Japan Railway Management System Market Size, Share, Trends and Forecast by Component, Deployment Mode, Organization Size, and Region 2026-2034

Japan Railway Management System Market Size, Share, Trends & Forecast (2026-2034)

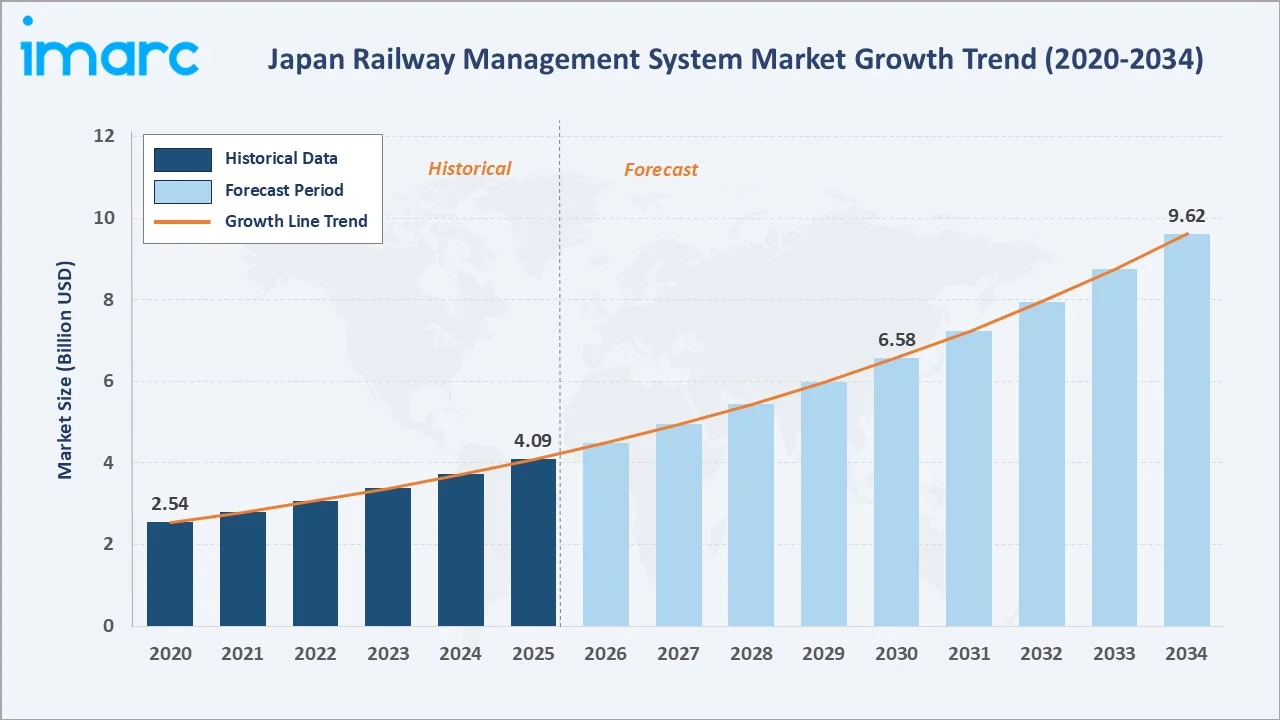

The Japan railway management system market reached USD 4.09 Billion in 2025 and is projected to reach USD 9.62 Billion by 2034, growing at a CAGR of 9.98% during 2026-2034. Japan's extensive and highly complex rail network is undergoing a systematic digital transformation driven by aging infrastructure replacement, acute labor shortages among train operators and maintenance personnel, escalating passenger volumes across Shinkansen and urban metro lines, and the government's Society 5.0 mandate for AI-integrated smart mobility.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.09 Billion |

|

Forecast Market Size (2034) |

USD 9.62 Billion |

|

CAGR (2026-2034) |

9.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

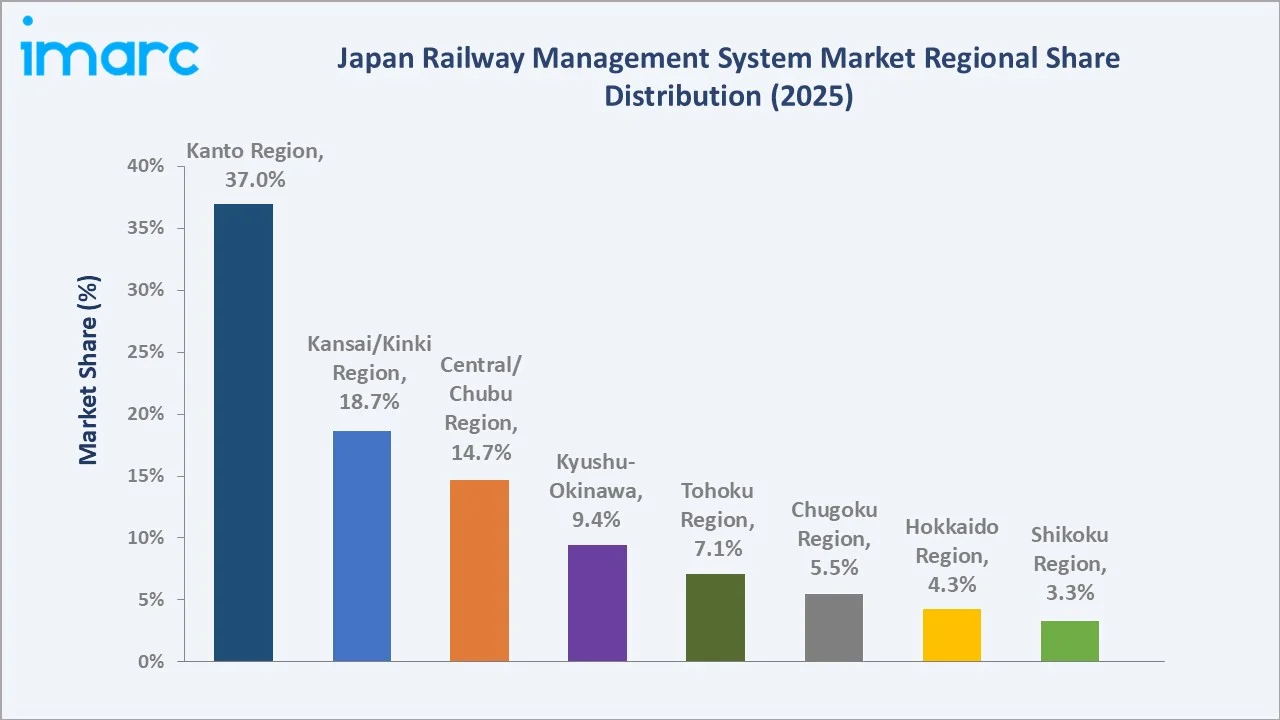

The Kanto region leads regionally, holding a 37.0% market share in 2025, anchored by the Greater Tokyo metropolitan rail network and the Shinkansen operational control centers managing Japan's high-speed rail corridor. Solutions dominate the component breakdown at 66.8%, while on-premises deployment retains the largest share at 57.6% among deployment modes.

To get more information on this market, Request Sample

Japan's railway management system market is underpinned by three structural forces: the digital transformation imperative across JR operators and private rail companies managing combined daily ridership exceeding 30 million passengers, government-mandated sustainability targets requiring AI-driven energy optimization, and the labor crisis compelling automation of manually intensive train control and maintenance scheduling functions.

Executive Summary

The Japan railway management system market is experiencing accelerated expansion, driven by the convergence of Japan's digital railway transformation agenda, acute railway labor shortages, and the government's Society 5.0 smart mobility framework. The market reached USD 4.09 Billion in 2025 and is forecast to reach USD 9.62 Billion by 2034, growing at a CAGR of 9.98%.

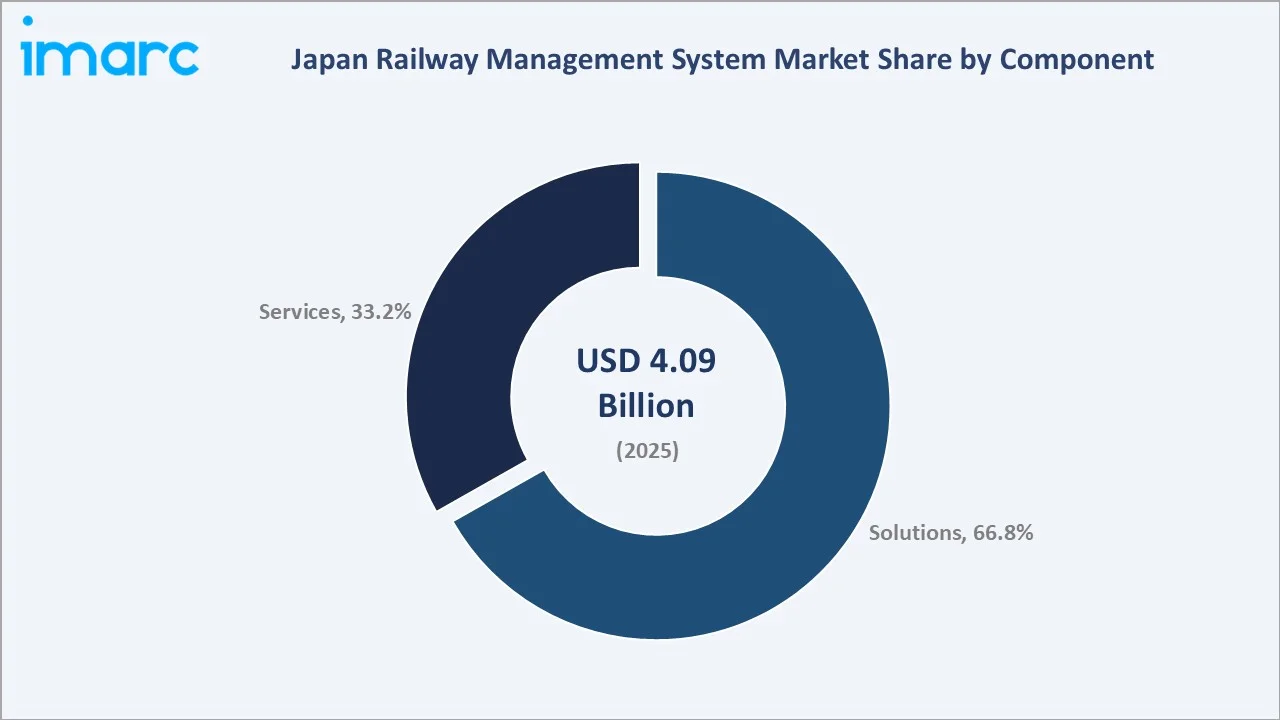

Solutions-based deployments dominate the component segment with a 66.8% share in 2025, encompassing traffic management systems, asset management platforms, crew management solutions, passenger information systems, and predictive maintenance analytics.

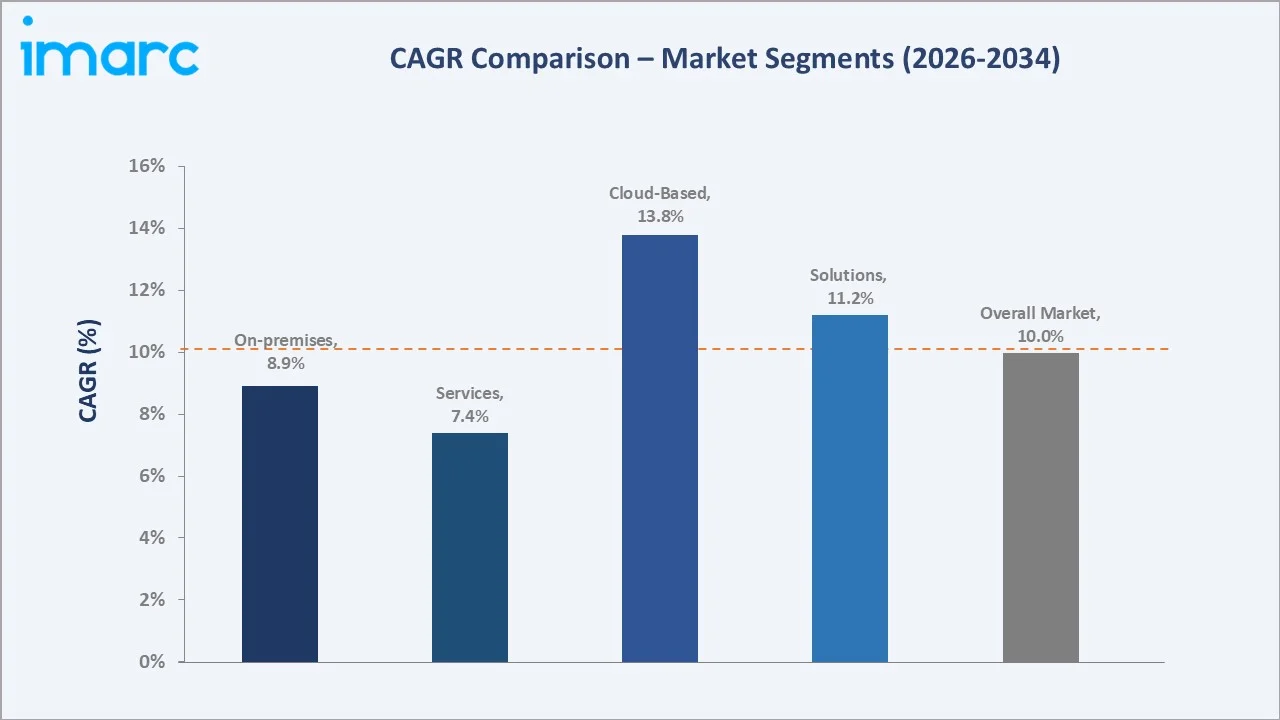

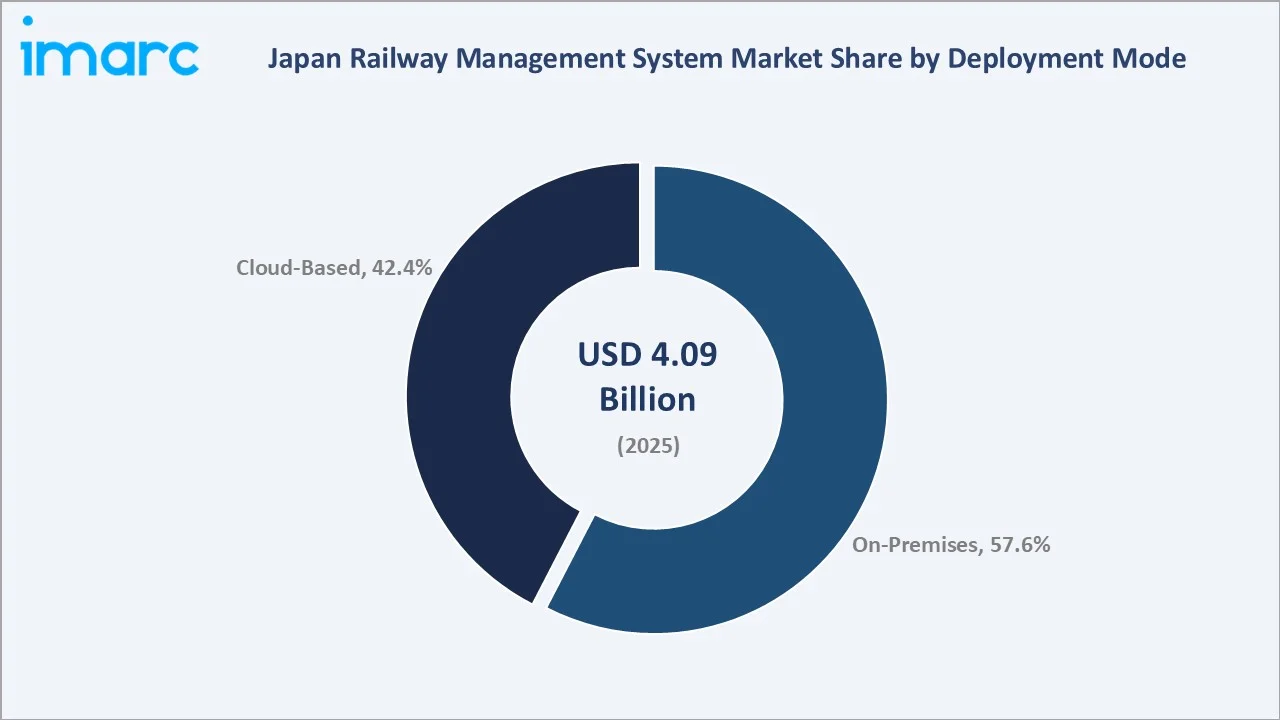

On-premises deployment retains a 57.6% majority share, reflecting the critical-infrastructure security requirements of Shinkansen and urban metro operators, though cloud-based deployments are growing fastest at approximately 13.8% CAGR as regional rail operators adopt SaaS-model management platforms to reduce IT overhead.

The Kanto Region at 37.0% leads regionally, anchored by the JR East operational headquarters, Tokyo Metro's network control centers, and the Tokaido Shinkansen command infrastructure. Leading vendors, including Hitachi, Ltd., Fujitsu Limited, Toshiba Corporation, NEC Corporation, and Nippon Signal Co., Ltd., dominate the market through integrated system portfolios spanning signaling, control, and passenger information.

Key Market Insights

|

Insight |

Data |

|

Largest Deployment Mode |

On-premises – 57.6% share (2025) |

|

Fastest Growing Deployment |

Cloud-based – ~13.8% CAGR (2026-2034) |

|

Largest Component |

Solutions – 66.8% share (2025) |

|

Fastest Growing Component |

Solutions – ~11.2% CAGR (2026-2034) |

|

Leading Region |

Kanto Region – 37.0% share (2025) |

|

Top Companies |

Hitachi, Ltd., Fujitsu Limited, Toshiba Corporation, NEC Corporation, Nippon Signal Co., Ltd. |

Key Analytical Observations Supporting the Above Data:

- On-premises deployment at 57.6% (2025) remains dominant due to the stringent operational technology (OT) security requirements of Japan's railway critical infrastructure. Shinkansen operational control systems and urban metro ATC/ATO platforms handling real-time train control cannot tolerate the latency or availability uncertainty associated with cloud-dependent architectures, necessitating on-premises deployment for safety-critical management functions.

- Cloud-based deployments at 42.4% (2025) are growing fastest as regional and private rail operators adopt subscription-model passenger information systems, crew scheduling platforms, and maintenance management solutions that reduce CapEx barriers and enable rapid feature updates without on-premises infrastructure management overhead.

- Solutions dominate at 66.8% (2025), reflecting the capital-intensive nature of traffic management system upgrades, automatic train protection (ATP) modernization, and integrated operations control center (OCC) platform replacements occurring across Japan's major rail operators.

- The Kanto Region's 37.0% share (2025) reflects Greater Tokyo's status as Japan's densest rail environment, with JR East operating 70+ lines, Tokyo Metro's 9 lines, and the Toei Subway's 4 lines, and the Shinkansen operational control infrastructure concentrated at Omiya and Tokyo stations requiring continuous system upgrades to manage headways below 3 minutes.

Japan Railway Management System Market Overview

Railway management systems encompass the integrated suite of software solutions, hardware platforms, and managed services used to optimize the planning, operation, maintenance, and safety management of rail networks. The market spans traffic management and control systems, asset and maintenance management platforms, crew and resource management solutions, passenger information systems, energy management tools, and freight operations platforms.

Macroeconomic drivers include Japan's working-age population declining at 0.6% annually, alongside the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) mandate for standardized digital railway operations by 2030. Additionally, Japan's 2050 net-zero carbon target requires AI-driven energy optimization across rail operations, where traction energy represents 60–70% of total railway operating costs, creating a technology investment imperative independent of capacity or safety considerations.

Market Dynamics

To evaluate market opportunities, Request Sample

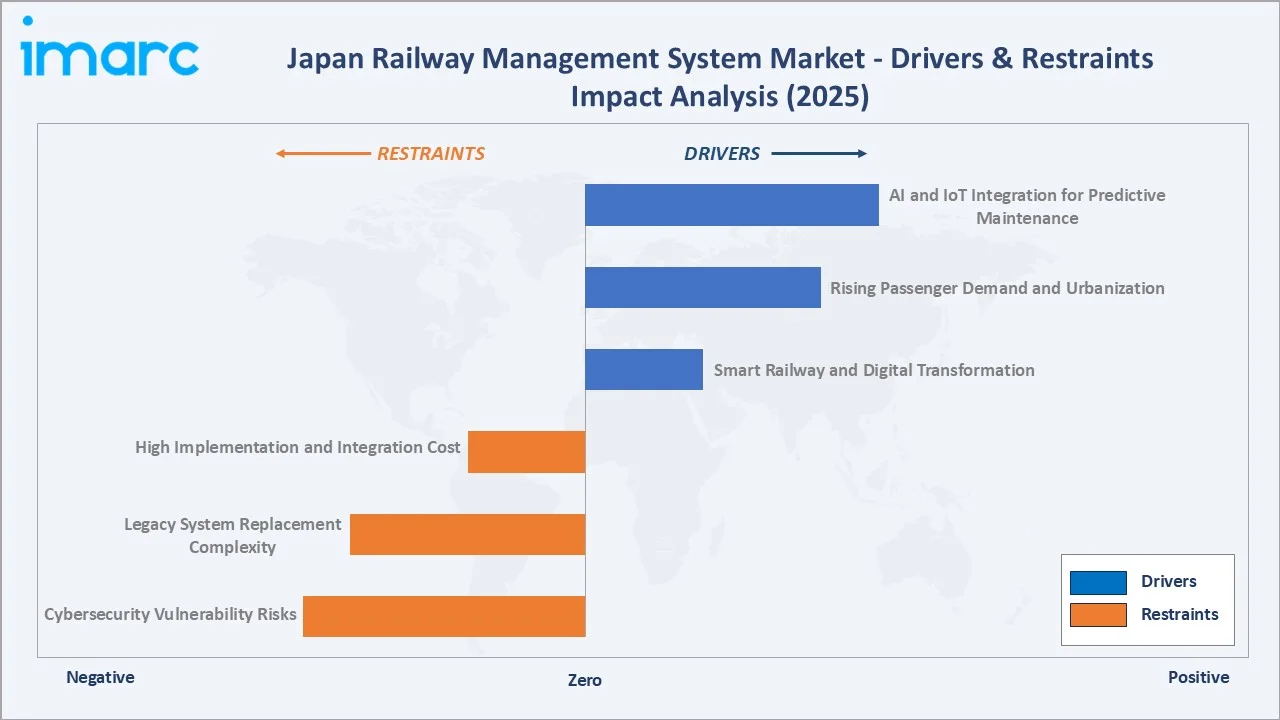

Market Drivers

- Smart Railway and Digital Transformation: Japan's rail operators are executing systematic digital transformation programs. The growing adoption of AI-based traffic control, predictive maintenance, digital twins, and automated inspection systems is strengthening demand in the Japan railway management system market.

- Rising Passenger Demand and Urbanization: Japan's Tokaido Shinkansen line transports around 170 million people annually, while Tokyo Metro’s 195-kilometer network serves an average of 6.84 million passengers per day in FY2024. The Hokuriku Shinkansen extension to Tsuruga (March 2024) is adding network complexity, requiring advanced traffic management system upgrades to maintain service reliability on expanded networks with reduced headways.

- AI and IoT Integration for Predictive Maintenance: JR East plans to introduce automated Shinkansen operations, starting with partial automation on the Joetsu Shinkansen from 2028, and fully automated high-speed trains between Niigata Station and a Niigata Depot by fiscal year 2029. This may require comprehensive AI-based train control and monitoring systems.

Market Restraints

- High Implementation and Integration Cost: A comprehensive railway management system replacement for a major urban metro operator costs JPY 5–50 billion, depending on network scale. For Japan's 100+ private rail operators, this capital commitment requires multi-year budget planning and often regulatory approval for fare adjustments to fund technology investments.

- Legacy System Replacement Complexity: Japan's rail network includes operational systems from multiple technology generations operating with proprietary hardware and communication protocols that require bespoke interface development for integration with modern RMS platforms. Legacy system replacement at safety-critical facilities must be executed with zero service disruption, requiring parallel-run periods of 12–24 months that significantly increase project costs and timelines.

- Cybersecurity Vulnerability Risks: The digitalization of railway operational technology creates cybersecurity attack surfaces previously absent in physically isolated legacy systems. NISC’s critical infrastructure protection guidelines require Japanese railway operators to implement comprehensive OT security frameworks, adding JPY 500 million to JPY 2 billion in security infrastructure costs to major RMS deployment projects.

Market Opportunities

- Autonomous Train Operation (ATO) System Upgrades: Japan's grade of automation (GoA) upgrade program requires comprehensive train control management system replacements at 200+ wayside locations per line segment. Each Shinkansen line automation project represents JPY 80–200 billion in total technology investment, of which 15–25% is attributable to RMS and control system software platforms.

- Integrated MaaS and Multimodal Transport Platforms: Japan's MaaS (Mobility as a Service) ecosystem requires sophisticated integrated rail management systems capable of real-time capacity data sharing, dynamic fare adjustment, and multimodal connection optimization across trains, buses, and emerging eVTOL networks.

Market Challenges

- Procurement Timeline Constraints: Japan's railway infrastructure procurement follows multi-year competitive tendering processes under MLIT oversight, with major RMS contracts subject to 18–36 month procurement cycles from initial specification to contract award. These extended timelines slow revenue recognition for RMS vendors and create planning challenges for operators.

- Interoperability Across Fragmented Operator Ecosystem: Japan's 150+ rail operators operate incompatible proprietary signaling and management system architectures. Creating interoperable through-ticketing, delay notification, and capacity management services across this fragmented ecosystem requires expensive bespoke integration development that individual vendors cannot standardize into scalable product offerings.

Emerging Market Trends

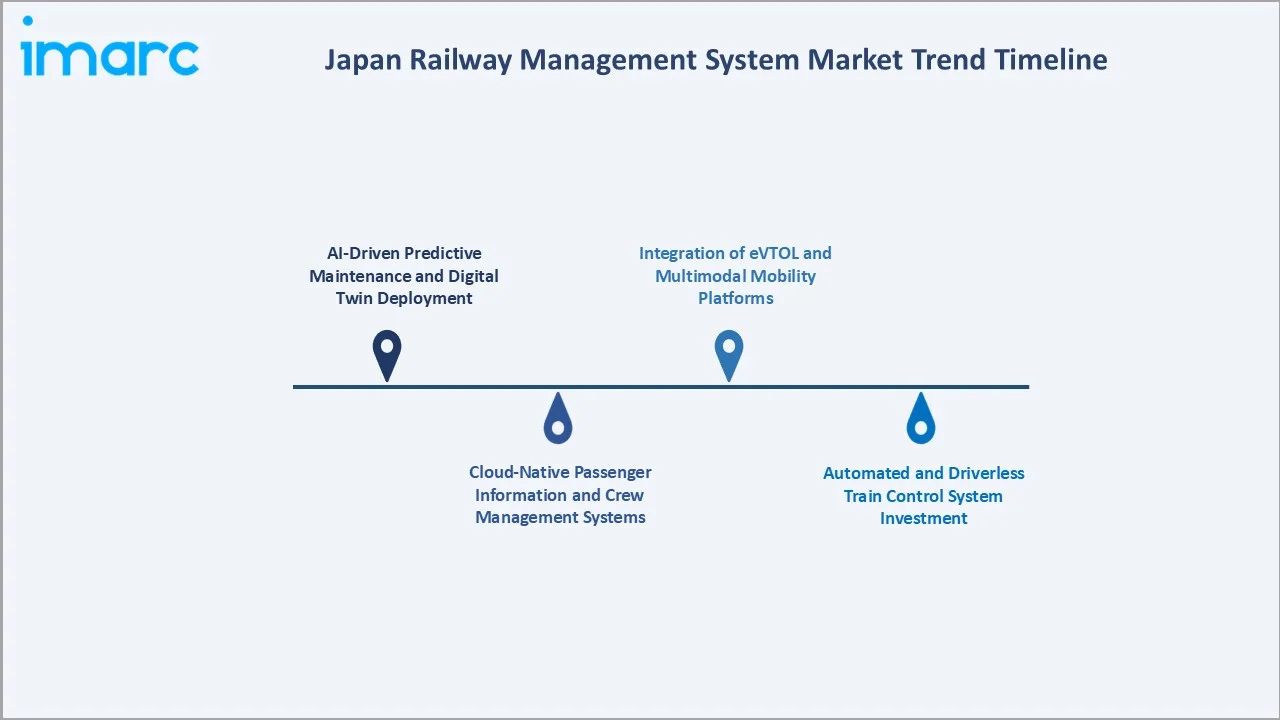

1. AI-Driven Predictive Maintenance and Digital Twin Deployment

In July 2024, West Japan Railway deployed a humanoid maintenance robot developed with Nippon Signal Co. and Jinki Ittai Co. for overhead wire maintenance, demonstrating how AI-driven maintenance platforms are extending from software analytics to physical autonomous maintenance execution. The digital twin technology market for Japanese railways is forecast to grow at 18%+ CAGR through 2034 as operators create virtual replicas of entire network segments for maintenance simulation and capacity planning.

2. Cloud-Native Passenger Information and Crew Management Systems

The rapid adoption of cloud-based SaaS RMS platforms, particularly for passenger information display management, crew scheduling, and revenue management, is being driven by Japan's regional railway operators seeking to eliminate on-premises server management overhead. In March 2025, JR East launched Welcome Suica Mobile, its first cloud-native international passenger service, enabling non-resident visitors to create and reload Suica transit cards without station kiosk interaction.

3. Automated and Driverless Train Control System Investment

In September 2024, JR East announced plans to introduce driverless Shinkansen operations to improve safety, reliability, operational efficiency, and flexibility amid Japan’s population decline and changing workforce needs. The Joetsu Shinkansen will be the first target line, with GOA2 automatic operation planned between Nagaoka Station and Niigata Depot by FY2028 and GOA4 driverless deadhead operation between Niigata Station and Niigata Depot from FY2029.

4. Integration of eVTOL and Multimodal Mobility Platforms

In September 2025, SkyDrive and JR East held a joint exhibition at Takanawa Gateway City to promote seamless railway × eVTOL combination travel, showcasing how passengers could integrate eVTOL flights with conventional rail journeys. The two companies also announced a pre-order agreement for one SKYDRIVE aircraft, further accelerating their growing collaboration.

Industry Value Chain Analysis

Japan's railway management system value chain spans hardware component manufacturing through railway operator deployment, with each stage occupied by specialized manufacturers, software developers, system integrators, and managed service providers whose performance directly influences system reliability, deployment timelines, and lifecycle support quality.

|

Stage |

Key Players / Examples |

|

Hardware & Component Manufacturing |

Sensors, trackside equipment producers, communication device manufacturers, and display system OEMs |

|

Software & Platform Development |

RMS software vendors, AI/ML analytics platform developers, and cloud-native SaaS application developers |

|

System Integration |

Leading system integration firms specializing in railway management technology and delivering end-to-end solution design |

|

Railway Operators |

National and regional railway operating organizations deploying railway management systems |

|

Managed Service Providers |

IT operations, NOC monitoring, cybersecurity managed services, and performance SLA management |

|

End Users |

Daily commuters, Shinkansen long-distance passengers, freight shippers, and rail infrastructure operators |

Technology Landscape in the Japan Railway Management System Industry

Traffic Management and Operations Control Systems

Japan's operations control centers (OCCs) represent the most sophisticated real-time railway traffic management environments globally, managing sub-3-minute headways across Tokaido Shinkansen and 3–5 minute headways on Tokyo Metro Hibiya Line. Hitachi, Ltd.’s ATOS (Autonomous decentralized Transport Operation control System) is deployed across JR East's Tokyo metropolitan network, providing real-time train position monitoring, automated conflict detection, rescheduling after delays, and integrated passenger information management from a unified control platform.

Asset Management and Predictive Maintenance Platforms

Japan's railway asset management market is transitioning from scheduled preventive maintenance to condition-based predictive maintenance enabled by IoT sensor networks and AI analytics. In March 2024, Fujitsu and JR Freight launched a new system in Tokyo, Japan, to digitize and centrally manage rolling stock maintenance and inspection records for railway operators. The system helps reduce maintenance labor, standardize processes, improve inspection accuracy, and address labor shortages in Japan’s railway industry.

Crew Management and Resource Planning Systems

Japan's railway labor shortage is the primary driver of crew management system investment, with operators using AI-driven scheduling platforms to optimize driver and conductor assignments across variable demand patterns, minimize overtime costs, and ensure regulatory compliance with crew rest requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Deployment Mode |

On-premises |

57.6% |

2025 |

|

Component |

Solutions |

66.8% |

2025 |

|

Organization Size |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

37.0% |

2025 |

By Deployment Mode

The on-premises segment dominates with a 57.6% share in 2025. On-premises deployment reflects the stringent operational technology security requirements of Japan's safety-critical railway systems; automatic train control (ATC), operations control center platforms, and interlocking systems cannot tolerate the availability uncertainty or network latency associated with cloud-dependent architectures.

To access detailed market analysis, Request Sample

Cloud-based deployment represents 42.4% and is growing fastest (~13.8% CAGR) as Japan's regional and private rail operators adopt SaaS-model management platforms for non-safety-critical functions, including passenger information management, crew scheduling, revenue management, freight tracking, and maintenance work order management.

By Component

The solutions segment commands a 66.8% share in 2025. Solutions encompass all software platforms and integrated hardware-software systems used in railway management: traffic management systems, automatic train control software, asset management platforms, crew management applications, passenger information systems, energy management tools, and freight operations platforms.

Services represent 33.2% of the market, encompassing professional services, maintenance and support services, training and change management, and managed operations services. The services segment is growing at approximately 7.4% CAGR as Japan's railway operators shift toward outcome-based service agreements.

Regional Market Insights

The Kanto Region's market leadership (37.0%, 2025) reflects Greater Tokyo's position as Japan's most complex and highest-volume railway environment globally. JR East's headquarters and primary operations control center in Shinjuku Station in Tokyo has 36 platforms with more than 3 million passengers passing through daily.

The Kansai/Kinki Region at 18.7% (2025) represents Japan's second-largest RMS market, bolstered significantly by Osaka Expo 2025's smart mobility demonstration infrastructure and the related acceleration of digital railway deployments across Osaka, Kyoto, and Kobe metro systems.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

37.0% |

Large-scale railway network digitalization programs, metro system operational control upgrades, and high-speed rail management system modernization |

|

Kansai/Kinki Region |

18.7% |

Regional railway operator digitalization initiatives, smart mobility infrastructure investment, and AI-driven maintenance platform adoption |

|

Central/Chubu Region |

14.7% |

Advanced rail construction project management system requirements, high-speed railway upgrade programs, and urban metro automation implementation |

|

Kyushu-Okinawa Region |

9.4% |

Regional transit system capacity expansion, urban metro automation upgrades, and multimodal transport integration programs |

|

Tohoku Region |

7.1% |

Railway network resilience and safety system upgrades, operations management platform modernization, and remote infrastructure condition monitoring programs across the regional rail network |

|

Chugoku Region |

5.5% |

High-speed rail control system upgrades, regional rail MaaS platform integration, and industrial corridor railway automation and logistics management programs |

|

Hokkaido Region |

4.3% |

Railway network rationalization technology programs, high-speed rail extension management system requirements, and AI-driven maintenance solutions |

|

Shikoku Region |

3.3% |

Government-supported regional railway digital transformation programs, smart station deployment initiatives, and multimodal mobility integration across the regional rail network |

Competitive Landscape

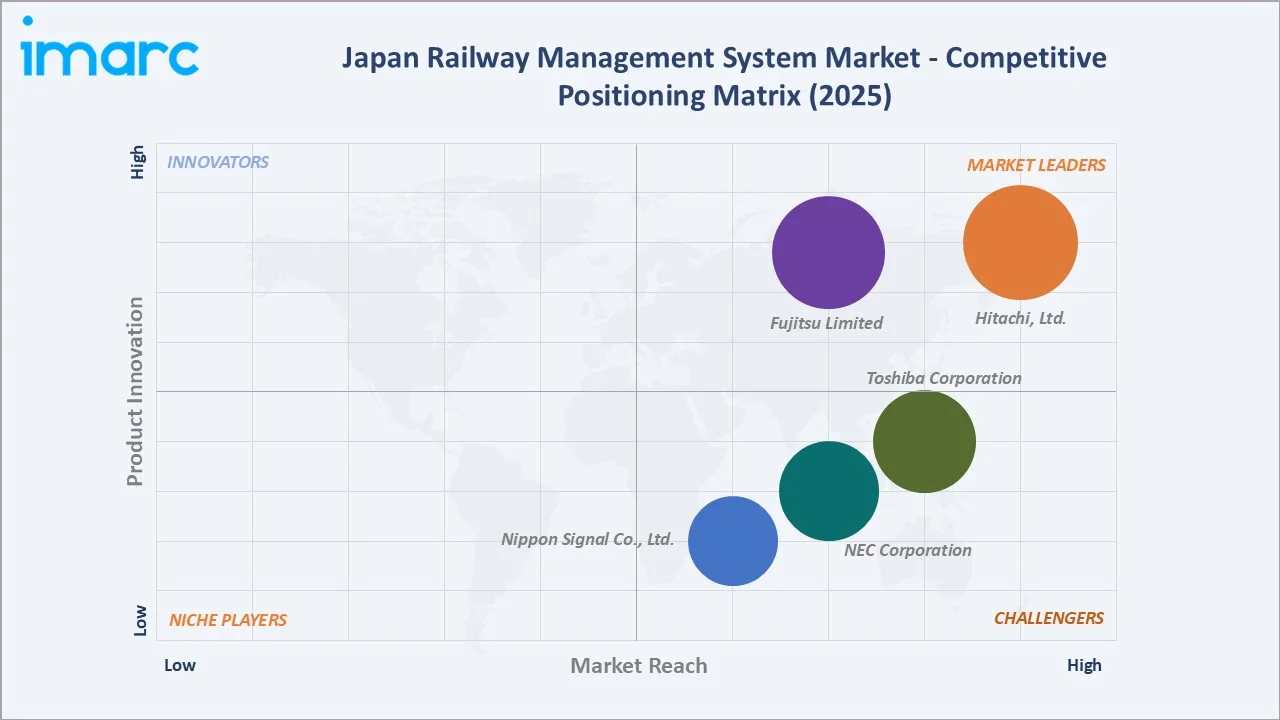

Japan's railway management system market exhibits high concentration among domestic integrators collectively holding approximately 60–68% of market revenue in 2025.

|

Company Name |

Solutions |

Market Position |

Core Strength |

|

Hitachi, Ltd. |

Rolling Stock Solutions, Urban Rail Control & Supervision, Mainline Rail Control & Supervision, Freight Rail Control & Supervision, Ticketing & Payment, Digital Asset Management |

Market Leader |

Comprehensive end-to-end railway management system portfolio; deep integration expertise across major national and urban rail operator environments |

|

Fujitsu Limited |

Security Protocols And Operational Management Services, Data Collection, Connectivity, And Utilization |

Market Leader |

Advanced cloud-native maintenance and operations management capabilities; strong data analytics and AI integration expertise |

|

Toshiba Corporation |

Remote Monitoring Service, Full Turn Key Solution |

Strong Challenger |

Integrated traffic management and energy optimization solutions; proven operations control center capabilities |

|

NEC Corporation |

NEC Mobility Platform |

Strong Challenger |

Integrated operations and mobility management platform capabilities; advanced station technology and passenger flow management solutions |

|

Nippon Signal Co., Ltd. |

Railway Signal Safety System, Station Service Automation Systems, Platform Safety System |

Challenger |

Specialized railway signaling, safety, and station automation expertise; advanced AI-based infrastructure inspection capabilities |

Japan's domestic vendor dominance reflects the technical complexity of operating Japan's unique railway infrastructure, where deep domain expertise in proprietary JR and private railway signaling protocols is a prerequisite for system integration capability.

Key Company Profiles

Hitachi, Ltd.

Hitachi, Ltd. is one of Japan's largest railway management system integrators, providing end-to-end solutions spanning rolling stock management, traffic control systems, operations control center platforms, and predictive maintenance analytics.

- Product Portfolio: Rolling stock solutions, urban rail control & supervision, mainline rail control & supervision, freight rail control & supervision, ticketing & payment, and digital asset management.

- Recent Developments: In November 2025, Hitachi, Ltd. and Tobu Railway launched a strategic co-creation initiative in Japan to deploy Hitachi’s HMAX digital asset management platform for train maintenance. The initiative will focus on automating vehicle inspections, optimizing manual operations, and strengthening on-site maintenance through AI and digital tools.

- Strategic Focus: Lumada platform expansion across Japan's private railway operators; autonomous train control system development; global railway management system exports; digital twin deployment for network capacity simulation.

Fujitsu Limited

Fujitsu Limited provides railway management systems with particular strength in freight rail digitalization, cloud-native passenger service platforms, and AI-powered maintenance management.

- Product Portfolio: Security protocols and operational management services, and data collection, connectivity, and utilization.

- Recent Developments: In March 2024, Fujitsu Limited and JR Freight launched a new system in Japan to digitize and centrally manage rolling stock inspection, repair records, maintenance plans, and parts information. The system reduces administrative workload, improves inspection accuracy, supports regulatory compliance, and will be promoted to other railway operators facing similar maintenance challenges.

- Strategic Focus: Freight rail digitalization leadership; cloud-native RMS SaaS expansion for regional operators; AI-driven maintenance analytics; MaaS platform integration for seamless multimodal journeys.

Market Concentration Analysis

Japan's railway management system market exhibits high concentration, with the top five domestic vendors holding 60–68% of total market revenue in 2025. Below the top tier, a competitive mid-market of 10–15 specialized vendors serves specific subsystem categories, including level crossing control, point machine management, and depot management systems.

Market consolidation is occurring through capability expansion into adjacent software categories, with established hardware-centric vendors building software analytics capabilities through joint ventures and acquisitions of AI and data engineering firms. This convergence of hardware domain expertise with software analytics capability is creating integrated RMS platforms that are difficult for pure-software competitors to replicate without deep railway signaling knowledge.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud-based deployment (~13.8% CAGR), AI-powered predictive maintenance platforms (~16% CAGR), autonomous train control management systems (~18% CAGR from an emerging base), and integrated MaaS platform components (~20% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined addressable market exceeding USD 3 billion within Japan's railway management system ecosystem by 2030.

Emerging Market Expansion

Japan's Chuo Maglev Line represents a USD 400+ million purpose-built management system opportunity with no comparable global reference architecture. Vendors capable of developing maglev-specific RMS components will establish technology precedents applicable to future international maglev projects in the United States, Europe, and Southeast Asia, creating export revenue potential multiples larger than the domestic deployment value.

Venture and Institutional Investment Trends

- Japan's 2030 GoA automation targets are creating non-discretionary technology investment programs that are independent of ridership economics or operator financial performance, providing highly predictable long-term revenue streams for train control management system vendors.

- Railway-as-a-Service (RaaS) managed operations models are emerging among Japan's smaller regional operators, where system integrators assume full technology management responsibility under performance-linked contracts.

Future Market Outlook (2026-2034)

Japan's railway management system market is positioned for sustained growth through 2034. From a base of USD 4.09 Billion in 2025, the market is projected to reach USD 9.62 Billion by 2034, representing total incremental value creation of USD 5.53 Billion at a CAGR of 9.98%. This growth is supported by Japan's multi-decade railway infrastructure investment commitment and the demographic imperative for automation.

The technology composition of the market will shift significantly by 2034, with cloud-based deployment growing from 42.4% to approximately 55% as regional operators complete on-premises-to-cloud migrations for non-safety-critical management functions.

Solutions-category expenditure will expand as the software content of railway management systems increases relative to hardware, driven by AI platform subscriptions, digital twin licensing, and MaaS integration software replacing one-time hardware procurement as the dominant expenditure category.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants in 2024–2025, including railway management system vendors, railway operator IT and operations directors, signaling engineers, government transport policy officials, and institutional investors across Japan, France, Germany, and the United Kingdom. Expert input validated market sizing, technology adoption rates, and regional deployment trends.

Secondary Research

Secondary research encompassed vendor annual reports, MLIT railway statistics, Japan Railways Group annual disclosures, Tokyo Metro IPO prospectus, 3GPP and ETCS technical specifications, and industry publications (Railway Gazette International, Nikkei Construction, Rail Technology Magazine Japan).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating MLIT infrastructure investment budget allocations, railway operator CapEx disclosures, average RMS deployment values, and vendor revenue trends. A base-case CAGR of 9.98% reflects consensus estimates validated against publicly disclosed railway operator technology investment programs from FY2020 to FY2025.

Japan Railway Management System Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Modes Covered | On-premises, Cloud-based |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Hitachi, Ltd., Fujitsu Limited, Toshiba Corporation, NEC Corporation, Nippon Signal Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan railway management system market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan railway management system market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan railway management system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Railway Management System Market Report

The Japan railway management system market reached USD 4.09 Billion in 2025 and is projected to reach USD 9.62 Billion by 2034.

The market is expected to grow at a CAGR of 9.98% during 2026-2034, driven by digital transformation investment, autonomous train program rollouts, and cloud-based platform adoption.

The Kanto region leads with a 37.0% share in 2025, anchored by Greater Tokyo's complex rail network, JR East's digitalization program, and Tokyo Metro's post-IPO technology investment.

On-premises deployment dominates with a 57.6% share in 2025, reflecting stringent OT security requirements for safety-critical train control and operations management systems.

Solutions hold the largest share at 66.8%, encompassing traffic management systems, ATC/ATO platforms, asset management software, and crew management applications.

Some of the key players in the market include Hitachi, Ltd., Fujitsu Limited, Toshiba Corporation, NEC Corporation, and Nippon Signal Co., Ltd.

Cloud-based deployment is growing at ~13.8% CAGR as regional and private rail operators adopt SaaS-model management platforms for passenger information, crew scheduling, and maintenance management—eliminating on-premises infrastructure costs while enabling rapid feature deployment.

Key challenges include high implementation costs, legacy system replacement complexity, cybersecurity vulnerability risks for digitalized OT systems, and a severe shortage of railway IT/OT integration engineers, constraining deployment velocity.

Autonomous train control systems, cloud-native RMS platforms, AI predictive maintenance, Chuo Maglev management systems, and Railway-as-a-Service managed operations models represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade