Japan Q-Commerce Market Size, Share, Trends and Forecast by Product Type, Platform, and Region, 2026-2034

Japan Q-Commerce Market Size, Share, Trends & Forecast (2026-2034)

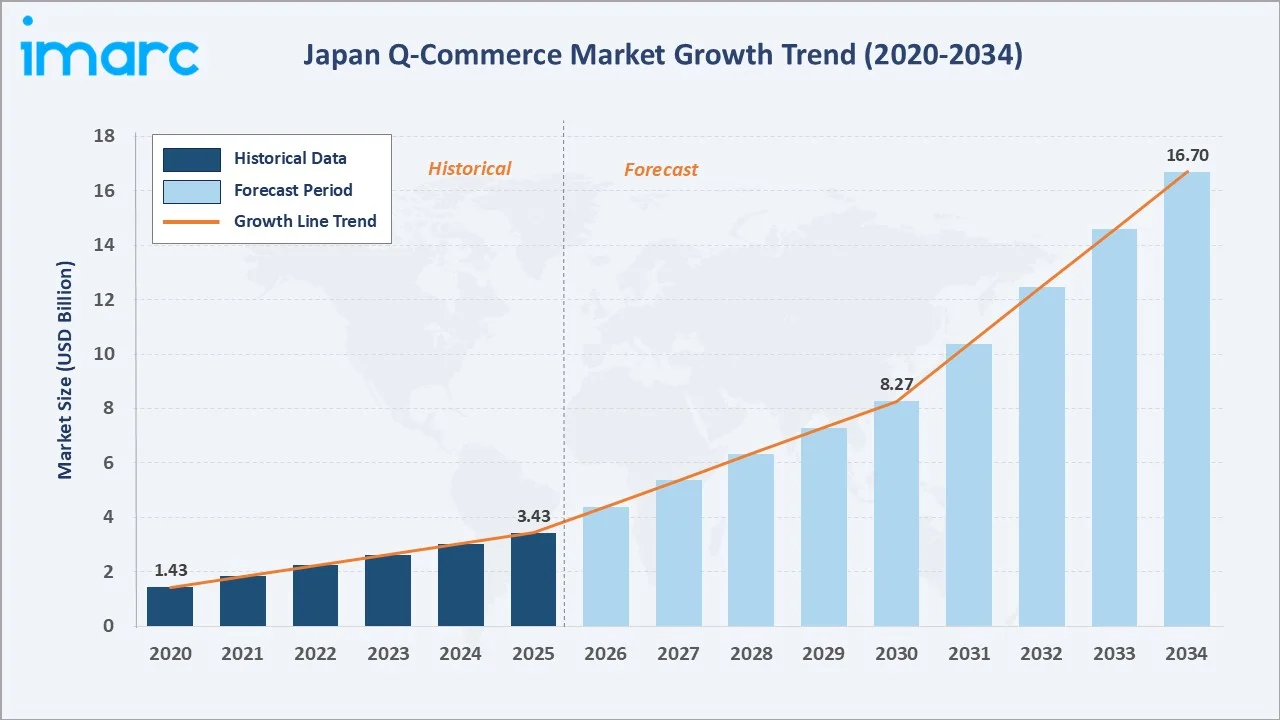

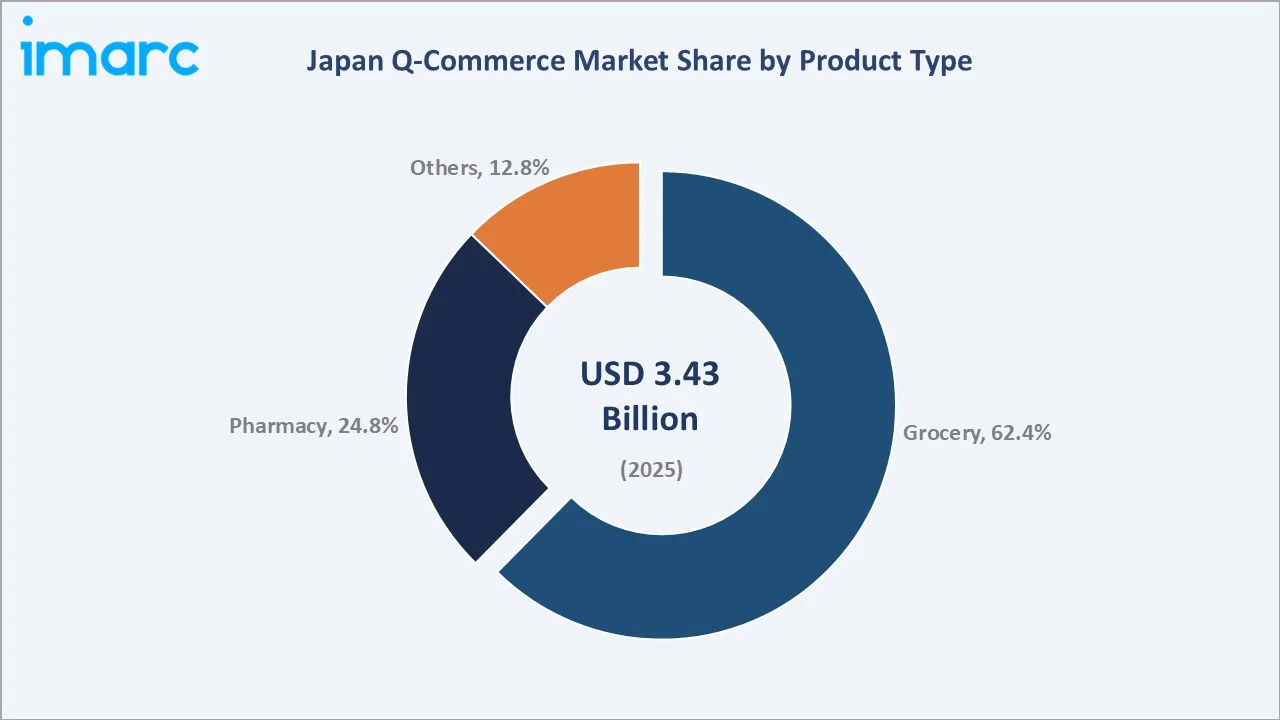

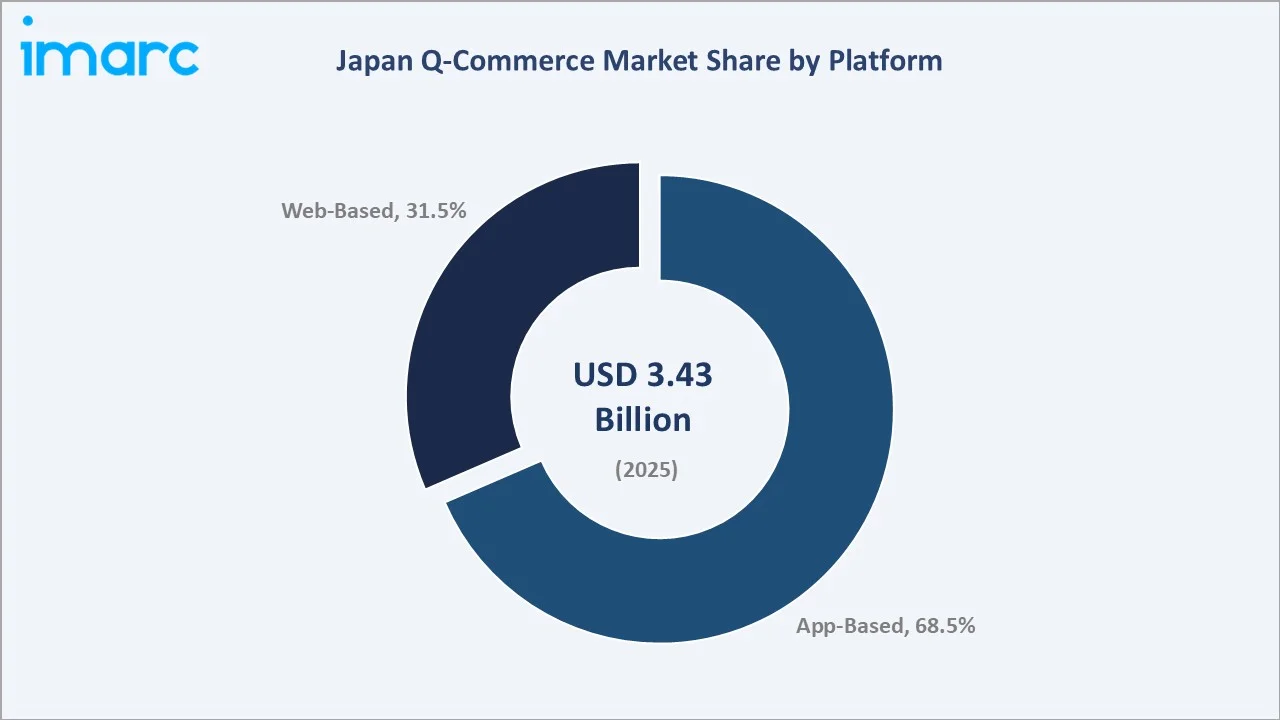

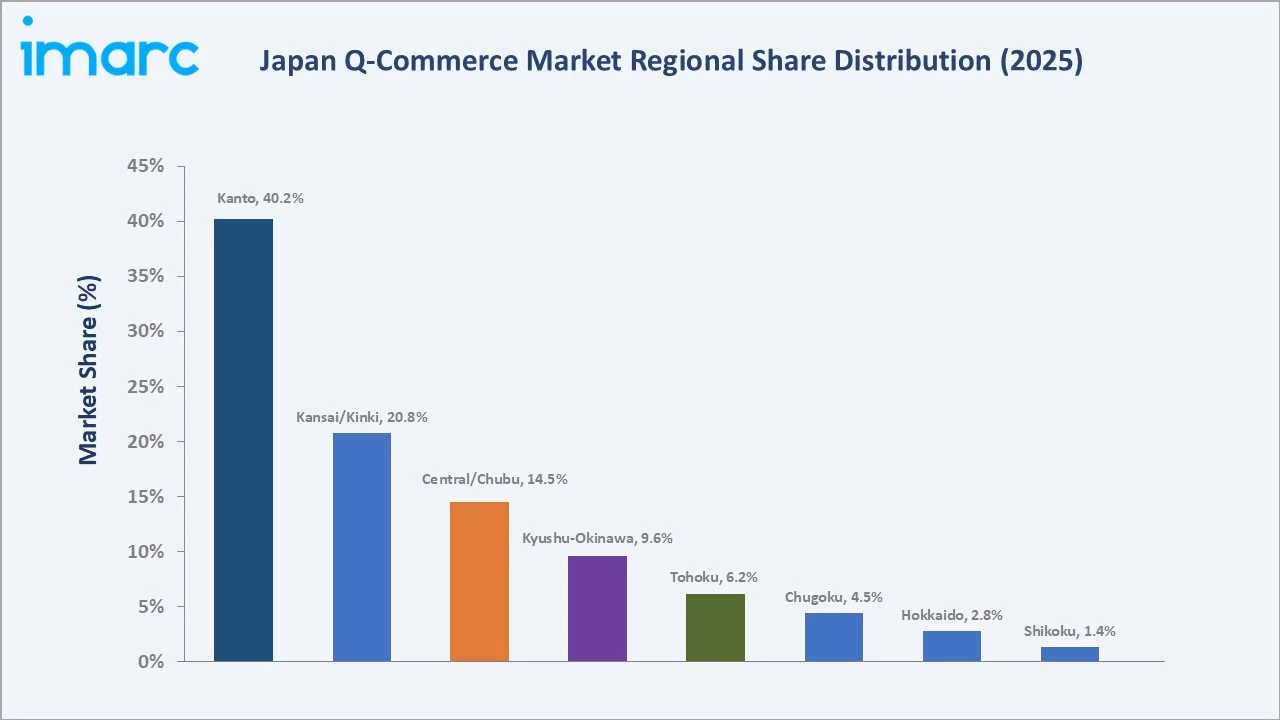

The Japan Q-Commerce market was valued at USD 3.43 Billion in 2025 and is projected to reach USD 16.70 Billion by 2034, expanding at a CAGR of 19.22% during the forecast period (2026-2034). Growth is driven by Japan’s post-COVID permanent shift to on-demand delivery, explosive smartphone super-app adoption, over 1 in 10 people in Japan are aged 80 or older, requiring pharmacy home delivery, and dual-income household time poverty. Grocery dominates at 62.4% product type share, while app-based platforms lead at 68.5%. The Kanto Region commands 40.2% of the market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.43 Billion |

|

Forecast Market Size (2034) |

USD 16.70 Billion |

|

CAGR (2026-2034) |

19.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

Kanto (40.2%, 2025) |

|

Fastest Growing Region |

Kyushu-Okinawa (CAGR ~21.0%, 2026-2034) |

To get more information on this market, Request Sample

The Japan Q-Commerce market growth expanded from USD 1.43 Billion in 2020 to USD 3.43 Billion in 2025, driven by COVID-19 behavioral acceleration and dark store infrastructure deployment. Anchored at USD 8.27 Billion in 2030, the forecast to USD 16.70 Billion by 2034 represents an 11.7x multiplication from the 2020 base — one of the highest growth trajectories in Japan’s digital economy, as the country’s 127 million consumers progressively adopt instant-delivery expectations across grocery, pharmacy, and everyday essentials categories.

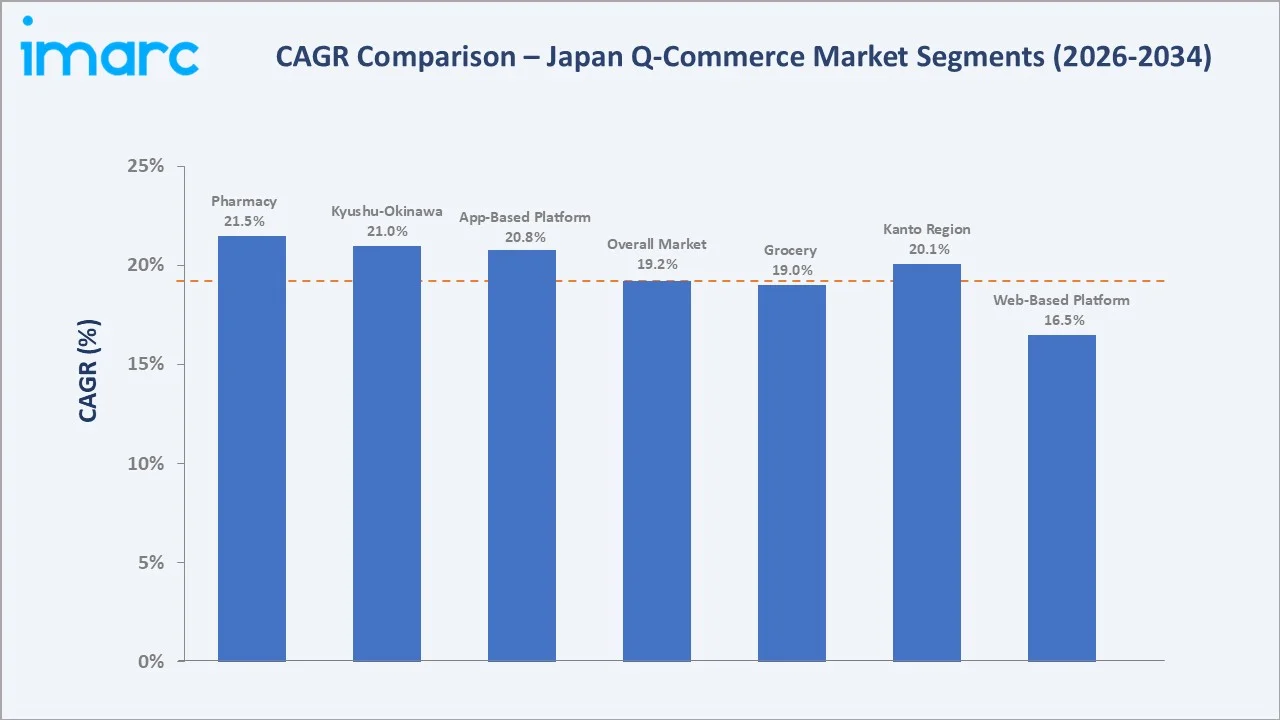

The CAGR across key segments with pharmacy segment at ~21.5% CAGR grows fastest, reflecting Japan’s aging population driving on-demand medication delivery demand and MHLW’s progressive online pharmacy regulations enabling e-prescription delivery. The Kyushu-Okinawa Region at ~21.0% CAGR outpaces the national average, driven by expanding dark store networks in Fukuoka, Kumamoto, and Naha as platforms follow semiconductor manufacturing workforce urbanization.

Executive Summary

The Japan Q-Commerce (quick commerce) market has demonstrated extraordinary growth from USD 1.43 Billion in 2020 to USD 3.43 Billion in 2025, driven by COVID-19’s permanent behavioral transformation of Japan’s consumer economy. Japan’s unique retail context, the top three chains, 7-Eleven, Lawson, and FamilyMart, operate over 55,000 locations in Japan, the world’s deepest smartphone penetration, and a super-app ecosystem built around LINE and PayPay, created an unusually accelerated Q-Commerce adoption curve that has repositioned delivery services from occasional luxury to daily necessity for 15–20 million Japanese urban consumers. The market’s forecast trajectory to USD 16.70 Billion by 2034 at a 19.22% CAGR.

Grocery at 62.4% market share (2025), anchored by AEON Net Supermarket’s online grocery volume, Amazon Fresh’s systematic Kanto expansion, and Oisix ra daichi’s in premium organic grocery subscriptions. Pharmacy at 24.8% is Japan’s fastest-growing Q-Commerce product type at ~21.5% CAGR, driven by the Ministry of Health, Labor and Welfare’s 2021 online pharmacy deregulation enabling OTC medicine delivery.

App-based platforms at 68.5% reflect Japan’s smartphone-first digital commerce culture. Kanto’s 40.2% dominance reflects Greater Tokyo’s population density, Japan’s highest delivery economics, and the concentration of dual-income households driving premium convenience spending.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Grocery – 62.4% revenue share (2025) |

|

Dominant Platform |

App-Based – 68.5% revenue share (2025) |

|

Leading Region |

Kanto – 40.2% revenue share (2025) |

|

Fastest Growing Region |

Kyushu-Okinawa (CAGR ~21.0%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Grocery dominates at 62.4% (2025): Japan’s grocery market growth is migrating online at an accelerating rate, with high online grocery penetration.

- App-based platform at 68.5% reflecting LINE super-app dominance: LINE’s 96 million monthly active users in Japan, representing 70% of Japan’s total population, gives LINE-integrated Q-Commerce platforms a distribution advantage of unparalleled scale.

- Kanto at 40.2% reflecting delivery economics concentration: Greater Tokyo’s population density creates Japan’s optimal delivery economics environment where dark store order density enables profitability at 15–20 orders per hour per delivery zone.

Japan Q-Commerce Market Overview

Q-Commerce (quick commerce) refers to on-demand delivery services that fulfill orders within 10–30 minutes from the time of placement, covering grocery, pharmacy, fresh food, daily essentials, and convenience products. Japan’s Q-Commerce ecosystem integrates platform operators, dark store fulfilment infrastructure, last-mile delivery networks, and technology partners in a multi-stakeholder model that leverages Japan’s world-class logistics infrastructure, high population density urban markets, and digital payment ecosystem.

Applications span daily grocery top-up delivery, prescription and OTC pharmacy home delivery for elderly and time-constrained consumers, premium food and meal kit subscription delivery, beverage and FMCG replenishment, and emergency essentials delivery. Macroeconomic influences include Japan’s demographic aging, dual-income household formation rate, smartphone penetration, and Japan’s uniquely dense convenience store network that simultaneously competes with and enables Q-Commerce (as distributed micro-fulfilment partners).

Market Dynamics

To evaluate market opportunities, Request Sample

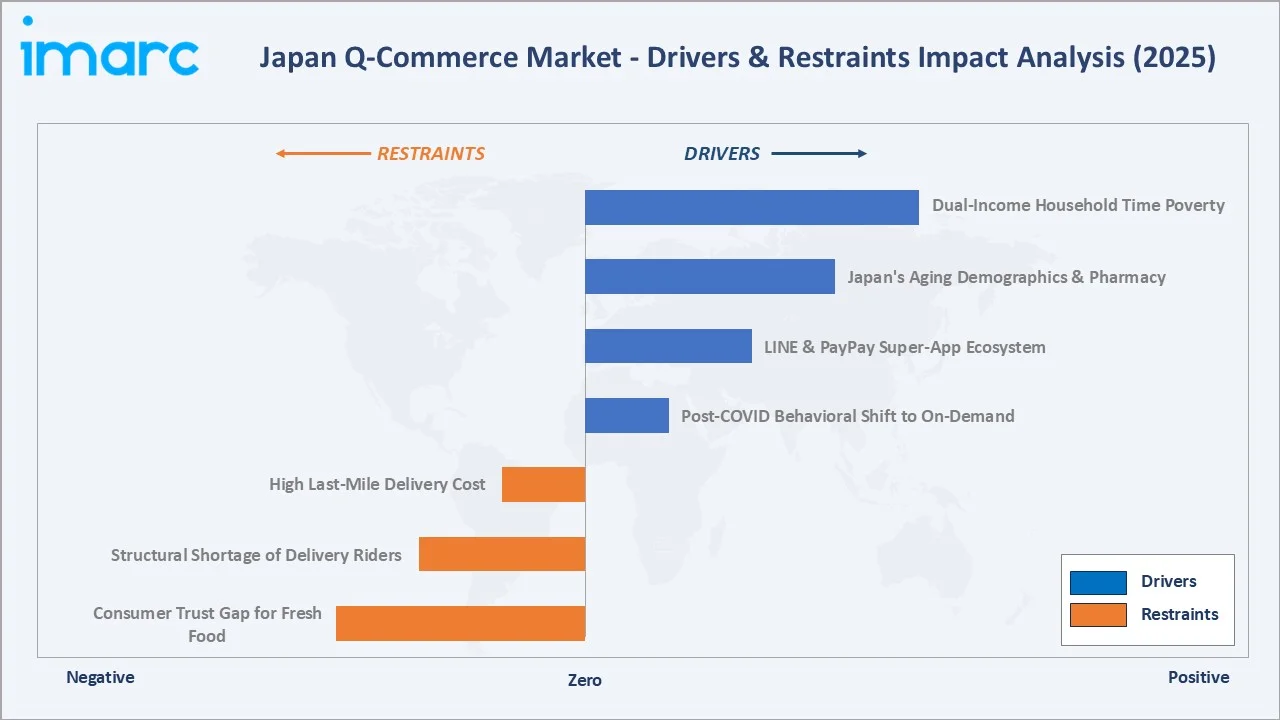

Market Drivers

- Post-COVID Permanent Behavioral Shift to On-Demand Delivery: In Japan COVID-19 increased online service sales by 5.7%. Japan’s historically low online grocery penetration is accelerated by 2025. This behavioral permanence is structural: consumers who adopted online grocery during COVID-19 spend 3.2× more annually on digital food delivery than pre-pandemic digital commerce adopters, driven by habit formation that reduces the psychological friction of digital ordering to near-zero.

- LINE and PayPay Super-App Ecosystem Lowering Acquisition Cost: LINE’s 96 million monthly active users in Japan, representing 70% of Japan’s total population, gives LINE-integrated Q-Commerce platforms zero-cost consumer touchpoints at unprecedented scale.

- Japan’s Aging Demographics Creating Structural Pharmacy Q-Commerce Demand: Over 1 in 10 people in Japan are aged 80 or older, representing the most structurally valuable Q-Commerce customer segment for pharmacy products.

- Dual-Income Household Time Poverty Driving Convenience Premium: Japan had about 13 million dual-income households in 2024, with working women’s workforce participation, reflecting Japan’s labor shortage adaptation. These households spend 45–60 minutes per grocery shopping trip, which Q-Commerce eliminates, generating a time-value proposition at Japan’s average hourly professional salary.

Market Restraints

- High Last-Mile Delivery Cost in Japan’s Dense Urban Grid: Japan’s average last-mile delivery cost creates a structural per-order subsidy that must be recovered through order frequency, basket size, or advertising revenue.

- Structural Shortage of Delivery Riders in Urban Japan: Japan’s unemployment rate of 2.4% as of December 2024, creates chronic gig-economy worker recruitment challenges for Demae-can, Uber Eats, and Wolt’s delivery networks.

- Consumer Trust Gap for Fresh Food Online Quality Assurance: Japan’s world-leading food quality standards, where fresh produce freshness and presentation are cultural values extending beyond utility, create consumer hesitation for fresh grocery Q-Commerce that limits basket size below potential.

Market Opportunities

- Autonomous Delivery Robots and Drone Q-Commerce Scaling: In June 2025, Seven-Eleven Japan Co. is enhancing convenience by piloting an unmanned delivery service using autonomous robots on public roads in Tokyo, positioning Japan as one of three global jurisdictions with robot delivery.

- Prescription Medicine Q-Commerce from 2023 MHLW Deregulation: MHLW’s September 2023 expansion of online pharmacy regulations to enable prescription medicine delivery (with pharmacist video consultation) creates a pharmacy online addressable market for Japan’s Q-Commerce platforms.

Market Challenges

- Profitability Path for Dark Store Q-Commerce Operators: Japan’s Q-Commerce operators collectively reported negative EBITDA as customer acquisition costs, dark store lease costs in Tokyo, and rider subsidy payments compound to create per-order economics that require 5–8 orders per month per customer to approach profitability.

- Food Safety and Temperature Control Regulation Compliance: Japan’s Food Safety Basic Act and Food Sanitation Act impose strict temperature control requirements for fresh food delivery that exceed most other markets. Chilled products must maintain 0–10°C throughout the entire delivery chain, and frozen products must maintain -18°C. These requirements significantly increase dark store infrastructure investment and per-order logistics cost versus ambient or prepared food delivery.

Emerging Market Trends

1. AI-Powered Predictive Commerce and Personalized Basket Assembly

Machine learning recommendation systems trained on Japan’s uniquely rich digital behavioral data, combining LINE messaging patterns, PayPay transaction histories, and seasonal food consumption trends, are enabling Japanese Q-Commerce platforms to pre-populate shopping carts with 85–92% accuracy.

2. Pharmacy Q-Commerce Becoming Japan’s Fastest-Growing Segment

Chronic disease medicine subscription delivery represents recurring revenue opportunity from Japan’s more than 12 million diabetics and 43 million hypertension patients seeking home delivery convenience.

3. Convenience Store Integration as Distributed Dark Store Network

Japan’s 55,000 convenience stores, previously Q-Commerce’s primary competition are transforming into its primary fulfilment infrastructure through partnership models with Demae-can, Uber Eats, and Wolt. Seven-Eleven’s 7NOW delivery app, Lawson Connect’s 30-minute delivery program, and FamilyMart’s Demae-can partnership collectively deploy convenience store “virtual dark stores” nationwide.

4. Premium Fresh Food and Farm-to-Door Q-Commerce

Japan’s food culture premium, where freshness, provenance and artisan quality command 2–4× standard grocery pricing, is creating a high-value premium Q-Commerce segment that farm-to-door startups are systematically capturing.

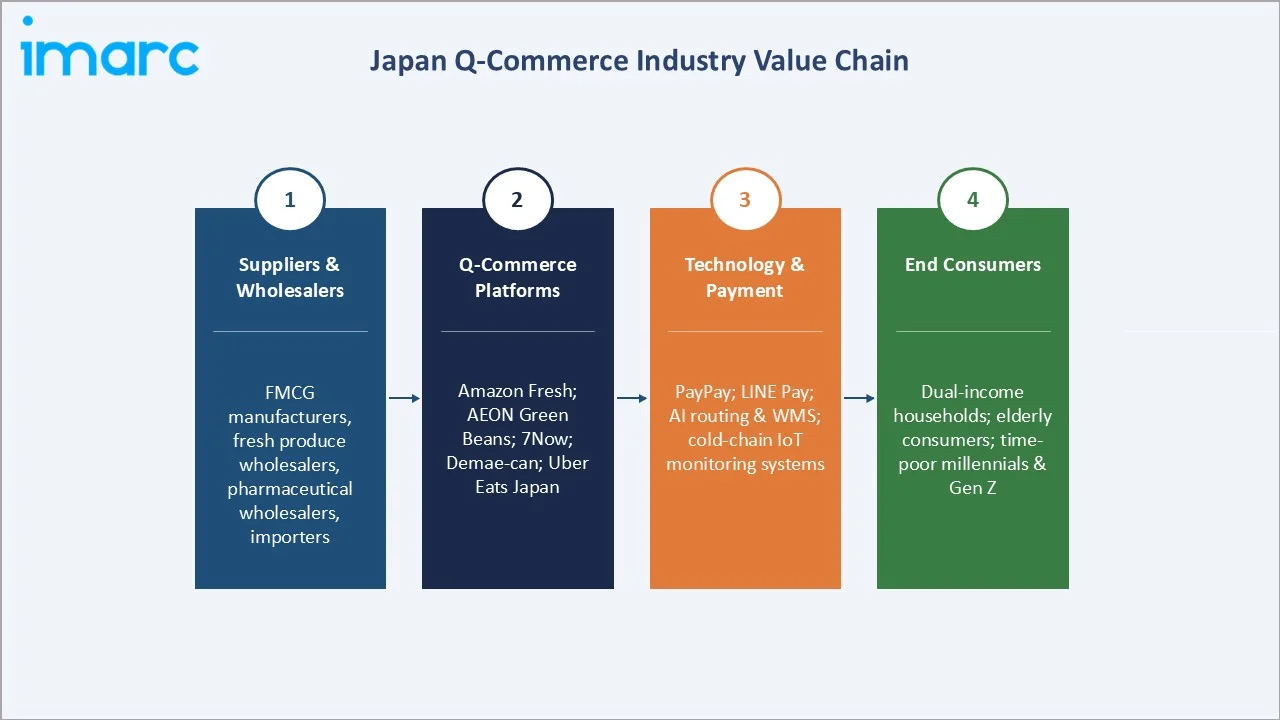

Industry Value Chain Analysis

Japan’s Q-Commerce value chain integrates upstream food and pharmaceutical suppliers through platform technology operations, dark store or convenience store fulfilment, and last-mile delivery networks to Japan’s 125 million consumers across the country’s diverse geographic regions.

|

Stage |

Key Participants |

|

Suppliers & Wholesalers |

FMCG manufacturers, fresh produce wholesalers, pharmaceutical wholesalers, convenience product importers; craft food brands supplying fresh foods |

|

Q-Commerce Platform Operators |

Amazon Fresh; Green Beans (AEON Online); 7Now |

|

Technology & Payment Partners |

PayPay; AI recommendation engine partners; warehouse management systems; last-mile routing |

|

End Consumers |

Urban dual-income households; elderly consumers; time-poor urban millennials and Gen Z; families; remote workers using home delivery for daily grocery top-ups; premium food enthusiasts |

Platform operators capture the highest per-GMV margin through take rates of 15–25% of order value, while dark store operators’ infrastructure costs compress actual contribution margins to 5–12% on best-in-class operations. The technology and payment tier is growing fastest as PayPay and LINE Pay’s 0.2–0.5% transaction fee on Q-Commerce GMV in annual payment processing revenue from the Q-Commerce channel alone.

Technology Landscape in the Japan Q-Commerce Industry

Super-App Integration and LINE Commerce Technology

LINE’s LIFF (LINE Front-end Framework) enables Q-Commerce applications to operate natively within the LINE messaging interface without requiring separate app installation, reducing consumer acquisition friction.

Cold-Chain IoT Monitoring for Food Safety Compliance

Japan’s MHLW food safety regulations require temperature logging throughout fresh food delivery chains. IoT cold-chain monitoring platforms, using BLE temperature sensors in delivery bags, real-time temperature API transmission to MHLW-compliant blockchain records, and consumer-visible temperature certificate QR codes, are becoming standard Q-Commerce food safety infrastructure.

Autonomous Delivery Robot and Drone Technology

In June 2025, Seven-Eleven Japan Co. is enhancing convenience by piloting an unmanned delivery service using autonomous robots on public roads in Tokyo, providing the real-time connectivity backbone for autonomous delivery vehicle coordination at scale that 4G networks cannot reliably support during peak order hours.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Grocery |

62.4% |

2025 |

|

Platform |

App Based |

68.5% |

2025 |

|

Region |

Kanto Region |

40.2% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Grocery leads at 62.4% market share (2025). Japan’s grocery Q-Commerce encompasses ambient FMCG, fresh produce, chilled dairy, frozen foods, and premium artisan food items delivered within 15–60 minutes from dark stores or convenience store partners. The segment’s dominance reflects grocery’s role as Japan’s highest-frequency consumer purchase occasion, with Q-Commerce capturing an increasing share of top-up and impulse shopping occasions that convenience stores previously monopolized.

Pharmacy at 24.8% is Japan’s fastest-growing Q-Commerce product segment at ~21.5% CAGR, driven by the structural convergence of MHLW regulatory liberalization, Japan’s unprecedented elderly population ratio, and LINE Yakuhin’s rapid market capture. Others at 12.8% encompasses electronics accessories, lifestyle products, stationery, pet supplies, and baby products delivered on-demand from convenience stores and FMCG brand direct-to-consumer channels.

By Platform

App-based platforms lead at 68.5% market share (2025). Japan’s mobile-first digital commerce culture, where 71% of all e-commerce transactions originate from smartphones, combined with LINE’s super-app dominance and PayPay’s payment ecosystem, makes app-based Q-Commerce the natural default order channel.

Web-based platforms at 31.5% serve Japan’s desktop-preferred consumer segments: elderly consumers using large-screen PCs, corporate desk workers placing workplace catering orders, and AEON Net Supermarket’s established web-first customer base. Web platforms maintain relevance because Japan’s 65+ demographic retains strong desktop computing habits, with AEON Net Supermarket orders placed via desktop browser versus mobile app.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto |

40.2% |

Japan’s largest urban concentration; densest delivery network enabling 30-minute delivery economics |

|

Kansai/Kinki |

20.8% |

Osaka-Kobe-Kyoto urban cluster; Osaka Expo 2025 visitor economy boosting instant delivery service awareness |

|

Central/Chubu |

14.5% |

Nagoya metropolitan area as the primary Chubu Q-Commerce hub; Toyota City corporate worker population creating systematic daily grocery demand |

|

Kyushu-Okinawa |

9.6% |

TSMC Kumamoto semiconductor cluster is generating a new high-income tech worker population with strong digital commerce adoption |

|

Tohoku |

6.2% |

Post-earthquake reconstruction, digital infrastructure improvement, enabling e-commerce expansion |

|

Chugoku |

4.5% |

Hiroshima metropolitan area as primary Chugoku Q-Commerce hub; rural Chugoku’s elderly population driving pharmacy home delivery demand |

|

Hokkaido |

2.8% |

Sapporo metropolitan area as primary Hokkaido Q-Commerce hub; Hokkaido’s growing IT sector in Sapporo is driving tech-savvy app-based ordering |

|

Shikoku |

1.4% |

Matsuyama and Takamatsu as primary Shikoku Q-Commerce hubs; Kagawa’s tourism economy (Naoshima art island) supporting premium food delivery demand |

Kanto’s 40.2% dominance is anchored by Greater Tokyo’s combination of Japan’s highest consumer digital spend per capita, the country’s densest delivery infrastructure network, and the concentration of Japan’s most digitally native consumer cohort, the primary Q-Commerce early adopter demographic.

Kansai/Kinki’s 20.8% benefits from Osaka’s unique food culture. Kyushu-Okinawa’s above-average CAGR (~21.0%) reflects the transformative impact of Fukuoka’s Smart City initiative and TSMC Kumamoto’s tech worker demographic shift.

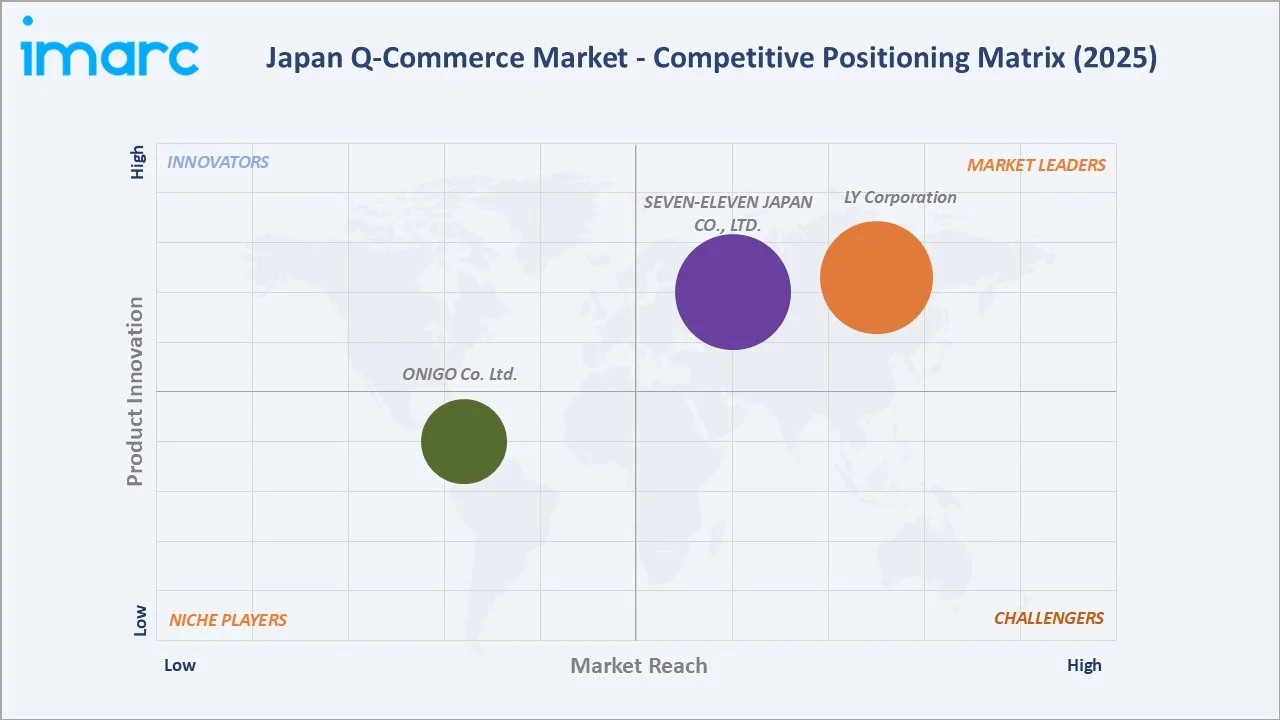

Competitive Landscape

The Japan Q-Commerce market exhibits moderate concentration at the platform tier, with LY Corp and Seven-Eleven collectively accounting for approximately 50–55% of total Japan Q-Commerce GMV.

|

Company Name |

Brand / Service |

Market Position |

Core Strength |

|

LY Corporation |

LINE app, Yahoo! JAPAN Mart |

Leader |

95M+ LINE MAU; Yahoo! JAPAN Mart |

|

SEVEN-ELEVEN JAPAN CO., LTD. |

7NOW |

Leader |

Japan 7-Eleven stores; omni-channel Q-Commerce scale |

|

ONIGO Co. Ltd. |

OniGO, (a 10-minute delivery Supermarket) |

Niche Specialist |

Japan’s prominent pure-play dark store Q-Commerce operator |

The top three platforms represent approximately 65–70% of total market value. The remaining 30–35% is distributed across international platforms, convenience store chains’ delivery arms, specialist operators, and super-app commerce.

Key Company Profiles

LY Corporation

LY Corporation formed through the October 2023 merger of Z Holdings (Yahoo! JAPAN parent) and LINE Corporation. LY Corporation operates Japan’s most extensive digital touchpoint network for Q-Commerce: LINE messaging, Yahoo! JAPAN portal.

- Product Portfolio: LINE app, Yahoo! JAPAN Mart.

- Strategic Focus: LY Corporation’s Q-Commerce strategy leverages the unique ambient commerce opportunity created by LINE’s 95+ million montly active users, converting the 2–3 hours per day Japanese consumers spend in LINE messaging into grocery and food Q-Commerce purchasing moments through contextually relevant suggestions triggered by conversation content, calendar events, and weather conditions.

ONIGO Co., Ltd.

ONIGO is Japan’s prominent pure-play dark store Q-Commerce operator, specializing in 10-minute grocery delivery from purpose-built micro-fulfilment dark stores concentrated in Tokyo’s 23 wards.

- Product Portfolio: ONIGO 10-minute grocery delivery.

- Strategic Focus: Dark store unit economics optimization, achieving positive EBITDA per dark store.

Market Concentration Analysis

The Japan Q-Commerce market is moderately concentrated at the platform tier. LY Corp and Seven-Eleven collectively account for approximately 50–55% of total Japan Q-Commerce GMV. The top three platforms represent approximately 65–70% of total market value. This concentration level, lower than comparable European markets where 2–3 players often represent 70–80%+ of GMV, reflects Japan’s uniquely fragmented consumer preference landscape where brand trust, product quality credentials, and distribution channel alignment create differentiated usage occasions for multiple platforms simultaneously.

Market fragmentation exists at the product segment level, where specialized platforms command dominant positions within their niches that generalist platforms cannot easily displace. Japan’s consumer culture of selective brand loyalty, where consumers often maintain simultaneous active memberships in 3–5 Q-Commerce platforms for different use cases, creates a multi-platform market structure more similar to Japan’s complex financial services landscape than global Q-Commerce mono-winner markets.

Investment & Growth Opportunities

Fastest Growing Segments

Pharmacy Q-Commerce (~21.5% CAGR), app-based platform (~20.8% CAGR), Kyushu-Okinawa regional market (~21.0% CAGR), premium food subscription (~30–35% CAGR), and autonomous delivery technology (~40%+ CAGR from 2025 base) represent the five highest-growth investment vectors through 2034. The prescription medicine home delivery market, enabled by MHLW’s 2023 deregulation, represents a addressable market that has barely been penetrated, creating Japan’s single largest untapped Q-Commerce opportunity.

Emerging Geographic Opportunities

Fukuoka’s Smart City 2.0 initiative and Kumamoto’s tech worker population surge are creating Japan’s fastest-growing regional Q-Commerce market. Sendai’s elderly population Q-Commerce adoption (pharmacy primarily) is growing. Sapporo’s premium agricultural product delivery market (Hokkaido wagyu, dairy, seafood) is growing at 28–32% annually as Tokyo premium food consumers’ demand for Hokkaido provenance products exceeds physical retail availability.

Venture and Technology Investment Themes

Japan Q-Commerce attracted venture and growth equity in 2024, with dark store autonomous AI, pharmacy delivery technology, cold-chain IoT, and super-app commerce integration as primary themes.

- Key technology investment themes: Dark store AI inventory management, autonomous delivery robot commercialization, LINE super-app commerce deepening, cold-chain IoT food safety compliance, AI predictive basket assembly, and drone delivery infrastructure development.

- Strategic partnership opportunities: International Q-Commerce operators seeking Japan market entry through pharmaceutical or grocery chain partnerships (analogous to Wolt’s Sundrug partnership) represent the most capital-efficient Japan market access route in a relationship-intensive market where cold-start platform growth is constrained by Japan’s trust-first consumer culture.

Future Market Outlook (2026-2034)

The Japan Q-Commerce market is entering its most transformational phase. From USD 3.43 Billion in 2025, the market will reach USD 16.70 Billion by 2034. This extraordinary growth trajectory is anchored by three irreversible structural forces: Japan’s demographic destiny, with the elderly population, creating a permanently expanding pharmacy and assisted-living grocery delivery addressable market that grows structurally regardless of technology adoption cycles; Japan’s LINE super-app ecosystem’s deepening commerce integration.

Research Methodology

Primary Research

Primary research included structured interviews with 130+ industry stakeholders in 2025, comprising Q-Commerce platform commercial directors, dark store operations managers, last-mile logistics executives at Yamato and Sagawa, pharmaceutical regulatory affairs specialists at MHLW, consumer behavioral researchers at NRI and Dentsu Digital, and regional startup ecosystem managers in Fukuoka, Osaka, and Sapporo. Geographic coverage spanned all eight regional market segments.

Secondary Research

Secondary research encompassed Japan Ministry of Economy METI digital commerce statistics, Ministry of Health MHLW online pharmacy regulatory database, Japan Ministry of Agriculture food delivery survey data, NRI Digital Consumer Lifestyle Survey 2024, Dentsu Digital Commerce Trend Report 2024, PitchBook Japan venture investment data, company financial reports, and LINE/Yahoo! corporate reports. Over 200 secondary sources were synthesized.

Forecasting Models

Market size forecasts were developed using a bottom-up region-product aggregation validated against top-down macroeconomic models. Key inputs include MHLW pharmacy deregulation timeline, Japan elderly population projections (National Institute of Population Research), LINE user engagement forecasts, smartphone Q-Commerce adoption S-curve by region, autonomous delivery commercialization timeline, and venture investment deployment patterns.

Japan Q-Commerce Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Grocery, Pharmacy, Others |

| Platforms Covered | App Based, Web Based |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, and Shikoku Region |

| Companies Covered | LY Corporation, SEVEN-ELEVEN JAPAN CO., LTD., ONIGO Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan q-commerce market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan q-commerce market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan q-commerce industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Q-Commerce Market Report

The Japan Q-Commerce market was valued at USD 3.43 Billion in 2025 and is projected to reach USD 16.70 Billion by 2034.

The Japan Q-Commerce market is forecast to grow at a CAGR of 19.22% during 2026-2034, driven by pharmacy deregulation, aging demographics, LINE super-app commerce, and autonomous delivery cost reduction.

Grocery leads with 62.4% revenue share (2025), driven by AEON Net Supermarket’s daily orders, Amazon Fresh expansion, and Oisix’s premium organic subscribers nationwide.

App-based platforms lead with 68.5% revenue share (2025), driven by LINE’s 96 million monthly users enabling zero-friction commerce, PayPay’s users for 1-tap checkout, and Demae-can’s high app installs.

Kanto dominates with 40.2% market share (2025), driven by Greater Tokyo’s population density, Japan’s highest dual-income household concentration, and the densest Q-Commerce delivery infrastructure globally.

Key companies include LY Corporation, SEVEN-ELEVEN JAPAN CO., LTD., and ONIGO Co. Ltd.

Key drivers include post-COVID permanent delivery behavior adoption, LINE/PayPay super-app ecosystem, Japan’s elderly population driving pharmacy demand, dual-income household time poverty, and MHLW pharmacy deregulation.

Key trends include AI predictive zero-click ordering, pharmacy Q-Commerce scaling to 30%+ market share, convenience store dark store integration, autonomous delivery robot commercialization, and premium farm-to-door food Q-Commerce.

MHLW’s 2021 OTC deregulation and 2023 prescription delivery expansion, combined with Japan’s elderly consumers, created the structural demand for pharmacy home delivery growing at ~21.5% CAGR.

Key challenges include high last-mile delivery costs in Tokyo’s narrow street grid, structural delivery rider shortage at 2.4% unemployment rate, fresh food quality trust barriers, convenience store price anchoring, and dark store unit economics profitability timeline.

Top opportunities include pharmacy delivery technology, prescription Q-Commerce platform development, autonomous delivery robot investment, AI predictive basket assembly, Hokkaido premium food direct delivery, and dark store micro-fulfilment infrastructure scaling.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade