Japan Gaming Market Size, Share, Trends by Device Type, Platform, Revenue Type, Type, Age Group, and Region, 2026-2034

Japan Gaming Market Size, Share, Trends & Forecast (2026-2034)

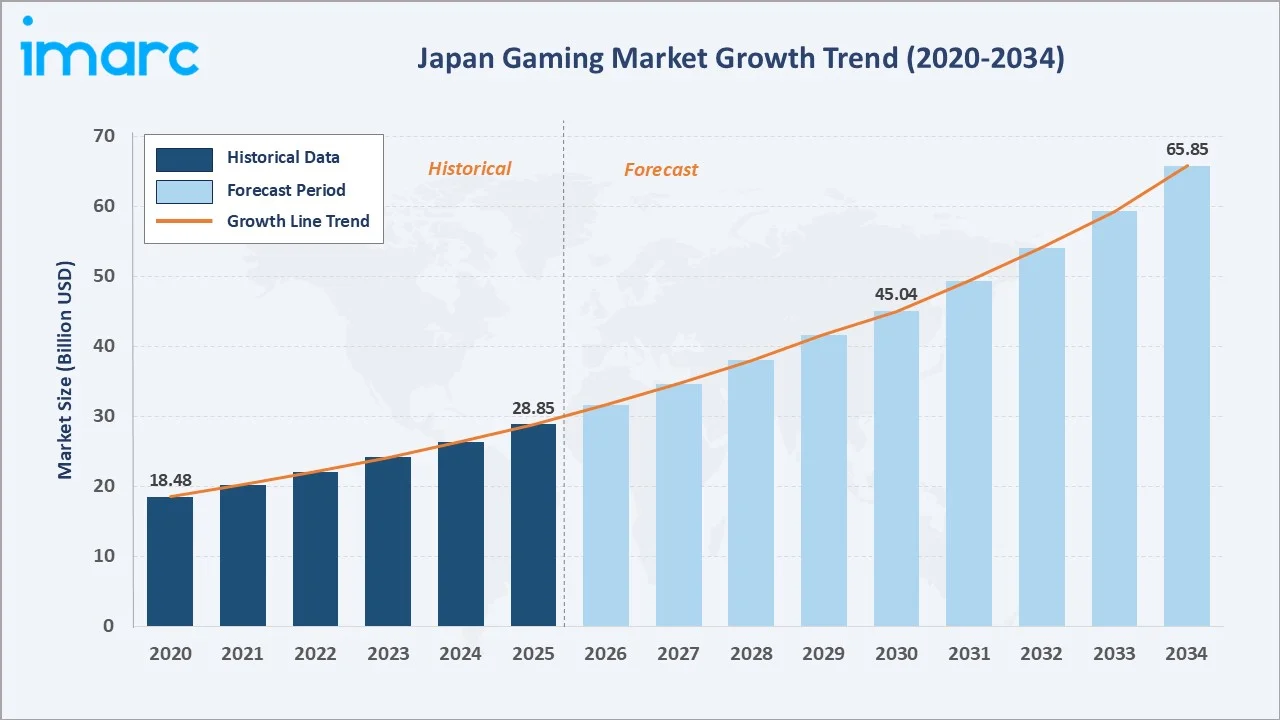

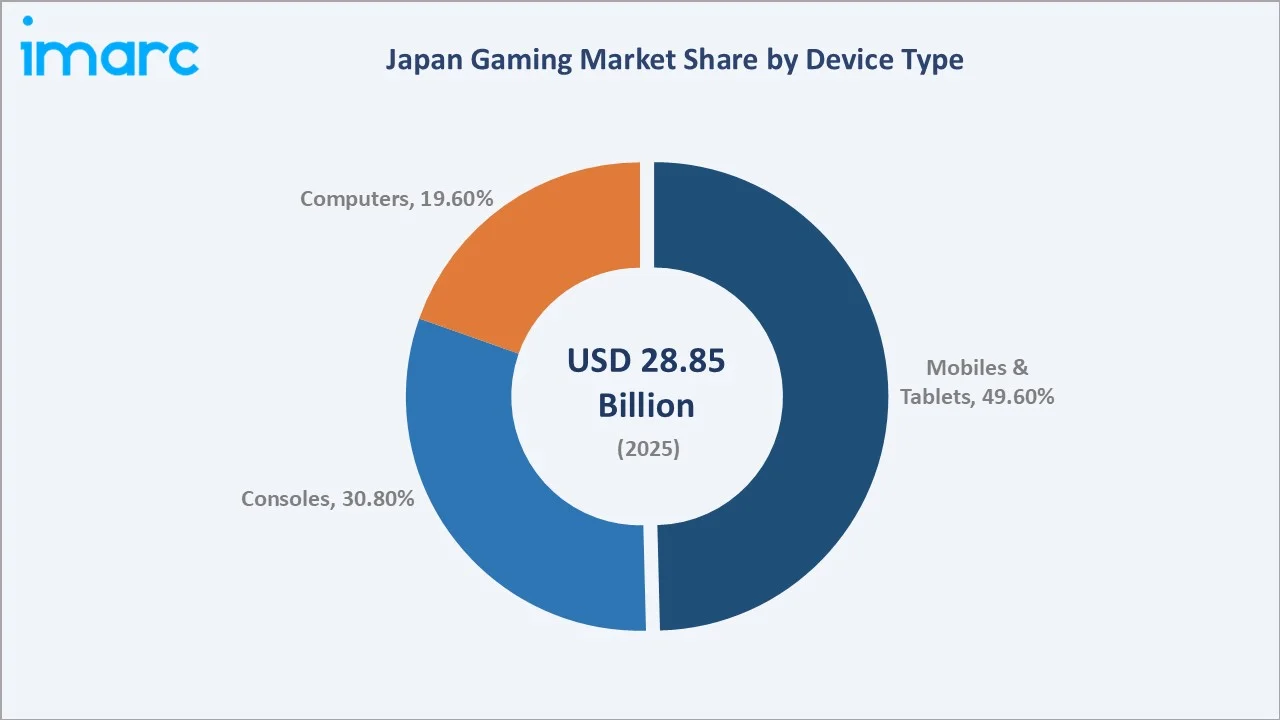

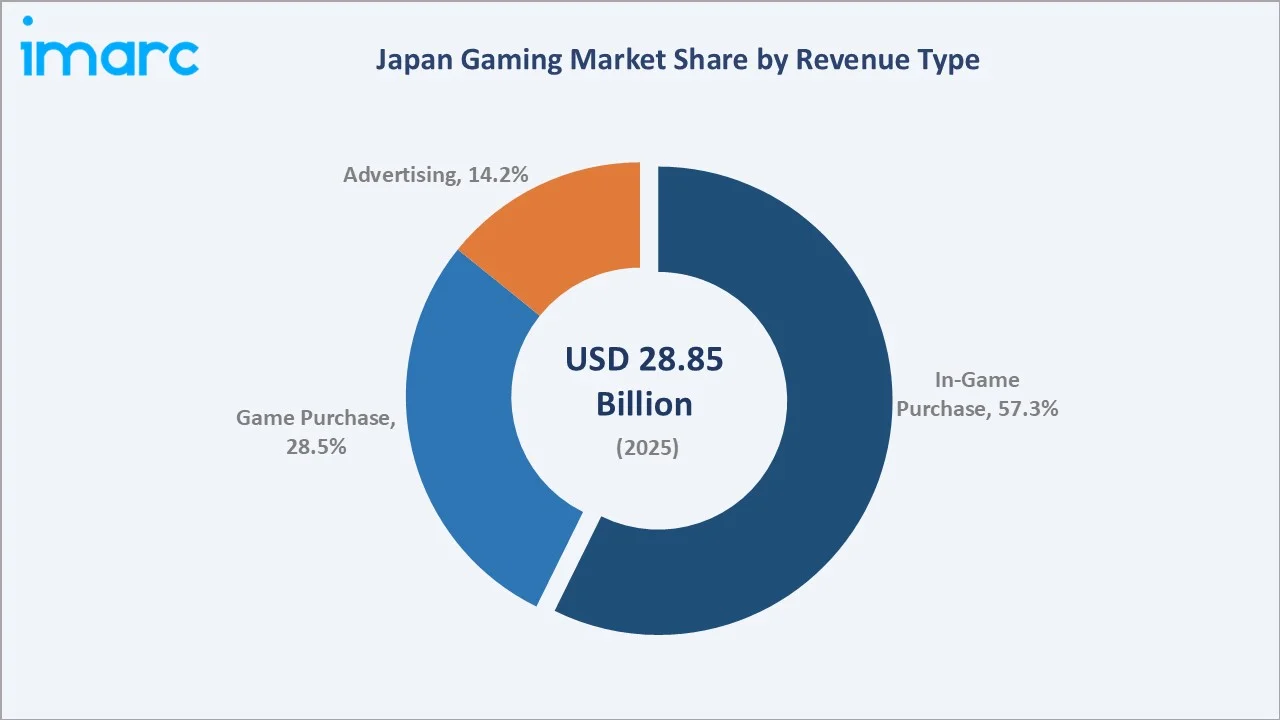

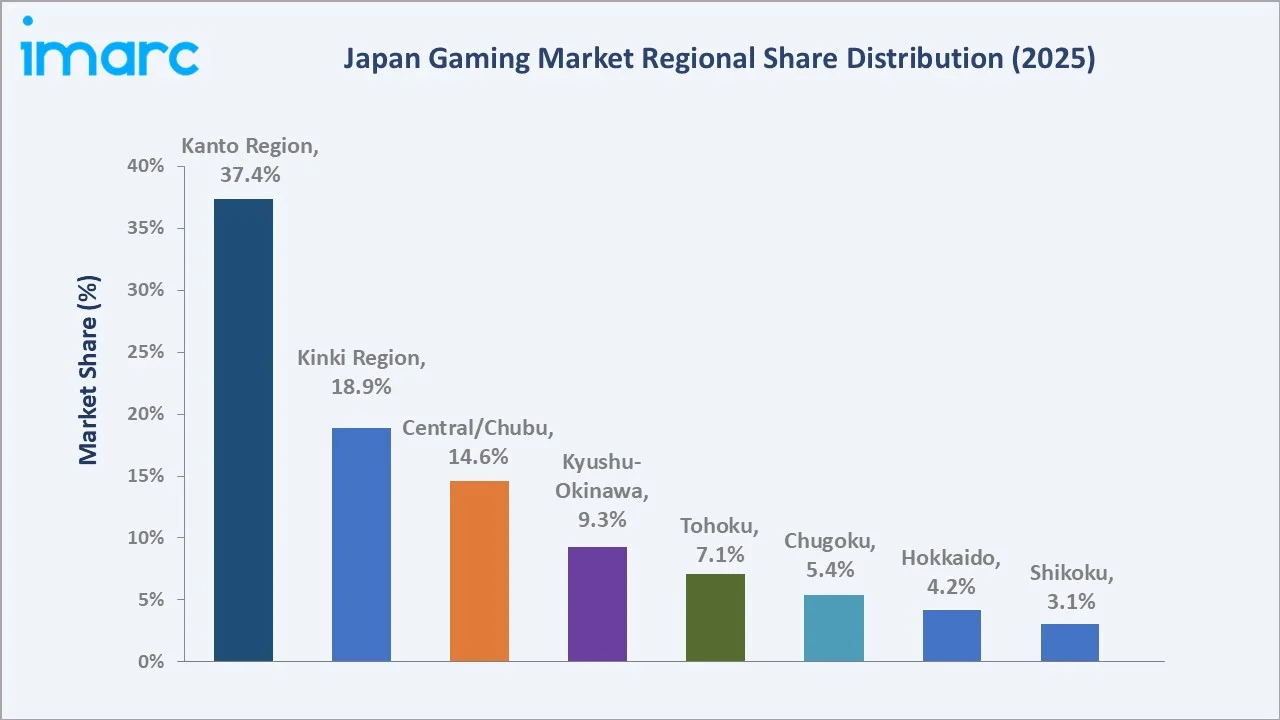

The Japan gaming market was valued at USD 28.85 Billion in 2025 and is projected to reach USD 65.85 Billion by 2034, growing at a CAGR of 9.31% during 2026-2034. Japan hosts one of the most mature and culturally embedded gaming ecosystems globally, with over 55.5 million gamers recorded in 2023, according to CESA. Mobiles and Tablets lead device usage at 49.6% share (2025), driven by deep smartphone penetration and the dominance of free-to-play titles. In-Game Purchases account for 57.3% of total revenue, fueled by Japan's gacha mechanics and strong player engagement. The Kanto region dominates with a 37.4% share, reflecting Tokyo's concentration of gaming studios, esports venues, and high-income consumers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 28.85 Billion |

|

Forecast Market Size (2034) |

USD 65.85 Billion |

|

CAGR (2026-2034) |

9.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (37.4%) |

|

Fastest Growing Region |

Kyushu-Okinawa Region |

The market grew from USD 18.48 Billion in 2020 to USD 28.85 Billion in 2025, anchored at USD 45.04 Billion in 2030, and is forecast to reach USD 65.85 Billion by 2034. The Nintendo Switch 2 launch in June 2025 propelled hardware sales by 49.3% in Japan, creating a new software adoption cycle. Mobile gaming remains the revenue backbone, with Japan's mobile IAP revenues second only to China in the Asia-Pacific region.

To get more information on this market, Request Sample

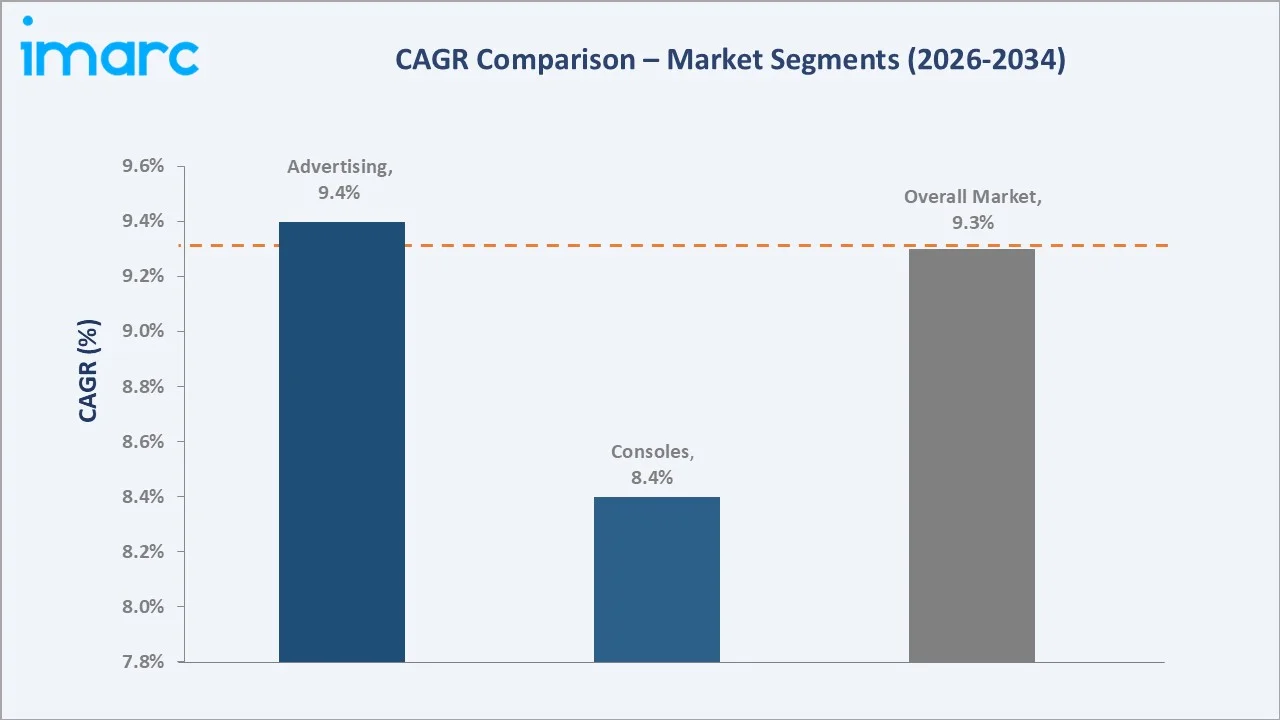

Mobiles & Tablets segment grows at an estimated 11.2% CAGR (2026-2034), outpacing Consoles at ~8.4%, as smartphone-first game design and 5G adoption unlock higher-quality mobile gaming experiences. In-Game Purchases expand at ~10.6% CAGR, supported by Japan's deeply entrenched monetization culture of gacha mechanics and event-driven spending.

Executive Summary

The Japan gaming market reached USD 28.85 Billion in 2025, representing Asia's second-largest gaming economy. Japan's over 55.5 million active gamers (2023, CESA) interact across a richly segmented ecosystem spanning console, mobile, PC, and arcade platforms. The 9.31% CAGR trajectory toward USD 65.85 Billion by 2034 reflects strong growth drivers including the Nintendo Switch 2 hardware cycle, mobile gaming expansion, and cloud gaming infrastructure buildout.

In-Game Purchase revenue at 57.3% (2025) anchors the market's monetization model, driven by gacha mechanics embedded in Japan's top mobile titles. Mobiles & Tablets at 49.6% device share confirm the shift from console-first to mobile-first engagement patterns among younger demographics. Japan's domestic publishers - including Bandai Namco, Nintendo, Capcom, and Sony Interactive Entertainment - collectively account for approximately 70% of all domestic mobile IAP revenue, demonstrating strong local market control.

Regionally, Kanto leads at 37.4% share, anchored by Tokyo's dense concentration of studios, esports facilities, and premium consumers. Kinki Region follows at 18.9%, with Osaka and Kyoto serving as secondary development hubs. The government's Society 5.0 digital strategy and expanding 5G infrastructure provide the macroeconomic foundation for sustained gaming market growth through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Device Segment |

Mobiles & Tablets – 49.6% share (2025) |

|

Leading Revenue Type |

In-Game Purchase – 57.3% share (2025) |

|

Dominant Region |

Kanto Region – 37.4% share (2025) |

|

Top Companies |

Nintendo, Sony Group Corporation, Bandai Namco Holdings Inc., DeNA Co., Ltd. |

|

Fastest Growing Device |

Mobiles & Tablets (~11.2% CAGR, 2026-2034) |

|

Market Opportunity |

Cloud gaming & AR/VR expansion post-5G rollout |

Key Analytical Observations Supporting The Above Data:

- Mobiles & Tablets at 49.6% (2025): Japan's smartphone penetration reached approximately 88% in 2024, per Ministry of Internal Affairs and Communications (MIC) data, enabling free-to-play mobile titles with gacha monetization to command the largest device share. Popular titles such as Pokemon TCG Pocket and Dragon Ball Z Dokkan Battle generate billions in annual IAP revenue domestically.

- In-Game Purchase at 57.3% (2025): Japan's gaming culture normalizes incremental in-app spending. Gacha pull rates and limited-time character unlocks drive per-user spending among Japan's 55.5 million active gamers (CESA 2023), creating a structurally high IAP share relative to global averages.

- Kanto Region dominance at 37.4%: Greater Tokyo accounts for roughly 28% of Japan's total GDP and houses the headquarters of Nintendo's Tokyo offices, Sony Interactive Entertainment, Bandai Namco, DeNA, SEGA, and Capcom's publishing operations, creating a self-reinforcing cluster of talent, capital, and consumer demand.

- Nintendo Switch 2 hardware launch (June 2025): Global sell-through exceeded 3.5 million units in the first four days, making it the highest-ever global launch for any Nintendo platform, per Nintendo investor disclosures. Japan domestic sales reached 2.46 million units within five months, driving hardware revenue growth of 49.3% in Japan in 2025.

- Cloud gaming opportunity: Japan's 5G commercial coverage reached 98% of populated areas by 2025, per the Ministry of Internal Affairs and Communications. This connectivity foundation underpins cloud gaming services from PlayStation Plus Premium, Xbox Cloud Gaming, and emerging domestic providers through 2034.

Japan Gaming Market Overview

Japan's gaming market encompasses consumer hardware, software, mobile applications, in-game monetization, digital distribution, esports, streaming, and emerging cloud-based gaming services. The ecosystem integrates hardware manufacturers (Nintendo, Sony), domestic and international game publishers, the Computer Entertainment Supplier's Association (CESA) regulatory framework, digital distribution platforms (Nintendo eShop, PlayStation Store, Google Play, App Store), and a deeply engaged consumer base of over 55.5 million gamers.

The Japan gaming market operates under MIC (Ministry of Internal Affairs and Communications) oversight for digital communications regulation and under CESA self-regulatory guidelines for game content ratings. Japan's advanced broadband infrastructure and near-universal smartphone access provide the digital backbone. Macroeconomic drivers include the Nintendo Switch 2 hardware cycle, 5G-enabled cloud gaming, government digital transformation mandates under Society 5.0, and Japan's globally influential gaming IP culture spanning franchises such as Pokemon, Mario, Final Fantasy, and Monster Hunter.

Market Dynamics

To evaluate market opportunities, Request Sample

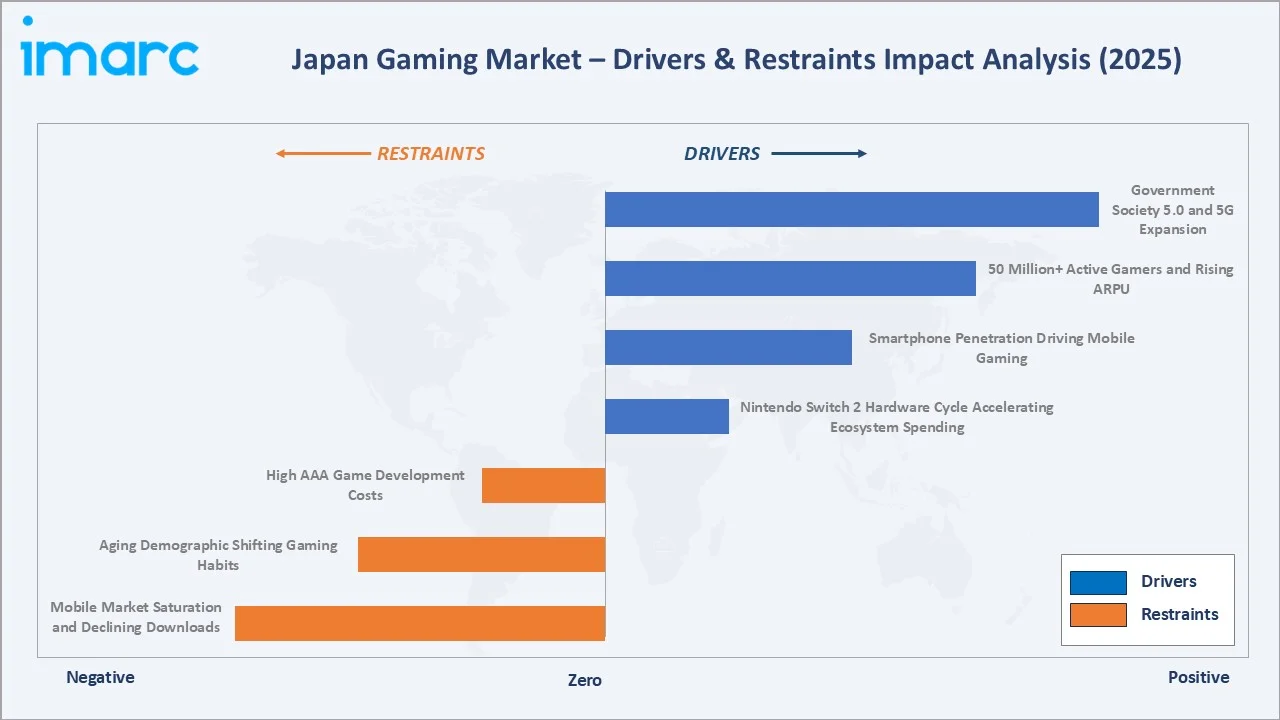

Market Drivers

- Nintendo Switch 2 Hardware Cycle Accelerating Ecosystem Spending: Nintendo launched the Switch 2 globally in June 2025, recording the highest-ever global sales launch in Nintendo history at 3.5 million units in four days, per Nintendo investor disclosures. The associated software pipeline, including Mario Kart World (2.66 million copies in Japan) and Pokemon Legends Z-A (2.5 million copies), expands the addressable game software market significantly through 2027.

- Smartphone Penetration Driving Mobile Gaming: Japan's smartphone penetration reached approximately 88% by 2024, according to Ministry of Internal Affairs and Communications (MIC) statistics. Mobile games account for the largest segment at 49.6% device share. In-app purchase (IAP) revenue from Japan's mobile market reached USD 11 billion in 2025, second only to China in Asia-Pacific, per Sensor Tower's 2025 Japan gaming report.

- 50 Million+ Active Gamers and Rising ARPU: Japan recorded 55.5 million active gamers in 2023. This high-spending culture supports premium titles, live service revenue, and recurring in-game purchases.

- Government Society 5.0 and 5G Expansion: Japan's Cabinet Office-led Society 5.0 initiative supports digital entertainment infrastructure. 5G commercial coverage reached 98% of populated areas by 2025 (MIC), providing the infrastructure for cloud gaming, AR/VR gaming, and high-fidelity mobile experiences through 2034.

Market Restraints

- Mobile Market Saturation and Declining Downloads: Japan's total mobile game downloads reached approximately 628 million for August 2024-July 2025, down 2.5% year-over-year, per Sensor Tower. The market may have reached peak download density, shifting growth pressure toward ARPU improvement rather than new user acquisition.

- Aging Demographic Shifting Gaming Habits: Japan's population aged 65 or older reached 34.9% in 2020 and is projected to reach 46.5% by 2050, per Cabinet Office statistics. Older demographics show lower gaming engagement rates, structurally limiting long-term user base growth absent significant cross-demographic product innovation.

- High AAA Game Development Costs: Production budgets for major Japanese IP titles have escalated significantly. Regulatory compliance, content localization, and platform certification costs add overhead for mid-tier developers, limiting the competitive breadth of Japan's game development ecosystem.

Market Opportunities

- Cloud Gaming Infrastructure Investment: Japan's 5G coverage at 98% of populated areas (MIC, 2025) creates a direct infrastructure opportunity for cloud gaming services. PlayStation Cloud, Xbox Cloud Gaming, and domestic providers are investing in low-latency streaming that could add USD 3-5 Billion in incremental market revenue by 2030.

- AR/VR Gaming Post-5G Rollout: Japan's advanced robotics and technology culture positions it as a primary AR/VR gaming adoption market. Investment in XR headsets and associated game content is accelerating post-5G commercial deployment, targeting Japan's premium consumer segment willing to adopt new gaming formats.

- Global IP Monetization: Japanese gaming IPs such as Pokemon, Mario, Final Fantasy, Dragon Ball, and Monster Hunter command loyal global audiences. Expanding digital and physical IP monetization outside Japan through licensed games, merchandise, and streaming adaptations represents a structurally growing revenue stream.

Market Challenges

- Loot Box and Gacha Regulatory Risk: Japan's Consumer Affairs Agency (CAA) has reviewed gacha mechanics that may constitute gambling-adjacent activities, particularly for under-18 players. Potential regulatory restrictions on gacha could materially affect Japan's dominant in-game purchase revenue model, which constitutes 57.3% of the market.

- Competition from Korean and Chinese Mobile Publishers: Foreign publishers from China and South Korea dominate Japan's top mobile download charts, per Sensor Tower's 2025 report. This competitive pressure compresses domestic publishers' mobile market share, particularly in casual and social game categories.

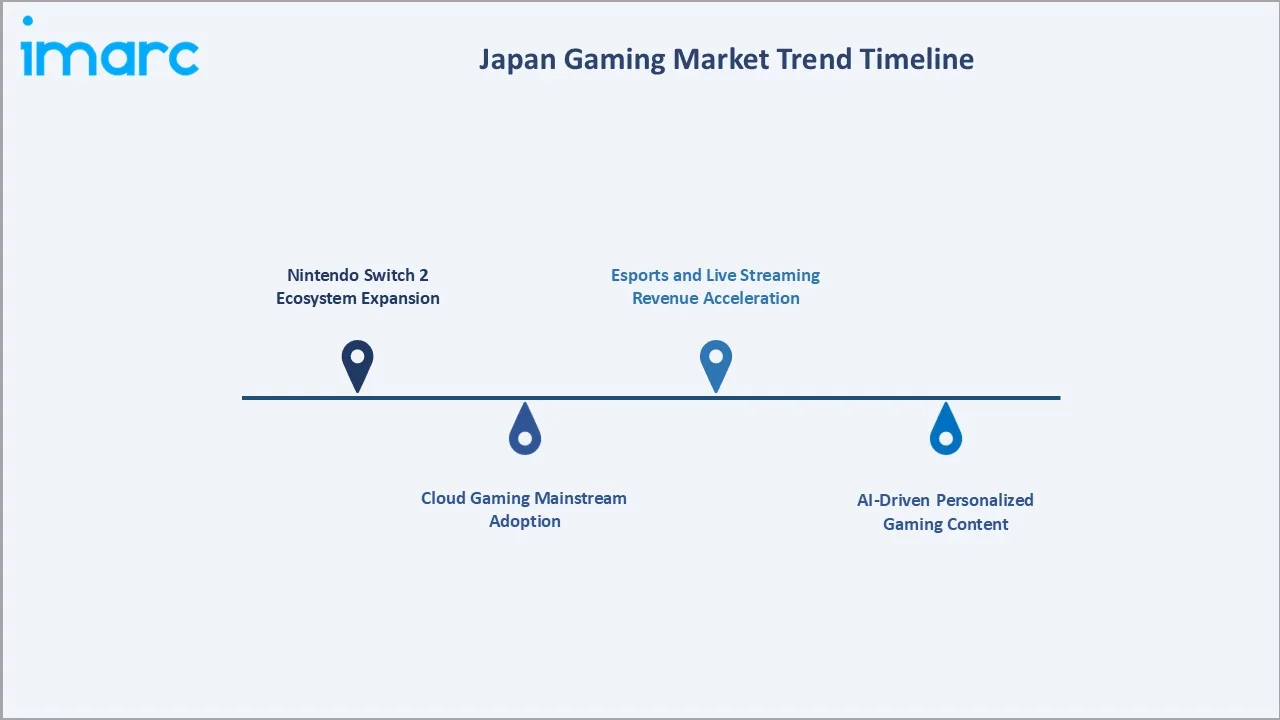

Emerging Market Trends

1. Nintendo Switch 2 Ecosystem Expansion

Nintendo's Switch 2 launch in June 2025 sold 19.86 million units globally by March 2026, per Nintendo annual disclosures. In Japan, Mario Kart World and Pokemon Legends Z-A collectively surpassed 5 million copies. The Switch 2 ecosystem creates a multi-year software attach rate cycle, with first-party title revenue expanding the market through 2028.

2. Cloud Gaming Mainstream Adoption

Japan's 5G coverage at 98% (MIC, 2025) and low-latency fiber penetration provide the ideal infrastructure for subscription-based cloud gaming. PlayStation Plus and Xbox Game Pass are expanding subscriber bases in Japan, while domestic providers are developing Japan-exclusive cloud gaming platforms targeting mobile-first users who cannot afford premium console hardware.

3. Esports and Live Streaming Revenue Acceleration

Japan's esports market is expanding rapidly, supported by the Japan Esports Union (JeSU) licensing framework and corporate sponsorship from major brands. Streaming platforms including YouTube Gaming, Twitch, and domestic platforms such as NicoNicoDouga integrate game content into Japan's USD 28 Billion+ gaming ecosystem, creating advertising and partnership revenue streams that are growing at double-digit rates.

4. AI-Driven Personalized Gaming Content

Japanese game studios are integrating AI tools for procedural content generation, adaptive difficulty systems, and personalized event scheduling within live service games. Companies such as DeNA and CyberAgent's Cygames division are investing in AI-powered backend systems that improve player retention metrics and optimize gacha event timing for maximum per-user revenue.

5. AR/VR Gaming and Location-Based Experiences

Building on the global success of Pokemon GO (Niantic) and domestic VR arcade experiences, Japan is positioning for the next wave of mixed reality gaming. Japan's dense urban infrastructure, public transit ridership, and cultural openness to location-based entertainment create a favorable environment for AR gaming expansion. VR arcade revenues in Japan are projected to grow at over 18% CAGR through 2030.

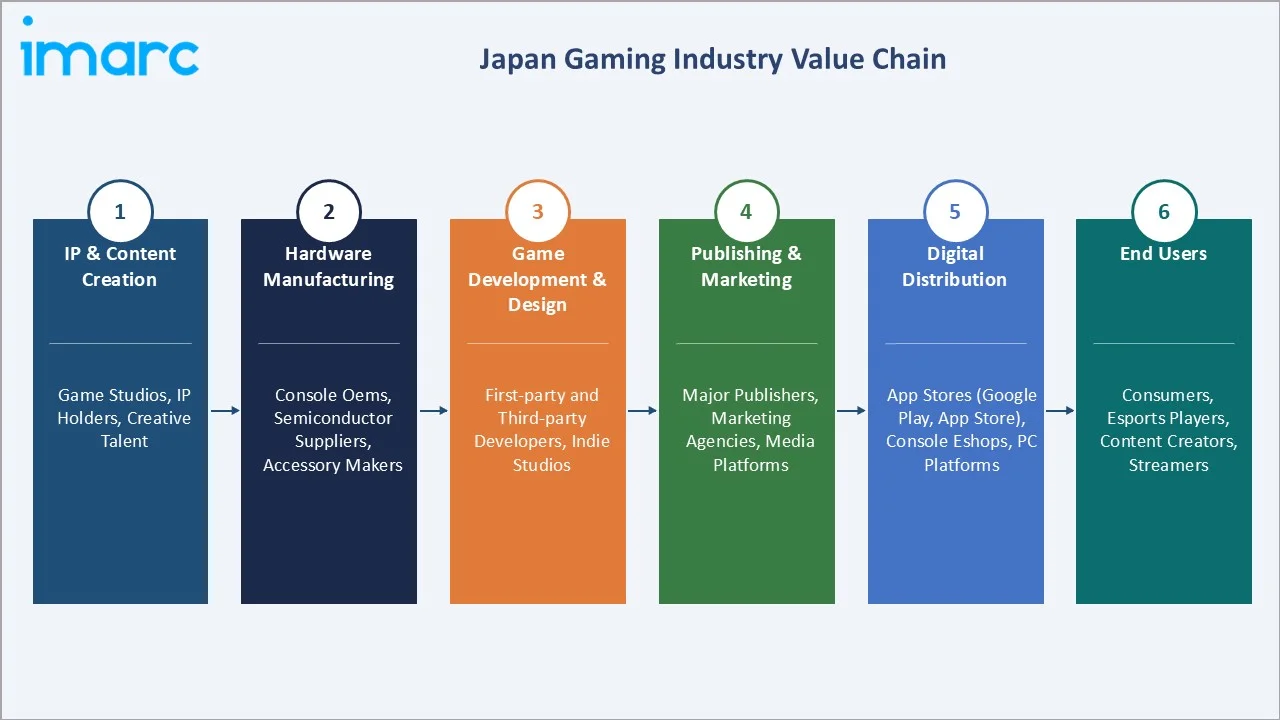

Industry Value Chain Analysis

Japan's gaming market value chain integrates IP creation, hardware and software development, publishing and marketing, digital and physical distribution, platform operation, and retail/app-store dispensing serving over 55.5 million active gamers under a mature regulatory and content rating environment.

|

Stage |

Key Participants |

|

IP & Content Creation |

Game studios, IP holders, creative talent |

|

Hardware Manufacturing |

Console OEMs, semiconductor suppliers, accessory makers |

|

Game Development & Design |

First-party and third-party developers, indie studios |

|

Publishing & Marketing |

Major publishers, marketing agencies, media platforms |

|

Digital Distribution |

App stores (Google Play, App Store), console eShops, PC platforms |

|

End Users |

Consumers, esports players, content creators, streamers |

Japan's game distribution operates through a well-established physical retail infrastructure alongside rapidly growing digital channels. Physical game retail is concentrated among major electronics chains such as Yodobashi Camera and Bic Camera, while digital distribution through Nintendo eShop and PlayStation Store is capturing growing share, with digital game sales at Nintendo reaching JPY 126.5 billion in Q3 FY2026, up 60% year-on-year.

Technology Landscape in the Japan Gaming Industry

Console Hardware Innovation

Nintendo's Switch 2 (launched June 2025) introduces an upgraded Nvidia-based GPU architecture, 4K docked output capability, and improved Joy-Con magnetic attachment. The hybrid console-handheld design maintains Nintendo's core differentiation. Sony's PlayStation 5 continues its market cycle with a Japan-exclusive budget model, though PS5 Japan unit sales declined around 40% in 2025 as Switch 2 captured consumer attention and spending.

Mobile and Cloud Gaming Technology

Japan's 5G commercial rollout, reaching 98% of populated areas by 2025 (MIC), enables cloud game streaming with sub-20ms latency in urban areas. DeNA and CyberAgent are actively developing cloud-native mobile game architectures that eliminate device hardware as a barrier to AAA-quality mobile gaming. Subscription-based cloud gaming services are growing at double-digit rates in Japan's mobile segment.

Artificial Intelligence in Game Development

AI-driven game development tools are reducing production timelines for Japanese studios. Procedural content generation, AI-based quality assurance, and adaptive NPC behavior systems are being integrated by studios including Capcom (used for Monster Hunter Wilds AI pathfinding) and Square Enix (AI narrative generation tools). Japan's Ministry of Economy, Trade and Industry (METI) has designated AI game technology as a strategic sector under its content industry roadmap.

AR/VR and Mixed Reality Gaming

Japan leads Asia in VR arcade infrastructure, with over 300 VR experience facilities operating in major cities as of 2024. The metaverse gaming layer, supported by Sony's PlayStation VR2 and emerging XR headsets, is attracting Japanese gaming IP holders to develop immersive extensions of flagship franchises. Nintendo has filed multiple AR patent applications for future Switch-adjacent AR gaming accessories.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Device Type |

Mobiles and Tablets |

49.6% |

2025 |

|

Revenue Type |

In-Game Purchase |

57.3% |

2025 |

|

Platform |

🔒 |

🔒 |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Age Group |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

37.4% |

2025 |

By Device Type

Mobiles & Tablets lead at 49.6% market share (2025). Japan's mobile gaming market generated approximately USD 11 billion in annual revenue for the 12-month period ending July 2025, second only to China in Asia-Pacific, per Sensor Tower's 2025 Japan gaming report. Revenue leaders include Bandai Namco (Dragon Ball Z Dokkan Battle), The Pokemon Company (Pokemon TCG Pocket), and Konami (eFootball). The free-to-play with gacha monetization model drives high ARPU and sustained engagement.

To access detailed market analysis, Request Sample

Consoles at 30.8% share are dominated by the Nintendo Switch ecosystem and Sony PlayStation 5. Nintendo Switch 2 sold 3.7 million units in Japan in 2025, representing more than half of all home console sales in the country, per industry data. Computers at 19.6% are anchored by Japan's growing PC gaming community on Steam, where Japanese publishers Bandai Namco, SEGA, and Capcom rank among the global top ten publishers by all-time Steam revenue, per Sensor Tower.

By Revenue Type

In-Game Purchase at 57.3% (2025) is the dominant revenue model. Japan's deeply embedded gacha culture and event-driven limited-time content systems sustain premium per-session spending across both mobile and console platforms. Japan's Consumer Affairs Agency (CAA) guidelines regulate gacha mechanics, but the core IAP model remains structurally intact. Game Purchase at 28.5% reflects both physical and digital title sales, with Nintendo's Mario Kart World (2.66 million Japan units in 2025) and Sony's exclusive software portfolio driving one-time purchase revenue.

Advertising at 14.2% is the fastest-growing revenue type within Japan's gaming segment, driven by programmatic in-game advertising adoption on mobile platforms and brand sponsorships within esports tournaments. Japan's digital advertising market is growing at approximately 15% annually, with gaming-embedded advertising capturing an increasing share of digital budgets from automotive, consumer electronics, and beverage brands.

Regional Market Insights

Japan's gaming market is geographically concentrated in major metropolitan regions with high population density, broadband penetration, and consumer electronics spending. The eight regions analyzed collectively represent the full domestic market.

|

Region |

Market Share (2025) |

Key Growth Drivers |

|

Kanto |

37.4% |

Tokyo studio concentration, high ARPU consumers, esports venues |

|

Kinki |

18.9% |

Osaka & Kyoto gaming culture, content development clusters |

|

Central/Chubu |

14.6% |

Industrial base supporting hardware manufacturing |

|

Kyushu-Okinawa |

9.3% |

Growing tech startup ecosystem, university-driven indie development |

|

Tohoku |

7.1% |

Rebuilding digital infrastructure, rural mobile-first gaming |

|

Chugoku |

5.4% |

Hiroshima & Okayama tech investment, manufacturing base |

|

Hokkaido |

4.2% |

Tourism-linked gaming venues, northern Japan digital adoption |

|

Shikoku |

3.1% |

Compact geography enabling targeted mobile game campaigns |

The Kanto Region's 37.4% dominance reflects Greater Tokyo's role as Asia's premier gaming industry hub. The region houses the global or regional headquarters of Japan's leading gaming companies. Kinki Region's 18.9% share is driven by Osaka-based Capcom, whose Monster Hunter and Street Fighter franchises generate billions in annual revenue. The Kyushu-Okinawa Region at 9.3% is emerging as Japan's second-tier gaming development hub, with government-backed digital startup incentives attracting mobile game studios.

Competitive Landscape

Japan's gaming market is moderately concentrated at the hardware level (Nintendo-Sony duopoly) and competitive at the software and mobile publishing level. Japanese publishers collected approximately 70% of all domestic mobile IAP revenue in 2025, per Sensor Tower, demonstrating strong local publisher control despite competitive pressure from Korean and Chinese titles in download rankings.

|

Company Name |

Key Brand / Product |

Position |

Strategic Focus |

| Nintendo | Switch 2, Mario, Pokemon, Zelda | Market Leader | Switch 2 software attach rate: 48.71M games sold alongside 19.86M hardware units (2.5x) by March 2026. |

| Sony Group Corporation | PlayStation 5, God of War, Spider-Man | Market Leader | PS5 lifetime shipments: 93.7M units by March 2026. |

| Bandai Namco Holdings Inc. | Tekken, Dragon Ball, Pac-Man | Established Player | Operates via Bandai Namco Entertainment. One of Steam's highest-revenue Japanese publishers. |

| DeNA Co., Ltd. | Multiple mobile titles, Nintendo mobile partnership |

Challenger |

Co-developer of Nintendo mobile titles (Fire Emblem Heroes, Mario Kart Tour, Animal Crossing: Pocket Camp). |

Nintendo and Sony together command the console hardware segment with a combined market share that leaves limited room for challengers. At the software level, Bandai Namco's Elden Ring surpassed 30 million copies sold globally by 2025, demonstrating Japan's capacity to produce globally dominant premium titles.

Key Company Profiles

Nintendo

Nintendo is Japan's most globally dominant gaming company and a world leader in interactive entertainment. Founded in 1889 and headquartered in Kyoto, Nintendo combines proprietary hardware design with world-renowned first-party software IP.

- Product Portfolio: Switch 2, Mario, Pokemon, Zelda, and among others.

- Recent Developments: In June 2025, Nintendo launched Nintendo Switch 2, recording 3.5 million units sold in the first four days, the highest global launch in Nintendo's history.

- Strategic Focus: Hardware-software ecosystem lock-in through exclusive first-party IP; expanding IP monetization beyond gaming into films and theme parks; Nintendo Switch Online at 34 million subscribers as of September 2025; growth expected as Switch 2 install base expands.

Sony Group Corporation

Sony Interactive Entertainment (SIE), a subsidiary of Sony Group Corporation headquartered in San Mateo (California) with significant Japan operations, is the creator of the PlayStation brand. PlayStation 5 maintains a 45% global gaming console market share, per industry data.

- Product Portfolio: PlayStation 5 (standard and Digital Edition), PlayStation VR2, PlayStation Plus subscription tiers (Essential, Extra, Premium), and exclusive software including God of War, Spider-Man, Horizon, Gran Turismo, and others.

- Recent Developments: In July 2025, Sony and Bandai Namco Holdings Inc. signed a strategic business alliance agreement where Sony became a shareholder holding approximately 2.5% of the total issued shares of Bandai Namco.

- Strategic Focus: Live service game investment; PlayStation PC publishing strategy; expanding PlayStation brand beyond hardware through media and streaming; cloud gaming infrastructure development.

Bandai Namco Holdings Inc.

Bandai Namco Entertainment, a subsidiary of Bandai Namco Holdings Inc. (Tokyo), is one of Japan's largest and most globally recognized game publishers. The company blends gaming with anime IP, toys, and theme park attractions, creating a diversified entertainment ecosystem. Bandai Namco ranks among the top global Steam publishers by all-time revenue, per Sensor Tower 2025.

- Product Portfolio: Tekken 8, Dragon Ball Z Dokkan Battle, Pac-Man, Naruto series, and others.

- Recent Developments: In May 2025, Bandai Namco Entertainment Inc. published ELDEN RING NIGHTREIGN, a standalone co-op roguelike action RPG developed by FromSoftware, Inc., which sold 5 million units by July 2025.

- Strategic Focus: Expanding global franchise IP; live service game monetization through seasonal content; anime-to-game pipeline reinforcing existing IP ecosystems.

Market Concentration Analysis

Japan's gaming market exhibits moderate concentration at the hardware level and moderate fragmentation at the software and mobile levels. Nintendo and Sony Interactive Entertainment together control the console hardware segment with a duopoly structure.

Consolidation trends are emerging. Microsoft's acquisition of Activision Blizzard strengthened Xbox Game Pass content in Japan. Bandai Namco's subsidiary acquisition in September 2023 signals active consolidation. The mobile segment is consolidating around IP-anchored live service titles, with smaller mobile studios struggling to compete against established gacha ecosystems. The market is expected to become moderately concentrated at the mobile publisher level by 2030.

Investment & Growth Opportunities

Fastest Growing Segments

Mobiles & Tablets segment (~11.2% CAGR), Advertising revenue type (~12-15% CAGR within gaming), cloud gaming infrastructure (~18% CAGR), AR/VR gaming (~20%+ CAGR from a lower base), esports and live streaming partnerships (~15% CAGR), and Nintendo Switch 2 software ecosystem (high volume through 2028) represent Japan's highest-growth investment vectors through 2034.

Emerging Market Opportunities

Japan's 5G-enabled cloud gaming market is in early commercial stage with significant room for penetration. Rural Japan's digitization, supported by MIC's Universal Service framework, creates mobile gaming adoption opportunities in Tohoku, Hokkaido, and Shikoku regions, which collectively hold 14.4% market share but are growing faster than mature metropolitan regions. The esports education and career pathway market, supported by Japan's growing university esports programs, creates a developing ecosystem for youth engagement.

Investment Themes

- Switch 2 Software Ecosystem Investment: Nintendo's Switch 2 platform with 19.86 million hardware units by March 2026 creates a receptive installed base for AAA third-party software investment. Developers investing in Switch 2-exclusive or enhanced ports can access Japan's highest-spending hardware demographic through 2030.

- Cloud Gaming Infrastructure Buildout: Japan's 98% 5G population coverage (MIC) creates infrastructure readiness for cloud gaming at scale. Data center investment in low-latency edge computing nodes in Osaka and Tokyo is accelerating, attracting gaming cloud service providers seeking Asia-Pacific hub deployments.

- Japan IP Global Licensing Opportunities: Japanese gaming IPs command globally loyal audiences. Licensing Japanese gaming IP for international mobile adaptations, animated series, and live service games represents a multi-billion dollar opportunity for content rights holders and licensing intermediaries.

Future Market Outlook (2026-2034)

The Japan gaming market is projected to grow from USD 28.85 Billion in 2025 to USD 65.85 Billion by 2034, at a 9.31% CAGR that reflects Japan's unique market dynamics – a hardware cycle driven by Nintendo Switch 2, mobile market maturation with premium ARPU growth, and cloud gaming infrastructure buildout fueled by 5G. Japan's intermediate milestone of USD 45.04 Billion in 2030 confirms consistent compound growth anchored by multiple structural tailwinds.

Three structural forces anchor this growth with predictability: the Nintendo Switch 2 software ecosystem expanding through 2030 as the installed base of nearly 20 million global units (March 2026) generates multi-year software attach revenue; the continued dominance of Japan's in-game purchase monetization model at 57.3% (2025) growing at ~10.6% CAGR; and Japan's Society 5.0 digital transformation agenda systematically building cloud gaming, AR/VR, and AI-driven gaming infrastructure.

Japan's USD 65.85 Billion gaming market by 2034 will consolidate the country's position as a global gaming technology innovation leader, generating world-class IPs, hardware platforms, and digital entertainment experiences that drive both domestic consumption and significant export-driven licensing revenue across global markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with 75+ industry stakeholders (2025-2026), including game development directors from Japan's leading studios; CESA (Computer Entertainment Supplier's Association) representatives; digital distribution platform executives; esports organization operators; mobile gaming monetization specialists; and retail electronics chain buyers. Interviews were conducted in both Japanese and English and validated against public financial disclosures.

Secondary Research

Secondary research encompassed CESA Game Industry Report 2024, Ministry of Internal Affairs and Communications (MIC) ICT Infrastructure Surveys 2024, Cabinet Office Society 5.0 Digital Policy Documents, Nintendo investor relations disclosures (FY2025-FY2026), Sony Group Corporation annual reports, Sensor Tower Japan Gaming Report 2025, METI Content Industry Roadmap, Japan Esports Union (JeSU) annual statistics, and company annual reports for Japan's leading gaming companies. Over 120 secondary sources were reviewed across Japanese and English language publications.

Forecasting Models

Market forecasts were developed using hardware installed base x software attach rate x ARPU models, segmented by device type and revenue type, validated against CESA industry statistical data and Nintendo/Sony public financial disclosures. Key inputs include MIC smartphone penetration data, Switch 2 global unit sales trajectory, mobile IAP market data from Sensor Tower, 5G coverage expansion data from MIC, and Cabinet Office demographic aging projections. Historical data (2020-2025) anchors the forecast baseline, with USD 18.48 Billion (2020) to USD 28.85 Billion (2025) trajectory validated against CESA and public company data.

Japan Gaming Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Device Types Covered | Consoles, Mobiles and Tablets, Computers |

| Platforms Covered | Online, Offline |

| Revenue Types Covered | In-Game Purchase, Game Purchase, Advertising |

| Types Covered | Adventure/Role Playing Games, Puzzles, Social Games, Strategy, Simulation, Others |

| Age Groups Covered | Adult, Children |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Nintendo, Sony Group Corporation, Bandai Namco Holdings Inc., DeNA Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan gaming market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan gaming market.

- The study maps the leading, as well as the fastest-growing, markets. It further enables stakeholders to identify the key country-level markets within the regi

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan gaming industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Gaming Market Report

The Japan gaming market was valued at USD 28.85 Billion in 2025, covering console, mobile, PC, and emerging cloud gaming segments.

The Japan gaming market is projected to grow at a CAGR of 9.31% during 2026-2034, reaching USD 65.85 Billion by 2034, driven by Nintendo Switch 2 ecosystem expansion, mobile gaming, and 5G-enabled cloud gaming infrastructure.

Mobiles & Tablets lead at 49.6% market share (2025), driven by Japan's 88% smartphone penetration and dominant free-to-play gacha-monetization mobile games generating approximately USD 11 billion in annual IAP revenue.

In-Game Purchase holds the largest share at 57.3% (2025), anchored by Japan's gacha game mechanics, live service events, and per-character unlocks that drive consistently high ARPU across mobile and console platforms.

Kanto Region leads at 37.4% share (2025), reflecting Tokyo's concentration of major gaming studios, publisher headquarters, esports venues, and premium consumer demographics with high disposable income and gaming engagement.

Leading companies include Nintendo, Sony Group Corporation, Bandai Namco Holdings Inc., DeNA Co., Ltd., among others.

Japan's gaming market is projected to reach approximately USD 45.04 Billion by 2030, driven by Nintendo Switch 2 software ecosystem growth, mobile gaming ARPU expansion, and 5G-enabled cloud gaming platform adoption.

Mobile gaming growth is driven by Japan's 88% smartphone penetration (MIC 2024), free-to-play gacha monetization culture, dominant Japanese publishers capturing 70% of domestic IAP revenue, and 5G enabling higher-quality mobile experiences.

Nintendo Switch 2 launched June 2025 with 3.5 million units in the first four days globally, sold 3.7 million units in Japan in 2025, and drove Japan hardware revenues up 49.3%. The hardware cycle creates a multi-year software attach revenue expansion through 2028.

Fastest growing segments include Mobiles & Tablets (~11.2% CAGR), In-Game Purchase revenue type (~10.6% CAGR), cloud gaming infrastructure, AR/VR gaming, and in-game advertising monetization, all growing above the market's 9.31% average CAGR.

Japan's esports market, governed by the Japan Esports Union (JeSU), generates growing revenue through sponsorships, streaming rights, and tournament attendance. Esports-linked advertising and broadcasting represent a rapidly expanding segment within Japan's USD 28.85 Billion gaming ecosystem.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)