LTE and 5G Broadcast Market Size, Share, Trends and Forecast by Technology, End User, and Region, 2026-2034

Global LTE and 5G Broadcast Market Size, Share, Trends & Forecast (2026-2034)

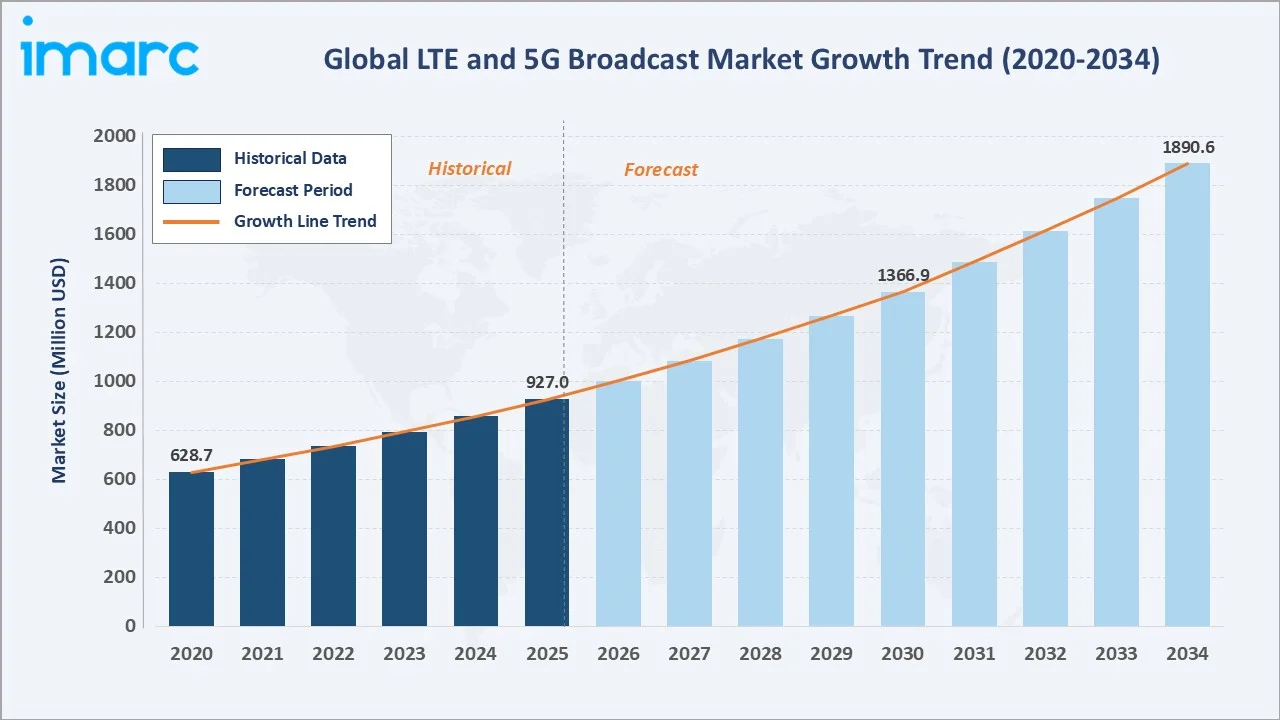

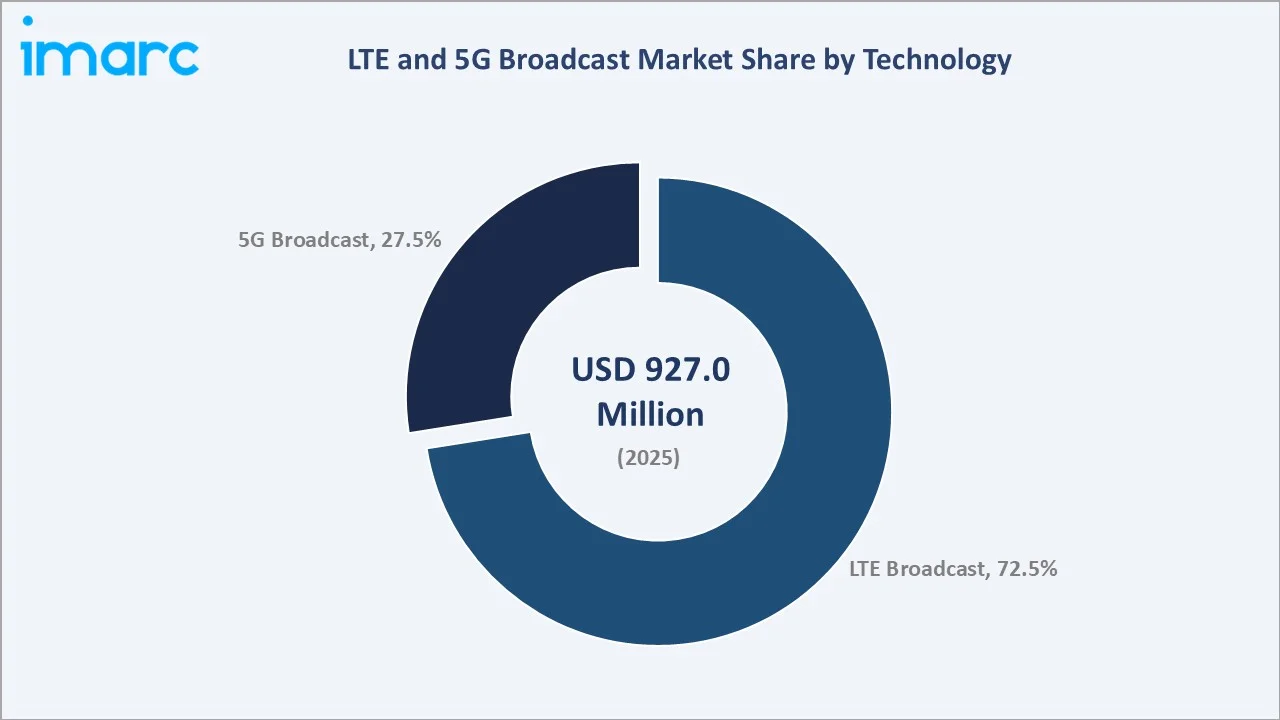

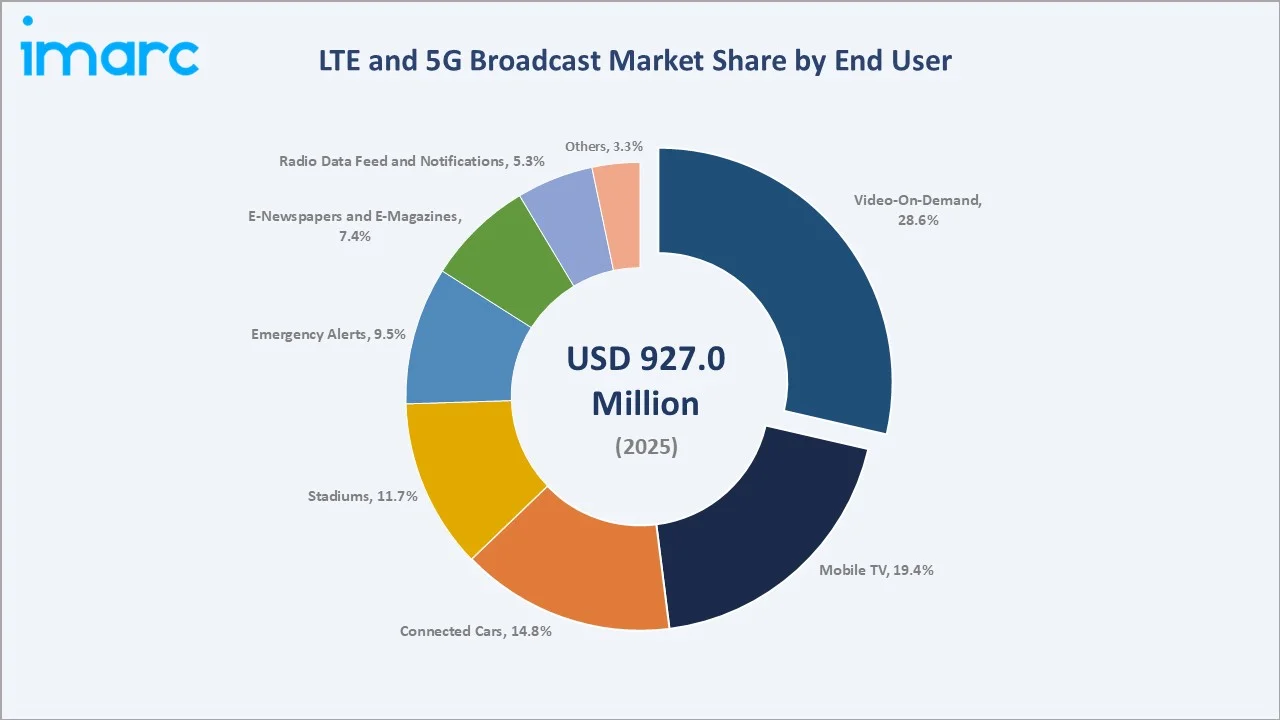

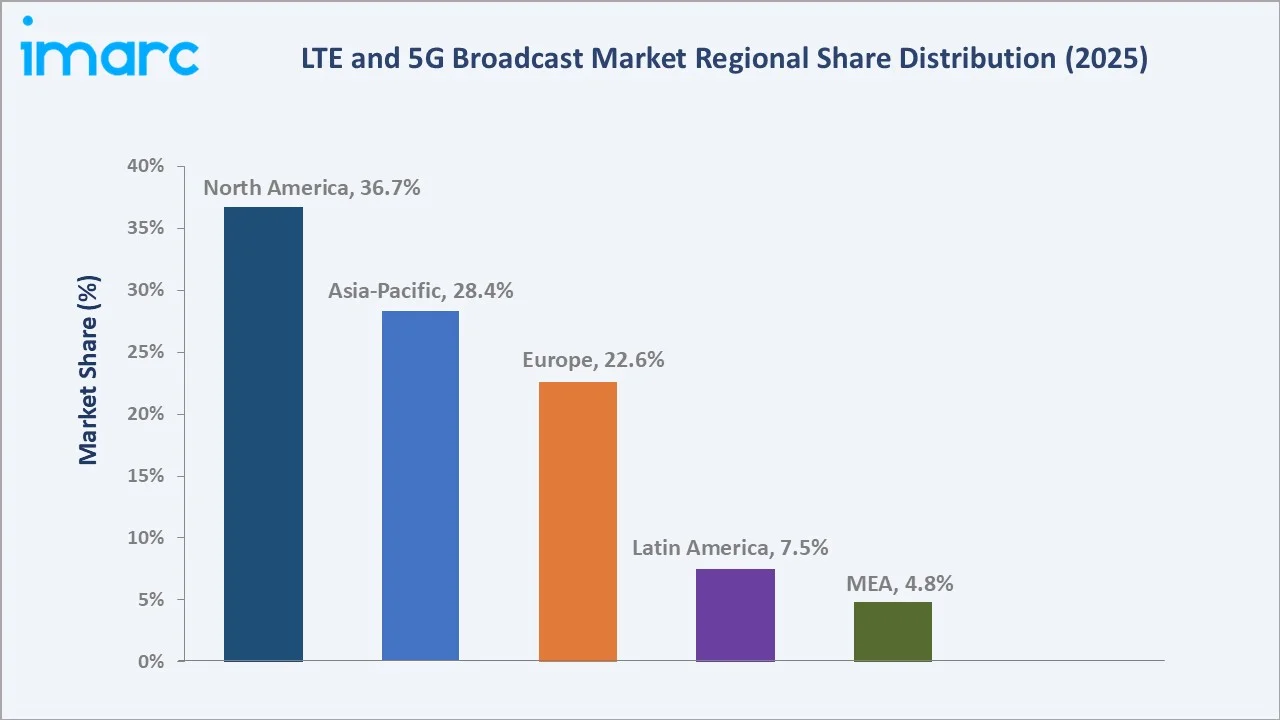

The global LTE and 5G broadcast market size was valued at USD 927.0 Million in 2025 and is projected to reach USD 1,890.6 Million by 2034, exhibiting a CAGR of 8.08% during the forecast period 2026-2034. Surging mobile video traffic, expanding live sports streaming, the rise of connected vehicles, and growing smart-city emergency alert systems are powering the LTE and 5G broadcast market growth. LTE Broadcast leads with 72.5% share in 2025, while Video-On-Demand applications account for 28.6% of demand. North America dominates with 36.7% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 927.0 Million |

|

Forecast Market Size (2034) |

USD 1,890.6 Million |

|

CAGR (2026-2034) |

8.08% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.7% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Technology |

LTE Broadcast (72.5%, 2025) |

|

Leading End User |

Video-On-Demand (28.6%, 2025) |

The chart below maps the global LTE and 5G broadcast market trajectory from 2020 through 2034, contrasting historical expansion against a sharp forecast curve powered by 5G NR Broadcast deployments, connected car growth, and rising live event streaming demand.

To get more information on this market, Request Sample

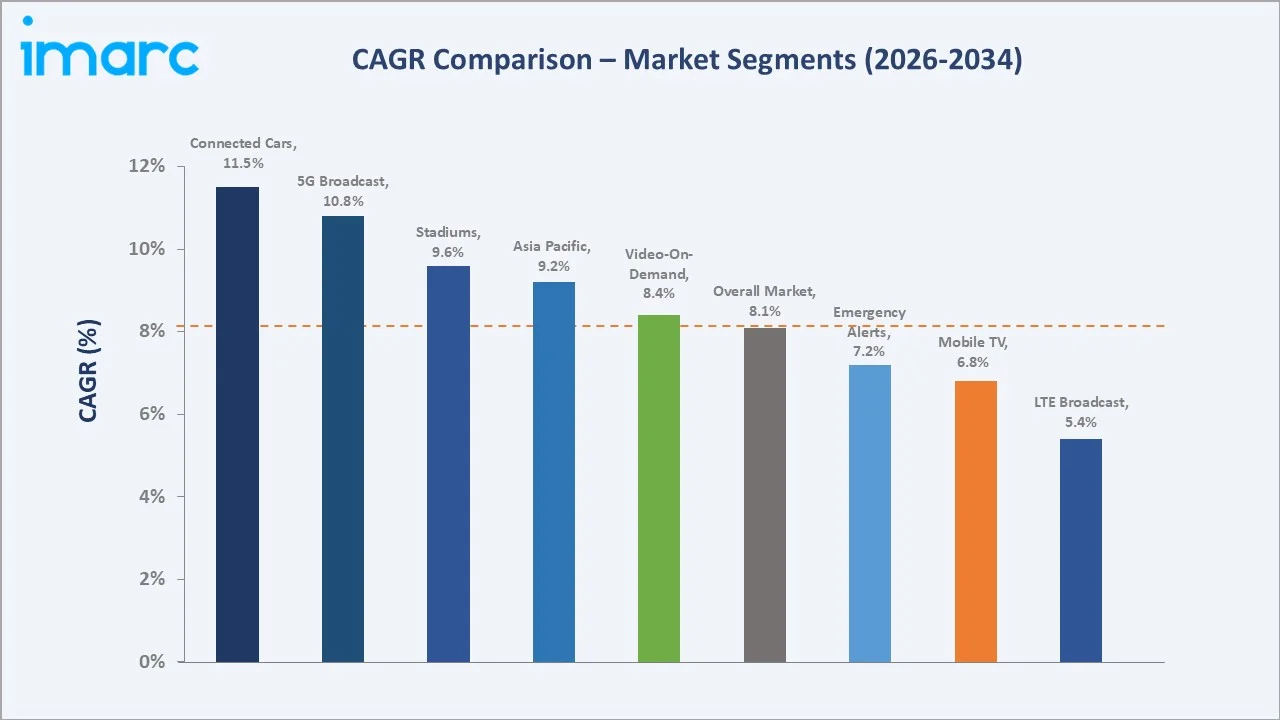

Segment-level CAGR comparisons highlight Connected Cars and 5G Broadcast technology as the fastest-growing sub-categories within the global LTE and 5G broadcast market forecast through 2034, supported by V2X adoption and 5G NR Broadcast standardization.

Executive Summary

The global LTE and 5G broadcast market is undergoing a rapid transformation. It is shaped by surging video traffic, 5G NR Broadcast standardization, and the rise of connected vehicles. Valued at USD 927.0 Million in 2025, the market is projected to reach USD 1,890.6 Million by 2034 at a CAGR of 8.08%.

LTE Broadcast (eMBMS) commands a 72.5% share in 2025, supported by mature carrier deployments across North America, Europe, and Asia. 5G Broadcast is the fastest-growing technology, advancing at an estimated CAGR of around 10.8% through 2034. Video-On-Demand leads end-users demand at 28.6%, followed by Mobile TV at 19.4% and Connected Cars at 14.8%.

North America leads with 36.7% global revenue share in 2025, anchored by T-Mobile carrier deployments. Asia-Pacific holds 28.4% and Europe 22.6%. The LTE and 5G broadcast market outlook remain positive as 5G NR Broadcast trials, smart-city emergency alerts, and live sports streaming converge across major economies.

Key Market Insights

|

Insight |

Data |

|

Largest Technology |

LTE Broadcast – 72.5% share (2025) |

|

Fastest Growing Technology |

5G Broadcast – ~10.8% CAGR (2026-2034) |

|

Largest End User |

Video-On-Demand – 28.6% share (2025) |

|

Second End User |

Mobile TV – 19.4% share (2025) |

|

Leading Region |

North America – 36.7% revenue share (2025) |

|

Top Companies |

Nokia Corporation, Huawei Technologies Co., Cisco Systems Inc., NEC Corporation. |

|

Global Mobile Video Traffic |

Estimated 79% of mobile data (2025) |

Key Analytical Observations Supporting the Above Data:

- LTE Broadcast's 72.5% dominance in 2025 reflects mature eMBMS deployments across KT Corporation, and Reliance Jio, supporting live sports, mobile TV, and stadium experiences with proven LTE infrastructure.

- 5G Broadcast's 27.5% share is rising sharply, driven by 3GPP Release 16 and 17 enhancements. Major 5G NR Broadcast field trials by Qualcomm, Rohde & Schwarz, and ATSC 3.0 partners are accelerating commercial readiness.

- Video-On-Demand's 28.6% majority is underpinned by surging mobile video consumption. According to Ericsson Mobility Report 2024, video accounts for around 79% of global mobile data traffic, projected to exceed 5 GB per smartphone monthly.

- North America's 36.7% global dominance reflects early carrier investments, NextGen TV (ATSC 3.0) deployments crossing 75% U.S. household coverage by 2024, and large stadium and emergency alert pilot programs.

- Connected Car demand is accelerating with 14.8% share in 2025, supported by V2X rollout and over 400 million connected vehicles forecast globally by 2030 per GSMA estimates, fueling broadcast infotainment and HD map updates.

Global LTE and 5G Broadcast Market Overview

LTE and 5G broadcast technologies enable point-to-multipoint content delivery across cellular networks. The standards include eMBMS (LTE Broadcast), Further evolved Multimedia Broadcast Multicast Service (FeMBMS), and 5G NR Broadcast, designed to efficiently deliver video, audio, alerts, and data to unlimited users without congesting unicast networks.

The industry sits at the convergence of telecom, media, automotive, and public safety. Growth is supported by the explosion of mobile video consumption, the rise of connected vehicles, and growing smart-city alerting requirements. The market is also pivoting toward 5G NR Broadcast standardization, FeMBMS terrestrial trials, and dedicated free-to-air broadcast use cases through 2030.

Market Dynamics

To evaluate market opportunities, Request Sample

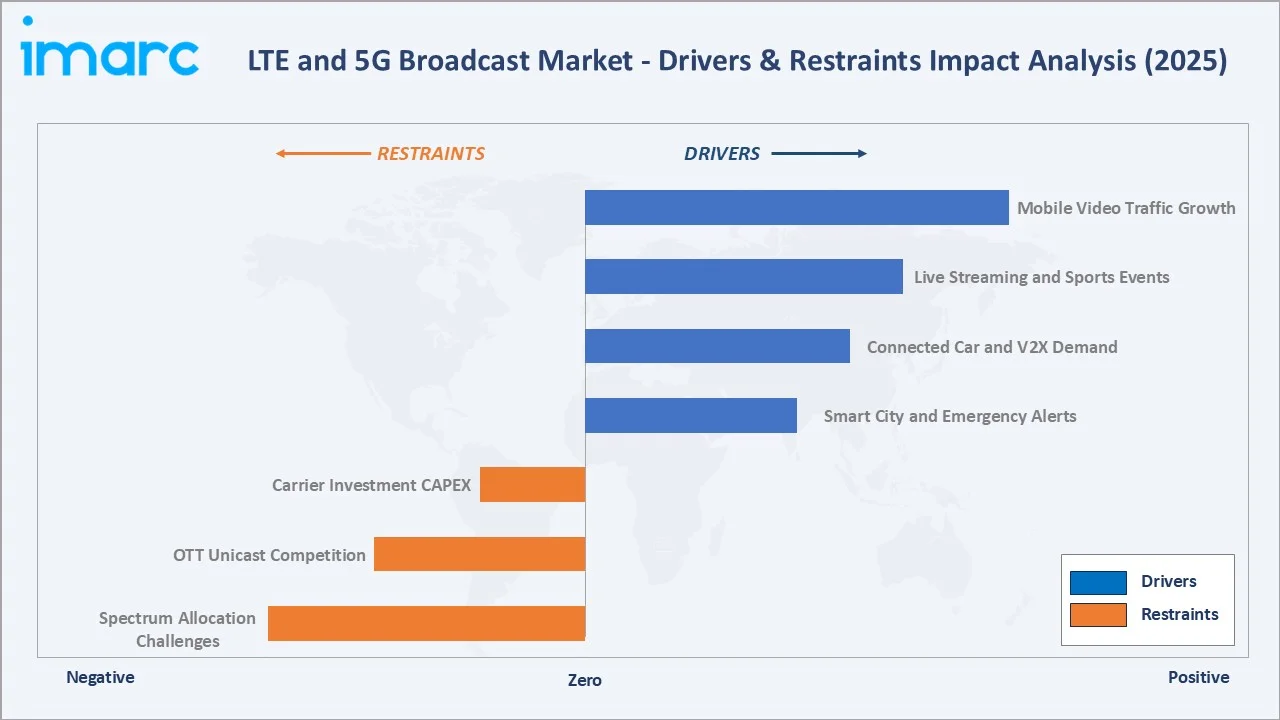

Market Drivers

- Mobile Video Traffic Growth: The Ericsson Mobility Report highlighted that 5G subscriptions in India are expected to reach around 970 million by 2030, accounting for 74% of total mobile subscriptions, while 5G networks are projected to carry nearly 80% of global mobile data traffic, reflecting the rapid shift toward high-speed connectivity and data-intensive usage. Broadcast technologies offload congestion at scale, making them economically attractive for carriers serving high-density urban areas.

- Live Streaming and Sports Events: Major sports events such as FIFA World Cup, NFL, and IPL are driving carrier-grade live streaming demand. Broadcast technologies enable simultaneous delivery to millions of users in stadiums and surrounding hotspots without unicast congestion or latency penalties.

- Connected Car and V2X Demand: GSMA estimates over 400 million connected vehicles globally by 2030. LTE and 5G broadcast supports HD map updates, traffic alerts, infotainment streaming, and V2X messaging, creating a strong automotive growth lane through the forecast period.

- Smart City and Emergency Alerts: Government-backed initiatives across the U.S. (WEA), EU (EU-Alert), Japan (J-Alert), and South Korea (KPAS) are driving cell broadcast and 5G broadcast adoption for public safety alerting, with mandates accelerating after major natural disasters globally.

Market Restraints

- Carrier Investment CAPEX: Deploying LTE and 5G broadcast requires dedicated MBMS-GW, BMSC, and broadcast-capable RAN upgrades, creating significant capital expenditure burdens that slow rollout among cost-sensitive carriers in emerging markets.

- OTT Unicast Competition: OTT services such as Netflix, YouTube, and Disney+ rely on adaptive unicast streaming. Their dominant subscriber bases and content libraries create structural competitive pressure on dedicated broadcast platforms among consumers.

- Spectrum Allocation Challenges: Dedicated broadcast spectrum allocation faces regulatory delays and competing demands from unicast 5G, IoT, and Wi-Fi 6E across major regions, slowing FeMBMS and 5G Broadcast rollout schedules through 2028.

Market Opportunities

- 5G NR Broadcast Standardization: 3GPP Release 16 and Release 17 enhancements have made 5G NR Broadcast commercially viable. Major trials by Qualcomm, Rohde & Schwarz, and ATSC 3.0 partners are creating premium opportunities across free-to-air mobile TV.

- Stadium and Hospitality Use Cases: High-density venues such as large sports stadiums are emerging as a key growth segment, where 5G enables multi-camera live feeds, instant replays, and AR-enhanced experiences for tens of thousands of users simultaneously, driving significant spikes in mobile data traffic and creating new monetization opportunities through 2030.

Market Challenges

- Limited Device Ecosystem: Native LTE Broadcast and 5G Broadcast support remains limited in mainstream smartphones beyond a few certified models. This dependency on device chipsets and OEM enablement constrains addressable subscriber penetration.

- Business Model Uncertainty: Monetization models for broadcast services remain fragmented across carrier wholesale, advertiser-funded, and pay-per-event approaches, slowing carrier commitment to dedicated broadcast service expansion.

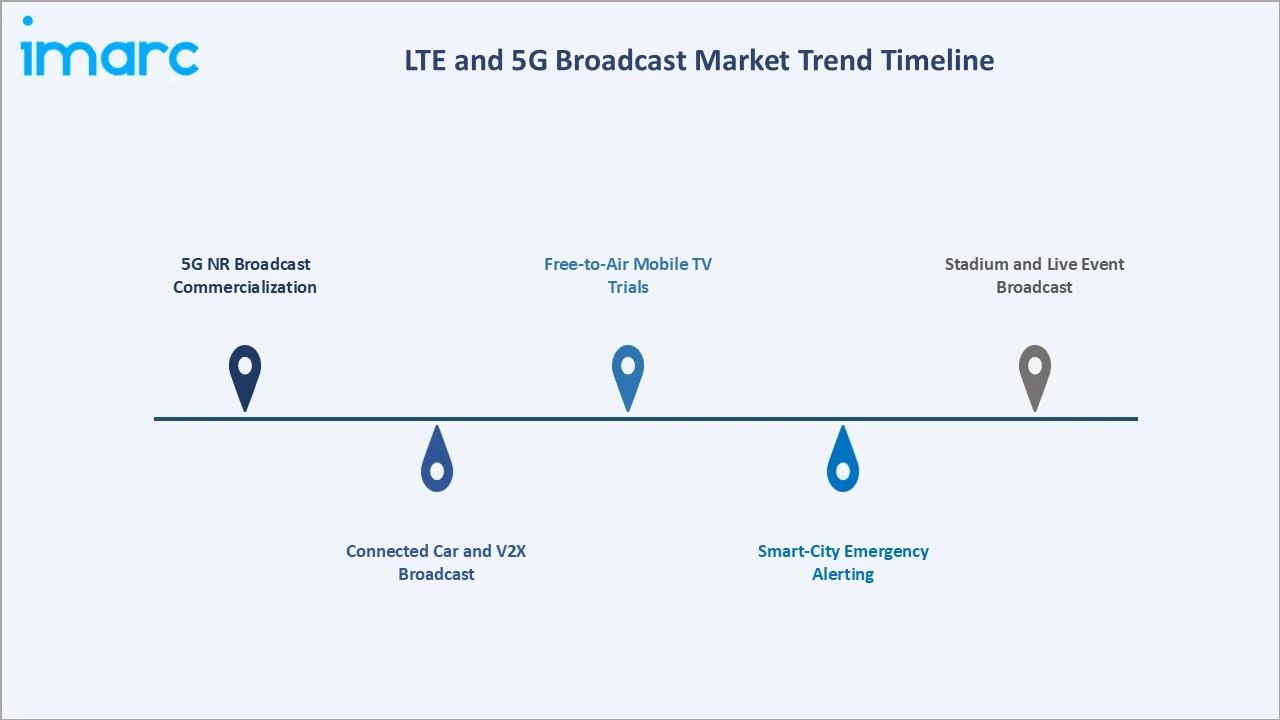

Emerging Market Trends

1. 5G NR Broadcast Commercialization

3GPP Release 16 and Release 17 standards have unlocked commercial 5G NR Broadcast. Field trials by Qualcomm, Rohde & Schwarz, BBC, and ATSC 3.0 partners across Germany, the UK, the US, and South Korea are scaling rapidly between 2024 and 2027.

2. Connected Car and V2X Broadcast

Automakers are adopting LTE and 5G broadcast for HD map distribution, traffic alerts, and infotainment streaming. Over 400 million connected vehicles are forecast globally by 2030, with broadcast emerging as the lowest-cost data delivery option for fleet-wide updates.

3. Free-to-Air Mobile TV Trials

FeMBMS and 5G Broadcast enable terrestrial free-to-air mobile TV without SIM cards. Trials by ARD/ZDF in Germany, BBC in the UK, and Korean broadcasters are demonstrating new advertising-supported and public service business models through 2028.

4. Smart-City Emergency Alerting

Government-backed cell broadcast alerts have accelerated post-2023 disaster events. The U.S. WEA, EU-Alert, Japan J-Alert, and Indian SACHET systems are now reaching billions of subscribers, with 5G broadcast enabling richer multimedia alerts through 2030.

5. Stadium and Live Event Broadcast

Stadium operators are deploying 5G broadcast for multi-camera live feeds, instant replays, and AR experiences. Major venues across the U.S., UK, Japan, and the GCC are integrating broadcast into venue Wi-Fi to handle simultaneous users at peak events.

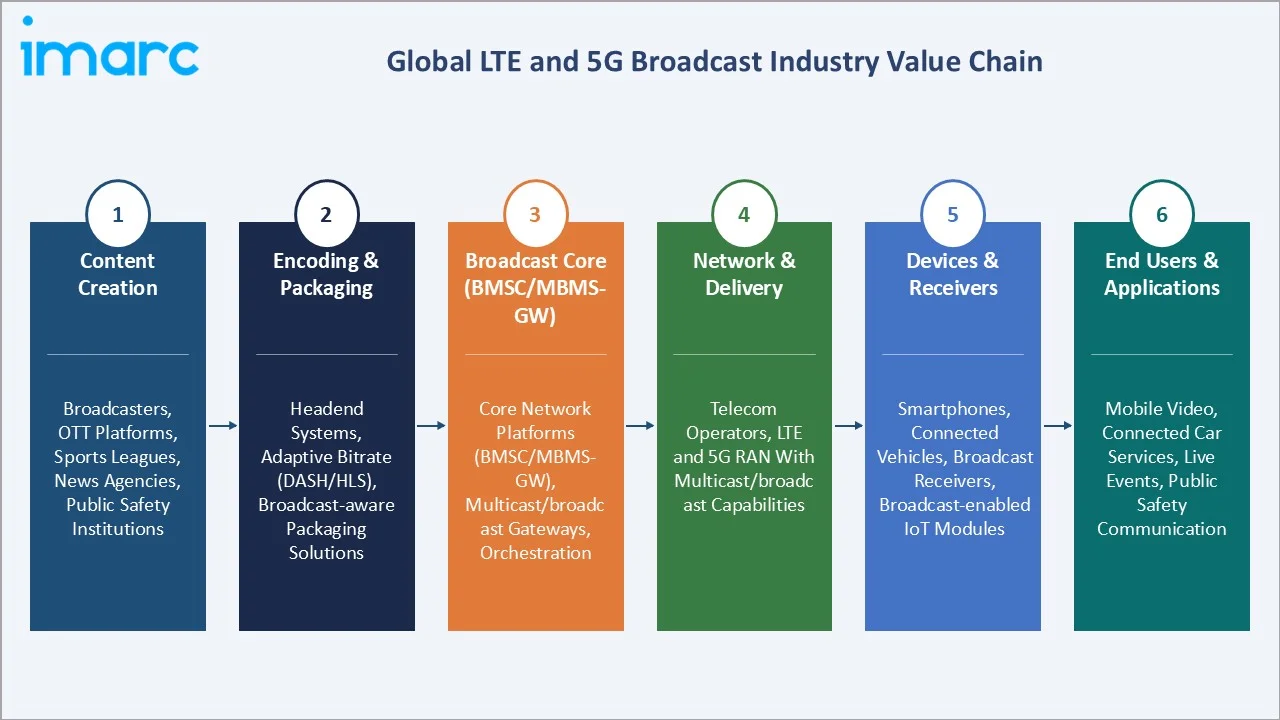

Industry Value Chain Analysis

The global LTE and 5G broadcast industry value chain spans six integrated stages from content creation through end-user consumption. Each stage shows distinct margin profiles, technology investment requirements, and competitive dynamics relevant to the overall LTE and 5G broadcast market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Content Creation |

Broadcasters, OTT platforms, sports organizations, news agencies, and public safety institutions generating video and data content |

|

Encoding and Packaging |

Providers of headend systems, adaptive bitrate encoding (DASH/HLS), and broadcast-aware packaging solutions for efficient content delivery |

|

Broadcast Core (BMSC/MBMS-GW) |

Vendors supplying core network platforms, multicast/broadcast gateways, and orchestration systems for content distribution |

|

Network and Delivery |

Telecom operators managing LTE and 5G radio access networks with multicast/broadcast capabilities for wide-area content delivery |

|

Devices and Receivers |

Manufacturers of smartphones, connected vehicles, broadcast receivers, and IoT modules capable of receiving broadcast-enabled signals |

|

End Users and Applications |

Consumers of mobile video, connected car services, live event streaming, and public safety communication services |

Network operators and core infrastructure vendors hold the highest strategic value, controlling broadcast spectrum, RAN capability, and BMSC platforms. Meanwhile, content rights holders and chipset suppliers shape device-side enablement and consumer reach, capturing margin at the front and back ends of the value chain.

Technology Landscape in the LTE and 5G Broadcast Industry

eMBMS and FeMBMS Evolution

eMBMS (LTE Broadcast) was standardized in 3GPP Release 9 and matured through Release 14. FeMBMS extensions enable terrestrial free-to-air mobile TV without SIM cards. Carriers including KT Corporation and Reliance Jio have deployed eMBMS commercially, supporting live sports, news, and mobile TV streaming.

5G NR Broadcast (Release 16 and Beyond)

5G NR Broadcast was specified in 3GPP Release 16 and enhanced in Release 17. It supports both standalone receivers and 5G smartphones, enables free-to-air broadcasting on dedicated frequencies, and offers improved spectral efficiency, latency, and signal robustness compared to LTE Broadcast.

Connected Car and V2X Broadcast

Cellular V2X (C-V2X) and 5G NR-V2X leverage broadcast to deliver HD maps, traffic alerts, and infotainment to vehicles. Major OEMs including BMW, Mercedes, Hyundai, and Tesla are integrating broadcast capabilities to support fleet-wide over-the-air updates and ADAS data distribution.

Public Safety and Emergency Alerts

Cell broadcast for emergency alerts has expanded under U.S. WEA, EU-Alert, Japan J-Alert, and India SACHET frameworks. 5G Broadcast extensions support rich multimedia alerts including video and images, increasing the effectiveness of public safety messaging across major regions.

Market Segmentation Analysis

IMARC Group provides a detailed analysis of the key trends across each segment of the global LTE and 5G broadcast market, with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been segmented based on technology and end user.

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

LTE Broadcast |

72.5% |

2025 |

|

End User |

Video-On-Demand |

🔒 |

2025 |

|

Region |

North America |

36.7% |

2025 |

By Technology

To access detailed market analysis, Request Sample

LTE Broadcast leads the global market with a 72.5% share in 2025. Demand is anchored by mature eMBMS deployments across North American, European, and Asian carriers, supporting live sports, mobile TV, and stadium experiences. 5G Broadcast accounts for 27.5% but is the fastest-growing technology at an estimated CAGR of around 10.8% through 2034. 3GPP Release 16 and 17 enhancements, ATSC 3.0 convergence, and standalone receiver compatibility are accelerating 5G Broadcast commercial readiness across global markets.

By End User

Video-On-Demand commands the largest end-user share at 28.6% in 2025, driven by surging mobile video consumption that accounts for around 79% of global mobile data traffic. Mobile TV follows at 19.4%, supported by free-to-air FeMBMS trials and live sports streaming. Connected Cars represent 14.8% and are among the fastest-growing categories, supported by 400 million connected vehicles forecast by 2030.

Stadiums account for 11.7% of demand, driven by multi-camera live feeds and AR experiences in major sports venues. Emergency Alerts hold 9.5%, accelerated by U.S. WEA, EU-Alert, and J-Alert mandates. E-Newspapers and E-Magazines (7.4%), Radio Data Feed and Notifications (5.3%), and other niche applications (3.3%) round out the end-user landscape.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.7% |

ATSC 3.0 NextGen TV rollout, FCC WEA mandates, stadium pilots |

|

Asia-Pacific |

28.4% |

KT Corp and Reliance Jio leadership, China 5G expansion, Japan J-Alert, India PMAY safety mandates |

|

Europe |

22.6% |

BBC and ARD/ZDF FeMBMS trials, EU-Alert mandates, 5G-MAG initiatives, Vodafone/Deutsche Telekom rollouts |

|

Latin America |

7.5% |

Brazil and Mexico mobile video growth, Telefonica/America Movil deployments, sports broadcast demand |

|

Middle East & Africa |

4.8% |

GCC stadium investments, Saudi Vision 2030 digital infrastructure, MTN and Vodacom carrier rollouts |

North America commands 36.7% global revenue share in 2025. The U.S. is the single most important national market, anchored by T-Mobile carrier deployments, ATSC 3.0 NextGen TV reaching over 75% household coverage by 2024, and FCC Wireless Emergency Alert mandates. Major sports broadcasters and stadium operators have actively piloted LTE and 5G broadcast for live event delivery, reinforcing regional dominance through 2034.

Asia-Pacific holds 28.4% of global revenue and is the fastest-growing region, supported by KT Corporation's pioneering eMBMS commercial launch, Reliance Jio's mass-scale LTE Broadcast deployment, China's 5G network expansion, and Japan's J-Alert public safety system. India's emergency alert SACHET framework and rapid mobile video adoption further reinforce regional growth momentum through 2034.

Europe accounts for 22.6% of global revenue, characterized by BBC and ARD/ZDF FeMBMS field trials, EU-Alert public safety mandates, and 5G Media Action Group (5G-MAG) initiatives driving carrier and broadcaster collaboration. Vodafone, Deutsche Telekom, and Orange have all conducted 5G Broadcast trials, supporting the regional shift toward standardized free-to-air mobile TV by 2030.

Latin America represents 7.5% of global revenue, led by Brazil and Mexico's combined mobile broadband expansion, Telefonica and America Movil deployments, and rising sports broadcast demand. The Middle East and Africa region accounts for 4.8%, driven by GCC stadium investments, Saudi Vision 2030 digital infrastructure programs, and MTN and Vodacom carrier expansion across Africa.

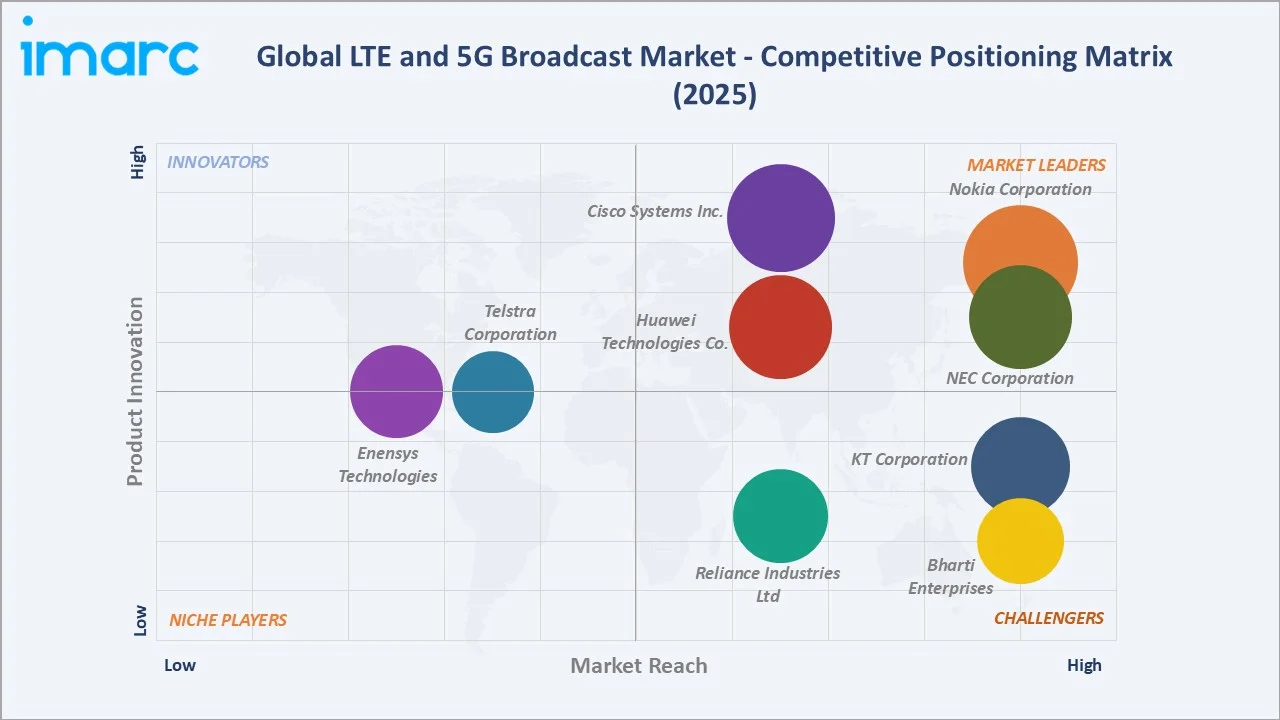

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Nokia Corporation |

Nokia Corporation |

Leader |

5G NR Broadcast leadership, RAN portfolio breadth, global carrier reach |

|

Huawei Technologies Co. |

Huawei Carrier |

Leader |

Largest 5G base station footprint, Asia Pacific dominance, R&D scale |

|

Cisco Systems Inc. |

Cisco Systems |

Leader |

BMSC platforms, video orchestration, North American leadership |

|

NEC Corporation |

NEC |

Leader |

Japanese carrier solutions, broadcast engineering depth |

|

KT Corporation |

KT Corporation |

Challenger |

Pioneering Korean eMBMS commercial launch, sports broadcast |

|

Reliance Industries Ltd |

Reliance Jio Infocomm |

Challenger |

Mass-scale Indian LTE Broadcast deployment, content integration |

|

Bharti Enterprises |

Bharti Airtel Limited |

Challenger |

Pan-India LTE expansion and content delivery integration at scale. |

|

Telstra Corporation |

Telstra |

Emerging |

Australian leadership, sports and live event broadcast specialist |

|

Enensys Technologies |

Enensys |

Emerging |

Specialty broadcast equipment, FeMBMS and ATSC 3.0 expertise |

The global LTE and 5G broadcast market's competitive landscape is moderately fragmented, with global infrastructure vendors competing alongside major carriers and specialty broadcast equipment players. Leading players compete on standards leadership, carrier deployment scale, content partnerships, and 5G NR Broadcast technology readiness. Strategic carrier-broadcaster collaborations and 5G-MAG initiatives are reshaping competitive positioning through 2030.

Key Company Profiles

Nokia Corporation

Nokia Corporation is a global telecommunications equipment leader headquartered in Espoo, Finland. Founded in 1865, Nokia operates Mobile Networks, Network Infrastructure, Cloud and Network Services, and Nokia Technologies businesses, with a presence in over 130 countries.

- Product & Platform Portfolio: Nokia's broadcast portfolio includes the AirScale RAN platform with eMBMS and 5G NR Broadcast capability, AirGile cloud-native packet core, and broadcast orchestration solutions for Tier-1 carriers globally.

- Recent Developments: In November 2025, Nokia and Telefónica Germany signed a five-year agreement to modernize and expand the operator’s nationwide radio access network, accelerating 5G rollout using Cloud RAN and AI-driven automation technologies.

- Strategic Focus: Nokia's strategy centers on leading 5G NR Broadcast standardization, growing private network broadcast deployments, and partnering with broadcasters and automakers to enable connected car and free-to-air mobile TV use cases through 2030.

Huawei Technologies Co.

Huawei Technologies is a global ICT solutions leader headquartered in Shenzhen, China. Founded in 1987, Huawei operates Carrier, Enterprise, Consumer, and Cloud businesses, serving over 170 countries and powering more than 50% of global 5G base station deployments.

- Product & Platform Portfolio: Huawei's broadcast portfolio includes 5G NR Broadcast-capable RAN platforms, eMBMS-enabled core network solutions, and end-to-end broadcast orchestration tools for carrier deployments across Asia, Europe, the Middle East, and Africa.

- Recent Developments: In January 2024, Huawei, in collaboration with China Unicom, deployed a large-scale 5.5G (5G-Advanced) pilot network in Beijing, achieving peak downlink speeds of up to 10 Gbps and enabling advanced applications such as UHD real-time broadcasting, AR/VR, and glasses-free 3D experiences.

- Strategic Focus: Huawei's focus is on dominating 5G infrastructure deployment, scaling broadcast capabilities into emerging markets, and embedding NR Broadcast into core 5G product roadmaps to enable mass-scale public safety, stadium, and connected car use cases.

Cisco Systems Inc.

Cisco Systems is a global networking technology leader headquartered in San Jose, California, USA. Founded in 1984, Cisco operates Networking, Security, Collaboration, and Observability businesses, serving service providers, enterprises, and public sector customers globally.

- Product & Platform Portfolio: Cisco's broadcast portfolio includes the Ultra Packet Core (UPC) BMSC platform, video orchestration solutions, and end-to-end media delivery infrastructure used by major North American and European carriers for eMBMS deployments.

- Recent Developments: In 2024, Cisco highlighted LTE Broadcast (eMBMS) capabilities within its ASR 5000 platform, enabling efficient point-to-multipoint content delivery for applications such as live streaming, mobile TV, and emergency alerts.

- Strategic Focus: Cisco's strategy emphasizes core network leadership, expanding cloud-native broadcast platforms, and partnering with carriers and broadcasters to enable scalable VOD, mobile TV, and emergency alert services across North America and Europe.

Market Concentration Analysis

The global LTE and 5G broadcast market exhibits moderate fragmentation. The top five players - Nokia, Huawei, Cisco, and NEC Corporation - collectively account for approximately 45-50% of global market revenue in 2025. The remaining share is distributed across KT Corporation, Reliance Jio, Airtel, Telstra, Enensys and a long tail of regional infrastructure vendors and specialty broadcast equipment suppliers.

The market shows a bifurcated dynamic. At the infrastructure tier, consolidation is occurring around 5G NR Broadcast leadership, RAN scale, and global carrier relationships. Simultaneously, regional specialists and emerging private network vendors such as Reliance Jio are capturing niche use cases including stadium broadcast, emergency alerts, and vertical industrial applications, intensifying competition across all delivery models through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Connected Cars represent the highest-growth end-user segment at an estimated CAGR of around 11.5% through 2034. 5G Broadcast technology is also expanding rapidly at approximately 10.8% CAGR, supported by 3GPP Release 16 and 17 standardization, ATSC 3.0 convergence, and the rising deployment of free-to-air mobile TV trials across major regions.

Emerging Market Expansion

India represents a high-potential growth corridor, supported by Reliance Jio's mass-scale LTE Broadcast deployment, the SACHET emergency alert system, and a rapidly expanding mobile video subscriber base. Southeast Asia, GCC stadium investments, and African carrier rollouts together create significant volume opportunities for infrastructure vendors with regional carrier relationships.

Strategic Investment Trends

Carrier-broadcaster joint ventures, 5G-MAG initiatives, and stadium operator partnerships are attracting major investment from Nokia, Huawei, Cisco, and Tier-1 carriers. In 2024, multiple Bundesliga, Premier League, and NFL stadium pilots demonstrated the commercial viability of 5G broadcast for live event delivery, reinforcing investment momentum through 2030.

Future Market Outlook (2026-2034)

The global LTE and 5G broadcast market forecast projects steady value expansion from USD 927.0 Million in 2025 to USD 1,890.6 Million by 2034 at a CAGR of 8.08%. North America will retain regional leadership while Asia-Pacific accelerates structurally as the fastest-growing region, supported by Indian and Chinese carrier deployments and live event broadcast adoption.

Three key shifts will reshape the market through 2034. First, 5G NR Broadcast will become the dominant technology by 2030, scaling from 27.5% share in 2025 to over 50% as Release 16 and 17 commercial deployments mature. Second, Connected Cars and emergency alert applications will emerge as the highest-growth end-user lanes, supported by 400 million connected vehicles globally and tightening public safety mandates. Third, 5G-MAG, ATSC 3.0, and FeMBMS convergence will unlock free-to-air mobile TV at scale, intensifying competition across both broadcast and OTT delivery models.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with LTE and 5G broadcast stakeholders, including network architects at Tier-1 carriers, product managers at infrastructure vendors, broadcast operators, public safety agencies, and chipset suppliers. Primary insights validated market sizing, segmentation estimates, and 5G Broadcast deployment timelines.

Secondary Research

Secondary sources include 3GPP technical specifications, 5G Media Action Group (5G-MAG) publications, ATSC 3.0 documentation, Ericsson Mobility Report, GSMA Intelligence, FCC public notices, ITU spectrum publications, company annual reports, and trade publications including IBC Daily, RCR Wireless, and Mobile World Live.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating mobile subscriber data, video traffic forecasts, connected car projections, carrier CAPEX trends, and historical broadcast deployment patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for technology adoption uncertainty.

LTE and 5G Broadcast Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | LTE Broadcast, 5G Broadcast |

| End Users Covered | Video-On-Demand, Mobile TV, Connected Cars, Emergency Alerts, Stadiums, E-Newspapers and E-Magazines, Radio Data Feed and Notifications, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Nokia Corporation, Huawei Technologies Co., Cisco Systems Inc., NEC Corporation, KT Corporation, Reliance Industries Ltd, Bharti Enterprises, Telstra Corporation, Enensys Technologies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the LTE and 5G broadcast market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global LTE and 5G broadcast market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the LTE and 5G broadcast industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the LTE and 5G Broadcast Market Report

The global LTE and 5G broadcast market was valued at USD 927.0 Million in 2025, supported by mobile video traffic growth, carrier eMBMS deployments, and rising connected car and emergency alert applications.

The market is projected to reach USD 1,890.6 Million by 2034, growing at a CAGR of 8.08% during 2026-2034, supported by 5G NR Broadcast standardization, V2X adoption, and stadium broadcast pilot scale-up.

LTE Broadcast leads with a 72.5% share in 2025, driven by mature eMBMS deployments across major carriers in North America, Europe, and Asia, supporting live sports, mobile TV, and stadium experiences.

North America dominates with a 36.7% share in 2025. ATSC 3.0 NextGen TV rollout, FCC WEA mandates, and stadium broadcast pilots all anchor regional leadership through 2034.

Some of the major players in the LTE and 5G broadcast market include AT&T Inc., Athonet srl, Cisco Systems Inc., Enensys Technologies SA, Huawei Technologies Co. Ltd., KT Corporation, NEC Corporation, Nokia Corporation, Reliance Jio Infocomm Limited, Spinner Group, and Telstra Corporation, among others.

Key drivers include mobile video traffic growth, live sports streaming demand, connected car and V2X adoption, smart-city emergency alert mandates, and 5G NR Broadcast standardization across global markets.

Major players include Nokia Corporation, Huawei Technologies Co., Cisco Systems Inc., NEC Corporation, KT Corporation, Reliance Industries Ltd, Bharti Enterprises, Telstra Corporation, Enensys Technologies.

Video-On-Demand is the largest end-user segment with 28.6% share in 2025, supported by mobile video accounting for around 79% of global mobile data traffic per Ericsson Mobility Report 2024 estimates.

Key opportunities include 5G NR Broadcast deployments, connected car broadcast platforms, stadium and live event use cases, free-to-air mobile TV trials, and emerging market expansion across India and Southeast Asia.

5G Broadcast holds 27.5% of global revenue in 2025, with rapid commercial readiness emerging from 3GPP Release 16 and 17 enhancements, ATSC 3.0 convergence, and growing field trials across the U.S., Germany, and Korea.

Emergency alert mandates such as U.S. WEA, EU-Alert, J-Alert, and India SACHET are accelerating cell broadcast adoption, with 5G Broadcast extensions enabling rich multimedia public safety alerts at national scale through 2030.

Connected Cars hold 14.8% share in 2025 and are forecast to grow rapidly, supported by over 400 million connected vehicles globally by 2030 per GSMA estimates, fueling broadcast-based HD map updates and infotainment delivery.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)