LiDAR Market Size, Share, Trends and Forecast by Installation Type, Component, Application, and Region, 2026-2034

Global LiDAR Market Size, Share, Trends & Forecast (2026-2034)

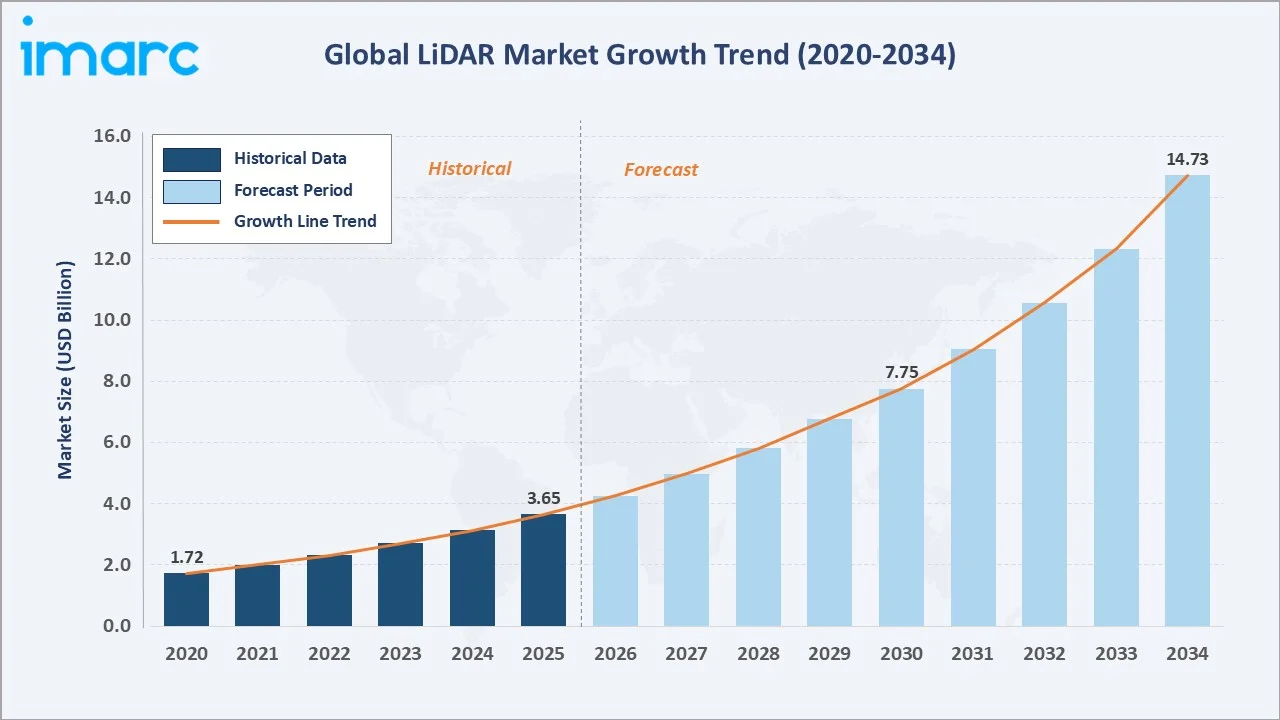

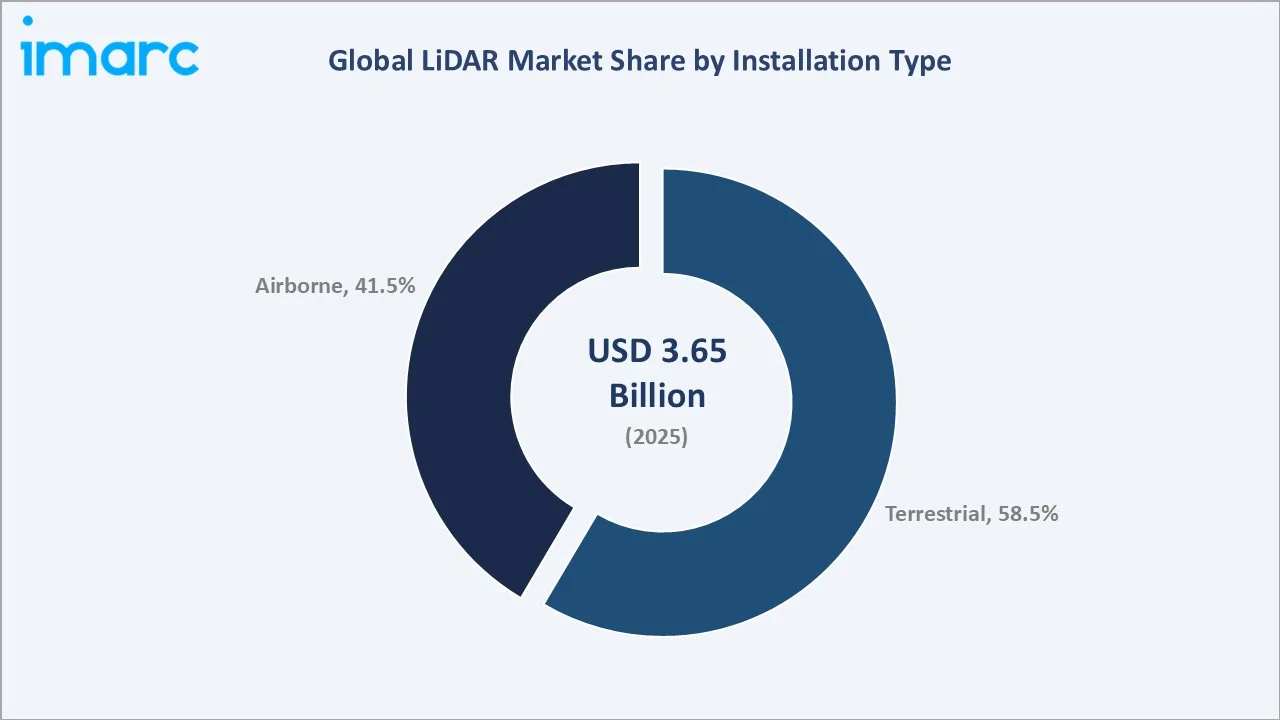

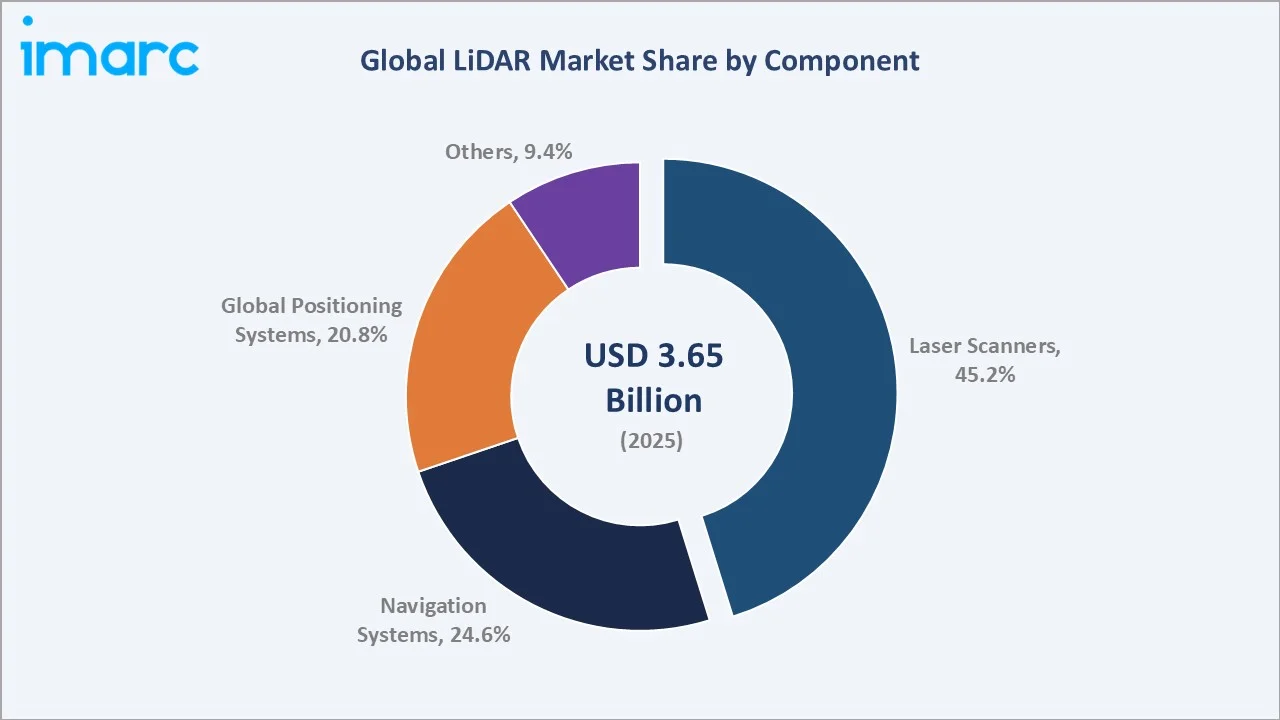

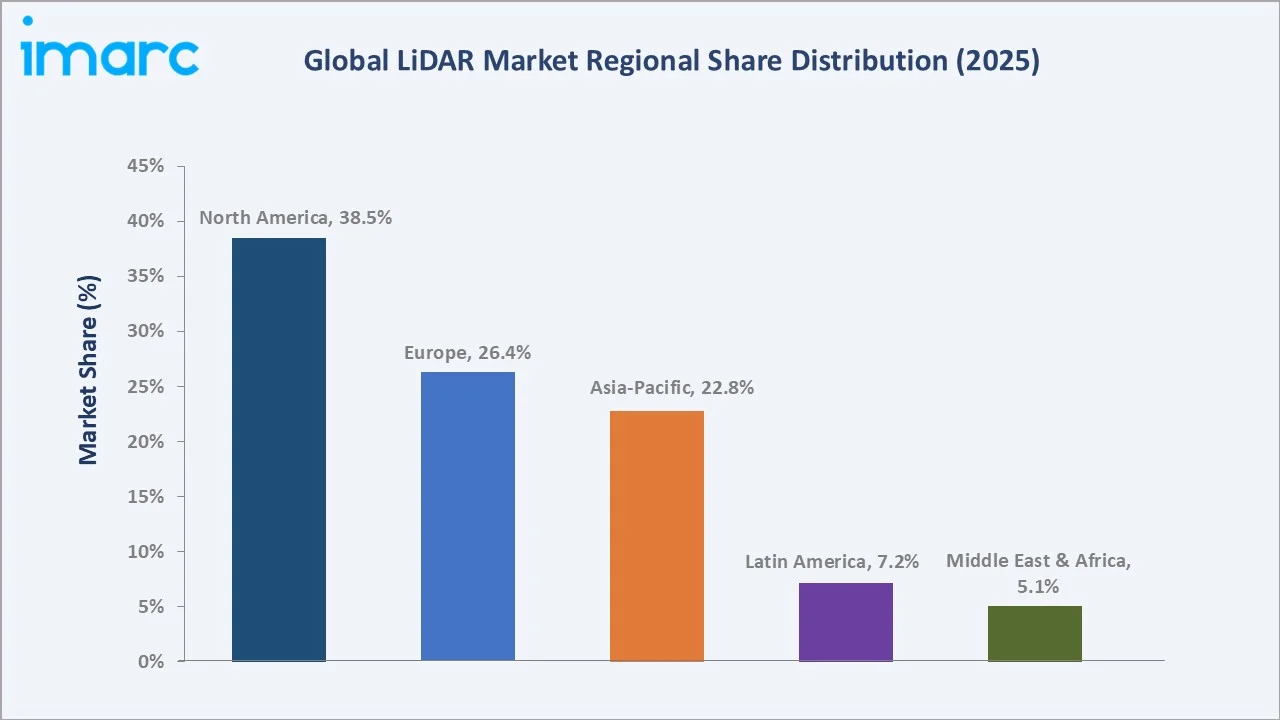

The global LiDAR market size was valued at USD 3.65 Billion in 2025 and is projected to reach USD 14.73 Billion by 2034, exhibiting a CAGR of 16.27% during the forecast period 2026-2034. Rapid acceleration in autonomous vehicle development, smart city infrastructure programs, precision agriculture, and defense reconnaissance is driving broad-based demand. Terrestrial LiDAR dominates installation with a 58.5% share in 2025. Laser Scanners lead component revenues at 45.2%. North America retains global leadership with a 38.5% revenue share, underpinned by major autonomous mobility and geospatial survey investments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.65 Billion |

|

Forecast Market Size (2034) |

USD 14.73 Billion |

|

CAGR (2026-2034) |

16.27% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.5%) |

|

Fastest Growing Region |

Asia-Pacific |

The chart below illustrates the global LiDAR market growth trajectory from 2020 through 2034, contrasting a strong historical expansion phase against a sustained high-CAGR forecast curve powered by autonomous vehicle commercialization, geospatial digitization mandates, and expanding defense LiDAR deployments.

To get more information on this market, Request Sample

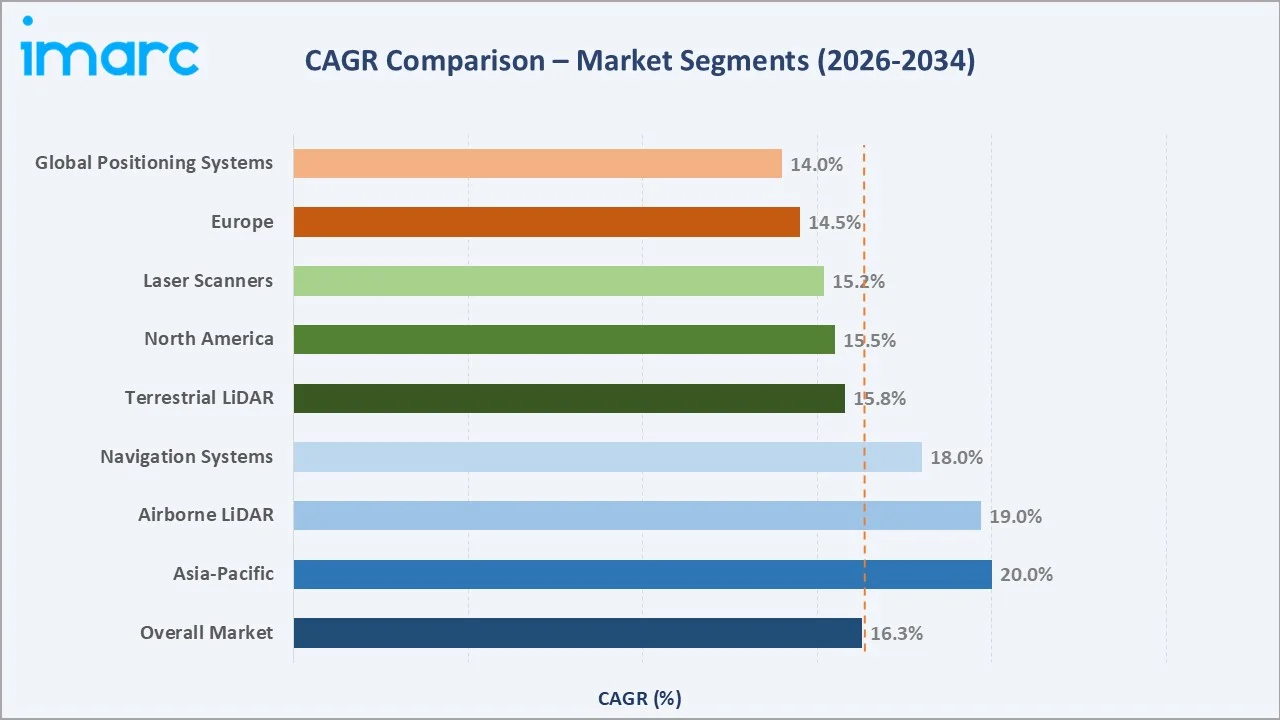

The chart below presents a CAGR comparison across key LiDAR market segments and regions, highlighting Navigation Systems and Asia-Pacific as the fastest-growing areas, both tracking above the overall market CAGR of 16.27% over the forecast period 2026–2034.

Executive Summary

The global LiDAR market is experiencing one of the most sustained high-growth phases in the broader remote sensing industry. Valued at USD 3.65 Billion in 2025, the market is forecast to reach USD 14.73 Billion by 2034, driven by the convergence of autonomous mobility, precision geospatial intelligence, and AI-powered 3D perception platforms. The 16.27% CAGR over 2026–2034 reflects structural demand across automotive, industrial robotics, urban planning, and defense verticals.

Terrestrial LiDAR commands a 58.5% installation share in 2025, anchored by ground-level autonomous vehicle navigation programs, mobile mapping, and infrastructure inspection. Among components, Laser Scanners represent 45.2% of revenues, reflecting their indispensability as the highest-value subsystem in LiDAR hardware architecture. Navigation Systems, the fastest-growing component at an estimated 18% CAGR, are being tightly coupled with LiDAR in inertial-GNSS fusion stacks for all professional autonomous navigation deployments.

North America leads globally with a 38.5% revenue share in 2025, driven by US autonomous vehicle R&D, the USGS 3DEP national terrain mapping initiative, and defense UAV reconnaissance programs. Asia-Pacific is the fastest-growing region, with China’s NEV LiDAR mandates and Japan’s robotics ecosystem accelerating regional adoption. Europe, at 26.4%, benefits from Euro NCAP ADAS mandates and a mature aerial survey market.

Key Market Insights

|

Insight |

Data |

|

Largest Installation Type |

Terrestrial – 58.5% share (2025) |

|

Largest Component |

Laser Scanners – 45.2% share (2025) |

|

Fastest Growing Component |

Navigation Systems (~18% CAGR, 2026-2034) |

|

Leading Region |

North America – 38.5% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific (~20% CAGR, 2026-2034) |

|

Top Applications |

Autonomous Vehicles, Geospatial Survey, Smart Cities, Defense |

|

Market Opportunity |

Solid-state LiDAR sub-USD 500 enabling mass-market AV integration by 2028 |

Key Analytical Observations Supporting The Above Data:

- Terrestrial LiDAR’s 58.5% dominance in 2025 reflects the industry-wide acceleration of ground-based autonomous vehicle and robotics deployments requiring real-time, sub-centimeter-accuracy 3D environmental mapping.

- Laser Scanners account for 45.2% of component revenues in 2025, driven by demand for high-resolution, long-range point cloud sensor assemblies in both mobile and static scanning platforms.

- Navigation Systems at 24.6% represent the fastest-growing component segment, with IMU-GNSS-LiDAR tight coupling becoming standard across all professional autonomous navigation and UAV survey platforms.

- North America’s 38.5% global share in 2025 reflects substantial federal and private investment in autonomous transportation infrastructure, with the US DOD allocating over USD 2.1 Billion toward autonomous sensor fusion programs in FY2024.

- Asia-Pacific is the fastest-growing region at ~20% CAGR, led by China’s NEV policy requiring advanced LiDAR sensor packages and South Korea’s and Japan’s precision robotics manufacturing ecosystems.

- Over 40 global AV programs are actively deploying solid-state LiDAR in production-bound vehicles by 2025, representing a critical commercialization inflection that is reshaping component economics across the LiDAR supply chain.

Global LiDAR Market Overview

Light Detection and Ranging (LiDAR) is an active remote sensing technology that uses laser pulses to precisely measure distances and generate high-resolution 3D maps of terrain, objects, and environments. It is widely used across autonomous driving (ADAS), geospatial surveying, smart cities, agriculture, mining, defense, forestry, and building modeling.

The LiDAR ecosystem includes component suppliers, hardware manufacturers, software platforms, system integrators, and diverse end users. Growth is driven by urbanization, vehicle electrification, and defense modernization, with adoption scaling rapidly—over 85 countries had LiDAR-enabled drone survey programs by 2024.

Market Dynamics

To evaluate market opportunities, Request Sample

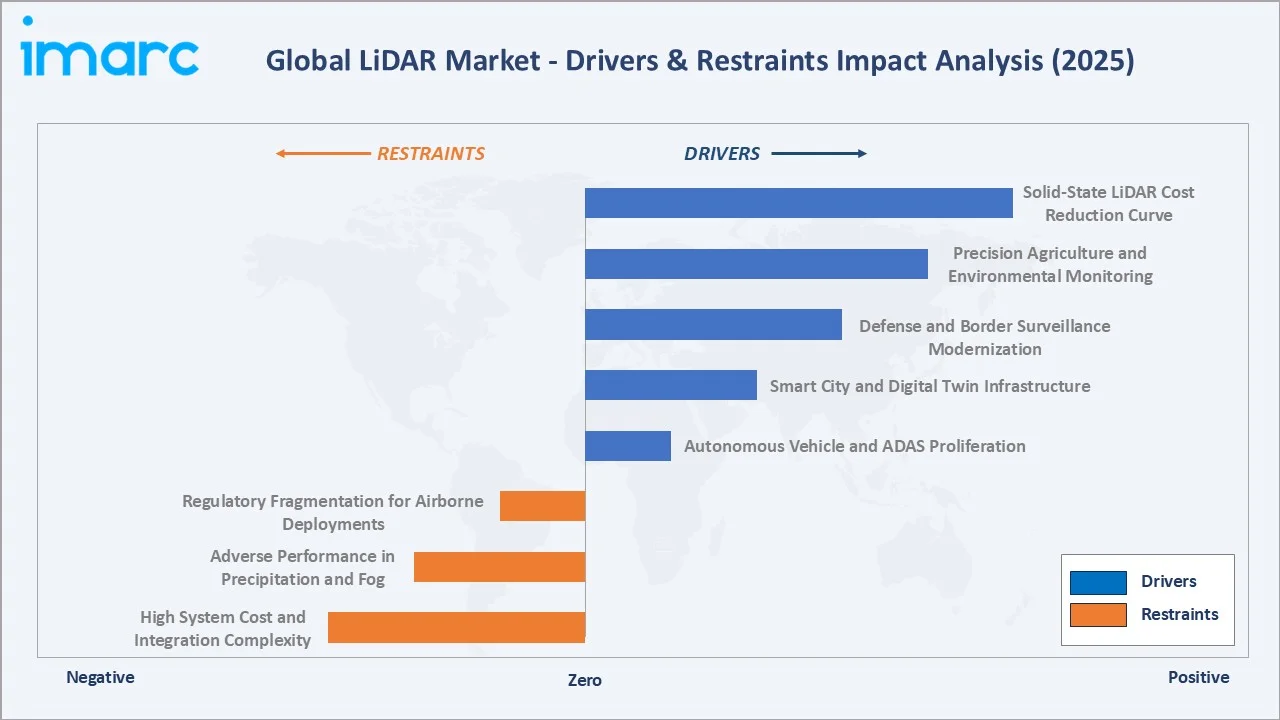

Market Drivers

- Autonomous Vehicle and ADAS Proliferation: The global AV sector is the largest single demand driver for LiDAR. Over 40 active AV programs are deploying LiDAR globally in 2025. Waymo’s commercial robotaxi fleet logs over 1 million autonomous miles per month, each vehicle equipped with multiple LiDAR units generating 2+ million data points per second. Euro NCAP 2025 safety protocols effectively mandate ADAS sensor suites, including LiDAR, across premium vehicle categories.

- Smart City and Digital Twin Infrastructure: Municipal governments globally are accelerating digital twin deployments, requiring high-density 3D data capture. Over 500 cities had active LiDAR-based urban mapping programs by 2024. Saudi Arabia’s NEOM project and UAE smart city initiatives represent flagship government commitments to LiDAR-enabled spatial intelligence at the urban scale.

- Defense and Border Surveillance Modernization: Defense agencies in North America, Europe, and Asia-Pacific are integrating airborne LiDAR into UAV and satellite reconnaissance platforms.

- Precision Agriculture and Environmental Monitoring: Agricultural LiDAR adoption is accelerating, with precision crop canopy analysis, yield mapping, and terrain modeling growing at over 20% annually in 2024. Forestry LiDAR for carbon credit verification programs is expanding rapidly as voluntary carbon markets scale globally.

Market Restraints

- High System Cost and Integration Complexity: Mechanical spinning LiDAR units remain expensive at USD 5,000–USD 15,000 per automotive-grade unit in 2024. Integration with camera, radar, and GPS fusion stacks requires significant engineering investment, limiting adoption in cost-sensitive commercial and consumer markets.

- Adverse Performance in Precipitation and Fog: LiDAR systems exhibit degraded point cloud accuracy in heavy rain, snow, or dense fog, as water droplets scatter laser pulses. This operational limitation constrains real-world AV deployment in challenging climate regions and raises reliability questions for safety-critical applications.

- Regulatory Fragmentation for Airborne Deployments: Airborne LiDAR via commercial UAVs faces complex, jurisdiction-varying drone operation regulations that slow commercial survey adoption in regulated airspaces across the EU, Asia, and the LiDAR Market in Latin America, increasing the compliance burden for survey operators.

Market Opportunities

- Solid-State LiDAR Cost Reduction Curve: Solid-state LiDAR using MEMS, OPA, and Flash architectures is on a rapid cost trajectory toward sub-USD 500 per automotive-grade unit by 2028. This will unlock mass-market vehicle integration at volumes of 30+ million vehicles annually, fundamentally expanding the LiDAR addressable market.

- AI-Powered Perception Platform Integration: Fusion of LiDAR with AI-powered object detection and semantic segmentation is creating new value across robotics, autonomous logistics, and industrial automation.

- Emerging Economy Smart Infrastructure Programs: India, Brazil, and Southeast Asian nations are launching urban digitization programs requiring large-scale LiDAR terrain and building surveys.

Market Challenges

- Sensor Miniaturization vs. Range Trade-offs: Solid-state LiDAR miniaturization faces engineering trade-offs between range (150–200m in most solid-state designs vs. 300m+ in mechanical units), field of view, and angular resolution that limit substitutability in long-range highway AV applications requiring high-confidence object detection at distance.

- Competitive Pressure from Camera-Only Sensor Stacks: Tesla’s camera-only Autopilot strategy and the broader camera-radar fusion debate challenge universal LiDAR adoption. Manufacturers must demonstrate clear cost-performance superiority to justify LiDAR inclusion against lower-cost sensor alternatives in the automotive mass market.

Emerging Market Trends

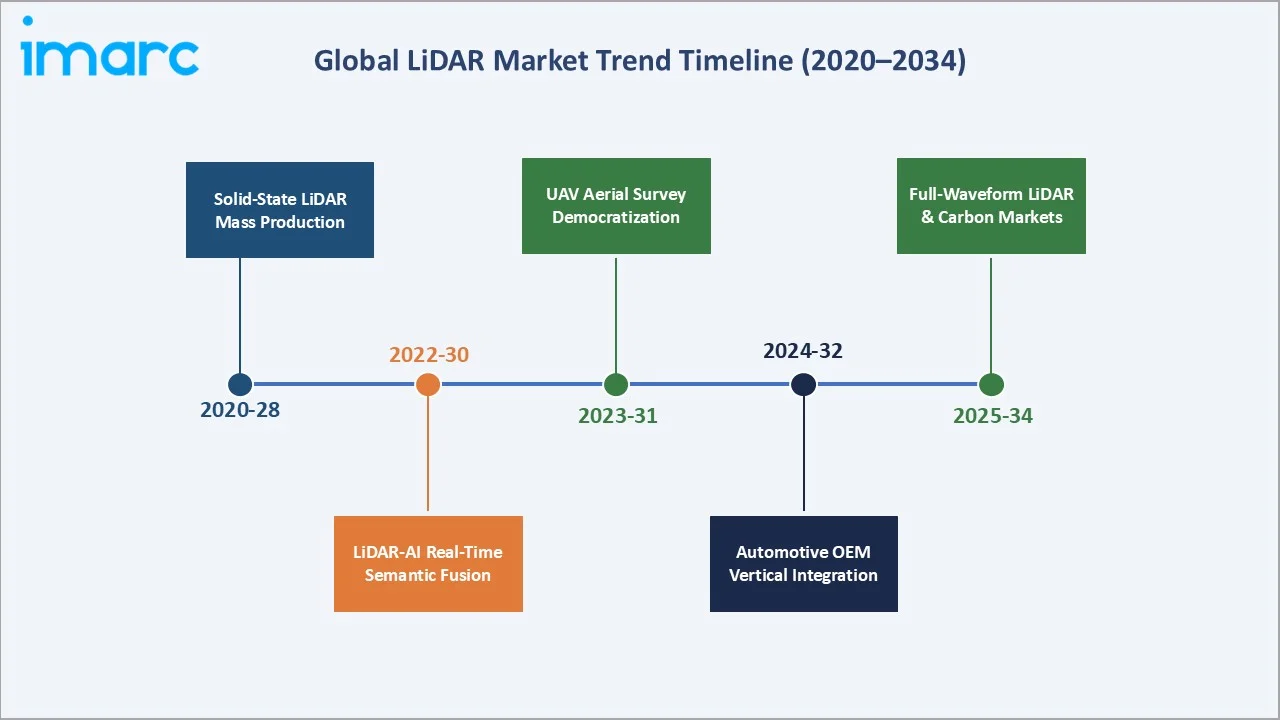

The following five technology and market trends are reshaping the global LiDAR industry’s competitive dynamics and growth trajectory through 2034.

1. Solid-State LiDAR Achieving Automotive-Grade Mass Production

MEMS-based and Flash LiDAR architectures are transitioning from prototype to mass production, eliminating moving parts that historically limited automotive durability. Quantum Computing Inc., Hesai Group, and Innoviz Technologies Ltd are each supplying solid-state LiDAR at scale to OEM production vehicle programs by 2025, marking a critical commercialization inflection. Unit costs are projected to fall below USD 500 for automotive-grade solid-state LiDAR by 2028.

2. LiDAR-AI Fusion Enabling Real-Time Semantic Mapping

Integration of LiDAR point clouds with deep learning-based semantic segmentation enables vehicles and robots to classify objects in real time at over 25 frames per second. This fusion capability is a foundational requirement for Level 4 autonomy, with global investment in AI perception middleware for autonomous systems.

3. UAV-Based Aerial LiDAR Survey Democratization

Sub-USD 50,000 LiDAR-equipped drone systems are democratizing aerial survey access for mid-tier engineering firms and agricultural operators. The commercial UAV LiDAR segment grew approximately 28% in 2024, driven by falling sensor costs and expanding DJI and Trimble ecosystem compatibility with professional survey workflows.

4. Automotive OEM Vertical Integration of LiDAR Supply Chain

Leading OEMs, including Volvo and multiple Chinese NEV manufacturers, are securing long-term LiDAR supply agreements and equity stakes in sensor suppliers. This structural vertical integration mirrors the battery supply chain model, reshaping competitive dynamics and supply security across the LiDAR value chain.

5. Full-Waveform LiDAR for Carbon Markets and Environmental Intelligence

Advanced full-waveform LiDAR systems capturing multiple returns per laser pulse enable unprecedented canopy structure analysis for carbon credit verification programs. The forestry LiDAR segment is projected to grow at over 22% CAGR through 2034 as voluntary carbon markets scale and environmental compliance requirements expand globally.

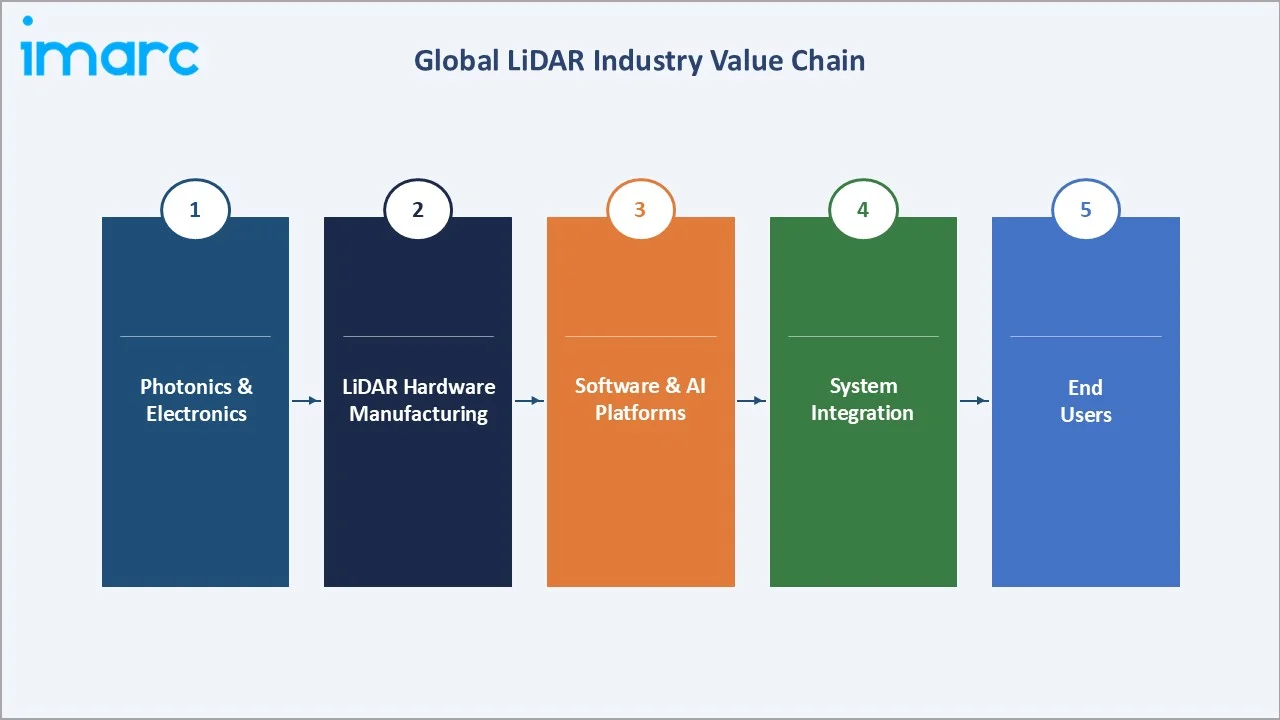

Industry Value Chain Analysis

The global LiDAR industry value chain spans five integrated stages from photonics component supply through end-user deployment. Each stage presents distinct technology barriers, margin profiles, and strategic investment requirements that shape the overall competitive structure of the market.

|

Value Chain Stage |

Key Players / Activities |

|

Photonics & Electronics |

laser diode and photodetector arrays, MEMS chips, SPAD detector ICs |

|

LiDAR Hardware Manufacturing |

full system integration of laser, scanner, optics, receiver |

|

Software & Point Cloud Processing |

3D mapping, semantic segmentation, AI object detection, HD map generation |

|

System Integration |

integration with vehicle ADAS stacks, UAV platforms, and geospatial survey systems |

|

End Users |

Airbus Defence, municipal smart city agencies, precision agriculture operators, and defense agencies |

LiDAR hardware manufacturers occupy the most visible position in the value chain, but software and AI perception platforms are emerging as the decisive competitive moat. As hardware performance converges across suppliers, the ability to process, interpret, and deliver actionable intelligence from LiDAR point cloud data is becoming the primary value driver and margin capture layer in the industry.

Technology Landscape in the LiDAR Industry

Mechanical vs. Solid-State Architecture Evolution

Mechanical spinning LiDAR (Velodyne HDL-64E class) dominated the market through 2022 due to its wide field-of-view and long-range performance. Solid-state alternatives using MEMS mirrors, Optical Phased Arrays (OPA), and Flash illumination are achieving comparable performance at significantly lower cost and superior automotive durability. Luminar’s Iris+ achieves 250m range at a USD 600 target unit cost by 2025, representing the benchmark solid-state automotive LiDAR value proposition.

Single-Photon and Geiger-Mode LiDAR Advances

Single-photon avalanche diode (SPAD) arrays and Geiger-mode LiDAR, originally developed for defense satellite ranging, are enabling centimeter-accuracy long-range detection at ultra-low signal levels.

LiDAR-Camera-Radar Sensor Fusion Middleware

The critical technology battleground has shifted from LiDAR hardware to sensor fusion middleware. NVIDIA DRIVE Orin, Qualcomm Snapdragon Ride, and Mobileye EyeQ6 are competing to establish the dominant compute platform for fusing LiDAR, camera, and radar data into a unified perception output for Level 3–4 autonomous systems.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Installation Type | Terrestrial | 58.5% | 2025 |

| Component | Laser Scanners | 45.2% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | North America | 38.5% | 2025 |

By Installation Type

Terrestrial LiDAR commands a 58.5% majority share in 2025, reflecting the sector’s dominance by autonomous vehicle ADAS programs, ground robotics, indoor mobile mapping, and infrastructure inspection applications. Ground-based LiDAR systems benefit from the exploding automotive sensor market, where over 40 OEM AV programs are actively specifying LiDAR in production vehicles, alongside smart city mobile mapping deployments and utility corridor inspection programs across North America and Europe.

To access detailed market analysis, Request Sample

Airborne LiDAR holds a 41.5% share in 2025, driven by UAV-mounted topographic survey, forestry carbon stock assessment, corridor infrastructure inspection (transmission lines, railways, pipelines), and defense-grade reconnaissance applications.

By Component

Laser Scanners dominate the component segment at 45.2% in 2025. The laser transmitter-receiver assembly is the highest-value, highest-margin component in LiDAR system architecture, incorporating precision diode lasers, collimation optics, and avalanche photodiode detectors.

Navigation Systems at 24.6% are the fastest-growing component segment, incorporating Inertial Measurement Units (IMU), GNSS receivers, and Real-Time Kinematic (RTK) positioning modules that enable LiDAR point clouds to be georeferenced with centimeter accuracy. Tightly coupled LiDAR-IMU-GNSS configurations are now standard in all professional-grade mobile mapping and UAV survey systems. Global Positioning Systems capture 20.8% of component revenues, with multi-constellation GNSS receivers from u-blox and Trimble providing the absolute coordinate reference for LiDAR-derived spatial datasets. The Others category (9.4%) encompasses processing units, power subsystems, and enclosure components.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.5% |

AV R&D investment, USGS 3DEP national mapping, DOD autonomous sensor programs |

|

Europe |

26.4% |

Euro NCAP ADAS mandates, Copernicus aerial survey program, strong UK-Germany-Netherlands corridor survey market |

|

Asia-Pacific |

22.8% |

China NEV LiDAR mandates, Japan robotics ecosystem, South Korea automotive R&D capabilities; fastest-growing region at ~20% CAGR |

|

Latin America |

7.2% |

Mining and forestry survey in Brazil and Chile; infrastructure mapping investment growing 14% annually in 2024 |

|

Middle East & Africa |

5.1% |

Smart city programs in the UAE and Saudi Arabia (NEOM); oil & gas pipeline inspection driving industrial LiDAR adoption |

North America leads with a 38.5% share in 2025, anchored by the United States, where LiDAR is integral to AV programs (Waymo, Cruise, Aurora), the USGS 3DEP national elevation dataset program, and DOD UAV reconnaissance.

Asia-Pacific at 22.8% is the fastest-growing region, projected to surpass Europe by 2028. Japan’s precision robotics sector and South Korea’s automotive R&D clusters further strengthen the regional outlook. Europe at 26.4% benefits from the Euro NCAP 2025 safety framework that effectively mandates advanced ADAS LiDAR suites across premium vehicle segments, and from the EU Copernicus programme driving continent-wide aerial survey investment. Latin America and MEA, while smaller, are growing at above-market rates driven by extractive industry digitization and government-led smart city commitments.

Competitive Landscape

|

Company Name |

Key Platform / Product |

Market Position |

Core Strength |

|

Quantum Computing Inc. |

Remote sensing |

Challenger |

Quantum photonics company developing sensing and imaging technologies |

|

Hesai Group |

AT128 |

Challenger |

Highest unit volume globally; vertical integration; 200K+ cumulative shipments by 2024 |

|

Ouster Inc. |

OS Digital Lidar |

Challenger |

Digital-native solid-state LiDAR; robotics and AV dual-market strategy |

|

Innoviz Technologies Ltd |

InnovizOne |

Emerging |

Solid-state MEMS; BMW series production supply; automotive IATF 16949 certified |

|

RoboSense |

RS-LiDAR-M1 |

Emerging |

Chinese domestic leader; smart transportation and robotics; rapid global expansion |

|

Trimble Inc. |

Trimble MX50 |

Leader |

Professional geospatial leader; survey-to-GIS workflow; AEC vertical dominance |

|

Hexagon AB |

Airborne Sensor |

Leader |

Premium terrestrial and mobile mapping; Hexagon ecosystem integration |

The global LiDAR market is characterized by intense competition between photonics-heritage players, venture-backed pure-play LiDAR manufacturers, professional geospatial instrument leaders, and deep-pocketed automotive Tier-1 suppliers. No single player commands more than 15% of global LiDAR revenues in 2025, creating a fragmented landscape with significant M&A activity. Key competitive dynamics include: automotive-grade IATF 16949 certification as the primary OEM qualification barrier; software stack differentiation emerging as the decisive competitive moat above hardware performance parity; and Chinese domestic players offering competitive specifications at 30–40% lower price points, driving global pricing pressure.

Key Company Profiles

Quantum Computing Inc.

Quantum Computing Inc. (QCi) is a quantum photonics company developing sensing and imaging technologies that leverage the quantum properties of light (photons) to enable next-generation remote sensing, imaging, and measurement applications.

- Product & Platform Portfolio: Quantum Photonic Vibrometer (QPV), Extinctiometer (aerosol and atmospheric sensing), Noise-Resistant Voxel Scanner (NRVS) LiDAR, and quantum-enabled imaging and spectroscopy platforms.

- Recent Developments: In January 2026, Quantum Computing Inc. announced that, following its previously announced agreement to acquire Luminar Semiconductor, Inc., it has submitted a bid and has been selected as the stalking horse bidder for selected remaining assets of Luminar Technologies, Inc.

- Strategic Focus: QCi leverages quantum photonics to surpass classical LiDAR with higher sensitivity, resolution, and noise rejection, enabling accurate detection in low-visibility conditions. It targets defense, infrastructure, environmental, and industrial applications while positioning its platform as a scalable, cost-effective sensing alternative.

Hesai Group

Hesai is a LiDAR manufacturer and a leading global supplier by unit volume, serving both the Chinese NEV market and international robotics and AV customers.

- Product & Platform Portfolio: AT128 automotive LiDAR, QT128 mid-range, XT32 short-range, Pandar series survey LiDAR.

- Recent Developments: In February 2023, Hesai Group raised $190 million in its IPO, the largest U.S. listing by a Chinese company since 2021.

- Strategic Focus: Hesai leverages vertical integration (in-house ASIC design, optics manufacturing) to achieve the lowest cost structure in the industry while pursuing international market diversification beyond China to US and European robotics customers.

Trimble Inc.

Trimble is a global leader in positioning technology and precision measurement, with a dominant position in professional-grade terrestrial and airborne LiDAR survey systems. Trimble’s geospatial portfolio integrates LiDAR with GNSS, photogrammetry, and cloud software to deliver end-to-end survey-to-GIS workflow solutions for engineering, construction, and environmental markets.

- Product & Platform Portfolio: SX12 scanning total station, MX9 mobile mapping system, Trimble SiteVision, and Trimble Stratus aerial LiDAR.

- Recent Developments: In April 2024, Trimble divested its agricultural technology segment to AGCO to sharpen its focus on geospatial and construction technology, reinforcing its LiDAR-enabled positioning leadership in professional survey markets.

- Strategic Focus: Trimble is integrating AI-powered point cloud classification and BIM workflow automation into its Trimble Connect platform, targeting engineering and construction verticals demanding seamless LiDAR-to-digital-twin pipeline delivery.

Market Concentration Analysis

The global LiDAR market exhibits low-to-moderate concentration, with the top 5 players (Quantum Computing Inc., Hesai Group, Trimble Inc., Innoviz Technologies Ltd, and Hexagon AB.) collectively accounting for approximately 40–48% of global revenue in 2025. The fragmented structure reflects the coexistence of automotive, industrial, defense, and geospatial verticals, each with distinct requirements and dominant supplier ecosystems that limit cross-segment concentration.

The automotive LiDAR sub-segment is consolidating faster, driven by OEM qualification processes that favor proven suppliers with multi-year supply commitments and proven IATF 16949 process control. In contrast, the geospatial and industrial sub-segments remain highly fragmented, with over 60 active commercial LiDAR hardware vendors globally in 2025. Chinese domestic players are gaining global share rapidly, collectively estimated at 20–25% of global automotive LiDAR unit volume by 2025, and are beginning to challenge established Western players in European and US commercial survey markets.

Investment & Growth Opportunities

Fastest-Growing Segments

Navigation Systems is the highest-growth component at an estimated 18% CAGR through 2034, driven by LiDAR-IMU-GNSS tight coupling becoming standard across all professional autonomous navigation platforms. The Airborne LiDAR installation segment is also outpacing the market at approximately 19% CAGR as UAV-based survey continues to displace manned aircraft and ground crew methods across forestry, mining, and corridor inspection applications globally.

Emerging Application Expansion

Indoor LiDAR for autonomous mobile robots (AMRs) in warehouse logistics is a high-growth adjacent opportunity, with Amazon Robotics, Geek+, and Mujin deploying LiDAR-navigated AMR fleets globally. Building inspection and BIM capture via handheld LiDAR is also expanding as digital twin construction workflows become standard in large-scale construction management.

Venture & Private Investment Trends

LiDAR sector venture investment, with notable activity in solid-state automotive LiDAR, AI perception middleware, and autonomous logistics platforms. Strategic M&A has consolidated Ouster and Velodyne into a single entity, while Trimble’s portfolio realignment signals ongoing restructuring in professional geospatial LiDAR. Chinese EV software and sensor start-ups continued to attract significant domestic investment for global expansion programs.

Future Market Outlook (2026-2034)

The global LiDAR market forecast projects strong value expansion from USD 3.65 Billion in 2025 to USD 14.73 Billion by 2034 at a CAGR of 16.27%, representing a four-fold increase in market value. This sustained high-growth trajectory is underpinned by three structural demand vectors: automotive ADAS and AV production ramp, smart infrastructure digitization investment, and defense sensor modernization programs globally.

Three technology shifts are likely to reshape the LiDAR market through 2034. First, the shift to solid-state architectures will drive meaningful reductions in cost, size, and power consumption, enabling broader adoption in automotive and other high-volume applications. Second, AI-native perception stacks are transforming LiDAR from a sensing hardware component into an intelligent system, enabling faster processing, lower latency, and real-time decision-making across autonomous platforms. Third, advances in long-range and high-sensitivity LiDAR are expanding performance boundaries, opening new use cases in defense, aerospace, and large-scale infrastructure monitoring.

By 2034, LiDAR is expected to evolve from a niche sensing technology into a core spatial intelligence layer embedded across vehicles, robots, drones, and smart infrastructure. The market will likely consolidate around three tiers: automotive-grade sensor manufacturers operating at scale, professional geospatial solution providers, and software platforms focused on processing and monetizing 3D spatial data.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024–2025 with LiDAR industry stakeholders, including engineering directors at hardware manufacturers, autonomous vehicle program managers at global OEMs, geospatial survey firm technology officers, defense procurement specialists, and LiDAR AI software platform developers. Quantitative surveys of 120+ industry participants supplemented the qualitative insight base.

Secondary Research

Secondary sources include USGS 3DEP program publications, IEA Global EV Outlook 2024, FAO forestry remote sensing reports, GSMA Connected Vehicle data, S&P Global Mobility (IHS Markit) automotive sensor fitment databases, EU Copernicus programme documentation, and IMARC Group’s proprietary spatial sensing industry database covering 2010–2025.

Forecasting Models

Market size estimations were derived using combined top-down and bottom-up forecasting models incorporating AV production forecasts, geospatial survey market spending data, government smart city investment budgets, and historical LiDAR cost reduction curves. Scenario analysis (base, optimistic, conservative) was applied to key uncertainty variables, including solid-state LiDAR cost trajectory and autonomous vehicle regulatory approval timelines across major geographies.

LiDAR Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and LiDAR Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Installation Types Covered | Airborne, Terrestrial |

| Components Covered | Laser Scanners, Navigation Systems, Global Positioning Systems, Others |

| Applications Covered | Corridor Mapping, Engineering, Environment, Exploration, ADAS, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Quantum Computing Inc., Hesai Group, Ouster Inc., Innoviz Technologies Ltd , RoboSense, Trimble Inc., Hexagon AB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the LiDAR market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global LiDAR market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the LiDAR industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the LiDAR Market Report

The global LiDAR market was valued at USD 3.65 Billion in 2025.

The market is projected to reach USD 14.73 Billion by 2034, growing at a CAGR of 16.27% during 2026 to 2034.

Terrestrial LiDAR leads with a 58.5% share in 2025.

Laser Scanners dominate at a 45.2% component share in 2025.

North America leads with a 38.5% share in 2025.

Key drivers include AV and ADAS proliferation, smart city digital twin adoption, defense UAV reconnaissance modernization, and solid-state LiDAR cost reduction.

Asia-Pacific is the fastest-growing region at approximately 20% CAGR through 2034.

Leading companies include Quantum Computing Inc., Hesai Group, Ouster Inc., Innoviz Technologies Ltd, RoboSense, Trimble Inc., and Hexagon AB.

LiDAR provides real-time 3D environmental mapping with sub-centimeter accuracy at ranges up to 300m, enabling autonomous vehicles to detect and classify obstacles, pedestrians, and road markings with reliability that camera-only systems cannot match in low-light or adverse weather conditions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)