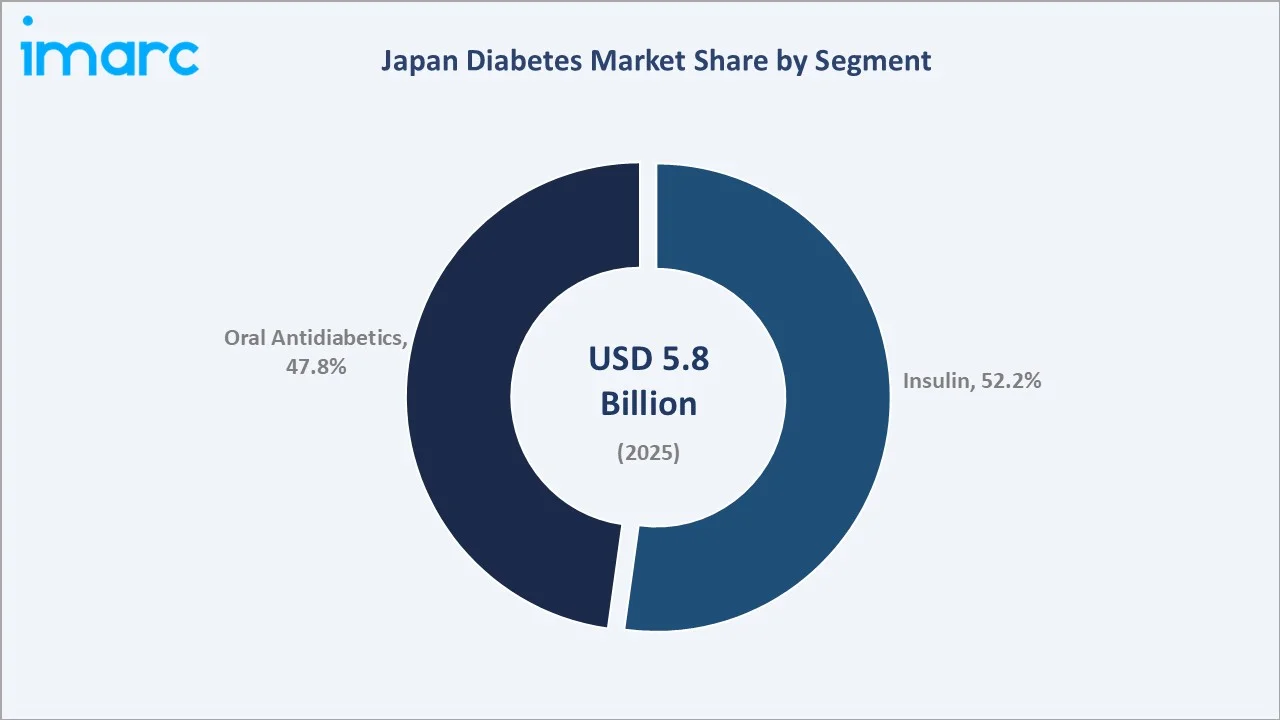

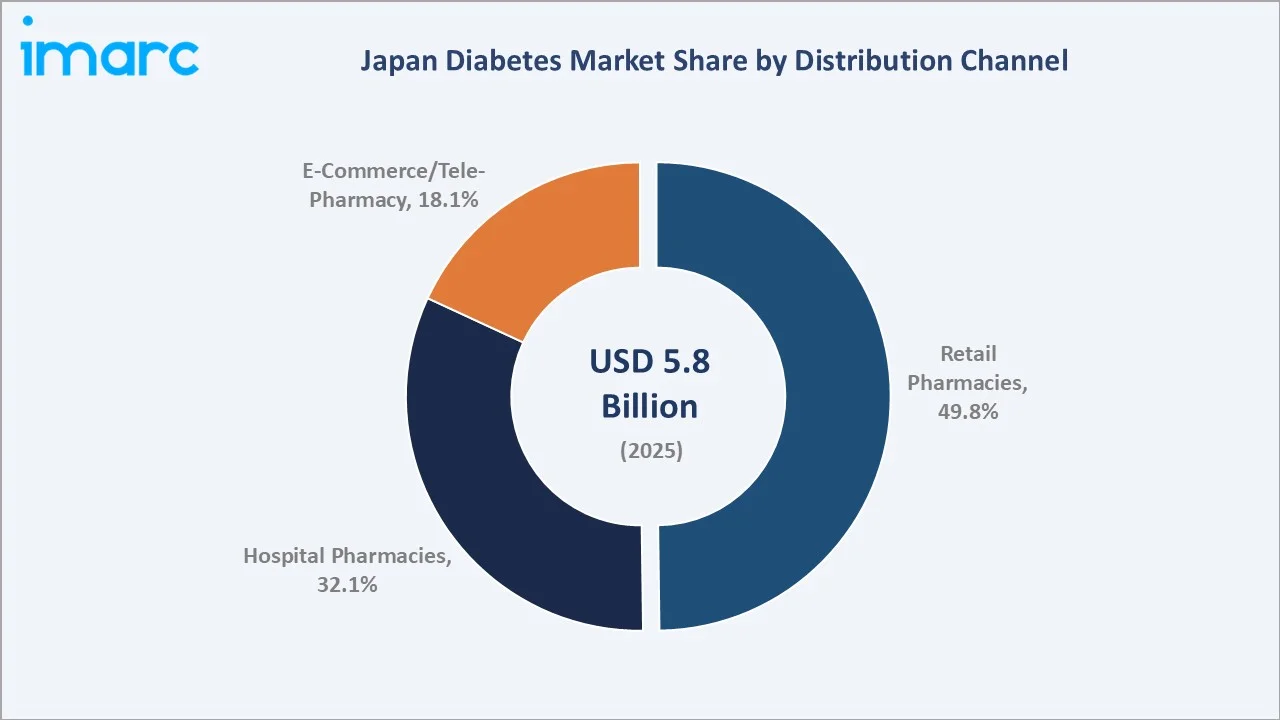

The Japan diabetes market was valued at USD 5.8 Billion in 2025 and is projected to reach USD 7.6 Billion by 2034, growing at a CAGR of 2.95% during 2026-2034. Japan has 10.8 million adults (20–79 years) with diabetes (2024), driven by its rapidly aging population, rising urbanization, and rising obesity cases. Insulin leads at 52.2% segment share, and retail pharmacies dominate the distribution channel at 49.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.8 Billion |

|

Forecast Market Size (2034) |

USD 7.6 Billion |

|

CAGR (2026-2034) |

2.95% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The market grew from USD 5.0 Billion in 2020 to USD 5.8 Billion in 2025, anchored at USD 6.7 Billion in 2030, and is forecast to reach USD 7.6 Billion by 2034. GLP-1 agonist class adoption and continuous glucose monitoring (CGM) device expansion are reshaping Japan's diabetes care economics above baseline health insurance price-cut pressures.

To get more information on this market, Request Sample

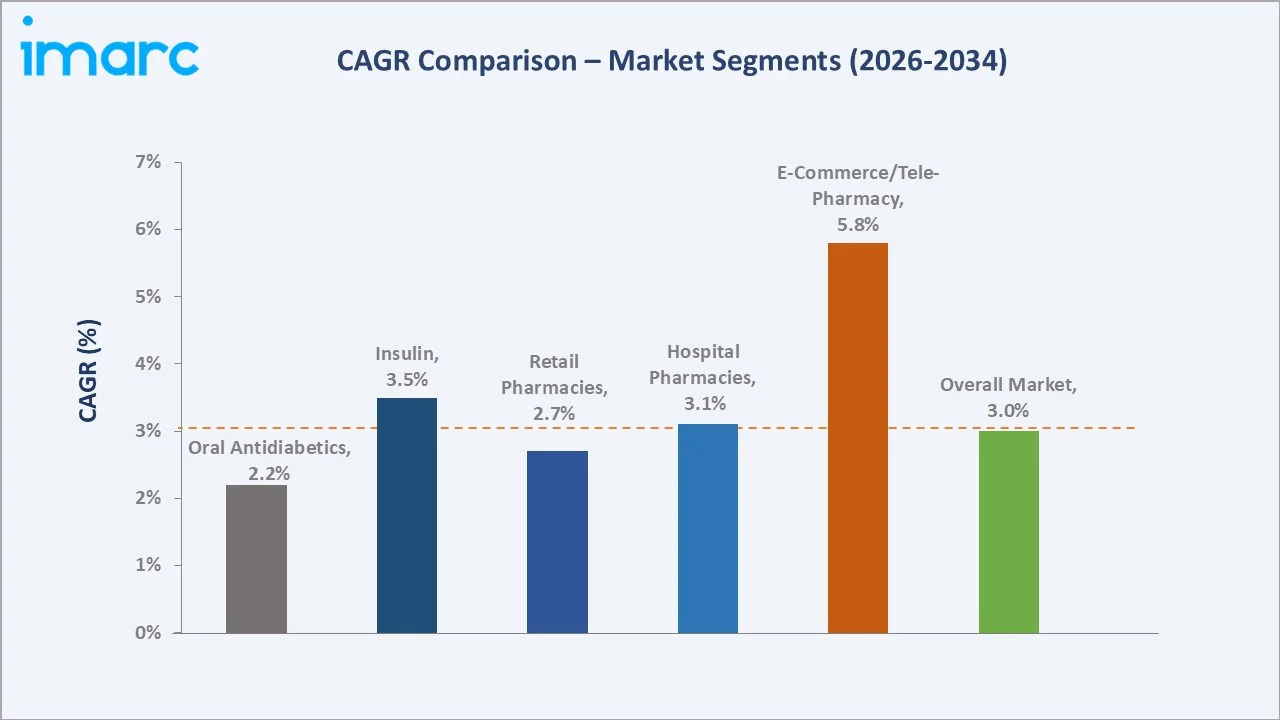

E-commerce/tele-pharmacy grows fastest at ~5.8% CAGR (2026-2034), driven by Japan's expanding online pharmacy regulatory access. Insulin segment grows at ~3.5% CAGR, outpacing oral antidiabetics at ~2.2%, as GLP-1 injectable agonists transition into the insulin category's addressable growth space through 2034.

Executive Summary

The Japan diabetes market reached USD 5.8 Billion in 2025, representing Asia's third-largest diabetes pharmaceutical market. Japan's 10.8 million adults (20–79 years) diagnosed with diabetes face a unique clinical profile, predominantly elderly-onset type-2 diabetes with low obesity rates but high metabolic risk from dietary transition, creating a structurally stable, premium-oriented market underpinned by universal health insurance coverage. Japan's 2.95% CAGR to USD 7.6 Billion by 2034 reflects steady growth constrained by biennial health insurance price revisions but supported by an aging population, GLP-1 class expansion, and CGM technology adoption.

Insulin leads at 52.2% segment share (2025), driven by Japan's sizeable Type-1 patient base and GLP-1 receptor agonist reclassification within the injectable segment. Oral antidiabetics at 47.8% are anchored by metformin generics, DPP-4 inhibitors, and SGLT-2 inhibitors. Retail pharmacies, at 49.8%, remain the primary dispensing channel, while E-commerce at 18.1% grows fastest at ~5.8% CAGR.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Insulin - 52.2% revenue share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies - 49.8% share (2025) |

Key Analytical Observations Supporting the Above Data:

- Insulin at 52.2% (2025) driven by type-1 patients and GLP-1 injectable growth: Japan's type-1 patients require lifelong insulin therapy. GLP-1 receptor agonists are classified within the injectable diabetes drug space, adding structural premium revenue to the insulin-adjacent market.

- Retail Pharmacies at 49.8% anchored by Japan's licensed dispensing pharmacies: Japan's Pharmaceuticals and Medical Devices Act, designed to safeguard public health by establishing regulatory standards governing the production, distribution, and use of pharmaceuticals and medical devices. The act mandates prescription dispensing through licensed pharmacies, forming Japan's organized retail pharmacy backbone for diabetes medication dispensing.

Japan Diabetes Market Overview

Japan's diabetes market encompasses pharmaceutical treatments and monitoring devices for type-1, type-2, and gestational diabetes patients. The ecosystem integrates API suppliers, domestic and multinational pharmaceutical manufacturers, Japan's PMDA regulatory framework, three-tier drug wholesalers, and retail/hospital/e-pharmacy dispensing channels serving 10.8 million patients (2024).

Japan's pharmaceutical market operates under MHLW (Ministry of Health, Labour and Welfare) oversight, with health insurance covering prescription drug costs for enrolled patients. Japan’s statutory health insurance system (SHIS) covers 98.3% of the population, creating near-universal reimbursement access for diabetes medications. Macroeconomic drivers include Japan's elderly population, JPY weakness, increasing imported drug costs, and diabetes prevalence among adults.

Market Dynamics

To evaluate market opportunities, Request Sample

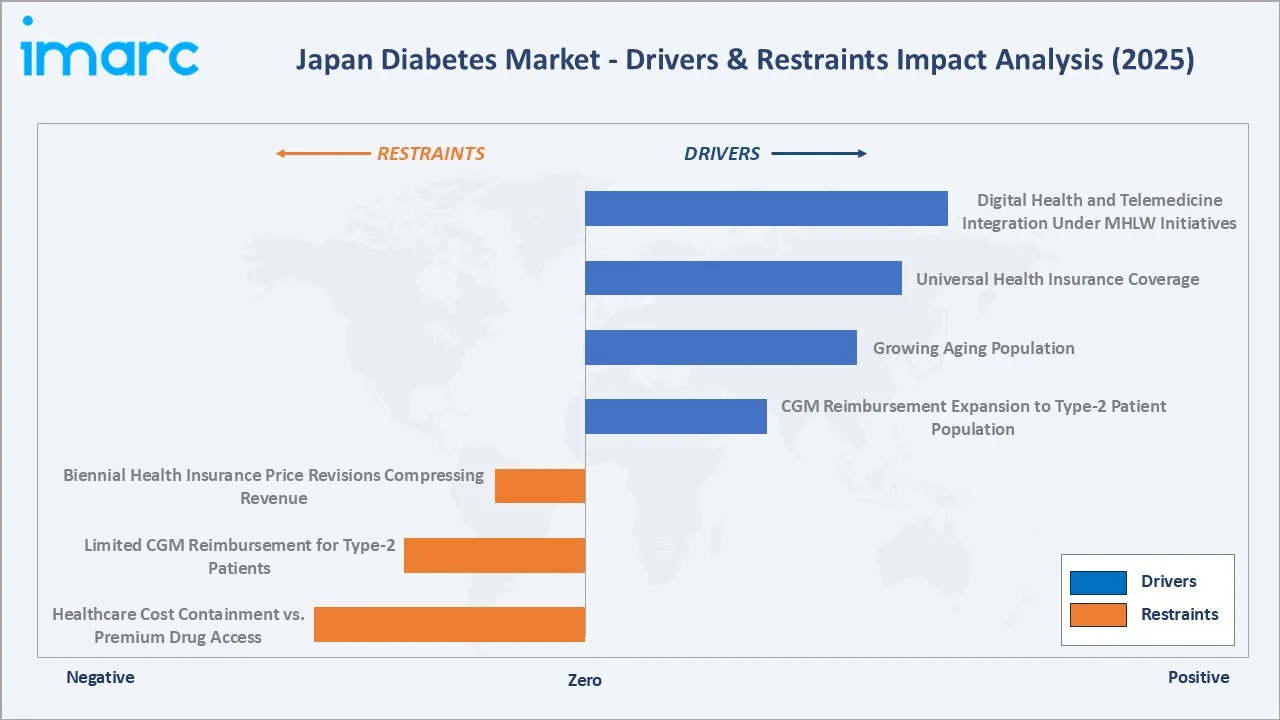

Market Drivers

- Growing Aging Population: Japan's elderly proportion aged 65 or older is projected to reach 46.5% in 2050, compared with 34.9% in 2020. Elderly patients have 20-25% type-2 diabetes prevalence, systematically increasing Japan's per-capita diabetes drug utilization beyond what patient count growth alone suggests. Japan recorded 10.8 million diabetes cases among adults aged 20-79 years in 2024. The patient base grows as Japan's elderly population generates disproportionate type-2 diabetes incidence, creating structural pharmaceutical demand that compounds annually.

- Universal Health Insurance Coverage: Japan’s statutory health insurance system (SHIS) covers 98.3% of the population, reimbursing diabetes prescription costs. This near-universal coverage eliminates the affordability barrier present in many markets, ensuring stable and predictable pharmaceutical revenue regardless of individual patient income levels.

Market Restraints

- Biennial Health Insurance Price Revisions Compressing Revenue: Japan's MHLW mandates biennial drug price revisions that systematically reduce reimbursement prices for established diabetes drugs. This creates structural revenue compression that limits market growth to volume gains, offsetting price declines.

- Limited CGM Reimbursement for Type-2 Patients: Japan's health insurance currently reimburses CGM only for type-1 patients and insulin-intensive type-2 patients. The type-2 patients on oral therapy are largely excluded from CGM reimbursement, limiting the CGM device market addressable size despite Japan's advanced digital health readiness.

Market Opportunities

- CGM Reimbursement Expansion to Type-2 Patient Population: MHLW is evaluating CGM reimbursement extension as real-world evidence demonstrates glycemic benefit and hospitalization reduction. Expanding health insurance for CGM coverage to additional type-2 patients could add market value to Japan's diabetes device market by 2030.

- Digital Health and Telemedicine Integration Under MHLW Initiatives: Japan's Society 5.0 digital transformation agenda includes telemedicine expansion, AI-assisted diabetes management, and remote monitoring reimbursement.

Market Challenges

- Healthcare Cost Containment vs. Premium Drug Access: Japan's fiscal sustainability concerns are driving MHLW to implement cost-effectiveness assessments that evaluate premium drugs' incremental clinical benefit versus cost before NHI price setting.

- Aging Pharmacist Workforce and Pharmacy Consolidation: Japan's licensed pharmacies face workforce aging challenges, with a pharmacist shortage projected in rural regions by 2030. Pharmacy chain consolidation is reshaping the retail pharmacy distribution landscape, potentially disrupting existing diabetes prescription dispensing patterns.

Emerging Market Trends

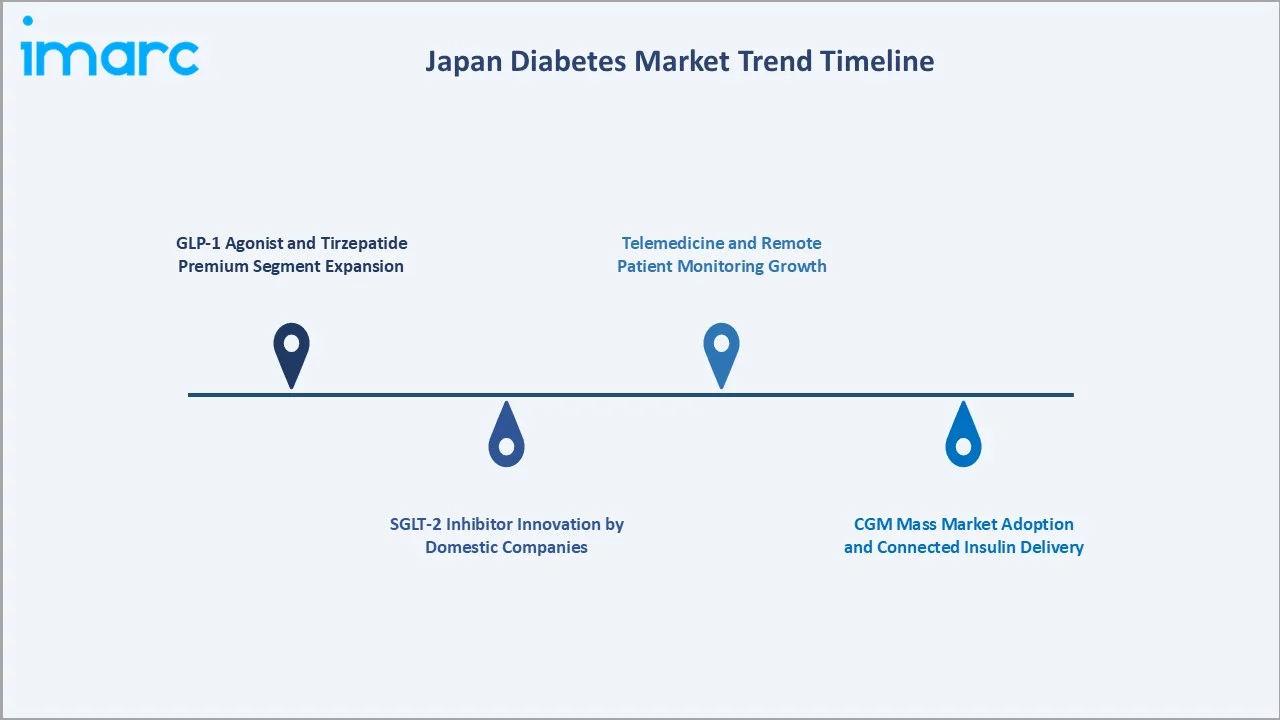

1. GLP-1 Agonist and Tirzepatide Premium Segment Expansion

In April 2023, Eli Lilly Japan K.K. and Mitsubishi Tanabe Pharma Corporation launched “Mounjaro subcutaneous injection 2.5 mg / 5 mg ATEOS” in Japan. The therapy, containing tirzepatide, is a sustained-release GIP/GLP-1 receptor agonist designed to support advanced diabetes management, shifting the market's premium center of gravity from basal insulin to injectable GLP-1 agonists.

2. SGLT-2 Inhibitor Innovation by Domestic Companies

In March 2024, Mitsubishi Tanabe Pharma Corporation secured approval for a new orally disintegrating (OD) tablet formulation of CANAGLU Tablets 100 mg. The drug, containing canagliflozin hydrate, is an SGLT2 inhibitor used in diabetes treatment, with the additional dosage form aimed at improving patient convenience and adherence.

3. CGM Mass Market Adoption and Connected Insulin Delivery

Abbott's FreeStyle Libre system is the first and only continuous glucose monitoring (CGM) system with expanded coverage in Japan. In March 2022, Abbott announced that Japan’s Ministry of Health, Labour and Welfare approved expanded reimbursement coverage for its FreeStyle Libre system. The update extends eligibility to all individuals with diabetes who administer insulin at least once daily, broadening patient access to continuous glucose monitoring in the country.

4. Telemedicine and Remote Patient Monitoring Growth

Japan's COVID-19 response expanded telemedicine reimbursement in 2020, which has been partially maintained post-pandemic. Remote monitoring of diabetes patients via connected devices (CGM, insulin pens) and teleconsultation platforms is growing in urban Japan.

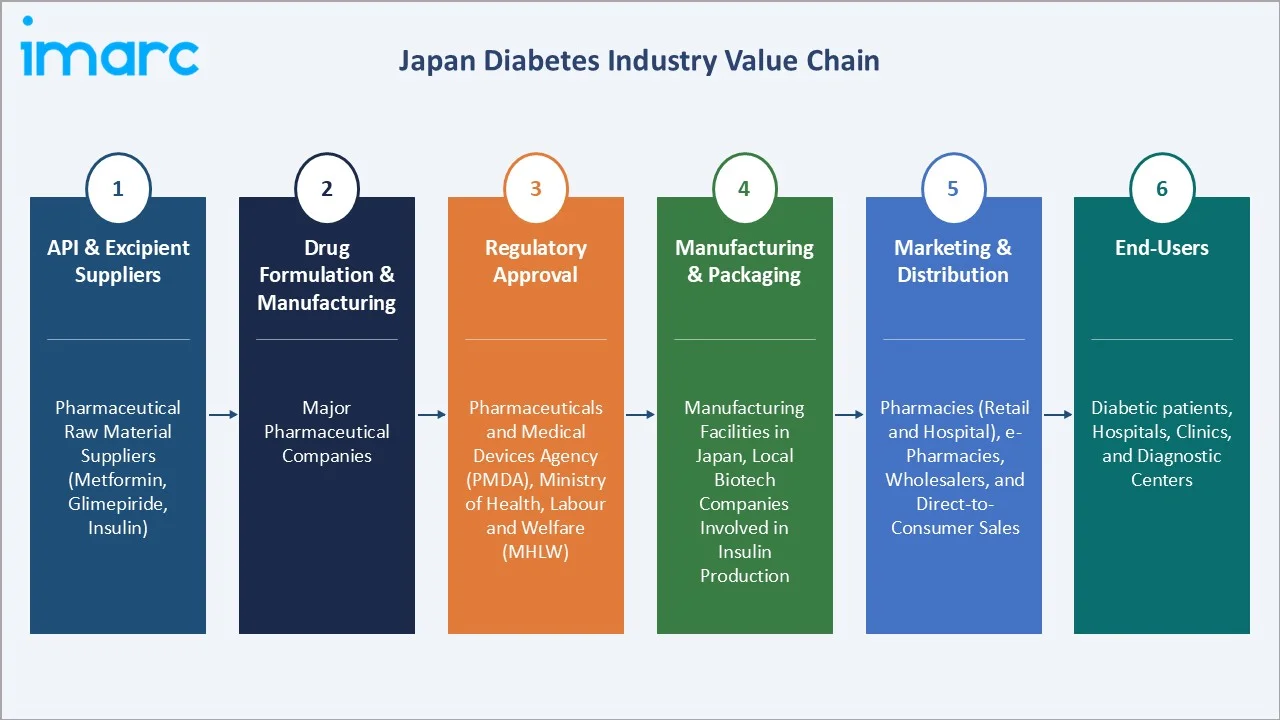

Industry Value Chain Analysis

Japan's diabetes market value chain integrates API supply through pharmaceutical production, PMDA regulatory approval, three-tier pharmaceutical distribution, and retail/hospital/e-pharmacy end dispensing serving 10.8 million patients under universal health insurance coverage.

|

Stage |

Key Participants |

|

API & Excipient Suppliers |

Pharmaceutical raw material suppliers (active ingredients like metformin, glimepiride, insulin) |

|

Drug Formulation & Manufacturing |

Major pharmaceutical companies |

|

Regulatory Approval |

Pharmaceuticals and Medical Devices Agency (PMDA), Ministry of Health, Labour and Welfare (MHLW) |

|

Manufacturing & Packaging |

Manufacturing facilities in Japan, local biotech companies involved in insulin production |

|

Marketing & Distribution |

Distribution channels through pharmacies (both retail and hospital), e-pharmacies, wholesalers, and direct-to-consumer sales |

|

End-Users |

Diabetic patients, hospitals, clinics, and diagnostic centers |

Japan's three-tier pharmaceutical distribution structure operates under Japan's unique distribution regulations. Primary wholesalers earn 2-3% margins; pharmaceutical manufacturers capture 50-65% gross margins on branded insulin analogs and GLP-1 agonists before NHI price revision impacts.

Technology Landscape in the Japan Diabetes Industry

GLP-1 Agonist and Novel Drug Delivery Innovation

Novo Nordisk's Rybelsus (oral semaglutide), approved in 2020, addresses Japan's significant injection-averse elderly patient segment, offering once-daily oral GLP-1 administration. Japan's drug delivery innovation is uniquely focused on patient convenience for elderly and dexterity-impaired patients.

Continuous Glucose Monitoring (CGM) Technology

Abbott FreeStyle Libre factory-calibrated flash CGM system leads Japan's device market. National health insurance for CGM reimbursement for type-1 covers high device costs.

Digital Health and Connected Device Ecosystem

Health2Sync's connected insulin pen data platform represents Japan's most advanced digital insulin management ecosystem. Hospital data system integration enables AI-driven population-level diabetes management analytics for healthcare providers.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Oral Antidiabetics | 47.8% | 2025 |

| Distribution Channel | Retail Pharmacies | 49.8% | 2025 |

By Segment

Insulin leads at 52.2% market share (2025). In January 2025, Novo Nordisk Pharma Ltd. introduced Awiqli (insulin icodec), marking the availability of the world’s first once-weekly basal insulin for patients in Japan who require insulin therapy. The GLP-1 injectable agonist class is the fastest-growing sub-segment within insulin-adjacent injectables in Japan.

To access detailed market analysis, Request Sample

Oral antidiabetics at 47.8% are anchored by Japan's large-volume DPP-4 inhibitor prescriptions. Japan was one of the world's first and largest DPP-4 markets, with sitagliptin and alogliptin commanding significant market share. SGLT-2 inhibitors are growing at 12-15% annually within oral antidiabetics, with cardiorenal indication expansion driving health insurance eligibility beyond glycemic control alone.

By Distribution Channel

Retail pharmacies lead at 49.8% market share (2025). Japan's licensed dispensing pharmacies remain the primary dispensing channel under Japan's Pharmaceutical and Medical Device Act dispensing mandates. The channel grows at ~2.7% CAGR through 2034, supported by Japan's dispensing pharmacy policy encouraging prescription separation from hospitals.

Hospital pharmacies at 32.1% serve inpatient and outpatient specialty diabetes management across Japan's hospitals. E-Commerce/Tele-Pharmacy at 18.1% grows fastest at ~5.8% CAGR, driven by post-pandemic telemedicine normalization expanding chronic disease prescription fulfilment.

Competitive Landscape

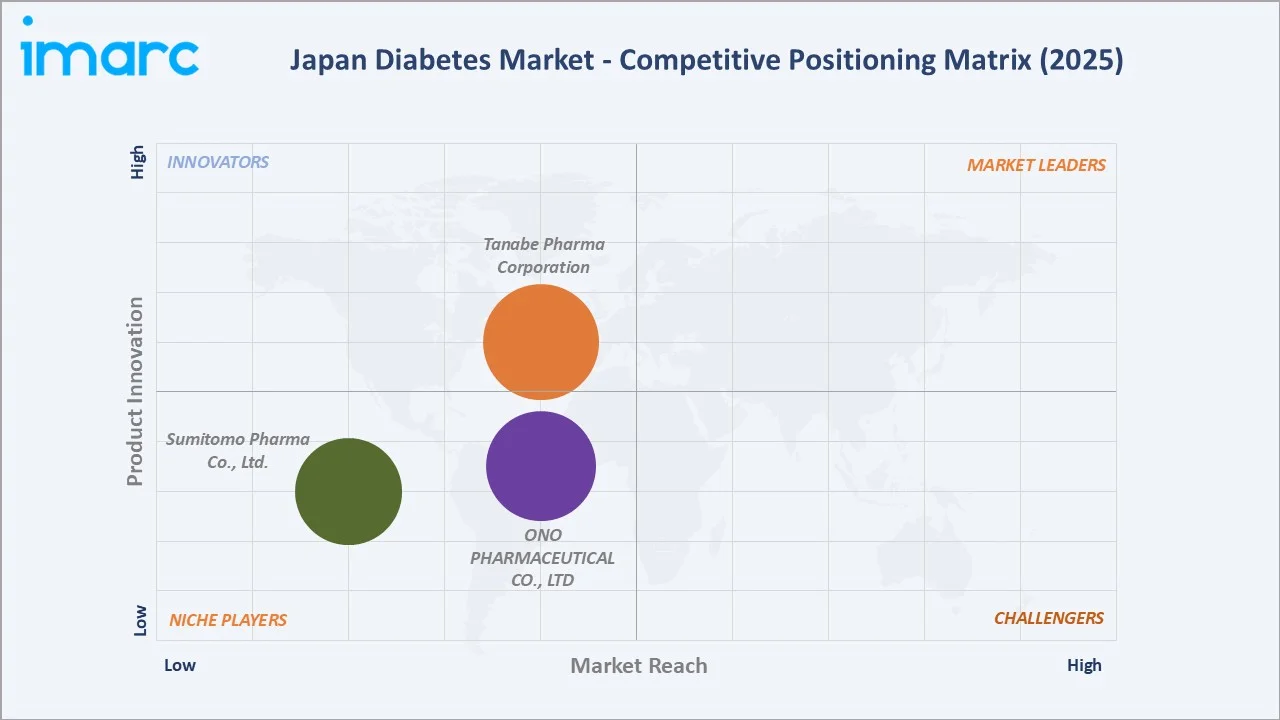

Japan's diabetes pharmaceutical market is moderately concentrated at the branded level. ONO Pharma and Tanabe together account for approximately 40-45% of Japan's diabetes market, while domestic SGLT-2 innovators hold significant positions in Japan-specific oral antidiabetic prescriptions.

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Tanabe Pharma Corporation |

CANAGLU, CANALIA |

Established Player |

Japan SGLT-2 innovation; CANAGLU OD Tablets for easy ingestion |

|

ONO PHARMACEUTICAL CO., LTD |

Glactiv |

Niche Player |

Japan-originated pharma company producing Glactiv oral drugs for type-2 diabetes |

|

Sumitomo Pharma Co., Ltd. |

TWYMEEG |

Niche Player |

Sumitomo’s TWYMEEG is the first agent in a class of tetrahydrotriazine-containing molecules |

CGM and device disruptors collectively capture 7-9% of the total Japan diabetes market revenues. This device revenue share is growing at 15%+ CAGR as CGM reimbursement expands and closed-loop insulin systems gain PMDA regulatory pathways toward 2034.

Key Company Profiles

Tanabe Pharma Corporation

Tanabe Pharma is Japan's most active domestic diabetes innovator, having launched CANAGLU OD Tablets, Japan's first OD SGLT-2 inhibitor specifically designed for elderly patients.

- Product Portfolio: CANAGLU, CANALIA.

- Recent Developments: In May 2024, Tanabe Pharma Corporation launched the SGLT2 inhibitor “CANAGLU OD Tablets 100 mg” on the same day after it was listed in the NHI drug price list.

- Strategic Focus: Japan-specific SGLT-2 formulation innovation for patient convenience.

ONO PHARMACEUTICAL CO., LTD.

Ono Pharmaceutical is a Japan-based pharmaceutical company with a niche presence in the diabetes market, primarily focused on oral therapies.

- Product Portfolio: Glactiv

- Recent Developments: In August 2021, AstraZeneca K.K. and Ono Pharmaceutical Co., Ltd. announced that Forxiga Tablets 5mg and 10mg received an additional approval for the indication of chronic kidney disease with and without type-2 diabetes

- Strategic Focus: Niche positioning in oral diabetes drugs through partnerships and lifecycle management, rather than broad portfolio expansion.

Market Concentration Analysis

Japan's diabetes pharmaceutical market exhibits moderate concentration at the branded injectable level. ONO Pharma and Tanabe together hold approximately 40-45% of the diabetes market by value. The oral antidiabetic segment is moderately fragmented, with DPP-4 inhibitors. SGLT-2 inhibitors are contested among market players, creating a balanced competitive SGLT-2 landscape unique to Japan's domestic pharmaceutical structure.

Consolidation trends are creating a duopoly in pharmaceutical distribution. Device consolidation is occurring through Abbott's FreeStyle Libre, gaining a dominant CGM share, while defending insulin delivery device positions against international competitors.

Investment & Growth Opportunities

Fastest Growing Segments

E-commerce/tele-pharmacy channel (~5.8% CAGR), GLP-1 agonist/tirzepatide class (~12-15% CAGR within injectables), CGM device market (~18% CAGR), digital diabetes management platforms (~25% CAGR), and SGLT-2 inhibitor expansion into CKD/heart failure (~8-10% class CAGR) represent Japan's highest-growth investment vectors through 2034. Oral semaglutide (Rybelsus) represents the highest-value single drug growth opportunity.

Emerging Market Opportunities

Japan's type-2 patients on oral-only therapy represent a CGM reimbursement expansion opportunity once MHLW expands NHI CGM coverage beyond insulin-intensive patients. Rural Japan's low specialist access creates a telemedicine-integrated diabetes management opportunity as MHLW's online prescription dispensing reforms take full effect.

Investment Themes

- PMDA fast-track for novel diabetes therapies: Japan's designation for breakthrough drugs can accelerate GLP-1 agonist, once-weekly insulin, and closed-loop device approval timelines by 6-12 months, creating earlier premium revenue windows for innovator companies investing in dedicated Japan clinical data.

- Japan-specific elderly diabetes device design: Japan's elderly diabetes patients are underserved by current Western-designed insulin delivery devices. Investment in Japan-optimized ergonomic pen devices, small-profile CGM sensors, and voice-guided dosing reminders represents a differentiated market segment.

Future Market Outlook (2026-2034)

The Japan diabetes market is projected to grow from USD 5.8 Billion in 2025 to USD 7.6 Billion by 2034, at a steady 2.95% CAGR that reflects Japan's unique market economics, structural patient volume growth offset by systematic NHI price compression, creating net positive growth driven by premiumization in GLP-1 agonists, CGM devices, and digital health. Japan's USD 6.7 Billion market in 2030 will consolidate its position as Asia's third-largest diabetes market.

Three structural forces anchor this growth with high predictability: Japan's irreversible demographic aging continuously expanding the Type-2 patient base; the GLP-1 agonist class transition from specialty to mainstream therapy as wider NHI prescription eligibility; and Japan's Society 5.0 digital health agenda systematically building AI-driven, connected diabetes management infrastructure that creates parallel digital revenue streams alongside pharmaceuticals.

Research Methodology

Primary Research

Primary research comprised structured interviews with 80+ industry stakeholders (2025), including endocrinologists and diabetologists from Juntendo University Hospital, Osaka University Hospital, and Kyushu University Hospital; Japan-based pharmaceutical company medical affairs directors; PMDA regulatory specialists; NHI coverage and pricing analysts from MHLW-affiliated institutions; and retail pharmacy chain executives.

Secondary Research

Secondary research encompassed Japan Diabetes Society (JDS) Clinical Practice Guidelines 2024, IDF Diabetes Atlas Japan country data 2023, MHLW National Patient Survey 2023, Ministry of Internal Affairs and Communications elderly population statistics, PMDA approval database 2024-2025, NHI Drug Price List revisions 2024, IQVIA Japan pharmaceutical market reports, and company annual reports for major Japan-operating diabetes companies. Over 140 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using patient population x treatment penetration x NHI-adjusted revenue per patient models, segmented by Segment and distribution channel, validated against IQVIA Japan prescription audit data and MHLW NHI drug expenditure statistics. Key inputs include JDS prevalence trend data, NHI biennial price revision assumptions, GLP-1 agonist S-curve penetration modeling, CGM reimbursement expansion scenarios, and Japan's Cabinet Office demographic aging projections through 2034.

Japan Diabetes Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Tanabe Pharma Corporation, ONO PHARMACEUTICAL CO., LTD, Sumitomo Pharma Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan diabetes market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan diabetes market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan diabetes industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Diabetes Market Report

The Japan diabetes market was valued at USD 5.8 Billion in 2025, covering oral antidiabetics, insulin therapies, CGM monitoring devices, and digital health solutions for approximately 10.8 million diagnosed adults across Japan.

The Japan diabetes market is projected to grow at a CAGR of 2.95% during 2026-2034, reaching USD 7.6 Billion by 2034, driven by aging demographics, GLP-1 agonist expansion, CGM adoption, and telemedicine integration.

Insulin leads at 52.2% market share (2025), anchored by Japan's Type-1 patient base, premium basal analog prescriptions, and GLP-1 injectable agonist growth classified within the injectable segment.

Retail pharmacies hold the largest share at 49.8% (2025), anchored by Japan's licensed dispensing pharmacies and MHLW's policy separating hospital prescribing from pharmacy dispensing.

E-commerce/tele-pharmacy grows fastest at ~5.8% CAGR (2026-2034), driven by post-COVID telemedicine normalization expanding diabetes prescription services.

Leading companies include Tanabe Pharma Corporation, ONO PHARMACEUTICAL CO., LTD., and Sumitomo Pharma Co., Ltd., among others.

Japan has approximately 10.8 million diagnosed diabetes adults, with the rising aging population, creating disproportionately high elderly-onset Type-2 diabetes incidence.

Japan's diabetes market is projected to reach approximately USD 6.7 Billion by 2030, driven by CGM expanding to additional reimbursed patients and MHLW digital health integration creating remote diabetes management revenue.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade