Japan Inflight Catering Market Size, Share, Trends and Forecast by Food Type, Flight Service Type, Aircraft Seating Class, and Region, 2026-2034

Japan Inflight Catering Market Size, Share, Trends & Forecast (2026-2034)

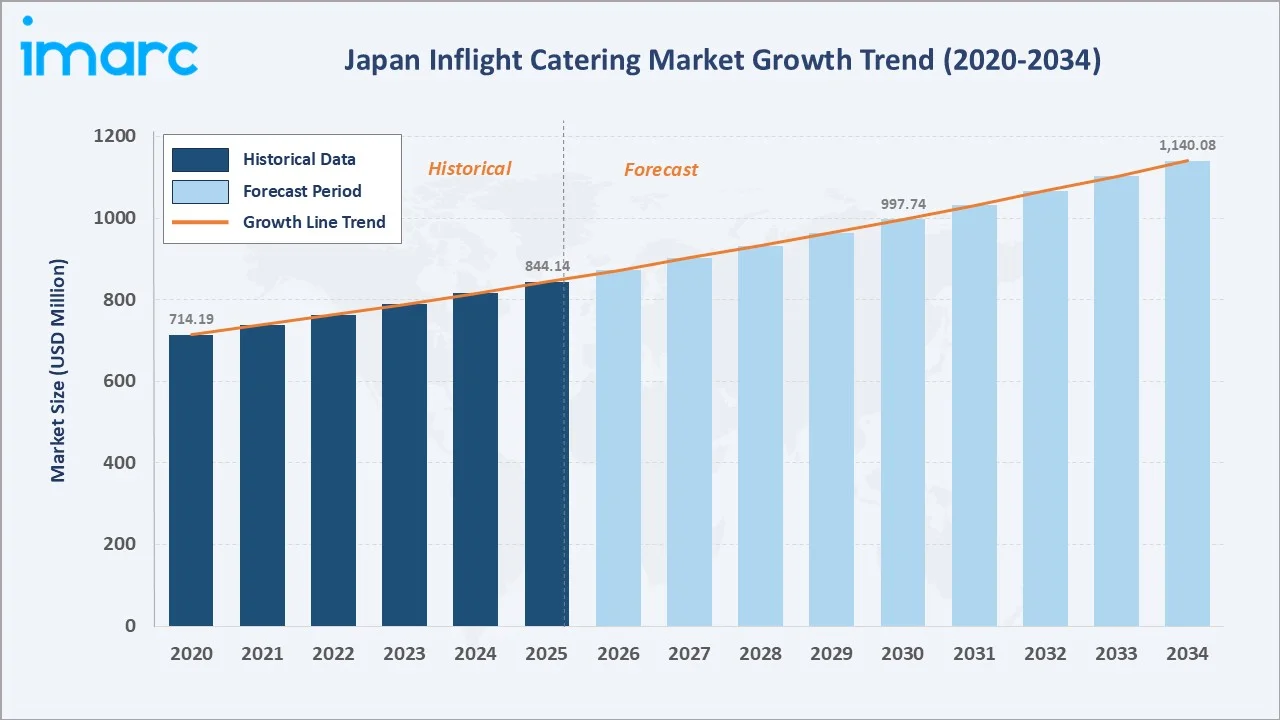

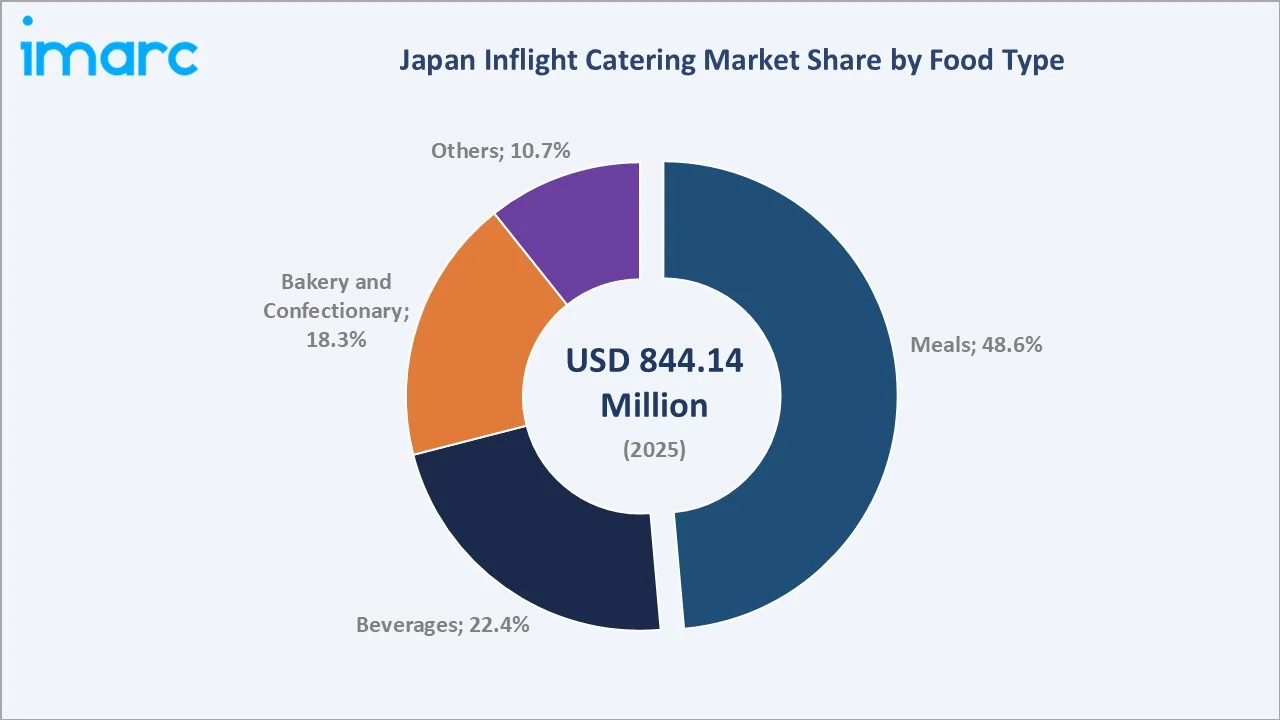

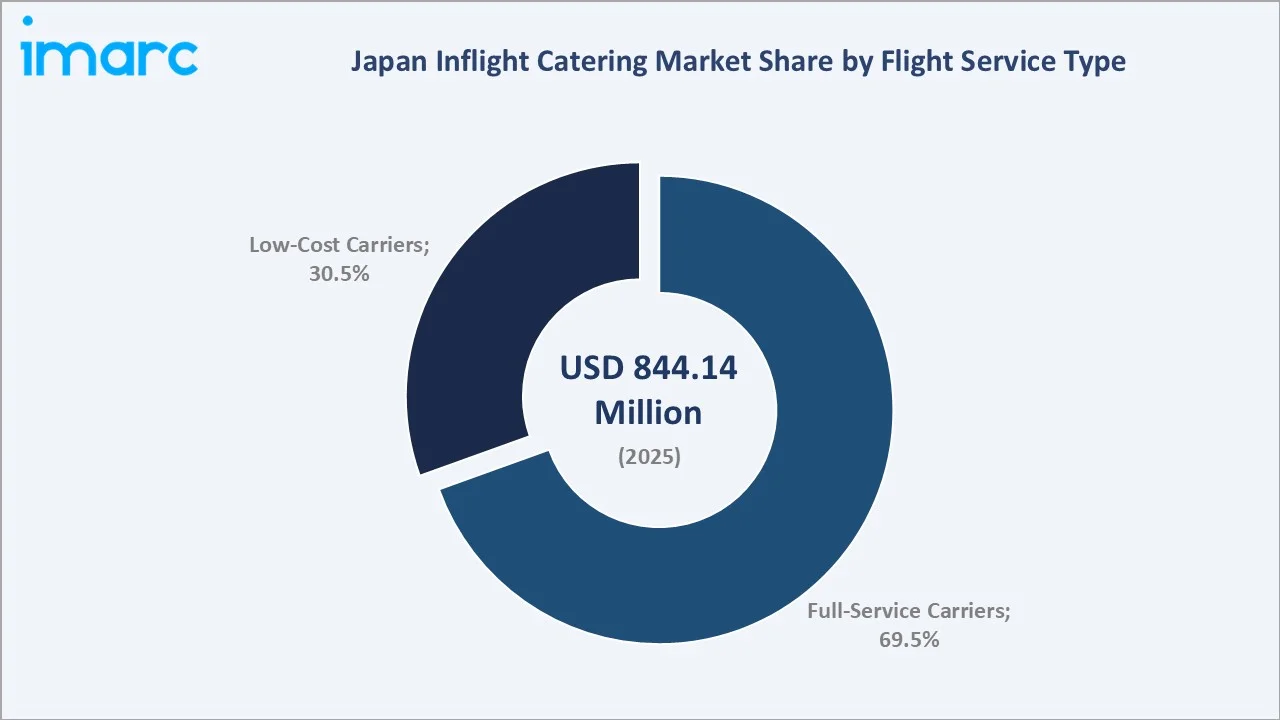

The Japan inflight catering market was valued at USD 844.14 Million in 2025 and is projected to reach USD 1,140.08 Million by 2034, exhibiting a CAGR of 3.40% during 2026-2034. The strong rebound in tourism arrivals, with Japan welcoming a record 36.87 Million international visitors in 2024, alongside the premiumization of onboard dining and rising demand for healthy, regional Japanese cuisine, are the primary drivers shaping market growth.

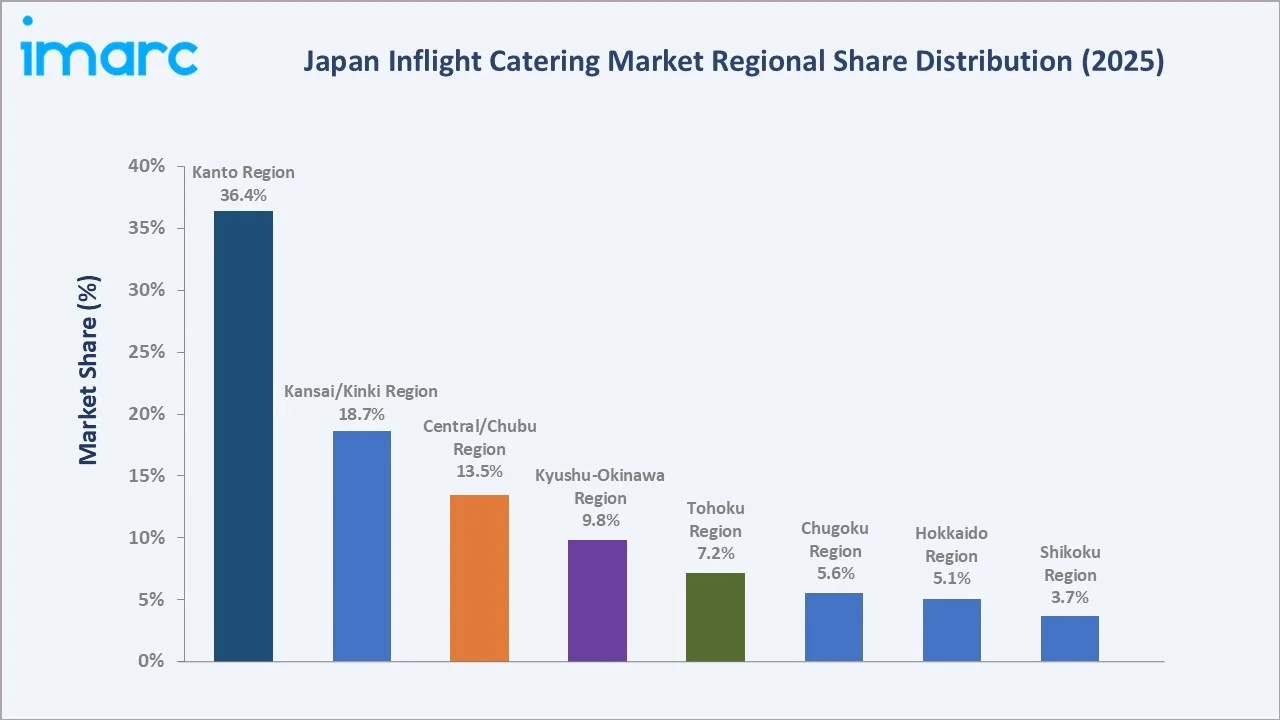

Meals lead the food type segment at 48.6%, full-service carriers dominate the flight service type segment at 69.5%, and Kanto Region commands 36.4% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 844.14 Million |

|

Forecast Market Size (2034) |

USD 1,140.08 Million |

|

CAGR (2026-2034) |

3.40% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (36.4%, 2025) |

|

Fastest Growing Region |

Kansai/Kinki Region (18.7%, 2025) |

|

Leading Food Type |

Meals (48.6%, 2025) |

|

Leading Flight Service Type |

Full-Service Carriers (69.5%, 2025) |

The Japan inflight catering market expanded from USD 714.19 Million in 2020 to USD 844.14 Million in 2025, supported by recovering air travel volumes, rising visitor arrivals to Japan, and renewed investment in premium onboard dining. Anchored at USD 997.74 Million in 2030, the trajectory to USD 1,140.08 Million by 2034 reflects steady demand from full-service carriers and the expanding low-cost carrier segment.

To get more information on this market, Request Sample

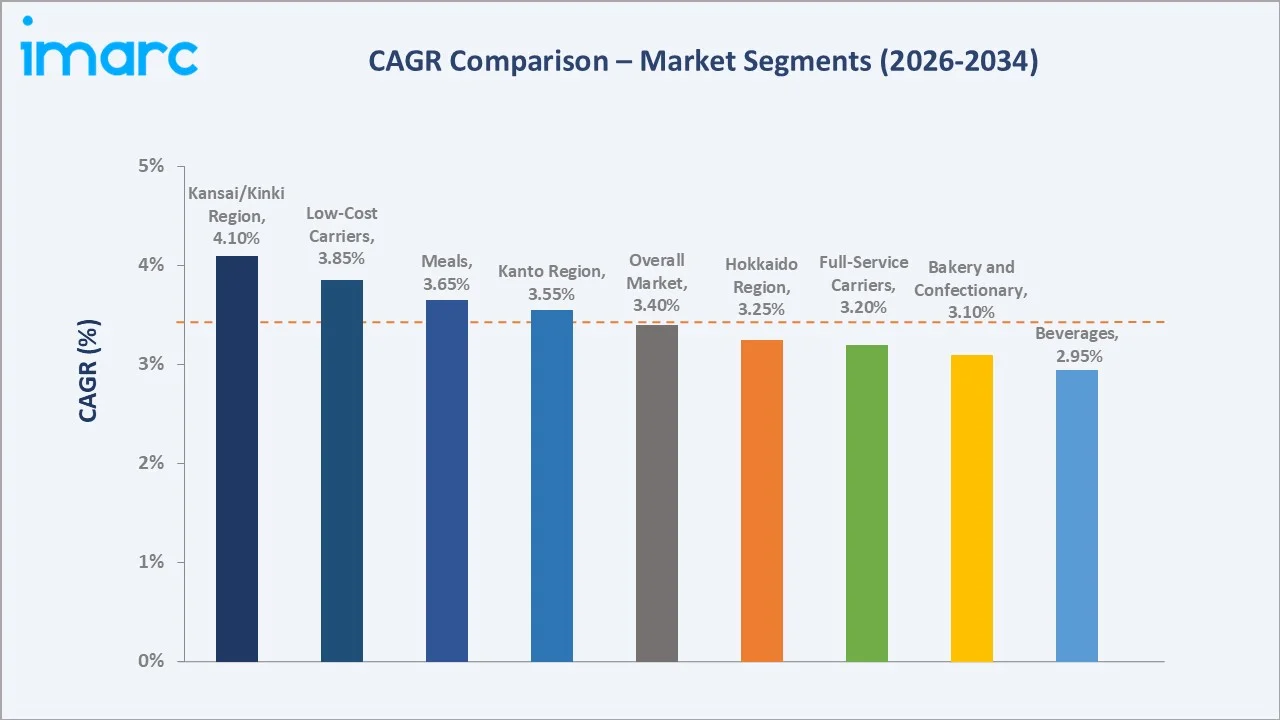

CAGR trajectories across food type and flight service type sub-segments show meals, low-cost carriers, and the Kansai/Kinki Region expanding faster than the overall 3.40% market CAGR, lifted by premiumization of onboard meals and Osaka-Kansai International Airport traffic growth.

Executive Summary

The Japan inflight catering market is on a steady growth path from USD 714.19 Million in 2020 to USD 1,140.08 Million by 2034. Inflight food has shifted from a basic service to a meaningful brand asset, with carriers leveraging Japanese cuisine as a differentiator. Increasing passenger volumes are encouraging airlines to invest in onboard menus. Premium meal experiences and specialty dietary options are further supporting adoption across cabin classes.

Meals dominate the food type segment at 48.6% in 2025, supported by long-haul international routes from Narita, Haneda, and Kansai airports. Full-service carriers lead the flight service type segment at 69.5%, fueled by Japan Airlines investments in chef-curated menus, premium cabin dining, and seasonal regional cuisine. In March 2026, Japan Airlines announced that it is set to upgrade its international inflight meals with menus created by famous chefs and RED U-35 culinary stars beginning spring 2026. First and Business Class dining showcases dishes crafted by Chef Natsuko Shoji and Chef Nae Ogawa. Kanto Region commands 36.4%, led by Tokyo's twin hubs at Haneda and Narita, supported by the highest passenger throughput and concentrated catering infrastructure.

Key Market Insights

|

Insight |

Data |

|

Leading Food Type |

Meals - 48.6% share (2025) |

|

Second Food Type |

Beverages - 22.4% share (2025) |

|

Leading Flight Service Type |

Full-Service Carriers - 69.5% share (2025) |

|

Second Flight Service Type |

Low-Cost Carriers - 30.5% share (2025) |

|

Leading Region |

Kanto Region - 36.4% share (2025) |

|

Fastest Growing Region |

Kansai/Kinki Region - 18.7% share (2025) |

|

Top Companies |

ANA Holdings Inc., SATS Ltd., Sojitz Corporation, gategroup, LSG Group |

Key Analytical Observations Expanding on the Data Above:

- Meals dominance at 48.6% is driven by long-haul international routes operated from Tokyo and Osaka, where multi-course tray meals remain core to the cabin experience. Haneda Airport handled 85.7 Million passengers in fiscal 2024, anchoring high-volume meal preparation demand for catering kitchens.

- Beverages share at 22.4% is sustained by the central role of Japanese tea, coffee, sake, and craft beer offerings in onboard service, alongside growing consumption of premium bottled water, juices, and signature cocktails on full-service carriers.

- Full-service carriers leadership at 69.5% reflects Japan Airlines emphasis on chef-curated meals, regional cuisine partnerships, and premium-class dining experiences that anchor brand differentiation across long-haul international and domestic routes.

- Low-cost carriers at 30.5% is growing through buy-on-board ancillary models, with airlines expanding paid meal options, bento-style snacks, and pre-order menus to capture incremental revenue per passenger.

- Kanto Region at 36.4% dominates owing to the concentration of Haneda and Narita international airports and high density of inbound and outbound long-haul flights from the country.

Japan Inflight Catering Market Overview

Inflight catering refers to the preparation, packaging, and delivery of meals, beverages, and snacks to commercial aircraft. In Japan, the service spans full-course Japanese cuisine, Western menus, special dietary meals, regional bento boxes, and ready-to-eat items prepared at airport-adjacent catering plants under strict food safety standards.

The Japan ecosystem integrates raw ingredient suppliers, central kitchens, packaging vendors, cold-chain logistics partners, ground handling firms, and full-service and low-cost carriers, supported by regulatory oversight from civil aviation authorities and food safety agencies, together enabling consistent meal delivery across several commercial airports.

Market Dynamics

To evaluate market opportunities, Request Sample

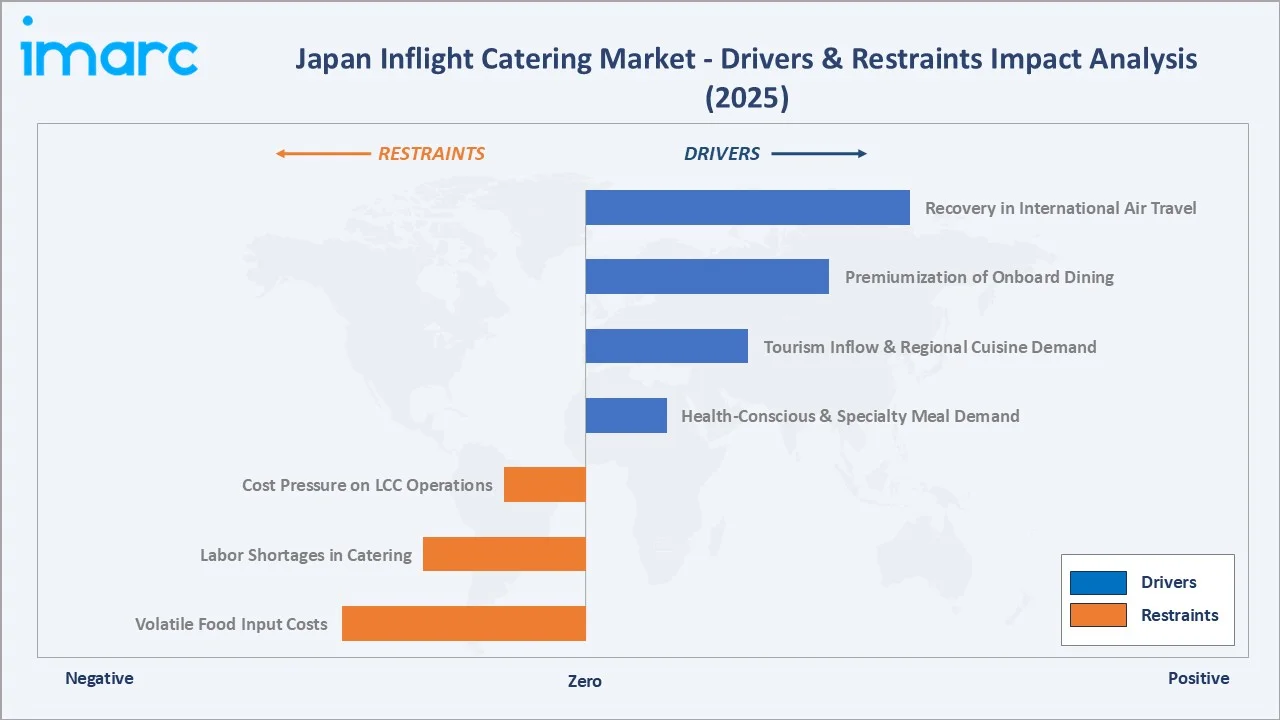

Market Drivers

- Recovery in International Air Travel: Cross-border travel into and from Japan has rebounded sharply, lifting onboard meal volumes for full-service and low-cost carriers. Higher passenger loads and longer average flight durations are further supporting catering demand.

- Premiumization of Onboard Dining: Japan Airlines continue to invest in chef-curated menus, partnerships with Michelin-rated restaurants, and seasonal regional ingredients, lifting per-passenger catering value across business and first-class cabins on long-haul routes.

- Tourism Inflow and Demand for Regional Cuisine: International visitors arriving in Japan are encouraging carriers to feature regional specialties, washoku-style menus, and prefectural ingredients as part of the onboard brand experience, supporting menu diversification and meal sophistication.

- Health-Conscious and Specialty Meal Demand: Rising demand for vegan, vegetarian, gluten-free, halal, and low-sodium options is encouraging caterers to expand specialty meal portfolios, with Japanese carriers steadily widening dietary choices across international routes. In October 2022, All Nippon Airways (ANA) unveiled that it was set to launch new vegan, vegetarian, and gluten-free options on international flights leaving Japan starting November 1. Award-winning chef Hideki Takayama, a member of the airline’s The Connoisseurs program, collaborated with ANA chefs to create the new menus.

Market Restraints

- Cost Pressure on Low-Cost Carriers: Buy-on-board models limit per-passenger catering spend, compressing kitchen margins and constraining menu complexity for budget operators serving short-haul domestic and regional Asian routes from Japan.

- Labor Shortages in Catering Operations: Japan's broader workforce shortage extends to airport catering plants, where shift-based food preparation, packing, and loading jobs face recruitment challenges, raising wage costs and limiting capacity expansion at peak travel periods.

- Volatile Food Input Costs: Imported ingredient prices, foreign exchange swings against the yen, and energy-driven cold-chain costs continue to pressure caterers, affecting menu economics for both full-service and low-cost carriers operating from Japanese hubs.

Market Opportunities

- Expansion of Premium Cabin Offerings: Growing premium-cabin demand on Japan-United States, Japan-Europe, and Japan-Southeast Asia routes is opening room for higher-margin catering services, signature menus, and dedicated premium beverage programs.

- LCC Ancillary Catering Growth: Japan's expanding low-cost carrier segment presents opportunities for paid meal programs, branded bento boxes, and pre-order ancillary menus that lift per-passenger revenue. This trend is supporting higher ancillary income streams for airline catering providers.

Market Challenges

- Strict Food Safety Compliance: Inflight catering in Japan operates under stringent HACCP-aligned food safety standards, requiring continuous quality audits, allergen control, traceability, and temperature management, all of which add operational complexity for caterers.

- Sustainability and Waste Pressures: Cabin waste reduction, single-use plastic phase-out targets, and growing scrutiny of food waste in catering operations are creating compliance pressure for kitchens and packaging suppliers serving Japanese carriers.

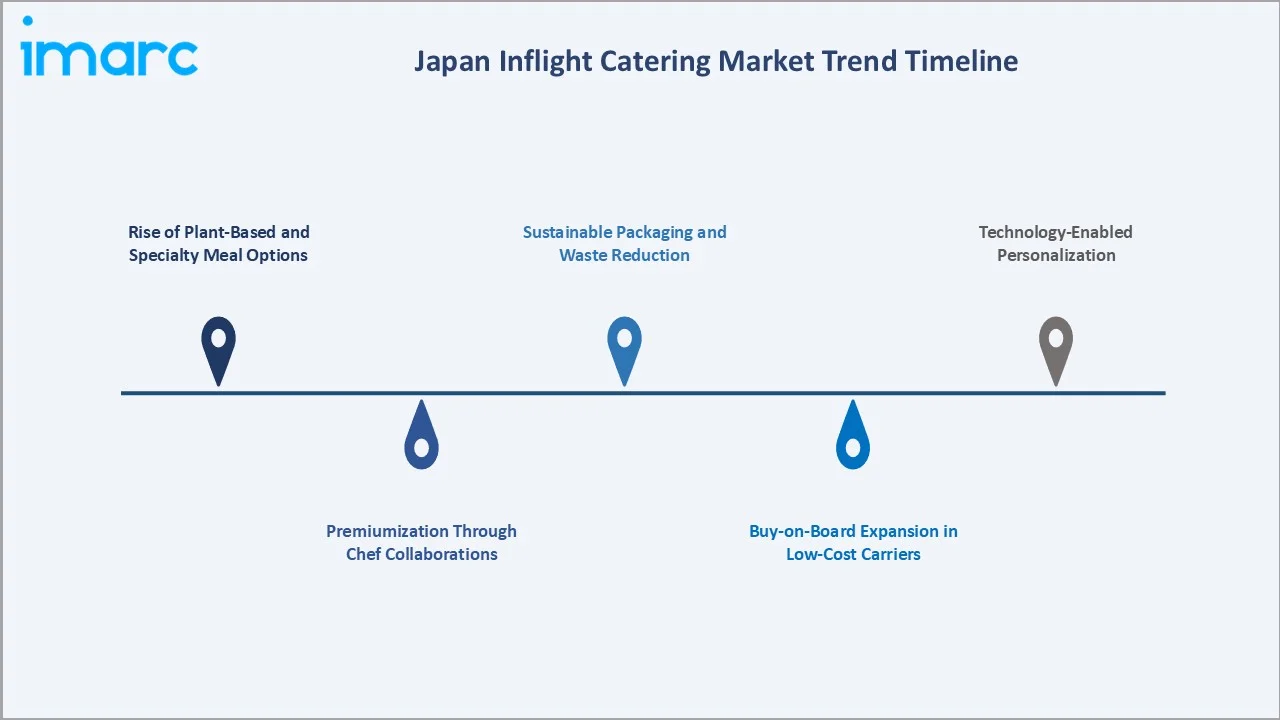

Emerging Market Trends

1. Rise of Plant-Based and Specialty Meal Options

Japanese carriers are steadily expanding plant-based, vegan, and gluten-free meal portfolios across international routes. This shift reflects evolving passenger preferences and growing demand for healthier, inclusive dining options.

2. Premiumization Through Chef Collaborations

Tie-ups with Michelin-starred and celebrity chefs are becoming a standard differentiator for Japanese full-service carriers, with ANA partnering with renowned Japanese chefs and Japan Airlines featuring chef-designed menus across business and first-class cabins on long-haul routes. In February 2024, ANA announced that it was set to refresh its celebrated THE CONNOISSEURS collaboration menu starting in March 2024. The revised menu, in partnership with THE CONNOISSEURSblank, featuring a collective of 12 celebrity chefs, beverage experts from Japan and beyond, alongside ANA's esteemed chefs, presented travelers with a wide array of Japanese, global, and unique dishes.

3. Sustainable Packaging and Waste Reduction

Catering plants serving Japanese carriers are progressively shifting from plastic to fiber-based, biodegradable, and reusable packaging formats. Carriers are also implementing meal pre-order systems to reduce uplift quantities and minimize cabin food waste across short and long-haul flights.

4. Buy-on-Board Expansion in Low-Cost Carriers

Low-cost carriers are expanding paid meal menus featuring local Japanese flavors, bento-style boxes, and branded snacks. Mobile pre-ordering and seat-back ordering platforms are improving uptake and lifting ancillary catering revenue per passenger.

5. Technology-Enabled Personalization

Digital pre-order platforms, in-app meal selection, and dietary preference profiles are giving passengers greater control over onboard meals. These tools also help caterers refine demand forecasting, reduce overproduction, and improve meal-mix accuracy for upcoming flights.

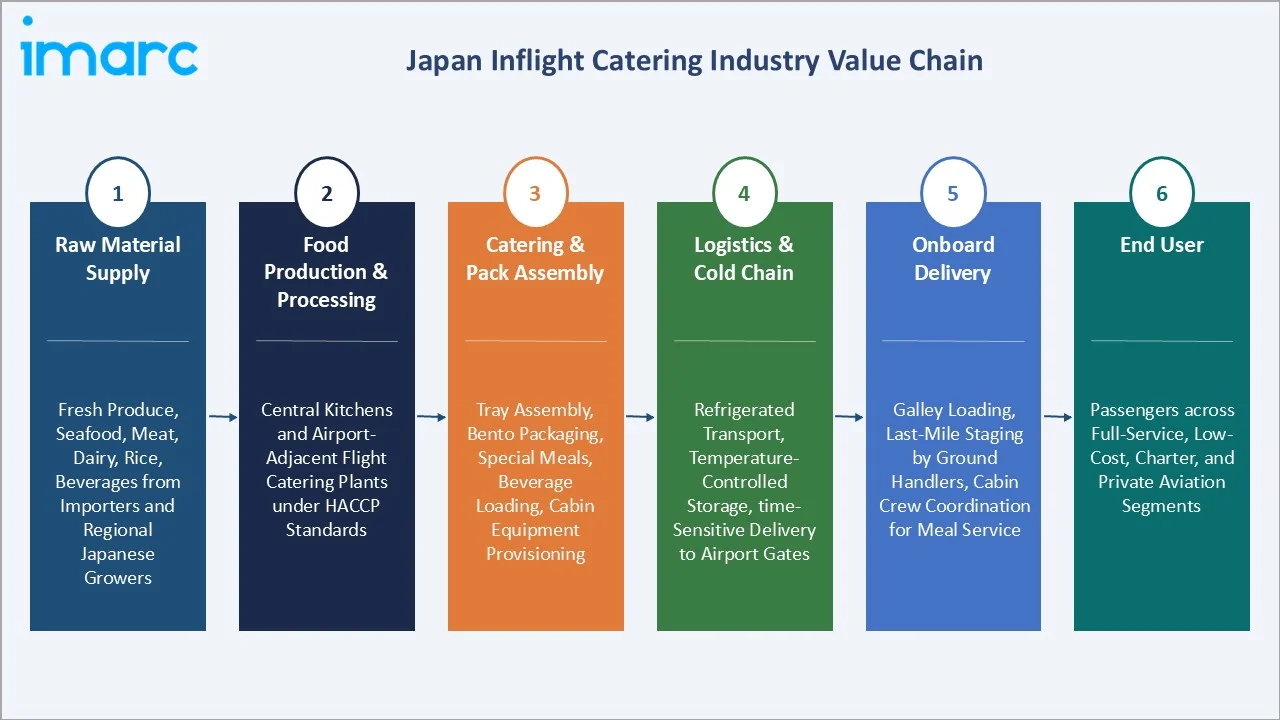

Industry Value Chain Analysis

The Japan inflight catering value chain spans six stages from raw material sourcing through onboard delivery and end user consumption. Central kitchen operations and last-mile cold-chain logistics capture the highest value-add, while airline relationships and quality compliance frameworks generate downstream competitive advantages in this regulated category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of fresh produce, seafood, meat, dairy, rice, and beverages, along with importers and regional Japanese growers supporting kitchen-grade ingredient flows |

|

Food Production & Processing |

Central kitchens and airport-adjacent flight catering plants preparing Japanese, Western, and special dietary menus under HACCP standards |

|

Catering & Pack Assembly |

Tray assembly, bento packaging, special meal preparation, beverage loading, and cabin equipment provisioning by integrated catering operators |

|

Logistics & Cold Chain |

Refrigerated transport, temperature-controlled storage, and time-sensitive delivery from kitchens to airport gates within food safety windows |

|

Onboard Delivery |

Galley loading, last-mile staging by airline ground handlers, and coordination with cabin crew for in-flight meal service execution |

|

End User |

Passengers across full-service, low-cost, charter, and private aviation segments at major Japanese airports |

Vertically integrated airline catering subsidiaries achieve tighter quality control and supply security versus standalone caterers, while multinational catering providers leverage scale and centralized operations to serve multiple airlines across major airport hubs.

Technology Landscape in the Japan Inflight Catering Industry

Cold Chain and Food Safety Technology

Catering plants serving Japanese carriers are deploying advanced refrigeration systems, Internet of Things (IoT)-enabled temperature monitoring, and HACCP-aligned digital traceability tools. These technologies help maintain end-to-end cold chain integrity, reduce contamination risk, and ensure compliance with stringent food safety regulations across high-volume meal production.

Automation and Robotics in Kitchens

Robotic tray assembly, automated portioning lines, and conveyor-based packing systems are gradually being adopted by major Japanese catering operators. Automation helps offset labor shortages, lift production throughput, and improve consistency in meal presentation, especially during peak international travel periods.

Digital Pre-Order and Personalization Platforms

Airline mobile apps and websites allow passengers to pre-select meals, indicate dietary needs, and even reserve premium menu items in advance. This data flow gives caterers improved visibility into per-flight demand, supporting better mix planning, reduced waste, and higher passenger satisfaction.

Sustainable Packaging Innovation

Caterers are progressively replacing single-use plastic with bagasse, paper-based, and bio-resin packaging formats. Reusable meal trays, washable cutlery, and lighter packaging are also being trialed to reduce cabin waste and lower onboard fuel burn through weight optimization.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Food Type | Meals | 48.6% | 2025 |

| Flight Service Type | Full-Service Carriers | 69.5% | 2025 |

| Aircraft Seating Class | 🔒 | 🔒 | 2025 |

| Region | Kanto Region | 36.4% | 2025 |

By Food Type

Meals command a 48.6% majority share in 2025, supported by long-haul international flights from Tokyo and Osaka where multi-course tray service remains the standard. Hot meals, washoku-inspired menus, and Western entrees together anchor the cabin dining experience across full-service carriers.

To access detailed market analysis, Request Sample

Beverages at 22.4% in 2025 cover Japanese tea, coffee, juices, mineral water, sake, beer, and premium-cabin wine and spirit selections. The category benefits from cultural emphasis on tea service and signature in-flight cocktail programs offered by full-service carriers on long-haul routes.

By Flight Service Type

Full-service carriers dominate with 69.5% share in 2025, reflecting the central role of inflight dining as a brand differentiator for ANA and Japan Airlines. Premium-cabin meal programs, chef collaborations, and complimentary beverage service across all classes drive the category's leadership.

Low-cost carriers at 30.5% in 2025 are expanding rapidly through buy-on-board ancillary catering, branded bento offerings, and seat-back ordering platforms. Low-cost carriers have widened paid menu options, lifting per-passenger ancillary catering revenue across short-haul and medium-haul routes.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

36.4% |

High passenger throughput, concentration of major international hubs, dense catering infrastructure, and strong full-service carrier presence |

|

Kansai/Kinki Region |

18.7% |

Rising inbound tourism, expanding low-cost carrier routes, growing regional cuisine integration, and rising long-haul international connectivity |

|

Central/Chubu Region |

13.5% |

Strong manufacturing-linked corporate travel, growing leisure traffic, and steady regional connectivity to Asian destinations |

|

Kyushu-Okinawa Region |

9.8% |

Expanding tourism arrivals, growing intra-Asia routes, and increasing demand for regional Japanese cuisine |

|

Tohoku Region |

7.2% |

High domestic travel demand, regional tourism initiatives, and growing onboard meal volumes from regional airports |

|

Chugoku Region |

5.6% |

Steady domestic connectivity, regional tourism flows, and stable full-service carrier presence on legacy routes |

|

Hokkaido Region |

5.1% |

Seasonal tourism inflow, expanding international charter routes, and rising demand for regional ingredients in onboard menus |

|

Shikoku Region |

3.7% |

Smaller passenger base, niche regional connectivity, and modest catering infrastructure supporting domestic operations |

Kanto Region at 36.4% in 2025 leads the Japan inflight catering market, anchored by Tokyo Haneda and Narita International Airports, the country's leading passenger gateways. Mature catering plants, dense full-service carrier operations, and high concentration of long-haul international departures together support sustained meal volumes.

Kansai/Kinki Region at 18.7% is the highest-growth region through 2034. Strong inbound tourism into Osaka and Kyoto, expanding low-cost carrier routes from Kansai International Airport, and rising long-haul connectivity are accelerating regional catering volumes and menu diversification.

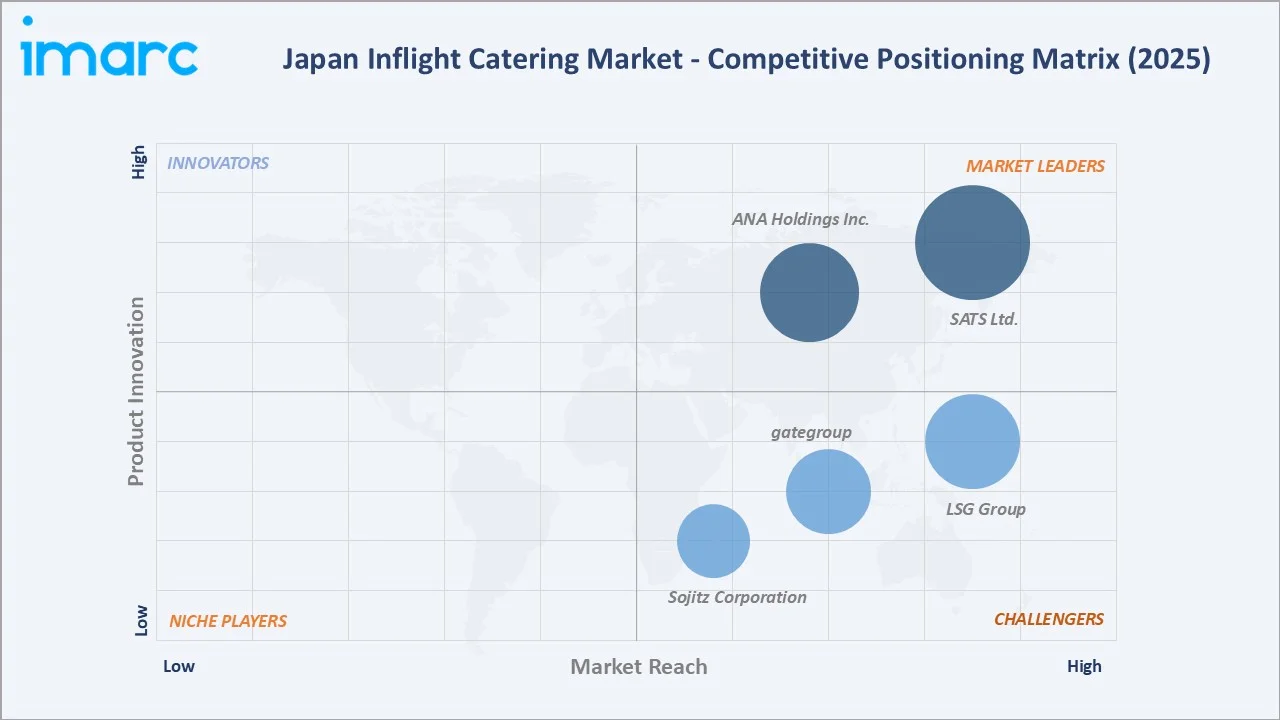

Competitive Landscape

The Japan inflight catering market is moderately consolidated, with airline-owned catering subsidiaries dominating high-volume domestic and full-service carrier flows, while global caterers serve foreign airlines transiting through Tokyo and Osaka. Strong airport-adjacent kitchen footprints and multi-decade airline relationships form the key competitive moats.

| Company Name | Brand / Key Service | Position | Strategic Focus |

| ANA Holdings Inc. | THE CONNOISSEURS | Leader | Vertically integrated airline catering operations; chef collaborations; emphasis on premium cabin differentiation across long-haul international routes |

| SATS Ltd. | SATS TFK | Leader | Multi-airline catering portfolio across major hubs; HACCP-aligned food safety; broad halal and special meal capabilities; global parent-network synergies |

| Sojitz Corporation | Sojitz Royal In-flight Catering Co., Ltd. | Challenger | Regional catering operations anchored at Kansai International, Fukuoka, and Naha airports; positioned for inbound tourism growth in western Japan |

| gategroup | gategourmet | Challenger | Global catering operations serving foreign carriers; broad menu library; route-flexible operations; cost optimization across multi-country networks |

| LSG Group | LSG Sky Chefs | Challenger | Global network catering for foreign and domestic carriers; menu innovation; food safety scale; investment in kitchen automation and digital workflows |

Key players include ANA Holdings Inc., SATS Ltd., Sojitz Corporation, gategroup, and LSG Group, among others.

Key Company Profiles

ANA Holdings Inc.

ANA Holdings Inc., through its wholly owned catering subsidiary ANA Catering Service Co., Ltd. (ANAC), prepares meals for All Nippon Airways across international and domestic routes. Operations center on production facilities serving Tokyo Haneda and Narita International Airports, supporting one of Asia's largest full-service carrier fleets.

- Service Portfolio: Multi-course international meals across First, Business, Premium Economy, and Economy classes; domestic meal services; specialty meals including vegan, halal, and allergen-free options; signature beverage programs.

- Recent Developments: The firm has continued to expand its chef-curated menus on international routes, partnering with renowned Japanese chefs and Michelin-rated restaurants to refresh seasonal menus across premium cabins.

- Strategic Focus: Emphasis on premium-cabin differentiation; ongoing investment in seasonal Japanese cuisine, special meals, and chef partnerships.

SATS Ltd.

SATS Ltd., the Singapore-listed aviation services group, owns TFK Corporation, a leading Japanese inflight catering company headquartered near Narita International Airport, acquired by SATS Ltd. in 2010. The combined SATS TFK operation leverages global scale to serve several airlines from Narita and Haneda, including Japanese and foreign carriers.

- Service Portfolio: Inflight meal preparation, special meal services, halal-certified items, beverage loading, and onboard equipment supply; complementary commercial food services for retail and MICE segments.

- Recent Developments: The firm has continued to strengthen its airline catering presence in Japan, enhancing quality control and supply reliability while leveraging centralized kitchens and efficient logistics to serve multiple airlines across major airport hubs.

- Strategic Focus: Multi-airline portfolio across Narita and Haneda; rigorous HACCP-aligned food safety; strong halal capability; SATS Ltd.-network synergies in procurement and operations.

Sojitz Corporation

Sojitz Corporation holds a 60% controlling stake in Sojitz Royal In-flight Catering Co., Ltd. (SRIC), a consolidated subsidiary engaged in inflight meal preparation. The company operates production facilities at Kansai International, Fukuoka, and Naha airports, anchoring regional catering capacity in western Japan.

- Service Portfolio: Inflight meal preparation and loading across multiple cabin classes, food sales, and bonded warehouse operations at Kansai International, Fukuoka, and Naha airports for both foreign and domestic carriers.

- Recent Developments: SRIC continues to leverage Sojitz Corporation's broader aviation services network and trading-house procurement capabilities to expand customer relationships across foreign and domestic carriers operating from western Japan hubs.

- Strategic Focus: Regional catering operations across Kansai, Fukuoka, and Naha airports; positioning for inbound tourism growth in western Japan.

Market Concentration Analysis

The Japan inflight catering market is moderately concentrated, with top airline-affiliated and global players (ANA Holdings Inc., SATS Ltd., Sojitz Corporation, gategroup, and LSG Group) estimated to hold approximately 60-70% of the country's inflight catering revenue in 2025.

Barriers to entry include airport-adjacent kitchen real estate, HACCP-aligned food safety certifications, established airline contracts, and the capital cost of high-volume catering plants, favoring well-capitalized incumbents with deep airline relationships and scale operations.

Consolidation trends include cross-border investment by global caterers, partnerships between Japanese carriers and regional restaurant brands, and selective expansion of catering-adjacent services, such as airport lounge catering and retail food production. Scale advantages in procurement, automation, and food safety further reinforce the position of established players.

Investment & Growth Opportunities

Fastest-Growing Segments

Low-cost carriers expand faster than the overall 3.40% market CAGR through 2034, driven by buy-on-board ancillary catering, branded bento programs, and pre-order meal platforms. Meals also expand above the market average, supported by long-haul international route growth from Tokyo and Osaka.

Emerging Opportunities

Kansai/Kinki Region presents the highest-growth opportunity through 2034 as Osaka-Kansai International Airport handles rising inbound tourism and LCC traffic. Premium cabin catering on Japan-Europe and Japan-United States routes also offers scope for higher-margin chef-curated menus.

Investment Trends

Investment is flowing into kitchen automation, sustainable packaging conversion, cold-chain digitization, and pre-order technology platforms. Catering companies are also expanding into adjacent segments such as airport lounge food and retail meal kits to diversify revenue beyond pure inflight operations.

Future Market Outlook (2026-2034)

The Japan inflight catering market is forecast to expand from USD 844.14 Million in 2025 to USD 1,140.08 Million by 2034 at a CAGR of 3.40%, adding roughly USD 296 Million in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: continued recovery and growth in international tourism arrivals; premiumization of onboard dining across full-service carrier cabins; rapid LCC ancillary catering expansion; and progressive substitution of single-use plastic with sustainable packaging across kitchens.

By 2034, inflight catering in Japan will be more digital, more personalized, and more sustainable, with mobile pre-ordering, automation in kitchens, and waste reduction targets becoming standard practice across major caterers and carriers operating from Japanese airports.

Research Methodology

Primary Research

Primary research included interviews with senior product managers at Japanese inflight catering companies, airline catering executives, kitchen operations leaders, food safety auditors, and supply chain heads, validating market sizing, regional demand, food type splits, and flight service type evolution.

Secondary Research

Secondary sources included Japan Tourism Statistics, Ministry of Land, Infrastructure, Transport and Tourism (MLIT) reports, International Air Transport Association data, airline annual reports, catering company filings, regional airport authority publications, and industry press releases from listed operators.

Forecasting Models

Market forecasts used top-down and bottom-up models combining airline passenger volumes, average meal value per passenger, route mix evolution, and regional airport throughput. Scenario analysis addressed tourism arrival sensitivities, fuel cost variation, and currency impacts on imported food inputs.

Japan Inflight Catering Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Food Types Covered | Meals, Bakery and Confectionary, Beverages, Others |

| Flight Service Types Covered | Full-Service Carriers, Low-Cost Carriers |

| Aircraft Seating Classes Covered | Economy Class, Business Class, First Class |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | ANA Holdings Inc., SATS Ltd., Sojitz Corporation, gategroup, LSG Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan inflight catering market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan inflight catering market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan inflight catering industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Inflight Catering Market Report

The Japan inflight catering market was valued at USD 844.14 Million in 2025, supported by surging international travel activities, rising visitor arrivals, and renewed investment in premium onboard dining.

The Japan inflight catering market is projected to grow at a 3.40% CAGR from 2026 to 2034, reaching USD 1,140.08 Million, supported by tourism inflow and LCC catering expansion.

Meals lead at 48.6% in 2025, supported by long-haul international flights. Beverages at 22.4% and bakery and confectionary at 18.3% follow as the next-largest categories.

Full-service carriers dominate at 69.5% in 2025, anchored by ANA and Japan Airlines premium cabin programs. Low-cost carriers at 30.5% are growing through buy-on-board ancillary catering.

Kanto Region commands 36.4% in 2025, led by Tokyo's Haneda and Narita airports. Kansai/Kinki Region at 18.7% is among the fastest-growing through 2034.

Leading players include ANA Holdings Inc., SATS Ltd., Sojitz Corporation, gategroup, and LSG Group operating across Japanese airports.

Premiumization is driven by chef collaborations with Michelin-starred and renowned Japanese chefs, regional ingredient sourcing, and seasonal menu refreshes across full-service carrier cabins.

Low-cost carriers are expanding paid menus, branded bento boxes, and pre-order platforms, lifting per-passenger ancillary catering revenue.

Catering operators are shifting from single-use plastic to fiber-based packaging, deploying meal pre-order platforms, and using BioRun-style wastewater treatment to reduce environmental impact.

Robotics in tray assembly, IoT-enabled cold chain monitoring, mobile pre-order platforms, and digital traceability are improving production throughput, food safety, and menu personalization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)