Location Analytics Market Size, Share, Trends and Forecast by Component, Deployment Mode, Location Type, Application, End Use Industry, and Region, 2026-2034

Location Analytics Market Size and Share:

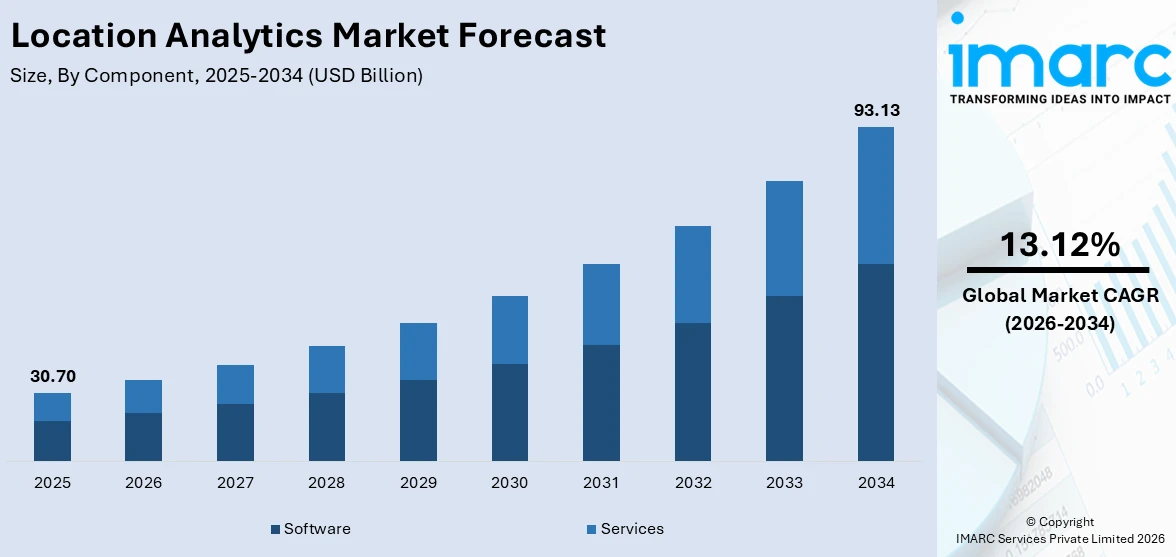

The global location analytics market size was valued at USD 30.70 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 93.13 Billion by 2034, exhibiting a CAGR of 13.12% from 2026-2034. North America currently dominates the market, holding a market share of 30% in 2025. The region benefits from advanced digital infrastructure, early adoption of geospatial technologies, strong presence of leading technology providers, and widespread integration of location-based solutions across retail, logistics, and healthcare sectors, all contributing to the location analytics market share.

The rising proliferation of Internet of Things (IoT) devices and connected sensors is generating massive volumes of spatial data, which is propelling the demand for advanced location analytics platforms capable of processing and interpreting geospatial information in real time. Moreover, the growing emphasis on enhancing customer experiences through personalized and context-aware engagement strategies is encouraging enterprises to leverage location intelligence for targeted marketing, optimized store layouts, and improved service delivery. Furthermore, the increasing need for real-time supply chain visibility and fleet management optimization is driving organizations across transportation, logistics, and manufacturing sectors to invest in location-based analytical solutions, fueling the location analytics market growth.

The United States has emerged as a major region in the location analytics market owing to many factors. The country benefits from a highly developed technology ecosystem characterized by robust digital infrastructure, widespread smartphone penetration, and extensive wireless network coverage that supports seamless location data collection and analysis. In February 2026, Palantir Technologies secured a five‑year, up to $1 billion contract with the U.S. Department of Homeland Security to expand use of its advanced AI and data analytics platforms across federal agencies, strengthening its geospatial and situational analytics footprint. The strong presence of major technology corporations and innovative startups specializing in geospatial intelligence and spatial analytics is accelerating product development and driving competitive advancements in the region.

To get more information on this market Request Sample

Location Analytics Market Trends:

Growing Integration of Artificial Intelligence

The increasing integration of artificial intelligence (AI) and machine learning (ML) capabilities into location analytics platforms is transforming how organizations derive actionable insights from spatial data. Advanced AI algorithms enable automated pattern recognition, predictive modeling, and anomaly detection within geospatial datasets, allowing businesses to anticipate consumer behavior, optimize delivery routes, and identify emerging demand hotspots with unprecedented accuracy. In January 2026, the geospatial technology firm SkyFi raised $12.7 million in a Series A funding round to expand its satellite imagery and analytics platform, reflecting broader investor confidence in AI‑driven spatial data solutions across industries. ML models continuously improve their analytical precision by processing historical location data alongside real-time inputs, creating increasingly sophisticated spatial intelligence that adapts to changing market conditions.

Expansion of Indoor Positioning Technologies

The rapid advancement of indoor positioning technologies, including Bluetooth Low Energy (BLE) beacons, ultra-wideband (UWB) sensors, and Wi-Fi-based triangulation systems, is significantly expanding the scope and application of location analytics beyond traditional outdoor environments. These technologies enable precise tracking and analysis of movement patterns within enclosed spaces such as shopping malls, airports, hospitals, and warehouses, providing organizations with granular insights into foot traffic, dwell times, and occupancy levels. In November 2025, the Italian indoor positioning firm Nextome was again recognized as a global leader in indoor positioning and navigation technologies, highlighting continued innovation and adoption of BLE, UWB, and Wi‑Fi hybrid solutions across industries. The continued miniaturization of positioning hardware and declining sensor costs are making indoor location analytics economically viable for medium-scale deployments, strengthening the location analytics market outlook.

Rising Demand for Geospatial Privacy Solutions

The escalating regulatory focus on data privacy and consumer protection is driving significant demand for privacy-compliant location analytics solutions that balance analytical capabilities with stringent data governance requirements. Regulations governing the collection, storage, and processing of personal location data are compelling organizations to adopt anonymization techniques, differential privacy frameworks, and consent management systems within their spatial analytics workflows. In January 2026, Consumer Reports proposed a model State Location Privacy Act restricting collection and commercial sale of precise geolocation data, gaining endorsements from privacy groups and influencing U.S. state regulations. Additionally, the emergence of federated learning approaches that enable collaborative spatial analysis without centralizing sensitive location data is gaining traction across healthcare and financial services sectors, where data sensitivity is paramount, reflecting evolving location analytics market trends.

Location Analytics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global location analytics market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on component, deployment mode, location type, application, and end use industry.

Analysis by Component:

- Software

- Services

Software holds 55% of the market share, encompassing geospatial platforms, geographic information systems, spatial data visualization tools, and real-time mapping applications that enable organizations to collect, process, and interpret location-based data. The dominance of the software segment is driven by the increasing enterprise demand for scalable analytical platforms that integrate seamlessly with existing business intelligence infrastructure and customer relationship management systems. As per sources, California-based startup Felt raised $15 million to expand its AI-driven geospatial mapping platform, adopted by insurers, emergency responders, and energy companies for custom location analytics. Organizations across diverse industries are prioritizing software investments to harness spatial data for strategic decision-making, including site selection, market penetration analysis, and competitive benchmarking. The growing availability of cloud-native software solutions is lowering implementation complexity and enabling rapid deployment, which is particularly attractive to small and mid-sized enterprises seeking cost-effective access to advanced geospatial capabilities.

Analysis by Deployment Mode:

- On-premises

- Cloud-based

Cloud-based currently leads the market with a share of 60%, due to the inherent advantages of cloud-based solutions over traditional on-premises solutions. Cloud-based solutions allow organizations to process large amounts of geospatial data without having to invest a substantial amount of capital in hardware infrastructure, making advanced spatial analytics more accessible to organizations of all sizes. The cloud-based pricing model also eliminates financial constraints and allows organizations to scale their analytical capabilities in line with their business needs. Cloud-based solutions also make it easy to integrate with other third-party sources, application programming interfaces, and enterprise software ecosystems, making the overall utility of location analytics more accessible across various operational workflows. The ability to access analytical dashboards and spatial visualizations from any device also supports collaboration between a distributed workforce and enables real-time decision-making across geographically dispersed teams, thus supporting the location analytics market forecast.

Analysis by Location Type:

- Indoor

- Outdoor

Outdoor leads the market, with a share of 65%, utilizing the capabilities of global positioning system (GPS) technology, satellite imagery, cellular network triangulation, and geographic information system platforms to monitor, analyze, and interpret geospatial data in open outdoor settings. The leading market position of outdoor location analytics is supported by its widespread use in fleet management, logistics analysis, urban planning, transportation network analysis, and agricultural land monitoring, where accurate geospatial intelligence is critical to operational efficiency. Retail businesses apply outdoor location data to analyze consumer movement patterns, assess new store locations, and optimize delivery routes in large geographic areas. The rising use of autonomous vehicles and drone delivery services is also fueling the need for high-accuracy outdoor positioning and geospatial analytics capabilities. Furthermore, government organizations and local administrations are increasingly applying outdoor location analytics to infrastructure development, environmental monitoring, and emergency response coordination, expanding the use cases and maintaining strong market performance in this segment.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Remote Monitoring

- Sales and Marketing Optimization

- Asset Management

- Risk Management

- Facility Management

- Others

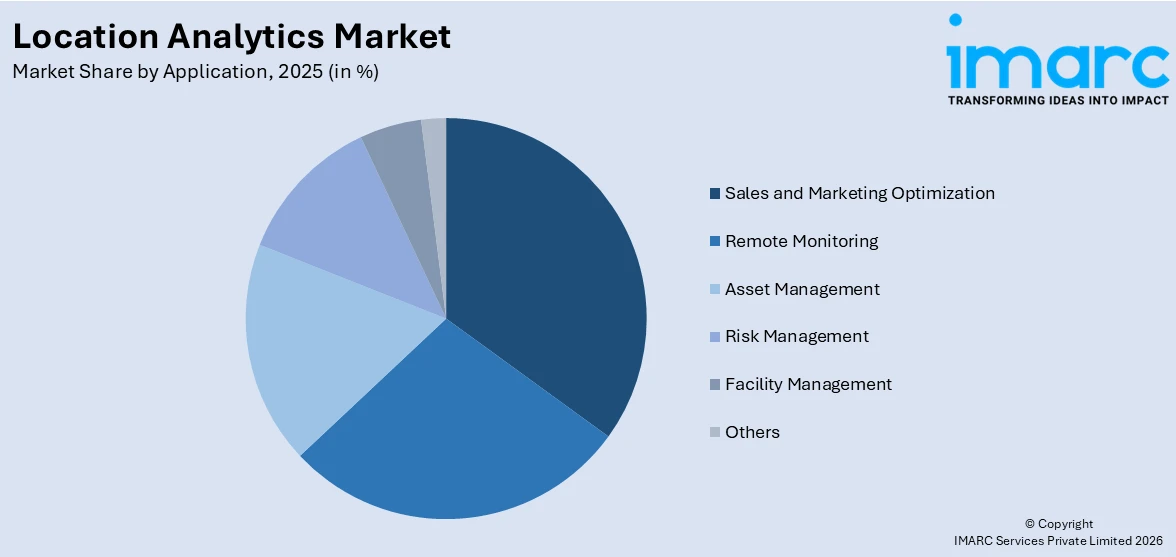

Sales and marketing optimization is the leading segment, with a market share of 20%. Location analytics is a crucial component that helps improve sales and marketing strategies by providing organizations with detailed location-based insights into consumer demographics, foot traffic, competitor proximity, and regional purchasing behaviors. Organizations use geospatial intelligence to discover high-value market locations, optimize advertising expenditures across geographic locations, and design marketing campaigns according to localized consumer preferences and seasonal variations in demand. The combination of location intelligence with customer relationship management solutions helps organizations personalize marketing communications in real-time, resulting in improved engagement and conversion results. Retailers and quick-service restaurants use geofencing solutions fueled by location analytics to send proximity-based offers and notifications that grab consumers' attention at strategic points of decision-making. The growing trend of adopting omnichannel marketing approaches is further fueling the demand for location intelligence solutions that connect offline and online consumer interactions, helping organizations create a unified brand experience.

Analysis by End Use Industry:

- BFSI

- Healthcare

- Hospitality

- Government

- Transport and Logistic

- IT and Telecom

- Retail and Consumer Goods

- Media and Entertainment

- Others

Retail and consumer goods account for 18% market share, thanks to the prime importance of spatial intelligence in optimizing retail store operations, understanding consumer shopping behavior, and improving customer engagement strategies. Retailers use location analytics solutions to analyze foot traffic patterns, calculate dwell time, assess the effectiveness of store layouts, and determine the effect of promotional activities on the conversion rate of in-store customers. The rising trend of experiential retail and personalized shopping experiences is forcing retailers to adopt sophisticated geospatial solutions that offer real-time insights into customer movements and preferences in physical stores. Additionally, consumer product companies use location intelligence to optimize distribution networks, territory planning, and demand forecasting at a detailed geographic level. The rising integration of online and offline retail channels is also fueling the adoption of location intelligence, as companies are looking for integrated spatial insights that link online engagement metrics with offline store performance metrics to inform comprehensive business strategies.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, contributing 30% to the market share, retaining the leading market position. The dominance of the North America market is due to the region’s well-developed technological foundation, high adoption rates of enterprise technology, and the prominent presence of leading location analytics solution vendors that are driving innovation and development. Organizations in the North American market, including retail, healthcare, logistics, and financial services, are early adopters of geospatial intelligence solutions, leveraging location data to enhance operations, customer experience, and strategic planning. The well-developed digital advertising market in the region is also fueling the demand for location-based marketing analytics solutions that provide tangible return on investment. Moreover, the increasing adoption of smart city projects and intelligent transportation systems in major cities is also driving a significant demand for sophisticated spatial analytics solutions. The region’s favorable regulatory framework for technology adoption and access to qualified data science talent is also solidifying the region’s position as the leading location analytics innovator and adopter worldwide.

Key Regional Takeaways:

United States Location Analytics Market Analysis

The United States represents the most significant national market for location analytics, driven by a highly developed technology ecosystem and widespread enterprise adoption of data-driven decision-making practices. The country's robust digital infrastructure, including extensive broadband connectivity, advanced cellular networks, and high smartphone penetration rates, provides a strong foundation for location data collection and analysis at scale. Enterprises across the retail, healthcare, financial services, and logistics sectors are increasingly leveraging location analytics to optimize store performance, personalize customer engagement, improve supply chain efficiency, and enhance risk management capabilities. The thriving e-commerce landscape is further fueling demand for location intelligence solutions that bridge online and offline consumer behaviors, enabling unified commerce strategies. Additionally, the growing emphasis on smart city development and intelligent transportation systems across major urban centers is creating significant opportunities for location analytics providers to deliver advanced spatial insights for urban planning and mobility optimization. The strong venture capital investment ecosystem supports continuous innovation in geospatial technology startups, ensuring a steady pipeline of advanced location analytics solutions entering the market and addressing evolving enterprise requirements.

Europe Location Analytics Market Analysis

Europe represents a significant and rapidly evolving market for location analytics, characterized by strong regulatory frameworks governing data privacy that are shaping the development of privacy-compliant geospatial solutions across the region. The general data protection Regulation has established stringent requirements for location data handling, compelling solution providers to develop innovative anonymization and consent management capabilities that balance analytical utility with individual privacy protection. European enterprises in the retail, automotive, logistics, and tourism sectors are actively adopting location analytics to enhance operational efficiency, optimize distribution networks, and deliver personalized customer experiences tailored to regional consumer preferences. The growing momentum behind smart city initiatives in major European metropolitan areas, particularly in Germany, the United Kingdom, France, and the Nordic countries, is driving substantial investment in spatial analytics platforms for urban planning, traffic management, and public service delivery. Furthermore, the expanding adoption of connected vehicle technologies and autonomous driving platforms across the European automotive industry is creating new demand for high-precision location intelligence solutions.

Asia-Pacific Location Analytics Market Analysis

The Asia-Pacific region is emerging as the fastest-growing market for location analytics, propelled by rapid digital transformation across developing economies, increasing smartphone penetration, and expanding mobile internet connectivity. China, Japan, India, South Korea, and Australia represent key growth markets where enterprises are investing heavily in geospatial intelligence capabilities to support urbanization planning, retail expansion, and logistics optimization. In October 2025, Grab partnered with May Mobility to deploy autonomous vehicles in Southeast Asia, leveraging GrabMaps for precise navigation, fleet management, and location-based analytics across eight countries. The region's dynamic e-commerce landscape, characterized by high mobile commerce adoption and innovative delivery models, is creating substantial demand for location-based analytical tools that optimize last-mile delivery operations and enhance consumer targeting precision. Government investments in smart city infrastructure and digital public services across multiple Asian economies are further driving adoption.

Latin America Location Analytics Market Analysis

Latin America is witnessing growing adoption of location analytics solutions, driven by expanding digital infrastructure, increasing mobile connectivity, and the rising emphasis on data-driven business strategies across key economies including Brazil and Mexico. The region's rapidly growing retail and e-commerce sectors are creating demand for spatial intelligence tools that support market expansion planning, store site selection, and consumer behavior analysis. Additionally, government initiatives aimed at modernizing transportation networks and developing smart urban infrastructure are generating opportunities for location analytics deployment in public sector applications. The increasing penetration of cloud computing services is lowering adoption barriers for regional enterprises seeking cost-effective geospatial analytical capabilities.

Middle East and Africa Location Analytics Market Analysis

The Middle East and Africa region is experiencing gradual yet steady growth in location analytics adoption, supported by ambitious smart city development programs, expanding telecommunications infrastructure, and increasing government investments in digital transformation. Major urban development projects across the Gulf Cooperation Council nations are driving demand for advanced spatial analytics in urban planning, transportation management, and tourism optimization. The growing retail modernization across the region is further encouraging location intelligence adoption for store performance analysis and consumer engagement enhancement. Additionally, the expanding mobile subscriber base and improving internet connectivity across African markets are creating new opportunities for location analytics providers to address emerging enterprise and public sector analytical requirements.

Competitive Landscape:

The global location analytics market exhibits a moderately consolidated competitive structure characterized by the presence of established technology corporations alongside specialized geospatial analytics providers. Leading market participants are actively pursuing strategies centered on product innovation, strategic partnerships, and geographic expansion to strengthen their competitive positioning. Companies are investing significantly in integrating artificial intelligence and machine learning capabilities into their location analytics platforms to deliver more sophisticated predictive and prescriptive spatial insights. Strategic acquisitions of niche geospatial technology firms are enabling major players to expand their solution portfolios and access specialized capabilities in indoor positioning, privacy-compliant analytics, and real-time spatial processing.

The report provides a comprehensive analysis of the competitive landscape in the location analytics market with detailed profiles of all major companies, including:

- Cisco Spaces

- Esri

- Galigeo

- GeoMoby

- Google LLC

- HERE Technologies

- INRIX, Inc

- Lepton Software

- Precisely

- SAP SE

- SAS Institute Inc.

- TomTom International BV.

Latest News and Developments:

- In December 2025, Esri India launched Bharat ENVI, an integrated satellite analytics software enabling advanced geospatial decision-making, image processing, and planning support for government and enterprise users, enhancing spatial intelligence applications across urban development, disaster management, and resource optimization in India.

- In September 2024, Esri India unveiled Indo ArcGIS Business Analyst, a location analytics solution for government organizations, enabling data-driven decisions using spatial and demographic insights to optimize resource distribution, public safety, urban planning, and socio-economic development. This launch strengthens geospatial intelligence adoption across Indian government departments.

Location Analytics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Software, Services |

| Deployment Modes Covered | On-premises, Cloud-based |

| Location Types Covered | Indoor, Outdoor |

| Applications Covered | Remote Monitoring, Sales and Marketing Optimization, Asset Management, Risk Management, Facility Management, Others |

| End Use Industries Covered | BFSI, Healthcare, Hospitality, Government, Transport and Logistic, IT And Telecom, Retail and Consumer Goods, Media and Entertainment, Others |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Cisco Spaces, Esri, Galigeo, GeoMoby, Google LLC, HERE Technologies, INRIX, Inc, Lepton Software, Precisely, SAP SE, SAS Institute Inc., TomTom International BV., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the location analytics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global location analytics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the location analytics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Location Analytics Market Report

The location analytics market was valued at USD 30.70 Billion in 2025.

The location analytics market is projected to exhibit a CAGR of 13.12% during 2026-2034, reaching a value of USD 93.13 Billion by 2034.

The location analytics market is primarily driven by the increasing adoption of IoT devices and connected sensors, the growing emphasis on personalized customer engagement, expanding cloud computing infrastructure, rising demand for real-time supply chain visibility, and the integration of artificial intelligence and machine learning capabilities into geospatial analytics platforms across diverse enterprise applications.

North America currently dominates the location analytics market, accounting for a share of 30%. The region benefits from advanced digital infrastructure, early technology adoption, strong presence of solution providers, and widespread enterprise demand for spatial intelligence across multiple industry verticals.

Some of the major players in the location analytics market include Cisco Spaces, Esri, Galigeo, GeoMoby, Google LLC, HERE Technologies, INRIX, Inc, Lepton Software, Precisely, SAP SE, SAS Institute Inc., TomTom International BV., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)