Limestone Market Size, Share, Trends and Forecast by Type, Size, End-Use Industry, and Region, 2026-2034

Global Limestone Market Size, Share, Trends & Forecast (2026-2034)

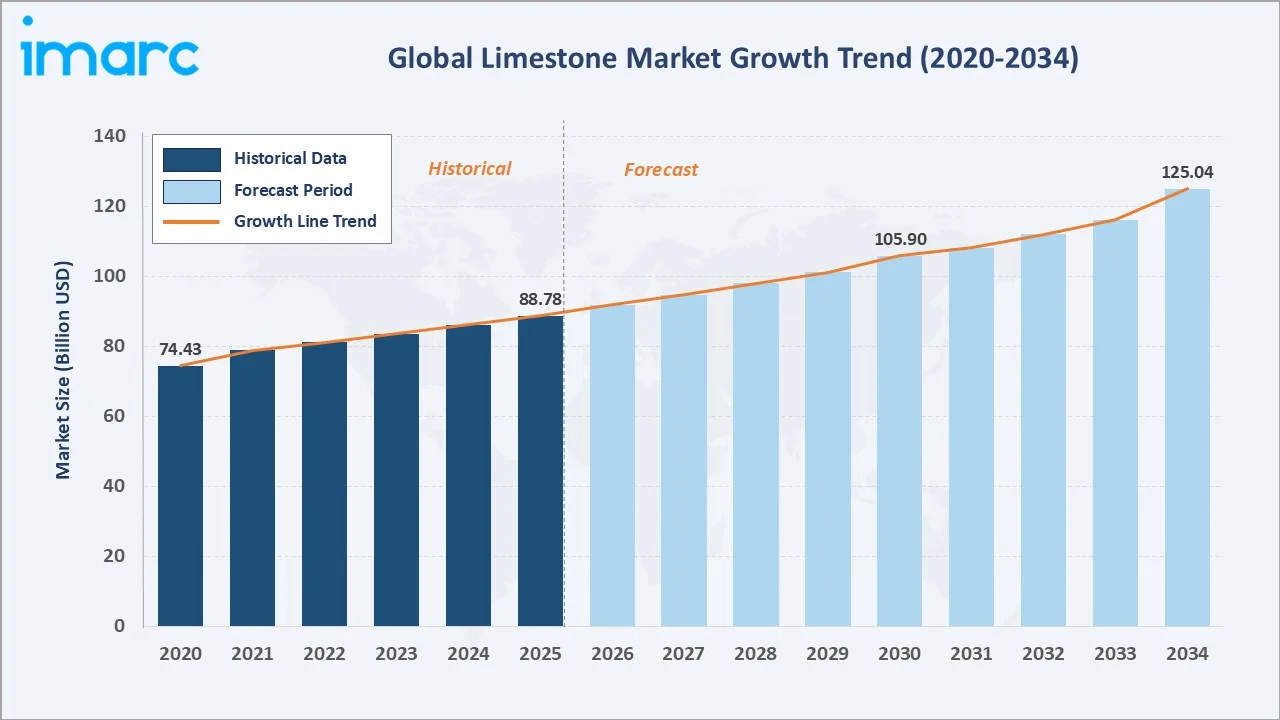

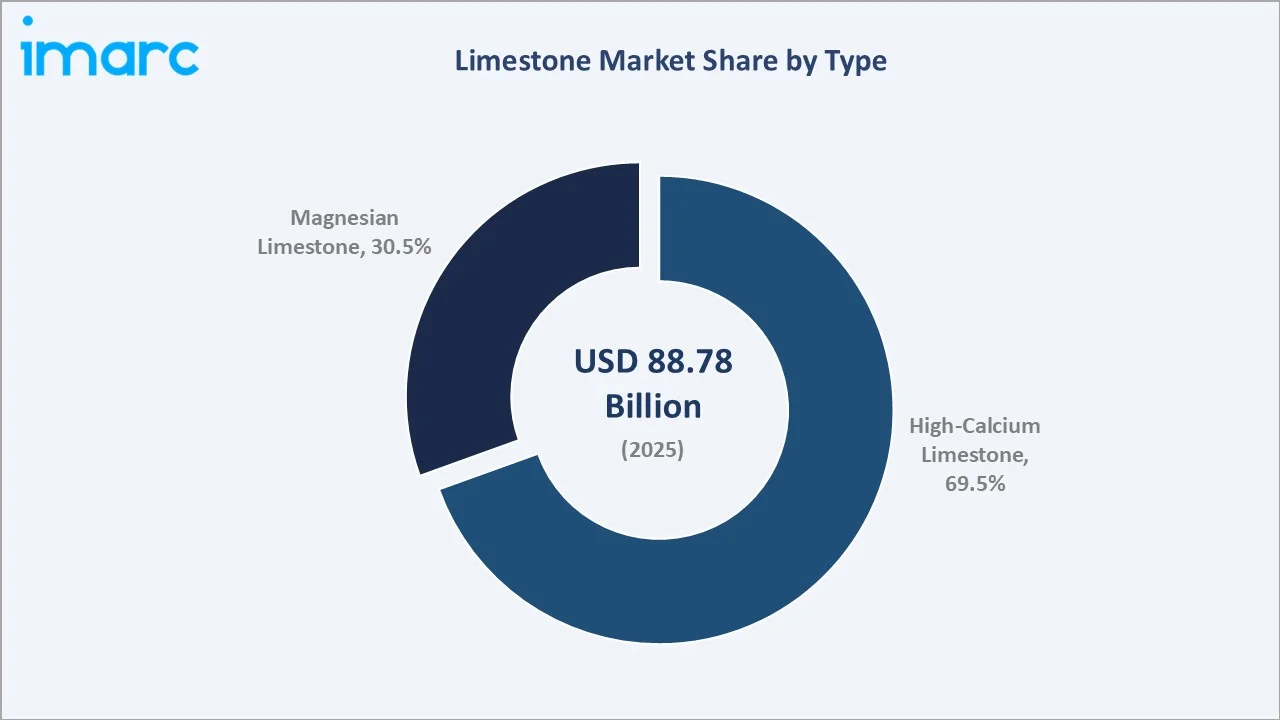

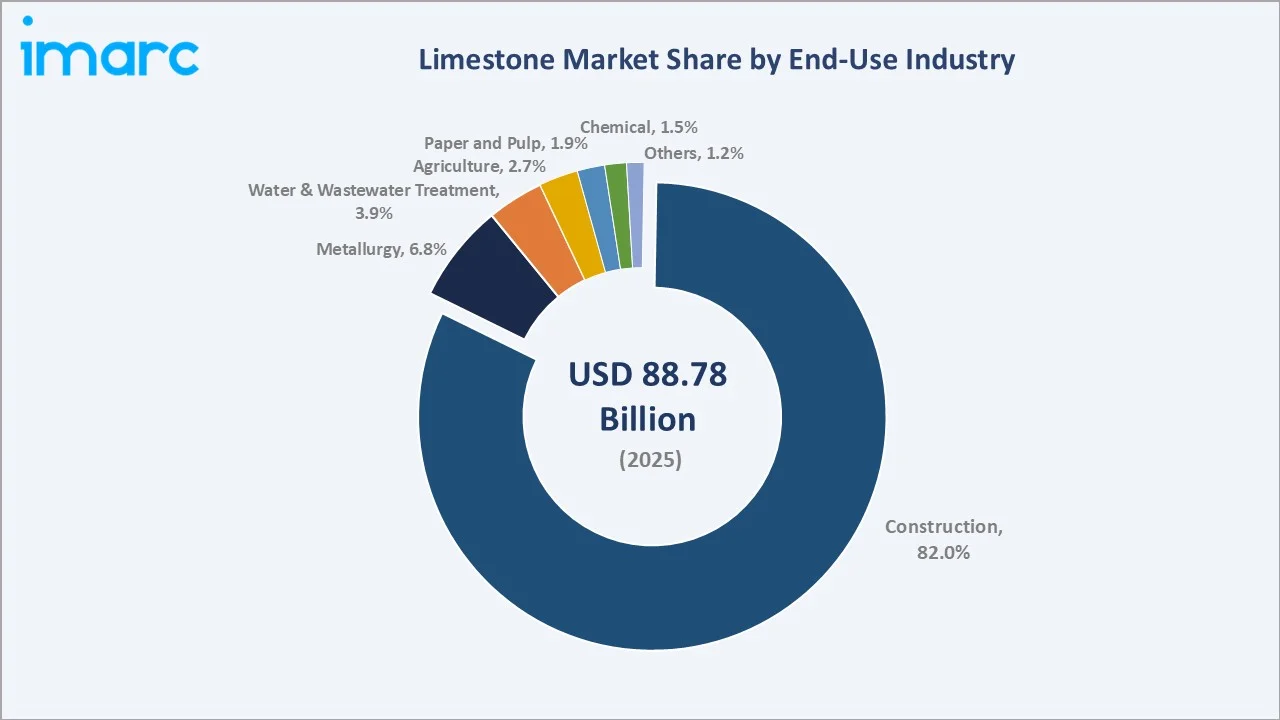

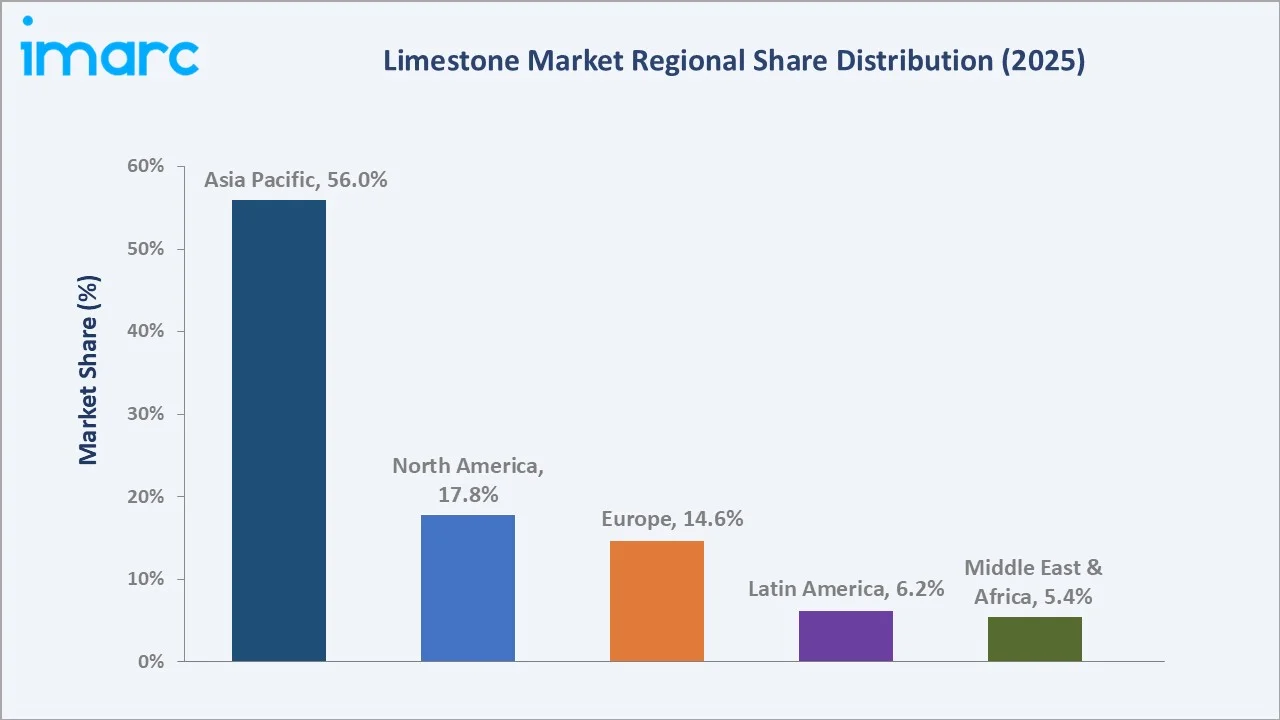

The global limestone market size was valued at USD 88.78 Billion in 2025 and is projected to reach USD 125.04 Billion by 2034, exhibiting a CAGR of 3.59% during the forecast period 2026-2034. Strong construction and infrastructure demand, expanding use of high-calcium grades in cement, flue gas desulfurization, and steel flux, and rising agricultural lime consumption are driving the limestone market growth. High-Calcium Limestone leads the type at 69.5% in 2025, while Construction dominates the end-use at 82.0%. Asia Pacific accounts for 56.0% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 88.78 Billion |

|

Forecast Market Size (2034) |

USD 125.04 Billion |

|

CAGR (2026-2034) |

3.59% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (56.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Type |

High-Calcium Limestone (69.5%, 2025) |

|

Leading End-Use Industry |

Construction (82.0%, 2025) |

The global limestone market growth trajectory from 2020 through 2034, contrasting a stable historical base against a sustained forecast curve powered by infrastructure spending, decarbonisation chemistry, and specialty product premiumisation.

To get more information on this market, Request Sample

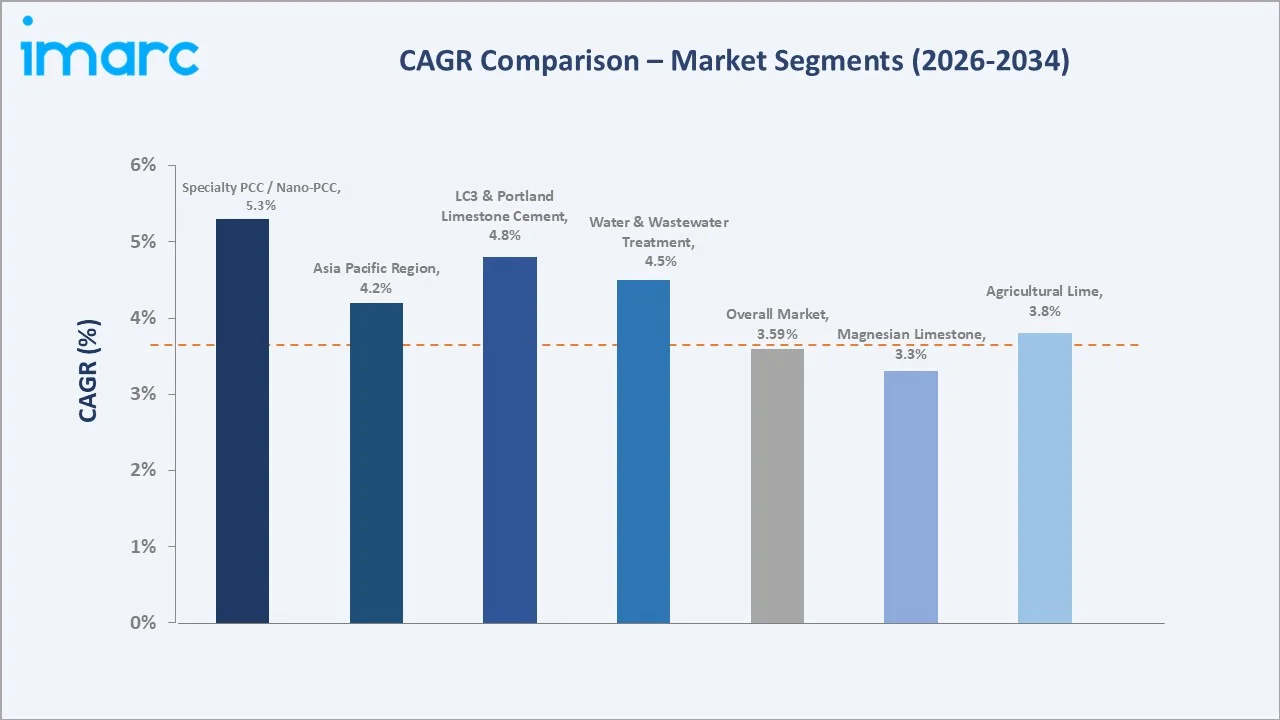

Segment-level CAGR comparisons highlighting specialty PCC and LC3 cement blends as among the fastest-growing sub-categories within the global limestone industry analysis through 2034.

Executive Summary

The global limestone market is undergoing steady expansion driven by the convergence of infrastructure spending, heavy-industry emission chemistry, and soil remineralisation across agriculture. Valued at USD 88.78 Billion in 2025, the market is forecast to reach USD 125.04 Billion by 2034 at a CAGR of 3.59%.

High-Calcium Limestone commands 69.5% of type revenue in 2025, favoured for cement, quicklime, flue gas desulfurization, and steel flux applications where purity above 95% CaCO3 is essential. Magnesian Limestone holds 30.5%, the strongest in agricultural dolomitic lime, refractory magnesia, and specialty glass.

Construction dominates end-use at 82.0% in 2025, followed by Metallurgy (6.8%) and Water and Wastewater Treatment (3.9%). Asia Pacific leads with a 56.0% global revenue share in 2025, driven by China's cement output, India's National Infrastructure Pipeline, and ASEAN urbanisation. North America holds 17.8% and Europe 14.6%, both shaped by decarbonisation policy and Portland-Limestone Cement adoption.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

High-Calcium Limestone - 69.5% share (2025) |

|

Largest End-Use Industry |

Construction - 82.0% share (2025) |

|

Leading Region |

Asia Pacific - 56.0% revenue share (2025) |

|

Second Region |

North America - 17.8% revenue share (2025) |

|

Top Companies |

Lhoist, Carmeuse, Graymont, Omya International AG, Imerys |

|

Key Market Opportunity |

Low-carbon cement and calcined clay blends (LC3) |

Key Analytical Observations Supporting the Above Data:

- High-Calcium Limestone's 69.5% lead in 2025 reflects its central role in Portland cement, steel flux, and FGD scrubbers, where chemistry purity drives selection over regional availability.

- Construction's 82.0% share in 2025 is anchored by above USD 2 trillion in annual global construction spending, with cement demand scaling alongside emerging-market urbanisation through 2034.

- Asia Pacific's 56.0% dominance in 2025 is led by China, the world's largest cement producer.

- Water and Wastewater Treatment at 3.9% in 2025 is a structurally expanding segment, with utilities shifting to hydrated lime for pH correction at 25-30% lower cost than caustic soda.

- Agricultural lime accounts for 2.7% in 2025, with the United States alone applying nearly 20 million tonnes annually to neutralise acidic farmland soils.

Global Limestone Market Overview

Limestone is a sedimentary rock composed predominantly of calcium carbonate (CaCO3), with magnesium-rich variants classified as dolomitic or magnesian limestone. It is the foundational raw material for Portland cement, quicklime, hydrated lime, and precipitated calcium carbonate, and a flux in iron and steel smelting. The ecosystem spans quarry operators, cement integrators, lime processors, logistics providers, and end users in construction, metallurgy, agriculture, paper, chemicals, and water treatment.

Applications span construction, infrastructure, steel and iron flux, flue gas desulfurization, agricultural soil conditioning, water and wastewater treatment, paper and pulp, chemicals, and specialty PCC applications in polymers and pharmaceuticals.

Macroeconomic enablers include annual global construction spending, global cement production, and tightening emissions regulations that favour lime-based flue gas and water treatment chemistries worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

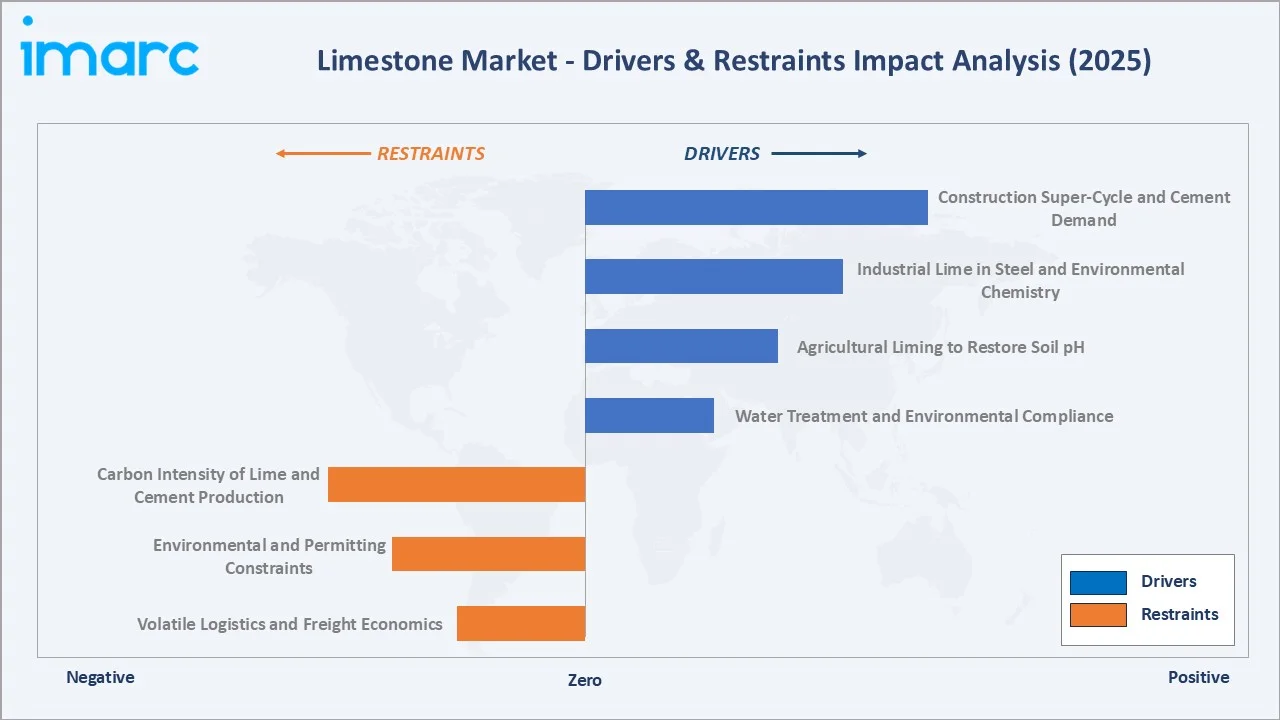

Market Drivers

- Construction Super-Cycle and Cement Demand: Global cement production reached 4.1 Billion tonnes in 2023, up from 1.39 Billion tonnes in 1995, translating directly into scaled limestone offtake given its ~85% share of clinker input. Urbanisation in India, Indonesia, Vietnam, and Nigeria is forecast to add over 2.5 Billion urban residents by 2050, requiring sustained clinker output.

- Industrial Lime in Steel and Environmental Chemistry: Blast furnace and basic oxygen steelmaking consume high-calcium limestone as a flux to remove silica and phosphorus impurities. Flue gas desulfurization installations at coal-fired power plants remain a multi-billion-dollar end-market, with limestone slurry capturing over 90% of sulfur dioxide emissions per US EPA data.

- Agricultural Liming to Restore Soil pH: Acidic soils affect over 30% of the world's arable land. Agricultural lime application improves crop yields by 10-15% in affected zones, with the US applying approximately 20 million tonnes annually and India accelerating soil health card programmes through 2030.

- Water Treatment and Environmental Compliance: Municipal and industrial utilities use limestone and hydrated lime for pH correction, fluoride removal, and phosphate precipitation. UN SDG 6 investment requirements of USD 150 billion annually through 2030 underpin this structural growth.

Market Restraints

- Carbon Intensity of Lime and Cement Production: Calcination releases roughly 0.5 tonnes of CO2 per tonne of quicklime produced. EU Emissions Trading System costs rose above EUR 70 per tonne CO2 in 2024, compressing margins for European lime producers and incentivising demand-substitution research.

- Environmental and Permitting Constraints: Quarry expansion faces tightening land-use regulations, dust and noise compliance, and community opposition in North America and Europe. New greenfield permit lead-times have stretched to 8-10 years in multiple jurisdictions.

- Volatile Logistics and Freight Economics: Limestone is a low-value, high-bulk commodity where transport typically represents 40-60% of delivered cost. Diesel and bulk freight volatility directly compresses producer margins in inland markets.

Market Opportunities

- Low-Carbon Cement and LC3 Blends: Limestone Calcined Clay Cement (LC3) can reduce clinker intensity by up to 50%, unlocking a premium market for finely ground limestone in blended cements. Global LC3 capacity announcements exceeded 40 million tonnes by 2025.

- Carbon Capture, Utilisation and Storage (CCUS): Calcium looping, mineral carbonation, and direct air capture use limestone-derived sorbents. The International Energy Agency forecasts CCUS capacity scaling from 50 Mt/year in 2024 toward 1.2 Gt/year by 2030 in the Announced Pledges Scenario.

- Precipitated Calcium Carbonate (PCC) in Paper and Plastics: PCC and ground calcium carbonate (GCC) are expanding into bioplastics, pharmaceuticals, and premium paper coatings. Asia Pacific PCC demand is projected to grow at above 5% CAGR through 2034.

Market Challenges

- Substitution Risk from Alternative Binders: Geopolymers, calcium sulfoaluminate cements, and alkali-activated materials are entering commercial niches where they can displace clinker by 30-70%, creating long-term volume pressure on traditional cement-grade limestone.

- Dust, Silica, and Worker Safety Compliance: Respirable crystalline silica exposure limits have tightened globally. OSHA and equivalent regulators drive capex into wet suppression, dust collection, and enclosed conveying systems that raise unit operating costs.

Emerging Market Trends

1. Green Cement and Clinker Substitution

Cement producers are shifting toward blended formulations that integrate 10-30% finely ground limestone as a supplementary cementitious material. Holcim, Heidelberg Materials, and UltraTech have each committed to LC3 or Portland-Limestone Cement rollouts that materially reshape downstream limestone specification requirements by 2030.

2. Carbon Capture Integration at Lime Plants

Oxy-fuel calcination, amine-based capture retrofits, and calcium looping pilots are scaling at European and Canadian lime plants. Lhoist's Rheinkalk site and Heidelberg Materials' Brevik project are landmark references, with carbon capture economics expected to normalise by 2028-2030.

3. Agricultural Lime Digitalisation and Precision Spreading

Variable-rate application, satellite-guided soil pH mapping, and pelletised lime formulations are converting traditional bulk agricultural lime into a higher-margin, precision-agronomy input. The US and Brazilian row-crop belts are the earliest adopters through 2028.

4. Nanomaterials and Advanced PCC Applications

Nano-precipitated calcium carbonate (NPCC) is entering high-performance plastics, rubber tyres, and pharmaceutical excipients. Minerals Technologies and Omya have commercialised particle-size-controlled grades that command 3-5x pricing over bulk ground products.

5. Circular Construction and CDW Recycling

Recycled concrete aggregate and carbonated construction demolition waste are emerging as partial substitutes for virgin crushed limestone in road base and non-structural concrete. The EU Waste Framework Directive's target of 70% construction waste recovery is accelerating this substitution.

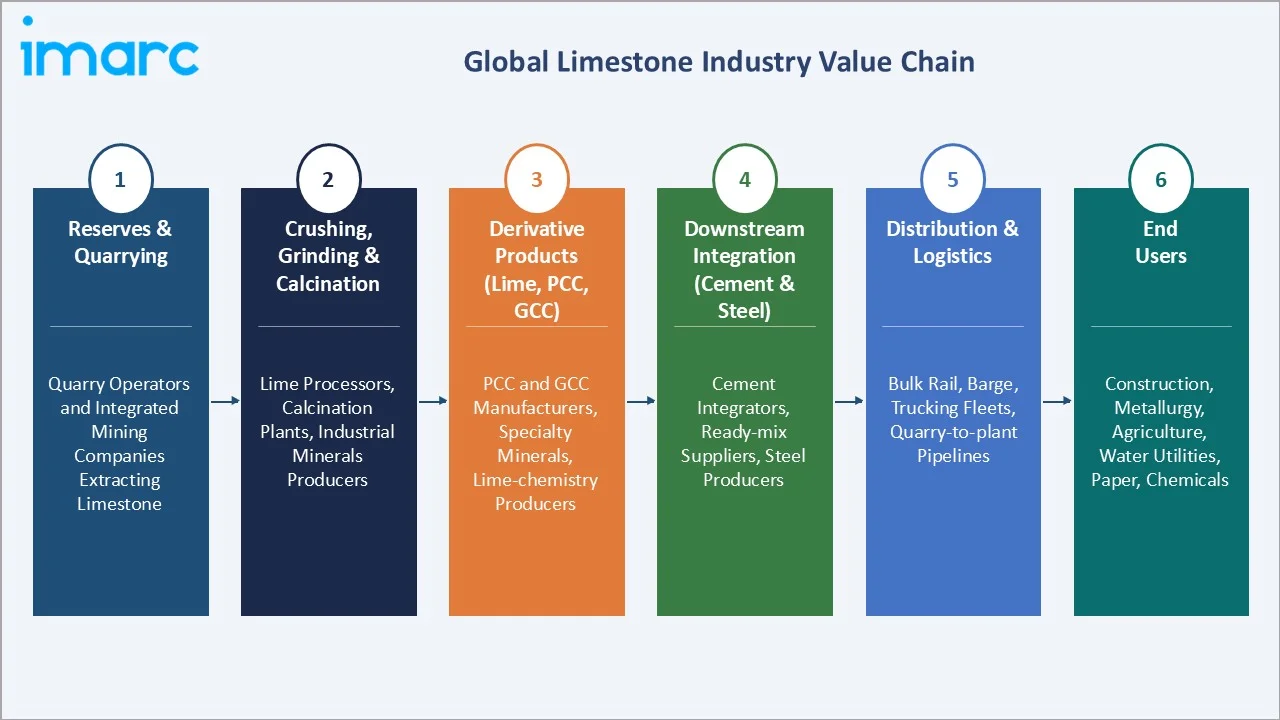

Industry Value Chain Analysis

The limestone value chain spans six integrated stages from quarry extraction through end-use consumption. Each stage presents distinct cost structures, logistics complexity, and margin profiles.

|

Stage |

Participants / Activities |

|

Reserves & Quarrying |

Quarry operators and integrated mining companies extracting limestone from surface and underground deposits |

|

Crushing, Grinding & Calcination |

Lime processors, calcination plants, and industrial minerals producers supplying graded products |

|

Derivative Products (Lime, PCC, GCC) |

Precipitated and ground calcium carbonate manufacturers, specialty minerals, and lime-chemistry producers |

|

Downstream Integration (Cement & Steel) |

Cement integrators, ready-mix concrete suppliers, steel producers, and construction material majors |

|

Distribution & Logistics |

Bulk rail, barge, trucking fleets, and quarry-to-plant pipelines |

|

End Users |

Construction, metallurgy, agriculture, water utilities, paper, chemicals |

Upstream reserve owners capture the highest margin when they control both quarrying and downstream calcination. Integrated players with vertically coordinated operations have gained share in Europe and North America by bundling limestone supply with lime processing and technical service.

Technology Landscape in the Limestone Industry

Extraction and Processing Technology

Modern quarry operations deploy GPS-guided drilling, fleet telematics, and ore-tracking sensors to reduce dilution and improve grade control. Dry-sorting X-ray transmission systems are gaining adoption at premium chemical-grade operations to separate high-calcium ore streams from dolomitic or silica-contaminated zones.

Calcination and Kiln Efficiency

Parallel-flow regenerative kilns now account for above 40% of new European lime kiln capacity, cutting specific energy consumption by 15-20% versus rotary kiln baselines. Alternative fuel substitution rates at lime and cement kilns have surpassed 50% in leading European operations, reducing scope-1 emissions intensity.

Digital Quarry and AI-Enabled Operations

Autonomous haul trucks, drone-based stockpile measurement, and AI-driven predictive maintenance are spreading from majors to mid-tier operators. Lhoist, Heidelberg, and CRH have publicly committed to digital quarry rollouts targeting 10-15% cost productivity improvements through 2028.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | High-Calcium Limestone | 69.5% | 2025 |

| Size | Crushed Limestone | 🔒 | 2025 |

| End-Use Industry | Construction | 82.0% | 2025 |

| Region | Asia Pacifi | 56.0% | 2025 |

By Type

High-Calcium Limestone commands a 69.5% majority share in 2025, anchored by cement production, flue gas desulfurization, and steelmaking flux demand. Its CaCO3 content above 95% makes it the preferred feedstock for quicklime and hydrated lime, which in turn supply water utilities, pulp bleaching, and soil stabilisation markets. Growth is underpinned by FGD retrofits in India and Southeast Asia and by Portland-Limestone Cement adoption in North America.

To access detailed market analysis, Request Sample

Magnesian Limestone holds 30.5% in 2025, driven by dolomitic agricultural lime, refractory magnesia production, and specialty glass manufacturing. Its magnesium content makes it valuable for soils where both pH correction and magnesium supplementation are required, and for steelmaking refractories exposed to basic slag chemistry.

By End-Use Industry

Construction leads at 82.0% in 2025, reflecting limestone's dominant role in Portland cement, aggregate, ready-mix concrete, and asphalt fillers. China's 2.0+ billion tonne cement output and India's USD 1.4 Trillion infrastructure pipeline anchor this share, while US Portland-Limestone Cement is scaling at above 10% annual cement volume conversion.

Metallurgy at 6.8% in 2025 is anchored by steel flux demand, with global crude steel production at 1.88 billion tonnes in 2024 per the World Steel Association. Water and Wastewater Treatment at 3.9% is the fastest-growing non-construction end-use, expanding above 4% CAGR through 2034 on utility capex. Agriculture (2.7%), Paper and Pulp (1.9%), Chemical (1.5%), and Others (1.2%) collectively provide margin diversification outside construction-linked volatility.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

56.0% |

China cement output, India infrastructure, ASEAN urbanisation, FGD retrofits |

|

North America |

17.8% |

Portland-Limestone Cement, US highway bill, shale gas lime, CCUS pilots |

|

Europe |

14.6% |

EU Green Deal, CBAM, LC3 cement, carbon capture at lime plants |

|

Latin America |

6.2% |

Brazil, Mexico construction, mining-sector lime demand |

|

Middle East & Africa |

5.4% |

GCC megaprojects, Saudi Vision 2030, and African cement capacity |

Asia Pacific commands a 56.0% global revenue share in 2025, the most dominant regional position across any commodity minerals segment. China leads with over 2.0 billion tonnes of annual cement output and the world's largest limestone reserve base. India is the fastest-growing national market on a volume basis, with the National Infrastructure Pipeline directing above USD 1.4 trillion into construction through 2030 and coal-plant FGD mandates scaling approximately 200 GW of retrofit demand.

North America holds 17.8% in 2025, anchored by the US Portland Cement Association's transition to PLC, which now exceeds 25% of cement shipments. The USD 1.2 Trillion Infrastructure Investment and Jobs Act continues to support aggregate and cement demand through 2030. Europe, at 14.6%, is defined by carbon policy: EU CBAM and ETS pricing above EUR 70 per tonne CO2 are reshaping production economics and customer specifications in favour of low-carbon lime and cement blends.

Latin America, at 6.2%, is led by Brazil and Mexico, where cement demand is recovering alongside housing and transport programmes. Middle East and Africa at 5.4% is anchored by GCC megaprojects, including NEOM, Qiddiya, and the Red Sea Project, and African cement capacity expansion, particularly in Nigeria, Egypt, and Ethiopia.

Competitive Landscape

|

Company Name |

Brand / Offerings |

Market Position |

Core Strength |

|

Lhoist |

Akdolit, Sorbacal, Calexor, Proviacal, Asphacal, Tradical, Calcifertil |

Leader |

Global lime and limestone, FGD, environmental solutions |

|

Carmeuse |

High Calcium Limestone, High Calcium Ag Lime, Ground Calcium Carbonate |

Leader |

Lime, limestone, mineral products, steel, and FGD |

|

Graymont |

Graymont, Limil |

Challenger |

High-calcium, dolomitic lime, North America, and APAC |

|

Omya International AG |

Omya Calcipur |

Leader |

GCC and PCC fillers, paper, plastics, paint |

|

Imerys |

Calcius range |

Leader |

Industrial minerals, PCC, GCC, paper, and polymers |

|

Minerals Technologies Inc. |

Specialty Minerals |

Challenger |

PCC for paper, performance materials |

|

Mississippi Lime Company |

Mississippi Lime |

Emerging |

Part of HBM Holdings Company, US high-calcium lime, chemical and environmental |

The global limestone competitive landscape is moderately concentrated at the international lime and specialty grades end, and highly fragmented at the regional crushed-limestone and aggregate tier. Lhoist, Carmeuse, and Graymont collectively hold roughly 25-30% of global lime and high-calcium limestone value in 2025, while Omya and Imerys dominate the downstream PCC and GCC filler markets.

Key Company Profiles

Lhoist Group

Lhoist is headquartered in Belgium and operates over 100 production sites across more than 25 countries. The group serves steel, construction, environmental, agriculture, and chemicals customers with integrated quarry-to-kiln operations.

- Product & Platform Portfolio: Quicklime, hydrated lime, ground limestone, Sorbacal sorbents for flue gas cleaning, PROVIRON mineral blends, and agricultural lime formulations.

- Recent Developments: In March 2023, Lhoist and industrial gases company Air Liquide are working on a plan for a large-scale industrial plant to capture the CO2 generated during lime production. Thyssenkrupp will be a beneficiary, as it aims to boost production of “green” steel using carbon-neutral lime.

- Strategic Focus: Decarbonisation of lime production, environmental chemistry expansion in FGD and water treatment, and selective emerging-market capacity additions where high-calcium reserves and downstream demand converge.

Carmeuse Group

Carmeuse is a Belgium-headquartered global producer of lime, limestone, and mineral-based chemistries, operating across Europe, North America, Africa, and Asia. The group integrates quarrying, calcination, hydration, and technical service for steel, cement, construction, environmental, and agricultural customers.

- Product & Platform Portfolio: Quicklime, hydrated lime, limestone aggregates, specialty milled products, flue gas sorbents, and water treatment chemistries.

- Recent Developments: In January 2026, Carmeuse Ventures announced the investment in Planeteers, a leading startup in the field of carbon capture and storage.

- Strategic Focus: Low-carbon kiln technology, vertical integration into environmental services, and selective M&A to consolidate North American regional lime positions.

Graymont Limited

Graymont is a privately held Canadian global lime and limestone producer with operations across North America and the Asia Pacific. The company serves steel, construction, environmental, and paper customers with a focus on high-calcium and dolomitic lime chemistries.

- Product & Platform Portfolio: High-calcium quicklime, dolomitic quicklime, hydrated lime, pulverised limestone, and specialty construction chemistry blends.

- Recent Developments: In April 2025, Graymont confirmed that it is proceeding with the investment to expand its operations in Victoria, Australia, to meet the needs of its growing customer base. The investment will enable increased local production of lime, which is a critical input for industries including construction, mining, and agriculture.

- Strategic Focus: Capacity modernisation with lower energy intensity, North American Portland-Limestone Cement supply growth, and disciplined Asia Pacific expansion.

Market Concentration Analysis

The global limestone market exhibits a bifurcated concentration profile. In international lime and specialty grades, the top five players (Lhoist, Carmeuse, Graymont, Omya, Imerys) collectively capture approximately 30-35% of value in 2025. In regional aggregate and cement-grade limestone, the market remains highly fragmented, with thousands of quarry operators serving local construction markets within 150 km transport radii.

Consolidation is accelerating in North America and Europe, where carbon policy costs, permitting complexity, and capex requirements for low-emission kilns favour larger integrated players. Conversely, Asia Pacific and Africa remain fragmented, with strong national champions competing alongside international majors.

Investment & Growth Opportunities

Fastest-Growing Segments

Water and Wastewater Treatment is the fastest-growing non-construction end-use, projected at above 4% CAGR through 2034 on utility modernisation. Specialty PCC and nano-PCC in polymers, pharmaceuticals, and premium paper are forecast above 5% CAGR, commanding 3-5x bulk pricing.

Emerging Market Expansion

India, Indonesia, Vietnam, and Nigeria represent the highest-growth national limestone markets on a volume basis through 2034, driven by urbanisation and infrastructure programmes. GCC states and North Africa are expanding chemistry-grade lime demand alongside megaprojects and desalination-driven water treatment.

Venture & Private Investment Trends

Private equity and strategic capital are targeting integrated lime platforms in North America and Europe. Carbon capture retrofit funding under US DOE 45Q credits and EU Innovation Fund grants is unlocking a new investment cycle of USD 2-5 billion through 2030 in the limestone and lime sector.

Future Market Outlook (2026-2034)

The global limestone market forecast projects steady value expansion from USD 88.78 Billion in 2025 to USD 125.04 Billion by 2034 at a CAGR of 3.59%, underpinned by infrastructure spending, environmental compliance capex, and specialty product premiumisation. Volume growth will be led by Asia Pacific, while value growth will accelerate in Europe and North America as carbon policy premia and specialty chemistry margins expand.

Three structural shifts will reshape the market by 2034. First, Portland-Limestone Cement and LC3 adoption will redefine mainstream cement-grade limestone specifications. Second, carbon capture at lime plants will move from pilot to commercial scale at the largest European and North American sites. Third, digital quarry operations and AI-enabled supply chains will consolidate mid-tier players into integrated platforms.

By 2034, the industry will likely feature a smaller number of integrated, lower-carbon lime majors, a diversified specialty chemistry tier led by Omya, Imerys, and Minerals Technologies, and a resilient regional aggregate base serving local construction needs.

Research Methodology

Primary Research

Primary research included more than 50 structured interviews conducted in 2024-2025 with quarry operators, lime plant managers, cement and steel procurement leads, water utility engineers, agricultural extension specialists, and institutional investors. Primary inputs validated market sizing, segmentation estimates, regional supply-demand balances, and competitive positioning.

Secondary Research

Secondary sources include USGS Mineral Commodity Summaries, International Cement Review (Global Cement Report), World Steel Association statistics, IEA Global Energy and Climate Outlook, UN Environment Programme publications, company annual reports, EU Commission CBAM documentation, and industry trade press, including Global Cement Magazine, International Mining, and World Lime.

Forecasting Models

Market size and forecasts were derived using combined top-down and bottom-up approaches. Top-down modelling used construction GDP elasticity, urbanisation indices, and steel and cement output linkages. Bottom-up modelling aggregated country-level quarry capacity and end-use consumption data. Base, optimistic, and conservative scenarios were tested against macroeconomic and policy variables.

Limestone Market Report Coverage:

|

Attribute |

Details |

|

Market Size (2025) |

USD 88.78 Billion |

|

Forecast (2034) |

USD 125.04 Billion |

|

CAGR |

3.59% (2026-2034) |

|

Historical Period |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation |

Type, Size, End-Use Industry, Region |

|

Regional Analysis |

Asia Pacific, North America, Europe, Latin America, Middle East & Africa |

|

Key Companies |

Lhoist, Carmeuse, Graymont, Omya International AG, Imerys, Minerals Technologies Inc., and Mississippi Lime Company |

|

Report Format |

PDF + Excel |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, limestone market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global limestone market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the limestone industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Limestone Market Report

The global limestone market was valued at USD 88.78 Billion in 2025, driven by construction demand, cement output, and environmental lime chemistries across major industrial economies.

The market is projected to reach USD 125.04 Billion by 2034, growing at a CAGR of 3.59% during 2026 to 2034, supported by infrastructure spending and specialty product demand.

High-Calcium Limestone leads with a 69.5% share in 2025, driven by cement, quicklime, flue gas desulfurization, and steel flux applications demanding above 95% CaCO3 purity.

Construction dominates at 82.0% in 2025, reflecting limestone's central role in Portland cement, aggregate, ready-mix concrete, asphalt, and global infrastructure projects.

Asia Pacific leads with a 56.0% share in 2025, driven by China's cement output, India's infrastructure pipeline, ASEAN urbanisation, and expanding flue gas desulfurization capacity.

Key drivers include 4.1 billion tonnes of annual global cement output, rising agricultural liming, environmental water treatment demand, and decarbonisation technologies using lime.

Specialty PCC, nano-PCC in polymers, and water treatment limestone are the fastest-growing sub-segments, supported by premium chemistries and utility modernisation investment.

Leading companies include Lhoist, Carmeuse, Graymont, Omya International AG, Imerys, Minerals Technologies Inc., and Mississippi Lime Company.

Carbon policy is driving kiln efficiency upgrades, alternative fuel substitution, and carbon capture pilots, reshaping cost structures and favouring producers with low-emission operations.

Limestone contributes approximately 85% of the raw mix for Portland cement clinker and is increasingly used in Portland-Limestone Cement blends to reduce CO2 intensity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)