Japan Luxury Hotel Market Size, Share, Trends and Forecast by Type, Room Type, Category, and Region 2026-2034

Japan Luxury Hotel Market Size & Forecast 2026-2034

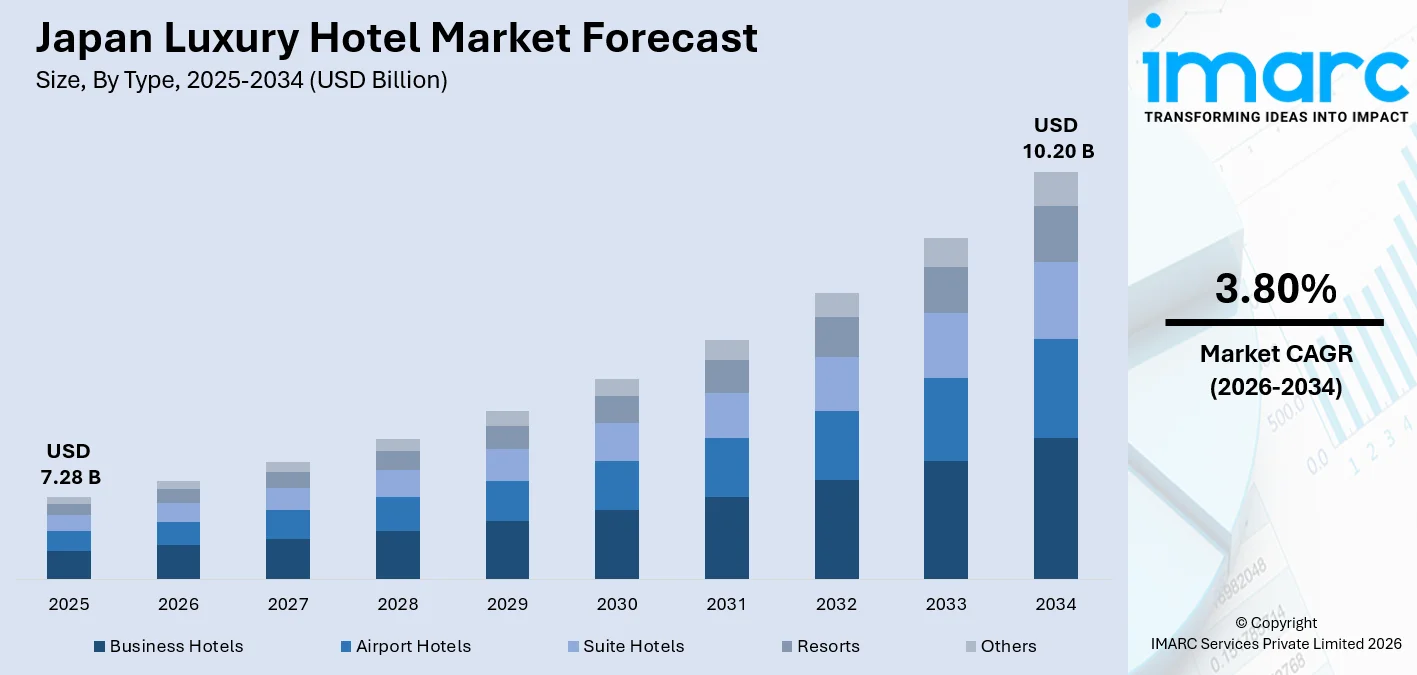

The Japan luxury hotel market size, valued at USD 7.28 Billion in 2025, is projected to reach USD 10.20 Billion by 2034, growing at a CAGR of 3.80% from 2026-2034, supported by record-breaking inbound tourism that saw 42.7 million international visitors arrive in Japan 2025, more than 15.8% increase than 2024 (36.9 million), according to Japan National Tourism Organization, alongside rising per-trip accommodation expenditure, a sustained yen-driven price advantage for international travellers, and an accelerating wave of global luxury brand entries into Japan's undersupplied premium room market. Foreign tourists' spending on accommodation now holds the largest share of inbound travel expenditure, fuelling Japan luxury hotel market share.

To get more information on this market Request Sample

Japan Luxury Hotel Industry Analysis - Key Insights

- Business hotels hold 42.0% of the market by type in 2025- the largest single type, reflecting Tokyo and Osaka's combined weight as Asia's premier business travel corridors. Corporate travel, MICE events, and government delegations anchor high average daily rates at luxury business properties year-round, independent of seasonal leisure fluctuations.

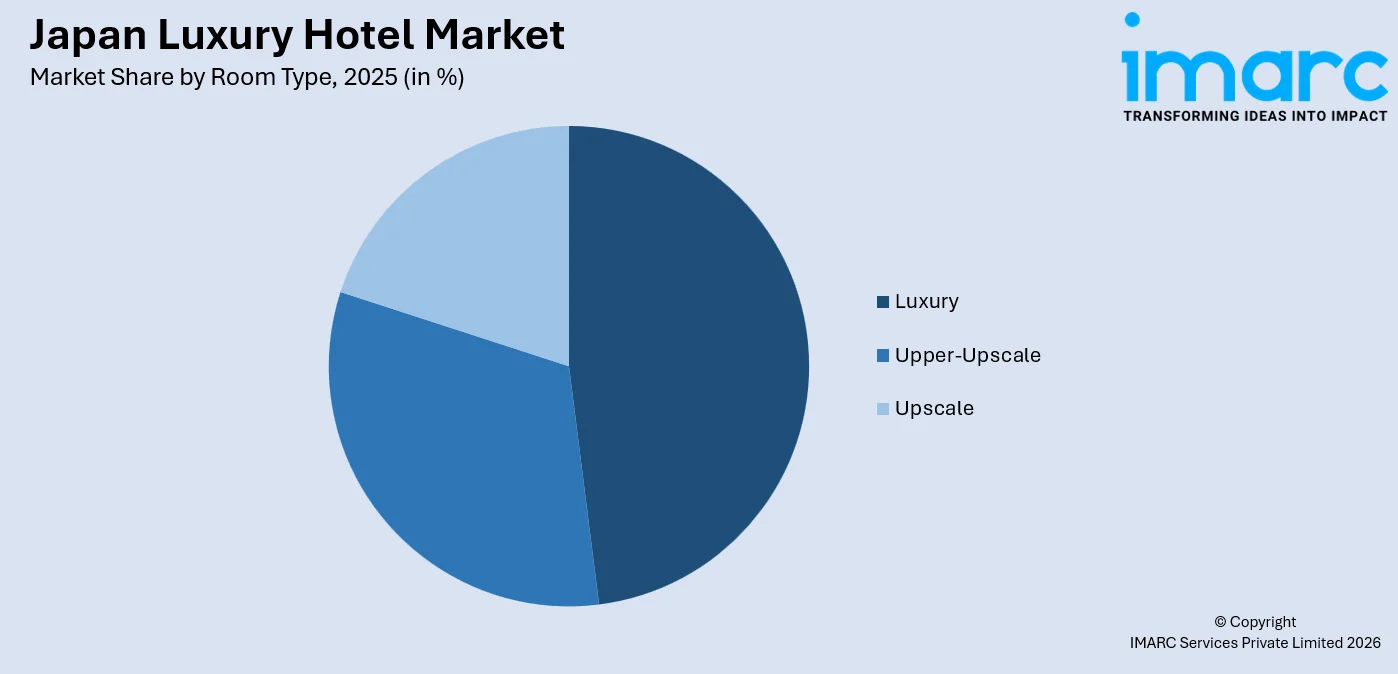

- Luxury commands 48.0% of market share by room type in 2025- nearly half the market concentrated in true luxury tier, driven by affluent inbound travellers from Europe, North America, and Australia who prioritise premium room quality and personalised service over price sensitivity.

- Chain dominates with 65.0% market share by category in 2025- international chain operators lead because their global loyalty programs, standardised service assurance, and brand recognition directly influence booking decisions for high-spending inbound travellers. At the same time, independent properties cater to niche seekers of cultural immersion.

- Kanto Region leads regionally at 52.0% in 2025- Tokyo's unrivalled concentration of premium properties, business travel demand, and gateway airport infrastructure creates a commanding lead.

Japan Luxury Hotel Market Trends and Dynamics 2026

Market Trends

Record inbound tourism is driving a structural demand shift toward luxury accommodation spending

Japan's inbound tourism reached an unprecedented scale, according to the Japan National Tourism Organization (JNTO) and the Japan Tourism Agency, the cumulative arrivals of foreign visitors from January to November 2025 reached 39,065,600, surpassing the previous all-time annual record set in 2024 (36.87 million). Critically, the spending composition has fundamentally shifted: accommodation now holds the largest share of inbound expenditure, representing a structural pivot from "bakugai" bulk purchasing toward "koto consumption" experiences, culture, and premium lodging. This shift directly elevates luxury hotel revenue per guest.

Global luxury hotel brands are accelerating Japan entry and property expansion programs

The combination of record inbound demand and Japan's acknowledged shortage of luxury-tier rooms is catalysing a wave of international luxury brand entries that is reshaping Japan luxury hotel market trends. Accor accelerated its Japan presence with an agreement to operate 23 properties and over 6,000 rooms. In March 2026, the Imperial Hotel Kyoto opened in Kyoto's historic Gion district, further diversifying the luxury supply into Japan's cultural heritage heartland.

Luxury resort development beyond gateway cities unlocking premium spending in regional destinations

Wealthy inbound travellers are moving beyond Tokyo, Osaka, and Kyoto to seek resort experiences in Okinawa, Hakone, and Hokkaido, driving investment in regional luxury properties. Four Seasons is planning the Four Seasons Resort and Private Residences Okinawa, a USD 400 million development comprising 120 hotel rooms, 120 residences, and 40 villas on a 12-hectare area, slated to open in 2027 with an estimated gross development value exceeding USD 1 billion.

- AI-Powered Personalisation and Smart Room Technology: Luxury hotels are integrating AI-driven concierge services, mobile check-in platforms, and smart room systems to deliver hyper-personalised guest experiences that sustain premium rate positioning against a backdrop of rising traveller expectations.

- Wellness Tourism Integration in Luxury Properties: Luxury hotel operators are embedding onsen, meditation retreats, and holistic spa programs as core offerings, capitalising on the surge in wellness-motivated travel.

- Yen Depreciation Sustaining Affordability Premium: Japan's historically weak yen continues to make luxury hotel stays significantly more affordable for inbound travellers from North America, Europe, and Australia relative to comparable destinations, directly supporting occupancy and rate growth across the premium segment.

- Cultural Immersion as a Luxury Differentiator: Luxury operators are integrating authentic Japanese cultural programming, tea ceremony, ikebana, Noh theatre access, and kimono dressing into guest itineraries, distinguishing Japanese luxury hospitality from standardised international offerings and justifying premium pricing.

Growth Drivers

Structural shortage of luxury-tier room supply is amplifying the rate and occupancy performance

Despite adding rooms since the pandemic, reaching 942,000 rooms at the end of 2024, Japan's luxury hotel room supply remains critically insufficient relative to surging premium demand, creating a structural supply-demand imbalance that directly powers Japan luxury hotel market growth.

Rising affluent traveller spending on accommodation over goods is driving luxury hotel revenue

The fundamental shift in inbound tourist spending patterns from goods-based "bakugai" shopping to experience-based "koto consumption" is structurally elevating luxury hotel revenue. Foreign tourists spent over 4.8 trillion yen ($32.23 billion) in the first half of 2025, a 22.9% increase year-on-year per Japan National Tourism Organization, with accommodation now the top spending category.

Government tourism policy and infrastructure investment are sustaining the long-term demand pipeline

Japan's government is actively driving luxury hotel demand through infrastructure investment, relaxed visa policies, and the JNTO's regional promotion campaigns. Japan Tourism Agency data projects over 40 million inbound visitors in the full-year 2025, but reached a record 42.7 million people, exceeding 40 million for the first time, creating a sustained demand.

- MICE and Business Travel Resilience: Japan's standing as a premier MICE destination sustains luxury business hotel demand through international conventions, diplomatic events, and corporate travel programs, providing a stable, high-rate revenue base that offsets leisure seasonality across Tokyo and Osaka properties.

- Domestic Luxury Leisure Expansion: Affluent Japanese travellers are increasingly choosing luxury domestic hotels for leisure stays, anniversaries, and special occasions, diversifying revenue sources beyond inbound demand and providing counter-cyclical demand stability during periods of international travel disruption.

- Loyalty Program-Driven International Bookings: International chain operators leverage Marriott Bonvoy, Accor ALL, and World of Hyatt loyalty ecosystems to capture repeat luxury bookings from high-value global travellers, generating stable direct booking volumes that reduce commission exposure to OTAs.

Market Restraints

Acute hospitality sector labour shortage constraining service delivery capacity: Japan's deep structural shortage of hospitality professionals, compounded by demographic decline and an aging workforce, limits the ability of luxury hotel operators to maintain the high staffing ratios that define premium guest experiences. The language barrier and cultural norms deterring foreign hospitality talent exacerbate the challenge, restricting the pace of luxury hotel expansion and reducing the scalability of personalised service standards across new properties.

Pronounced seasonality creating revenue volatility across the luxury hotel calendar: Japan's luxury hotel market is structurally exposed to seasonal demand peaks and troughs, driven by cherry blossom, autumn foliage, Golden Week, and winter resort seasons, creating periods of near-full occupancy at elevated rates alternating with materially softer off-peak periods. Managing this volatility without compromising brand positioning or rate integrity presents an ongoing operational challenge for luxury hotel operators across all regions.

Soaring construction costs and land prices impeding new luxury property development: Despite strong demand fundamentals, the combination of escalating construction costs, record land prices in prime tourist destinations, and a shortage of experienced luxury hospitality construction contractors is slowing new luxury hotel supply additions. These cost pressures extend project timelines, inflate development budgets beyond feasibility thresholds, and concentrate new supply in fewer high-confidence locations, limiting the geographic diversification of Japan's luxury hotel market.

Japan Luxury Hotel Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Type |

Business Hotels |

42.0% |

2025 |

|

Room Type |

Luxury |

48.0% |

2025 |

|

Category |

Chain |

65.0% |

2025 |

|

Region |

Kanto Region |

52.0% |

2025 |

Type Insights

Business Hotels - 42.0% Market Share (2025) | Leading Type

Business hotels hold the largest type share in Japan's luxury hotel market because Tokyo and Osaka collectively anchor two of Asia's most active MICE and corporate travel corridors. High average daily rates, sustained by year-round corporate demand, diplomatic events, and international conference traffic, make luxury business hotels the highest-revenue category independent of leisure seasonality. In November 2024, Marriott International unveiled its 100th Japanese hotel with Four Points Flex by Sheraton Osaka Umeda, and had 12 additional openings in early 2025, demonstrating the scale of chain investment in Japan's luxury business hotel segment.

|

Segment Breakdown Business Hotels (42.0%) · Airport Hotels · Suite Hotels · Resorts · Others |

Room Type Insights

Access the comprehensive market breakdown Request Sample

Luxury - 48.0% Market Share (2025) | Leading Room Type

The luxury room type commands nearly half the market, reflecting the profile of Japan's dominant inbound traveller segment, affluent visitors from Europe, North America, and Australia who prioritise suite-quality accommodations and bespoke service over price sensitivity. Tokyo's RevPAR climbed 28% year-on-year in 2024, and the average RevPAR growth for Japan in 2025 year-to-date reached approximately 18%, confirming that the highest-tier room category is capturing a disproportionate share of the overall rate uplift. Japan luxury hotel market outlook remains firmly tied to the continued expansion of this affluent inbound demographic through the forecast period.

|

Segment Breakdown Luxury (48.0%) · Upper-Upscale · Upscale |

Category Insights

Chain - 65.0% Market Share (2025) | Leading Category

Chain operators command Japan's luxury hotel market because international brand recognition, global loyalty programs, and standardised service assurance are critical booking decision factors for high-spending inbound travellers who may be unfamiliar with independent Japanese operators. Global chains like Marriott, Accor, Four Seasons, Mandarin Oriental, and Shangri-La are accelerating Japan market entry and expansion programs, supported by record transaction volumes. Japan's hotel transaction volume rose to USD 3.5 billion in 2024, a 15% year-on-year increase per HVS data, with global chains driving the majority of capital deployment.

|

Segment Breakdown Chain (65.0%) · Independent |

Regional Insights

Kanto Region - 52.0% Market Share (2025) | Leading Region

Kanto region in Japan's luxury hotel market is anchored by Tokyo's position as the country's premier gateway for international luxury travellers, MICE events, and corporate travel. Tokyo accommodates the highest concentration of five-star branded properties in Japan, including Mandarin Oriental, Shangri-La, Four Seasons at Otemachi, The Peninsula, Conrad, The Ritz-Carlton, Aman, Raffles, and Park Hyatt, creating an unmatched luxury accommodation ecosystem that commands Japan's highest average daily rates. In October 2025, JW Marriott, opened JW Marriott Hotel Tokyo, its second property in Japan, designed by Yabu Pushelberg, the 200-room hotel is envisioned as a “timeless sanctuary” that reflects balance and mindfulness.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 52.0% |

| Major Prefectures | Tokyo, Kanagawa, Chiba, Saitama, Ibaraki, Tochigi, and Gunma |

| Key Growth Drivers | Global luxury brand expansions, MICE and corporate travel demand, gateway airport tourism flow, yen-driven affordability for inbound luxury travellers |

| Outlook | Dominant region with deepening premium supply pipeline |

|

Regional Breakdown Kanto Region (52.0%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

The Kansai/Kinki Region is Japan's second-largest luxury hotel market, driven by Osaka's booming corporate and Expo-related travel demand and Kyoto's globally unrivalled cultural heritage tourism. Osaka's luxury hotels grew 24% YoY in 2025, driven by the World Expo 2025, further strengthening Kansai's luxury supply.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Osaka, Kyoto, Kobe, Nara, and Shiga prefectures |

| Key Growth Drivers | Expo 2025 Osaka legacy demand, Kyoto cultural luxury tourism, new luxury brand entries, MICE event pipeline |

| Outlook | Strong growth, cultural luxury brands reshaping supply |

Central/Chubu Region:

The Central/Chubu Region's luxury hotel market is anchored by Nagano's resort destinations and Nagoya's corporate travel demand from the automotive and manufacturing sectors.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Nagoya, Hamamatsu, Shizuoka, Kanazawa, Niigata, and Nagano |

| Key Growth Drivers | Hakone and Nagano resort demand, automotive corporate travel, Mitsui Hakone luxury opening, wellness and onsen tourism |

| Outlook | Resort luxury supply expanding into natural heritage sites |

Kyushu-Okinawa Region:

The Kyushu-Okinawa Region is a high-growth area for Japan's luxury resort market, with Okinawa's beachfront positioning attracting marquee international brand investment. Fukuoka's rapid emergence as an international visitor hub and Kyushu's onsen and cultural heritage circuit are generating additional demand for luxury boutique properties across the region.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Fukuoka, Kitakyushu, Nagasaki, Kagoshima, and Kumamoto prefectures |

| Key Growth Drivers | Four Seasons Okinawa resort development, Fukuoka international visitor growth, onsen resort luxury demand, Ryukyu cultural tourism |

| Outlook | Fast-growing, flagship resort openings transforming premium supply |

Tohoku Region:

Tohoku's luxury hotel market is emerging through JNTO-led regional tourism promotion programs targeting travellers seeking authentic, less-crowded destinations beyond Japan's main golden route. The region's hot spring towns, Matsushima bay, and samurai heritage sites attract affluent travellers who prioritise privacy and cultural depth, the profile most aligned with luxury hotel positioning.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Miyagi, Aomori, Iwaki, Akita, Yamagata, and Fukushima prefectures |

| Key Growth Drivers | JNTO regional diversification programs, onsen and cultural heritage tourism, Hoshino Resorts luxury brand presence, long-stay inbound travel growth |

| Outlook | Emerging boutique luxury destination gaining international recognition |

Market Outlook (2026-2034)

What is the future outlook of the Japan luxury hotel market?

The Japan luxury hotel market is expected to sustain steady revenue growth through 2034.

The sustained pipeline of global luxury brand entries, including Fairmont Tokyo, Capella Kyoto, Hotel The Mitsui Hakone, and Four Seasons Okinawa, combined with the structural shift in inbound tourist spending toward accommodation, JNTO's record of 42.7 million annual visitors, and the continued yen advantage for international premium travellers, will sustain positive RevPAR momentum. As wellness tourism, cultural immersion programming, and AI-enhanced guest personalisation become standard luxury differentiators, Japan's market is positioned to outperform its modest CAGR with expanding per-room revenue through 2034.

Japan Luxury Hotel Market - Leading Key Players

Japan's luxury hotel market is served by a highly competitive blend of global chain operators and prestigious regional luxury brands, each competing for high-net-worth guests through brand prestige, service excellence, and culturally immersive programming. International chains leverage global loyalty ecosystems and standardised luxury benchmarks, while domestic operators offer authentic Japanese hospitality that resonates with cultural travellers seeking immersion experiences beyond standard international hotel offerings.

| Company | Leading Brands | Highlights |

|---|---|---|

|

Accor Group |

Fairmont, Sofitel, Orient Express |

Agreed to operate 23 Japan properties; Fairmont Tokyo (217 rooms, Tokyo Bay views) as part of Shibaura mixed-use development |

|

Belmond Ltd. |

Belmond |

Aligned with Japan's "koto consumption" experiential luxury travel trend |

|

Four Seasons Hotels Limited |

Four Seasons |

USD 400 million Four Seasons Resort and Private Residences Okinawa slated for 2027 opening |

Some of the other key market players in Japan luxury hotel market are Mandarin Oriental Hotel Group International Limited, Marriott International Inc., Shangri-La International Hotel Management Ltd., etc.

Latest Development & News

- In November 2025, JW Marriott expanded its presence in Japan with the opening of the JW Marriott Hotel Tokyo, marking the brand’s debut in the capital. Located above Takanawa Gateway City, a visionary development often described as Tokyo’s “City of the Future,” the hotel offers guests a peaceful retreat in the sky. Inspired by Zen philosophy and the natural beauty of Takanawa, the property blends refined design with strong connectivity, providing convenient access to central Tokyo and other key destinations.

- In May 2024, Hyatt Hotels Corporation and Kiraku, Inc. announced that the ATONA brand, a modern hot spring ryokan (traditional Japanese inn) concept, will launch new properties in Yufu, Yakushima, and Hakone. The first ATONA ryokans are expected to open in 2026 in some of Japan’s most renowned hot spring and scenic destinations.

Japan Luxury Hotel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Business Hotels, Airport Hotels, Suite Hotels, Resorts, Others |

| Room Types Covered | Luxury, Upper-Upscale, Upscale |

| Categories Covered | Chain, Independent |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Accor S.A., Belmond Ltd. (LVMH Moët Hennessy Louis Vuitton), Four Seasons Hotels Limited, Mandarin Oriental Hotel Group International Limited, Marriott International Inc., Shangri-La International Hotel Management Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan luxury hotel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan luxury hotel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan luxury hotel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Luxury Hotel Market Report

The Japan luxury hotel market was valued at USD 7.28 Billion in 2025.

The Japan luxury hotel market is anticipated to reach a value of USD 10.20 Billion by 2034.

Business hotels dominate the market with a share of 42.0%, driven by Tokyo and Osaka's combined weight as Asia's premier MICE and corporate travel corridors, which sustain high average daily rates at luxury business properties year-round, independent of leisure seasonality fluctuations.

Luxury room type commands the market with a 48.0% share, reflecting the profile of Japan's dominant inbound traveller segment, affluent visitors from Europe, North America, and Australia who prioritise suite-quality accommodations and bespoke service and are sustaining record RevPAR growth across Tokyo and Osaka luxury properties.

Chain category leads the market with 65.0%, international chain operators lead because their global loyalty programs, standardised service assurance, and brand recognition directly influence booking decisions for high-spending inbound travellers.

Kanto Region currently leads the market, accounting for a share of 52.0%. The region's leadership is driven by Tokyo's unmatched concentration of five-star branded properties, MICE infrastructure, and gateway airport access, delivering Japan's highest average daily rates and RevPAR performance.

Some of the major players in the Japan luxury hotel market include Accor Group, Belmond Ltd., Four Seasons Hotels Limited, Mandarin Oriental Hotel Group International Limited, Marriott International Inc., Shangri-La International Hotel Management Ltd., etc.

Key trends include the structural shift in inbound tourist spending from shopping toward accommodation, accelerating global luxury brand entries including Fairmont Tokyo, Capella Kyoto, and Four Seasons Okinawa; the integration of wellness programming, AI-powered guest personalisation, and cultural immersion experiences as luxury differentiators; and the expansion of luxury resort development beyond gateway cities into Okinawa, Hakone, and Hokkaido driven by wealthy travellers seeking authentic regional experiences.

Key growth drivers include Japan inbound visitors, already a new annual record, with accommodation now the top spending category per Japan Tourism Agency data; the weak yen making Japan's luxury properties exceptionally affordable for Western travellers; government JNTO campaigns expanding tourism beyond gateway cities; and a USD 400 million Four Seasons Okinawa development signalling sustained high-value resort investment into the market.

Key challenges include Japan's acute hospitality labour shortage, with demographic decline limiting the staffing levels required to deliver premium luxury service experiences at scale; pronounced seasonality creating revenue volatility between peak cherry blossom and autumn foliage periods and softer off-peak months; soaring construction costs and land prices in prime destinations delaying new luxury property supply additions; overtourism pressures in Kyoto leading to lodging tax increases effective 2026; and currency normalisation risks that could reduce the yen's affordability advantage for international luxury travellers if exchange rates reverse.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade