Japan Off-The-Road Tire Market Size, Share, Trends and Forecast by Vehicle Type, Tire Type, Distribution Channel, Rim Size, End-Use, and Region, 2026-2034

Japan Off-The-Road Tire Market Size, Share, Trends & Forecast (2026-2034)

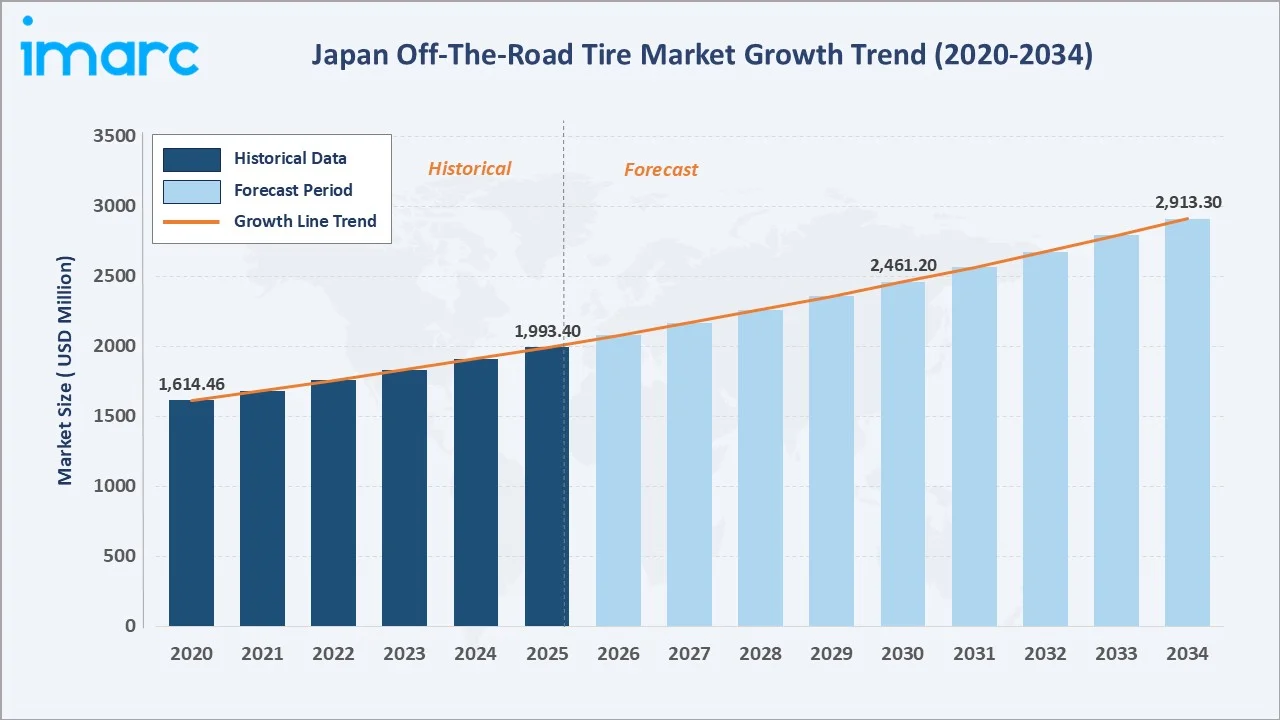

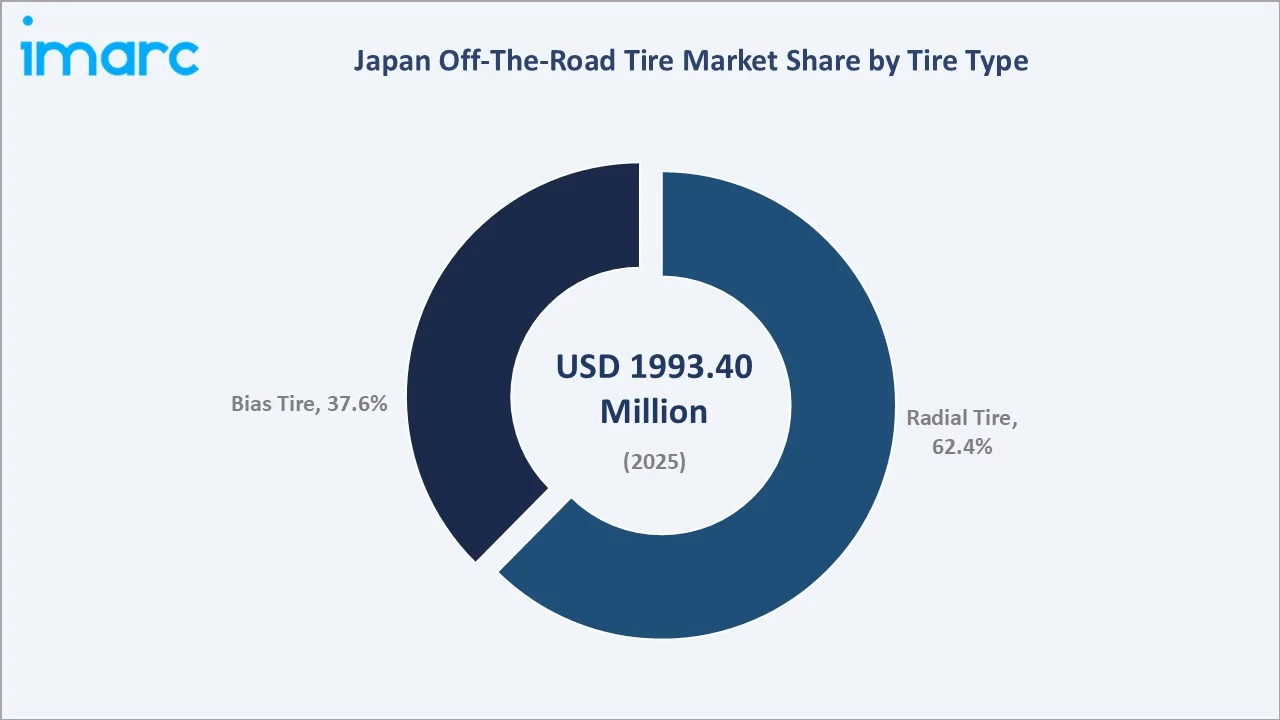

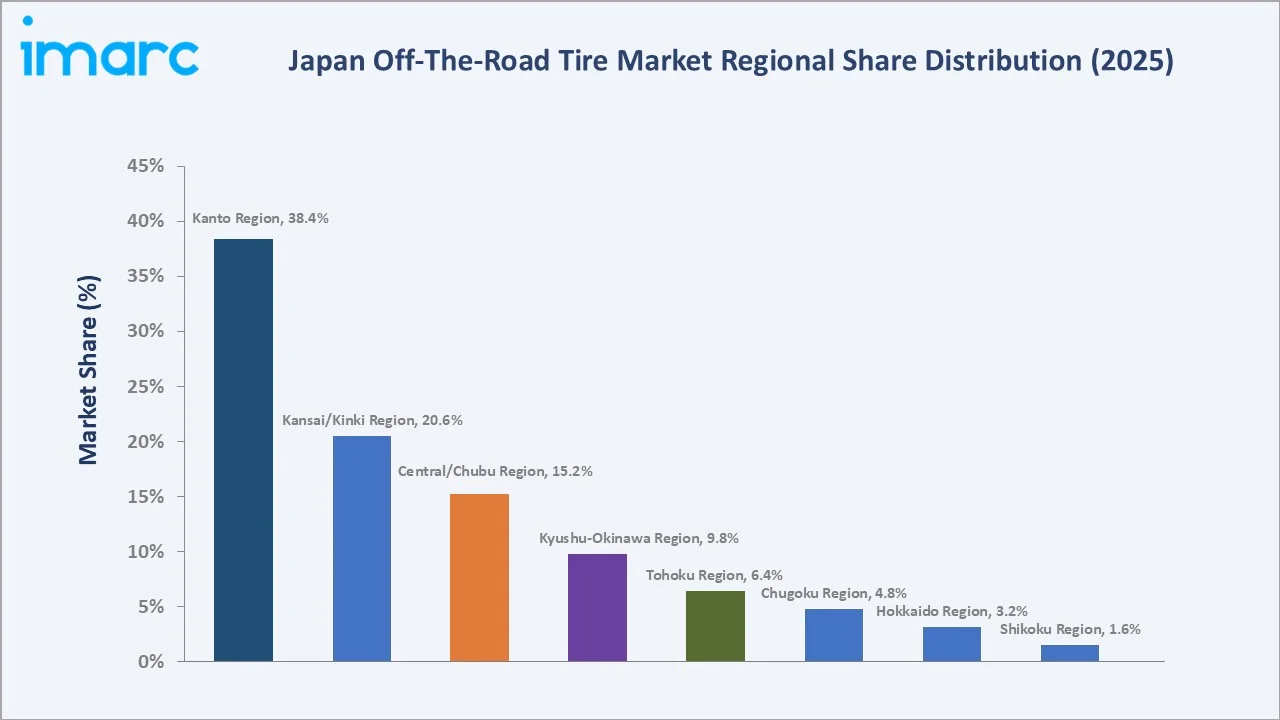

The Japan off-the-road (OTR) tire market was valued at USD 1,993.40 Million in 2025 and is projected to reach USD 2,913.30 Million by 2034, expanding at a CAGR of 4.31% during the forecast period (2026-2034). Growth is underpinned by Japan’s infrastructure renewal program, construction activity driven by TSMC Kumamoto semiconductor fab investment of $17 billion to mass produce advanced 3-nanometre chips, agricultural mechanization in Hokkaido and Tohoku, and the systematic replacement cycle of Japan’s world-class construction equipment fleet. Radial tires dominate at 62.4% tire type share, while offline distribution leads at 72.5%. The Kanto region commands 38.4% of national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,993.40 Million |

|

Forecast Market Size (2034) |

USD 2,913.30 Million |

|

CAGR (2026-2034) |

4.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

Kanto (38.4%, 2025) |

|

Fastest Growing Region |

Kyushu-Okinawa (CAGR ~4.9%, 2026-2034) |

The Japan OTR tire market growth expanded from USD 1,614.50 Million in 2020 to USD 1,993.40 Million in 2025, driven by post-COVID construction restart and domestic manufacturing investment. Anchored at USD 2,461.20 Million in 2030, the forecast to USD 2,913.30 Million by 2034, underpinned by sustained infrastructure spending, mining sector recovery, and next-generation OTR tire platform investment.

To get more information on this market, Request Sample

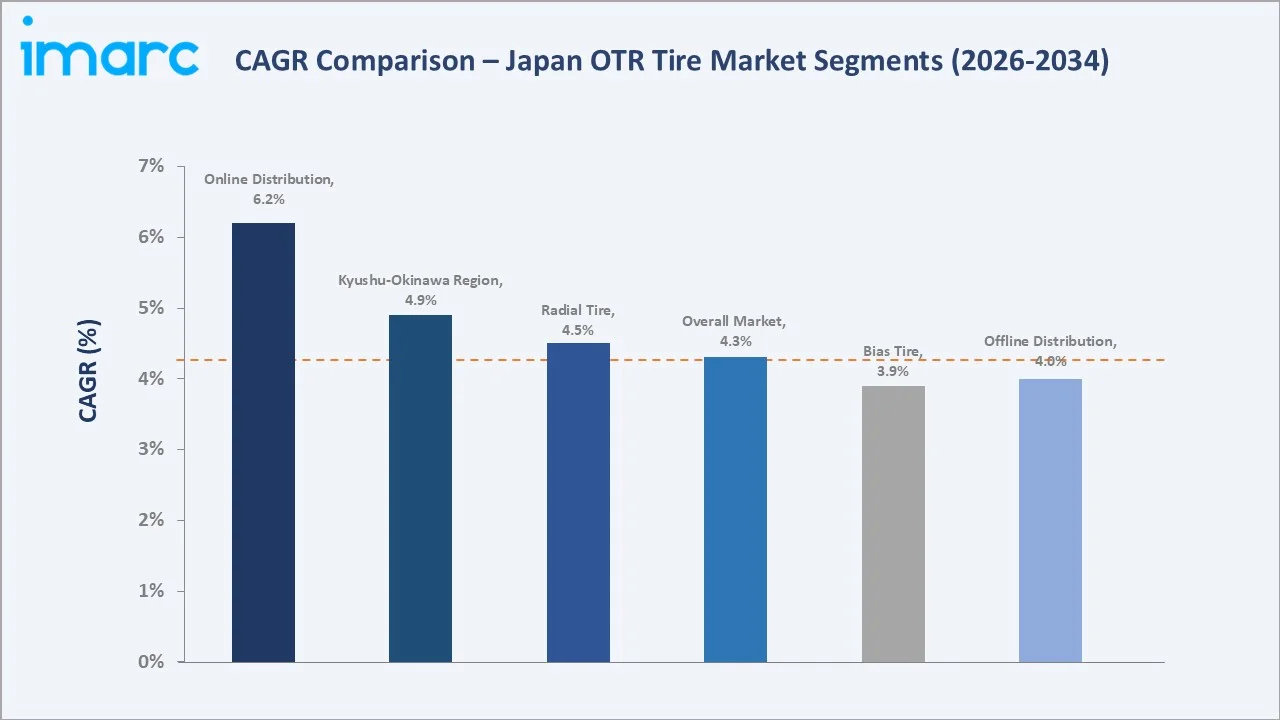

The CAGR across key segments with Online distribution at ~6.2% CAGR grows fastest, reflecting the digitalization of B2B OTR tire procurement as construction rental companies, mining operators, and agricultural cooperatives increasingly use e-procurement platforms for replacement tire orders. Kyushu-Okinawa Region at ~4.9% CAGR is the fastest-growing regional market, driven by TSMC Japan semiconductor supply chain manufacturing investment, creating new heavy-equipment operating demand in Kumamoto Prefecture.

Executive Summary

The Japan off-the-road tire market has expanded from USD 1,614.50 Million in 2020 to USD 1,993.40 Million in 2025, achieved through Japan’s COVID-19 economic recovery programs, sustained infrastructure investment, and the ongoing mechanization of Japan’s agricultural sector. The market’s forecast trajectory is to USD 2,913.30 Million by 2034 at 4.31% CAGR. Japan’s OTR market is structurally different from emerging market peers, dominated by premium high-performance tires at 2–3× global average price points, rigorous JATMA safety compliance requirements, and systematic digital tire management adoption.

Radial tires at 62.4% market share (2025), reflecting Japan’s world-leading construction and mining equipment quality standards. Bridgestone Corporation’s ¥25 billion investment to upgrade equipment at its Kitakyushu Plant, which produces radial off-the-road (OTR) tires for mining and construction vehicles, with completion by the end of 2027. Offline distribution’s 72.5% dominance reflects the technical nature of OTR tire procurement; large-format construction and mining tires require specialist fitting equipment, on-site service capability, and trained technicians that physical dealers provide, but online channels cannot yet match at scale.

Kanto’s 38.4% dominance reflects Greater Tokyo’s concentration of Japan’s largest construction project portfolio, including the JPY 9 trillion Japanese SC Maglev (Superconducting Maglev) project, Tokyo Metropolitan Expressway maintenance, and Narita and Haneda airport expansion.

Key Market Insights

|

Insight |

Data |

|

Dominant Tire Type |

Radial Tire – 62.4% revenue share (2025) |

|

Dominant Distribution Channel |

Offline – 72.5% revenue share (2025) |

|

Leading Region |

Kanto – 38.4% revenue share (2025) |

|

Fastest Growing Region |

Kyushu-Okinawa (CAGR ~4.9%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Radial tire at 62.4% (2025) leads Japan’s OTR market because Japan’s premium construction and mining equipment ecosystem prioritizes total cost of ownership over initial purchase price.

- Offline distribution at 72.5% (2025) reflects OTR’s unique service requirements that differentiate it from consumer tire retail. OTR tires for mining haul trucks and earthmovers require specialized fitting equipment, hydraulic tire handlers, nitrogen inflation stations, and certified rim assembly tools, that cannot be replicated in remote mine or construction site conditions without physical dealer support.

- Kanto Region’s 38.4% share reflects Greater Tokyo’s role as Japan’s construction activity epicenter.

Japan Off-The-Road Tire Market Overview

Off-the-road (OTR) tires are specialized large-format rubber tires designed for heavy-duty vehicles operated in demanding off-road environments including mining sites, construction projects, agricultural fields, port operations, and industrial logistics. Japan’s OTR tire market encompasses tires for mining haul trucks and front-end loaders, construction excavators and dump trucks, agricultural tractors and combine harvesters, industrial forklifts and reach stackers, and specialty vehicles including airport ground support equipment and underground mining vehicles.

The Japan OTR tire ecosystem integrates world-class domestic manufacturers, international premium suppliers, and India-origin value competitors. Applications span MLIT-funded infrastructure construction, private sector construction, agricultural mechanization, and mining/quarrying. Macroeconomic drivers include Japan’s public infrastructure budget (MLIT), private construction investment, agricultural machinery MAFF subsidy programs, and global commodity price cycles affecting rubber and steel input costs.

Market Dynamics

To evaluate market opportunities, Request Sample

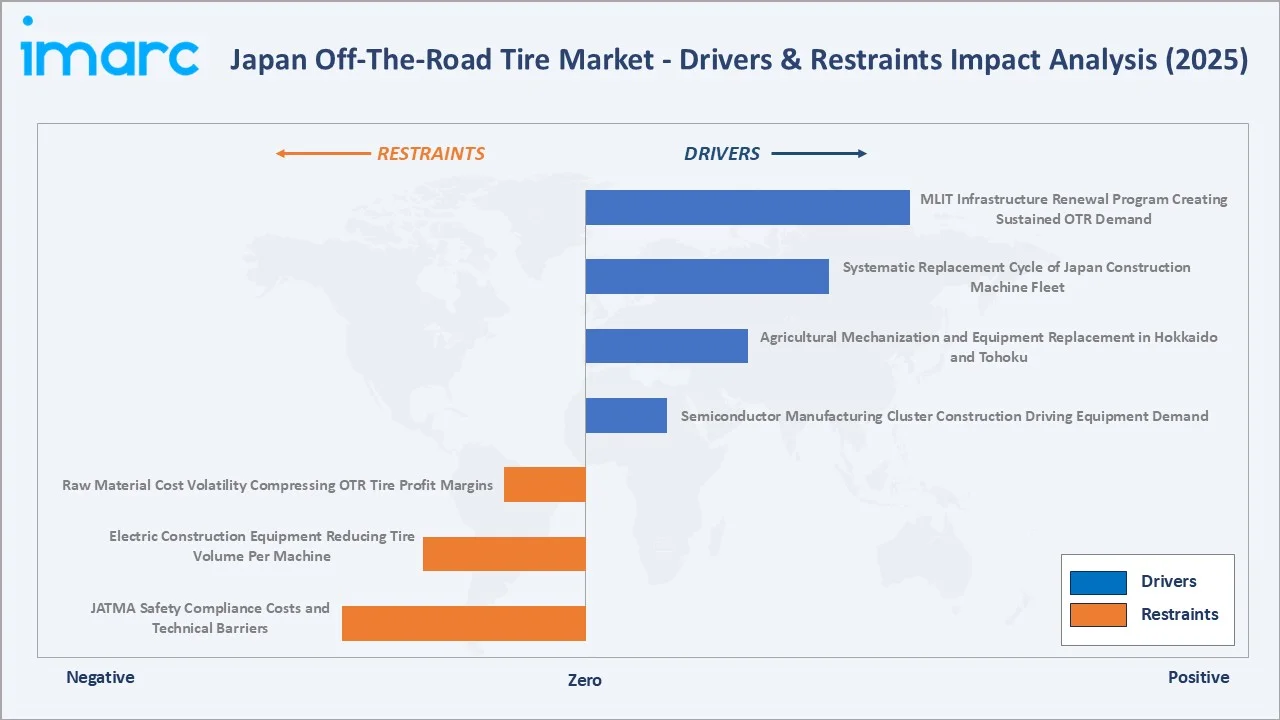

Market Drivers

- Semiconductor Manufacturing Cluster Construction Driving Equipment Demand: Japan’s semiconductor manufacturing renaissance, TSMC Kumamoto semiconductor fab investment of $17 billion to mass produce advanced 3-nanometre chips. Each large semiconductor fab site requires 24–36 months of intensive site preparation, foundation work, and construction, requiring 80–150 large excavators and dump trucks, consuming 400–800 OTR tires per site over the construction period.

- Agricultural Mechanization and Equipment Replacement in Hokkaido and Tohoku: Japan’s Ministry of Agriculture, Forestry and Fisheries (MAFF) ’s Smart Agriculture Implementation Program providing 180 billion yen in subsidies for farmers implementing precision agriculture technologies, creating a systematic annual agricultural OTR replacement demand.

- Systematic Replacement Cycle of Japan’s Construction Machine Fleet: Japan’s registered construction machinery fleet units encompass hydraulic excavators, dump trucks, wheel loaders, and graders. This fleet consumes OTR replacement tires, with replacement cycles of 12–18 months for construction OTR in Japanese conditions, creating highly predictable demand volume.

Market Restraints

- Raw Material Cost Volatility Compressing OTR Tire Profit Margins: Natural rubber, representing 40–50% of OTR tire raw material cost by value. Japan’s reliance on Southeast Asian rubber imports via Sumitomo Corporation and Bridgestone Agri-Business commodity procurement creates structural price risk that domestic tire manufacturers cannot fully offset through pricing, given competitive market dynamics and long-term OEM supply agreement pricing constraints.

- Electric Construction Equipment Reducing Tire Volume Per Machine: Battery electric construction equipment’s lower powertrain weight reduces ground pressure, enabling smaller OTR tire sizes that reduce per-machine revenue by 15–25%.

Market Opportunities

- Smart Tire Technology and TPMS Integration for OTR Applications: TPMS (Tire Pressure Monitoring Systems) on all construction vehicles over 3.5 tonnes is creating a new revenue layer for Japan’s premium OTR tire suppliers.

- Electric and Autonomous Mining Equipment OTR Specialty Development: The global transition to battery electric ultra-large mining haul trucks requires new OTR tire compounds optimized for the different torque delivery characteristics, lower cabin heat signature, and increased static load from battery weight.

- Offshore Wind Construction OTR Tire Demand: Japan’s target of offshore wind power projects of 10 GW by 2030 and 30 to 45 GW by 2040. Each offshore wind base port construction project deploys 30–60 heavy construction vehicles over 18–24 months, creating a port project in OTR tire demand for marine-environment-resistant compounds.

Market Challenges

- JATMA Safety Compliance Costs and Technical Barriers: JATMA’s voluntary OTR tire safety standards, which the construction industry treats as de facto mandatory for public works contracts, require Japanese Industrial Standard JIS K 6308 certification for all OTR tires used on MLIT-funded construction projects.

- Aging Construction Equipment Fleet and Extended Replacement Cycles: Japan’s construction sector’s operational efficiency culture means equipment is maintained and operated 30–40% longer than global averages. While extended equipment life creates ongoing OTR replacement demand, the trend toward extending machine lifetimes means OTR per-machine annual revenue declines as older machines are operated at lower intensity, reducing tire consumption rates.

Emerging Market Trends

1. Radial OTR Technology Advancing into Agricultural Applications

Japan’s agricultural sector, traditionally a bias tire stronghold, is systematically adopting radial OTR technology for large-scale Hokkaido farming operations. Yokohama’s AGRI STAR II is a new radial tractor tire by Alliance, featuring Stratified Layer Technology (SLT) for enhanced traction with an evolving footprint. Developed in close collaboration with farmers, it meets high standards, with success ultimately measured by user experience.

2. Eco-Compound OTR Tires for Japan’s Carbon Neutral 2050 Target

Japan’s Carbon Neutral 2050 declaration is cascading into construction equipment OTR tire specifications, with MLIT’s Green Infrastructure guidelines beginning to incorporate lifecycle carbon criteria into public works tire procurement.

3. Ultra-Large OTR Tires for Japanese Mining Expansion

Japan’s critical mineral strategy, targeting domestic production of lithium, cobalt, nickel, and rare earth elements to reduce dependence on Chinese imports for EV battery and semiconductor manufacturing, is investing in domestic mining capacity at Sumitomo Metal Mining’s Besshi-Niihama complex, Mitsubishi Materials’ Akita and Toyoha mines, and JOGMEC-funded exploration projects in Hokkaido and Tohoku.

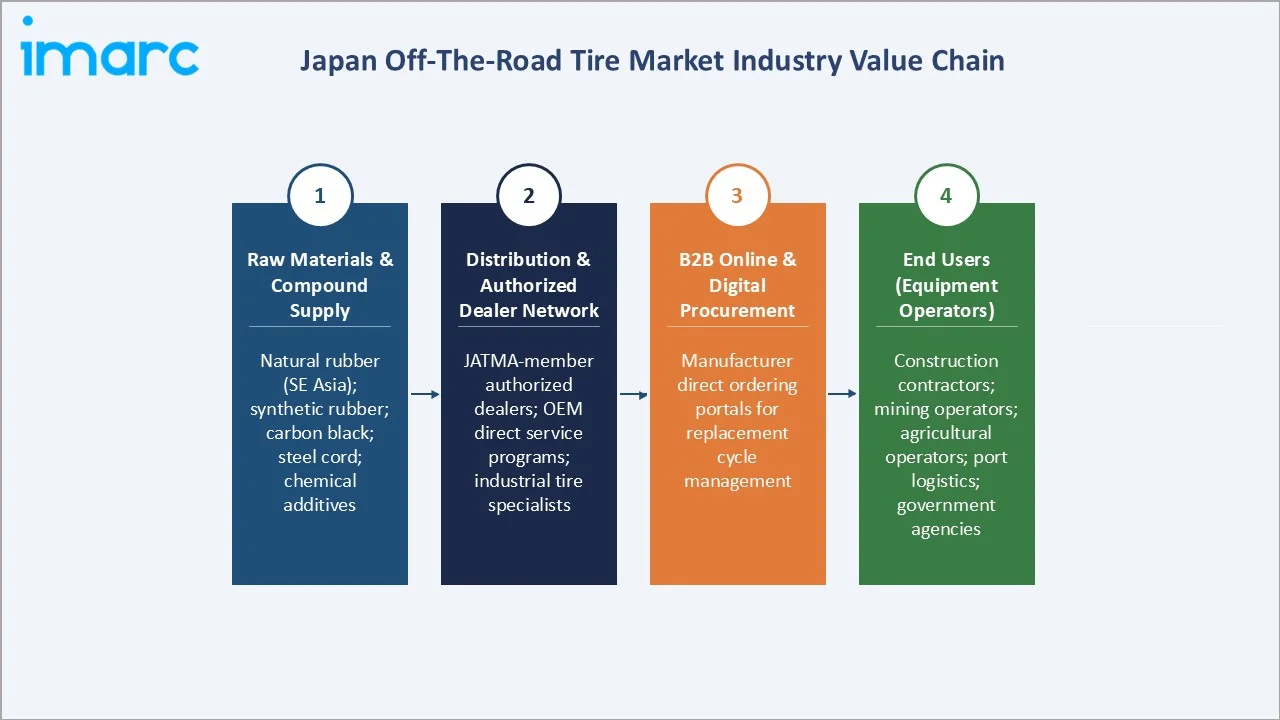

Industry Value Chain Analysis

Japan’s OTR tire value chain integrates Southeast Asian rubber and domestic steel raw materials through domestic compounding and manufacturing, OEM equipment supply, multi-tier dealer distribution, and specialized on-site industrial installation services across Japan’s diverse construction, mining, and agricultural end-use sectors.

|

Stage |

Key Participants |

|

Raw Materials & Compound Supply |

Natural rubber; synthetic rubber; carbon black; steel cord; chemical additives |

|

Distribution & Authorized Dealer Network |

Authorized tire dealers; JATMA-member distributor network; industrial tire specialty; OEM direct service agreements for large mining equipment; import distributors for specialty OTR tires |

|

B2B Online & Digital Procurement |

Manufacturer direct ordering portals for replacement cycle management; construction industry digital procurement platforms |

|

End Users (Equipment Operators) |

Construction contractors; mining operators; agricultural operators; port and industrial logistics; government infrastructure agencies |

Bridgestone and Sumitomo Rubber’s vertically integrated rubber plantation and domestic manufacturing model gives them a 15–20% cost advantage versus international peers importing fully manufactured OTR tires into Japan.

Technology Landscape in the Japan OTR Tire Industry

High-Load Radial OTR Compound Technology for Extreme Duty Applications

Bridgestone’s V-Steel compound technology uses woven steel belt structures that distribute load across a larger footprint than conventional bias tires, reducing ground pressure and penetration risk in rocky Japanese construction environments. In February 2026, Bridgestone unveiled three new off-the-road tires: the 27.00R49 Bridgestone MasterCore V-Steel M-Traction Deep (VMTD), 24.00R35 Bridgestone V-Steel Rock Deep Ultra (VRDU), and Firestone Multi Block T. These tires will be featured at the Bridgestone Off-the-Road booth, showcasing a range of premium tires for cranes, graders, haulers, and loaders.

Intelligent TPMS and IoT Sensor Integration in OTR Applications

Next-generation OTR smart tire systems embed MEMS (Micro-Electromechanical Systems) pressure and temperature sensors in the bead area, transmitting data via Bluetooth Low Energy (BLE) to on-board transceivers and then via 4G/5G LTE to cloud-based fleet management platforms.

Eco-Compound and Low-Rolling-Resistance OTR Technology

Japan’s Carbon Neutral 2050 mandate is driving tire compound R&D investment at Bridgestone’s Kodaira Technical Center, Sumitomo Rubber’s Kobe R&D laboratory, and Yokohama Rubber’s Hiratsuka Technology Centre.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

|

Tire Type |

Radial Tire |

62.4% |

2025 |

|

Distribution Channel |

Offline |

72.5% |

2025 |

|

Rim Size |

🔒 |

🔒 |

2025 |

|

End-Use |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

38.4% |

2025 |

By Tire Type

To access detailed market analysis, Request Sample

Radial tires lead at 62.4% market share (2025). Radial OTR’s dominance in Japan reflects the construction industry’s premium quality culture. The radial OTR segment is further driven by Japan’s large-scale mining and quarrying equipment deployment and rising investments. In August 2024, Bridgestone Corporation invested ¥25 billion (US$170 million) to upgrade its Kitakyushu Plant in Fukuoka Prefecture, Japan, which produces off-the-road (OTR) tires for mining and construction vehicles. Since opening in June 2009, the plant has been producing 170 tons of OTR radial tires daily.

Bias tires at 37.6% maintain market relevance in agricultural applications, small-format construction, and specialty applications where radial’s steel belt rigidity creates operational disadvantages. Bias tires’ simpler repair characteristics, punctures can be repaired field-side by a single technician versus radial’s specialist repair requirements, also sustain demand in remote agricultural and forestry sites where dealer service support is limited.

By Distribution Channel

Offline distribution leads at 72.5% market share (2025). This segment encompasses JATMA-member authorized tire dealers, OEM direct service programs, and specialty industrial tire service companies. Offline’s dominance is structural; large-format OTR tires physically cannot be shipped by standard parcel carriers and require specialized low-bed trailer logistics to construction sites, while the fitting process requires fixed-workshop hydraulic fitting equipment and JATMA-certified technicians that offline dealers provide.

Online distribution at 27.5% is growing, as B2B e-commerce platforms capture sub-29-inch OTR replacement orders from agricultural cooperatives, small construction contractors, and municipal vehicle operators.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto |

38.4% |

Largest construction equipment concentration in Japan |

|

Kansai/Kinki |

20.6% |

Kansai infrastructure renaissance, Osaka World Expo 2025 construction driving infrastructure investment |

|

Central/Chubu |

15.2% |

Toyota City automotive mega-cluster construction |

|

Kyushu-Okinawa |

9.8% |

TSMC Kumamoto fab construction requiring massive site preparation, excavation, and construction equipment OTR tire demand |

|

Tohoku |

6.4% |

Reconstruction infrastructure completion and ongoing maintenance |

|

Chugoku |

4.8% |

Mazda Motor Hiroshima plant expansion, EV production conversion requiring factory floor renovation and construction equipment |

|

Hokkaido |

3.2% |

Japan’s primary agricultural mechanization market; cold-climate specialty OTR tires for snow and frozen ground operations |

|

Shikoku |

1.6% |

Ehime Prefecture quarrying, Shikoku Expressway network maintenance and expansion construction |

Kanto’s 38.4% dominance is reinforced by Japan’s highest concentration of large construction contractors whose project fleets systematically deploy premium Bridgestone and Michelin OTR tires. The Linear Chuo Maglev Shinkansen project, Japan’s largest single infrastructure project at JPY 9 trillion, is deploying heavy construction vehicles in Kanagawa and Yamanashi tunneling sections, consuming an OTR tires annually during peak construction phase.

Chubu’s 15.2% share is anchored by Toyota’s Woven City construction project. Tohoku’s 6.4% share reflects the region’s unique dual OTR demand profile: construction and agriculture. The Akita Noshiro Port offshore wind development, Japan’s largest operational offshore wind project requiring OTR tire consumption during its construction phase.

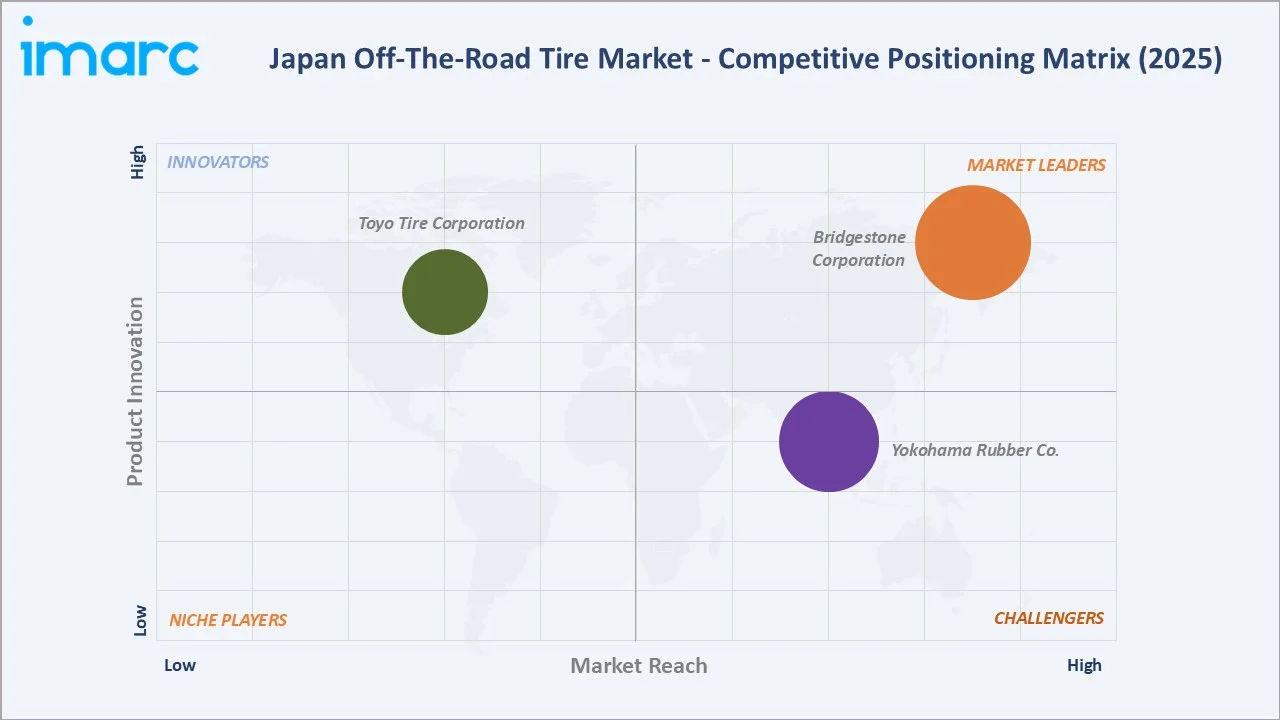

Competitive Landscape

The Japan OTR tire market is highly concentrated among domestic and multinational premium brands. Bridgestone Corporation and Yokohama together account for approximately 45–50% of total Japan OTR tire market revenue.

|

Company Name |

OTR Product Line |

Market Position |

Core Strength |

|

Bridgestone Corporation |

Surface Mining Tires, Underground Mining Tires, Quarries and Construction Tires, Ports and Terminal Tires |

Dominant Market Leader |

Bridgestone has been the world's second-largest tire manufacturer by revenue since 2021 and Japan’s #1 OTR tire company with high domestic market share |

|

THE YOKOHAMA RUBBER CO., LTD. |

Earthmover Tires, Loader & Dozer Tires, Grader Tires, Compactor Tires, Mobile Crane Tires, Industrial Tires |

Strong Challenger |

The Yokohama RB series (RB01, RB03) is designed for mobile cranes on highway use |

|

TOYO TIRE CORPORATION |

Open Country M/T, Open Country R/T Pro, Open Country R/T, Open Country R/T Trail, M655, M-55, Open Country A/T III, Open Country A/T III EV, Open Country C/T, Open Country SxS, Open Country M/T-R |

Established |

Agricultural OTR leadership |

The top three companies' combined share is approximately 70–75%. The remaining 25–30% is distributed across specialty/value competitors.

Key Company Profiles

Bridgestone Corporation

Bridgestone Corporation is one of the world’s largest tire manufacturers and Japan’s dominant OTR tire company.

- Product Portfolio: Surface Mining Tires, Underground Mining Tires, Quarries and Construction Tires, Ports and Terminal Tires.

- Recent Developments: In August 2024, Bridgestone Corporation invested ¥25 billion to upgrade equipment for certain facilities at the Kitakyushu Plant, which produces tires for mining and construction vehicles. This upgrade will be completed by the end of 2027.

- Strategic Focus: TIREMATICS digital tire service expansion to Japanese OTR fleet vehicles; agricultural radial OTR growth through MAFF Smart Agriculture subsidy program alignment.

THE YOKOHAMA RUBBER CO., LTD.

Yokohama Rubber is one of Japan’s domestic tire manufacturers with a focused OTR portfolio serving construction and agricultural segments.

- Product Portfolio: Earthmover Tires, Loader & Dozer Tires, Grader Tires, Compactor Tires, Mobile Crane Tires, Industrial Tires.

- Recent Developments: In May 2024, The Yokohama Rubber Co., Ltd., introduced the GEOLANDAR A/T4, a standard all-terrain tire with an aggressive design that enhances the off-road driving sensation.

- Strategic Focus: Agricultural OTR expansion targeting Hokkaido’s growing large-scale farming sector.

TOYO TIRE CORPORATION

Toyo Tire Corporation is Japan’s domestic tire manufacturer with a focused mid-market OTR positioning serving Japan’s second-tier construction contractors and quarrying operators.

- Product Portfolio: Open Country M/T, Open Country R/T Pro, Open Country R/T, Open Country R/T Trail, M655, M-55, Open Country A/T III, Open Country A/T III EV, Open Country C/T, Open Country SxS, Open Country M/T-R.

- Recent Developments: In November 2025, Toyo Tire Corporation joined the Global Data Service Organisation for Tyres and Automotive Components (GDSO). As a member of GDSO, Toyo Tire advance its initiatives to promote industry standards for data related to tires to establish individual tire identification and traceability.

- Strategic Focus: Eco-OTR compound development for MLIT green construction procurement alignment; quarrying sector growth through Ube Industries and Chugoku limestone quarry partnerships.

Market Concentration Analysis

The Japan OTR tire market is highly concentrated among premium domestic and multinational brands. Bridgestone and Yokohama collectively account for approximately 45–50% of total Japan OTR tire market revenue, anchored by their vertically integrated manufacturing, extensive JATMA-certified dealer networks, and deep OEM supply partnerships with Japan’s dominant construction equipment manufacturers. The top three participants represent approximately 70–75% of total Japan OTR market value.

Market fragmentation exists in agricultural OTR and specialty segments where import brands hold 8–12% combined share through price-competitive positioning. The ultra-large OTR segment is a de facto triopoly, as their proprietary large-size manufacturing capabilities create impenetrable barriers to entry for domestic mid-tier and Chinese competitors. This ultra-large concentration generates 15–20% of total Japan OTR market value from less than 3% of total tire units.

Investment & Growth Opportunities

Fastest Growing Segments

Online channel (~6.2% CAGR), radial tire type (~4.5% CAGR), Kyushu-Okinawa region (~4.9% CAGR), ultra-large OTR above 45-inch (~6–8% CAGR driven by critical mineral mining), and smart tire/TPMS-enabled OTR (~15–20% CAGR from a small base) represent the highest-growth investment vectors through 2034. The eco-OTR compound sub-segment growing at 15–20% annually under MLIT green procurement alignment.

Emerging Geographic and Application Opportunities

Offshore wind base port construction across Japan’s designated wind energy coastal locations represents high OTR tire demand during the construction phase. Japan’s critical mineral mining expansion targeting Hokkaido, Tohoku, and Kyushu mineral extraction will deploy 50–100 ultra-large haul trucks requiring high OTR tire and systematic replacement cycles.

Technology Investment Themes

- Key technology investment themes: Smart TPMS OTR sensor-tire integration, electric construction vehicle OTR compound development, eco-compound MLIT green procurement alignment, cold-climate Hokkaido specialty compounds, and ultra-large mining OTR for critical mineral extraction.

- Strategic partnership opportunities: International OTR tire companies seeking Japan market access through construction OEM partnerships (analogous to Michelin’s Sumitomo Metal Mining exclusive relationship) represent the highest-value market entry route in Japan’s relationship-intensive industrial procurement culture.

Future Market Outlook (2026-2034)

The Japan off-the-road tire market is entering a period of structurally anchored growth through 2034. From USD 1,993.40 Million in 2025, the market will reach USD 2,913.30 Million by 2034, at a 4.31% CAGR. This growth reflects three durable structural forces that simultaneously expand Japan’s OTR tire demand base: first, MLIT’s infrastructure renewal program creating sustained public sector construction equipment deployment through 2035 at a scale Japan has not experienced since the 1970s– 1980s highway construction era, with bridges, tunnels, and road surface requiring systematic heavy equipment intervention consuming OTR tires at predictable annual volumes; second, Japan’s semiconductor manufacturing cluster investment and Woven City construction driving private sector construction equipment demand that augments rather than substitutes public sector volumes; third, Japan’s critical mineral mining strategy generating systematic demand for ultra-large OTR tires.

Research Methodology

Primary Research

Primary research included structured interviews with 110+ industry stakeholders in 2025, comprising OTR tire fleet managers at major Japanese construction contractors (Kajima, Taisei, Obayashi), mining equipment operators, agricultural equipment dealers, JATMA safety standards committee members, MLIT infrastructure project procurement officials, and regional authorized OTR tire dealer network managers across Japan’s eight OTR tire market regions.

Secondary Research

Secondary research encompassed JATMA Tire Industry Statistical Data 2024, MLIT Construction Vehicle Registration Statistics, MAFF Agricultural Equipment Subsidy Program reports, JCMA market data, company annual reports, Bloomberg specialty chemicals data, and Japan OTR tire import/export statistics from Japan Customs. Over 160 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up regional-product aggregation validated against top-down drivers. Key inputs include MLIT infrastructure budget projections, MAFF agricultural mechanization subsidy programs, JCMA equipment production forecasts, TSMC and semiconductor fab construction timelines, and rubber commodity price forward curves.

Japan Off-The-Road Tire Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Mining Vehicles, Construction and Industrial Vehicles, Agricultural Vehicles, Others |

| Tire Types Covered | Radial Tire, Bias Tire |

| Distribution Channels Covered | Online, Offline |

| Rim Sizes Covered | Below 29 Inches, 29-45 Inches, Above 45 Inches |

| End-Uses Covered | OEM, Replacement |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Bridgestone Corporation, THE YOKOHAMA RUBBER CO., LTD., TOYO TIRE CORPORATION, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan off-the-road tire market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan off-the-road tire market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan off-the-road tire industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Off-The-Road Tire Market Report

The Japan off-the-road tire market reached a value of USD 1,993.4 Million in 2025.

The market is projected to grow at a CAGR of 4.31% during 2026-2034, reaching USD 2,913.3 Million by 2034.

Key growth drivers include infrastructure development, construction equipment demand, mining activities, agricultural mechanization, replacement tire needs, and expansion of industrial and logistics sectors.

The report covers segmentation by vehicle type, tire type, distribution channel, rim size, end-use, and region. Each segment includes detailed market size and forecast analysis.

Key trends include adoption of durable radial tires, smart tire monitoring systems, sustainable materials usage, retreading practices, and increasing demand for high-performance specialty tires

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)