Latin America Organic Coffee Market Size, Share, Trends and Forecast by Type, Packaging Type, Sales Channel, and Country, 2026-2034

Latin America Organic Coffee Market Size, Share, Trends & Forecast (2026-2034)

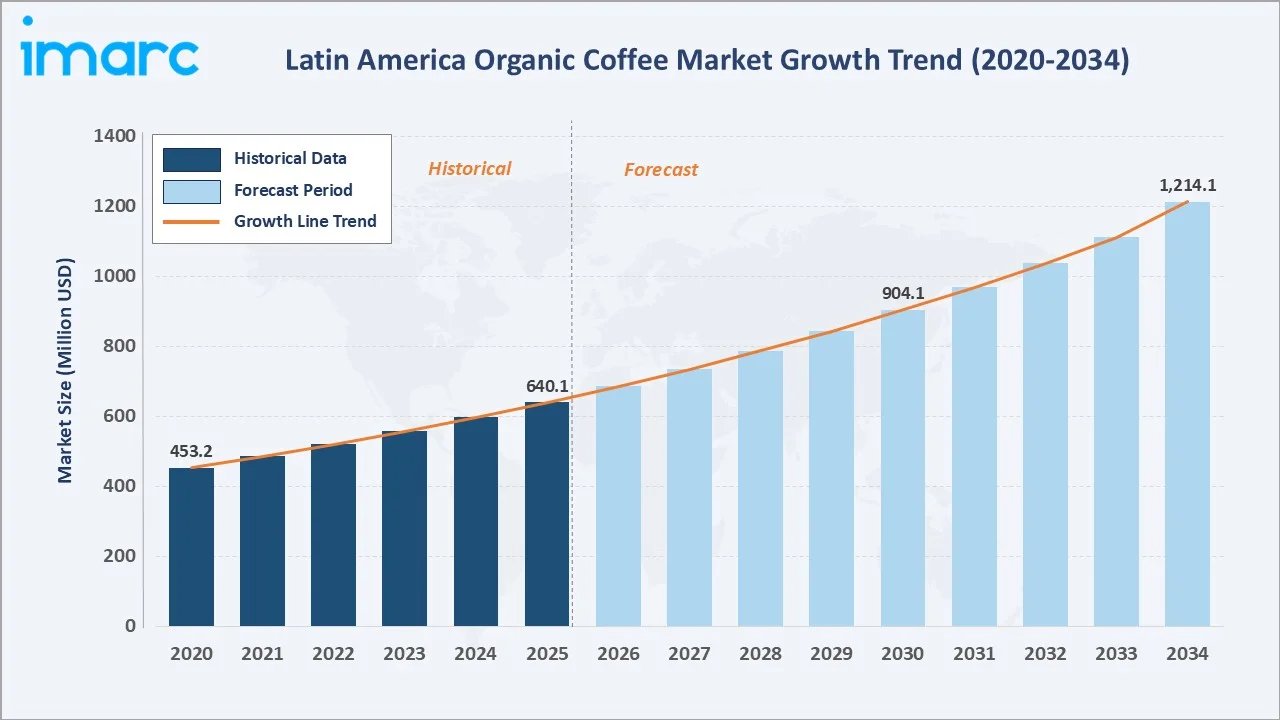

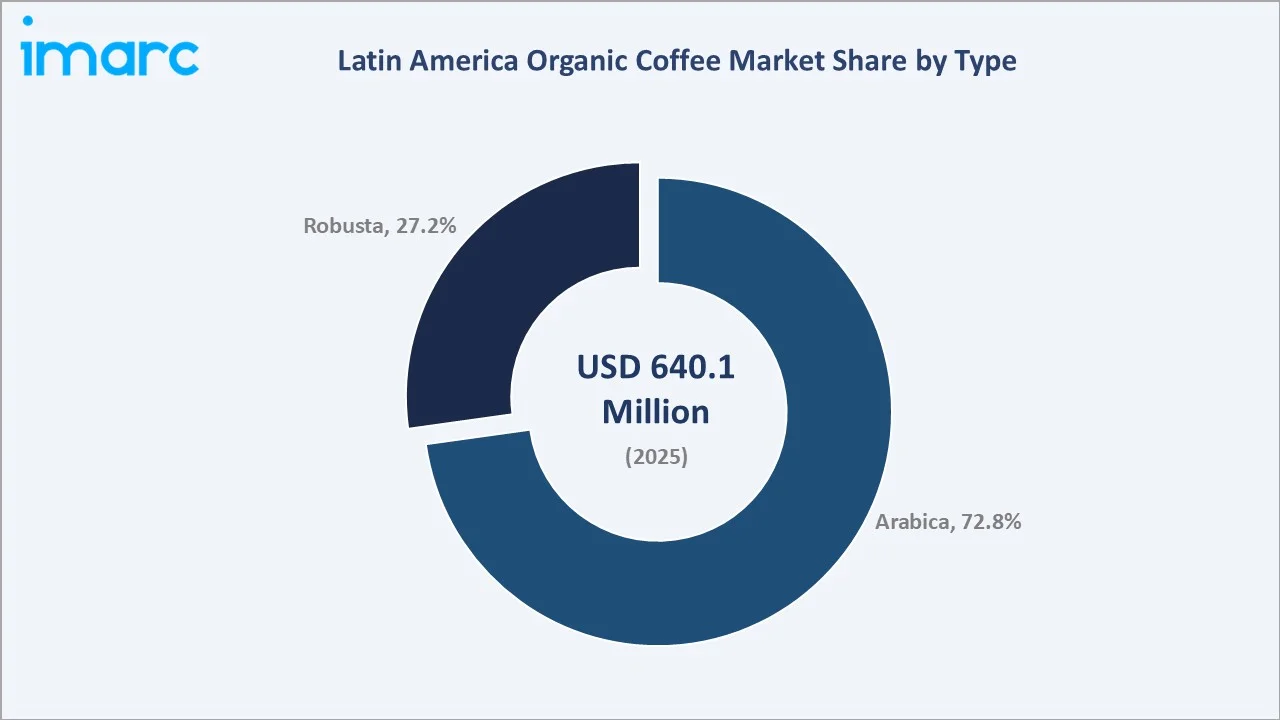

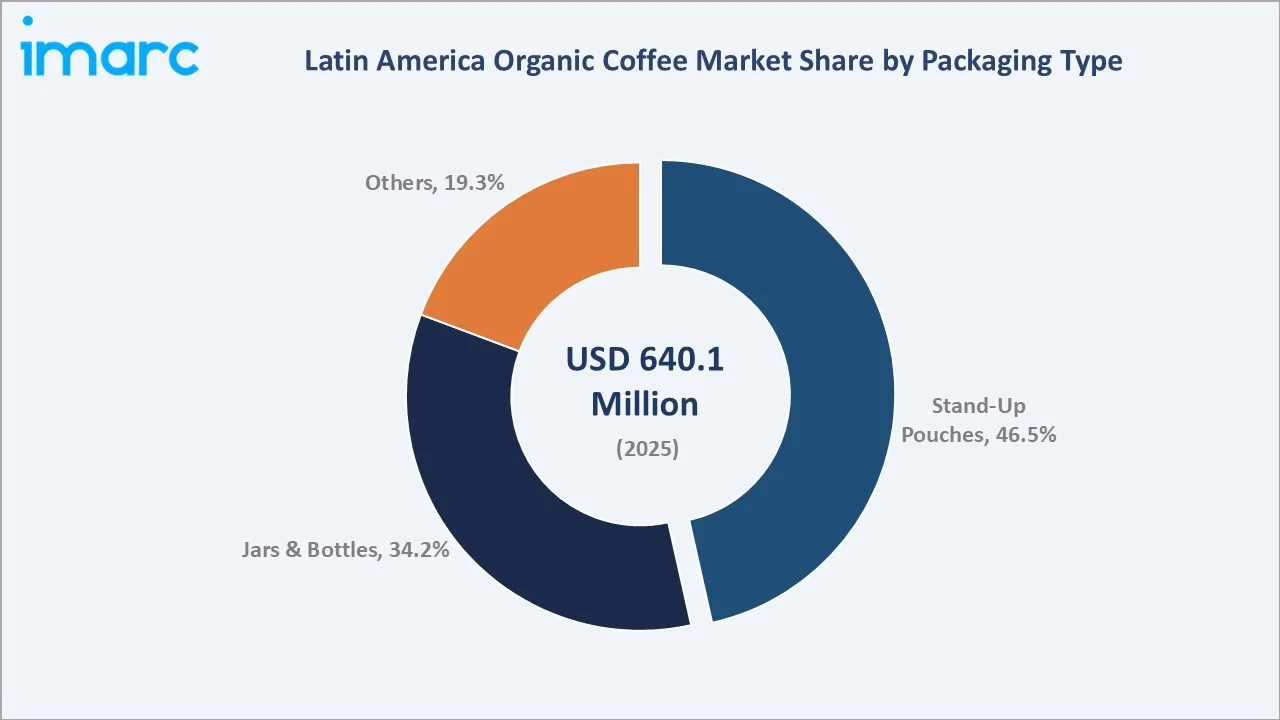

The Latin America organic coffee market reached USD 640.1 Million in 2025 and is projected to reach USD 1,214.1 Million by 2034, growing at a CAGR of 7.15% during 2026-2034. The market is driven by rising consumer preference for chemical-free, sustainable, and ethically sourced coffee. Growing exports, premiumization, and increasing demand for certified organic products are further supporting market growth. Latin America accounts for nearly 75% of global organic coffee production, with Mexico, Peru, and Costa Rica among the key producing countries. This is driving the Latin America organic coffee market by strengthening the region’s position as a major global supplier of certified organic coffee, attracting export demand, premium pricing, and investment in sustainable farming practices. Arabica leads the type at 72.8%. Stand-up pouches dominate packaging at 46.5%. Brazil leads regionally at 41.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 640.1 Million |

|

Forecast Market Size (2034) |

USD 1,214.1 Million |

|

CAGR (2026-2034) |

7.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Arabica (72.8%, 2025) |

|

Dominant Packaging Type |

Stand-Up Pouches (46.5%, 2025) |

|

Leading Country |

Brazil (41.9%, 2025) |

The Latin America organic coffee market expanded from USD 453.2 Million in 2020 to USD 640.1 Million in 2025, anchored at USD 904.1 Million in 2030, and forecast to reach USD 1,214.1 Million by 2034. Latin America is the most commercially significant organic coffee-producing and exporting geography. Organic coffee's commercial differentiation from conventional coffee is the most commercially well-documented single premium category in the coffee market.

To get more information on this market, Request Sample

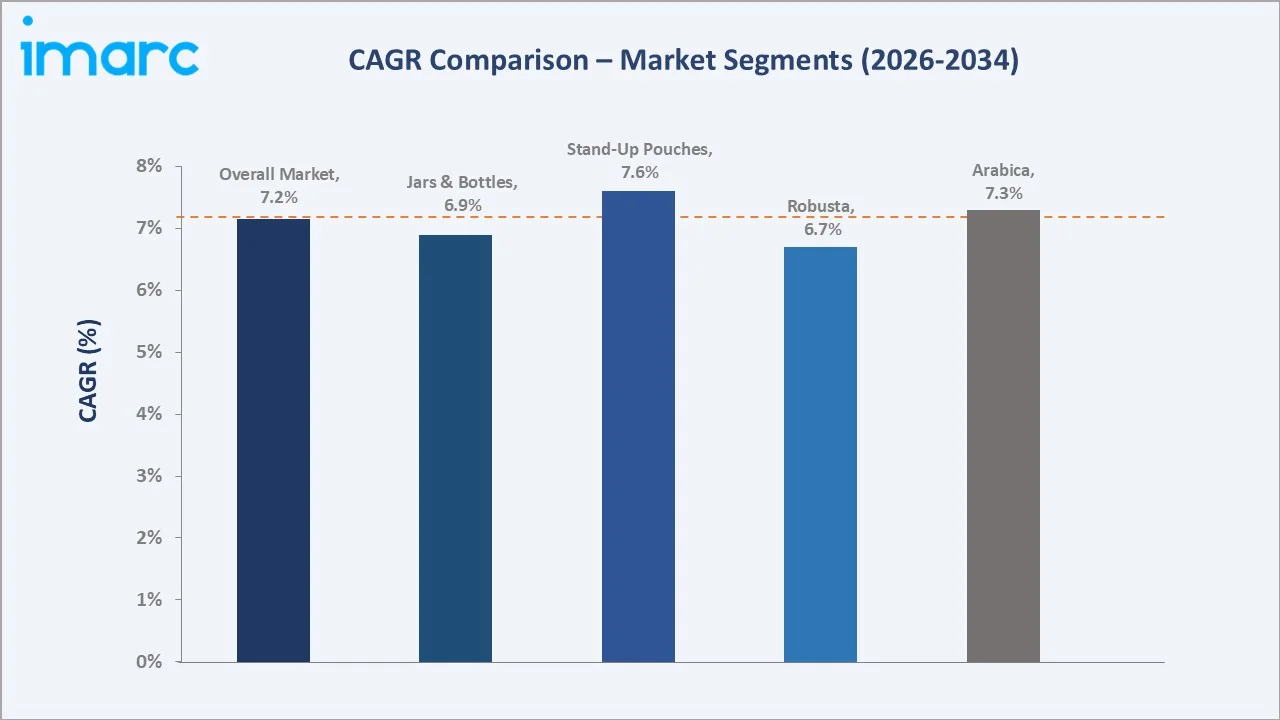

Stand-up pouches grow fastest at ~7.6% CAGR through e-commerce D2C specialty roaster adoption, creating the most commercially dynamic above-glass-jar packaging shift in Latin American organic coffee retail. Arabica grows at ~7.3% CAGR through specialty single-origin premium export expansion, creating above-Robusta price per kilogram growth trajectory through specialty café and home brewing premium market adoption.

Executive Summary

The Latin America organic coffee market at USD 640.1 Million in 2025 represents a market at the intersection of three commercially convergent megatrends, the global health and wellness consumer shift creating above-conventional organic food and beverage premium adoption, the specialty coffee third-wave culture creating above-commodity single-origin traceability demand that organically certified coffee supply chains naturally provide, and the export premium market paying above-conventional price for certified organic lots creating the most commercially compelling Latin American farmer conversion incentive in the organic food market. The market is projected to reach USD 1,214.1 Million by 2034.

Arabica at 72.8% leads through the variety's altitude-grown heritage, creating Latin America's most commercially premium single coffee type. Stand-up pouches at 46.5% lead through resealable functionality and e-commerce shipping efficiency. Brazil leads at 41.9% through volume production and a growing domestic premium market.

Key Market Insights

|

Insight |

Data |

| Dominant Type |

Arabica - 72.8% share (2025) |

|

Dominant Packaging Type |

Stand-Up Pouches - 46.5% market share (2025) |

| Leading Country |

Brazil - 41.9% share (2025) |

|

Market Opportunity |

Single-origin traceable organic coffee for specialty export; regenerative agriculture premium label; nootropic and functional organic coffee blends; e-commerce D2C subscription organic roast; carbon-neutral certified organic estate coffee |

Key Analytical Observations Supporting the Above Data:

- Arabica at 72.8%: The Arabica dominates due to the region’s favorable high-altitude growing conditions and strong reputation for premium-quality Arabica beans. Rising global demand for smooth, specialty, and certified organic coffee further supports its leading share.

- Stand-Up Pouches at 46.5%: The stand-up pouches dominate due to their lightweight, resealable, and shelf-friendly packaging format. They help preserve coffee freshness, reduce transportation costs, and appeal to consumers seeking convenient and premium-looking organic coffee packaging.

- Brazil at 41.9%: Brazil dominates regionally due to its large coffee production base, favorable growing conditions, and strong export network. Rising adoption of sustainable farming and growing demand for premium organic Arabica coffee further support its leading position.

Latin America Organic Coffee Market Overview

The Latin America organic coffee market operates within the broader organic beverage market as the most commercially culturally authentic single organic beverage category above all other organic beverage types through coffee's heritage in Latin American indigenous and colonial agricultural history. The market's commercial uniqueness is the origin-producing region's simultaneous role as a domestic consumer.

The Latin American organic coffee ecosystem integrates organic farmer and cooperative certification, wet and dry milling processing, green bean export trading, roasting and brand development, and retail distribution. Macroeconomic factors include rising disposable incomes, growing premium coffee consumption, and increasing export demand for certified organic products.

Market Dynamics

To evaluate market opportunities, Request Sample

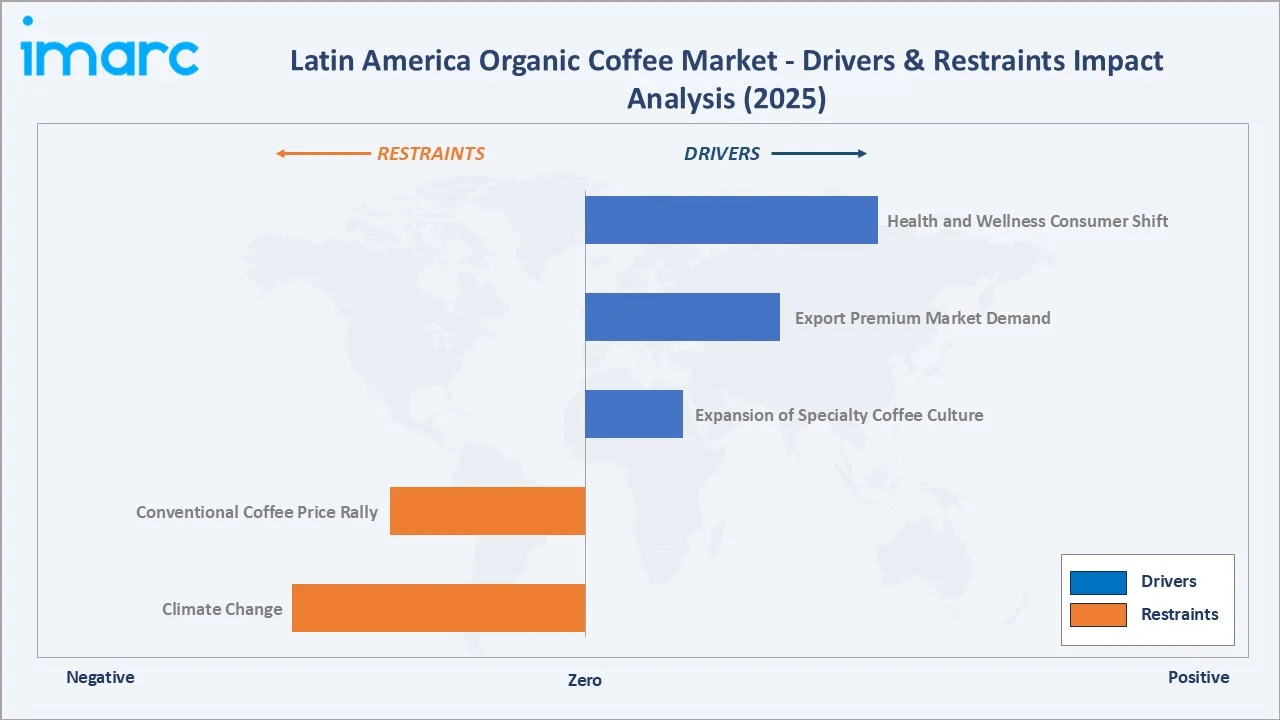

Market Drivers

- Health and Wellness Consumer Shift: Health and wellness consumer shift is driving the market as buyers increasingly prefer chemical-free, natural, and sustainably produced beverages. Organic coffee appeals to health-conscious consumers seeking products grown without synthetic pesticides or fertilizers. This trend is also supporting premium coffee consumption and stronger demand for certified organic labels. Rising awareness of clean-label and ethical sourcing is further boosting market growth.

- Export Premium Market Demand: In 2023, nearly 80% of U.S. unroasted coffee imports were sourced from Latin America, valued at around US$4.8 billion, mainly from Brazil (35%) and Colombia (27%). Traditionally, over 92% of U.S. coffee imports have been higher-quality Arabica beans, which are less acidic and command a premium over Robusta. This supports export premium demand by strengthening Latin America’s role as a key supplier of high-value Arabica coffee to major international markets. Rising demand for premium, traceable, and organic coffee encourages regional producers to expand certified organic cultivation and capture better export prices.

- Expansion of Specialty Coffee Culture: Expansion of specialty coffee culture is driving the market as consumers increasingly seek premium, single-origin, traceable, and high-quality coffee experiences. Organic coffee fits well with specialty trends because it emphasizes sustainable farming, ethical sourcing, and superior bean quality. This encourages cafés, roasters, and retailers to offer certified organic blends. Rising demand for artisanal and premium coffee is further strengthening market growth.

Market Restraints

- Climate Change: Climate change is increasing the frequency of droughts, irregular rainfall, rising temperatures, and extreme weather events. These conditions can reduce coffee yields, affect bean quality, and increase the risk of pests and diseases. Organic farmers have fewer chemical intervention options, making crop management more challenging. As a result, production becomes less predictable, leading to supply fluctuations and higher costs.

- Conventional Coffee Price Rally: The conventional coffee price rally is narrowing the perceived price advantage of organic coffee. When conventional coffee prices rise sharply, buyers may become less willing to pay additional premiums for organic certification. This can reduce the attractiveness of organic coffee for cost-sensitive importers, roasters, and consumers. As a result, organic producers may face pressure on margins and slower premium product adoption.

Market Opportunities

- Regenerative Organic Agriculture: Regenerative organic agriculture promotes soil health, biodiversity, carbon sequestration, and long-term farm productivity. These practices align with growing consumer and buyer demand for environmentally sustainable and climate-resilient coffee production. They also help producers differentiate their products through premium certifications and sustainability credentials. In December 2025, Suntory Holdings and Conservation International launched a regenerative agriculture pilot program in Huila, Colombia, a key global coffee-growing region. The initiative aims to support sustainable coffee bean sourcing while lowering GHG emissions by improving coffee residue and fertilizer management practices. As global brands increasingly prioritize regenerative sourcing, Latin American coffee growers can access higher-value export markets and strengthen their competitive position.

- D2C E-Commerce Coffee Subscription: D2C e-commerce coffee subscriptions enable producers and brands to sell directly to consumers without relying heavily on traditional retail channels. Subscription models provide recurring revenue, strengthen customer loyalty, and allow brands to showcase premium organic and specialty coffee offerings. They also help producers capture higher margins and gain valuable consumer insights. Growing online shopping adoption is further supporting the expansion of this channel.

Market Challenges

- Limited Farmer Awareness and Technical Training: Limited farmer awareness and technical training challenge the Latin America organic coffee market by slowing the adoption of organic farming practices, certification standards, and soil management techniques. Many smallholders may lack knowledge of composting, pest control, traceability, and regenerative methods. This can reduce yield quality, limit certification readiness, and create an inconsistent supply. As a result, producers may struggle to access premium organic export markets.

- Pest and Disease Pressure under Organic Farming Systems: Pest and disease pressure under organic farming systems is a significant challenge because growers have limited access to synthetic pesticides and chemical treatments. Coffee crops remain vulnerable to threats such as coffee leaf rust, berry borers, and fungal infections, which can reduce yields and bean quality. Managing these risks often requires more labor-intensive and costly biological or cultural control methods. This can increase production costs and create supply uncertainties for organic coffee producers.

Emerging Market Trends

1. Specialty Organic Cold Brew and Ready-to-Drink Expansion

Specialty organic cold brew and ready-to-drink (RTD) coffee expansion is emerging as consumers increasingly seek convenient, premium, and health-focused beverage options. Organic cold brew and RTD products combine the appeal of clean-label ingredients with on-the-go consumption. These products are attracting younger consumers and urban professionals looking for specialty coffee experiences. The trend is encouraging coffee brands to diversify product portfolios and capture higher-value market segments.

2. Robusta Organic Premiumization Through Process Innovation

Robusta organic premiumization through process innovation is emerging as producers adopt advanced fermentation, post-harvest processing, and quality enhancement techniques to improve flavor profiles. These innovations help reduce the quality gap between Robusta and premium Arabica varieties, enabling organic Robusta beans to command higher prices. The trend is expanding specialty coffee applications and creating new revenue opportunities for growers. It also supports product diversification and strengthens the value proposition of organic Robusta coffee in global markets.

3. Organic Coffee Capsules Fueling Specialty Coffee Market Growth

Organic coffee capsules are emerging as consumers seek convenient, single-serve options without compromising on quality or sustainability. In March 2024, Nespresso Professional announced the availability of a new Brazil Organic capsule, as a pure Arabica blend created to expand its Origins Organic range. The Brazil capsule joins Peru, Congo, and Colombia variants, with all coffees sourced from selected regions and produced using locally supported cultivation, harvesting, and processing practices. These capsules support at-home specialty coffee consumption and appeal to urban consumers looking for premium organic products. Compostable and recyclable capsule formats further strengthen their eco-friendly positioning. This trend is helping brands expand into higher-value retail and e-commerce channels.

4. Climate Adaptation and Shade-Grown Certification Convergence

Climate adaptation and shade-grown certification convergence is emerging as producers seek more resilient organic coffee farming systems. Shade-grown practices help protect coffee plants from heat stress, conserve soil moisture, and support biodiversity. When combined with organic and climate-focused certifications, they improve product traceability and premium positioning. This trend helps Latin American growers meet sustainability expectations while reducing climate-related production risks.

Industry Value Chain Analysis

The Latin America organic coffee value chain integrates organic coffee cultivation, certification & farm compliance, harvesting & primary processing, roasting & product development, packaging & value addition, and foodservice & end consumers.

|

Stage |

Key Participants |

| Organic Coffee Cultivation |

Organic coffee farmers, cooperatives, agricultural associations, estate plantations, and regenerative agriculture practitioners |

|

Certification & Farm Compliance |

Organic certification bodies, sustainability auditors, traceability providers, and agricultural extension agencies |

|

Harvesting & Primary Processing |

Wet mills, dry mills, coffee processors, post-harvest handling service providers, and local cooperatives |

|

Roasting & Product Development |

Coffee roasters, specialty coffee brands, private-label manufacturers, organic beverage producers |

|

Packaging & Value Addition |

Packaging suppliers, organic coffee capsule manufacturers, stand-up pouch producers, labeling and branding companies |

|

Foodservice & End Consumers |

Cafés, restaurants, hotels, offices, specialty coffee chains, and domestic and international consumers |

The roasting & product development stage is the most commercially consequential organic integrity checkpoint because it determines the final flavor profile, quality consistency, and premium positioning of organic coffee products. It is also the stage where maintaining segregation from conventional coffee and preserving organic certification standards are critical to protecting product value and consumer trust.

Technology Landscape in the Latin America Organic Coffee Industry

Blockchain Traceability and Digital Certification

Blockchain traceability and digital certification are improving transparency across the supply chain, from farm to consumer. These technologies enable stakeholders to verify organic certifications, origin details, farming practices, and sustainability claims in real time. They help reduce fraud, strengthen consumer trust, and support compliance with international certification standards. As demand for traceable and ethically sourced coffee grows, adoption of digital verification platforms is increasing across the region.

Organic Processing Innovation

Organic processing innovation is improving bean quality, consistency, and value addition through advanced fermentation, drying, and post-harvest techniques. Producers are adopting controlled fermentation, water-efficient processing, and precision drying systems to enhance flavor profiles while maintaining organic standards. These innovations help reduce waste, improve traceability, and increase premium market appeal. As specialty and organic coffee demand grows, technology-driven processing is becoming a key competitive differentiator.

Single-Origin Coffee Demand

Single-origin coffee demand is increasing the need for origin authentication, farm-level traceability, and digital certification tools. Producers and brands are using technology to verify region, variety, farming practices, and sustainability claims. In January 2026, Starbucks launched Starbucks Single-Origin Mexico, a limited-edition whole bean coffee available in select Latin America and Caribbean markets. The launch highlights Starbucks’ long-standing commitment to Mexican coffee growers and honors the communities that have shaped Mexico’s coffee heritage for generations. This supports premium positioning by giving consumers clear information about where and how the coffee is grown. As demand for transparent and specialty organic coffee rises, digital traceability and quality profiling systems are becoming more important.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Arabica |

72.8% |

2025 |

|

Packaging Type |

Stand-Up Pouches |

46.5% |

2025 |

|

Sales Channel |

🔒 |

🔒 |

2025 |

|

Country |

Brazil |

41.9% |

2025 |

By Type

Arabica leads at 72.8% (2025). Latin America's arabica organic coffee encompasses the full specialty spectrum from Colombia, Brazil, Peru, and Mexico, creating the most commercially geographically diverse above-single-variety single-region organic coffee product range of any region.

To access detailed market analysis, Request Sample

Robusta at 27.2% encompasses Brazil's organic, Vietnam's and Indonesia's organic Robusta, complementing Latin American supply for espresso blending. Robusta's commercial application in organic instant coffee processing creates above-arabica extraction efficiency demand from Latin American organic instant coffee manufacturers targeting the European and Asian organic instant consumer market above standard soluble conventional coffee.

By Packaging Type

Stand-up pouches lead at 46.5% (2025). Stand-up pouches encompass kraft paper valve zipper pouches, metallized barrier valve pouches, and compostable PLA-lined kraft pouches from 150g to 1kg size, serving specialty D2C, natural retail, and online subscription channels as the most commercially dynamic single packaging growth format in Latin American organic coffee.

Jars and bottles at 34.2% serve premium organic retail gift, specialty café whole bean, and artisan roaster premium display formats through glass's premium visual and sustainability positioning. Others at 19.3% include cans, multi-layer foil stand-up without valve, tin canisters, and capsule format.

Regional Market Insights

| Country |

Share (2025) |

Key Latin America Organic Coffee Market Drivers & Characteristics |

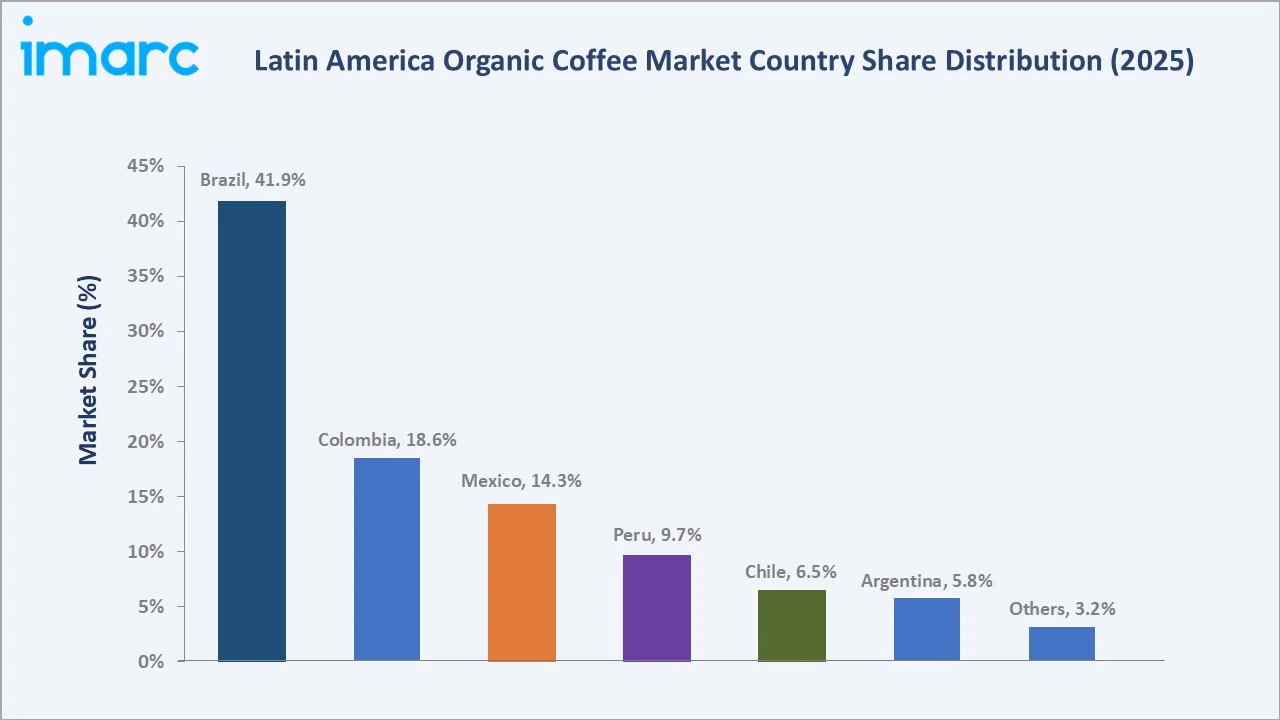

| Brazil | 41.9% | Supported by its extensive coffee cultivation area, strong export infrastructure, growing adoption of sustainable farming practices, and leadership in premium Arabica production. |

| Colombia |

18.6% |

Benefits from its reputation for high-quality Arabica coffee, well-established coffee cooperatives, and increasing demand for specialty and certified organic coffee in international markets. |

| Mexico |

14.3% |

Driven by strong organic farming traditions, significant participation of smallholder growers, and robust export demand. |

|

Peru |

9.7% |

Supported by favorable growing conditions, expanding organic cultivation, and strong participation in fair-trade and specialty coffee segments. |

| Chile |

6.5% |

Driven by growing consumer demand for premium, specialty, and sustainably sourced coffee products. |

| Argentina |

5.8% |

Benefits from increasing specialty coffee consumption, growing demand for premium beverages, and expanding availability of organic products through retail and foodservice channels. |

| Others |

3.2% |

Other Latin American countries contribute through niche organic coffee production, expanding specialty coffee exports, and increasing adoption of sustainable agricultural practices aimed at premium international markets. |

Brazil's 41.9% dominance reflects the largest coffee producer's organic market leadership through volume production and growing domestic premium consumption. Colombia's 18.6% reflects brand infrastructure creating Latin America's most commercially institutionally supported single-origin organic marketing platform. Mexico's 14.3% reflects the indigenous cooperative organic production's heritage, creating the most commercially documented sustainable smallholder organic coffee supply chain.

Peru's 9.7% reflects Latin America's highest certified organic coffee share of total production, creating Peru's most commercially specialized above-conventional organic production orientation. Chile's 6.5% reflects domestic premium consumption above production capability, creating the most commercially import-dependent national organic coffee market in Latin America. Argentina's 5.8% reflects sophisticated café culture, creating the most commercially active domestic organic coffee consumption market.

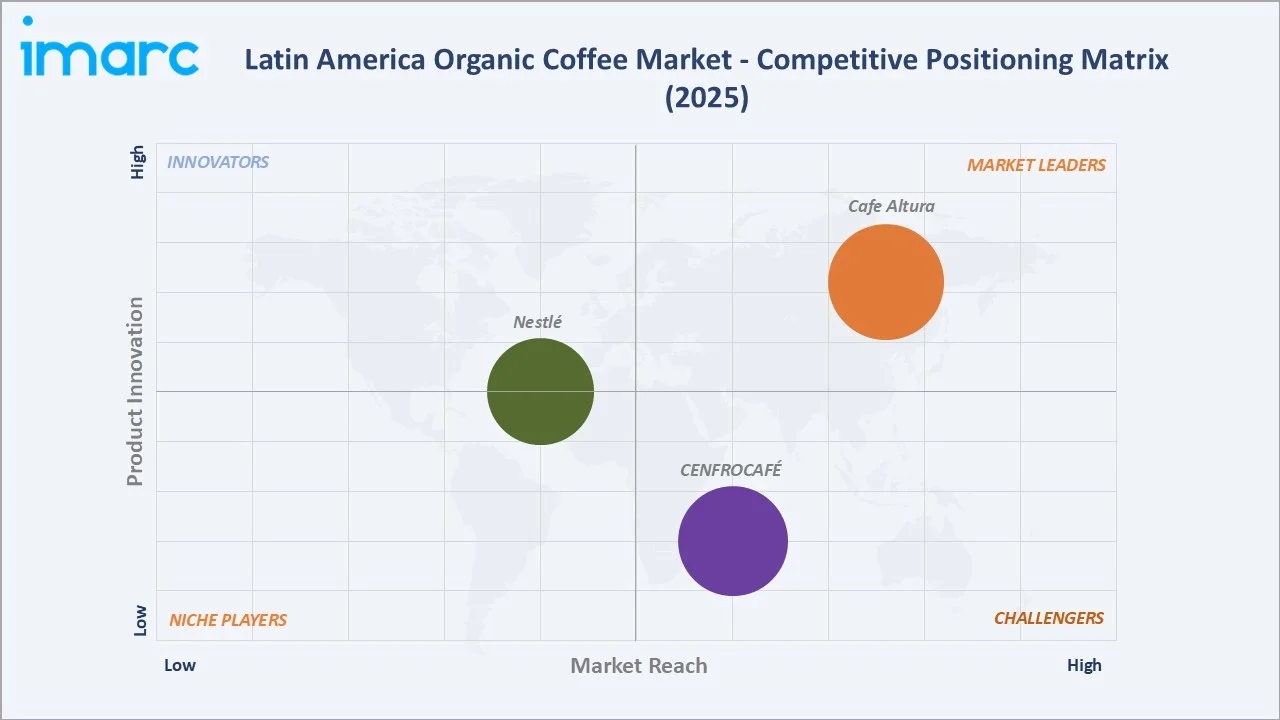

Competitive Landscape

The Latin America organic coffee competitive landscape is commercially distributed across four distinct business model archetypes: green coffee trading specialist, origin-country exporter-cooperative, branded roaster, and farm-level estate brand.

|

Company |

Key Brands |

Market Position |

Core Strength |

| Cafe Altura | Cafe Altura |

Market Leader |

Cafe Altura played a pioneering role in Latin American organic coffee by becoming the first organic coffee supplier. |

| CENFROCAFÉ |

CENFROCAFÉ |

Strong Challenger | CENFROCAFÉ is a leading Peruvian cooperative that plays a critical role in producing high-quality organic coffee. |

| Nestlé | Nespresso | Established Player | Nestlé is actively transforming its Latin American organic coffee market through its brand Nespresso. |

The competitive landscape is evolving through three forces: direct trade relationship deepening, regenerative organic premium creation, and D2C brand model disrupting traditional wholesale.

Key Company Profiles

Cafe Altura

Cafe Altura is a pioneer in the organic coffee industry. By fostering early partnerships, they set ethical standards for organic farming and Fairtrade practices in countries like Mexico, ensuring sustainable livelihoods and ecological protection for local farmers.

- Key Brands: Cafe Altura

- Strategic Focus: Strengthening its position in the organic and specialty coffee segment through the sourcing of certified organic, biodynamic, and sustainably grown coffee from Latin American producers.

CENFROCAFÉ

CENFROCAFÉ is one of Peru’s leading coffee cooperatives and a prominent participant in the Latin America organic coffee market. It specializes in the production, processing, and export of certified organic coffee.

- Key Brands: CENFROCAFÉ

- Strategic Focus: Expanding the production and export of certified organic, Fair Trade, and specialty Arabica coffee while improving the livelihoods of smallholder farmers.

Market Concentration Analysis

The Latin America organic coffee competitive landscape is highly fragmented at the production and cooperative level and moderately concentrated at the international green coffee trading tier. The most commercially concentrated single competitive segment is Mexico's Chiapas organic export. While large cooperatives and export-oriented organizations hold significant shares in key producing countries such as Brazil, Peru, Colombia, and Mexico, no single player dominates the regional market, resulting in moderate market concentration.

Investment & Growth Opportunities

Highest Growth Segments

Regenerative organic certified coffee (~15-20% CAGR from near-zero base through 2034), organic cold brew RTD in Latin America domestic market (~14-18% CAGR), single-origin estate organic for D2C subscription (~10-12% CAGR), functional nootropic organic coffee blend (~18-22% CAGR), organic capsule for Nespresso-compatible premium single-serve (~9-11% CAGR), and organic instant soluble coffee for Asian export market (~8-10% CAGR) represent the highest-growth Latin American organic coffee investment vectors through 2034.

Investment Themes

- Regenerative Organic Certification investment: Investment in ROC certification technical support, soil carbon measurement protocol implementation, creates the most commercially premium above-standard-organic coffee product tier.

- D2C subscription organic roaster brand development: Building a Shopify-powered D2C organic coffee roaster brand, creating above-retail 45-55% margin versus natural food retail's 15-25% margin through direct consumer subscription relationship.

Future Market Outlook (2026-2034)

The Latin America organic coffee market is projected to grow from USD 640.1 Million in 2025 to USD 1,214.1 Million by 2034, delivering a 7.15% CAGR over the forecast period. The market's anchor value of USD 904.1 Million in 2030 represents Latin American organic coffee at structural commercial maturity. Domestic Latin American premium consumption is overtaking pure export-driven demand structure as the primary growth driver, regenerative organic premium creating above-standard-organic product tier above certification-only differentiation, and D2C e-commerce roaster democratizing organic premium access above specialty café and natural food retail gate-keeping.

Three structural forces define Latin American organic coffee's growth through 2034: health and wellness permanence creates sustainable above-conventional organic demand above cyclical wellness trend reversal risk, certification area expansion creates supply availability above premium scarcity constraint, and domestic Latin American premium consumption creates the most commercially novel growth vector.

Research Methodology

Primary Research

Primary research comprised structured interviews with Latin America organic coffee industry stakeholders, including export directors, origin buyers, Q-graders, organic certification auditors, and a consumer survey from organic coffee buyers across Brazil, Colombia, Mexico, Chile, and Peru.

Secondary Research

Secondary research encompassed organic coffee statistics, certified organic handler database, organic producer database, Peru annual organic production report, Brazil organic certification agricultural registry, company annual reports, specialty coffee price report, organic differential analysis, and Latin America agribusiness competitiveness report. Over 40 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using an organic certified production volume model: Latin American organic certified coffee production by country multiplied by blended farmgate-to-retail value chain multiplier plus domestic retail value added.

Latin America Organic Coffee Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Arabic, Robusta |

| Packaging Types Covered | Stand-Up Pouches, Jars and Bottles, Others |

| Sales Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Others |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | Cafe Altura, CENFROCAFÉ, Nestlé, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America organic coffee market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America organic coffee market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America organic coffee industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Organic Coffee Market Report

The Latin America organic coffee market reached USD 640.1 Million in 2025, driven by rising demand for chemical-free, sustainable, and ethically sourced coffee. Strong export demand, specialty coffee culture, premium Arabica production, and growing organic certification adoption are further supporting market growth.

The Latin America organic coffee market grows at 7.15% CAGR during 2026-2034, reaching USD 1,214.1 Million by 2034. The overall growth is sustained by health and wellness consumer shift, export premium market demand, specialty coffee culture expansion, and growing certified organic farm area in Brazil, Colombia, Peru, and Mexico.

Arabica leads at 72.8% through Latin America's altitude geography, creating the most commercially premium single coffee variety above lowland Robusta. The organic Arabica premium above conventional Arabica creates the most commercially compelling single certification return for the Latin American highland farmer whose altitude-grown Arabica naturally aligns with specialty organic importer's combined altitude-terroir-certification procurement criteria.

Stand-up pouches lead at 46.5% through resealable zipper functionality, nitrogen-flush freshness preservation, and e-commerce shipping efficiency, creating the most commercially functional above-glass packaging for the home specialty coffee enthusiast who opens and reseals daily.

Brazil leads at 41.9% through the largest coffee production volume, creating Latin America's most commercially significant above-all-other-origin single-country organic coffee supply, combined with Brazil's growing domestic premium organic consumption through natural food retail and specialty café.

Leading companies include Cafe Altura, CENFROCAFÉ, and Nestlé, among others.

The Latin America organic coffee market is projected to reach approximately USD 904.1 Million by 2030, with regenerative organic certification reaching commercial scale above pilot stage, creating the most commercially premium above-standard-organic product tier.

Three priority investment opportunities: regenerative organic certification program development for Colombia and Peru cooperative farms, creating a premium product, D2C subscription organic roaster brand in São Paulo and Bogotá domestic market, creating above-wholesale 45-55% margin, and functional nootropic organic coffee blend development, creating above-plain-organic premium product.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)