Latin America Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Region, 2026-2034

Latin America Data Center Market Size, Share, Trends & Forecast (2026-2034)

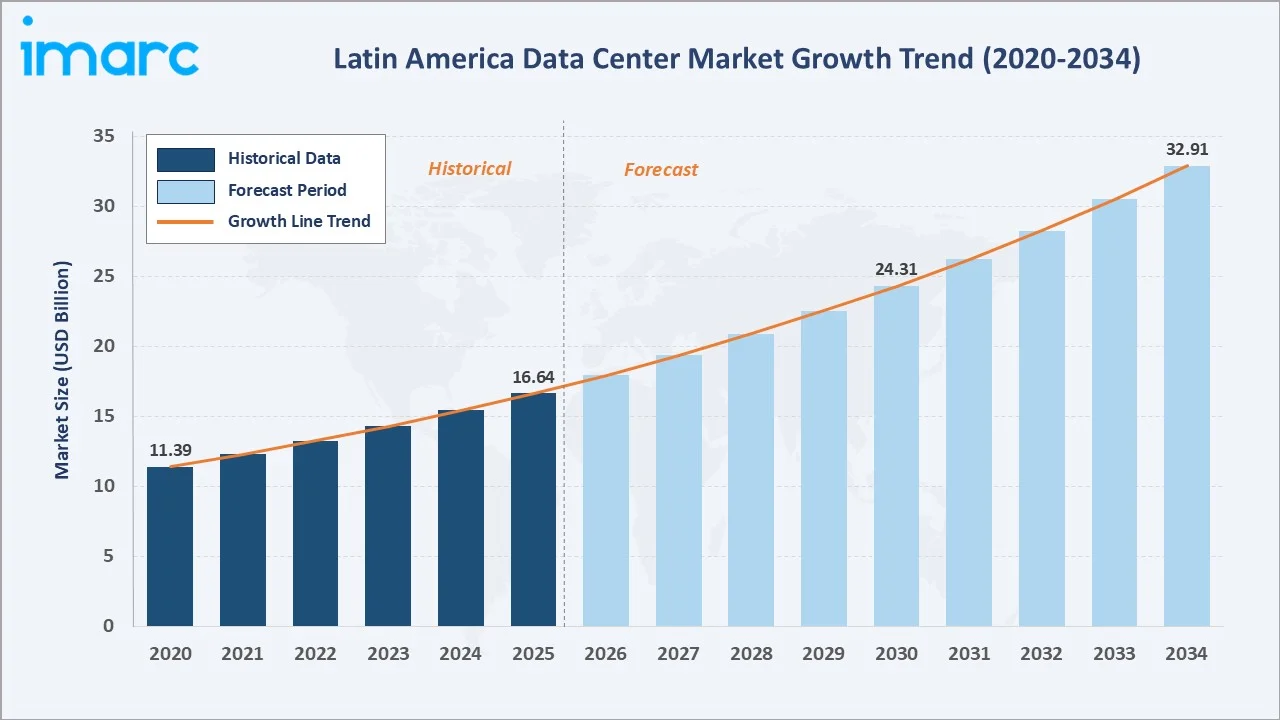

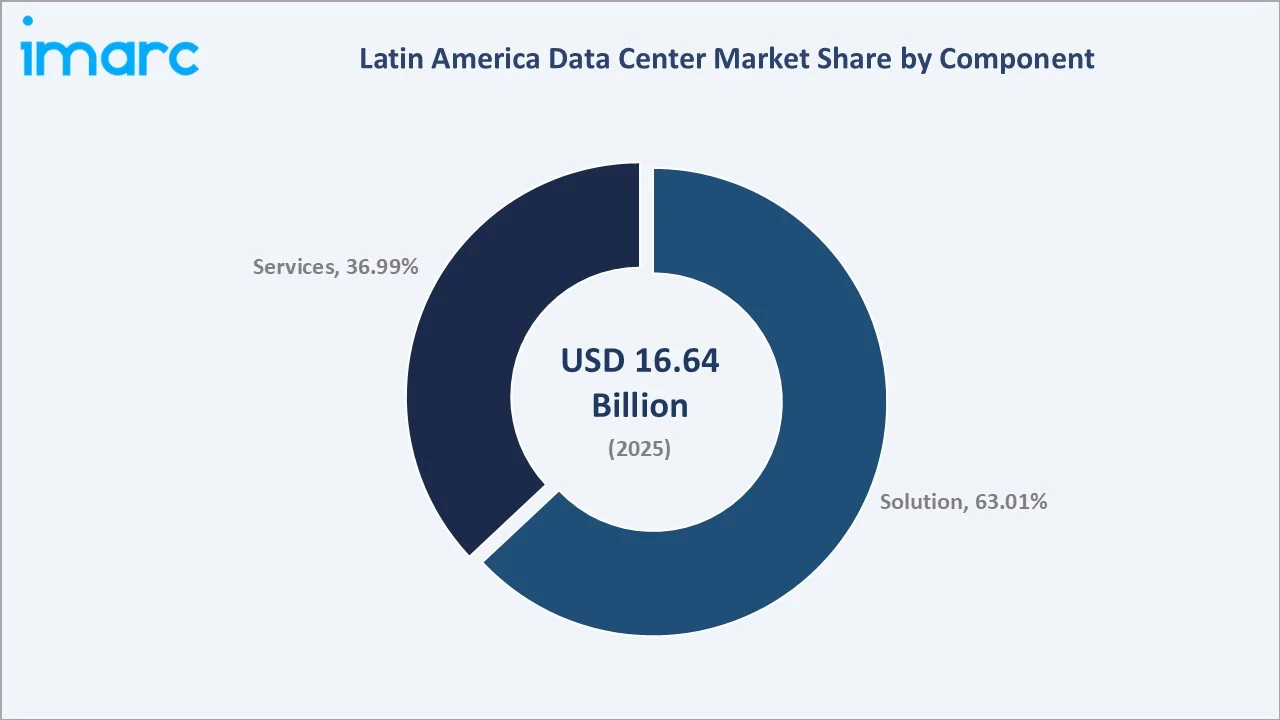

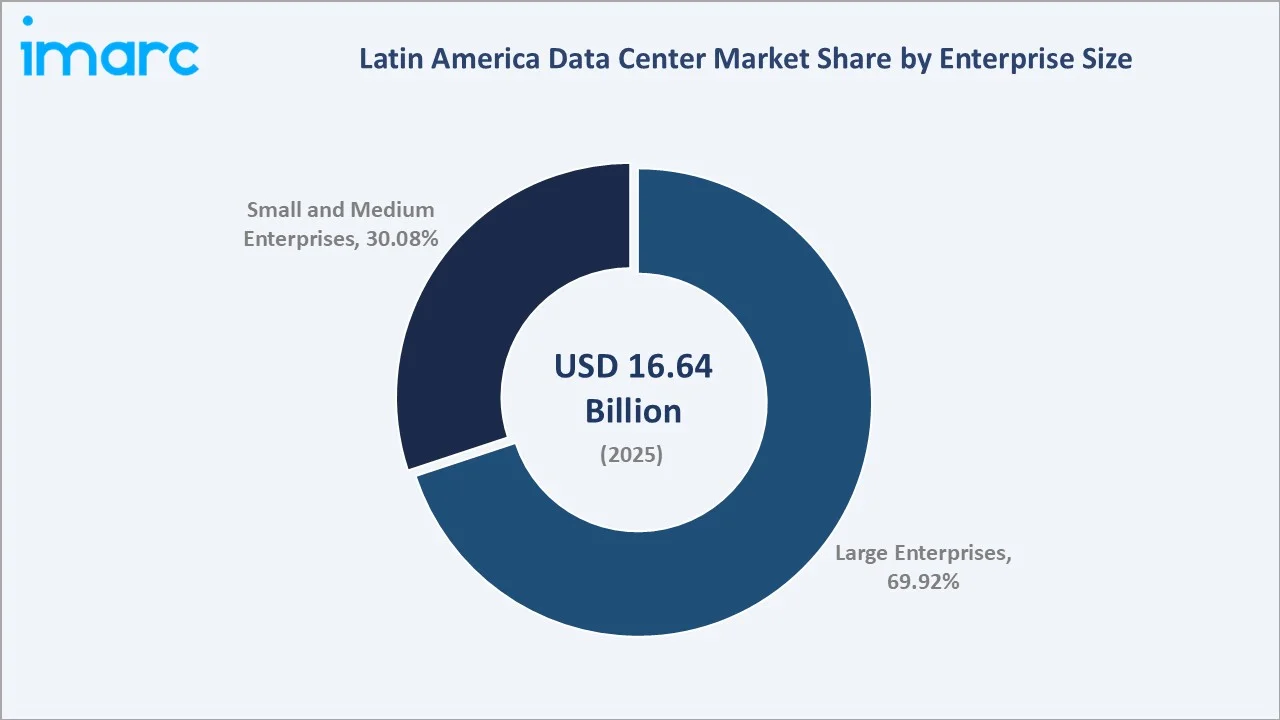

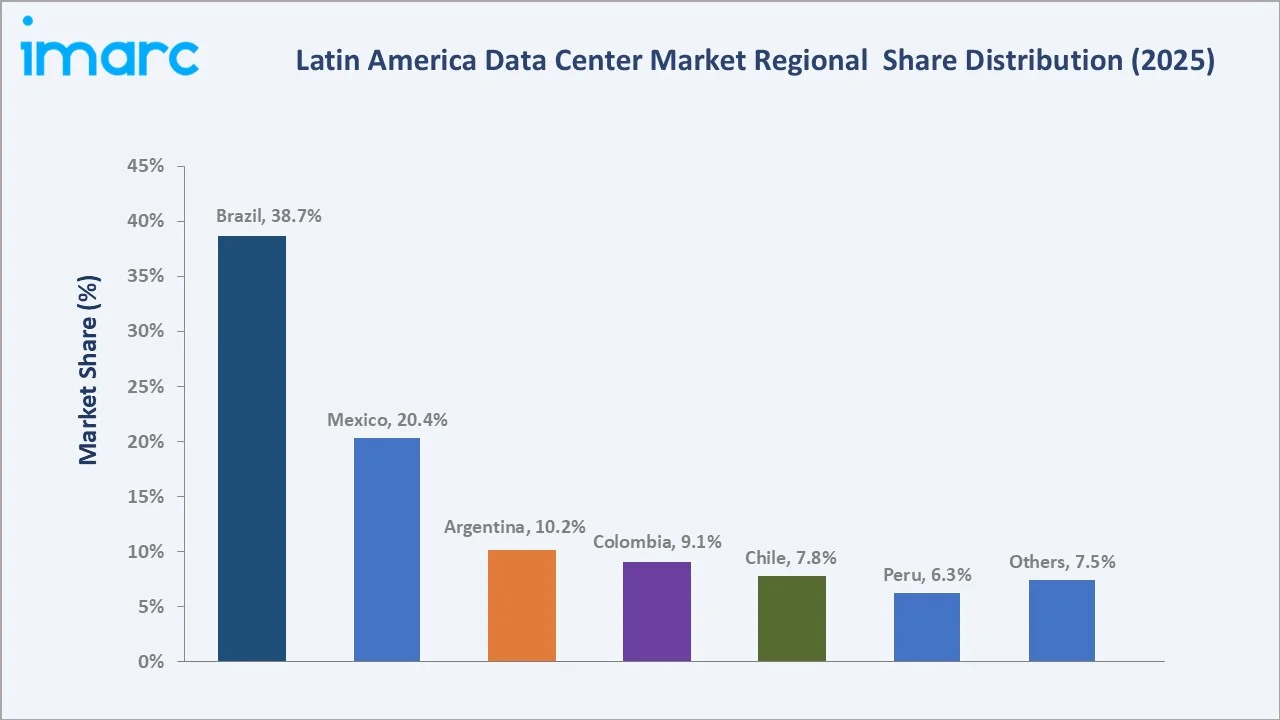

The Latin America data center market reached USD 16.64 Billion in 2025 and is projected to reach USD 32.91 Billion by 2034, growing at a CAGR of 7.87% during 2026-2034. The market is driven by rising cloud adoption, rapid digitalization, growing internet traffic, and expanding demand for colocation services. In 2024, investments in new data centers across Latin America surpassed US$2 billion, while the number of hyperscalers in the region is expected to rise to 15 by 2032. This is driving the market by accelerating cloud infrastructure expansion, improving regional computing capacity, and supporting rising demand for colocation, AI workloads, and enterprise digital transformation. Solution leads component at 63.01%. Large enterprises dominate at 69.92%. Brazil leads regionally at 38.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 16.64 Billion |

|

Forecast Market Size (2034) |

USD 32.91 Billion |

|

CAGR (2026-2034) |

7.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Solution (63.01%, 2025) |

|

Dominant Enterprise Size |

Large Enterprises (69.92%, 2025) |

|

Leading Region |

Brazil (38.7%, 2025) |

Latin America data center market expanded from USD 11.39 Billion in 2020 to USD 16.64 Billion in 2025, anchored at USD 24.31 Billion in 2030, and forecast to reach USD 32.91 Billion by 2034. COVID-19 accelerated the region's cloud adoption timeline as enterprises and government entities simultaneously validated remote work infrastructure, digital service delivery, and cloud-hosted business continuity, while exposing the vulnerability of purely on-premise systems.

To get more information on this market, Request Sample

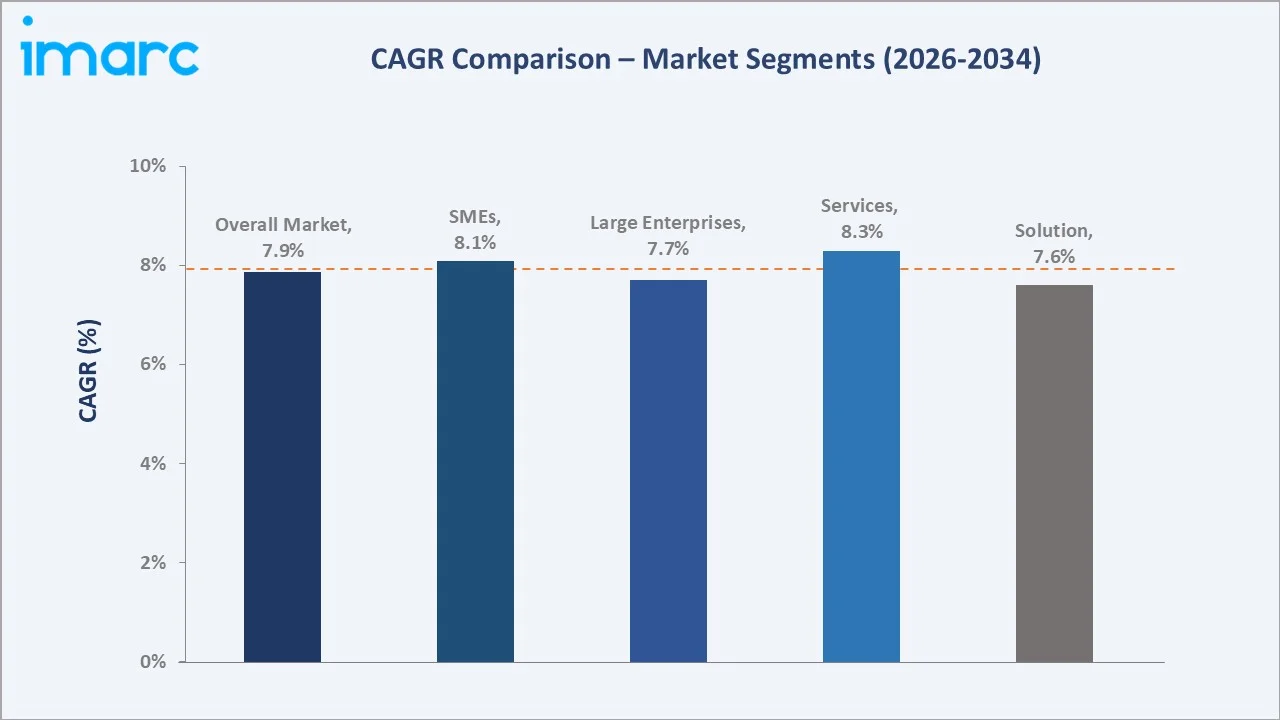

Services grow fastest at ~8.3% CAGR through managed colocation, cloud migration consulting, DC-as-a-service, and remote hands services, creating above-hardware revenue growth as Latin American enterprises shift from CAPEX-intensive on-premise infrastructure toward OPEX-based managed service consumption. SMEs grow at ~8.1% CAGR through cloud-first IT adoption, reducing the entry barrier to enterprise-grade data processing infrastructure above the traditional large enterprise data center dominance.

Executive Summary

Latin America data center market at USD 16.64 Billion in 2025 represents the most commercially underdeveloped major regional data center market relative to economic scale, with Latin America's combined GDP generating data center investment at below-Asia-Pacific-equivalent density, creating the most commercially compelling emerging market data center investment argument through demonstrated hyperscaler, sovereign wealth fund, and private equity conviction above more mature regional markets' lower incremental returns. The market is projected to reach USD 32.91 Billion by 2034.

Solution at 63.01% leads through greenfield data center construction CAPEX dominance. Large enterprises at 69.92% dominate through financial sector, telecom, and government institutional data center investment, above SME cloud adoption. Brazil leads at 38.7% through São Paulo's hyperscaler hub concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Solution - 63.01% share (2025) |

|

Dominant Enterprise Size |

Large Enterprises - 69.92% market share (2025) |

|

Leading Region |

Brazil - 38.7% share (2025) |

|

Market Opportunity |

AI GPU cluster and generative AI training infrastructure; hyperscaler co-location campuses; edge DC for 5G MEC deployment; green DC with renewable energy certification |

Key Analytical Observations Supporting The Above Data:

- Solution at 63.01%: The solution segment dominates as enterprises increasingly adopt integrated infrastructure, cooling, power management, networking, and security solutions. Rising cloud, colocation, and hyperscale deployments are further increasing demand for end-to-end data center solutions.

- Large Enterprises at 69.92%: The large enterprises dominate as major banks, telecom firms, cloud providers, and multinational companies require high-capacity, secure, and scalable IT infrastructure. Their growing use of cloud, AI, big data, and digital services is further increasing demand for advanced data center solutions.

- Brazil at 38.7%: Brazil dominates due to its large digital economy, strong cloud adoption, and high concentration of enterprises, telecom operators, and hyperscale investments. Growing demand for colocation, AI workloads, fintech, and e-commerce services further strengthens Brazil’s regional leadership.

Latin America Data Center Market Overview

Latin America data center market operates within the broader global data center market as a structurally underpenetrated region with above-average growth potential. The region's commercial uniqueness is its dual-speed development, which creates both a premium hyperscale campus and an emerging secondary market opportunity simultaneously.

The Latin America data center ecosystem integrates global hardware and power infrastructure supply, international and regional data center operators, national telecom carrier-owned facilities, submarine cable connectivity, and the regulatory framework. Macroeconomic factors include rapid digitalization, rising cloud adoption, expanding e-commerce, and growing enterprise IT spending.

Market Dynamics

To evaluate market opportunities, Request Sample

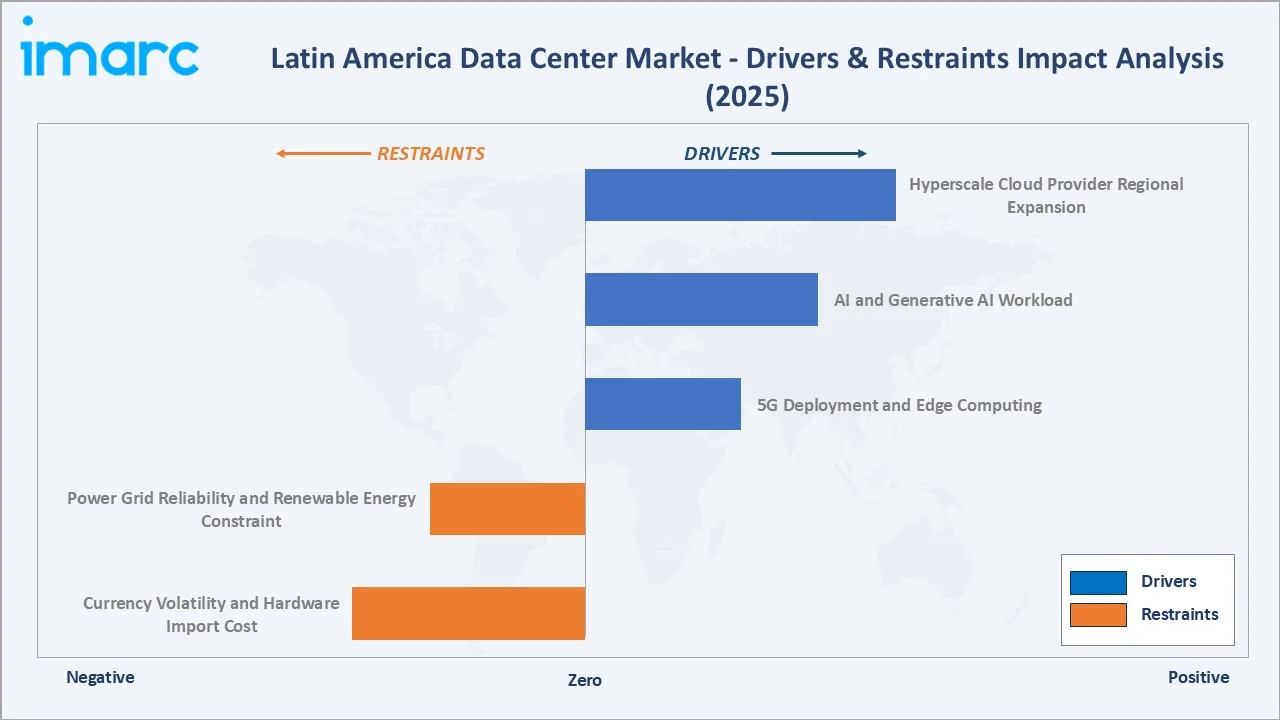

Market Drivers

- Hyperscale Cloud Provider Regional Expansion: Hyperscale cloud provider expansion is driving the market as key players increase regional capacity to support cloud, AI, and enterprise workloads. New hyperscale facilities improve latency, data processing speed, and service reliability for local businesses. This expansion also attracts colocation providers, telecom operators, and infrastructure investors, strengthening the overall data center ecosystem.

- AI and Generative AI Workload: AI and generative AI workloads are increasing demand for high-performance computing, GPU servers, and scalable cloud infrastructure. These workloads require advanced cooling, reliable power systems, and low-latency connectivity. As enterprises adopt AI for banking, retail, healthcare, telecom, and customer analytics, regional data center capacity is expanding rapidly. GenAI could affect around 26% to 38% of jobs in Latin America, mainly by enhancing and reshaping work rather than fully replacing workers. It also indicates that nearly 8% to 14% of jobs could benefit from productivity gains through GenAI. This supports data center growth by increasing demand for AI-ready cloud infrastructure, GPU capacity, faster data processing, and secure enterprise platforms as more businesses adopt GenAI tools across workflows.

- 5G Deployment and Edge Computing: 5G deployment and edge computing are increasing the demand for low-latency, locally distributed data processing. By the end of 2026, 5G is projected to account for nearly 43% of mobile subscriptions across Latin America. As 5G adoption rises, telecom operators and cloud providers are investing in edge data centers to support IoT, streaming, gaming, fintech, and smart city applications. As telecom operators expand 5G networks, more edge facilities are needed to support IoT, streaming, gaming, fintech, and smart city applications. This is encouraging investments in smaller, regional data centers closer to end users.

Market Restraints

- Power Grid Reliability and Renewable Energy Constraint: Power grid reliability and renewable energy constraints increase risks of downtime, unstable power supply, and higher backup power costs. Data centers require continuous electricity, but grid limitations in some countries can restrict large-scale facility expansion. Limited availability of reliable renewable energy also challenges sustainability targets. This makes site selection, power procurement, and operating costs more complex for data center operators.

- Currency Volatility and Hardware Import Cost: Currency volatility and hardware import costs increase the cost of servers, cooling systems, power equipment, and networking hardware, much of which is imported. Fluctuating exchange rates make project budgeting and long-term contracts more uncertain for operators. Higher import costs can delay new facility construction, raise CAPEX, and reduce profitability. This particularly affects smaller providers with limited financial flexibility.

Market Opportunities

- Increasing Demand for Colocation Services: Increasing demand for colocation services is creating significant opportunities as enterprises seek cost-effective alternatives to building and managing their own facilities. Colocation providers offer scalable infrastructure, reliable connectivity, and enhanced security while reducing capital expenditure. Growing cloud adoption, digital transformation initiatives, and demand for low-latency services are further driving colocation uptake across the region. This is encouraging investments in new and expanded data center facilities.

- Smart City, IoT, and Connected Device Deployment: Smart city, IoT, and connected device deployment are increasing the demand for real-time data processing, storage, and low-latency connectivity. Applications such as traffic monitoring, public safety, utilities, healthcare, and smart buildings generate large data volumes. This supports the need for edge and regional data centers closer to users and devices, driving new infrastructure investments.

Market Challenges

- Limited Connectivity Infrastructure in Some Regions: Limited connectivity infrastructure in some regions is restricting reliable, high-speed data transmission. Weak fiber networks and uneven broadband coverage can increase latency and reduce service quality for cloud, colocation, and edge deployments. This limits the feasibility of building data centers outside major urban hubs. As a result, operators face higher network investment needs and slower expansion in underserved markets.

- Land Acquisition and Site Selection Challenges: Land acquisition and site selection challenges are limiting Latin America data center growth as operators need large, secure sites with reliable power, fiber connectivity, water access, and low disaster risk. Suitable locations near major cities can be expensive or limited. Delays in permits, zoning approvals, and environmental clearances can also slow project timelines. These issues raise development costs and make expansion planning more complex.

Emerging Market Trends

1. Hyperscaler Availability Zone Expansion to Secondary Markets

Hyperscaler availability zone expansion to secondary markets is emerging as cloud providers move beyond major hubs such as São Paulo and Mexico City. Expanding into secondary cities helps reduce latency, improve service resilience, and meet growing regional demand for cloud services. It also supports data localization requirements and enables businesses in underserved areas to access advanced digital infrastructure. This trend is driving investments in new regional and edge data center facilities.

2. AI Infrastructure and GPU Cluster Colocation

AI infrastructure and GPU cluster colocation are emerging as enterprises need high-density facilities to run AI, machine learning, and generative AI workloads. Colocation providers are upgrading power capacity, liquid cooling, and network connectivity to support GPU-intensive deployments. This allows businesses to access AI-ready infrastructure without building their own data centers. The trend is creating new revenue opportunities for operators offering specialized, high-performance colocation services.

3. Green Data Center Expansion

Green data center expansion is emerging in Latin America as operators focus on energy-efficient facilities powered by renewable sources. Rising demand from hyperscalers, AI workloads, and global enterprises is pushing providers to adopt efficient cooling, renewable energy procurement, and sustainability certifications. In May 2026, Rafay Systems partnered with Mexico-based AI Green Data Centers (AI-GDC) to support self-service, token-based AI solutions for educational institutions, enterprises, and public sector users across Mexico. AI-GDC aims to develop Latin America’s first HPC and AI platform, backed by over 30 years of combined IaaS experience. This trend helps reduce operating costs and carbon emissions while improving investor and customer confidence. It is also positioning Latin America as a competitive location for low-carbon digital infrastructure.

4. Nearshoring and Manufacturing Digitalization

Nearshoring and manufacturing digitalization are emerging as companies shift operations closer to North American markets and modernize factories with automation, IoT, and cloud-based systems. These activities generate higher demand for secure data storage, low-latency connectivity, and enterprise cloud services. As manufacturers adopt smart production, supply chain analytics, and connected equipment, demand for regional data center capacity increases.

Industry Value Chain Analysis

The Latin America data center value chain integrates hardware & equipment supply, data center design & construction, power & cooling infrastructure, data center platforms & software management, colocation & cloud service delivery, and operations, monitoring & maintenance.

|

Stage |

Key Participants |

|

Hardware & Equipment Supply |

Server manufacturers, storage vendors, networking equipment providers, power system suppliers, and cooling equipment manufacturers |

|

Data Center Design & Construction |

Engineering firms, EPC contractors, architects, civil construction companies, and project management consultants |

|

Power & Cooling Infrastructure |

Utility companies, renewable energy providers, UPS manufacturers, generator suppliers, and cooling technology providers |

|

Data Center Platforms & Software Management |

Virtualization software vendors, cloud platform providers, and cybersecurity solution providers |

|

Colocation & Cloud Service Delivery |

Colocation operators, hyperscale cloud providers, managed service providers, edge data center operators |

|

Operations, Monitoring & Maintenance |

Data center operators, facility management companies, security providers, maintenance service providers, and technical support teams |

Technology Landscape in the Latin America Data Center Industry

Power and Cooling Infrastructure Evolution

Power and cooling infrastructure evolution is shaping the technology landscape as operators upgrade facilities to support high-density cloud and AI workloads. Advanced cooling technologies, including liquid cooling and energy-efficient HVAC systems, are being adopted to improve performance and reduce energy consumption. At the same time, investments in intelligent power management, renewable energy integration, and backup systems are enhancing reliability and sustainability. These developments are enabling data centers to handle growing computing demands more efficiently.

Hybrid and Multi-Cloud Architecture

Hybrid and multi-cloud architecture is transforming the technology landscape as enterprises distribute workloads across private and public cloud environments to improve flexibility and resilience. Organizations are increasingly adopting multi-cloud strategies to avoid vendor lock-in, optimize costs, and meet regulatory requirements. This trend is driving demand for advanced connectivity, cloud interconnection services, and data management platforms. As a result, data centers are evolving into integrated digital hubs that support seamless workload mobility across multiple cloud ecosystems.

Data Center Infrastructure Management (DCIM) Platforms

Data center infrastructure management (DCIM) platforms provide centralized monitoring and control of power, cooling, space, and IT assets. These platforms help operators improve operational efficiency, optimize energy consumption, and enhance uptime across facilities. In December 2025, TERRANOVA, a hyperscale data center platform launched by Actis and backed by General Atlantic, officially entered the Latin American market. The platform aims to support the region’s next stage of digital expansion by developing energy-efficient, customer-centric data centers for rising AI and cloud infrastructure demand across Brazil, Mexico, and Chile. As large-scale data centers expand, DCIM solutions become essential for improving operational visibility, predictive maintenance, and sustainable infrastructure management.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

63.01% |

2025 |

|

Type |

Hyperscale |

40.9% |

2025 |

|

Enterprise Size |

Large Enterprises |

69.92% |

2025 |

|

End User |

IT and Telecom |

34.91% |

2025 |

|

Region |

Brazil |

38.7% |

2025 |

By Component

Solution leads at 63.01% (2025). The solution segment encompasses server and storage hardware, power infrastructure, cooling systems, and network switching, creating the CAPEX-intensive physical infrastructure foundation for Latin America's above-trend data center construction.

To access detailed market analysis, Request Sample

Services at 36.99% grows fastest at ~8.3% CAGR through managed colocation, cloud migration consulting, DCIM-as-a-service, and remote monitoring services, creating above-hardware recurring revenue for data center operators and managed service providers.

By Enterprise Size

Large enterprises lead at 69.92% (2025). Large enterprises encompass financial institutions, telecom operators, government agencies, and multinationals requiring a Tier III/IV enterprise-grade data center with regulatory compliance and customized security posture above standard retail colocation.

Small and medium enterprises (SMEs) at 30.08% grow fastest at ~8.1% CAGR through cloud-first digital adoption.

Regional Market Insights

|

Country |

Share (2025) |

Key Latin America Data Center Market Drivers & Characteristics |

|

Brazil |

38.7% |

Supported by strong cloud adoption, hyperscale investments, a large enterprise base, and growing demand from fintech, e-commerce, and digital services sectors. |

|

Mexico |

20.4% |

Benefits from its expanding nearshoring activities, growing cloud demand, and increasing investments in hyperscale and colocation facilities. |

|

Argentina |

10.2% |

Supported by rising digitalization, increasing enterprise cloud adoption, and growing demand for local data storage and processing capabilities. |

|

Colombia |

9.1% |

Emerging as a regional digital hub due to improving connectivity infrastructure, growing cloud deployments, and increasing investments from telecom and technology providers. |

|

Chile |

7.8% |

Driven by stable business conditions, strong renewable energy availability, advanced telecommunications infrastructure, and increasing hyperscale investments. |

|

Peru |

6.3% |

Witnessing growing demand for colocation and cloud services as businesses accelerate digital transformation, and internet penetration continues to improve. |

|

Others |

7.5% |

Other Latin American countries are gradually expanding their data center footprint through improvements in digital infrastructure, cloud adoption, mobile connectivity, and enterprise IT investments. |

Brazil's 38.7% dominance reflects São Paulo's hyperscaler campus concentration. Mexico's 20.4% reflects technology park and nearshoring industrial IT demand. Argentina's 10.2% reflects a sophisticated but economically constrained market.

Colombia's 9.1% reflects the emergence as a regional cloud hub through hyperscaler investment and fintech growth. Chile's 7.8% reflects renewable energy advantage and OECD-grade regulatory stability. Peru's 6.3% reflects the most commercially anticipated region, creating above-current trajectory demand acceleration.

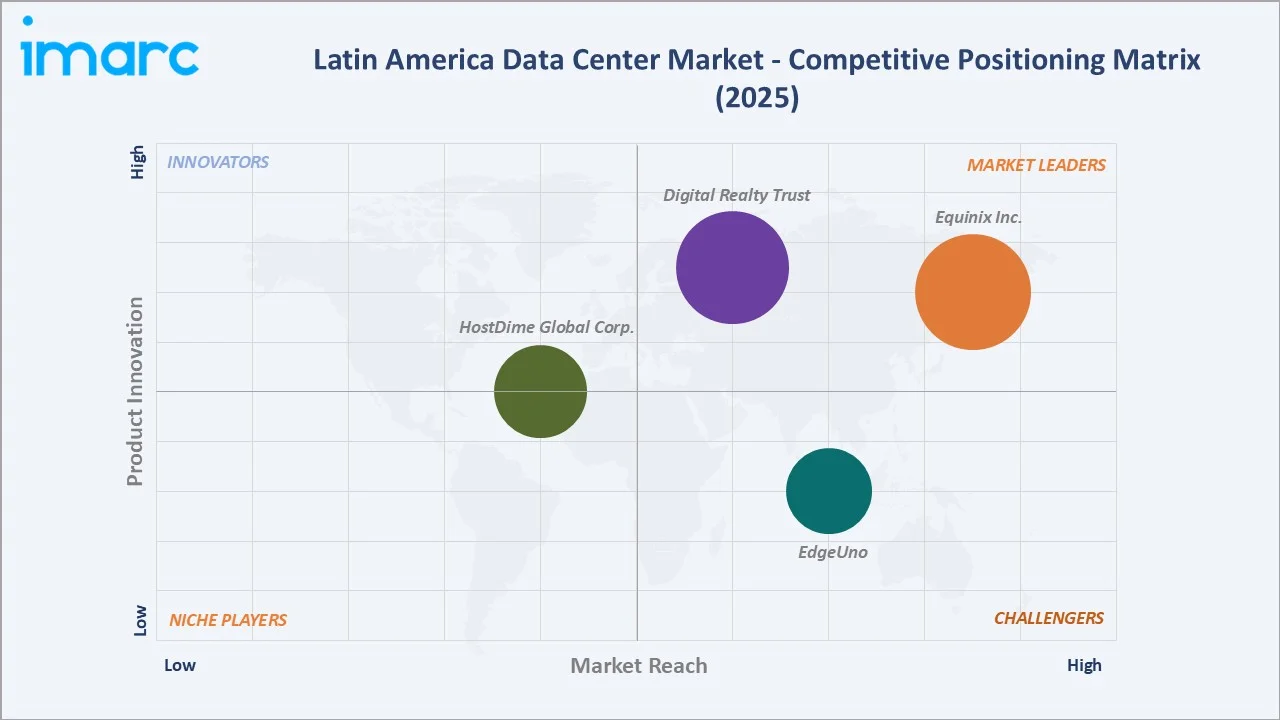

Competitive Landscape

Latin America data center competitive landscape is commercially stratified across three tiers: global colocation and infrastructure specialists, regional telecom carrier-owned operators, and hyperscale developer specialists. The most commercially significant competitive dynamic is the separation between carrier-neutral colocation valued for the interconnection ecosystem and carrier-owned colocation valued for bundled network-data-center procurement above best-of-breed technology selection.

|

Company |

Key Data Center Locations |

Market Position |

Core Strength |

|

|

Rio de Janeiro, São Paulo, Santiago, Lima, Mexico City, Monterrey |

Market Leader |

Equinix, Inc. is a leading provider of interconnected data center services in Latin America, serving as a critical hub for cloud, enterprise, and network connectivity. |

|

|

Rio de Janeiro, Santiago, São Paulo |

Market Leader |

Digital Realty Trust plays a central role in the Latin American data center market primarily through its joint venture and acquisition of Ascenty, establishing it as a dominant player in the region. |

|

|

João Pessoa, São Paulo, Bogotá |

Established Player |

HostDime Global Corp. is a significant player in the Latin American data center market, focusing on designing, constructing, and operating purpose-built, Tier IV data centers, particularly in Colombia, Brazil, and Mexico. |

|

|

Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Mexico, Peru |

Strong Challenger |

EdgeUno operates highly interconnected, carrier-neutral Tier III and IV data centers across Latin American countries, specializing in low-latency edge computing. |

Latin America data center competitive landscape is being reshuffled through three forces: hyperscale developer specialization, sustainability differentiation, and sovereign cloud demand.

Key Company Profiles

Equinix Inc.

Equinix Inc. is one of the leading data center and digital infrastructure providers operating in the Latin America data center market. The company offers carrier-neutral colocation, interconnection, cloud connectivity, and digital infrastructure services through a network of data centers across key Latin American markets.

- Key Data Center Locations: Rio de Janeiro, São Paulo, Santiago, Lima, Mexico, Monterrey.

- Recent Developments: In April 2026, Equinix opened its latest data center, SP6, in Santana de Parnaíba within the São Paulo metropolitan area. The facility spans 32,045 sq ft and involved an investment of US$114 million, with the first phase reportedly providing 1,125 racks.

- Strategic Focus: Expanding its interconnection and carrier-neutral data center ecosystem across key Latin American markets to support growing cloud, AI, and digital transformation demand.

Digital Realty Trust

Digital Realty Trust is a leading global data center operator and a prominent participant in the Latin America data center market. The company provides colocation, interconnection, and hyperscale data center solutions through strategically located facilities across key Latin American markets. Through its regional presence, Digital Realty supports cloud providers, enterprises, telecom operators, and digital service companies with scalable and secure infrastructure.

- Key Data Center Locations: Rio de Janeiro, Santiago, São Paulo.

- Recent Developments: In June 2024, Digital Realty launched its ServiceFabric service orchestration platform in Latin America, initially available in São Paulo, Brazil, through Ascenty, its joint venture with Brookfield Infrastructure. The platform is designed to help regional customers connect workflows, applications, cloud environments, and digital ecosystems more efficiently through PlatformDIGITAL, Digital Realty’s global data center platform.

- Strategic Focus: Expanding hyperscale and colocation infrastructure across key Latin American markets to meet growing demand for cloud computing, AI workloads, and enterprise digital transformation.

Market Concentration Analysis

Latin America data center market is moderately concentrated at the hyperscale and carrier-neutral colocation tier and highly fragmented nationally across the Latin America market, where each country's largest data center operator commands 20-40% national market share above a long tail of government-owned and SME hosting operators. Market concentration is accelerating through institutional capital investment, creating capacity scale advantages above self-funded national operators in hyperscale and AI infrastructure investment.

Investment & Growth Opportunities

Highest Growth Segments

AI GPU cluster colocation (~15-20% CAGR from emerging application base), green data center with renewable energy certification (~10-12% CAGR), hyperscaler campus development in secondary countries (~12-15% CAGR), edge data center (~18-22% CAGR from near-zero base), sovereign cloud for regulated industries (~9-11% CAGR through data sovereignty regulation expansion), and managed security services (~10-12% CAGR through Latin America's above-global cybersecurity incident rate) represent the highest-growth data center investment vectors through 2034.

Investment Themes

- AI-ready liquid-cooled data center campus: Developing liquid-cooled high-density colocation halls within or adjacent to existing São Paulo and Mexico City carrier-neutral campus creates the most commercially premium above-standard-colocation product for Latin America's most commercially urgent new data center demand.

- Greenfield data center campus: Developing 50-150 MW purpose-built campus of hyperscaler availability zone announcement creates first-mover developer advantage, each hyperscaler region requiring 150-500 MW of associated colocation above own-developed capacity, creating above-vacant-land value appreciation for developed and pre-committed hyperscale campus above undeveloped site.

Future Market Outlook (2026-2034)

The Latin America data center market is projected to grow from USD 16.64 Billion in 2025 to USD 32.91 Billion by 2034, delivering a 7.87% CAGR over the forecast period. The market's anchor value of USD 24.31 Billion in 2030 represents the Latin America data center industry at the peak construction phase. Hyperscaler availability zones in all primary countries are creating above-current geographic coverage, AI GPU cluster infrastructure reaching commercial deployment scale above experimental proof-of-concept, and 5G edge data center creating geographic distribution above primary metropolitan concentration.

Three structural forces define Latin America data center growth through 2034: Hyperscaler global expansion creating greenfield Latin America country entry above existing region expansion, AI infrastructure creating a premium data center product tier, and sustainability regulation creating a renewable energy certified data center as hyperscaler procurement prerequisite.

Research Methodology

Primary Research

Primary research comprised structured interviews with Latin America data center industry stakeholders, including VP operations, CEOs, CTOs, regional directors, data center procurement managers, the LATAM infrastructure lead, and an enterprise IT survey from large and mid-enterprise organizations across Brazil, Mexico, Colombia, Chile, and Peru.

Secondary Research

Secondary research encompassed the annual data center survey, Brazil telecommunications infrastructure, datacenter dynamics Latin America market report, company annual reports, and Latin America mobile economy. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using the installed capacity model: Latin America data center installed IT load by country estimated from datacenter dynamics, structure research, and primary data sources, multiplied by average revenue per MW by facility tier and operator type. Country growth rate calibrated against hyperscaler region announcement pipeline, financial regulation digital mandate, and 5G spectrum obligation timeline. Services segment modelled separately as % of solution segment with above-solution CAGR through managed service adoption.

Latin America Data Center Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Services |

| Types Covered | Colocation, Hyperscale, Edge, Others |

| Enterprise Sizes Covered | Large Enterprise, Small and Medium Enterprises |

| End Users Covered | BFSI, IT and Telecom, Government, Energy and Utilities, Others |

| Regions Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | Equinix Inc., Digital Realty Trust, HostDime Global Corp., EdgeUno, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Latin America Data Center Market Report

The Latin America data center market reached USD 16.64 Billion in 2025, driven by rising cloud adoption, hyperscale expansion, growing AI workloads, and increasing demand for colocation services. Rapid digitalization across banking, telecom, e-commerce, and government sectors is further boosting the need for scalable, secure, and low-latency data infrastructure.

The Latin America data center market grows at 7.87% CAGR during 2026-2034, reaching USD 32.91 Billion by 2034. The overall growth is sustained by hyperscale cloud expansion, AI GPU cluster infrastructure demand, data sovereignty regulation creating in-country hosting mandate, and 5G edge computing expanding geographic addressable market beyond primary metropolitan concentration.

Solution leads at 63.01% through Latin America's active greenfield data center construction phase, requiring above-services-proportional hardware CAPEX.

Large enterprises lead at 69.92% through financial sector, telecom, and government institutional data center investment, driven by regulatory compliance requirements, creating non-discretionary data center procurement.

Brazil leads at 38.7% through São Paulo's hyperscaler campus concentration.

Leading companies include Equinix Inc., Digital Realty Trust, HostDime Global Corp., and EdgeUno, among others.

The Latin America data center market is projected to reach approximately USD 24.31 Billion by 2030, with the AI-ready liquid-cooled GPU cluster colocation segment from a near-zero base as hyperscaler AI training demand reaches Latin America commercial scale, hyperscaler availability zones creating above-current geographic coverage, and green data center with renewable PPA becoming standard specification above uncertified facilities for hyperscaler anchor tenant procurement.

Three priority investment opportunities: AI-ready liquid-cooled hyperscale campus creating the most commercially premium above-standard-colocation product for Latin America's AI workload market, greenfield hyperscale campus development, and sovereign cloud platform development for Brazil's financial sector, creating above-hyperscaler regulatory compliance documentation positioning for the most commercially compliance-intensive single enterprise segment in Latin America.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)