Laboratory Centrifuge Market Size, Share, Trends and Forecast by Product Type, Model Type, Rotor Design, Intended Use, Application, End-User, and Region, 2026-2034

Laboratory Centrifuge Market Size and Share:

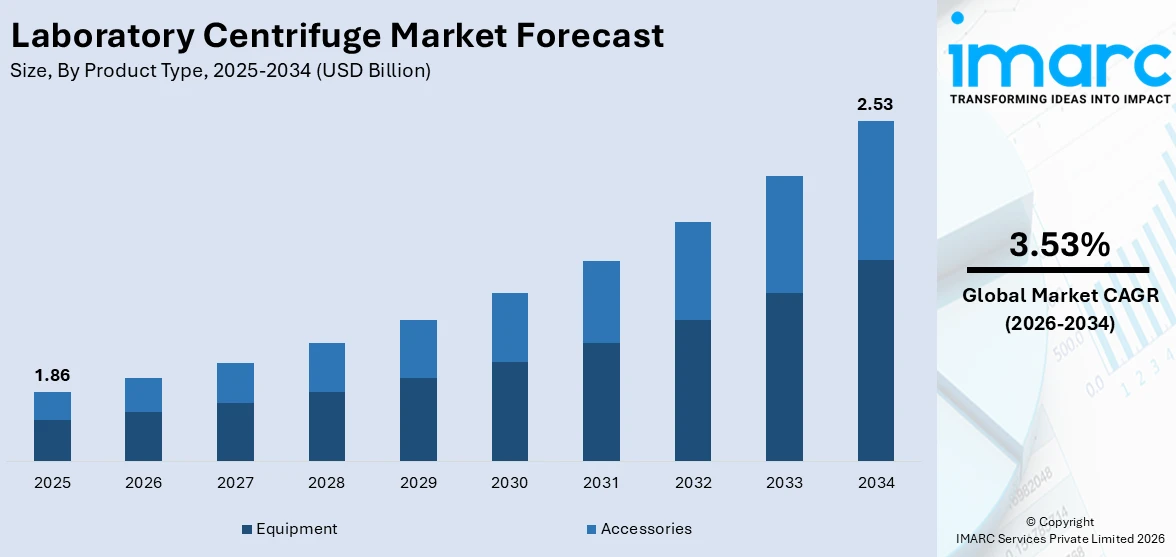

The global laboratory centrifuge market size was valued at USD 1.86 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 2.53 Billion by 2034, exhibiting a CAGR of 3.53% during 2026-2034. North America currently dominates the market, holding a significant market share of over 36.4% in 2025. The growing prevalence of chronic diseases and viral infections, including cancer, and cardiovascular diseases, governmental efforts across various countries to enhance medication regulatory policies, and wide utilization of centrifuges across various sectors are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1.86 Billion |

|

Market Forecast in 2034

|

USD 2.53 Billion |

| Market Growth Rate (2026-2034) | 3.53% |

The global market is primarily driven by the rising demand for advanced diagnostic tools and increasing research activities in life sciences and biotechnology. The growth of the pharmaceutical industry, supported by the development of biologics and personalized medicine, significantly enhances the adoption of centrifuge technologies. Additionally, the increasing prevalence of chronic diseases along with the subsequent need for accurate diagnostics are propelling the market. Continual technological advancements, such as automated centrifuge systems, enhance operational efficiency and further stimulate demand. Expanding healthcare infrastructure in emerging economies and increasing government funding for research and development are also contributing to the market. Moreover, the growth across various applications, including clinical diagnostics and molecular biology is creating a positive market outlook.

To get more information on this market Request Sample

The United States stands out as a key regional market, primarily driven by the increasing utilization of laboratory centrifuges in forensic science and environmental testing laboratories. The rising adoption of centrifuge technology in food safety testing, particularly for microbial analysis, is also gaining momentum. Stringent regulatory frameworks and quality standards in healthcare and pharmaceuticals necessitate the use of reliable laboratory equipment, including centrifuges, further fueling market growth. Moreover, the growing trend of academic and industrial collaborations is driving innovation and expanding the adoption of cutting-edge centrifuge systems. The rapid advancement in cell-based therapies and regenerative medicine, along with the rising role of centrifuges in drug development and protein purification, significantly increases demand in the U.S. market. On 8th December 2023, Casgevy, a cell-based gene therapy, received approval for the treatment of sickle cell disease in patients 12 years of age and older with recurrent vaso-occlusive crises. Casgevy is the first FDA-approved therapy that uses CRISPR/Cas9, which is a genome editing technology. Patients' hematopoietic or blood stem cells are engineered using the genome editing technology CRISPR/Cas9.

Laboratory Centrifuge Market Trends:

Rapid technological advancements

The healthcare industry worldwide is witnessing increased adoption of important technological innovations. These advancements, from digitization to nano-devices, have been extremely advantageous for the laboratory centrifuges market. Equipment like benchtop and floor standing centrifuges are gaining popularity. Increasingly complex chronic and infectious diseases are driving healthcare providers to explore advanced treatments and diagnostic methods, making the use of sophisticated laboratory centrifuges essential. A study published in The Lancet Infectious Diseases highlights the substantial impact of infectious diseases on global health. Of the total 704 Million DALYs attributed to the 85 pathogens, bacterial infections were associated with 415 Million, viral infections with 178 Million, parasitic infections with 172 Million, and fungal infections with 18.5 Million. With the growth of the healthcare sector, there is a rising demand for various laboratory procedures, leading to an increase in clinical trials and analytical tests. The need for additional labs and equipment will keep driving the laboratory centrifuge demand. Due to their affordability, they are in high demand in the market.

Rising research and development activities

The sector for companies specializing in pharmaceuticals and biopharmaceuticals has experienced significant growth in recent years. For instance, the rapid growth of the UK’s biopharmaceutical sector, contributing 68% of the life sciences turnover amounting to USD 17.1 Billion in manufacturing GVA in 2022 according to the UK government, underscores increased adoption of laboratory centrifuges driven by research-intensive innovation and post-pandemic advancements. Many government and business funds are being allocated towards researching and developing different medical fields, leading to an increased need for laboratory centrifuges. The market has seen a notable rise in the need for laboratory centrifuges due to the presence of COVID-19 vaccines and tests. Scientists were working on creating a remedy in different areas to lower the death toll from the virus. This, in turn, has accelerated the laboratory centrifuge market revenue.

Increasing focus on bioprocessing and biomanufacturing

Centrifuges with enormous processing capacities, gentle separation mechanisms, and easy scalability are in high demand to meet the needs of bioprocessing facilities. According to BioPlan’s 18th Annual Report of Biopharmaceutical Manufacturing 2023, nearly 40% of biopharmaceutical respondents identified continuous processing/perfusion as a key area for evaluation in 2021, reflecting steady growth in bioprocessing investments. Furthermore, the rise of regenerative medicine and cell treatment has increased the demand for specialized centrifuges capable of handling sensitive and precious cellular materials. The laboratory centrifuge market responds to these needs by developing technologies that improve bioprocessing workflows. This, in turn, is bolstering the market.

Laboratory Centrifuge Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global laboratory centrifuge market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, model type, rotor design, intended use, application, and end-user.

Analysis by Product Type:

- Equipment

- Multipurpose Centrifuges

- Microcentrifuges

- Ultracentrifuges

- Minicentrifuges

- Others

- Accessories

- Rotors

- Tubes

- Centrifuge Bottles

- Buckets

- Plates

- Others

Equipment stands as the largest component in 2025, holding around 57.6% of the market. Laboratory centrifuge equipment encompasses different types of machinery that leverage centrifugal force in the differentiation of heterogeneous samples for medical and scientific use. This category is dominated by a few major equipment categories, which comprise microcentrifuges, ultracentrifuges, and chilled centrifuges. The supremacy of the laboratory centrifuges' equipment stems from their diversified requirements in relation to laboratory researchers, doctors, and even bioprocessing experts across a discipline. As scientific and medical diagnostics continue advancing, the equipment needed for the field becomes more precise, efficient, and technologically advanced. Manufacturers respond with improvements in centrifuge designs to enhance user experience, increase processing speed, and accommodate a wider range of sample types and sizes.

Analysis by Model Type:

- Benchtop Centrifuges

- Floor-Standing Centrifuges

Benchtop centrifuges lead the market with around 71.2% of market share in 2025. Benchtop centrifuges are designed with benchtops to keep the product safe in the enclosed chamber. These are simple to operate and include an auto-lock system that allows you to quickly replace rotors with one hand for maximum application variety and throughput. The design of these centrifuges reduces dangerous pinch spots while opening and shutting the lid, and a motorized lid lock adds added security. The benchtop centrifuge market is predicted to develop significantly over the forecast period due to its low cost, ease of use, and versatility for chromatography, sedimentation, and sample filtration purposes.

Analysis by Rotor Design:

- Fixed-Angle Rotors

- Swinging-Bucket Rotors

- Vertical Rotors

- Others

Fixed-angle rotors lead the market with around 36.5% of market share in 2025. Fixed angle rotors dominate the laboratory centrifuge industry. The growing demand for high-throughput processing and precise sample separation in a variety of applications, such as cell culture, blood sample preparation, and protein purification, is driving the market adoption of fixed angle rotors. In line with this, continual advancements in rotor design and materials improve their performance and longevity, cementing their role as critical components in modern laboratory centrifuges.

Analysis by Intended Use:

- General Purpose Centrifuges

- Clinical Centrifuges

- Preclinical Centrifuges

General purpose centrifuges stand as the largest component in 2025, holding around 46.6% of the market. General purpose centrifuges are designed to accept a wide range of sample types, sizes, and volumes. The versatility of general-purpose centrifuges is enhanced by their compatibility with many rotor types, including fixed angle and swinging bucket rotors. This versatility enables researchers to customize centrifugation settings to individual experimental needs, improving the quality and reproducibility of results. General purpose centrifuges are essential in clinical laboratories for sample processing because they help separate blood components, urine sediments, and other biological fluids.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Diagnostics

- Microbiology

- Cellomics

- Genomics

- Proteomics

- Blood Component Separation

- Others

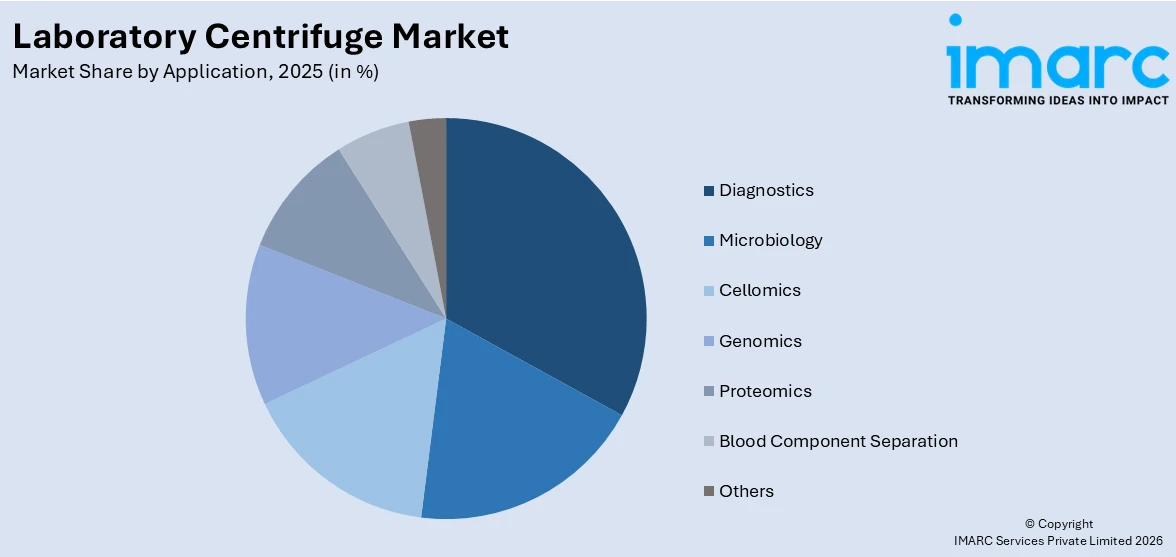

The diagnostics segment holds a significant share, driven by the widespread use of centrifuges in clinical laboratories for blood and fluid analysis. The rising prevalence of chronic diseases and the increasing demand for accurate diagnostic tools continue to fuel growth in this application area.

As a cornerstone of blood banking and transfusion medicine, the blood component separation segment is driven by the rising demand for plasma, platelets, and other blood components in therapeutic and surgical procedures. The growing focus on managing blood disorders and emergencies further boosts its adoption.

Apart from this, numerous innovations in genetic and molecular research activities have made genomics a critical segment. Centrifuges play a vital role in DNA, RNA, and protein isolation processes, supporting applications in personalized medicine, drug discovery, and advanced research in life sciences.

Analysis by End-User:

- Hospitals

- Biotechnology and Pharmaceutical Companies

- Academic and Research Institutions

Hospitals represent a key segment, driven by the increasing use of centrifuges for diagnostic purposes, particularly in clinical laboratories. The growing need for accurate blood analysis and the management of diseases like cancer and infectious conditions further boosts demand in this sector.

The biotechnology and pharmaceutical companies segment plays a critical role due to the rising investment in drug discovery, biologics production, and vaccine development. Centrifuges are indispensable in these processes, supporting cell culture harvesting, protein purification, and other essential applications.

With growing research initiatives in genomics, proteomics, and molecular biology, academic and research institutions are a major end-user segment. The increasing focus on innovation and scientific exploration fuels the adoption of advanced centrifuge technologies in this sector.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

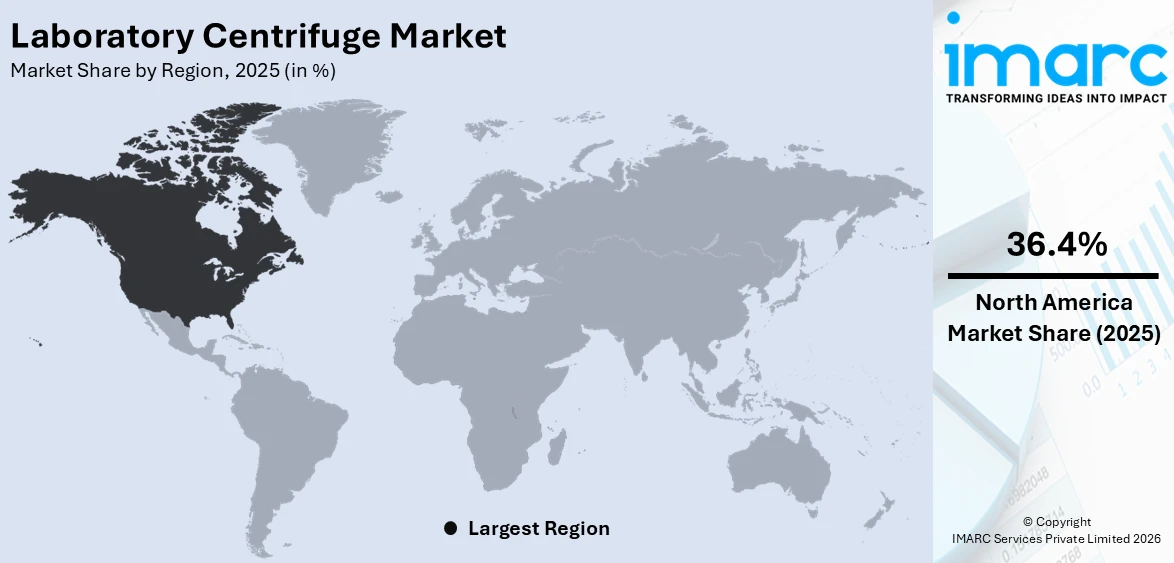

In 2025, North America accounted for the largest market share of over 36.4%. The presence of significant market players leads to product launches, mergers, collaborations, and acquisitions, which fuels the expansion of the market in the region. The rising incidence of tuberculosis (TB) in North American countries is bolstering the usage of centrifuges to diagnose samples. Optimal tuberculosis testing often entails sputum centrifugation followed by broth culture, and so the country's high TB case count is fuelling market expansion. Moreover, technological developments and partnerships, mergers, acquisitions, and new product launches are propelling the growth of this market in the region.

Key Regional Takeaways:

United States Laboratory Centrifuge Market Analysis

In 2025, US accounted for around 89.10% of the total North America laboratory centrifuge market. In the USA, the laboratory centrifuge market is primarily driven by advancements in healthcare and diagnostics, increasing research and development activities, and a rapidly aging population. According to the Census, U.S. population age 65 and over grew from 2010 to 2020 at the fastest rate since 1880 to 1890 and reached 55.8 Million, a 38.6% increase in just 10 years. The demand for laboratory centrifuges is growing as healthcare providers and research institutions seek more efficient tools for diagnosing and testing a wide range of conditions, including chronic diseases like diabetes and cancer. According to the CDC's (Centers for Disease Control) National Diabetes Statistics Report for 2022 cases of diabetes have risen to an estimated 37.3 Million. The U.S. is a global leader in biotechnology and pharmaceutical research, which drives the need for high-performance centrifuges in drug development and clinical trials. Additionally, the rise in healthcare automation, including the integration of automated centrifuge systems in laboratories, is enhancing efficiency and workflow, further contributing to market growth. The ongoing focus on infectious diseases, highlighted by the COVID-19 pandemic, has also increased the demand for diagnostic tools, including centrifuges, to support testing and research. With significant investments in healthcare and research, the U.S. continues to be a key market for laboratory centrifuges.

Asia Pacific Laboratory Centrifuge Market Analysis

The Asia Pacific region is witnessing rapid growth in the laboratory centrifuge market, driven by the expanding healthcare infrastructure, increasing healthcare expenditure, and rising awareness of laboratory-based diagnostics. The region's large population base and the growing burden of infectious diseases and chronic health conditions are contributing to the high demand for centrifuges in diagnostic laboratories, research facilities, and hospitals. World Health Organization data estimates that average total healthcare expenditure per capita in ASEAN is USD 630, about 4,7 percent of GDP. Also, according to the NIH, the 3 major NCDs in the Asia Pacific region are CVDs, cancer and diabetes due to the increasing loss of disability adjusted life years (DALYs). Emerging economies like China and India are investing heavily in healthcare and research infrastructure, which is further propelling the market. Additionally, the growing pharmaceutical and biotechnology industries in the region are boosting the demand for centrifuges for drug development and clinical trials.

Europe Laboratory Centrifuge Market Analysis

In Europe, the laboratory centrifuge market is being driven by the region's strong emphasis on healthcare and life sciences research, particularly in countries such as Germany, the UK, and France. Europe's aging population and the increasing focus on personalized medicine are fueling the demand for diagnostic tools that include centrifuges. According to WHO, in 2021, there were 215 Million aged population in Europe; by 2030, it is projected to be 247 Million. Furthermore, the growing investments in biotechnology and pharmaceutical sectors, along with advancements in automation and laboratory technology, are driving the growth of the centrifuge market. According to the McKinsey and Company, by 2018, the average size of biotech M&A deals in Europe had grown to USD165 Million—20 percent per annum growth since 2012. The region also benefits from a high standard of healthcare, which encourages the use of cutting-edge laboratory equipment.

Latin America Laboratory Centrifuge Market Analysis

In Latin America, the laboratory centrifuge market is growing due to the increasing focus on healthcare improvements and the expansion of diagnostic services in countries such as Brazil and Mexico. According to the ITA, Brazil is the largest healthcare market in Latin America and spends 9.47% of its GDP on healthcare, which represents USD161 Billion. The demand for laboratory centrifuges is being driven by a rise in healthcare investments, particularly in diagnostics and clinical research. Moreover, the increasing prevalence of diseases such as diabetes, cancer, and cardiovascular conditions in the region is stimulating the need for accurate diagnostic tools, including laboratory centrifuges. Government initiatives to improve healthcare access in underserved areas also support the growth of the market.

Middle East and Africa Laboratory Centrifuge Market Analysis

In the Middle East and Africa, the laboratory centrifuge market is being driven by significant advancements in healthcare infrastructure, particularly in countries like the United Arab Emirates, Saudi Arabia, and South Africa. Governments in the region are investing in modernizing their healthcare systems and improving diagnostic capabilities, which is boosting demand for laboratory equipment like centrifuges. According to the World Economic Forum, in 2023, Saudi Arabia allocated more than USD 50 Billion into various initiatives aimed at transforming its healthcare system, including a significant focus on digital health services. Additionally, the growing focus on medical research, combined with rising incidences of infectious diseases, is creating a need for efficient diagnostic and research tools. The expansion of medical tourism in the region also plays a role in increasing demand for state-of-the-art laboratory equipment.

Competitive Landscape:

The market is highly competitive, with, prominent laboratory centrifuge suppliers focusing on strategic partnerships, collaborations, acquisitions, and new software launches to stay ahead. Leading market participants prioritize constant innovation to create a seamless client-customer interaction. In June 2021, for instance, Quest Diagnostics completed its acquisition of Mercy's Outreach Laboratory Services. The acquisition aimed to improve access to innovative, high-quality, and low-cost laboratory services in the Midwest, offering inexpensive care. In recent years, prominent players have introduced centrifuges with upgraded rotors and other features. To expand their market reach and product portfolios, several key players are acquiring or merging with other companies. This strategy allows them to leverage the strengths of merged entities to increase market share and influence in various regional markets. Companies are expanding their operations into emerging markets where there is increasing demand for research and diagnostics, thereby creating a positive.

The report provides a comprehensive analysis of the competitive landscape in the laboratory centrifuge market with detailed profiles of all major companies, including:

- Agilent Technologies, Inc.

- Andreas Hettich GmbH

- Becton, Dickinson and Company

- Cardinal Health

- DH Life Sciences, LLC

- Eppendorf SE

- Hermle Labortechnik GMBH

- KUBOTA Corporation

- Qiagen N.V.

- Sartorius AG

- Sigma Laborzentrifugen GMBH

- Thermo Fisher Scientific Inc.

Latest News and Developments:

- January 5, 2024: Hettich Group announced its acquisition of Kirsch Medical, a leading producer of cooling and freezing solutions tailored for laboratories and healthcare settings. This strategic acquisition aims to enhance Hettich's capabilities in developing advanced laboratory centrifuge solutions. By integrating Kirsch's expertise in refrigeration technology, Hettich plans to expand its product range and improve its offerings for the medical and scientific sectors. The move underscores Hettich's commitment to innovation and strengthening its presence in laboratory equipment markets.

- June 2023: Becton, Dickinson and Company launched a new robotic system “BD FACSDuet” to automate clinical flow cytometry. The premium sample preparation system leverages liquid-handling robotics to automate the entire sample preparation process, for both in vitro diagnostics (IVD) and user-defined tests, including cocktailing, washing, and centrifuging.

- July 2024: The Hettich Group, a third-generation family-owned life science equipment company renowned for its laboratory centrifuges, has announced a strategic growth partnership with Bregal Unternehmerkapital GmbH. This collaboration aims to bolster Hettich's market presence and drive innovation in the laboratory equipment sector.

- April 2023: Eppendorf, a prominent life science company, has unveiled the Centrifuge 5427 R, marking its debut in the microcentrifuge segment equipped with hydrocarbon cooling. This innovation aims to enhance sustainability in laboratory environments by offering a refrigerated device that utilizes a natural cooling agent with a Global Warming Potential (GWP) nearly zero.

Laboratory Centrifuge Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Model Types Covered | Benchtop Centrifuges, Floor-Standing Centrifuges |

| Rotor Designs Covered | Fixed-Angle Rotors, Swinging-Bucket Rotors, Vertical Rotors, Others |

| Intended Uses Covered | General Purpose Centrifuges, Clinical Centrifuges, Preclinical Centrifuges |

| Applications Covered | Diagnostics, Microbiology, Cellomics, Genomics, Proteomics, Blood Component Separation, Others |

| End-Users Covered | Hospitals, Biotechnology and Pharmaceutical Company, Academic and Research Institutions |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Agilent Technologies, Inc., Andreas Hettich GmbH, Becton, Dickinson and Company, Cardinal Health, DH Life Sciences, LLC, Eppendorf SE, Hermle Labortechnik GMBH, KUBOTA Corporation, Qiagen N.V., Sartorius AG, Sigma Laborzentrifugen GMBH, Thermo Fisher Scientific Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the laboratory centrifuge market from 2020-2034.

- The laboratory centrifuge market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the laboratory centrifuge industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Laboratory Centrifuge Market Report

A laboratory centrifuge is a device used to separate components of a fluid by utilizing centrifugal force. It plays a vital role in research, diagnostics, and clinical laboratories by enabling the separation of particles such as cells, proteins, and nucleic acids for scientific and medical applications.

The global laboratory centrifuge market was valued at USD 1.86 Billion in 2025.

IMARC estimates the global laboratory centrifuge market to exhibit a CAGR of 3.53% during 2026-2034.

The market is driven by the growing demand for advanced diagnostic tools, increasing R&D in life sciences and biotechnology, advancements in centrifuge technologies, and the rising prevalence of chronic diseases requiring accurate diagnostics.

Equipment represented the largest segment by product type, driven by its versatility and efficiency in various scientific and medical applications.

Benchtop centrifuges lead the market by model type due to their affordability, ease of use, and versatility for diverse laboratory procedures.

Fixed-angle rotors are the leading segment by rotor design, driven by their efficiency in high-throughput processing and precise sample separation.

General purpose centrifuges are the leading segment by intended use, driven by their ability to handle various sample types and volumes for diverse applications.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and the Middle East and Africa, wherein North America currently dominates the market due to advanced healthcare infrastructure and significant R&D investments.

Some of the major players in the global laboratory centrifuge market include Agilent Technologies, Inc., Andreas Hettich GmbH, Becton, Dickinson and Company, Cardinal Health, DH Life Sciences, LLC, Eppendorf SE, Hermle Labortechnik GMBH, KUBOTA Corporation, Qiagen N.V., Sartorius AG, Sigma Laborzentrifugen GMBH, and Thermo Fisher Scientific Inc., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)