Japan Perovskite Solar Cell Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Japan Perovskite Solar Cell Market Summary:

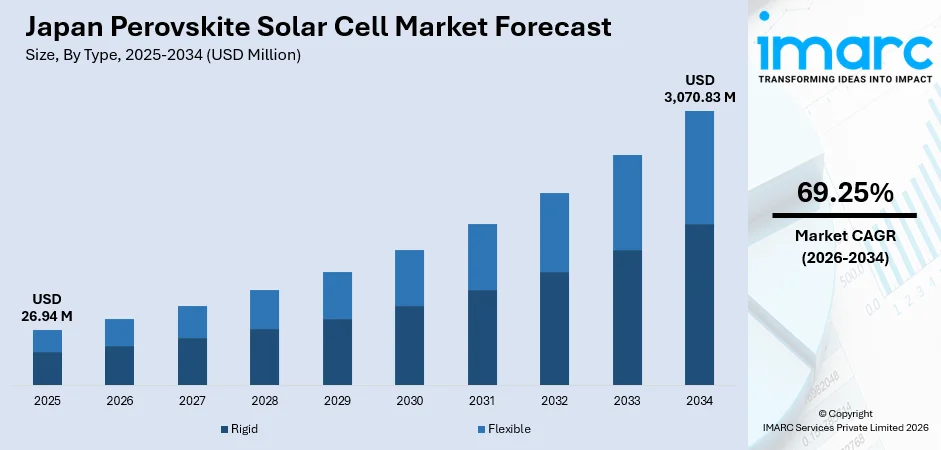

The Japan perovskite solar cell market size was valued at USD 26.94 Million in 2025 and is projected to reach USD 3,070.83 Million by 2034, growing at a compound annual growth rate of 69.25% during 2026-2034.

The Japan perovskite solar cell market is advancing at a notable pace, driven by strong government policy commitment, increasing research and development (R&D) investment, and the growing demand for lightweight and flexible solar solutions in space-constrained urban environments. Rising corporate activity in manufacturing scale-up, expanding building-integrated applications, and Japan's iodine-rich domestic supply chain are collectively contributing to the Japan perovskite solar cell market share.

Key Takeaways and Insights:

- By Type: Rigid dominates the market with a share of 61.3% in 2025, driven by its superior conversion efficiency and structural advantages that align with large-scale building-integrated and commercial power generation applications.

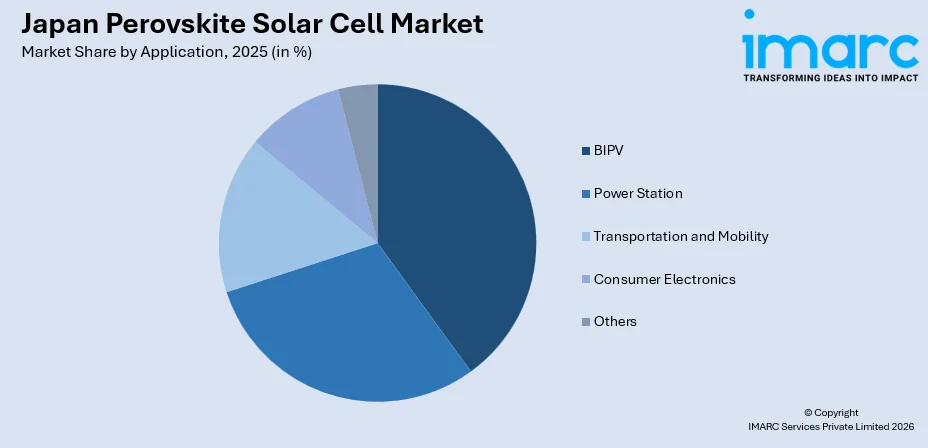

- By Application: BIPV leads the market with a share of 34.7% in 2025, underpinned by the growing demand for power-generating glass and wall-mounted solar solutions across Japan's dense urban commercial and residential building stock.

- By Region: Kanto Region represents the largest segment with a market share of 38.5% in 2025, owing to its concentration of research institutions, major corporate headquarters, high-value construction activity, and strong government-backed pilot project deployments.

- Key Players: The Japan perovskite solar cell market features an active competitive landscape comprising specialist materials companies, electronics conglomerates, and university spin-offs investing in film-type, glass-type, and tandem perovskite technologies across research, demonstration, and early commercial stages.

To get more information on this market Request Sample

The Japan perovskite solar cell market is gaining momentum due to strong policy support, ongoing technological advancements, and rising demand for flexible and lightweight solar solutions. Government initiatives are playing a central role in accelerating commercialization and encouraging early adoption across diverse applications, including building-integrated systems. For example, in 2025, Japan introduced two subsidy programs to promote perovskite deployment and battery-integrated solutions, offering financial support for lightweight film-type modules and higher incentives for critical infrastructure, such as evacuation centers. This move was aimed at scaling adoption, lowering overall system costs, and progressing toward national capacity targets. Additionally, collaboration between research institutions and industry players, along with increasing focus on energy security and decentralized power generation, is further strengthening the market growth prospects across residential, commercial, and infrastructure segments.

Japan Perovskite Solar Cell Market Trends:

Government-Backed Industrial Scaling and Multi-Player Commercialization

Strong government funding is accelerating the transition of perovskite solar cells from research to commercial-scale production in Japan. Public investment is enabling multiple domestic players to advance parallel technology pathways, reducing dependence on a single approach. In 2025, Japan’s Ministry of Economy, Trade and Industry allocated ¥24.6 billion to Panasonic, Ricoh, and EneCoat to scale production and advance both glass-based and flexible film technologies. This coordinated support is strengthening domestic supply chains, enabling capacity expansion, and aligning industry efforts with national targets, thereby improving commercialization readiness across multiple application segments.

Emergence of Dedicated Manufacturing Infrastructure for Flexible Solar Films

The development of specialized production facilities is supporting the transition toward scalable and cost-efficient manufacturing of perovskite technologies. Companies are investing in dedicated infrastructure to commercialize lightweight and flexible modules suited for unconventional surfaces. In 2024, Sekisui Chemical announced plans to establish a 100 MW production line by repurposing Sharp’s Osaka facility and launching SEKISUI SOLAR FILM. This reflects a broader trend of leveraging existing industrial assets to accelerate production readiness while targeting applications, such as low load-bearing rooftops and public infrastructure, with gradual expansion into private-sector buildings as scale improves.

Advancements in Low-Cost and Scalable Production Techniques

Innovations in production processes are playing a crucial role in improving the commercial viability of perovskite solar cells. New manufacturing methods are being developed to enhance efficiency, reduce material damage, and lower overall production costs. For example, in 2025, Sumitomo Heavy Industries developed a low-temperature plasma-based method (RPD) to manufacture key layers in perovskite solar cells more efficiently. The process enabled faster production, reduces material damage, and lowers costs significantly compared to conventional high-temperature methods. This advancement supports scalable manufacturing and could accelerate commercialization of perovskite solar technology.

Market Outlook 2026-2034:

The Japan perovskite solar cell market is projected to deliver notable revenue growth throughout the forecast period, supported by strong government backing, rising investments in next-generation photovoltaics, and increasing demand for lightweight, flexible solar solutions. The market generated a revenue of USD 26.94 Million in 2025 and is projected to reach a revenue of USD 3,070.83 Million by 2034, growing at a compound annual growth rate of 69.25% from 2026-2034. Ongoing research advancements, improved efficiency levels, and commercialization efforts by domestic players are further accelerating adoption across building-integrated and portable energy applications.

Japan Perovskite Solar Cell Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Rigid |

61.3% |

|

Application |

BIPV |

34.7% |

|

Region |

Kanto Region |

38.5% |

Type Insights:

- Rigid

- Flexible

Rigid dominates with a market share of 61.3% of the total Japan perovskite solar cell market in 2025.

Rigid holds the biggest market share attributed to its structural stability and ease of integration into conventional solar module systems. These cells offer better durability and consistent performance, making them suitable for large-scale installations and building-integrated applications. Manufacturers prefer rigid formats as they align well with existing production processes and infrastructure, reducing transition complexity. Additionally, rigid perovskite cells provide improved protection against environmental factors such as moisture and mechanical stress, ensuring longer operational life. Their compatibility with established installation techniques further supports adoption across commercial and industrial projects, strengthening their position in Japan’s evolving solar energy market.

The dominate of the segment is further reinforced by the ongoing advancements in efficiency and reliability. Research and development efforts are focused on enhancing stability and scalability, making rigid formats more commercially viable. These cells are increasingly used in pilot projects and early-stage deployments, where performance consistency is critical. The presence of strong manufacturing capabilities and material innovation in Japan further supports their growth. Additionally, partnerships between technology developers and energy companies are accelerating commercialization. As demand for dependable and high-performance solar solutions increases, rigid perovskite cells remain the preferred choice, reinforcing their leadership in the Japan perovskite solar cell market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- BIPV

- Power Station

- Transportation and Mobility

- Consumer Electronics

- Others

BIPV leads with a market share of 34.7% of the total Japan perovskite solar cell market in 2025.

BIPV represents the largest segment because of its excellent compatibility with urban infrastructure and space limitations. In crowded urban areas, embedding solar cells straight into building materials like windows, facades, and rooftops facilitates effective energy production without the need for extra land. Perovskite solar cells, recognized for being lightweight, flexible, and semi-transparent, are especially ideal for these applications. This allows for smooth integration into contemporary architectural styles without compromising visual appeal. Moreover, increasing attention to energy-efficient structures and carbon reduction goals is promoting the use of integrated solar solutions, positioning BIPV as a favored option in both commercial and residential projects.

BIPV remains the market leader, bolstered by increasing investments in green building and energy-efficient city infrastructure. Developers are progressively incorporating solar technologies into construction materials to comply with regulations and improve energy efficiency. In 2023, Panasonic launched a long-term demonstration initiative in Fujisawa Sustainable Smart Town, evaluating perovskite photovoltaic glass for windows and balconies to enhance efficiency and longevity. This advancement underscores increasing cooperation within the industry and strengthens the position of BIPV as a viable option for urban solar integration and distributed energy production.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region exhibits a clear dominance with a 38.5% share of the total Japan perovskite solar cell market in 2025.

Kanto Region leads the market owing to its high concentration of research facilities, technology firms, and governmental backing for innovative energy solutions. Tokyo and its nearby regions are home to top universities, R&D facilities, and corporate headquarters engaged in advanced solar technologies. This ecosystem promotes innovation, pilot programs, and commercialization of perovskite solar technologies. Moreover, increased energy requirements in heavily populated cities boosts the necessity for efficient and compact solar options. Government-supported initiatives and financing programs enhance deployment, establishing Kanto as an important center for progress and acceptance in Japan’s advancing renewable energy sector.

The Kanto Region also advantages from its developed infrastructure and prompt embrace of new technologies. The area gains from solid cooperation among academic institutions, industry stakeholders, and public entities, facilitating quicker testing and expansion of innovative solar technologies. Urban uses like building-integrated photovoltaics are gaining momentum, bolstered by tall structures and smart city projects. Furthermore, the existence of prominent electronics and materials firms enhances supply chain efficiency and fosters technological progress. Supportive policy structures and investments in the clean energy shift further strengthen Kanto’s leadership, placing it at the leading edge of Japan’s perovskite solar cell market.

Market Dynamics:

Growth Drivers:

Why is the Japan Perovskite Solar Cell Market Growing?

Expansion into Advanced and Space-Based Energy Applications

Perovskite solar technology is expanding into advanced applications, particularly in aerospace environments where lightweight and flexible power solutions are critical. In 2025, Ricoh installed its perovskite solar cells on JAXA’s HTV-X1 spacecraft for in-orbit testing to evaluate durability and efficiency under space conditions. This development demonstrated the growing confidence in the technology’s performance in extreme environments and highlights its potential beyond terrestrial applications. Such advancements position perovskite cells as a viable option for next-generation energy systems, supporting Japan’s ambitions in both space exploration and specialized high-performance energy use cases.

Validation of Performance in Challenging Environmental Conditions

Real-world testing in harsh environments is becoming essential to validate the durability and reliability of perovskite solar modules. In 2025, a consortium including Macnica, Reiko, and Peccell Technologies initiated pilot testing of lightweight flexible modules at Yokohama’s Osanbashi Pier under demanding coastal conditions. The project evaluated efficiency, durability, and installation methods using roll-to-roll manufactured panels on advanced substrates. This reflects efforts to demonstrate performance across challenging infrastructure settings such as ports and transport systems, helping build confidence among end users and expanding the potential deployment scope across diverse environments.

Integration into Indoor and Low-Light Commercial Environments

Perovskite solar cells are increasingly being integrated into indoor and low-light environments, enabling new commercial applications. In 2024, H.I.S., Saule Technologies, and Lawson launched a pilot project in Tokyo to test film-based cells within a retail store, powering electronic shelf labels and interior systems using indoor light. This trend highlights the ability of perovskite technology to function beyond traditional outdoor installations, supporting energy efficiency within commercial spaces. Such applications reduce dependence on conventional power sources while opening new avenues for integrating solar technology into everyday indoor environments.

Market Restraints:

What Challenges the Japan Perovskite Solar Cell Market is Facing?

Durability Limitations Relative to Conventional Silicon Solar Panels

Perovskite solar cells face durability concerns compared with established silicon panels, creating hesitation among commercial buyers, developers, and infrastructure operators seeking long-term investment reliability. Addressing sensitivity to moisture and heat requires advanced encapsulation solutions that raise production costs. These combined challenges slow wider adoption across Japan’s mainstream construction and energy sectors despite ongoing technological progress in the near term outlook.

High Production Costs Limiting Price Competitiveness Against Established Solar Technologies

Current perovskite solar cell production costs in Japan remain higher than conventional silicon-based alternatives, limiting widespread adoption. Until manufacturing processes mature and scale efficiencies lower costs, deployment will stay focused on premium applications where flexibility and lightweight properties justify higher pricing. This cost disparity continues to restrict broader market penetration despite growing interest and technological advancements across multiple end-use sectors.

Lead Content and Environmental Regulatory Compliance Risks

Most commercially viable perovskite formulations contain lead as a key component, raising environmental concerns as applications expand into residential buildings, public spaces and agriculture. Compliance with strict regulations requires safe containment or development of lead-free alternatives, introducing technical risks and potential liabilities that may slow adoption across certain markets and use cases over time as oversight frameworks tighten globally further.

Competitive Landscape:

The Japan perovskite solar cell market shows a distinct competitive structure where electronics firms, chemical companies, and university spin-offs pursue complementary approaches rather than direct rivalry. Domestic players focus on flexible films and glass-integrated modules for building applications, unlike global peers targeting utility-scale solutions. Companies are progressing across multiple production methods, supported by government funding that encourages parallel development. Partnerships with construction, automotive, and infrastructure firms are shaping demand, as manufacturers align product innovation with real-world deployment opportunities while building scalable production capabilities and strengthening commercialization pathways within domestic markets.

Recent Developments:

- February 2026: Japan’s METI announced plans to subsidize overseas trials of perovskite solar cells starting FY2026 to accelerate commercialization. The initiative focuses on funding international demonstration projects to validate performance, durability, and economic viability across diverse environments. This move aims to build global market acceptance and strengthen Japan’s position in next-generation solar technology.

- October 2025: Japan’s NEDO launched an R&D call under its Green Innovation Fund to advance mass production of next-generation tandem perovskite solar cells. The program focused on improving efficiency, scaling manufacturing, and real-world testing of solar technologies. This initiative supported Japan’s push toward carbon neutrality by accelerating commercialization of advanced solar solutions.

Japan Perovskite Solar Cell Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Rigid, Flexible |

|

Applications Covered |

BIPV, Power Station, Transportation and Mobility, Consumer Electronics, Others |

|

Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Perovskite Solar Cell Market Report

The Japan perovskite solar cell market size was valued at USD 26.94 Million in 2025.

The Japan perovskite solar cell market is expected to grow at a compound annual growth rate of 69.25% during 2026-2034 to reach USD 3,070.83 Million by 2034.

Rigid holds the largest share at 61.3% in 2025, driven by superior conversion efficiency, structural durability advantages, and strong alignment with glass-integrated BIPV applications across Japan's commercial building sector.

Key factors driving the Japan perovskite solar cell market include advancements in manufacturing processes that improve efficiency and reduce costs. In 2025, Sumitomo Heavy Industries developed a low-temperature plasma-based method enabling faster production, lower material damage, and scalable manufacturing, accelerating commercialization potential across multiple applications.

Major challenges include durability limitations for silicon panels, high production costs limiting price competitiveness against conventional solar technologies, lead content regulatory compliance risks, and the need for further manufacturing process maturation to achieve commercial scale viability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)