Liquid Biopsy Market Size, Share, Trends and Forecast by Product and Service, Circulating Biomarker, Cancer Type, End User, and Region, 2026-2034

Global Liquid Biopsy Market Size, Share, Trends & Forecast (2026-2034)

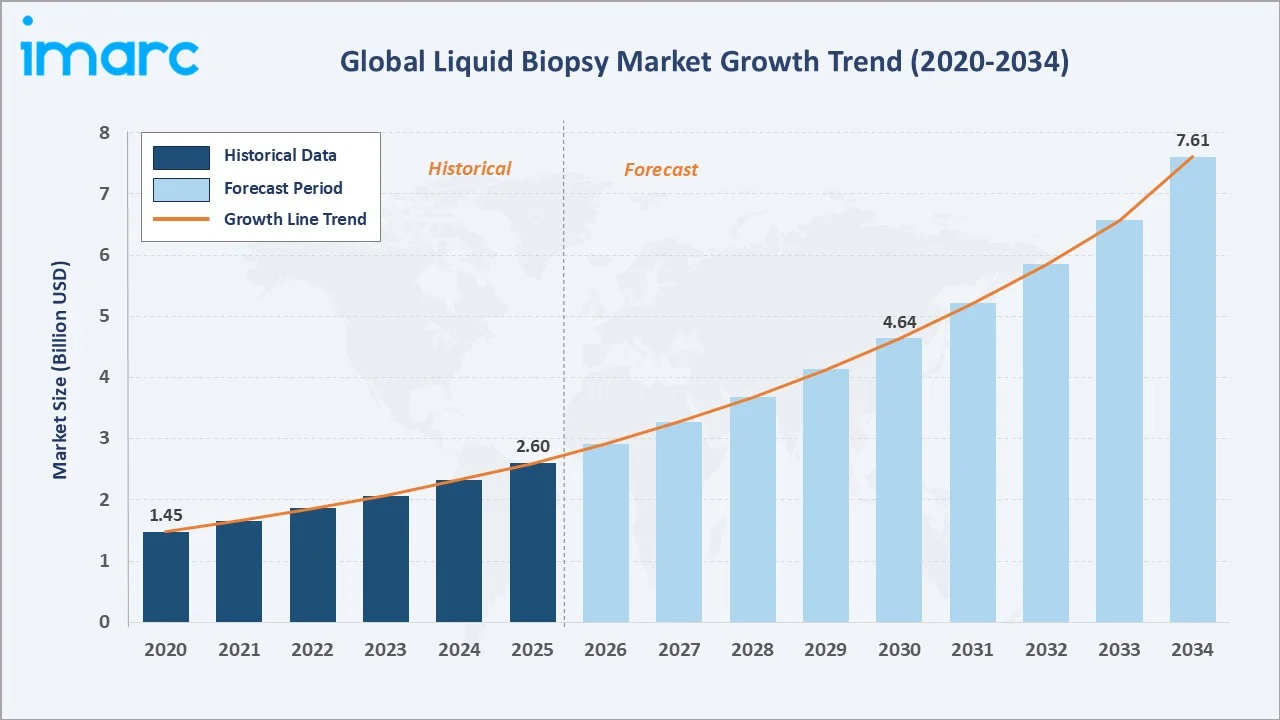

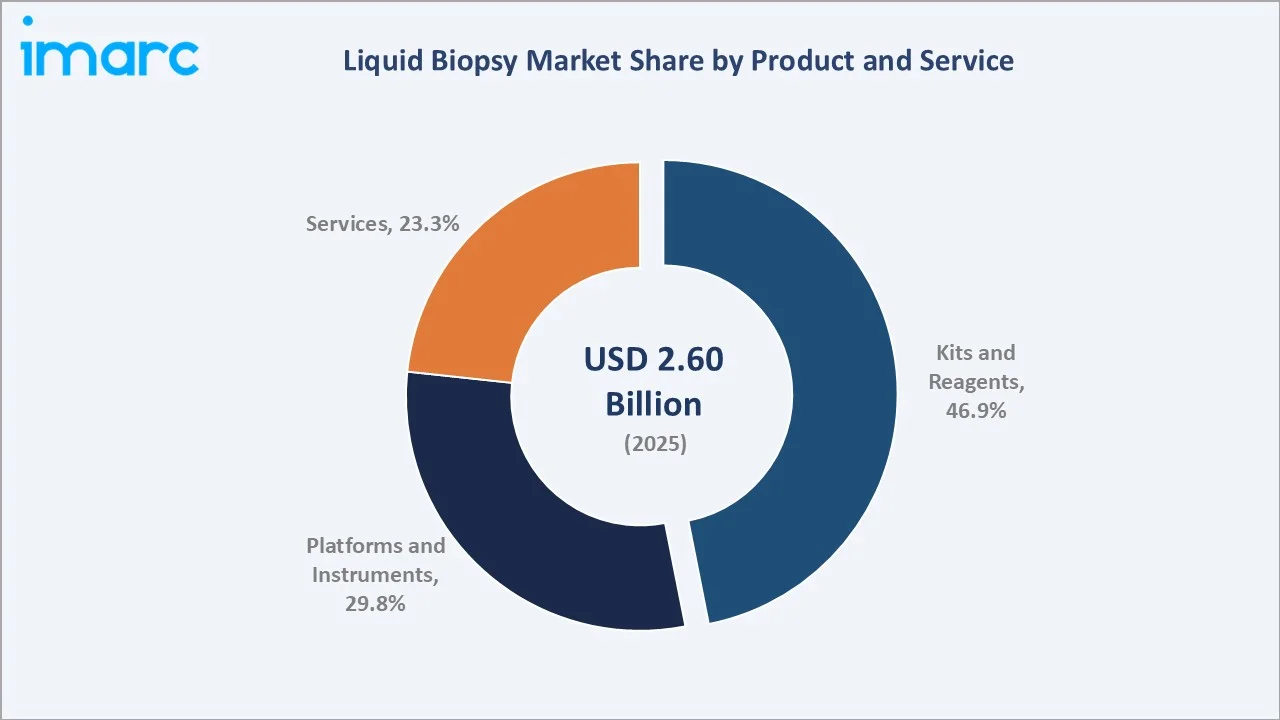

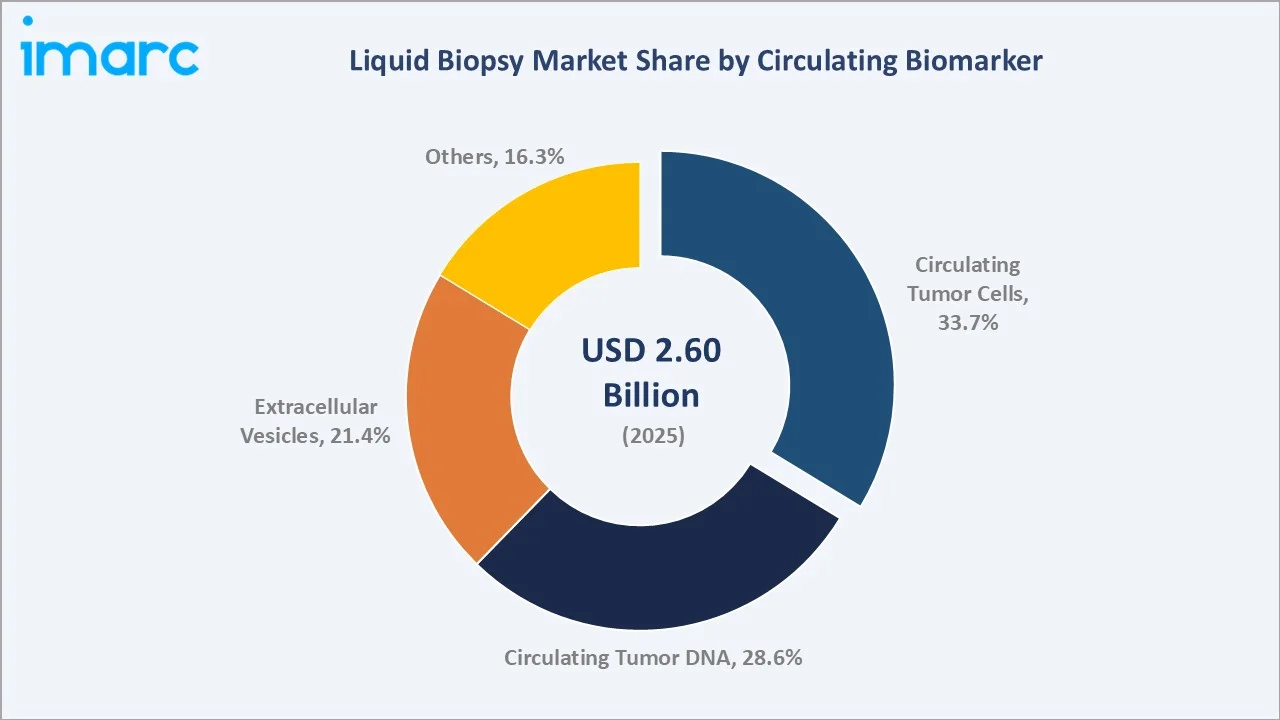

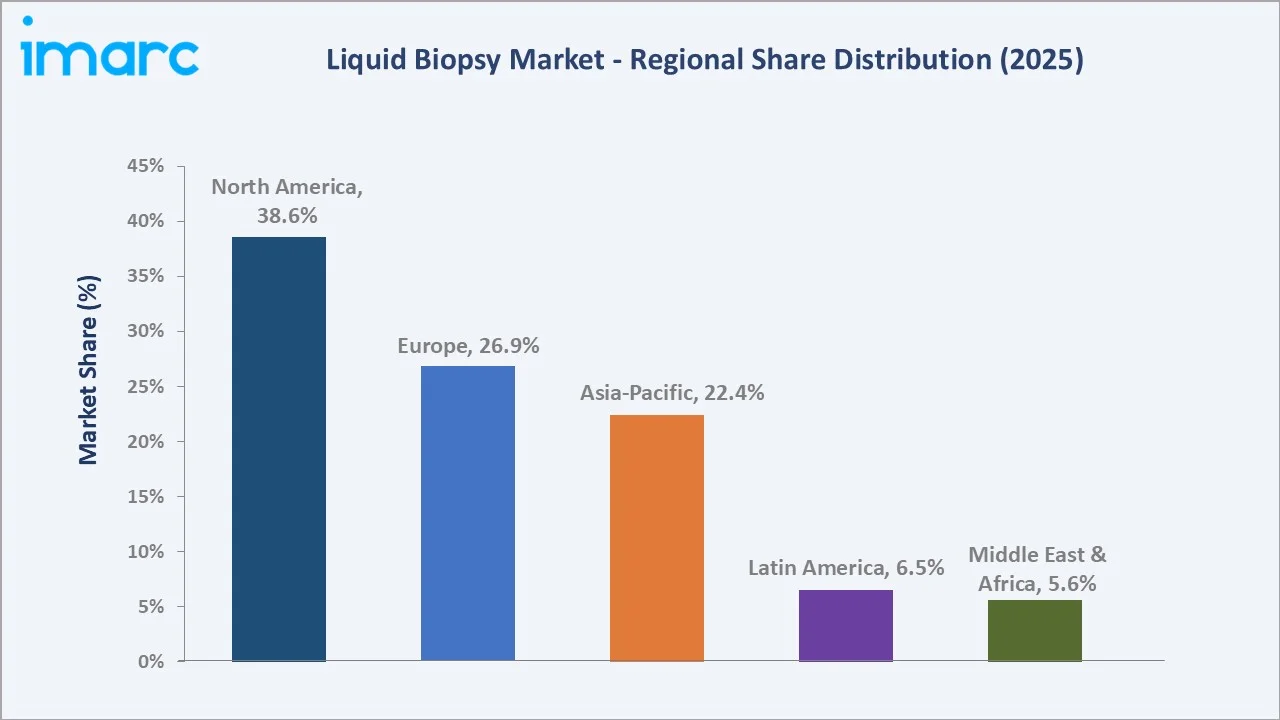

The global liquid biopsy market size was valued at USD 2.60 Billion in 2025 and is projected to reach USD 7.61 Billion by 2034, exhibiting a CAGR of 12.31% during the forecast period 2026-2034. Rising global cancer burden, rapid advances in next-generation sequencing (NGS), expanding precision oncology adoption, and growing demand for non-invasive early detection are driving the liquid biopsy market growth. Kits and Reagents lead the product segment at 46.9% in 2025, while Circulating Tumor Cells dominate the biomarker segment at 33.7%. North America accounts for 38.6% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.60 Billion |

|

Forecast Market Size (2034) |

USD 7.61 Billion |

|

CAGR (2026-2034) |

12.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.6% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~15.6%) |

|

Leading Products and Services |

Kits and Reagents (46.9%, 2025) |

|

Leading Circulating Biomarker |

Circulating Tumor Cells (33.7%, 2025) |

The liquid biopsy market's growth trajectory from 2020 through 2034 reflects consistent historical expansion and a sharply accelerating forecast curve, supported by precision oncology adoption, ctDNA reimbursement, and NGS-based multi-cancer early detection rollouts.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight Kits and Reagents and Asia-Pacific as the fastest-growing sub-categories through 2034, reflecting the expanding test adoption curve in emerging oncology markets.

Executive Summary

The liquid biopsy market is transforming rapidly, driven by precision oncology, NGS innovation, and growing clinical adoption of non-invasive diagnostics. Valued at USD 2.60 Billion in 2025, it is forecast to reach USD 7.61 Billion by 2034 at a CAGR of 12.31%. Per WHO, cancer caused nearly 10 million deaths globally in 2022, fuelling demand for earlier, less invasive detection.

Kits and Reagents lead the product segment at 46.9% in 2025, supported by recurring demand for ctDNA extraction kits and NGS library preparation. Platforms and Instruments follow at 29.8%, benefitting from rising NGS installations, while Services at 23.3% reflect growing outsourced testing by hospitals and oncology clinics.

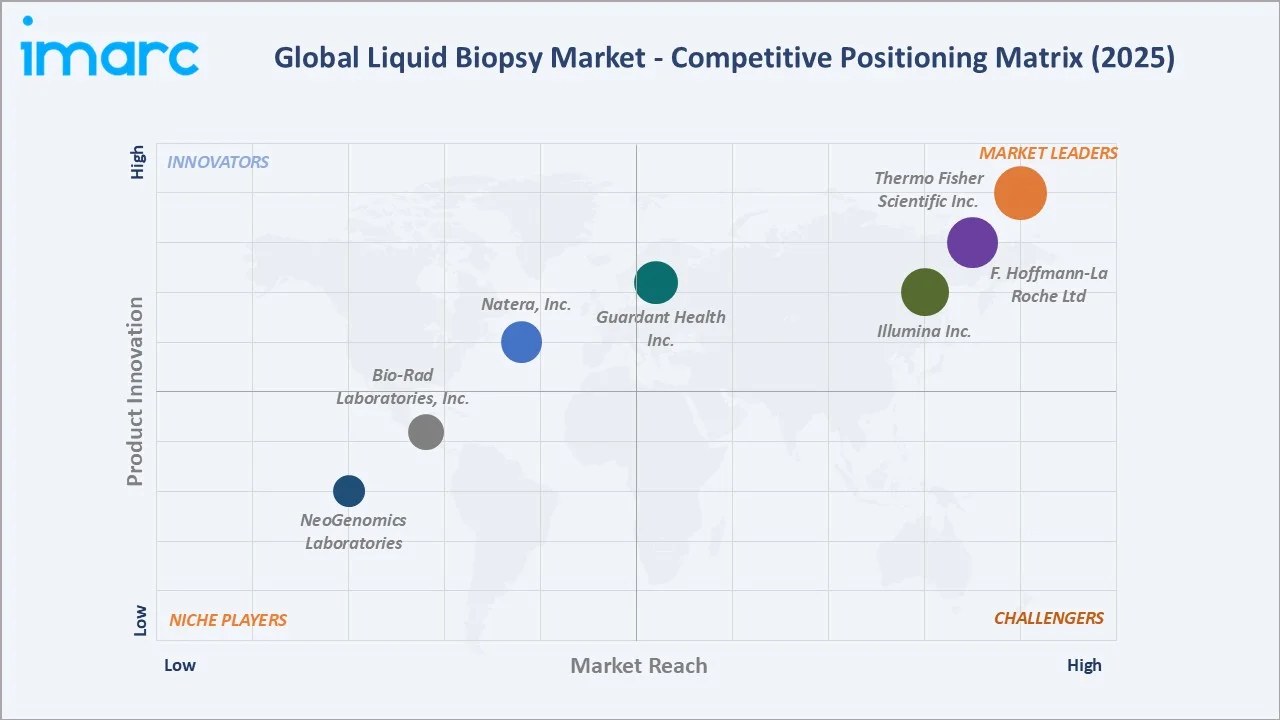

North America leads with a 38.6% global revenue share in 2025, anchored by FDA-cleared liquid biopsy approvals and broad Medicare/private payer reimbursement. Europe holds 26.9%, while Asia-Pacific, at 22.4%, is the fastest-growing region, propelled by oncology infrastructure expansion in China, Japan, and India. The competitive landscape is concentrated among F. Hoffmann-La Roche Ltd, Guardant Health Inc., Illumina Inc., and Thermo Fisher Scientific Inc.

Key Market Insights

|

Insight |

Data |

|

Largest Product and Services |

Kits and Reagents - 46.9% share (2025) |

|

Largest Circulating Biomarker Segment |

Circulating Tumor Cells - 33.7% share (2025) |

|

Leading Region |

North America - 38.6% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific - CAGR ~15.6% (2026-2034) |

|

Top Companies |

F. Hoffmann-La Roche Ltd, Guardant Health Inc., Illumina Inc., Thermo Fisher Scientific Inc., Natera, Inc. |

|

Market Opportunity |

Multi-cancer early detection and ctDNA-based MRD monitoring |

Key Analytical Observations Supporting the Above Data:

- Kits and Reagents' 46.9% dominance in 2025 reflects recurring per-test economics, with each workflow consuming USD 300-800 in cfDNA extraction and NGS library prep reagents.

- Circulating Tumor Cells lead the biomarker segment at 33.7% in 2025, supported by CellSearch FDA-approved platforms in breast, prostate, and colorectal cancer monitoring.

- North America's 38.6% share in 2025 is anchored by FDA approvals of Guardant360 CDx and Epi proColon, and broad CMS reimbursement for genomic profiling.

Global Liquid Biopsy Market Overview

Liquid biopsy is a minimally invasive diagnostic approach that analyses tumour-derived components circulating in body fluids, primarily blood, but also urine, saliva, and cerebrospinal fluid. It captures circulating tumour cells (CTCs), circulating tumour DNA (ctDNA), extracellular vesicles, and tumour-educated platelets to support cancer screening, diagnosis, companion diagnostics, and treatment monitoring.

Applications span the oncology care pathway: early screening, therapy selection, minimal residual disease detection, recurrence surveillance, and emerging uses in transplant rejection monitoring and prenatal testing. Clinical adoption is supported by regulatory clearances, payer reimbursement, and clinical guideline inclusion.

Macroeconomic enablers include the global cancer burden, which GLOBOCAN 2022 estimates at 19.97 million new cases and projects at 35 million by 2050, oncology R&D spending, and over 30,000 NGS instruments installed worldwide. Favourable reimbursement, particularly CMS coverage for comprehensive genomic profiling, further strengthens market expansion.

Market Dynamics

To evaluate market opportunities, Request Sample

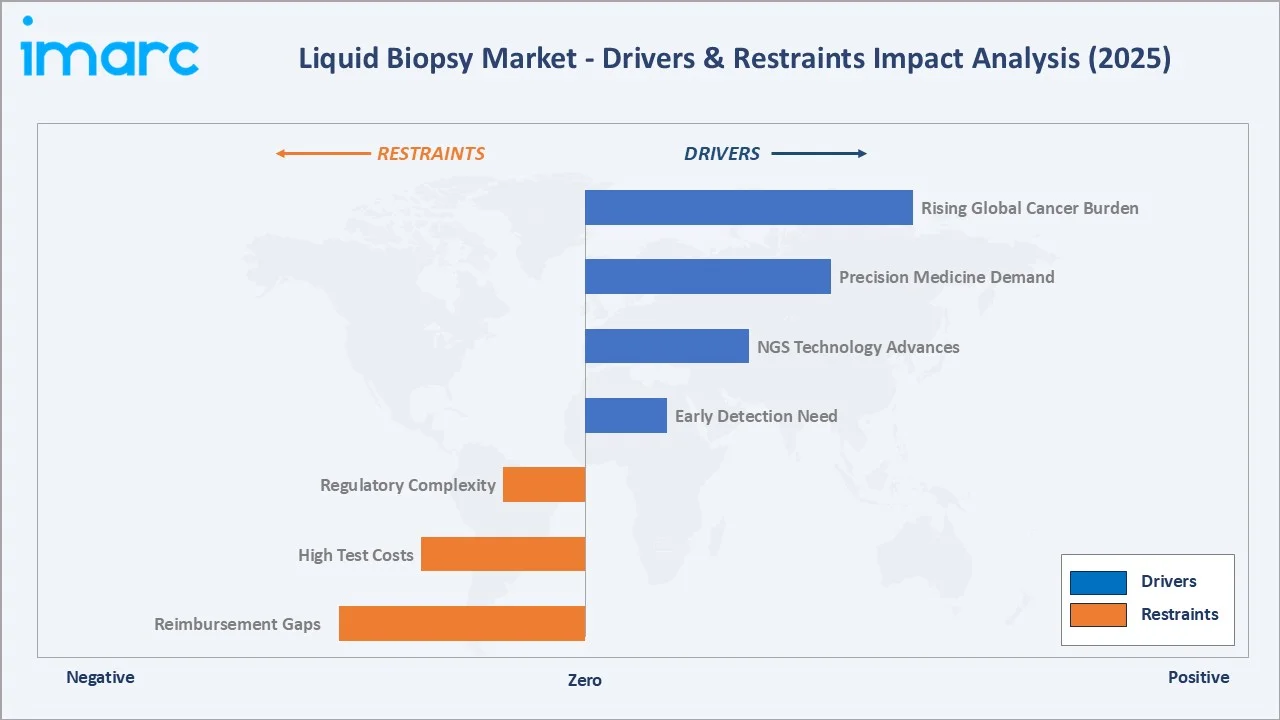

Market Drivers

- Rising Global Cancer Burden: GLOBOCAN 2022 estimated 19.97 million new cancer cases globally, with incidence projected to surpass 35 million by 2050. This structural rise directly expands the liquid biopsy's demand base.

- Precision Oncology and Companion Diagnostics: Over 100 FDA-approved targeted therapies require molecular profiling, with ~40% now accepting liquid biopsy as an alternative to tissue.

- NGS Cost Reduction: Sequencing cost dropped in consecutive years, making comprehensive genomic profiling economically viable across community oncology.

- Multi-Cancer Screening: MCED tests such as GRAIL's Galleri can detect 50+ cancer types from a single blood draw.

Market Restraints

- Reimbursement Coverage Gaps: Coverage for early detection, MRD monitoring, and non-FDA-approved indications remains inconsistent across private payers in the US and Europe.

- High Test Cost: Premium panels range from USD 3,000 to USD 5,500 per test, limiting adoption in price-sensitive emerging markets and non-reimbursed screening.

- Clinical Validation Challenges: Detecting low-fraction ctDNA in early-stage cancers remains difficult, with sensitivity often below 50% in stage I disease.

Market Opportunities

- Minimal Residual Disease Monitoring: Post-treatment ctDNA surveillance is the highest-growth application, with Signatera and NeoGenomics' RaDaR targeting a USD 1.5-2 Billion opportunity by 2030.

- Expansion Beyond Oncology: Transplant rejection monitoring, non-invasive prenatal testing, and infectious disease diagnostics leverage the same cfDNA infrastructure.

- Emerging Market Penetration: China, India, and Brazil are structurally underpenetrated, where national screening programmes create multi-billion-dollar expansion potential.

Market Challenges

- Regulatory Complexity: Navigating FDA, EMA (IVDR), NMPA, and PMDA pathways adds significant time and cost, with IVDR compliance alone adding 2-3 years of European market preparation.

- Data Standardization: Inter-laboratory variability in ctDNA quantification and variant calling remains a structural barrier to guideline integration.

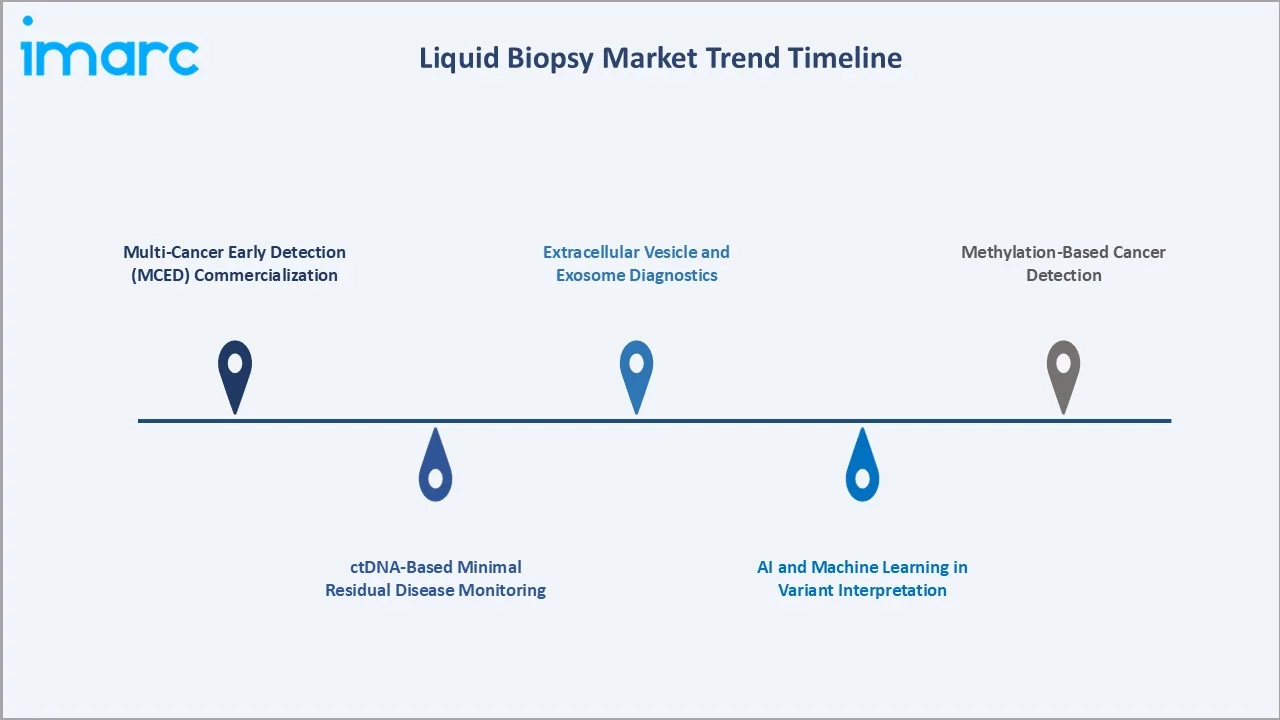

Emerging Market Trends

1. Multi-Cancer Early Detection (MCED) Commercialization

MCED tests screening 50+ cancer types from a single blood draw are moving from pilot deployments to commercial rollout. GRAIL's Galleri, Exact Sciences' Cologuard Plus, and Freenome's pipeline represent the reference footprint, with NHS England's 140,000-participant Galleri trial supporting broader adoption.

2. ctDNA-Based Minimal Residual Disease Monitoring

MRD monitoring post-surgery or chemotherapy is the fastest-growing clinical application in 2025, with Natera's Signatera, Guardant Reveal, and NeoGenomics' RaDaR competing for standard-of-care integration across adjuvant protocols.

3. AI and Machine Learning in Variant Interpretation

AI models are increasingly deployed in variant calling, fragmentomics, and methylation signature interpretation. Delfi Diagnostics' FirstLook lung cancer test leverages AI-based fragmentomics as its core differentiation.

4. Extracellular Vesicle and Exosome Diagnostics

EV-based liquid biopsy is a complementary approach to ctDNA, offering enhanced protein and RNA content. Bio-Techne, Exosome Diagnostics, and Caris lead commercial development, with ExoDx Prostate IntelliScore as the first FDA-breakthrough EV diagnostic.

5. Methylation-Based Cancer Detection

DNA methylation signature profiling, pioneered by GRAIL and Bluestar Genomics, is moving from research to commercial deployment. Methylation tests offer superior tissue-of-origin accuracy versus mutation-only panels.

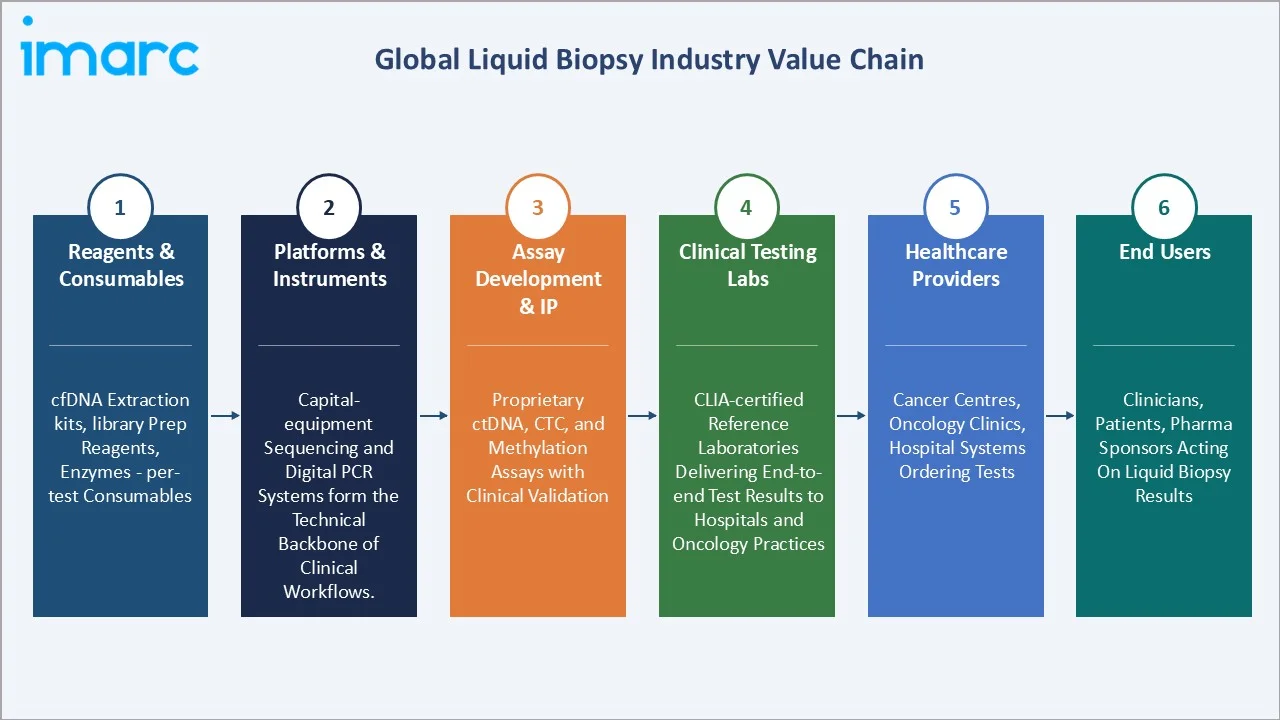

Industry Value Chain Analysis

The liquid biopsy value chain integrates reagent suppliers, instrument platforms, diagnostic laboratories, and healthcare providers into a cohesive workflow spanning sample collection through clinical report delivery. Each stage contributes a distinct margin, differentiation, and technology investment profile.

|

Stage |

Description |

|

Reagents & Consumables |

Per-test consumables - cfDNA extraction kits, library prep reagents, and enzymes - driving recurring revenue. |

|

Platforms & Instruments |

Capital-equipment sequencing and digital PCR systems form the technical backbone of clinical workflows. |

|

Assay Development & IP |

Proprietary ctDNA, CTC, and methylation assays backed by clinical validation and regulatory approvals. |

|

Clinical Testing Labs |

CLIA-certified reference laboratories delivering end-to-end test results to hospitals and oncology practices. |

|

Healthcare Providers |

Cancer centres, clinics, and hospital systems that order tests and integrate results into cancer care. |

|

End Users |

Clinicians, patients, and pharma trial sponsors receiving, acting on, or funding liquid biopsy output. |

Assay developers occupy the highest-value position by integrating IP-protected bioinformatics, clinical validation, and regulatory clearances into defensible platforms. However, they face margin pressure from instrument vendors commoditizing workflow costs and from vertically integrated labs internalising assay development.

Technology Landscape in the Liquid Biopsy Industry

Next-Generation Sequencing (NGS) Platforms

NGS is the backbone of liquid biopsy, with Illumina commanding over 70% installed base share in 2025 via NovaSeq X, NextSeq 2000, and MiSeq. Thermo Fisher's Ion Torrent serves targeted panel workflows, while Element Biosciences and PacBio add alternative chemistries.

Digital PCR and Droplet-Based Detection

Bio-Rad's QX600 Droplet Digital PCR and Thermo Fisher's QuantStudio Absolute Q are reference platforms for sensitive ctDNA mutation detection below 0.01% allele frequency, ideal for MRD applications.

Methylation and Fragmentomics

Methylation profiling using bisulfite conversion or enzymatic methyl sequencing enables multi-cancer detection via signature patterns. Fragmentomics is an emerging AI-driven approach pioneered by Delfi Diagnostics.

AI-Driven Bioinformatics

Machine learning is standard in variant calling, noise filtering, and tissue-of-origin prediction. Tempus Labs, Caris, and GRAIL deploy proprietary AI pipelines integrating genomic, methylomic, and clinical outcomes data.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product and Service | Kits and Reagents | 46.9% | 2025 |

| Circulating Biomarker | Circulating Tumor Cells | 33.7% | 2025 |

| Cancer Type | Lung Cancer | 🔒 | 2025 |

| End User | Hospitals and Laboratories | 🔒 | 2025 |

| Region | North America | 38.6% | 2025 |

By Product and Service

Kits and Reagents command a 46.9% majority share in 2025, supported by the recurring per-test consumable economics of liquid biopsy workflows. Every clinical test consumes USD 300-800 in extraction kits, library preparation reagents, and enzymes, creating a revenue base that grows in lockstep with test volume. QIAGEN, Thermo Fisher, and Roche lead this segment.

To access detailed market analysis, Request Sample

Platforms and Instruments at 29.8% in 2025 represent the capital-equipment layer, dominated by Illumina's NovaSeq and NextSeq. Services at 23.3% capture outsourced clinical testing volume handled by specialty labs such as Guardant Health, Natera, and NeoGenomics.

By Circulating Biomarker

Circulating Tumor Cells (CTCs) dominate at 33.7% in 2025, benefitting from established FDA-cleared platforms such as Menarini Silicon Biosystems' CellSearch for breast, prostate, and colorectal cancer monitoring. The segment reflects over two decades of clinical validation.

Circulating Tumor DNA at 28.6% in 2025 is the fastest-growing biomarker at ~14.2% CAGR, propelled by ctDNA-based MRD and comprehensive genomic profiling. Extracellular Vesicles at 21.4% are gaining traction in prostate, pancreatic, and lung cancer. Others (16.3%) include tumour-educated platelets, circulating RNA, and cell-free proteins.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.6% |

FDA-cleared tests, CMS reimbursement, Guardant/GRAIL leadership, precision oncology |

|

Europe |

26.9% |

IVDR framework, NHS MCED rollout, EORTC adoption, Roche/QIAGEN base |

|

Asia-Pacific |

22.4% |

China NMPA approvals, Japan PMDA reimbursement, India oncology expansion |

|

Latin America |

6.5% |

Brazil/Mexico oncology infrastructure, private hospital adoption |

|

Middle East & Africa |

5.6% |

GCC precision medicine, Saudi Vision 2030, South Africa growth |

North America commands a 38.6% global revenue share in 2025, the most dominant regional position in the global liquid biopsy market. The United States is the anchor, supported by FDA approvals for Guardant360 CDx, FoundationOne Liquid CDx, Epi proColon, and GRAIL's Galleri. CMS National Coverage Determination provides universal Medicare reimbursement for eligible advanced cancer patients.

Europe holds 26.9% in 2025, with the IVDR framework providing harmonised approval pathways across the EU-27. Germany, France, and the UK account for roughly 65% of European demand.

Asia-Pacific at 22.4% in 2025 is the fastest-growing region at ~15.6% CAGR, propelled by China's NMPA approvals for domestic products from BGI Genomics, Burning Rock, and Genetron Health. Japan's Precision Medicine Initiative and India's Ayushman Bharat oncology expansion add further growth vectors.

Competitive Landscape

|

Company Name |

Key Platform / Offerings |

Market Position |

Core Strength |

|

F. Hoffmann-La Roche Ltd |

AVENIO ctDNA Analysis Kits V2 |

Leader |

Pharma synergy, global reach, companion diagnostics |

|

Guardant Health Inc. |

Guardant360 CDx |

Challenger |

ctDNA profiling, MRD, FDA-cleared MCED |

|

Illumina Inc. |

NovaSeq 6000 System |

Leader |

NGS platform dominance, TSO 500 ctDNA |

|

Thermo Fisher Scientific Inc. |

MagMAX |

Leader |

Targeted NGS panels, lab automation, global footprint |

|

Natera, Inc. |

Constellation |

Challenger |

MRD monitoring, personalised ctDNA |

|

Bio-Rad Laboratories, Inc. |

QX200 Droplet Digital PCR System |

Emerging |

Sensitive MRD detection, research, and clinical ddPCR |

|

NeoGenomics Laboratories |

NEO PanTracer LBx |

Emerging |

Reference lab services, MRD, oncology CLIA |

The competitive landscape features diversified global leaders (Roche, Illumina, QIAGEN, Thermo Fisher) with broad reagent, platform, and assay portfolios, alongside focused pure-play innovators (Guardant Health, Natera, GRAIL) specialising in clinical-grade ctDNA applications and MRD monitoring.

Key Company Profiles

F. Hoffmann-La Roche Ltd

Roche is the global leader in in-vitro diagnostics, combining a broad liquid biopsy portfolio spanning ctDNA assays, companion diagnostics, and integrated pharma-diagnostic co-development through Genentech. The 2018-closed Foundation Medicine acquisition anchors its comprehensive genomic profiling leadership.

- Product & Platform Portfolio: AVENIO ctDNA Analysis Kits, cobas EGFR Mutation Test, FoundationOne Liquid CDx.

- Recent Developments: In September 2023, Roche France, Foundation Medicine, Inc., and the Institut Gustave Roussy announced a unique partnership to establish in-house liquid biopsy testing at the Institut Gustave Roussy’s facilities in France, by transferring technology from Foundation Medicine’s FoundationOne®Liquid CDx, a blood-based comprehensive genomic profiling (CGP) test.

- Strategic Focus: Leveraging the Roche-Genentech-Foundation Medicine value chain to pair companion diagnostics with targeted therapies, expand AVENIO in decentralised hospital labs, and grow ctDNA-based MRD services globally.

Guardant Health, Inc.

Guardant Health is the pure-play leader in ctDNA comprehensive genomic profiling. Guardant360 CDx is a reference FDA-approved companion diagnostic for advanced solid tumours. The company operates a fully integrated CLIA-certified laboratory model with direct oncologist engagement.

- Product & Platform Portfolio: Guardant360 CDx, Guardant360 TissueNext, Guardant Reveal (MRD), Shield (colorectal cancer screening).

- Recent Developments: In July 2024, the FDA approved Guardant Health's Shield blood test for primary colorectal cancer screening in average-risk adults aged 45 and older, expanding the addressable market beyond advanced cancer into population screening.

- Strategic Focus: Expanding Shield for broad colorectal screening reimbursement, scaling Reveal for MRD monitoring across solid tumour indications, and growing pharma collaboration revenue through companion diagnostic partnerships.

Illumina, Inc.

Illumina commands over 70% of the global NGS installed base in 2025 and is the dominant sequencing platform provider for liquid biopsy. Beyond instruments, Illumina develops its own liquid biopsy assays through the TruSight Oncology (TSO) portfolio.

- Product & Platform Portfolio: NovaSeq X, NextSeq 2000, MiSeq, TruSight Oncology 500 ctDNA, TruSight Oncology Comprehensive.

- Recent Developments: In November 2024, Illumina, Inc. announced that it will release TruSight Oncology 500 v2 (TSO 500 v2), a new version of its flagship cancer research assay to enable comprehensive genomic profiling (CGP). The assay is currently under development, with global release planned for mid-2025.

- Strategic Focus: Consolidating NGS platform dominance via NovaSeq X volume expansion, growing the TSO 500 ctDNA footprint in distributed clinical testing, and enabling third-party assay developers through integrated workflow solutions.

Market Concentration Analysis

The global liquid biopsy market is moderately concentrated, with the top 5 players (Roche, Guardant Health, Illumina, QIAGEN, Thermo Fisher) accounting for approximately 42-48% of global revenue in 2025. The remainder is distributed across specialised diagnostic developers (Natera, NeoGenomics, GRAIL) and regional champions.

The market has a bifurcated structure: established reagent and platform giants leverage broad infrastructure scale, while pure-play innovators compete on assay sensitivity, clinical validation depth, and oncology specialty focus. Consolidation trends include Roche's Foundation Medicine integration, Illumina's GRAIL divestiture, and ongoing M&A among mid-tier laboratory service providers.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia-Pacific liquid biopsy services grow at ~15.6% CAGR through 2034, the fastest regional path, driven by China's oncology infrastructure expansion and Japan's precision medicine reimbursement. Kits and Reagents grow at ~13.5% CAGR, while ctDNA biomarker assays grow at ~14.2% CAGR.

Emerging Market Expansion

Multi-cancer early detection is the largest single opportunity, targeting a USD 2+ Billion addressable market by 2030. ctDNA-based MRD monitoring is the second-largest opportunity at USD 1.5-2 Billion by 2030.

Venture and Private Investment Trends

Cumulative venture and growth equity investment in liquid biopsy exceeded USD 12 Billion between 2020 and 2025 per PitchBook data, with notable transactions including GRAIL's separation from Illumina, Natera's Signatera financing, and Asia-Pacific rounds in BGI Genomics, Burning Rock, and Singlera Genomics.

Future Market Outlook (2026-2034)

The global liquid biopsy market forecast projects expansion from USD 2.60 Billion in 2025 to USD 7.61 Billion by 2034 at a CAGR of 12.31%, a near-tripling of market value supported by multi-cancer early detection commercialization, MRD standard-of-care integration, and Asia-Pacific regional penetration.

Three structural shifts will reshape the industry through 2034. First, multi-cancer early detection will transition from pilot programmes to reimbursed population-scale deployment. Second, ctDNA-based MRD monitoring will become standard-of-care post-surgical decision support across colorectal, breast, and lung adjuvant protocols.

Third, AI-driven bioinformatics and methylation/fragmentomics will enable next-generation multi-modal liquid biopsy platforms combining mutation, methylation, protein, and fragment-size signatures into unified diagnostic outputs. By 2034, liquid biopsy is forecast to complete its transition from specialised companion diagnostics into a mainstream pillar of global cancer care infrastructure.

Research Methodology

Primary Research

Primary research included over 55 structured interviews in 2024-2025 with senior executives at Tier-1 diagnostic developers, oncology clinical directors at major US and European cancer centres, reference laboratory directors, payer policy specialists, and institutional investors. Primary insights validated market sizing, segmentation breakdowns, adoption timelines, and competitive positioning.

Secondary Research

Secondary sources include IARC GLOBOCAN 2022 cancer statistics, WHO burden reports, US FDA device approval databases, CMS coverage determinations, EMA/IVDR publications, NMPA approvals, company annual reports, and trade publications, including GenomeWeb and 360Dx.

Forecasting Models

Market size estimates and growth projections were derived using a blended top-down and bottom-up forecasting approach, incorporating cancer incidence projections, test adoption curves, pricing evolution, and reimbursement modelling. Base, optimistic, and conservative scenarios were developed to reflect regulatory and reimbursement uncertainty.

Liquid Biopsy Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product and Services Covered | Kits and Reagents, Platforms and Instruments, Services |

| Circulating Biomarker Covered | Circulating Tumor Cells, Extracellular Vesicles, Circulating Tumor DNA, Others |

| Cancer Types Covered | Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Liver Cancer, Others |

| End Users Covered | Hospitals and Laboratories, Academic and Research Centers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | F. Hoffmann-La Roche Ltd, Guardant Health Inc., Illumina Inc., Thermo Fisher Scientific Inc., Natera, Inc., Bio-Rad Laboratories, Inc., NeoGenomics Laboratories, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the liquid biopsy market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global liquid biopsy market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the liquid biopsy industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Liquid Biopsy Market Report

The global liquid biopsy market was valued at USD 2.60 Billion in 2025, driven by rising cancer incidence, NGS cost reductions, and precision oncology adoption globally.

The market is projected to reach USD 7.61 Billion by 2034, growing at 12.31% CAGR from 2026 to 2034, powered by MCED commercialization and MRD monitoring expansion.

Kits and Reagents lead with a 46.9% share in 2025, driven by recurring per-test consumable economics and rising global test volume across oncology workflows.

Circulating Tumor Cells dominate at 33.7% share in 2025, reflecting established FDA-cleared CellSearch platforms and deep clinical validation across multiple cancers.

North America leads with a 38.6% share in 2025, anchored by FDA-cleared tests, CMS reimbursement, and leadership of Guardant Health, GRAIL, and Foundation Medicine.

Key drivers include rising global cancer burden, NGS cost decline, precision oncology adoption, MRD monitoring, and multi-cancer early detection deployment.

Asia-Pacific is the fastest-growing region at ~15.6% CAGR through 2034, led by China NMPA approvals, Japan PMDA reimbursement, and India's oncology infrastructure.

Leading companies include F. Hoffmann-La Roche Ltd, Guardant Health Inc., Illumina Inc., Thermo Fisher Scientific Inc., Natera, Inc., Bio-Rad Laboratories, Inc., and NeoGenomics Laboratories.

MRD monitoring uses ctDNA to detect residual cancer cells post-treatment. Signatera and Guardant Reveal support for adjuvant therapy decisions across solid tumours.

Liquid biopsy is minimally invasive, uses blood, enables repeat sampling, and captures tumour heterogeneity, whereas tissue biopsy requires surgery and samples only one location.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)