Japan Online Gambling Market Size, Share, Trends and Forecast by Game Type, Device, and Region, 2026-2034

Japan Online Gambling Market Size, Share, Trends & Forecast (2026-2034)

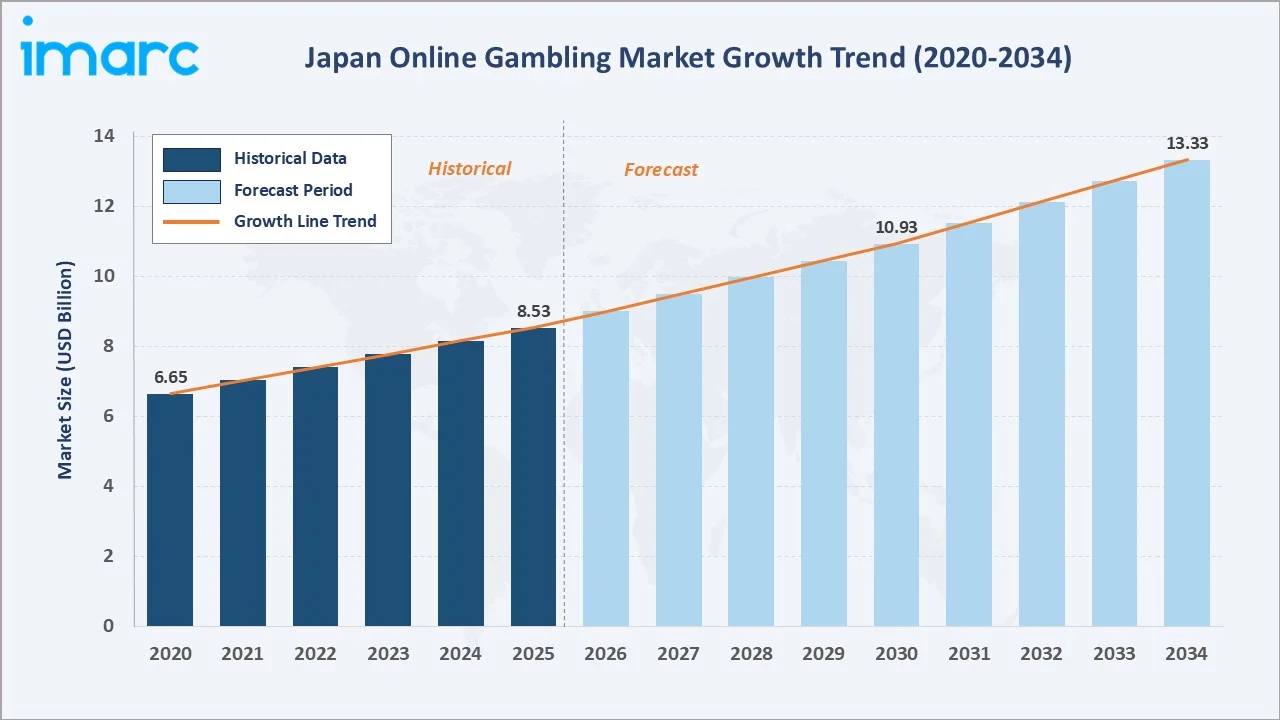

The Japan online gambling market size reached USD 8.53 Billion in 2025 and is projected to reach USD 13.33 Billion by 2034, exhibiting a CAGR of 5.09% during 2026-2034. Expanding digital infrastructure, smartphone penetration, and the evolving regulatory environment with integrated resort development are the primary forces driving market growth.

Casino leads the game type segment at 52% in 2025, while mobile devices dominate device access at 65%. The Kanto Region commands a leading 30% regional share in 2025, reflecting Tokyo's dense, tech-savvy population and robust digital ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.53 Billion |

|

Forecast Market Size (2034) |

USD 13.33 Billion |

|

CAGR (2026-2034) |

5.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (30% share, 2025) |

|

Second Region |

Kinki Region (22.5% share, 2025) |

|

Leading Game Type |

Casino (52%, 2025) |

|

Leading Device |

Mobile (65%, 2025) |

The Japan online gambling market growth trajectory from 2020 through 2034, with historical expansion to USD 8.53 Billion in 2025, reflects sustained digital-connectivity-driven demand, while the forecast to USD 13.33 Billion captures accelerating mobile gaming investment, crypto-enabled betting, and integrated resort development.

To get more information on this market, Request Sample

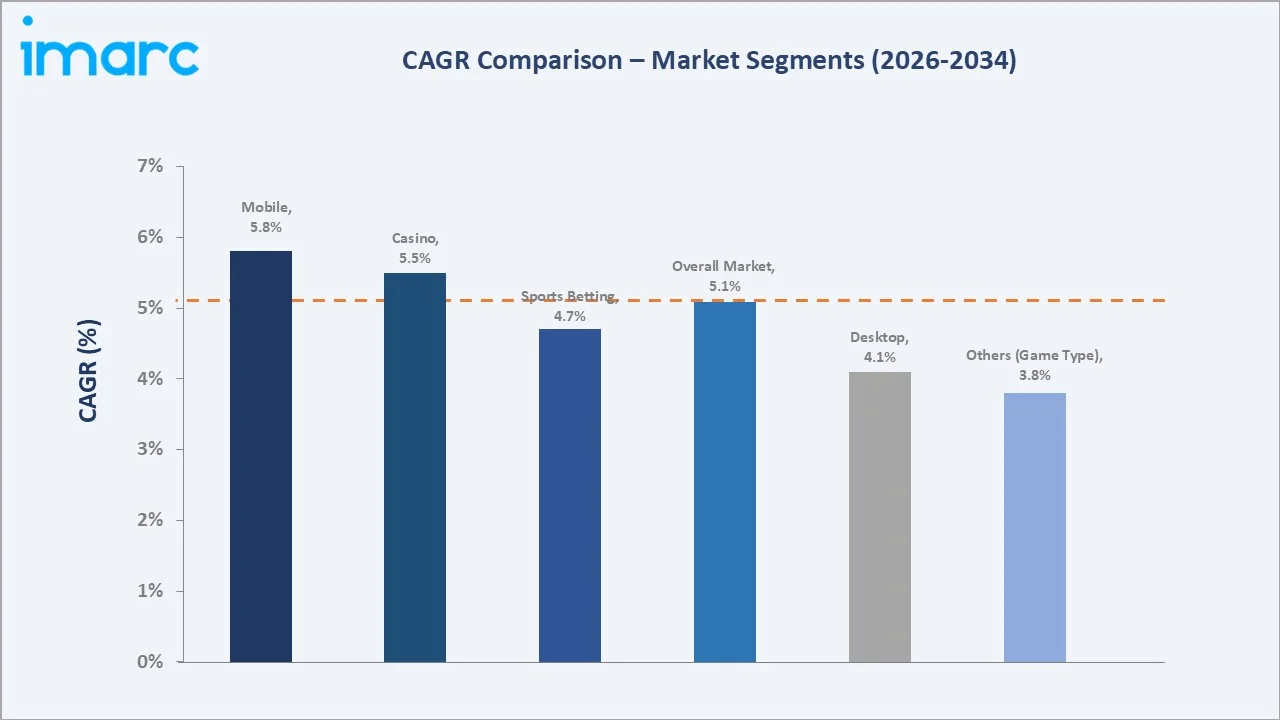

The CAGR trajectories across key game type, device, and regional sub-segments, with mobile at ~5.8% CAGR and casino at ~5.5% CAGR, are the fastest-growing categories within the Japan online gambling industry analysis through 2034.

Executive Summary

The Japan online gambling market is on a sustained growth trajectory from USD 8.53 Billion in 2025 to USD 13.33 Billion by 2034. Online gambling, an evolving entertainment sector encompassing casino games, sports betting, and other digital wagering activities, benefits from Japan's world-class digital infrastructure and shifting consumer preferences toward interactive digital entertainment.

Casino dominates game type at 52% in 2025, driven by the strong appeal of live dealer experiences, baccarat, blackjack, poker, and digital slots among Japanese players. Sports betting (32%) capitalizes on Japan's deeply rooted horse racing culture and growing e-sports engagement, growing steadily through 2034.

Mobile devices lead access at 65% in 2025, reflecting Japan's exceptional smartphone penetration and advanced mobile payment infrastructure.

The Kanto Region dominates at 30% in 2025, anchored by Tokyo's dense population of digitally connected consumers. Kinki Region (22.5%) and Central/Chubu Region (15.8%) follow, driven by Osaka and Nagoya's urban digital ecosystems and growing appetite for online entertainment platforms.

Key Market Insights

|

Insight |

Data |

|

Largest Game Type |

Casino - 52% share (2025) |

|

Leading Device |

Mobile - 65% share (2025) |

|

Leading Region |

Kanto Region - 30% revenue share (2025) |

|

Second Region |

Kinki Region - 22.5% revenue share (2025) |

|

Top Companies |

Bet365, Entain |

Key Analytical Observations Expanding On The Above Data:

- Casino's 52% dominance in 2025reflects the broad appeal of live dealer formats, culturally localized themes drawing on anime and manga aesthetics, and blockchain-enabled transparent transactions that resonate with Japan's tech-savvy gambling audience.

- Mobile's 65% share in 2025 reflects Japan's exceptional smartphone penetration rate and 5G deployment across major urban centers, enabling real-time streaming, live dealer interactions, and seamless multi-platform gambling experiences for on-the-go users.

- The Kanto Region's 30% dominance reflects Tokyo's position as Japan's economic and cultural epicenter, concentrating the nation's largest population of digitally connected consumers with high disposable income and robust digital payment infrastructure.

- Kinki Region's 22.5% share benefits from Osaka's role as Japan's second-largest metropolitan area and the planned MGM Osaka integrated resort development on Yumeshima Island, expected to reshape the gaming perception landscape by 2030.

Japan Online Gambling Market Overview

Online gambling encompasses digital wagering activities conducted through internet-connected devices, spanning casino-style games (live dealer, slots, table games), sports betting, lottery, and other interactive wagering formats. In Japan's context, the market operates in a complex regulatory environment where most gambling forms remain legally restricted under the Penal Code, driving significant offshore platform activity targeting Japanese users.

The Japan ecosystem integrates international game developers, offshore platform operators, digital payment providers, marketing affiliates, responsible gambling organizations, and regulatory bodies. The market's structure reflects a unique interplay between strict domestic legal restrictions and the practical reality of significant user participation on offshore platforms offering Japanese-language interfaces and yen-based transactions.

Market Dynamics

To evaluate market opportunities, Request Sample

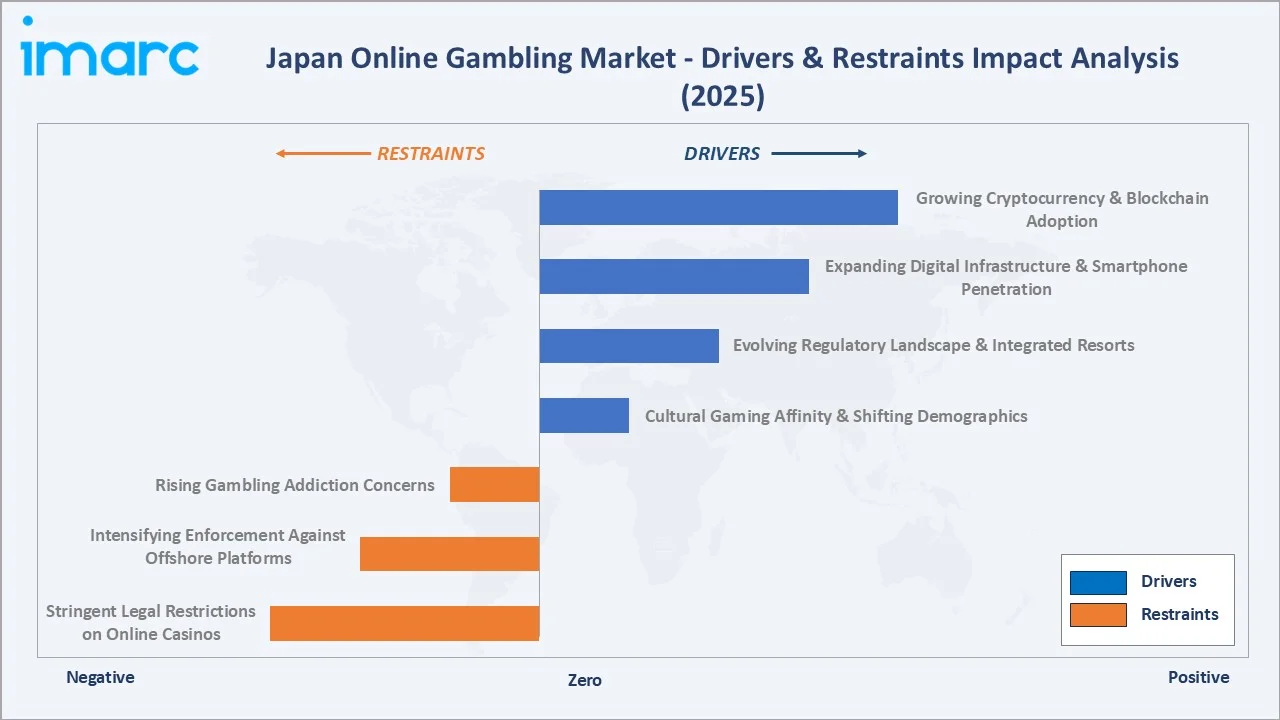

Market Drivers

- Expanding Digital Infrastructure and Smartphone Penetration: Japan's world-class digital infrastructure, with approximately 109 million internet users and 88.2% online penetration at the start of 2025, serves as a foundational growth driver. Widespread 5G deployment across urban centers significantly enhances mobile gaming capabilities, enabling real-time streaming and live dealer interactions that drive online gambling participation.

- Evolving Regulatory Landscape and Integrated Resort Development: Japan's gambling regulatory landscape is evolving, with progress toward regulated casino infrastructure legitimizing the sector and attracting institutional investment. The MGM Osaka integrated resort development on Yumeshima Island, commencing construction in April 2025, signals a significant regulatory shift that is reshaping public perception of gambling activities.

- Cultural Gaming Affinity and Shifting Demographic Preferences: Japan's long-standing cultural engagement with gaming, from traditional horse racing and pachinko to modern digital entertainment, provides a strong base for online gambling expansion. In 2024, total consumer spending across all gaming platforms reached an estimated $16 billion (2.4 trillion yen), according to the 2025 edition of the Famitsu Game Hakusho published by Kadokawa ASCII Research Laboratories. Younger demographics increasingly favor digital platforms with anime-inspired visuals and gamification features, creating a natural pathway for online gambling operators to attract digitally engaged users.

Market Restraints

- Stringent Legal Restrictions on Online Casino Operations: The Penal Code of Japan prohibits most gambling forms, with online casino activities legally restricted. This regulatory framework compels operators to function as offshore platforms, creating both regulatory and operational ambiguity for market participants and limiting the development of domestically regulated online gambling infrastructure.

- Intensifying Enforcement Against Offshore Gambling Platforms: Japanese authorities have intensified crackdowns on offshore gambling organizations and their domestic clientele. The revised Basic Law on Measures against Addiction, effective September 2025, explicitly prohibits online casino establishment operations and associated advertising, with active international coordination to restrict access to unlicensed platforms.

Market Opportunities

- Cryptocurrency and Blockchain-Enabled Gambling Growth: Growing adoption of cryptocurrency payments among Japanese online gambling users, attracted by enhanced privacy, faster processing, and blockchain-based transparency, is expanding the addressable market. Japan's openness toward innovative financial technologies creates favorable conditions for crypto-native gambling platforms to capture users seeking alternative transaction methods.

- Integrated Resort Development and Market Legitimization: MGM Osaka's development and Japan's broader integrated resort framework present significant opportunities for market participants to benefit from regulatory normalization and improved public perception. The anticipated opening by autumn 2030 is expected to strengthen governance frameworks and create favorable conditions for adjacent online gambling platform development.

Market Challenges

- Rising Gambling Addiction Concerns Among Younger Demographics: The rapid growth of online gambling among younger Japanese citizens has intensified regulatory scrutiny and societal concern. Stricter advertising bans, including prohibitions on celebrity endorsements and social media promotions under the revised Basic Law, constrain operators' marketing capabilities and limit user acquisition strategies.

- Legal Uncertainty Surrounding Cryptocurrency Gambling Transactions: Despite growing user adoption, cryptocurrency-based gambling transactions face increasing regulatory scrutiny in Japan. The intersection of gambling laws and cryptocurrency regulations creates compliance complexity for operators, with authorities actively investigating fund transfer methods associated with offshore gambling platforms.

Emerging Market Trends

1. Rise of Cryptocurrency and Blockchain-Based Gambling Transactions

Japanese online gambling users are increasingly turning to cryptocurrencies for transactions, attracted by greater privacy, quicker processing, and blockchain-enabled security. The use of digital assets aligns with Japan's openness toward innovative payment solutions. In November 2024, Japanese authorities referred 57 individuals to prosecutors for offshore online casino gambling using cryptocurrencies, underscoring both the scale of crypto-based gambling activity and intensifying regulatory supervision.

2. Integration of Artificial Intelligence and Virtual Reality for Enhanced Experiences

Online gambling platforms targeting Japanese users are increasingly adopting AI and VR to create personalized and immersive gaming experiences. AI-powered systems tailor game suggestions based on user behavior, while VR features replicate physical casino atmospheres digitally. Japan's advanced digital infrastructure supports these technologies, enhancing engagement and accessibility while reshaping the competitive positioning of platform operators.

3. Growing Influence of Social Media and Influencer-Driven Marketing

Japanese gambling operators are increasingly leveraging social media and influencer collaborations to reach specific audience segments, particularly younger users engaging with sports through digital platforms. The revised Basic Law's advertising restrictions have prompted operators to develop alternative engagement strategies, including interactive campaigns and special offers designed to attract and retain users within regulatory constraints.

4. Mobile Gaming Culture Driving Platform Investment

Japan's broader mobile gaming culture, with the Japan mobile gaming market reaching USD 7.5 Billion in 2024 and projected to reach USD 19.6 Billion by 2033, creates a natural crossover audience for mobile online gambling platforms. Operators have invested heavily in responsive mobile applications with Japanese language support, localized payment methods, and live streaming capabilities that capitalize on Japan's mobile-first digital behavior patterns.

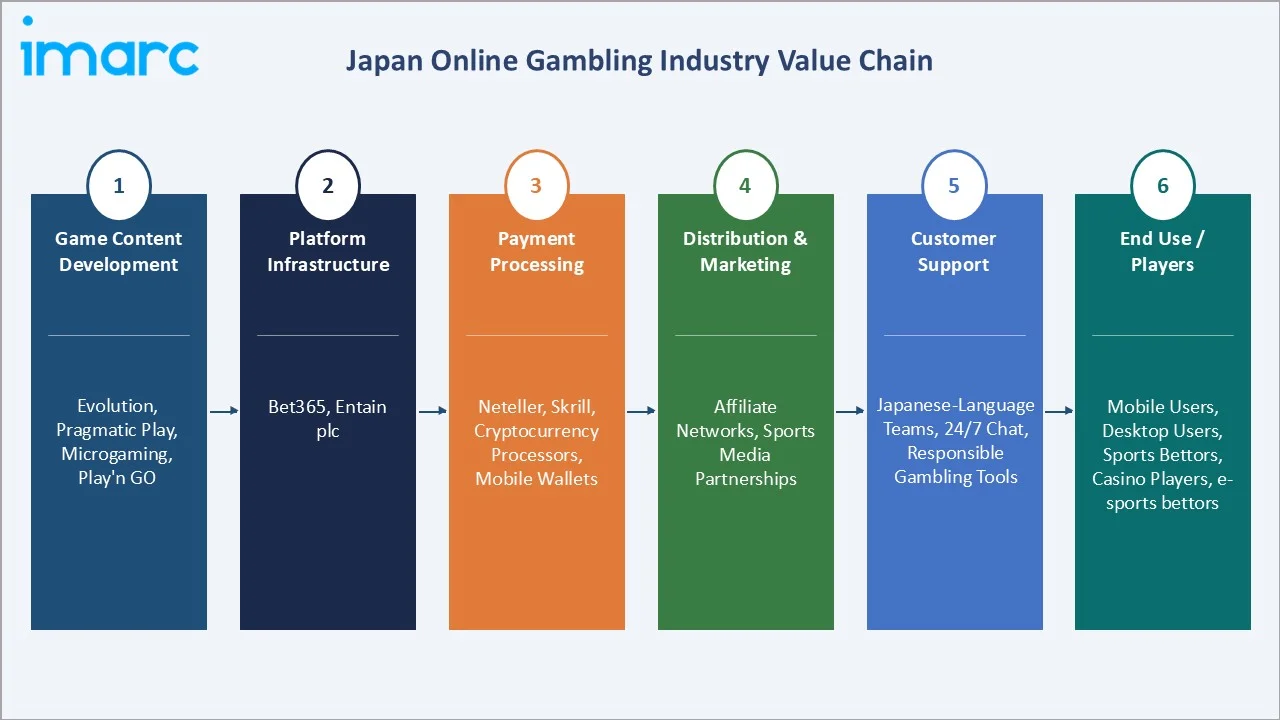

Industry Value Chain Analysis

The Japan online gambling value chain spans six stages from game content development through end-user engagement. Platform infrastructure and payment processing capture the highest value-add margins, while marketing and customer acquisition generate significant ongoing investment requirements that favor well-capitalized international operators over new market entrants.

|

Stage |

Key Players / Examples |

|

Game Content Development |

Evolution, Pragmatic Play, Microgaming, Play'n GO |

|

Platform Infrastructure |

Bet365, Entain plc |

|

Payment Processing |

Neteller, Skrill, cryptocurrency processors, mobile wallet providers |

|

Distribution & Marketing |

Affiliate marketing networks, sports media partnerships |

|

Customer Support |

Japanese-language support teams, 24/7 chat services, responsible gambling tools |

|

End Use / Players |

Mobile users, desktop users, sports bettors, casino players, e-sports bettors |

Integrated platform operators with proprietary game libraries, multi-currency payment capabilities, and established Japanese-language support teams achieve stronger user retention and lifetime value metrics than single-vertical operators. Vertical integration across game content and platform infrastructure is a meaningful competitive advantage in a market were user experience quality and payment reliability drive platform loyalty.

Technology Landscape in the Japan Online Gambling Industry

Live Dealer Technology and Real-Time Streaming Infrastructure

Live dealer technology represents the most significant technological differentiator in Japan's online gambling market, enabling real-time studio-based casino experiences that replicate physical gaming venue interactions. High-definition streaming infrastructure, low-latency video delivery optimized for Japan's 5G networks, and multi-language dealer capabilities with Japanese-speaking hosts drive strong user engagement and premium revenue per player metrics.

Blockchain Integration and Smart Contract-Based Gaming

Blockchain technology is progressively entering Japan's online gambling ecosystem, enabling provably fair gaming mechanics, transparent transaction records, and smart contract-based payout automation. Decentralized gambling protocols that remove operator intermediaries and enable direct player-to-player wagering are attracting technically sophisticated users who prioritize transparency and reduced counterparty risk in gambling transactions.

Mobile Application Technology and Progressive Web Apps

Japanese online gambling operators have invested heavily in native mobile application development and progressive web app (PWA) technology optimized for iOS and Android environments. Advanced features including push notification betting alerts, biometric authentication integration, seamless QR-code-based payment flows, and offline-capable game previews reduce friction in the user experience and drive session frequency increases.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Game Type |

Casino |

52.0% |

2025 |

|

Device |

Mobile |

65.0% |

2025 |

|

Region |

Kanto Region |

30.0% |

2025 |

By Game Type

To access detailed market analysis, Request Sample

Casino commands a 52.0% majority share in 2025 owing to its diverse offering depth, culturally localized presentation, and the immersive quality of live dealer formats. The strong preference for baccarat and slots among Japanese players, combined with offshore platforms' investment in anime-themed and manga-styled game variants, establishes casino as the dominant and fastest-growing game type category.

Sports betting at 32.0% in 2025 capitalizes on Japan's deeply embedded horse racing culture, growing e-sports viewership, and football betting participation. The legal horse racing, bicycle racing, motorboat racing, and motorcycle racing channels provide a regulated foundation that normalizes sports betting participation. Others (16.0%) encompasses lottery-style products, virtual sports, and emerging formats.

By Device

Mobile devices lead the device segment at 65.0% in 2025, driven by Japan's exceptional smartphone penetration and 5G network deployment. The convenience of on-the-go gaming, combined with sophisticated mobile payment ecosystems and operators' investment in responsive mobile applications with Japanese language support, makes smartphones the preferred platform for both casual and regular gambling participants.

Desktop at 28.0% in 2025 remains preferred for longer gaming sessions, particularly live dealer casino formats where larger screens enhance the immersive experience quality. Others (7.0%) encompasses tablet devices, smart TVs, and emerging gaming console platforms, representing a nascent but growing access channel as connected entertainment ecosystems expand across Japanese households.

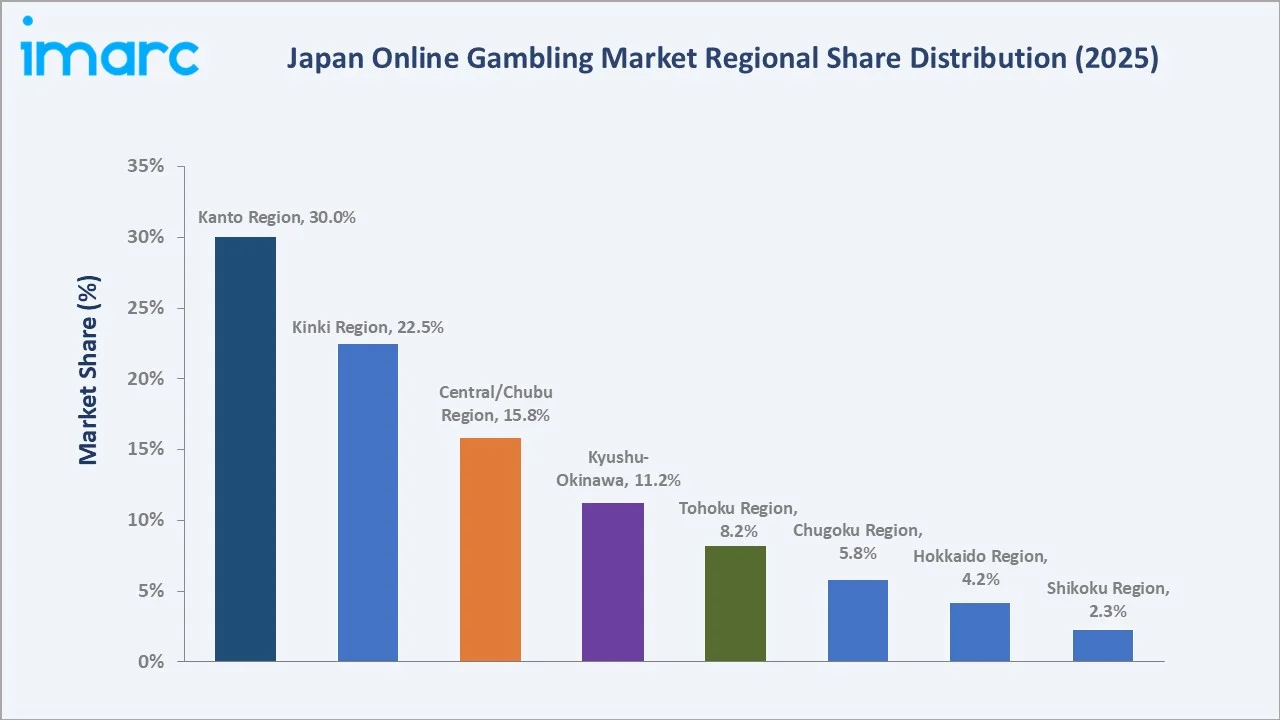

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

30.0% |

Tokyo tech-savvy population; high-speed digital infrastructure; strong casino and mobile gaming demand |

|

Kinki Region |

22.5% |

Osaka integrated resort development; Osaka-Kobe-Kyoto metro digital engagement; sports betting culture |

|

Central/Chubu Region |

15.8% |

Nagoya manufacturing hub digital connectivity; growing mobile gambling adoption; young professional demographics |

|

Kyushu-Okinawa Region |

11.2% |

Fukuoka digital economy growth; tourism-adjacent gaming culture; expanding 5G infrastructure |

|

Tohoku Region |

8.2% |

Post-reconstruction digital infrastructure investment; Sendai urban digital adoption; mobile platform growth |

|

Chugoku Region |

5.8% |

Hiroshima digital expansion; improving broadband connectivity; incremental mobile gambling adoption |

|

Hokkaido Region |

4.2% |

Sapporo urban digital infrastructure; tourism-linked gambling activity; gradual mobile penetration growth |

|

Shikoku Region |

2.3% |

Emerging digital connectivity; smaller urban population base; incremental online gambling adoption |

The Kanto Region's 30% market dominance in 2025 is driven by Tokyo's exceptional concentration of digitally connected consumers with high disposable income and advanced internet infrastructure. The region hosts Japan's largest base of traditional gambling enthusiasts, particularly in horse racing, who are progressively transitioning to online platforms as mobile-optimized experiences improve.

The Kinki Region, with 22.5% in 2025, benefits from Osaka's planned MGM integrated resort development, which is expected to reshape the broader gaming perception landscape and drive increased interest in related online gambling platforms. The Osaka-Kobe-Kyoto metropolitan corridor creates a dense digital consumer base with strong engagement in both sports and casino-style gambling formats.

Competitive Landscape

The Japan online gambling market exhibits a complex and dynamic competitive landscape shaped by strict domestic regulations and the proliferation of offshore operators targeting Japanese users. International platforms compete aggressively through localized features including Japanese language interfaces, yen-based transaction processing, culturally adapted game themes, and region-specific payment methods encompassing cryptocurrency and mobile wallets.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Bet365 |

Sports betting, casino, live dealer, poker, bingo |

Leader |

Global leader; Japan-localized interface; crypto payments |

|

Entain |

Coral, Ladbrokes, bwin, partypoker brands |

Leader |

Multi-brand global; sports & casino; Japan affiliate |

Key players include Bet365, Entain, and others.

Key Company Profiles

Bet365

Bet365 is one of the world's largest online gambling companies, headquartered in Stoke-on-Trent, United Kingdom. The company operates one of the most comprehensive gambling platforms globally, offering sports betting, casino, poker, bingo, and live streaming services across multiple languages including Japanese. Its technologically advanced platform and extensive sports coverage make it a primary destination for Japanese online gambling users.

- Product Portfolio: Offers sports betting covering global sports including Japanese horse racing and football, live casino with Japanese-language dealers, slots and table games, and virtual sports betting.

- Recent Developments: In March 2026, bet365 announced a landmark multi-year agreement with Ultimate Fighting Championship, becoming the official sports betting partner.

- Strategic Focus: Bet365's strategy leverages its industry-leading sports betting depth, comprehensive live streaming capabilities, and Japanese-language platform localization to maintain market share among Japanese users, while investing in crypto payment integration and mobile application performance optimization to align with evolving user preferences.

Entain

Entain is a leading global sports betting and gaming entertainment company operating numerous well-known brands including Coral, Ladbrokes, bwin, and partypoker. The company's technology-led approach and multi-brand portfolio enable targeted engagement across distinct Japanese user segments, from sports bettors to casino enthusiasts, with localized content and culturally resonant marketing approaches.

- Product Portfolio: Operates multiple brands offering sports betting with comprehensive Japanese sports coverage, live casino with dedicated Asian gaming content, online poker, and virtual sports.

- Recent Developments: In May 2024, BetMGM, a JV between Entain and MGM Resorts International, announced the rollout of new baseball-focused betting features, including expanded home run markets, enhanced parlay options, and a Grand Slam Jackpot contest. The company stated that the integration of advanced analytics capabilities significantly improved the betting experience, offering users a wider range of wagering options and more dynamic engagement during games.

- Strategic Focus: Entain's multi-brand strategy enables precise audience segmentation in the Japanese market, targeting distinct user cohorts with brand-specific product propositions, while its BetTech platform licensing model creates additional revenue opportunities from third-party operator partnerships targeting Japanese users.

Market Concentration Analysis

The Japan online gambling market is moderately fragmented at the operator level, with no single platform holding more than 10-12% of estimated active Japanese user share. International platforms compete vigorously through localization quality, payment method breadth, promotional generosity, and game content depth, creating a competitive landscape where user switching costs are relatively low and platform loyalty requires continuous investment.

Consolidation through M&A is ongoing among global operators, creating larger entities with greater technology investment capacity and brand portfolio breadth. Japan's regulatory evolution toward integrated resort development is expected to attract further institutional investment that could reshape competitive concentration over the 2026-2034 forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Mobile gambling at ~5.8% CAGR through 2034 is the highest-growth access channel segment, driven by 5G deployment, mobile payment ecosystem advancement, and Japan's mobile-first digital lifestyle. Casino gaming at ~5.5% CAGR represents the broadest-based revenue growth opportunity, combining established user preference with technological innovation in live dealer and blockchain-enabled gaming formats.

Emerging Opportunities

The Kinki Region's MGM Osaka integrated resort development represents the most significant emerging opportunity in Japan's broader gaming ecosystem. The JPY 1.27 trillion project, with planned opening by autumn 2030, is expected to legitimize gambling participation more broadly and stimulate complementary online gambling platform growth. Crypto-native gambling platforms targeting Japan's approximately 11 million cryptocurrency owners represent a high-value, underserved segment.

Venture & Investment Trends

Private equity and strategic investment in online gambling technology companies serving Asia-Pacific markets is growing, driven by the region's superior CAGR profile relative to saturated European markets. Investment in responsible gambling AI technology is strategically positioned ahead of anticipated Japanese regulatory requirements, with compliance-ready platforms expected to command preference advantages as formal regulation of online activities progresses.

Future Market Outlook (2026-2034)

The Japan online gambling market is forecast to expand from USD 8.53 Billion in 2025 to USD 13.33 Billion by 2034 at a CAGR of 5.09%, adding USD 4.80 Billion in incremental annual market value over the forecast period. This sustained growth reflects the market's digital-connectivity-driven demand characteristics and Japan's progressive regulatory evolution.

Three technological forces will most significantly shape the Japan online gambling industry landscape through 2034. The integration of AI-powered personalization and VR casino environments will create premium gaming experiences that command higher revenue per user. Cryptocurrency and blockchain-based gaming protocols will capture a growing share of transaction volume, particularly among younger demographics. The MGM Osaka integrated resort's 2030 opening will reshape public and regulatory attitudes toward gambling, creating a more favorable environment for complementary online platform development.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024-2025 with Japan online gambling industry stakeholders, including platform executives, digital payment specialists, sports betting operators, responsible gambling practitioners, and regulatory affairs specialist’s familiar with Japan's evolving gaming legal framework. Primary data validated market sizing, game type and device segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Japan National Police Agency gambling investigation reports, Ministry of Internal Affairs and Communications internet usage statistics, Japan Internet Provider Association connectivity data, Gambling Commission international comparative data, IMARC Group primary market databases, and trade publications including iGaming Business, Gambling Insider, and Japan Times digital economy coverage.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, internet penetration indices, consumer expenditure data on entertainment, and historical market evolution patterns. Scenario analysis was performed to account for regulatory uncertainty, with base, optimistic (integrated resort acceleration), and conservative (regulatory tightening) cases informing the central forecast.

Japan Online Gambling Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Game Types Covered |

|

| Devices Covered | Desktop, Mobile, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Bet365, Entain, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Online Gambling Market Report

The Japan online gambling market reached USD 8.53 Billion in 2025, reflecting sustained demand from mobile platform engagement, casino game adoption, and sports betting participation across Japan's highly digitally connected population.

The market is projected to reach USD 13.33 Billion by 2034, growing at a CAGR of 5.09% during 2026-2034, driven by mobile gaming expansion, cryptocurrency payment adoption, integrated resort development, and continued growth in live dealer casino formats.

Casino leads with a 52% game type share in 2025, valued for its culturally localized content, immersive live dealer formats, and broad game variety including baccarat, blackjack, poker, and slots that resonate strongly with Japanese players.

Mobile leads at 65% in 2025, reflecting Japan's high smartphone penetration rate, advanced mobile internet infrastructure including 5G deployment, and operators' investment in Japanese-language mobile applications with seamless digital payment integration.

The Kanto Region commands a leading 30% market share in 2025, driven by Tokyo's dense, tech-savvy population, superior digital infrastructure, high disposable income levels, and strong cultural engagement with both traditional and online gambling platforms.

Casino is the fastest-growing game type at ~5.5% CAGR through 2034, driven by continued investment in live dealer technology, AI personalization, blockchain-enabled transparency, and culturally tailored game themes that resonate with Japanese user preferences.

Leading companies include Bet365 and Entain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)