Japan Metal Recycling Market Size, Share, Trends and Forecast by Metal, Sector, and Region, 2026-2034

Japan Metal Recycling Market Size & Forecast 2026-2034

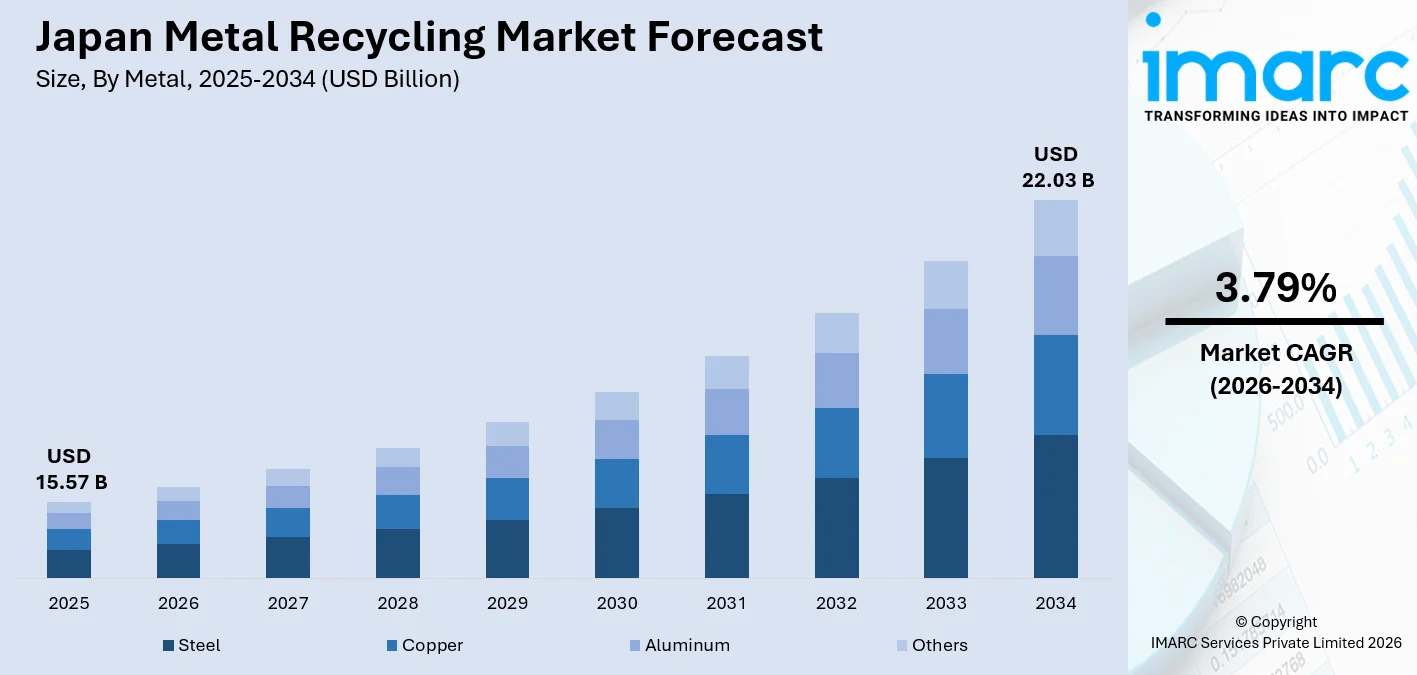

The Japan metal recycling market size, valued at USD 15.57 Billion in 2025, is projected to reach USD 22.03 Billion by 2034, growing at a CAGR of 3.79% from 2026-2034, underpinned by scrap metal demand and rising investments. The Japan Iron and Steel Federation (JISF) set a goal to increase domestic scrap circulation by about 6.9 million metric tons by 2030, in response to the expected rapid rise in demand for scrap metal.

To get more information on this market Request Sample

Japan Metal Recycling Industry Analysis - Key Insights

- Steel commands the largest share at 45.2% by metal in 2025- structurally anchored by Japan's massive installed stock of 1.4 billion tons of accumulated steel and the dominance of electric arc furnace minimills that convert scrap into rebar and structural sections.

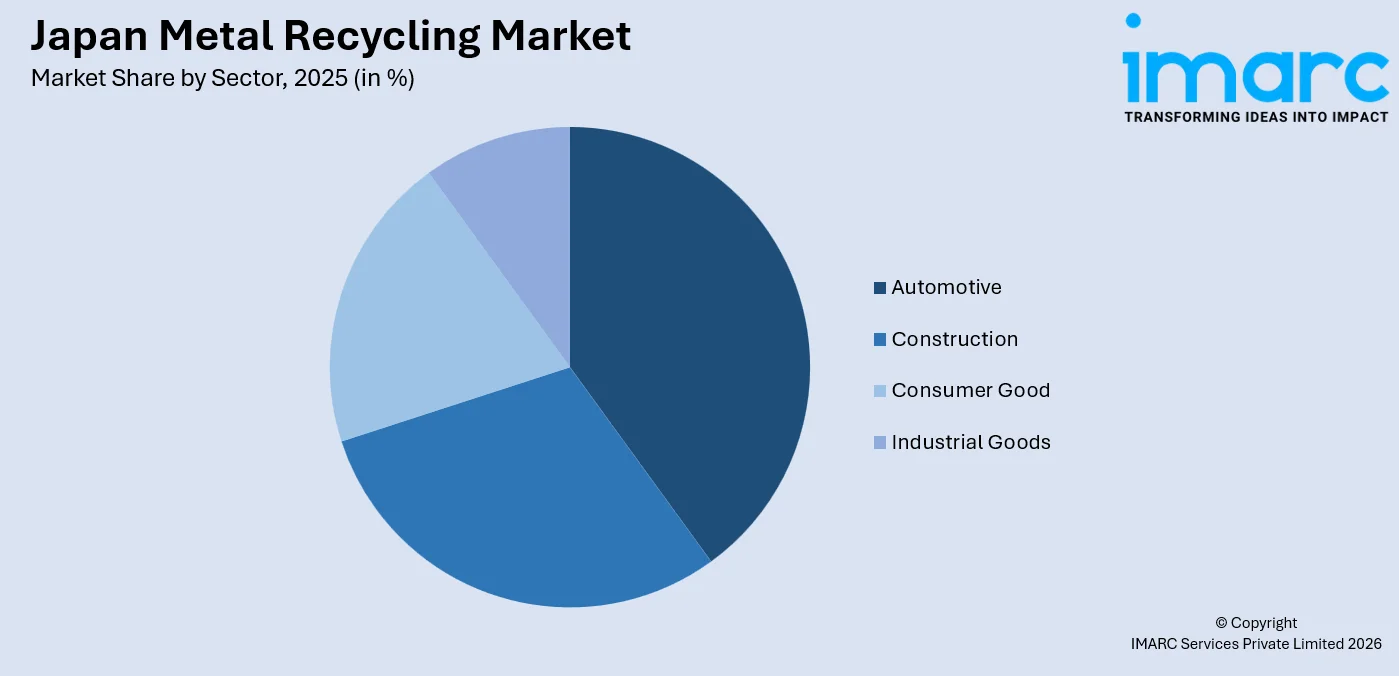

- Automotive drives the leading sector at 32.7% in 2025- with a recycling rate exceeding 99% by weight, the automotive scrap pipeline into steel and aluminum recovery is deeply institutionalized.

- Kanto Region leads regionally at 38.4% in 2025- anchored by Tokyo's dense urban industrial base, the Keihin coastal industrial cluster, and the Kanto Tetsugen Cooperative's scrap export network spanning eight prefectures.

Japan Metal Recycling Market Trends and Dynamics 2026

Market Trends

Accelerating Transition to Electric Arc Furnace Steelmaking

Japan's steel industry is undergoing a fundamental structural shift from coal-intensive blast furnace and basic oxygen furnace production toward scrap-fed electric arc furnaces (EAFs). In June 2025, Nippon Steel announced plans to invest ¥870 billion (approximately USD 6 billion) to transition three domestic facilities, at its Kyushu Works plant, to EAF technology, with a combined annual capacity of 2.9 million tonnes of recycled-content steel from fiscal 2029.

Green Steel Policy and GX Promotion Act Support

Japan's government is deploying substantial fiscal support to accelerate the recycling-to-steel pathway. In February 2025, the Ministry of Economy, Trade and Industry (METI) introduced a JPY 50,000 subsidy per clean energy vehicle (CEV) manufactured using low-carbon steel.

Digital Sorting and AI-Driven Scrap Classification

Advanced sensor-based sorting systems using X-ray fluorescence (XRF) and AI-assisted imaging are being adopted by Japanese recyclers to produce higher-grade, contamination-free scrap streams.

- EV Battery Metals Recovery: Rising electric vehicle penetration is accelerating demand for recovery of lithium, cobalt, nickel, and manganese from battery packs through specialized hydrometallurgical processes.

- Scrap Export Diversification: Japan ranks fourth globally in annual scrap exports, with South Korea, Vietnam, and Taiwan as primary destinations; export-oriented cooperatives like Kanto Tetsugen are expanding sales into Southeast Asia.

- Circular Economy Legislation Tightening: Amendments to the Automobile Recycling Law introduce incentive payments to dismantlers for handing over aluminium, copper, and glass to certified material recyclers, expanding material recovery scope.

Growth Drivers

Resource-Scarce Economy and Strategic Recycling Imperative

Japan imports virtually all primary iron ore, copper concentrate, and bauxite required for domestic production, making secondary metal recovery a national resource-security strategy. The Japan Iron and Steel Federation (JISF) set a formal target to increase domestic scrap circulation by 6.9 million metric tons by 2030 through upgraded collection infrastructure and new incentive schemes.

Industrial Manufacturing Base Generating High-Grade Prompt Scrap

Japan's precision manufacturing clusters in automotive, electronics, and machinery produce continuous volumes of high-quality scrap. Toyotsu Materials (Toyota Tsusho subsidiary) commenced operations at its JPY 490 million Toyotsu Sotec joint venture in November 2023, specifically targeting aluminium scrap sorting and processing for horizontal aluminium recycling into equivalent-grade output.

- GX Green Transformation Policy: METI's GX Promotion Act provides a JPY 251.4 billion subsidy framework for blast furnace-to-EAF conversion, directly stimulating demand for recycled scrap steel.

- Electronics and E-Waste Urban Mining: Japan's precision instrument and consumer electronics manufacturing generates high-value precious metal scrap.

- Semiconductor Supply Chain Localization: Japan's government-backed semiconductor expansion at facilities such as TSMC Kumamoto is driving demand for high-purity recycled copper wiring materials.

Market Restraints

Scrap quality degradation and contamination challenges: As Japan's manufacturing base evolves toward increasingly complex multi-material products, including vehicles with advanced composites, coated steels, and embedded electronics, the quality and purity of recovered metal scrap are becoming harder to maintain.

Structural demographic shift reducing industrial scrap generation: Japan's shrinking and ageing population is reducing domestic demand for steel-intensive construction and manufacturing output over the long term. As crude steel production declines and the BF-BOF share contracts, the supply of high-quality home scrap and prompt scrap, closely tied to production volumes, will progressively diminish, tightening the supply-demand balance.

High energy costs constraining EAF competitiveness: Electric arc furnace recycling operations are highly sensitive to electricity prices. Japan's power sector remains structurally exposed to imported liquefied natural gas and coal, and grid electricity costs remain elevated relative to global averages. Without access to competitive and predictable renewable electricity, EAF operators face cost disadvantages versus overseas integrated producers, limiting the pace of blast furnace-to-EAF capacity conversion.

Japan Metal Recycling Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

|

Metal |

Steel |

45.2% |

2025 |

|

Sector |

Automotive |

32.7% |

2025 |

|

Region |

Kanto Region |

38.4% |

2025 |

.webp)

Metal Insights

Steel - 45.2% market share (2025) | Leading Metal

Steel dominates Japan's metal recycling landscape due to the country's deep reliance on electric arc furnace minimills that consume scrap as primary feedstock. The top five EAF steel producers in Japan, Tokyo Steel, Kyoei Steel, Godo Steel, Nakayama Steel Works, and Yamato Steel, together account for about 10% of the country’s total crude steel production.

|

Segment Breakdown Steel (45.2%) · Copper · Aluminum · Others |

Sector Insights

Access the comprehensive market breakdown Request Sample

Automotive - 32.7% market share (2025) | Leading Sector

The automotive sector is Japan's most institutionalized source of secondary metal, underpinned by the mandatory Automobile Recycling Law that assigns extended producer responsibility to manufacturers across the entire vehicle lifecycle. In 2023, approximately 2.73 million ELVs were collected and processed.

|

Segment Breakdown Automotive (32.7%) · Construction · Consumer Good · Industrial Goods |

Regional Insights

Kanto Region - 38.4% market share (2025) | Leading Region

Kanto Region dominates the market, anchored by the Greater Tokyo Metropolitan Area's unmatched density of industrial scrap generators, dismantling yards, and EAF steelmakers. The Kanto Tetsugen Cooperative Association, comprising 80 scrap metal companies across Tokyo, Saitama, Kanagawa, Chiba, Gumma, Tochigi, Ibaraki, and Yamanashi prefectures, exported approximately 250,000 tonnes of ferrous scrap annually, primarily to South Korea and Southeast Asian markets.

|

Metric

|

Details

|

|---|---|

| Market share in 2025 | 38.4% |

| Major Prefectures | Tokyo, Kanagawa, Chiba, Saitama, Ibaraki, Tochigi, and Gunma |

| Key Growth Drivers | Dense EAF minimill network, Keihin industrial cluster, urban redevelopment scrap, Kanto Tetsugen export infrastructure |

| Outlook | Sustained leadership driven by EAF conversion pipeline |

|

Regional Breakdown Kanto Region (38.4%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

The Kansai/Kinki region is Japan's second most significant metal recycling hub, driven by Osaka's port-based non-ferrous trading infrastructure and the manufacturing clusters of Hyogo Prefecture.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Osaka, Kyoto, Kobe, Nara, and Shiga |

| Key Growth Drivers | Non-ferrous trading infrastructure, aluminium scrap sorting investment, Osaka port export access, specialty steel recycling |

| Outlook | Growing non-ferrous and specialty metal recovery hub |

Central/Chubu Region:

The Chubu region is deeply integrated with Japan's automotive manufacturing complex, hosting major players and a dense network of precision metal parts manufacturers. This generates the highest per-unit-production volumes of high-quality automotive prompt scrap, cut steel, aluminium die-cast off-cuts, and copper wiring in Japan. Chubu Steel Plate produces the "Sumiles" low-carbon EAF green steel brand, underscoring local commitment to recycled steel value-addition.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Nagoya, Hamamatsu, Shizuoka, Kanazawa, Niigata, and Nagano |

| Key Growth Drivers | Toyota Group automotive prompt scrap, precision parts manufacturing residues, low-carbon green steel branding, ROMAE benchmark scrap pricing hub |

| Outlook | Stable, high-quality automotive scrap source |

Kyushu-Okinawa Region:

Kyushu-Okinawa is gaining strategic significance as a metal recycling destination following Nippon Steel’s plans to construct a new electric arc furnace at its Kyushu works. These investments result in a total annual capacity of 2.9 million metric tons. This investment materially increases local scrap consumption across the region, requiring upgrades in regional scrap collection and logistics.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Fukuoka, Kitakyushu, Nagasaki, Kagoshima, and Kumamoto |

| Key Growth Drivers | Nippon Steel Kyushu EAF investment, TSMC Kumamoto semiconductor copper recovery, automotive ELV dismantling, port-based scrap export access |

| Outlook | Rising scrap consumption from new EAF capacity |

Tohoku Region:

DOWA Holdings' flagship mining and smelting operations in Akita Prefecture remain an important non-ferrous metals recovery site, where the Kosaka Smelting and Refining subsidiary extracts from electronic scrap.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Miyagi, Aomori, Iwaki, Akita, Yamagata, and Fukushima |

| Key Growth Drivers | Reconstruction scrap recovery, DOWA Kosaka non-ferrous smelting, green EAF steel production, government post-disaster infrastructure investment |

| Outlook | Steady growth anchored by non-ferrous smelting heritage |

Market Outlook (2026-2034)

What is the future outlook of the Japan Metal Recycling market?

The Japan Metal Recycling market is expected to sustain steady revenue growth through 2034.

Japan's metal recycling sector is well-positioned for consistent expansion, supported by the EAF transition wave led by Nippon Steel, deepening circular economy policy under the GX Promotion Act, and growing demand for high-purity recycled aluminium and copper from EV manufacturers and semiconductor fabs. In 2023, Japan exported 6.9 million tons of scrap steel, which was used to produce 5.8 million tons of lower-carbon steel, a requirement of 1.2 tons of scrap per ton of steel produced, underpinning supply-side investment, while tightening carbon border measures in export markets reinforce domestic demand for low-carbon recycled steel, sustaining the Japan metal recycling market outlook through 2034.

Japan Metal Recycling Market - Leading Key Players

The Japan metal recycling market is shaped by a competitive tier spanning integrated steelmakers, dedicated non-ferrous recyclers, and trading house subsidiaries. Market participants compete on scrap procurement network depth, processing technology capability, and ability to certify recycled content for premium green steel applications.

| Company | Leading Brands | Highlights |

|---|---|---|

|

Sumitomo Metal Mining Co., Ltd. |

Non-ferrous Metal Recycling |

Major Japanese mining and metals company involved in recycling precious and non-ferrous metals, supporting sustainable resource management and circular economy initiatives. |

|

Mitsubishi Materials Corporation |

Precious Metal Recycling, Non-Ferrous Metal Recycling |

Recovers valuable metals such as gold, silver, and copper from industrial waste and scrap materials through advanced smelting and refining processes. |

|

Matsuda Sangyo Co., Ltd. |

Precious Metal Recycling |

Provides integrated recycling services for precious metals like gold, silver, platinum, and palladium. |

Some of the other key market players in Japan metal recycling market are DOWA Holdings Co., Ltd., Nippon Steel Corporation, Hanwa Co., Ltd., Metal Do Co., Ltd., MM & Stainless Recycling Corporation, Keiaisha Co., Ltd., Kyoei Steel Ltd., etc.

Latest Development & News

- In June 2025, DOWA Electronics Materials Co., Ltd. honored with a supplier award from Murata Manufacturing Co., Ltd. This recognition highlights the joint efforts of DOWA Group and Murata Manufacturing in developing a resource circulation system that ensures the secure collection and use of recycled metals through effective metal resource recycling.

- In May 2025, Nippon Steel plans to invest nearly JPY 870 billion ($6.05 billion) to introduce electric arc furnaces at three of its facilities in Japan as part of its effort to cut carbon emissions. A portion of the funding will be provided by the Japanese government, which plans to subsidize 251 billion yen of the company’s decarbonization initiatives across these three facilities by fiscal year 2028/2029.

- In February 2025, Japan recently introduced an incentive for green steel, with the Ministry of Economy, Trade, and Industry (METI) offering a 50,000 yen subsidy for clean energy vehicles (CEVs) produced using low-carbon emission steel.

Japan Metal Recycling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Metals Covered | Steel, Copper, Aluminum, Others |

| Sectors Covered | Construction, Automotive, Consumer Goods, Industrial Goods |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan metal recycling market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan metal recycling market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan metal ecycling industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Metal Recycling Market Report

The Japan metal recycling market was valued at USD 15.57 Billion in 2025.

The Japan metal recycling market is anticipated to reach a value of USD 22.03 Billion by 2034.

Steel dominates the market with a share of 45.2% in 2025, driven by the country's extensive installed base of electric arc furnace minimills that consume scrap steel as primary feedstock.

Automotive leads the market with a share of 32.7% in 2025, underpinned by mandatory end-of-life vehicle recycling legislation, the processing of approximately 2.73 million ELVs per year.

The Kanto Region currently leads the market, accounting for a share of 38.4% in 2025. The region's leadership is driven by the Greater Tokyo industrial base, the Keihin coastal manufacturing cluster in Kawasaki and Yokohama, the Kanto Tetsugen scrap export cooperative, and high urban demolition scrap volumes from post-Olympic infrastructure renewal in the metropolitan area.

Some of the major players in the market include Sumitomo Metal Mining Co., Ltd., Mitsubishi Materials Corporation, Matsuda Sangyo Co., Ltd. DOWA Holdings Co., Ltd., Nippon Steel Corporation, Hanwa Co., Ltd., Metal Do Co., Ltd., MM & Stainless Recycling Corporation, Keiaisha Co., Ltd., Kyoei Steel Ltd., etc.

Key trends include the rapid shift toward electric arc furnace steelmaking supported by GX Promotion Act subsidies, growing AI-assisted scrap sorting for high-purity separation, expansion of aluminium horizontal recycling as the automotive lightweighting trend deepens, and the emerging recovery of battery-grade metals (lithium, cobalt, nickel) from end-of-life electric vehicle packs.

Key growth drivers include Japan's near-total import dependence on primary metal ores, making secondary recovery a strategic necessity, and rising demand for recycled copper and aluminium from EV manufacturers and semiconductor fabrication facilities.

Key challenges include quality degradation and contamination from increasingly complex multi-material vehicle and electronics designs, declining crude steel production constraining home and prompt scrap supply over the long term, elevated electricity costs limiting the competitiveness of EAF operations relative to overseas integrated producers, ageing demographics reducing industrial scrap generation, and fluctuating global scrap export prices that periodically erode domestic market margins for recyclers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)