Japan Smart Medical Devices Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, Application, End User, and Region, 2026-2034

Japan Smart Medical Devices Market Summary:

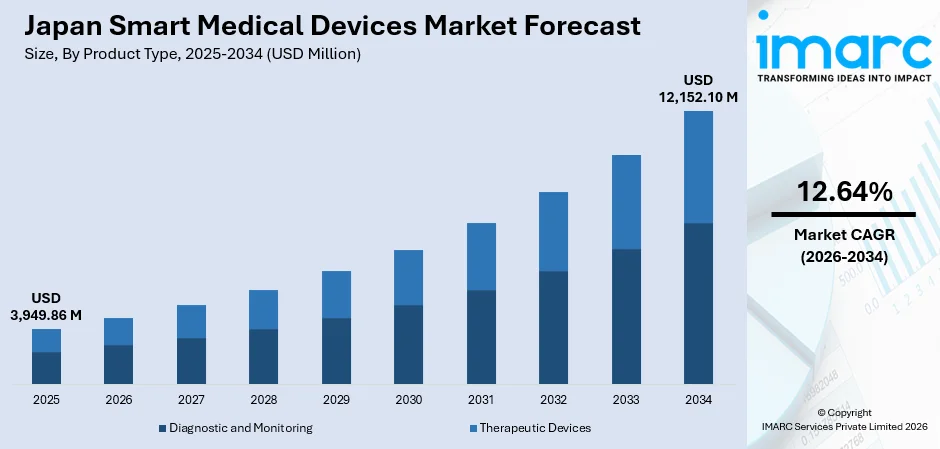

The Japan smart medical devices market size was valued at USD 3,949.86 Million in 2025 and is projected to reach USD 12,152.10 Million by 2034, growing at a compound annual growth rate of 12.64% during 2026-2034.

The Japan smart medical devices market is growing, driven by the country's deepening demographic aging crisis and a strong national push toward healthcare digitalization. Rising prevalence of chronic diseases, particularly diabetes and cardiovascular conditions, is creating sustained demand for real-time monitoring and connected therapeutic solutions. The convergence of artificial intelligence (AI), Internet of Things (IoT) integration, and regulatory modernization is accelerating device innovation and adoption, thereby contributing to the Japan smart medical devices market share.

Key Takeaways and Insights:

- By Product Type: Diagnostic and monitoring dominate the market with a share of 61.3% in 2025, driven by the growing need for real-time health tracking among Japan's aging population and rising adoption of AI-enabled monitoring devices across clinical and home-care settings.

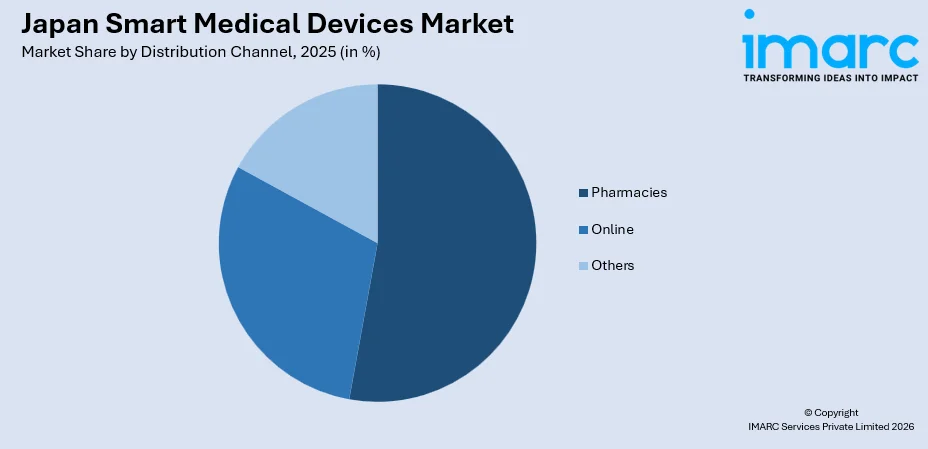

- By Distribution Channel: Pharmacies lead the market with a share of 52.7% in 2025, benefitting from their widespread nationwide presence, established patient trust, and capacity to provide both product access and basic health consultations for chronic disease management.

- By Application: Diabetes represents the largest segment with a market share of 34.8% in 2025, reflecting Japan's high diabetes prevalence rate and the increasing reliance on smart glucose monitoring systems and connected insulin delivery solutions.

- By End User: Hospitals and Clinics dominate the market with a share of 57.9% in 2025, supported by advanced clinical infrastructure, strong physician adoption of connected diagnostic equipment, and favorable reimbursement frameworks for smart medical devices.

- By Region: Kanto Region leads the market with a share of 38.6% in 2025, owing to its high concentration of leading healthcare institutions, research centers, and technology companies within the greater Tokyo metropolitan area.

- Key Players: The Japan smart medical devices market is moderately competitive, featuring domestic technology conglomerates and global device manufacturers investing in AI integration, product miniaturization, and clinical connectivity to strengthen market presence.

To get more information on this market Request Sample

The Japan smart medical devices market is supported by the rising burden of chronic diseases, a rapidly aging population, and increasing demand for continuous and remote patient monitoring solutions. Technological advancements in AI, IoT, and cloud integration are improving device efficiency and enabling real time health tracking across care settings. Government support for healthcare digitalization, along with favorable reimbursement structures, is encouraging broader adoption in both clinical and home environments. In line with this, in 2024, Kobe University announced the launch of a Department of Medical Device Engineering, opening in April 2025. The initiative focused on integrating medicine and engineering to train skilled professionals for developing advanced medical devices. It aimed to boost domestic innovation, reduce reliance on imports, and strengthen collaboration between academia, industry, and government. Additionally, increasing healthcare expenditure, rising awareness of preventive care, expanding telehealth services, and improving connectivity infrastructure continue to drive sustained adoption of smart medical devices across Japan.

Japan Smart Medical Devices Market Trends:

Growing Aging Population Increasing Demand for Advanced Healthcare Solutions

Japan’s rapidly aging population is a major factor driving the demand for smart medical devices, as elderly individuals require continuous monitoring and personalized care solutions. These devices provide accurate, real time health data and enable remote access, allowing healthcare providers to manage age related conditions more effectively while reducing the need for frequent hospital visits. This demographic transition is placing increasing pressure on healthcare systems to adopt efficient, technology driven solutions. Reflecting the scale of this shift, Japan had an estimated 36.19 million people aged 65 and above in 2025, accounting for 29.4% of the total population, as reported by the Ministry of Internal Affairs and Communications. This growing geriatric population continues to accelerate adoption of smart healthcare technologies.

Rising Prevalence of Chronic Diseases Driving Continuous Monitoring Demand

The increasing burden of chronic diseases, such as diabetes, cardiovascular conditions, and respiratory disorders, is a key factor supporting the growth of the Japan smart medical devices market. These conditions require continuous monitoring, timely intervention, and structured management, which smart devices enable through real time data tracking and remote connectivity. The need for such solutions is reinforced by epidemiological trends, as the International Diabetes Federation reported that Japan’s adult population reached 93,187,400 in 2024, with an 8.1% diabetes prevalence, accounting for 8,970,500 cases. This growing patient base increases reliance on connected health technologies. Additionally, the aging population further intensifies the demand, encouraging healthcare providers to adopt smart devices to improve outcomes, reduce hospital readmissions, and enhance overall treatment efficiency.

Strategic Collaborations Accelerating Innovation

Strategic partnerships between technology developers and established healthcare companies are driving innovation and adoption of smart medical devices in Japan. These collaborations combine expertise in medical technology, data analytics, and device manufacturing to develop advanced, user-friendly solutions that support continuous health monitoring. Such alliances enable faster product development, regulatory alignment, and market entry, strengthening the overall ecosystem. A notable instance is the 2025 partnership between Sky Labs and OMRON to introduce a smart ring-based blood pressure monitor in Japan. This device supported real time tracking and early detection of hypertension, reflecting how collaborative efforts are enhancing accessibility, improving patient outcomes, and expanding the scope of wearable healthcare solutions.

Market Outlook 2026-2034:

The Japan smart medical devices market is expected to demonstrate notable revenue expansion throughout the forecast period, underpinned by irreversible demographic trends and accelerating healthcare digitalization. The market generated a revenue of USD 3,949.86 Million in 2025 and is projected to reach a revenue of USD 12,152.10 Million by 2034, growing at a compound annual growth rate of 12.64% from 2026-2034. This trajectory will be sustained by increasing AI adoption in diagnostics, expanding home-care monitoring, regulatory reforms streamlining device approvals, and the government's ongoing digital transformation agenda.

Japan Smart Medical Devices Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Diagnostic and Monitoring |

61.3% |

|

Distribution Channel |

Pharmacies |

52.7% |

|

Application |

Diabetes |

34.8% |

|

End User |

Hospitals and Clinics |

57.9% |

|

Regional Insights |

Kanto Region |

38.6% |

Product Type Insights:

- Diagnostic and Monitoring

- Blood Glucose Monitors

- Heart Rate Monitors

- Pulse Oximeters

- Blood Pressure Monitors

- Breath Analyzer

- Other Diagnostic Monitoring Products

- Therapeutic Devices

- Portable Oxygen Concentrators and Ventilators

- Insulin Pumps

- Hearing AidOther Therapeutic Devices

Diagnostic and monitoring lead with a market share of 61.3% of the total Japan smart medical devices market in 2025.

Diagnostic and monitoring hold the biggest market share owing to the rising demand for continuous health tracking and early disease detection. Increasing prevalence of chronic conditions, such as cardiovascular diseases, diabetes, and respiratory disorders, is driving the need for real time monitoring solutions. Smart devices, including wearable sensors, remote patient monitoring systems, and connected diagnostic tools, enable timely data collection and accurate assessment of patient health. These technologies support preventive care and reduce hospital admissions by allowing early intervention. Additionally, the growing awareness among patients and healthcare providers encourages widespread adoption of diagnostic and monitoring devices across both clinical and home settings.

The segment’s dominance is strengthened by rapid technological advancements and integration with digital health platforms, enhancing accuracy and usability of diagnostic and monitoring devices. Technologies such as cloud connectivity and data analytics support real time tracking and improved clinical decisions. Reflecting this progress, in 2025, MEDIROM MOTHER Labs partnered with TOPPAN Inc. to deploy the MOTHER Bracelet and REMONY system in Japan, enabling continuous monitoring of vital signs without charging. Such innovations improve preventive care and efficiency. Combined with the growing telehealth adoption and institutional collaborations, these developments continue to reinforce the leadership of diagnostic and monitoring applications.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Pharmacies

- Online

- Others

Pharmacies dominate with a market share of 52.7% of the total Japan smart medical devices market in 2025.

Pharmacies lead the market due to their widespread presence, accessibility, and trusted role in healthcare delivery. People frequently rely on pharmacies for purchasing over the counter (OTC) smart medical devices, such as glucose monitors, blood pressure monitors, and wearable health trackers. The convenience of immediate availability, along with professional guidance from pharmacists, supports higher adoption among patients managing chronic conditions. Pharmacies also play a key role in educating users about device usage and maintenance. Their integration with healthcare systems and prescription services further strengthens their position as a primary point of access for smart medical devices across urban and rural areas.

The segment’s dominance is further driven by strong distribution networks, efficient supply chains, and partnerships with medical device manufacturers. Pharmacies benefit from increasing demand for home healthcare solutions, as more patients prefer monitoring their health outside hospital settings. Government support for community-based healthcare and preventive care programs encourages pharmacies to expand their offerings of smart devices. In addition, digital integration such as e pharmacy platforms and online ordering enhances product reach and user convenience. Promotional activities, insurance coverage for certain devices, and the growing individual awareness contribute to higher sales through pharmacies, reinforcing their leading role in the distribution of smart medical devices in Japan.

Application Insights:

- Oncology

- Diabetes

- Auto-Immune Disorders

- Infectious Diseases

- Others

Diabetes exhibits a clear dominance with a 34.8% share of the total Japan smart medical devices market in 2025.

Diabetes represents the largest segment because of its high prevalence and the need for continuous monitoring and management. The growing aging population and sedentary lifestyles are contributing to a steady rise in diabetic patients, increasing the demand for advanced monitoring solutions. Smart devices like continuous glucose monitors, insulin pumps, and connected health apps enable real time tracking and better glycemic control. These technologies help reduce complications and improve patient outcomes through timely interventions. Additionally, strong awareness among patients and healthcare providers supports the widespread adoption of smart diabetes management devices across clinical and home care settings in Japan.

The dominance of diabetes is reinforced by continuous technological progress and supportive healthcare initiatives promoting digital adoption in Japan. Integration of smart devices with mobile and cloud platforms enables efficient data sharing and improved treatment outcomes. In this context, a 2024 Japan based study introduced an improved smartwatch based glucose monitoring method using a signal quality index to enhance accuracy and reliability of non-invasive readings. This advancement supports continuous glucose tracking and strengthens patient management. Combined with reimbursement support and preventive care focus, such innovations continue to drive demand for smart diabetes devices across the country.

End User Insights:

- Hospitals and Clinics

- Home-Care Setting

- Others

Hospitals and clinics lead with a market share of 57.9% of the total Japan smart medical devices market in 2025.

Hospitals and clinics dominate the market driven by their high patient inflow, need for continuous monitoring, and strong investment capacity in advanced medical technologies. These facilities rely heavily on smart devices, such as patient monitoring systems, connected imaging equipment, and wearable diagnostic tools, to improve clinical outcomes and operational efficiency. Integration of digital health systems within hospital infrastructure enables real time data tracking and better decision making. Moreover, increasing burden of chronic diseases and aging population drives the demand for continuous care solutions, encouraging hospitals and clinics to adopt smart medical devices across departments for enhanced patient management and treatment accuracy.

Hospitals and clinics also benefit from established reimbursement frameworks and government support programs that promote the use of digital and connected healthcare technologies. Their structured workflows and trained medical staff allow seamless integration of smart devices into routine care, ranging from diagnostics to post treatment monitoring. The growing emphasis on reducing hospital stays and improving patient outcomes encourages the use of remote monitoring and minimally invasive smart solutions within these settings. In addition, partnerships with technology providers and participation in pilot programs enable early access to innovative devices. This continuous adoption cycle strengthens their position as the leading end users driving demand and technological advancement in the market.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region dominates with a market share of 38.6% of the total Japan smart medical devices market in 2025.

Kanto Region is the leading segment in the market attributed to its strong concentration of advanced healthcare infrastructure, leading hospitals, and research institutions clustered around Tokyo and Yokohama. The region hosts major medical device manufacturers, technology firms, and startups that drive innovation in areas such as wearable monitoring, remote diagnostics, and AI-assisted equipment. High healthcare spending, rapid adoption of digital health solutions, and strong collaboration between academia and industry further support market expansion. In addition, favorable regulatory support, access to skilled professionals, and early adoption by urban healthcare providers continue to strengthen Kanto’s dominant position in the market across key clinical and technology segments.

Kanto’s leadership is also supported by a large patient population, higher awareness of digital healthcare, and strong reimbursement systems that encourage adoption of smart medical devices. The presence of top universities and R&D centers accelerates product development and clinical validation, enabling faster commercialization of innovative solutions. Government initiatives promoting digital transformation in healthcare and smart hospital development are more actively implemented in this region, further boosting demand. Additionally, well-established distribution networks, partnerships between hospitals and tech companies, and a favorable investment environment attract both domestic and international players, reinforcing Kanto’s position as the primary hub for smart medical device growth in Japan across emerging and advanced healthcare technology segments.

Market Dynamics:

Growth Drivers:

Why is the Japan Smart Medical Devices Market Growing?

Advancements in Flexible and Skin-Compatible Wearable Technologies

The development of flexible and skin compatible electronic components is emerging as a key factor driving the Japan smart medical devices market. Innovations in materials and circuit design are enabling the creation of lightweight, stretchable, and non-intrusive devices that improve patient comfort and long-term usability. This shift supports continuous health monitoring without disrupting daily activities, increasing patient compliance and data reliability. In 2024, Murata introduced stretchable printed circuit technology that enhances wearable device performance by improving stability and enabling multi sensor integration for accurate vital tracking. Such advancements are accelerating the adoption of next generation wearable solutions, supporting more precise diagnostics and expanding the role of smart devices in continuous healthcare monitoring.

Integration of AI in Long-Term Cardiac Monitoring Solutions

The growing integration of AI with wearable diagnostic devices to improve cardiac monitoring is a crucial factor influencing the market in Japan. AI-enabled systems enhance data interpretation, enabling faster and more accurate detection of abnormalities, which supports improved clinical outcomes. There is a clear shift toward extended monitoring durations and minimally invasive solutions that provide comprehensive insights into patient health. This is demonstrated by the 2024 approval of iRhythm’s Zio 14-day ECG monitoring system, which combined a patch-based sensor with AI powered analytics to detect arrhythmias more effectively. This trend is advancing diagnostic accuracy, reducing reliance on traditional short term monitoring methods, and strengthening the role of smart devices in proactive cardiac care.

Government Support and Healthcare Digitalization Initiatives

Favorable government policies and initiatives promoting healthcare digitalization are playing a crucial role in driving the adoption of smart medical devices in Japan. Authorities are encouraging the integration of advanced technologies within healthcare systems to improve efficiency, accessibility, and quality of care. Investments in smart hospital infrastructure and digital health platforms support the widespread implementation of connected medical devices. Regulatory frameworks are also evolving to facilitate faster approval and deployment of innovative solutions. This supportive environment fosters collaboration between technology providers and healthcare institutions, accelerating the development and adoption of smart medical devices across the country.

Market Restraints:

What Challenges the Japan Smart Medical Devices Market is Facing?

High Device Costs Limiting Consumer Accessibility

Advanced smart medical devices, particularly AI-integrated diagnostic systems and continuous monitoring wearables, carry significant upfront costs that limit accessibility for Japan's elderly population living on fixed pension incomes. While national health insurance covers select devices, many premium smart monitoring solutions remain outside standard reimbursement schedules, creating financial barriers that slow broader adoption. This pricing gap is especially pronounced in rural and semi-urban regions where income levels are comparatively lower, restricting overall market penetration.

Data Privacy and Cybersecurity Concerns Inhibiting Adoption

The proliferation of connected smart medical devices requires continuous collection, transmission, and storage of sensitive patient health data, raising significant privacy and cybersecurity concerns among healthcare providers and individual users. Japan's Personal Information Protection Commission has issued heightened guidance on data security standards for digital health products. These compliance requirements increase development costs for manufacturers and create hesitation among risk-averse hospital procurement teams and elderly patients unfamiliar with connected health technology ecosystems, constraining adoption rates.

Interoperability Challenges Across Healthcare Systems

Despite strong digital health policy ambitions, Japan's healthcare infrastructure faces significant interoperability challenges between different electronic health record systems, hospital IT platforms, and smart medical device data formats. The absence of universal data standards across the fragmented healthcare provider landscape limits seamless integration of smart devices into clinical workflows. These technical barriers reduce practical clinical value, slowing institutional adoption in regional hospitals and smaller clinic networks outside major metropolitan areas, thus constraining the market's full growth potential.

Competitive Landscape:

The Japan smart medical devices market is characterized by moderate to highly competitive intensity, with domestic technology conglomerates and global medical device corporations competing across diagnostic monitoring, therapeutic, and connected health categories. Leading participants are investing heavily in AI integration, miniaturized sensor development, and cloud-based data management platforms to differentiate their product portfolios. Strategic alliances between device manufacturers and Japanese hospital networks are becoming increasingly prevalent, enabling co-development of specialized solutions tailored to Japan's clinical workflows. Regulatory pathway improvements are lowering barriers to new entrants, particularly for software-based diagnostic tools. Competition is further intensifying as e-commerce channels expand, enabling manufacturers to reach home-care consumers directly. Innovation in wearable formats, non-invasive monitoring, and interoperable platform integration continues to define competitive positioning across all market segments.

Recent Developments:

- January 2026: Japan introduced a non-invasive blood glucose sensor using advanced mid-infrared laser technology to measure glucose without needles. The device works by directing laser light through the fingertip to detect glucose levels in seconds, improving accuracy while reducing pain and infection risk. Developed by Light Touch Technology, it aims to transform diabetes care with easier monitoring and potential expansion to measure other blood components.

- December 2025: FIZE Medical launched its FIZE kUO® system in Japan through a partnership with Asahi Kasei Medical to expand smart critical care solutions. The system digitally monitored urine output in real time, enabling continuous kidney function tracking and data-driven clinical decisions. As a smart medical device, it improved fluid management, supports early intervention, and enhances outcomes for critically ill patients.

Japan Smart Medical Devices Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

|

|

Distribution Channels Covered |

Pharmacies, Online, Others |

|

Applications Covered |

Oncology, Diabetes, Auto-Immune Disorders, Infectious Diseases, Others |

|

End Users Covered |

Hospitals and Clinics, Home-Care Setting, Others |

|

Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Smart Medical Devices Market Report

The Japan smart medical devices market size was valued at USD 3,949.86 Million in 2025.

The Japan smart medical devices market is expected to grow at a compound annual growth rate of 12.64% during 2026-2034 to reach USD 12,152.10 Million by 2034.

Diagnostic and monitoring dominate the market with a 61.3% revenue share in 2025, driven by Japan's high chronic disease prevalence, advanced hospital infrastructure, and the growing adoption of AI-powered diagnostic monitoring solutions.

Key factors driving the Japan smart medical devices market include strategic partnerships between technology developers and healthcare companies, enabling innovation, commercialization, and monitoring solutions, as seen in the 2025 Sky Labs and OMRON collaboration introducing a smart ring for real time blood pressure tracking.

Major challenges include high device costs limiting accessibility among elderly consumers on fixed incomes, data privacy and cybersecurity concerns related to connected health platforms, and interoperability gaps across Japan's fragmented healthcare IT infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)