Japan Esports Market Size, Share, Trends and Forecast by Revenue Model, Platform, Games, and Region, 2026-2034

Japan Esports Market Size, Share, Trends & Forecast (2026-2034)

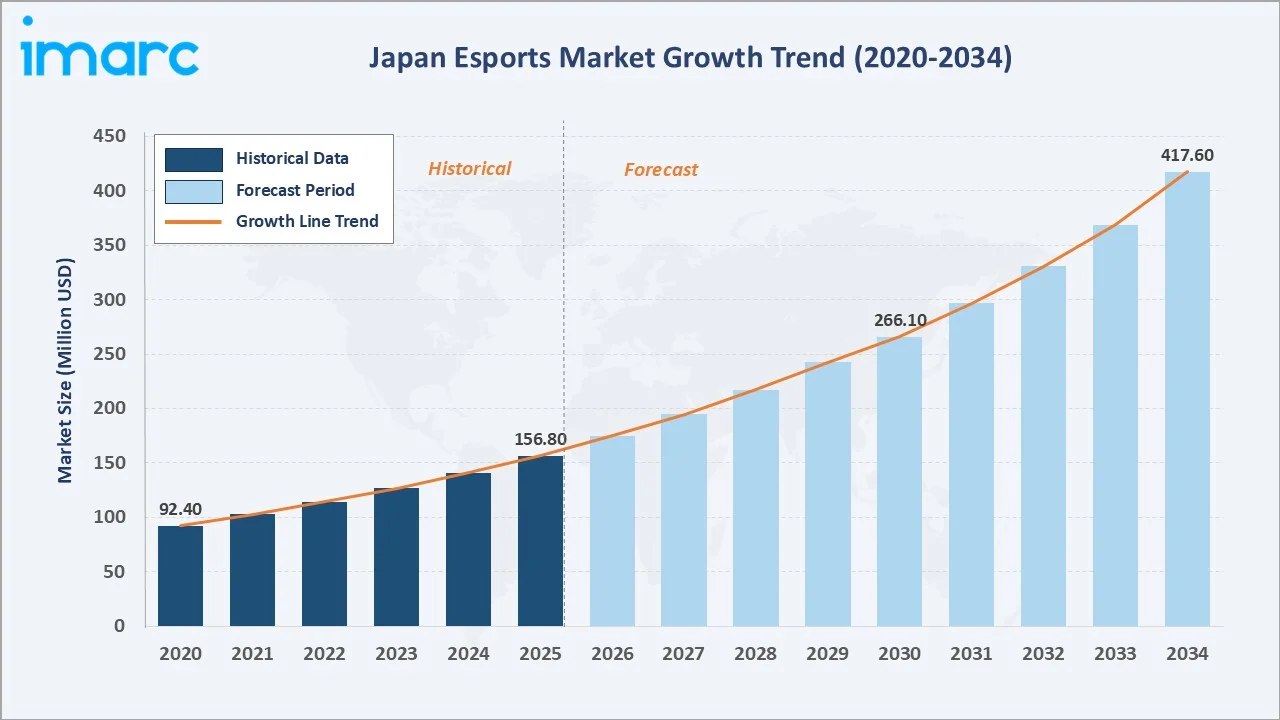

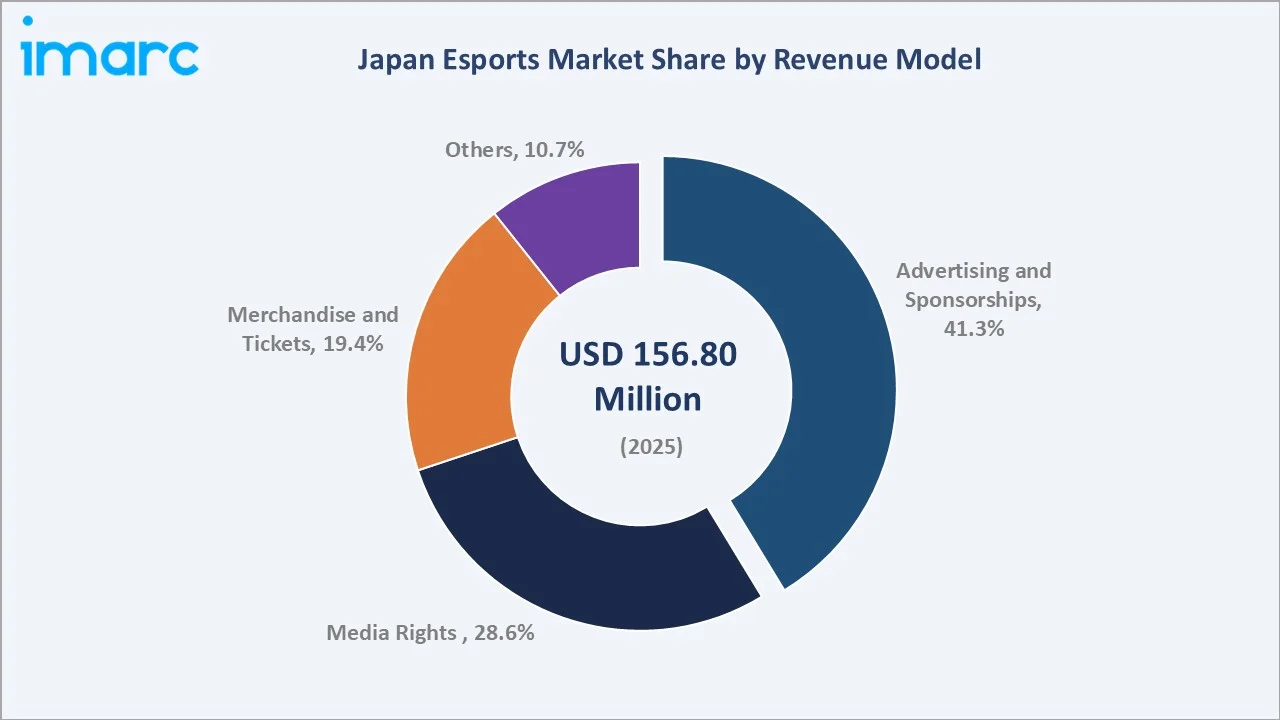

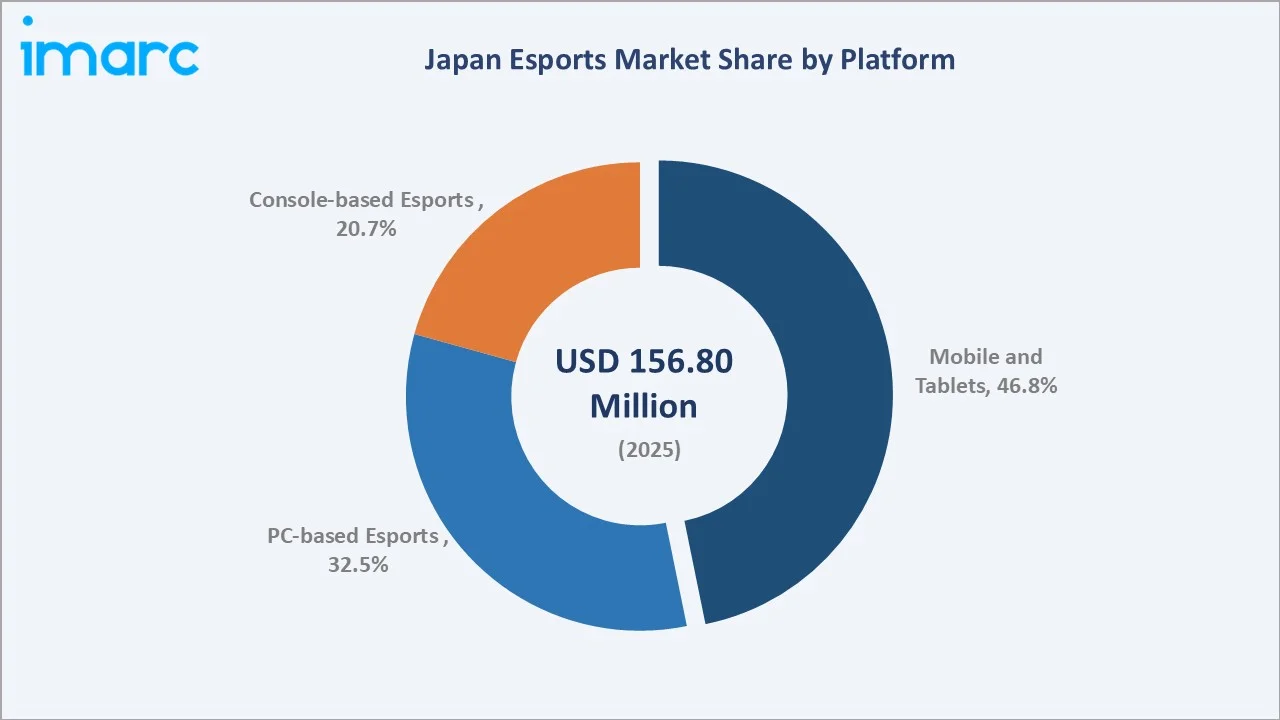

The Japan esports market was valued at USD 156.8 Million in 2025 and is projected to reach USD 417.6 Million by 2034, exhibiting a CAGR of 11.15% during 2026-2034. Rapid growth among Japan's youth - where over 40% of those aged 18-39 recognize esports as a future sport - is a primary driver. Advertising and Sponsorships lead at 41.3% share, while Mobile and Tablets dominate the platform segment at 46.8%. The Kanto region holds the largest regional share at 36.9% in 2025, anchoring Japan's position as a leading Asia-Pacific esports hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 156.8 Million |

|

Forecast Market Size (2034) |

USD 417.6 Million |

|

CAGR (2026-2034) |

11.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (36.9% Share, 2025) |

|

Fastest Growing Region |

Kinki Region |

The market grew from USD 92.4 Million in 2020 to USD 156.8 Million in 2025, anchored at USD 266.1 Million in 2030, and is projected to reach USD 417.6 Million by 2034. Government deregulation of prize money, 5G network expansion, and integration of esports into educational institutions are reshaping Japan's competitive gaming landscape above baseline digital entertainment trends.

To get more information on this market, Request Sample

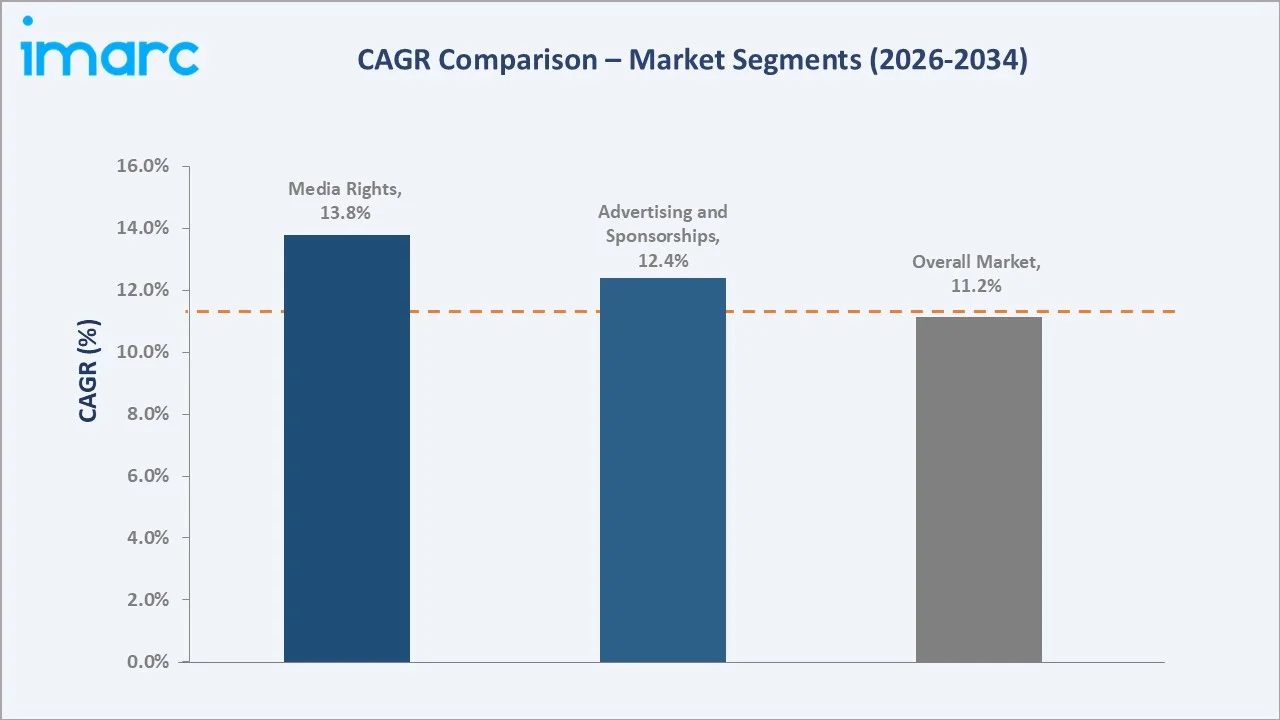

Media Rights at ~13.8% CAGR (2026-2034) and Mobile & Tablets at ~13.2% CAGR are the fastest-growing sub-segments. Advertising & Sponsorships, leading at 41.3% share in 2025, continue to attract major domestic and international brands investing in Japan's engaged young gaming audience.

Executive Summary

The Japan esports market reached USD 156.8 Million in 2025, representing one of Asia-Pacific's most rapidly expanding competitive gaming economies. Japan's unique convergence of a deeply embedded gaming culture, government-backed regulatory reform - specifically the easing of prize money restrictions in 2018 - and strong corporate sponsorship infrastructure underpins this high-growth trajectory. The market is projected to grow at 11.15% CAGR, reaching USD 417.6 Million by 2034, reflecting accelerating monetization across multiple revenue streams.

Advertising and Sponsorships lead revenue generation at 41.3% share (2025), as domestic and multinational brands increasingly target Japan's engaged esports audience of predominantly 18-39 year-olds. Media Rights at 28.6% represent the fastest-growing model, driven by streaming platform investment. Mobile and Tablets dominate the platform segment at 46.8%, consistent with Japan's high smartphone penetration. Professional leagues for titles like League of Legends (LJL), VALORANT (VCT Japan), and Street Fighter 6 continue to attract investment.

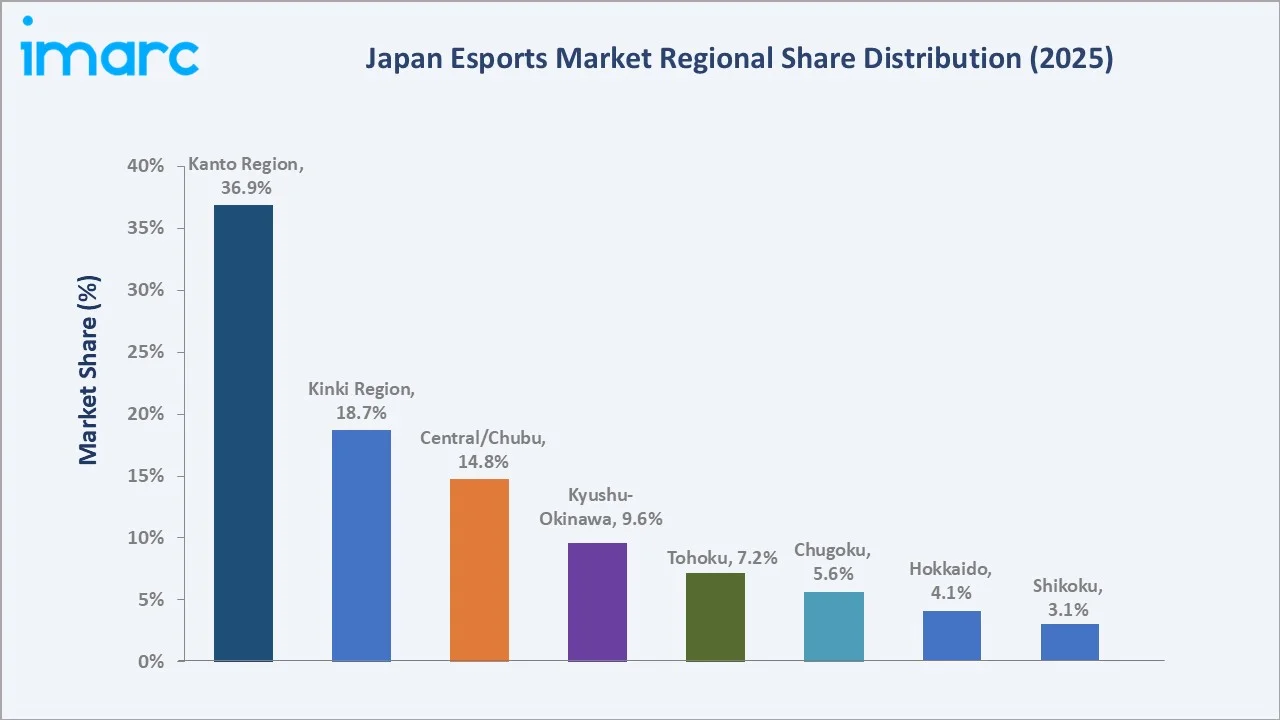

The Kanto region commands 36.9% market share, followed by Kinki at 18.7%, anchored by Tokyo's concentration of game publishers, esports organizations, and tournament infrastructure. Strategic government support - including esports integration into regional tourism and education - positions Japan for sustained growth through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Revenue Segment |

Advertising & Sponsorships - 41.3% share (2025) |

|

Largest Platform Segment |

Mobile & Tablets - 46.8% share (2025) |

|

Leading Region |

Kanto Region - 36.9% market share (2025) |

|

Fastest Growing Segment |

Media Rights - ~13.8% CAGR (2026-2034) |

|

Top Companies |

Sony Group Corporation, Tencent Holdings Ltd., CyberAgent, Inc., and Nintendo |

|

Market Opportunity |

Mobile esports & 5G streaming integration driving incremental USD ~260M by 2034 |

Key Analytical Observations Supporting the Above Data:

- Advertising & Sponsorships at 41.3% (2025) reflect growing brand investment: Japan's esports audience, predominantly aged 18-39, is among the most engaged digital demographics. In September 2024, Sony's INZONE gaming brand became the official monitor provider for the ALGS Year 4 Championship in Sapporo, exemplifying premium brand integration into esports events.

- Mobile & Tablets at 46.8% anchored by smartphone penetration and 5G rollout: Japan's mobile gaming market benefits from near-universal smartphone ownership. 5G network expansion enables high-quality mobile tournament streaming and real-time competitive gameplay at scale.

- Kanto Region at 36.9% represents Japan's esports nerve center: Tokyo hosts the headquarters of Riot Games Japan, CyberAgent, DeNA, Bandai Namco, and CAPCOM. The density of gaming studios and sponsors makes Kanto structurally dominant.

- Media Rights growing fastest at ~13.8% CAGR (2026-2034): Twitch Japan, YouTube Gaming, and Mildom are expanding live tournament broadcast deals. Hours watched for Japanese esports grew 16% in Q1 2024, with 28.1 million total hours recorded across platforms.

Japan Esports Market Overview

Japan's esports market encompasses competitive gaming events, professional leagues, digital streaming ecosystems, and associated revenue streams including advertising, media rights, merchandise, and tickets. The industry integrates game developers, professional organizations, tournament operators, streaming platforms, and brand sponsors. Japan's domestic game content market reached approximately USD 16 billion in 2024, per the Famitsu Game White Paper 2025, providing a deep commercial foundation for esports growth.

The esports ecosystem operates within Japan's broader gaming cultural framework - the country that pioneered arcade competitive gaming in the 1970s-80s. Regulatory changes since 2018, including the Japan Esports Union (JeSU) issuance of professional licenses, have normalized competitive gaming. Macroeconomic drivers include Japan's youth demographic engagement, increasing 5G mobile infrastructure, and the government's digital economy agenda supporting esports as a creative industry.

Market Dynamics

To evaluate market opportunities, Request Sample

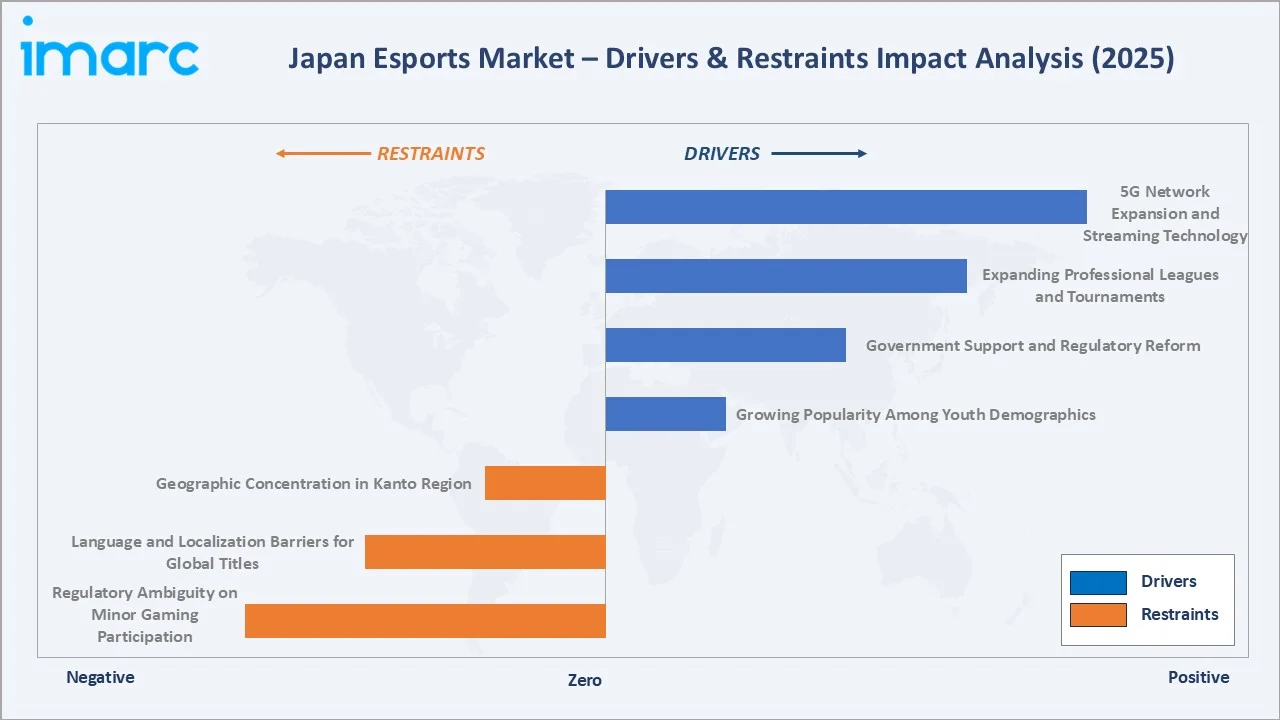

Market Drivers

- Growing Popularity Among Youth Demographics (Ages 18-39): A 2024 survey found more than 40% of Japanese individuals aged 18-39 believe esports will become part of future sports. Support among 18-29 year-olds reached 43.7%, with 48% of participants viewing esports as a sport poised to gain popularity. This reflects the structural consumer base driving audience growth, viewership, and downstream advertising revenue.

- Government Support and Regulatory Reform: The Japanese government has eased legal restrictions on prize money and promotes esports incorporation into tourism and regional regeneration initiatives. JeSU-recognized professional licenses legitimize competitive gaming as a career, attracting talent and institutional investment.

- Expanding Professional Leagues and Tournaments: Well-established competitions for League of Legends (LJL, 16 championship seasons), VALORANT (VCT Japan), and Street Fighter 6 attract growing sponsorship. In March 2024, Riot Games revised LoL Esports' business model, with overall regional league growth of 16% AMA recorded at MSI and Worlds 2023.

- 5G Network Expansion and Streaming Technology: Japan's total 5G base station deployment exceeded 260,000 units by 2024. High-speed, low-latency 5G infrastructure supports HD mobile esports streaming, real-time multiplayer gaming, and emerging VR/AR competitive formats.

Market Restraints

- Geographic Concentration in Kanto Region: With 36.9% of the market concentrated in Kanto, and Shikoku at only 3.1%, Japan's esports infrastructure outside major urban centers remains underdeveloped. Tournament venues, team facilities, and sponsorship pipelines are heavily Tokyo-centric, limiting nationwide market depth.

- Language and Localization Barriers for Global Titles: Japan's domestic gaming preferences lean toward Japanese-language content. Global esports titles require Japanese localization - commentary, interfaces, community platforms - creating cost barriers that can slow adoption of internationally-dominant games in the domestic competitive scene.

- Regulatory Ambiguity on Minor Gaming Participation: Japan lacks comprehensive national regulation on competitive gaming participation for minors (under 18). This creates organizational complexity for leagues considering youth divisions and limits systematic talent pipeline development at school-age levels.

Market Opportunities

- Esports Integration into Educational Institutions: In January 2024, Temple University Japan Campus partnered with the Asian Electronic Sports Federation (AESF) to advance esports education and training. School and university esports programs create structured talent pipelines, sustainable audience growth, and institutional sponsorship opportunities.

- Government Tourism and Regional Revitalization Initiatives: Japan has identified esports events as tourism drivers, particularly in regions outside Kanto. The 2025 ALGS Championship in Sapporo exemplifies this approach, generating inbound tourism revenue from international competitive gaming audiences.

Market Challenges

- Monetization Gap Versus Global Esports Markets: Despite strong viewership growth, Japan's esports revenue per viewer remains below comparable markets in South Korea and the United States. Prize pool sizes and media rights deal values lag global benchmarks, requiring structural scaling of monetization across all revenue streams.

- Talent Retention and Professional Career Viability: Japan's professional esports salary structures remain limited outside top-tier organizations. Without competitive compensation and career longevity frameworks, retaining top domestic talent against international team recruitment represents an ongoing structural challenge.

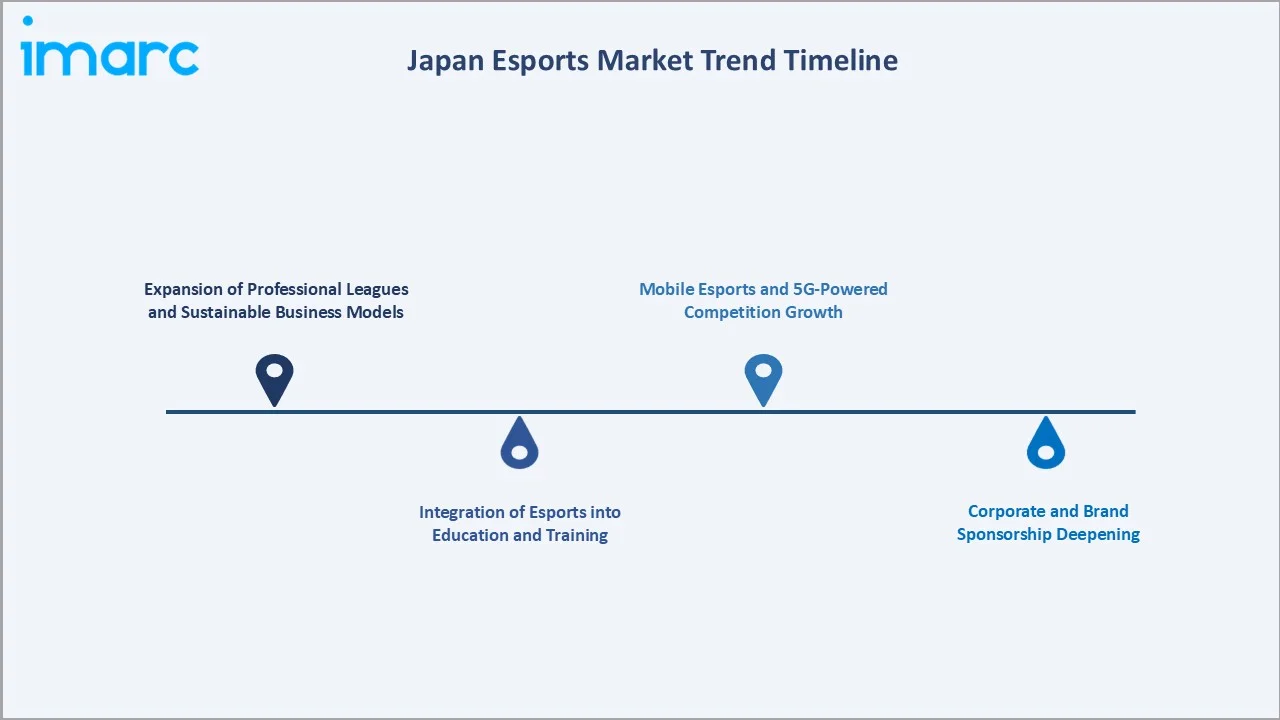

Emerging Market Trends

1. Expansion of Professional Leagues and Sustainable Business Models

In March 2024, Riot Games announced a revised business model for League of Legends Esports, targeting sustainability by reducing sponsorship dependence. The new model introduced fixed team stipends, in-game digital content revenue sharing, and a Global Revenue Pool (GRP) divided into General (50%), Competitive (35%), and Fandom (15%) components. Overall regional league AMA grew 16%, indicating resilient audience engagement.

2. Integration of Esports into Education and Training

As esports gains recognition as a legitimate professional pathway, Japan's schools and universities are introducing dedicated programs. Temple University Japan Campus (TUJ) partnered with AESF in 2024 to advance esports education and competitive infrastructure. These programs develop players, commentators, event organizers, and industry professionals, creating a sustainable domestic talent and workforce pipeline.

3. Mobile Esports and 5G-Powered Competition Growth

Mobile and Tablets lead Japan's platform segment at 46.8% (2025), underpinned by Japan's near-universal smartphone ownership and 5G network rollout. Mobile-first esports titles are expanding competitive formats, enabling tournament participation without dedicated hardware infrastructure. Mobile esports grew at approximately 15-18% annually from 2020-2025, outpacing PC and console competitive gaming in audience acquisition.

4. Corporate and Brand Sponsorship Deepening

In September 2024, Sony's INZONE gaming brand became the official monitor provider for the ALGS (Apex Legends Championship Series) Year 4 Championship in Sapporo. In 2024, HP and Heineken joined as Valorant Esports partners, reflecting accelerating premium brand participation in Japan's esports commercial ecosystem.

5. Metaverse and VR Competitive Gaming on the Horizon

Japan's Society 5.0 digital transformation agenda and established gaming hardware manufacturing capability position the country as a potential leader in VR esports development. While still nascent - under 1% of market revenue in 2025 - VR competitive gaming represents a structural growth vector targeted for meaningful commercialization by 2030, particularly given Sony's PlayStation VR2 ecosystem investments.

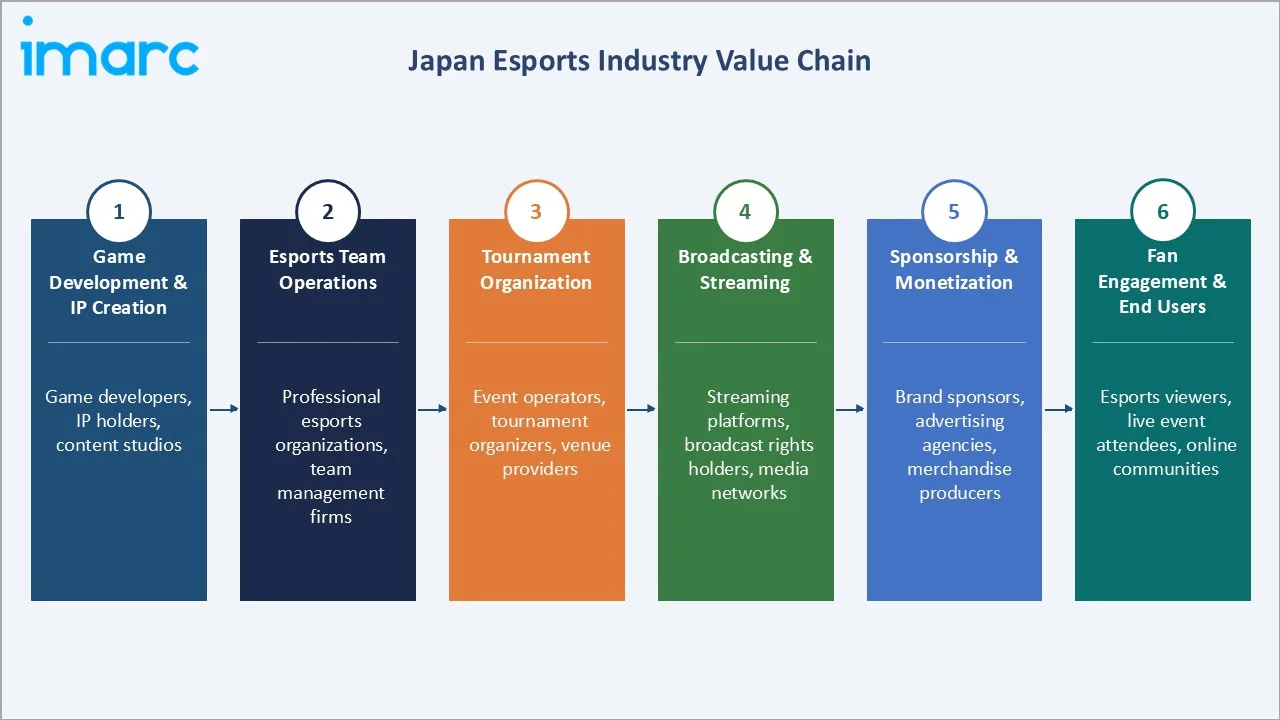

Industry Value Chain Analysis

Japan's esports market value chain integrates game IP development through event monetization and fan engagement, operating within an ecosystem anchored by Kanto-based publishers, JeSU-recognized professional organizations, digital streaming platforms, and corporate sponsorship networks serving Japan's growing competitive gaming audience.

|

Stage |

Key Participants |

|

Game Development & IP Creation |

Game developers, IP holders, content studios |

|

Esports Team Operations |

Professional esports organizations, team management firms |

|

Tournament Organization |

Event operators, tournament organizers, venue providers |

|

Broadcasting & Streaming |

Streaming platforms, broadcast rights holders, media networks |

|

Sponsorship & Monetization |

Brand sponsors, advertising agencies, merchandise producers |

|

Fan Engagement & End Users |

Esports viewers, live event attendees, online communities |

Technology Landscape in the Japan Esports Industry

Mobile and 5G Gaming Infrastructure

Japan's 5G deployment - exceeding 260,000 base stations by 2024 - enables high-bandwidth, low-latency mobile competitive gaming at scale. Major telecoms including NTT Docomo and SoftBank have invested in dedicated esports network solutions supporting tournament streaming and real-time gameplay. Mobile tournaments hosted through platforms like YouTube Gaming Japan achieve sub-50ms latency across major urban centers.

Streaming and Broadcast Technology

Twitch Japan, YouTube Gaming, and domestic platform Mildom collectively serve Japan's esports streaming audience. Real-time translation and Japanese commentary overlay technologies are enabling greater audience engagement with internationally-produced events, expanding addressable viewer populations beyond dedicated esports fans.

Tournament Production and Venue Technology

Professional esports venues in Japan integrate broadcast-grade production infrastructure. Tournament organizers like CyberZ/RAGE deploy cloud-based tournament management systems across multiple simultaneous events, enabling efficient multi-title operation at scale.

Esports Education and Training Technology

University and school esports programs increasingly deploy dedicated gaming lab infrastructure. Performance analytics platforms tracking player statistics, reaction times, and strategic decision patterns are being adopted by professional organizations including ZETA DIVISION and DetonatioN FocusMe. AI-driven coaching tools represent an emerging technology layer expected to reshape talent development by 2027-2028.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Revenue Model |

Advertising and Sponsorships |

41.3% |

2025 |

|

Platform |

Mobile and Tablets |

46.8% |

2025 |

|

Games |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

36.9% |

2025 |

By Revenue Model

Advertising and Sponsorships lead at 41.3% market share (2025). In September 2024, Sony's INZONE brand partnered with the ALGS as official monitor provider for the Year 4 Championship in Sapporo - a landmark deal reflecting premium hardware brand entry into Japan's esports sponsorship ecosystem. Sponsorship and advertising revenue is growing at ~12.4% CAGR through 2034, driven by increasing brand recognition of esports audiences' high purchase intent and youth demographic alignment.

To access detailed market analysis, Request Sample

Media Rights at 28.6% represent the fastest-growing revenue model at ~13.8% CAGR (2026-2034). Streaming rights deals for LJL, VCT Japan, and Apex Legends Japan are being formalized on multi-year terms, providing structural recurring revenue. Merchandise and Tickets at 19.4% benefit from Japan's strong concert and event attendance culture, with esports events driving premium merchandise sales at live tournament venues.

By Platform

Mobile and Tablets lead platform share at 46.8% (2025), underpinned by Japan's near-universal smartphone penetration rate of approximately 94% among adults (2024). The segment grows at ~13.2% CAGR, driven by accessible mobile esports titles and 5G-enabled competitive gaming capabilities. Mobile's dominance reflects Japan's unique gaming demographic, where casual-to-competitive crossover is particularly pronounced.

PC-based Esports at 32.5% is anchored by Japan's professional competitive scene, where VALORANT, League of Legends, and Apex Legends operate on PC infrastructure. Console-based Esports at 20.7% benefits from Japan's PlayStation and Nintendo ecosystem strength, with fighting games (Street Fighter 6, Tekken 8) and sports titles driving structured competitive events accessible through consumer consoles.

Regional Market Insights

|

Region |

2025 Share |

Key Growth Drivers |

|

Kanto Region |

36.9% |

High concentration of gaming studios, tournament venues, and sponsorship headquarters |

|

Kinki Region |

18.7% |

Strong gaming culture, university esports programs, and regional league presence |

|

Central/Chubu Region |

14.8% |

Manufacturing ecosystem supports gaming hardware; regional tournaments expanding |

|

Kyushu-Okinawa Region |

9.6% |

Rising youth demographics; government-backed digital economy initiatives |

|

Tohoku Region |

7.2% |

Post-2011 digital revitalization programs supporting gaming infrastructure |

|

Chugoku Region |

5.6% |

Expanding broadband and 5G coverage supporting online esports participation |

|

Hokkaido Region |

4.1% |

Tourism-linked esports events; winter season drives indoor digital entertainment |

|

Shikoku Region |

3.1% |

Smallest population base; niche mobile esports communities forming |

The Kanto Region accounts for 36.9% of Japan's esports market in 2025, anchored by Tokyo's concentration of Riot Games Japan, CyberAgent, DeNA, Bandai Namco Entertainment, and CAPCOM. Numerous game developers and media companies operating in Kanto enable frictionless sponsorship coordination, media rights negotiations, and content release alignment. Government digital innovation support further reinforces Kanto's structural dominance.

The Kinki Region at 18.7% is Japan's second-largest esports market, benefiting from Osaka's position as a major gaming and entertainment hub. Strong university esports program adoption and proximity to game development studios outside Tokyo support sustained above-average growth. Central/Chubu at 14.8% is supported by manufacturing infrastructure enabling gaming hardware distribution, with regional tournament activity expanding organically.

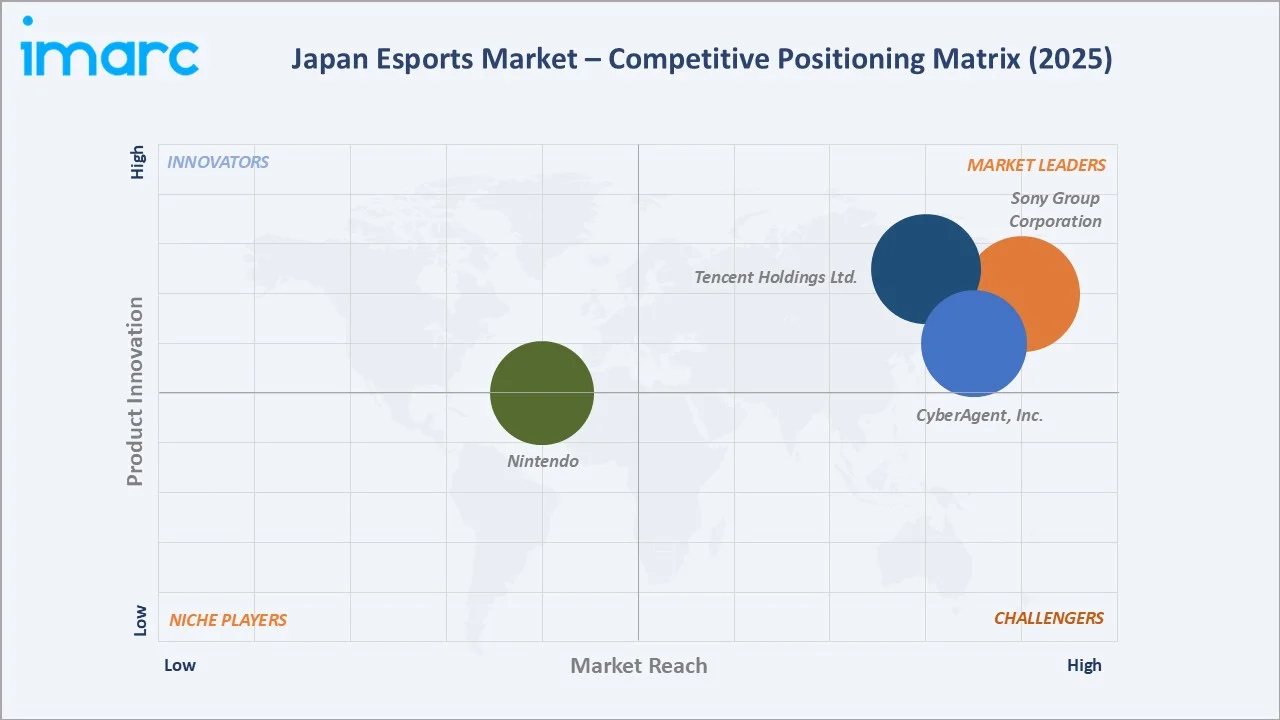

Competitive Landscape

Japan's esports market is moderately concentrated at the publisher and event organizer level. Sony, Tencent Holdings Ltd., and CyberAgent Inc., together anchor the top tier of tournament infrastructure,

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Sony Group Corporation |

INZONE and PlayStation Tournaments |

Leader |

Integrated hardware-to-event strategy via INZONE gaming monitors and PlayStation Tournaments grassroots infrastructure |

|

Tencent Holdings Ltd. |

League of Legends, VALORANT |

Leader |

Functional via Riot Games, Inc. International publisher with organized domestic league infrastructure |

|

CyberAgent, Inc. |

CyberZ / RAGE Esports |

Leader |

Japan's largest esports event organizer; RAGE tournament platform |

|

Nintendo |

Splatoon Koshien / Super Smash Bros |

Established Player |

Grassroots community-building, accessibility, and family-friendly competition |

Key Company Profiles

Sony Group Corporation

Sony Group Corporation is one of Japan's largest diversified technology and entertainment conglomerates, with a significant and growing footprint in the Japan esports market through three synergistic business units: Sony Interactive Entertainment (SIE), the INZONE gaming hardware brand, and Sony Music Entertainment Japan.

- Product Portfolio: INZONE and PlayStation Tournaments

- Recent Developments: In September 2024, the Apex Legends Championship Series (ALGS) partnered with Sony's INZONE gaming brand, making it the official monitor provider for the ALGS Year 4 Championship held in Sapporo, Japan in January 2025.

- Strategic Focus: Sony's Japan esports strategy is built on three pillars: hardware-driven tournament presence through INZONE as the premium performance brand for competitive gaming events in Japan; platform-level competitive infrastructure via PlayStation Tournaments enabling grassroots participation; and IP/content partnerships leveraging Sony Music and Sony Pictures to deepen esports fan engagement through original content.

Tencent Holdings Ltd.

Riot Games, which is a wholly-owned subsidiary of Tencent Holdings Ltd., operates two professional esports ecosystems in Japan, League of Legends (LJL) and VALORANT, spanning both domestic tier-2 and international tier-1 competition.

- Product Portfolio: League of Legends, VALORANT

- Recent Developments: In March 2024, Riot Games announced a new business model for League of Legends (LoL) esports franchises, with a new global revenue pool (GRP) to distribute all revenue from digital LoL esports.

- Strategic Focus: Long-term league sustainability through the Global Revenue Pool revenue model and in-game digital content monetisation

Market Concentration Analysis

Japan's esports market exhibits moderate-to-high concentration at the publisher and event organizer level. Sony, Tencent Holdings Ltd., and CyberAgent, Inc. together anchor approximately 45-50% of organized esports event activity by audience volume (2025).

The professional team layer is moderately fragmented. ZETA DIVISION and DetonatioN FocusMe lead in brand value and championship history, but eight to twelve organizations maintain active multi-title rosters, creating competitive tension for sponsorship. Consolidation is emerging in tournament operations, with RAGE and JeSU-affiliated organizers absorbing smaller regional events under centralized governance.

The streaming layer shows dual-platform dominance: Twitch Japan and YouTube Gaming collectively capture the majority of esports viewership hours, with domestic platform Mildom serving a loyal supplementary audience. New entrants face high switching costs given established streamer and viewer communities on major platforms.

Investment & Growth Opportunities

Fastest Growing Segments

Media Rights (~13.8% CAGR 2026-2034), Mobile Esports (~13.2% CAGR), and Advertising & Sponsorships (~12.4% CAGR) represent Japan's highest-growth investment vectors. Hours watched for Japanese esports grew 16% in Q1 2024, with 28.1 million total hours across platforms, demonstrating robust underlying demand. VALORANT alone generated 19.7 million watched hours in Q1 2024.

Emerging Market Opportunities

In November 2024, ITOCHU Corporation announced a capital and business alliance with REJECT Inc., a leading Japanese esports organization - signaling major trading house entry into competitive gaming investment. University esports programs (TUJ-AESF partnership, 2024) are creating structured entry points for talent development investment. Regional esports infrastructure outside Kanto - particularly in Kinki and Kyushu-Okinawa - represents geographic expansion opportunity backed by government regional revitalization funding.

Investment Themes

- Esports Tourism Integration: Japan's government-backed esports tourism model - demonstrated by the ALGS 2025 Sapporo Championship - creates co-investment opportunities between event organizers, regional governments, and hospitality sectors. Events in non-Kanto regions can attract international competitive gaming tourism, diversifying revenue beyond domestic audiences.

- Mobile Esports Platform Development: With Mobile and Tablets at 46.8% platform share (2025) and 5G infrastructure rapidly expanding, mobile-native esports platforms supporting real-time tournament participation represent an underpenetrated investment segment. Japan's established mobile gaming market (approximately 60% of USD 16 billion domestic games market) provides a structural consumer base.

- Esports Education and Training Infrastructure: University and school esports lab infrastructure, AI performance analytics platforms, and structured training programs are nascent but growing. TUJ's 2024 AESF partnership model demonstrates institutional validation for education-focused investment.

Future Market Outlook (2026-2034)

The Japan esports market is projected to grow from USD 156.8 Million in 2025 to USD 417.6 Million by 2034, at a CAGR of 11.15%. Japan's USD 266.1 Million market in 2030 will consolidate its position as a leading Asia-Pacific esports economy, positioned between South Korea's mature market and emerging Southeast Asian markets. Three structural forces anchor this growth with high predictability.

First, Japan's irreversible youth demographic engagement - with 40%+ of 18-39 year-olds actively engaged with esports and 48% viewing it as a growing sport - creates a compounding fan and consumer base. Second, government regulatory normalization and active support for esports as a cultural and economic asset generates structural institutional investment that private markets alone would not sustain at equivalent pace. Third, Japan's technology infrastructure leadership in 5G, mobile gaming, and console hardware provides competitive advantages in both competitive gaming execution and platform monetization.

Technological disruptions through 2034 include VR competitive gaming commercialization (targeting 3-5% market revenue by 2032), AI-integrated coaching and analytics platforms reshaping team preparation, and potential metaverse-based esports formats creating new spectator and participation models. Japan's position as a global gaming hardware and software innovator creates structural capacity to lead these transitions.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2024-2025), including esports organization executives from Sony Group Corporation, Tencent Holdings Ltd., CyberAgent, Inc., and Nintendo; sponsorship and media rights executives from JeSU-affiliated organizations; Riot Games Japan competitive operations staff; and game publisher esports division heads from Bandai Namco Entertainment and CAPCOM. Regional market experts across Kanto, Kinki, and Chubu regions contributed qualitative market intelligence.

Secondary Research

Secondary research encompassed the Japan Esports Union (JeSU) official industry data, Famitsu Game White Paper 2025 (Japan domestic game content market: USD 16 billion in 2024), government esports regulatory announcements, company investor relations materials and annual reports, tournament operator public disclosures, streaming platform viewership statistics (28.1 million hours watched Q1 2024, 16% growth), and trade publications covering Japan's competitive gaming ecosystem. Over 120 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using audience monetization modeling - audience size x monetization per viewer x revenue stream allocation - segmented by Revenue Model and Platform, validated against JeSU industry statistics and company revenue disclosures. Key inputs include youth demographic trend data from Japan's Ministry of Internal Affairs, 5G infrastructure deployment timelines, streaming platform viewership trajectory, and sponsor investment cycle analysis. Scenario modeling incorporated tournament prize pool growth, media rights deal benchmarking against comparable Asia-Pacific markets, and mobile esports penetration curves.

Japan Esports Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Revenue Models Covered | Media Rights, Advertising and Sponsorships, Merchandise and Tickets, Others |

| Platforms Covered | PC-based Esports, Consoles-based Esports, Mobile and Tablets |

| Games Covered | Multiplayer Online Battle Arena (MOBA), Player vs Players (PvP), First Person Shooters (FPS), Real Time Strategy (RTS) |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Sony Group Corporation, Tencent Holdings Ltd., CyberAgent, Inc., Nintendo, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan esports market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan esports market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan esports industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Esports Market Report

The Japan esports market was valued at USD 156.8 Million in 2025, covering advertising, sponsorships, media rights, merchandise, tickets, and other revenue streams across competitive gaming events and leagues nationwide.

The Japan esports market is projected to grow at a CAGR of 11.15% during 2026-2034, reaching USD 417.6 Million by 2034, driven by youth demographic engagement, expanding professional leagues, and 5G mobile infrastructure growth.

Advertising and Sponsorships lead at 41.3% share (2025), reflecting growing brand investment targeting Japan's highly engaged esports audience of predominantly 18-39 year-olds through tournament sponsorships and in-stream advertising.

Mobile and Tablets lead at 46.8% platform share (2025), driven by Japan's near-universal smartphone penetration and 5G network expansion enabling high-quality mobile competitive gaming and tournament participation.

The Kanto Region holds 36.9% market share (2025), anchored by Tokyo's concentration of major game publishers, esports organizations, tournament infrastructure, and corporate sponsors forming Japan's primary esports business ecosystem.

Japan's esports market is projected to reach approximately USD 266.1 Million by 2030, driven by media rights expansion, mobile esports growth, corporate sponsorship deepening, and government-backed esports tourism and education integration.

Leading companies include Sony Group Corporation, Tencent Holdings Ltd., CyberAgent, Inc., and Nintendo, among others.

Media Rights is the fastest-growing revenue segment at ~13.8% CAGR (2026-2034), driven by structured multi-year streaming rights deals for LJL, VCT Japan, and Apex Legends Championship Series events attracting domestic and international audiences.

A 2024 survey found over 40% of Japanese aged 18-39 believe esports will become part of future games, with 48% viewing it as a growing sport. University and school esports programs further deepen youth engagement and professional pathway recognition.

The Japanese government eased prize money restrictions and promotes esports for tourism and regional revitalization. JeSU-issued professional licenses legitimize competitive gaming careers, while government digital economy support funds esports infrastructure development across Japan.

Key opportunities include media rights monetization expansion, mobile esports platform development leveraging 5G infrastructure, esports tourism integration into regional government programs, university esports education investment, and VR-competitive gaming commercialization targeting post-2028 market entry.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)