Japan In-App Advertising Market Size, Share, Trends and Forecast by Advertising Type, Platform, Application, and Region, 2026-2034

Japan In-App Advertising Market Size, Share, Trends & Forecast (2026-2034)

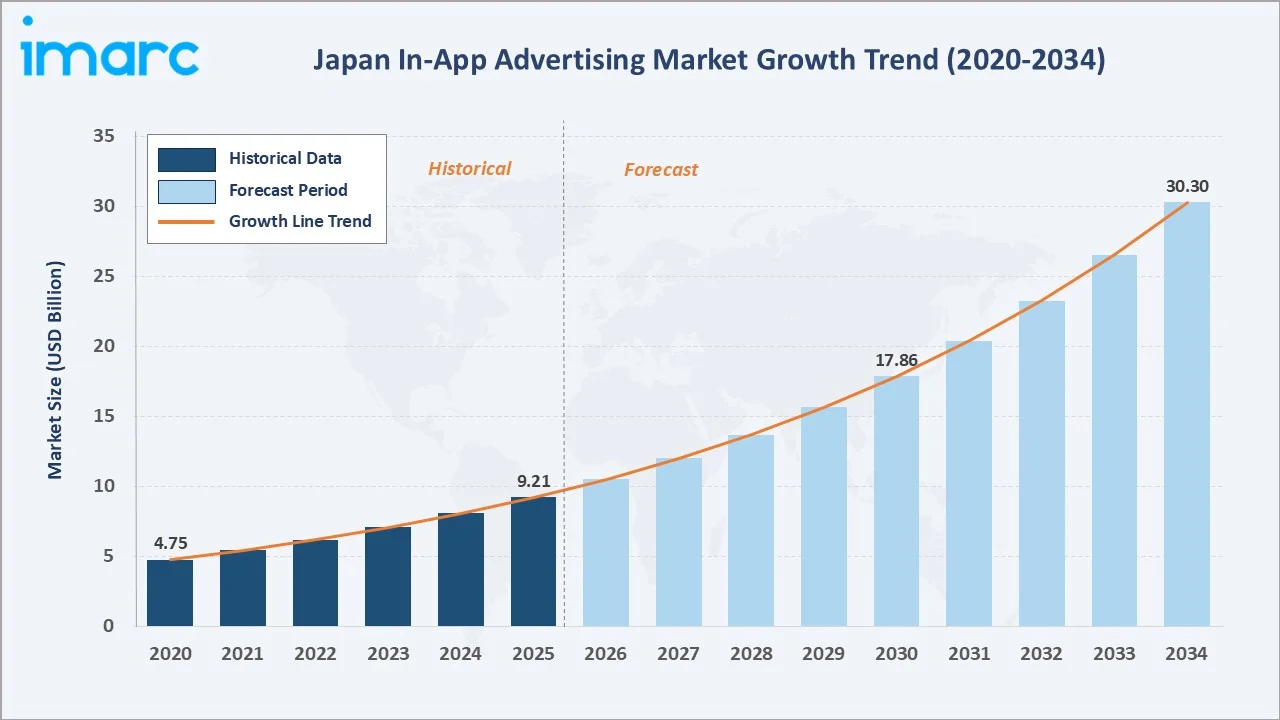

The Japan in-app advertising market size reached USD 9.21 Billion in 2025 and is projected to reach USD 30.30 Billion by 2034, exhibiting a CAGR of 14.16% during 2026-2034. Rising mobile device penetration, the growing mobile-first economy, and expanding 5G network coverage are the primary forces driving in-app advertising market growth.

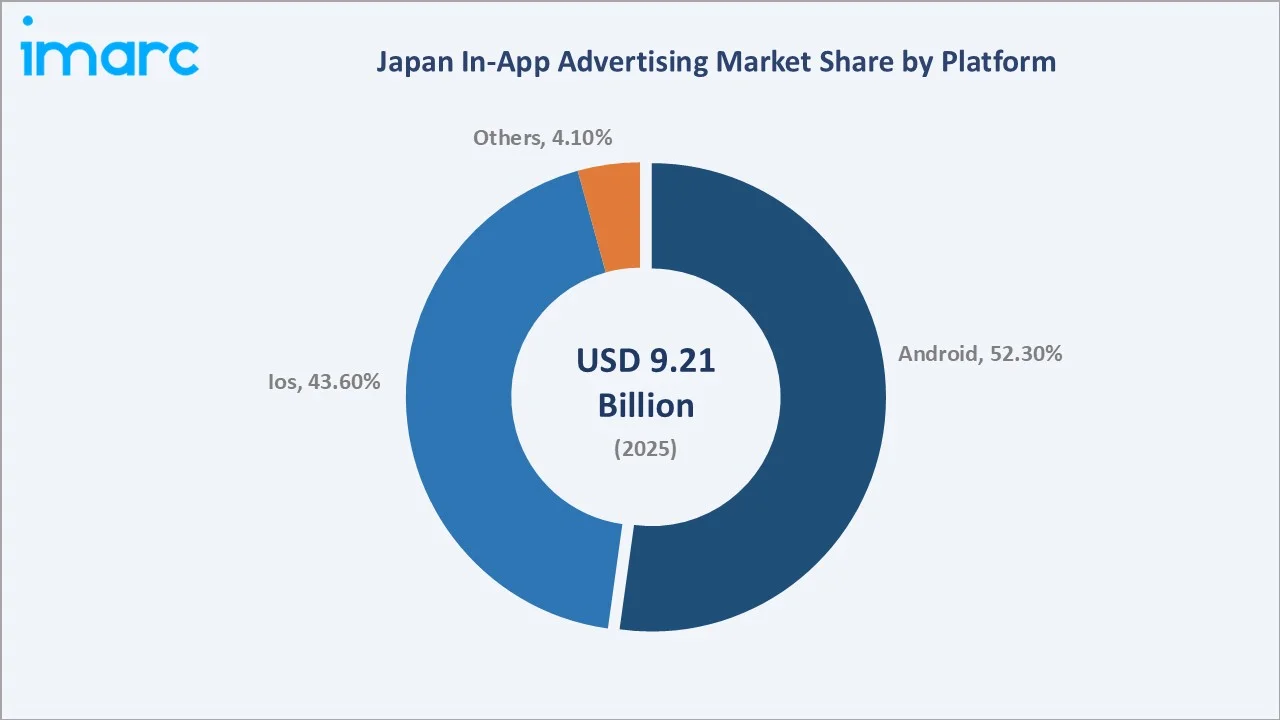

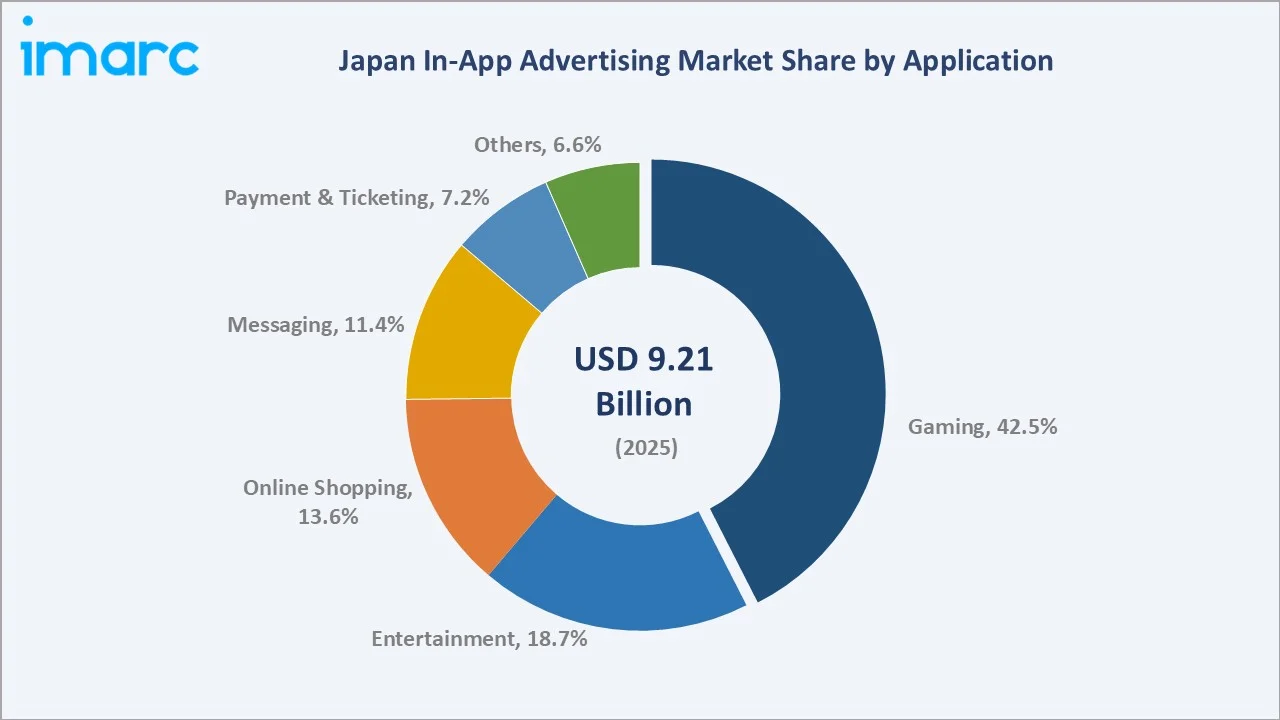

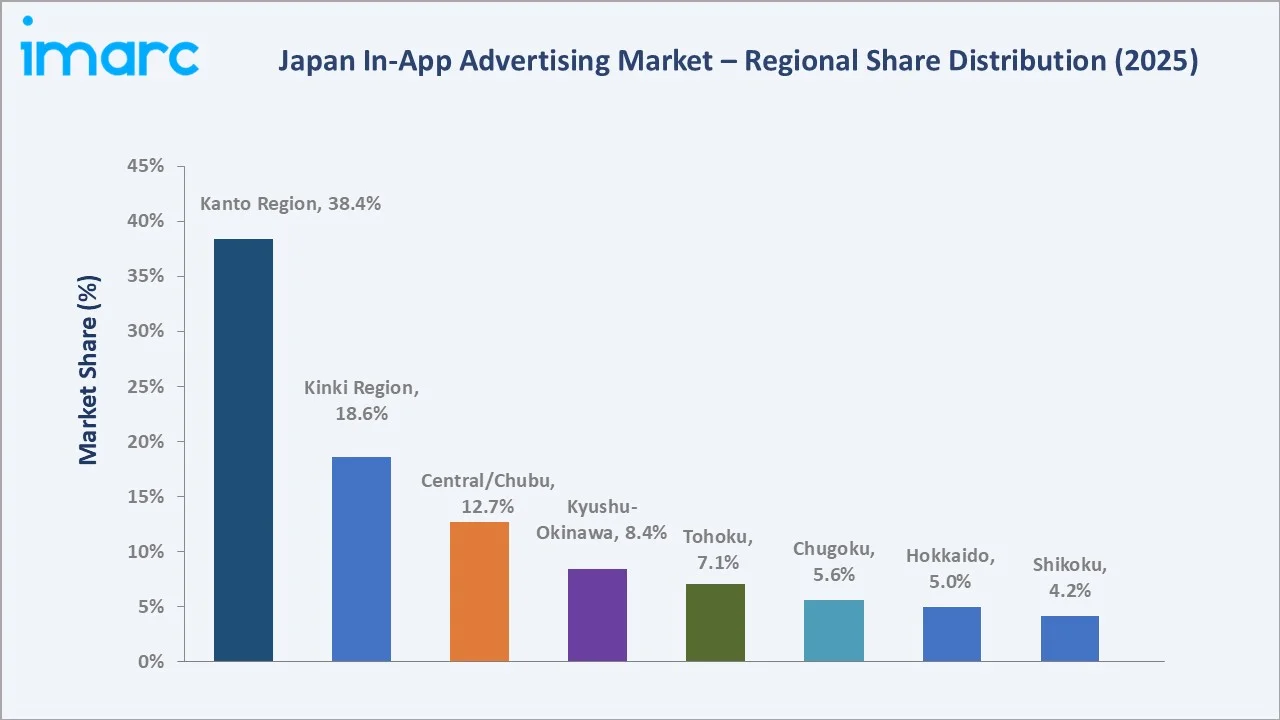

Android dominates the platform mix at 52.3% in 2025, while Gaming leads the application segment at 42.5%. The Kanto Region commands a dominant 38.4% regional share in 2025, reflecting the concentration of digital commerce and advertising activity in the Greater Tokyo area.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.21 Billion |

|

Forecast Market Size (2034) |

USD 30.30 Billion |

|

CAGR (2026-2034) |

14.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (38.4% share, 2025) |

|

Second Largest Region |

Kinki Region (18.6% share, 2025) |

|

Leading Platform |

Android (52.3%, 2025) |

|

Leading Application |

Gaming (42.5%, 2025) |

The Japan in-app advertising market growth trajectory from 2020 through 2034, with the historical expansion to USD 9.21 Billion in 2025, reflects consistent mobile-driven demand, while the forecast to USD 30.30 Billion captures accelerating 5G rollout, AI-driven targeting, and Japan's expanding digital-first consumer economy.

To get more information on this market, Request Sample

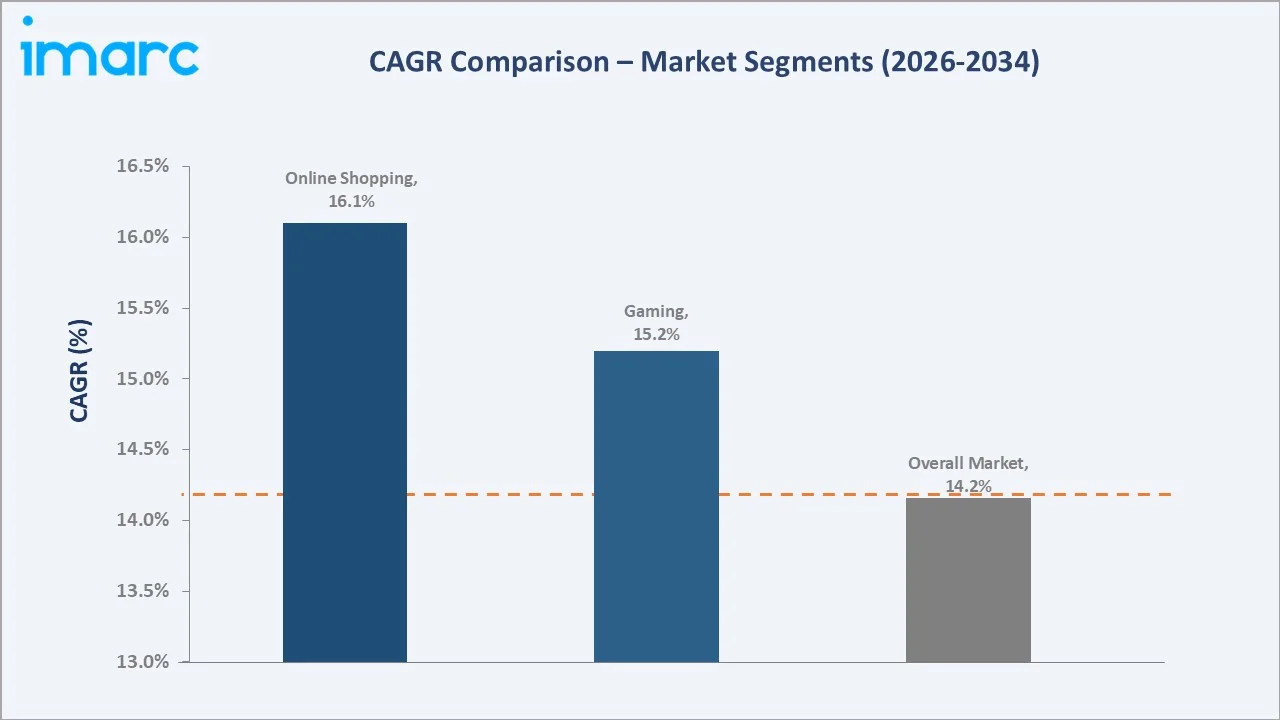

The CAGR trajectories across key platform and application sub-segments, with Online Shopping at ~16.1% CAGR and Gaming at ~15.2% CAGR, are the fastest-growing categories within the Japan in-app advertising industry analysis through 2034.

Executive Summary

The Japan in-app advertising market is on a sustained growth trajectory from USD 9.21 Billion in 2025 to USD 30.30 Billion by 2034. In-app advertising, an essential performance marketing channel within mobile applications spanning gaming, entertainment, e-commerce, and messaging, benefits from Japan's near-universal smartphone adoption and mobile-first digital consumption culture.

Android platform dominates at 52.3% in 2025, driven by broad device availability across consumer income segments and developer-friendly monetization tools. iOS captures 43.6%, commanding premium advertiser CPMs due to its concentrated high-value consumer demographic.

Gaming leads application segments at 42.5%, reflecting Japan's globally significant mobile gaming industry anchored by major domestic publishers and globally distributed titles.

The Kanto Region dominates at 38.4% in 2025, reflecting Tokyo's concentration of digital-native businesses, advertising agencies, and high-density smartphone user populations. Kinki Region (18.6%) and Central/Chubu Region (12.7%) follow, driven by Osaka and Nagoya's growing digital advertising ecosystems.

Key Market Insights

|

Insight |

Data |

|

Leading Platform |

Android - 52.3% share (2025) |

|

Second Platform |

iOS - 43.6% share (2025) |

|

Leading Application |

Gaming - 42.5% (2025) |

|

Second Application |

Entertainment - 18.7% (2025) |

|

Leading Region |

Kanto Region - 38.4% (2025) |

|

Top Companies |

Dentsu Group Inc., CyberAgent, Inc., LY Corporation, Google LLC, Hakuhodo DY Holdings Inc., Adways Inc., CyberZ Inc. |

Key Analytical Observations Expanding on the Above Data:

- Android's 52.3% platform dominance in 2025 reflects the OS's broader device penetration across Japan's mid-tier smartphone segment, combined with the comprehensive programmatic ad network offering advertisers deep integration across millions of Android applications and superior real-time bidding infrastructure for programmatic in-app placements.

- Gaming's 42.5% application share in 2025 is sustained by Japan's globally prominent mobile gaming market where publishers deploy rewarded video, offerwall, and interstitial formats within deeply engaging freemium game sessions generating the highest user engagement time-in-app metrics of any application category.

- Kanto Region's 38.4% market dominance reflects Tokyo's structural advantages as Japan's largest concentration of advertising agencies, brand headquarters, digital publishers, and app developers, creating a self-reinforcing ecosystem where advertiser budgets and premium inventory disproportionately concentrate.

- Kinki Region at 18.6% represents Osaka's growing role as Japan's second advertising hub, with Kansai-based consumer brands and e-commerce players increasingly allocating in-app budgets.

Japan In-App Advertising Market Overview

In-app advertising is a digital marketing practice that delivers promotional content within mobile applications installed on smartphones and tablets. Ad formats span banner advertisements, interstitial full-screen ads, rewarded video units, native ad placements, and playable ads, each offering distinct engagement profiles suited to different advertiser objectives and application contexts.

The Japan in-app advertising ecosystem integrates mobile OS platforms (Android and iOS), app developers and publishers, supply-side platforms (SSPs), demand-side platforms (DSPs), data management platforms (DMPs), ad networks, programmatic exchanges, and measurement and attribution vendors serving diverse end-use advertiser verticals including gaming, FMCG, financial services, entertainment, and e-commerce.

Market Dynamics

To evaluate market opportunities, Request Sample

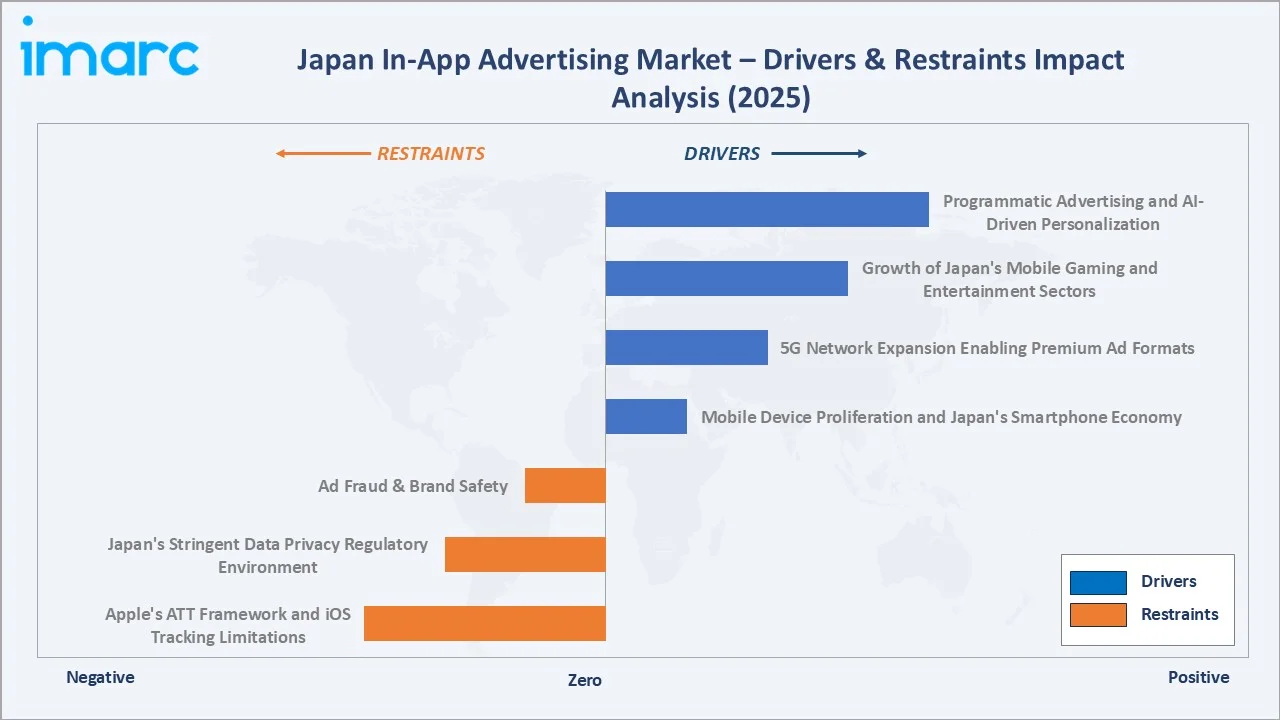

Market Drivers

- Mobile Device Proliferation and Japan's Smartphone Economy: As of 2023, Japan has approximately 97.44 million smartphone users, representing a smartphone penetration rate of 78.6% of its total population, creating an unparalleled in-app advertising inventory scale and engagement opportunity for brands targeting Japan's 95 million-plus active app users.

- 5G Network Expansion Enabling Premium Ad Formats: Japan's 5G network reached over 98% population coverage by 2025 under the Ministry of Internal Affairs and Communications' national rollout plan, enabling bandwidth-intensive rewarded video, playable ads, and interactive AR ad formats that generate 3-5x higher engagement rates than standard banner placements.

- Growth of Japan's Mobile Gaming and Entertainment Sectors: A survey indicated that 65% of Japanese smartphone users play games daily, and 92% play at least once a week, with freemium app monetization models generating premium advertising inventory from highly engaged, time-rich user sessions, making gaming in-app placements among the highest-CPM inventory globally.

Market Restraints

- Apple's ATT Framework and iOS Tracking Limitations: Apple Inc.’s App Tracking Transparency (ATT) framework has introduced stricter privacy requirements that limit cross-app user tracking unless users explicitly opt in; however, relatively low opt-in rates in many markets have reduced the availability of user-level data. As a result, advertisers are facing challenges in maintaining precise audience targeting and accurately measuring campaign performance, with the impact being especially pronounced on iOS, which continues to hold a significant share of the mobile ecosystem in several regions.

- Japan's Stringent Data Privacy Regulatory Environment: The revised Act on Protection of Personal Information (APPI), effective April 2022, imposes strict requirements on behavioral data collection, cross-application data sharing, and user consent management, increasing compliance costs for ad tech operators.

Market Opportunities

- Programmatic Advertising and AI-Driven Personalization: The adoption of programmatic in-app advertising in Japan is accelerating, with demand-side platform (DSP)-enabled real-time bidding expected to account for a growing share of in-app ad spend, driving greater efficiency for advertisers. At the same time, publishers are increasingly leveraging AI and machine learning capabilities, such as dynamic floor price optimization, to enhance monetization outcomes, resulting in a more automated, data-driven advertising ecosystem.

- Expansion of Contextual Advertising Post-Cookie Deprecation: The transition to cookie less, contextual targeting methodologies is creating demand for Japan-specific contextual intelligence solutions, where app-level content signals, behavioural cohorts, and publisher first-party data replace third-party identifiers, benefiting domestic ad tech innovators.

Market Challenges

- Ad Fraud and Brand Safety in the In-App Ecosystem: Ad fraud and brand safety concerns remain a persistent challenge within Japan’s in-app advertising ecosystem, where invalid traffic, such as bot activity, click injection, and SDK spoofing, accounts for a notable share of total ad impressions. This level of fraud exposure is increasing scrutiny from advertisers, prompting greater investment in third-party verification, fraud detection, and measurement technologies to ensure campaign integrity and improve transparency across the mobile advertising supply chain.

- Talent Shortage in Mobile Ad Tech Expertise: Japan's digital advertising industry faces a shortage of qualified programmatic advertising technologists, data scientists specializing in mobile attribution, and ad operations professionals capable of managing complex multi-DSP campaign structures across Japan's fragmented app publisher ecosystem.

Emerging Market Trends

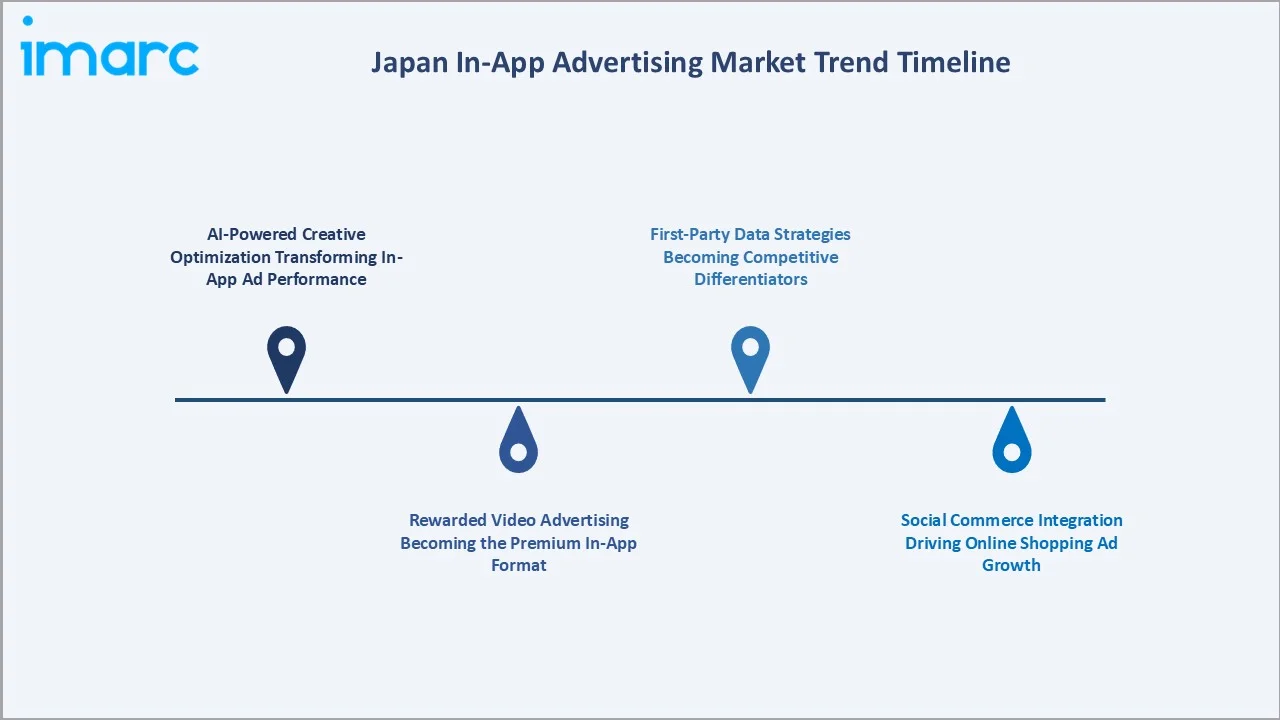

1. AI-Powered Creative Optimization Transforming In-App Ad Performance

Generative AI tools are enabling real-time dynamic creative optimization (DCO) for in-app advertising campaigns in Japan, where AI models generate thousands of ad creative variants and automatically optimize copy, visuals, and call-to-action elements based on audience response data, reducing campaign production costs significantly.

2. Rewarded Video Advertising Becoming the Premium In-App Format

Rewarded video ads, where user’s opt-in to view a 15-30 second advertisement in exchange for in-app currency or premium content access, generate opt-in rates of 70-80% in Japanese gaming applications, delivering 10-20x higher engagement than interstitial formats and commanding CPMs of USD 15-40.

3. Social Commerce Integration Driving Online Shopping Ad Growth

Messaging platform integration with e-commerce and in-app advertising is creating closed-loop shopping advertising ecosystems where Japanese consumers discover, evaluate, and purchase products within a single app session, directly driving the market of online shopping application advertising.

4. First-Party Data Strategies Becoming Competitive Differentiators

Japan's largest digital publishers and app networks are developing first-party data clean room solutions that enable advertisers to match customer data against publisher audience segments without exposing individual-level data, creating privacy-compliant targeting at premium CPMs aligned with Japan's APPI requirements.

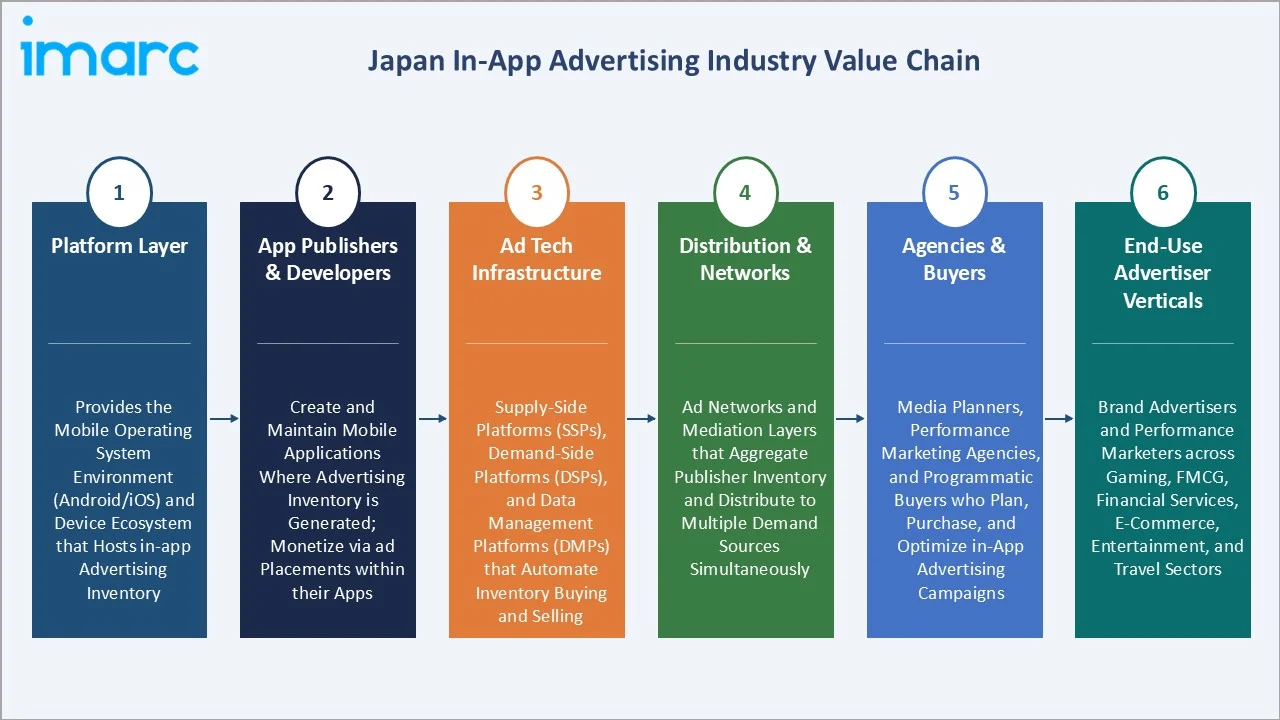

Industry Value Chain Analysis

The Japan in-app advertising value chain spans six stages from mobile OS platform through end-user engagement. Ad technology intermediaries and programmatic infrastructure capture the highest value-add margins, while data enrichment and measurement services generate significant recurring revenue streams for analytics and attribution vendors.

|

Stage |

Description |

|

Platform Layer |

Provides the mobile operating system environment (Android/iOS) and device ecosystem that hosts in-app advertising inventory. |

|

App Publishers & Developers |

Create and maintain mobile applications where advertising inventory is generated; monetize via ad placements within their apps. |

|

Ad Tech Infrastructure |

Supply-side platforms (SSPs), demand-side platforms (DSPs), and data management platforms (DMPs) that automate inventory buying and selling. |

|

Distribution & Networks |

Ad networks and mediation layers that aggregate publisher inventory and distribute to multiple demand sources simultaneously. |

|

Agencies & Buyers |

Media planners, performance marketing agencies, and programmatic buyers who plan, purchase, and optimize in-app advertising campaigns. |

|

End-Use Advertiser Verticals |

Brand advertisers and performance marketers across gaming, FMCG, financial services, e-commerce, entertainment, and travel sectors. |

Integrated publishers with first-party data assets and proprietary SSP infrastructure achieve superior yield optimization compared to publishers relying entirely on third-party mediation platforms, creating a meaningful competitive advantage in programmatic CPM maximization across Japan's premium app inventory segments.

Technology Landscape in the Japan In-App Advertising Industry

Programmatic Advertising and Real-Time Bidding Infrastructure

Japan's in-app advertising technology stack is dominated by programmatic buying infrastructure, with real-time bidding (RTB) auctions completing in under 100 milliseconds across Japan's 5G-connected publisher inventory. Header bidding implementations in mobile apps are enabling simultaneous demand partner competition, increasing publisher yield by 30-50% versus waterfall mediation models.

Mobile Measurement and Attribution Technology

Mobile measurement partners (MMPs) provide Japan's in-app advertising ecosystem with the event-level attribution data required for campaign optimization, with SKAdNetwork 4.0 integration becoming mandatory for iOS campaign measurement as Apple's privacy framework restricts device-level tracking capabilities across the 43.6% iOS platform segment.

AI and Machine Learning for Audience Targeting

Contextual AI systems, utilizing on-device machine learning models for audience segmentation without transmitting personal data, are gaining regulatory favor in Japan's APPI-compliant advertising environment. Telecom-anchored advertising platforms combining carrier behavioral data with app engagement signals at CDP scale represent a distinctly Japanese targeting approach with high precision.

AR Advertising and Immersive In-App Ad Formats

Japan's consumer technology affinity is driving early adoption of augmented reality (AR) in-app advertising, with filter advertising, AR Lenses, and gaming interstitial AR formats providing brands with highly memorable, shareable advertising experiences achieving 3x higher brand recall metrics versus standard display units.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Advertising Type | Video Ads | 35.2% | 2025 |

| Platform | Android | 52.3% | 2025 |

| Application | Gaming | 42.5% | 2025 |

| Region | Kanto Region | 38.4% | 2025 |

By Platform

Android commands a 52.3% majority share in 2025, reflecting the platform's dominance in Japan's mid-market and entry-level smartphone segment, combined with the comprehensive programmatic in-app advertising marketplace offering advertisers access to billions of auction signals daily and unmatched publisher reach across the country.

To access detailed market analysis, Request Sample

iOS captures 43.6% in 2025, commanding significant advertiser attention due to Apple App Store users demonstrated higher in-app purchase rates and premium demographic profiles. Japanese iOS users exhibit above-average engagement with rewarded ad formats and have historically delivered 40-60% higher eCPMs than Android inventory for premium gaming and financial services advertisers. Others (4.1%) encompasses Windows mobile and web-based PWA advertising inventory types.

By Application

Gaming dominates the application segment at 42.5% in 2025, anchored by Japan's globally prominent mobile gaming market where publishers deploy rewarded video, offer wall, and interstitial formats within deeply engaging freemium game sessions generating the highest user engagement time-in-app metrics of any application category globally.

Entertainment (18.7%) captures significant in-app ad spend driven by streaming video and music application advertising, where video pre-roll and mid-roll advertising commands premium pricing aligned with television-equivalent GRP metrics.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

38.4% |

Tokyo digital media hub; brand HQ concentration; high-density app users |

|

Kinki Region |

18.6% |

Osaka e-commerce growth; gaming publishers; digital retail expansion |

|

Central/Chubu Region |

12.7% |

Nagoya manufacturing brand digital shift; automotive sector app advertising |

|

Kyushu-Okinawa Region |

8.4% |

Regional e-commerce growth; tourism app advertising; university demographics |

|

Tohoku Region |

7.1% |

Post-reconstruction digital infrastructure; rural smartphone adoption growth |

|

Chugoku Region |

5.6% |

Hiroshima industrial digital transformation; regional retail app advertising |

|

Hokkaido Region |

5.0% |

Tourism-driven app advertising; agriculture tech digital; seasonal campaigns |

|

Shikoku Region |

4.2% |

Digital catch-up investment; regional brand mobile campaigns; SMB growth |

The Kanto Region's 38.4% market dominance in 2025 is driven by Tokyo's structural advantages as Japan's advertising, technology, and e-commerce capital. Japan's internet advertising expenditure reached 3,652 billion yen in 2024, with the Kanto Region accounting for most agency media buying, publisher headquarters, and ad tech investment that concentrates programmatic auction liquidity in the market.

The Kinki Region at 18.6% benefits from Osaka's established consumer retail economy and a growing cohort of Kansai-based digital publishers and mobile gaming developers, while the Central/Chubu Region at 12.7% is experiencing digital advertising acceleration driven by automotive industry brands shifting marketing budgets from traditional to mobile-first channels.

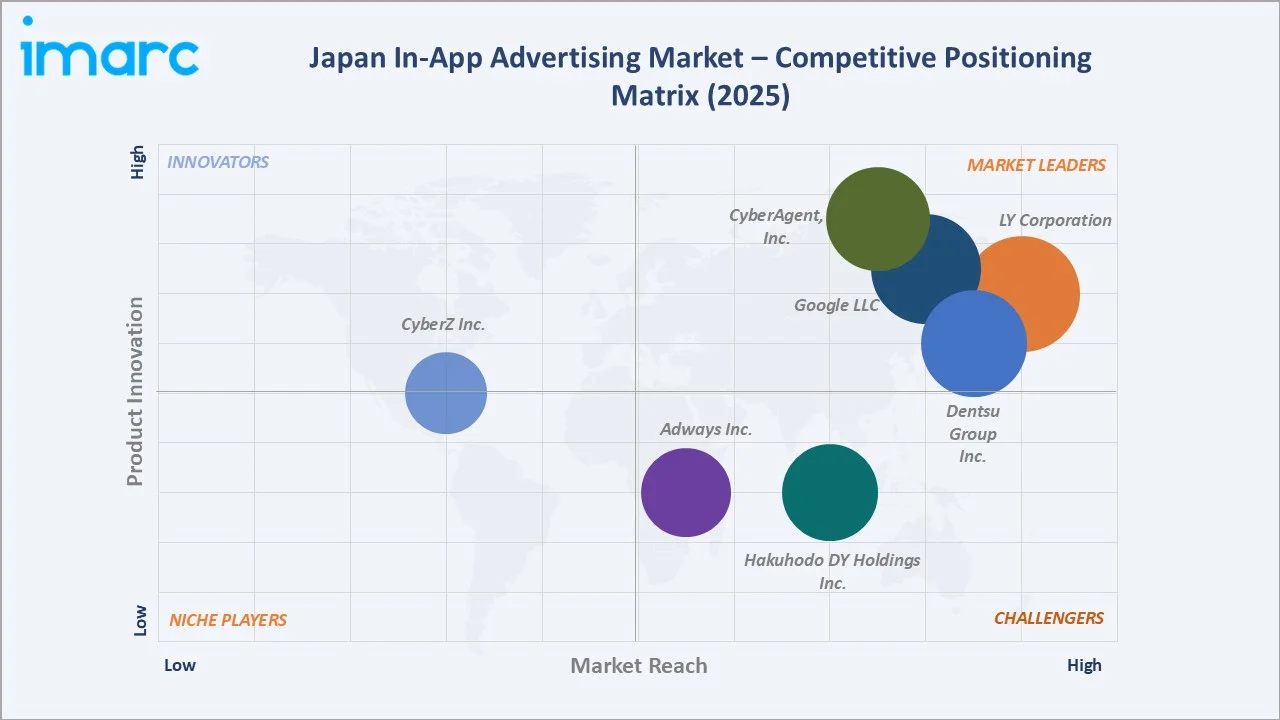

Competitive Landscape

The Japan in-app advertising market is moderately concentrated, with global technology platforms and domestic digital advertising conglomerates occupying leadership positions. Global programmatic networks dominate publisher-side inventory, while domestic players command significant agency-side and publisher-side market positions through proprietary data assets and Japan-specific audience intelligence.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Dentsu Group Inc. |

In-app Advertising Services |

Leader |

Japan's largest ad holding; integrated programmatic & creative; data-driven targeting |

|

CyberAgent, Inc. |

Internet Advertising Services |

Leader |

Largest internet ad agency; AI creative; ABEMA streaming inventory |

|

LY Corporation |

LINE Ads, LINE Promotion, LINE Point AD |

Leader |

Dominant messaging platform; 90M+ users; social commerce ad integration |

|

Google LLC |

AdMob, Google Ads |

Leader |

Largest in-app ad network; Android ecosystem; programmatic exchange leadership |

|

Hakuhodo DY Holdings Inc. |

In-app Advertising Services |

Challenger |

Second largest ad agency; audience intelligence; brand safety focus |

|

Adways Inc. |

Smart-C |

Challenger |

Independent mobile ad network; publisher monetization; performance campaigns |

|

CyberZ Inc. |

In-app Advertising Services |

Emerging |

Performance-based mobile; influencer ad integration; gaming focus |

Key players include Dentsu Group Inc., CyberAgent, Inc., LY Corporation, Google LLC, Hakuhodo DY Holdings Inc., Adways Inc., CyberZ Inc., and others.

Key Company Profiles

Dentsu Group Inc.

Dentsu Group Inc. is Japan's largest advertising holding company and among the world's largest by revenue, with its integrated digital advertising division operating Japan's most comprehensive in-app programmatic buying infrastructure. Dentsu's iX platform integrates first-party data from across its network of digital publishers and client CRM databases to deliver precision in-app targeting at scale.

- Product Portfolio: In-app Advertising Services

- Recent Developments: In February 2025, Dentsu announced 2024 internet advertising expenditure in Japan reached 3,651.7 billion yen, representing 47.6% of total advertising market, with in-app placements representing a growing majority of mobile advertising allocations across client portfolios.

- Strategic Focus: Dentsu's in-app advertising strategy leverages its integrated data and technology platform to offer advertisers closed-loop measurement from impression to purchase across Japan's app ecosystem, differentiating on brand-safe inventory curation and AI-powered creative optimization capabilities.

CyberAgent, Inc.

CyberAgent, Inc. is Japan's largest internet advertising agency and digital media company, operating a major free streaming platform, a leading blogging network, and a programmatic ad network. CyberAgent's AI-first advertising strategy focuses on proprietary generative AI creative tools to maintain competitiveness against global platforms offering self-serve programmatic capabilities.

- Product Portfolio: Internet Advertising Services

- Strategic Focus: CyberAgent's strategy centers on deepening its owned-media in-app advertising inventory through content investment while leveraging AI creative tools to differentiate its agency services against both domestic competitors and global DSP self-serve adoption by large Japanese advertisers.

LY Corporation

LY Corporation operates Japan's dominant mobile messaging platform, providing in-app advertising products across messaging, timeline, and commerce environments. Its closed ecosystem combining messaging, payments, loyalty, e-commerce, and content create uniquely rich first-party behavioral data for in-app targeting at scale.

- Product Portfolio: LINE Ads, LINE Promotion, LINE Point AD

- Recent Developments: In April 2026, The LY Ads platform was launched as a unified advertising solution that brings together previously separate systems into a single interface, allowing advertisers to manage campaigns more efficiently across LINE and Yahoo! JAPAN properties. By centralizing data and ad delivery, the platform enhances operational efficiency and leverages machine learning to optimize performance, enabling more streamlined campaign execution and improved outcomes.

- Strategic Focus: LINE's advertising strategy leverages its unique position as Japan's primary social communication infrastructure to offer advertisers first-party audience segments unavailable elsewhere, combined with direct social commerce conversion paths that enable full-funnel in-app campaign measurement.

Market Concentration Analysis

The Japan in-app advertising market is moderately concentrated at the platform infrastructure level, with the dominant global search and social platforms collectively capturing an estimated 55-65% of programmatic in-app advertising revenue, while the agency and media buying layer is dominated by Japan's top two holding companies with approximately 45-55% combined market share.

The mid-market is served by independent ad networks and international entrants, creating competitive pressure on publisher CPMs and advertiser CPC rates. Japan-specific consolidation is occurring at the agency holding company level, with acquisitions in data analytics and diversification into owned content serving as barriers to entry for regional challengers seeking to disrupt the concentrated top-tier structure.

Investment & Growth Opportunities

Fastest-Growing Segments

Online Shopping application advertising at ~16.1% CAGR through 2034 is the highest-growth segment, driven by Japan's expanding mobile commerce ecosystem where e-commerce platforms and social commerce tools are deepening in-app advertising budgets through performance marketing models with direct purchase attribution and measurable ROAS.

Gaming application advertising at ~15.2% CAGR through 2034 represents the broadest-based growth opportunity, as Japan's mobile gaming publishers adopt increasingly sophisticated monetization formats including mini-games, interactive playables, and AR-enabled ad experiences that command premium CPMs over standard display formats.

Emerging Markets

The Tohoku and Hokkaido regions at estimated 15-17% CAGRs through 2034 represent the fastest-growing regional markets for Japan in-app advertising, driven by digital catch-up investment, improving 5G rural coverage, and the entrance of national e-commerce and retail brands into previously underleveraged regional mobile advertising markets.

Venture & Investment Trends

Private equity and venture capital interest in Japan's ad tech ecosystem is growing, with mobile attribution, contextual AI targeting, and privacy-preserving measurement technology attracting seed to Series B investment. Regulatory-driven demand for consent management platforms and privacy-compliant data solutions is generating compliance technology investment within the in-app advertising supply chain.

Future Market Outlook (2026-2034)

The Japan in-app advertising market is forecast to expand from USD 9.21 Billion in 2025 to USD 30.30 Billion by 2034 at a CAGR of 14.16%, adding USD 21.09 Billion in incremental annual market value over the forecast period. This high-growth trajectory reflects the market's structural alignment with Japan's mobile-first economy, accelerating digital advertising reallocation from linear television, and expanding 5G-enabled rich media inventory across premium applications.

Three technological forces will most significantly shape Japan's in-app advertising industry through 2034. Generative AI creative automation will reduce campaign production costs significantly, enabling mid-market brands to deploy always-on in-app campaigns at scale. The maturation of privacy-preserving computation will restore measurement precision lost to ATT while maintaining APPI compliance. And the emergence of in-app extended reality advertising will create premium inventory tiers commanding the highest CPMs, expanding total addressable revenue substantially.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Japan in-app advertising industry stakeholders including programmatic platform executives, mobile app publisher monetization managers, digital advertising agency heads, brand marketing directors, and ad tech vendor representatives. Primary data validated market sizing, platform and application segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Dentsu Advertising Expenditure in Japan Survey (2024), Ministry of Internal Affairs and Communications Information and Communications White Paper (2024), IAB Japan Mobile Marketing Data Book, Japan Interactive Advertising Bureau digital advertising data, IDC Japan mobile advertising market reports, and trade publications including Nikkei Digital, Campaign Asia-Pacific, and Mobile Marketing Magazine Japan.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating smartphone penetration rates, mobile advertising spend-to-GDP ratios, digital advertising channel mix shift data, and historical market evolution patterns. Scenario analysis was performed across base, optimistic, and conservative cases to account for regulatory and macroeconomic uncertainty.

Japan In-App Advertising Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Advertising Types Covered | Banner Ads, Interstitial Ads, Rich Media Ads, Video Ads, Others |

| Platforms Covered | Android, iOS, Others |

| Applications Covered | Messaging, Entertainment, Gaming, Online Shopping, Payment and Ticketing, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Dentsu Group Inc., CyberAgent, Inc., LY Corporation, Google LLC, Hakuhodo DY Holdings Inc., Adways Inc., CyberZ Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan in-app advertising market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan in-app advertising market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan in-app advertising industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan In-App Advertising Market Report

The Japan in-app advertising market reached USD 9.21 Billion in 2025, reflecting consistent demand from Japan's near-universal smartphone adoption, mobile-first digital consumption culture, and the growing allocation of brand advertising budgets from traditional to mobile in-app channels.

The market is projected to reach USD 30.30 Billion by 2034, growing at a CAGR of 14.16% during 2026-2034, driven by 5G expansion, AI-powered advertising personalization, mobile gaming growth, and Japan's accelerating digital commerce ecosystem generating higher in-app ad spend across all major application categories.

Android leads with a 52.3% platform share in 2025, driven by its broader device penetration across Japan's smartphone market and the comprehensive programmatic in-app advertising network offering advertisers access to the largest volume of in-app auction inventory and publisher relationships.

Gaming dominates at 42.5% in 2025, representing Japan's globally prominent mobile gaming industry where freemium app monetization via rewarded video, interstitial, and offerwall ad formats generates the highest CPMs and advertiser ROI of any application category in the market.

The Kanto Region commands a dominant 38.4% share in 2025, driven by Tokyo's concentration of advertising agencies, brand headquarters, digital publishers, and programmatic technology infrastructure, creating Japan's deepest and most liquid in-app advertising marketplace with the highest CPM rates nationally.

Online Shopping is the fastest-growing application at ~16.1% CAGR through 2034, driven by Japan's mobile commerce expansion, social commerce integration, and performance advertising adoption by e-commerce brands seeking measurable in-app purchase attribution and direct ROAS-based campaign optimization.

Leading companies include Dentsu Group Inc., CyberAgent, Inc., LY Corporation, Google LLC, Hakuhodo DY Holdings Inc., Adways Inc., CyberZ Inc., and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)