Luxury Cosmetics Market Size, Share, Trends and Forecast by Product Type, Type, Distribution Channel, End User, and Region, 2026-2034

Global Luxury Cosmetics Market Size, Share, Trends & Forecast (2026-2034)

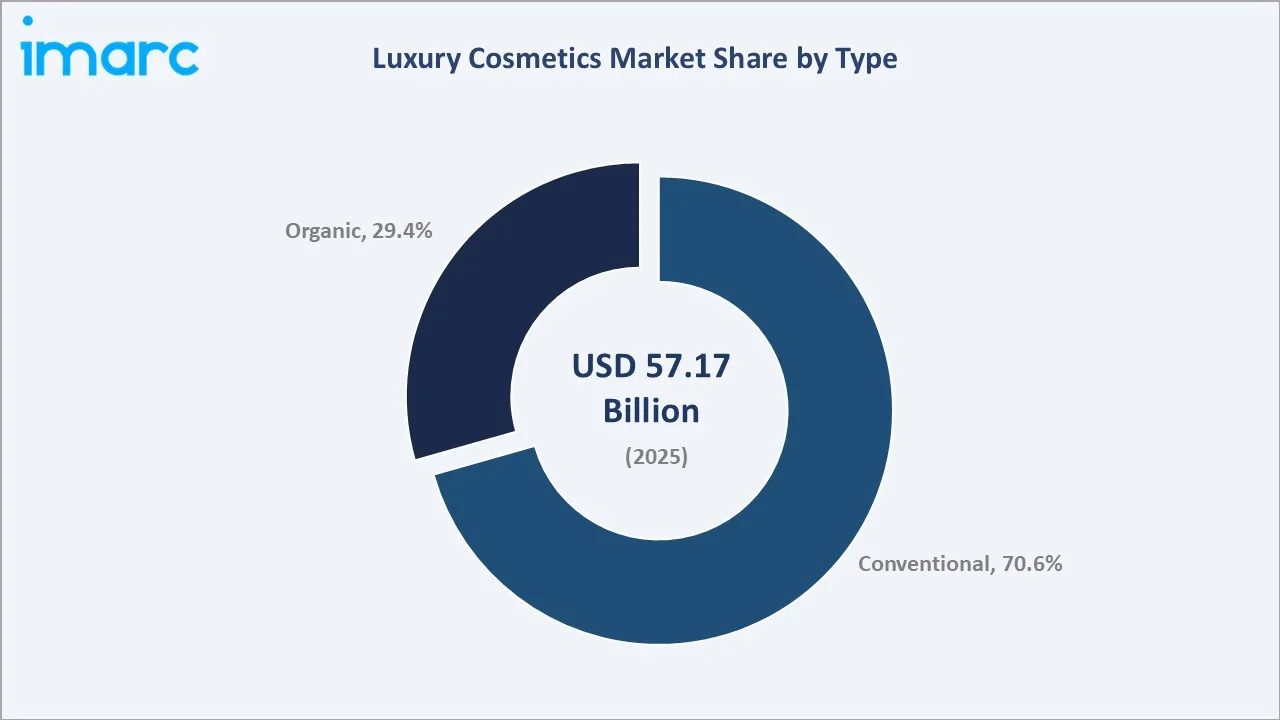

The global luxury cosmetics market size was valued at USD 57.17 Billion in 2025 and is projected to reach USD 80.83 Billion by 2034, exhibiting a CAGR of 3.92% during the forecast period 2026-2034. Rising affluence, growing self-care culture, e-commerce expansion, and surging demand for premium organic formulations are driving the luxury cosmetics market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 57.17 Billion |

|

Forecast Market Size (2034) |

USD 80.83 Billion |

|

CAGR (2026-2034) |

3.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

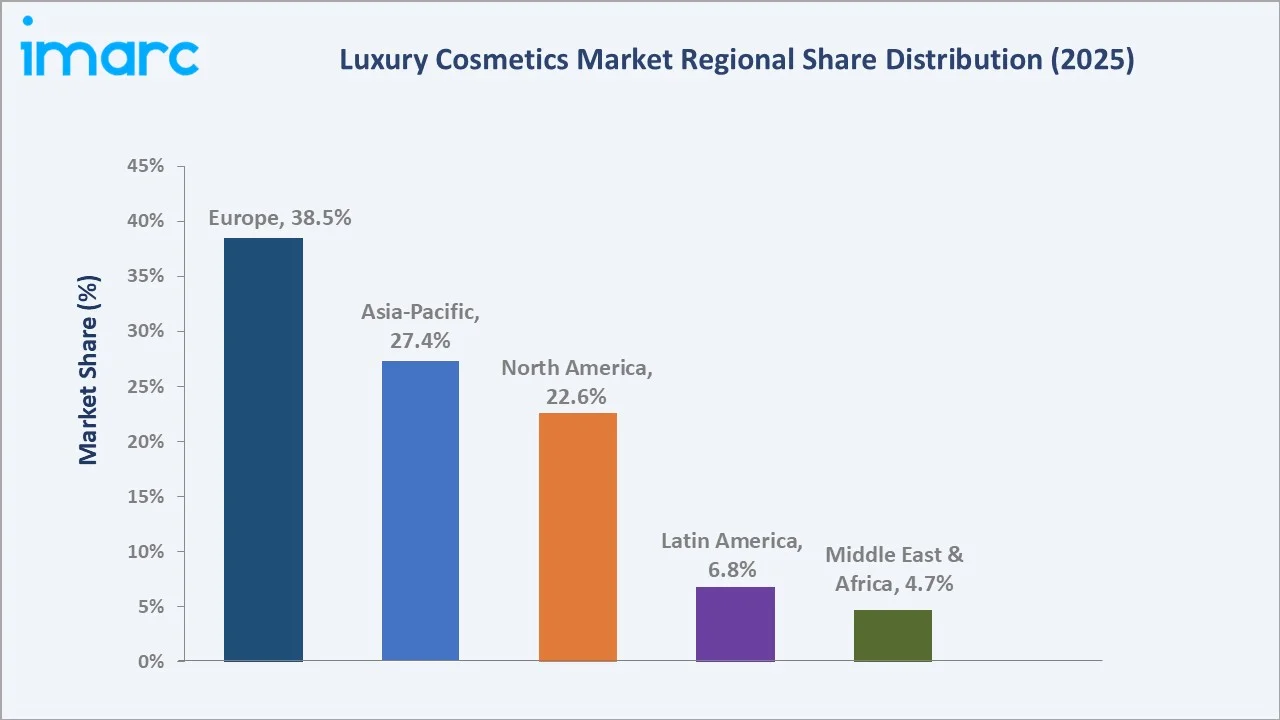

Largest Region |

Europe (38.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~4.5% CAGR) |

|

Leading Product Type |

Skincare (37.8%, 2025) |

|

Leading Type |

Conventional (70.6%, 2025) |

The global luxury cosmetics market growth trajectory from 2020 through 2034 reflects sustained expansion powered by premiumization, rising disposable incomes, and accelerating adoption of clean beauty formulations across all major geographies.

To get more information on this market, Request Sample

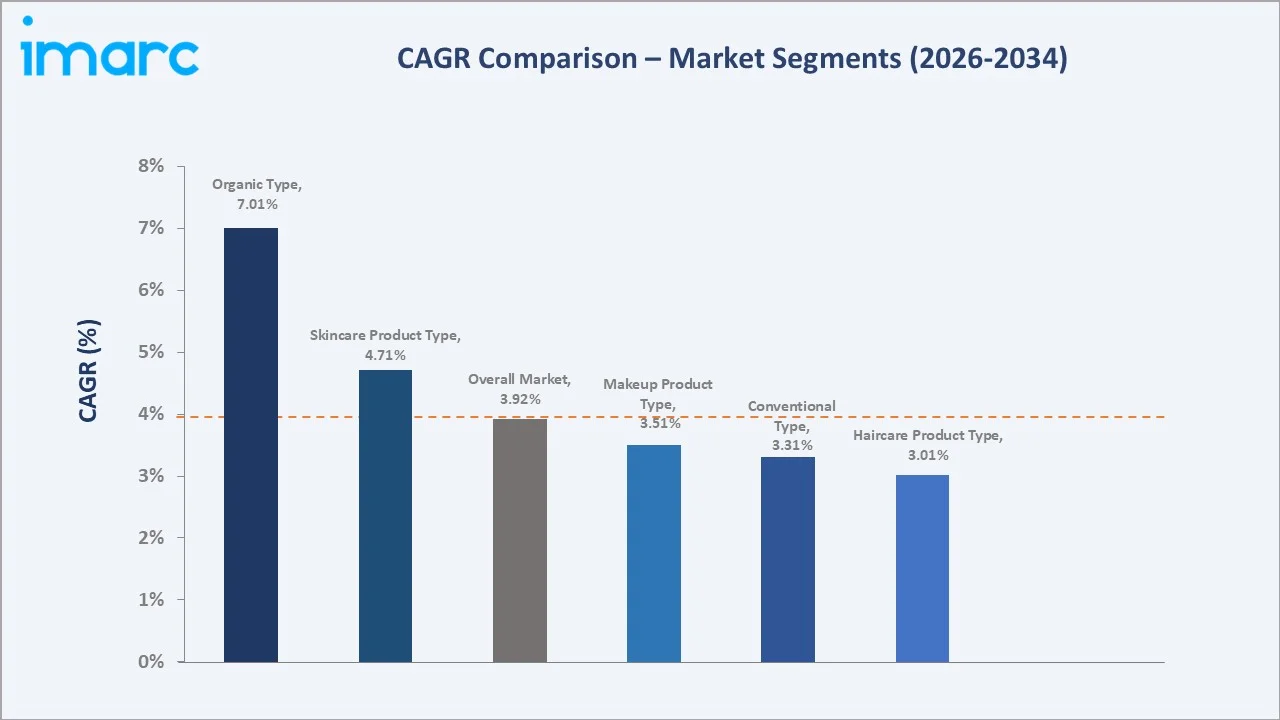

Segment-level CAGR comparisons highlight organic type adoption and skincare sub-category as the fastest-growing sub-categories within the global luxury cosmetics market forecast through 2034.

Executive Summary

The global luxury cosmetics market is undergoing a significant transformation driven by premiumization, evolving consumer self-care priorities, and growing digital retail ecosystems. Valued at USD 57.17 Billion in 2025, the market is forecast to reach USD 80.83 Billion by 2034 at a CAGR of 3.92%.

Skincare commands 37.8% share in 2025, propelled by consumer demand for anti-aging, brightening, and dermatologically backed prestige formulations. Makeup at 27.4% is driven by artisanal and limited-edition luxury collections. The organic sub-segment is expanding rapidly, projected at an estimated CAGR of 7.01% through 2034, reflecting clean-beauty preference shifts among younger affluent consumers.

Europe leads with 38.5% global revenue share in 2025, anchored by France, Italy, and the UK as heritage luxury beauty capitals. Asia-Pacific holds 27.4% and North America 22.6%. The luxury cosmetics market outlook remains highly positive as sustainability-led product design, AI-driven personalization, and omnichannel retail strategies converge across all major markets.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Skincare – 37.8% share (2025) |

|

Second Product Type |

Makeup – 27.4% share (2025) |

|

Dominant Type |

Conventional – 70.6% share (2025) |

|

Fastest Growing Type |

Organic – ~7.01% CAGR (2026-2034) |

|

Leading Region |

Europe – 38.5% revenue share (2025) |

|

Top Companies |

L'Oréal Groupe, LVMH, Estée Lauder Companies Inc., Kao Corporation, Kosé Corporation, and Puig |

|

Market Opportunity |

Asia-Pacific premiumization & organic beauty expansion |

Key Analytical Observations Supporting the Above Data:

- Skincare's 37.8% dominance in 2025 reflects surging demand for anti-aging, hyaluronic acid-infused serums, and dermatologist-endorsed prestige brands across North America and Europe.

- Makeup's 27.4% share is underpinned by celebrity-led luxury lines, limited-edition collections, and the recovery of color cosmetics spending post-pandemic, particularly in Asia-Pacific and the Middle East.

- Conventional type's 70.6% majority is anchored by decades of brand trust in established formulation technology; however, the organic segment is gaining ground at 7.01% CAGR, driven by regulatory pressure and Gen Z demand.

- Europe's 38.5% global dominance reflects France's role as the global fragrance and luxury cosmetics capital, with LVMH, L'Oréal, and Chanel collectively controlling significant global prestige beauty share.

- The organic beauty opportunity reached a segment value of approximately USD 16.8 Billion in 2025, with EU regulatory requirements on ingredient transparency accelerating brand reformulation across the premium tier.

- Fragrances at 21.6% are experiencing renewed demand through niche and artisanal luxury perfume houses, particularly in the Middle East, where oud and amber-based compositions drive premium pricing.

Global Luxury Cosmetics Market Overview

Luxury cosmetics are high-end beauty and personal care products marketed under premium brand identities, characterized by superior formulation quality, exclusive packaging, and aspirational brand positioning. The global market encompasses prestige skincare, color cosmetics, fragrances, and haircare products distributed primarily through specialty beauty retailers, department stores, duty-free channels, and digital-first direct-to-consumer platforms.

The industry operates at the convergence of fashion, lifestyle, dermatological science, and retail technology. Growth is supported by macroeconomic drivers such as rising disposable incomes in emerging economies, growing female workforce participation, and expanding male grooming culture. Simultaneously, the market is undergoing a structural shift toward sustainable, inclusive, and science-backed formulations, redefining product innovation and consumer engagement across all geographies. The luxury cosmetics industry analysis reveals robust structural resilience even during economic downturns, as the "lipstick effect" sustains premium beauty spending.

Market Dynamics

To evaluate market opportunities, Request Sample

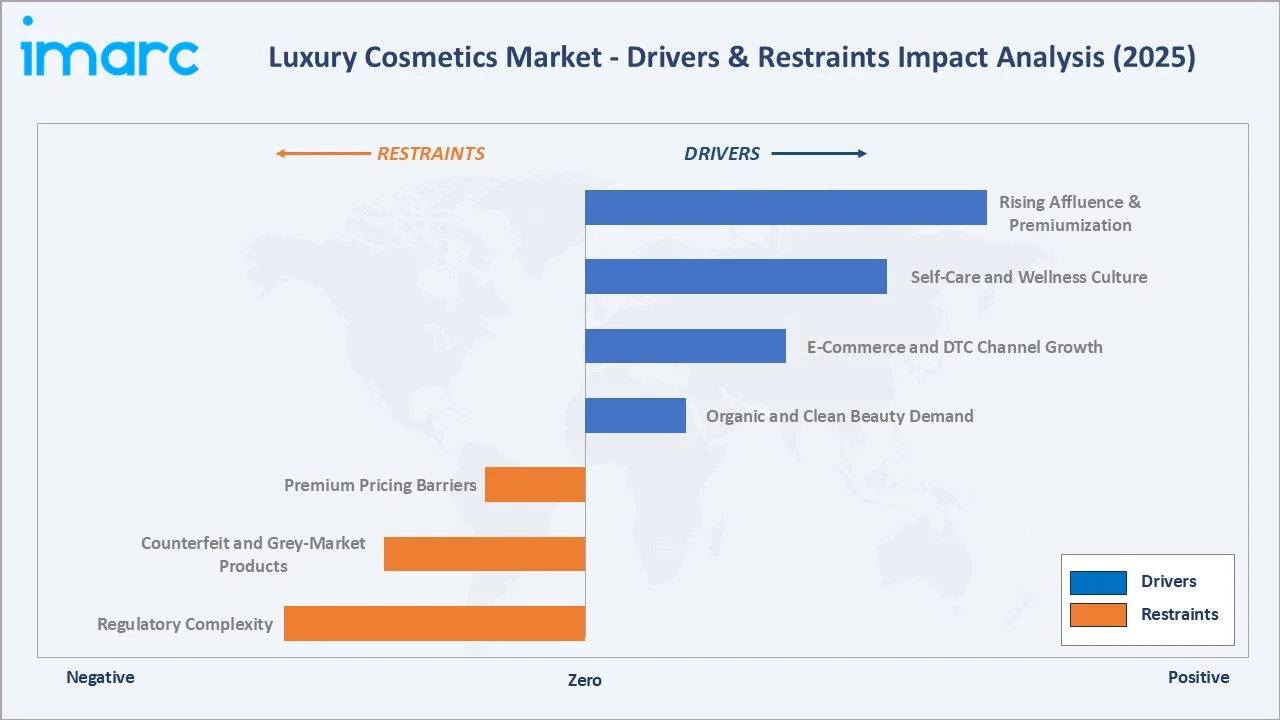

Market Drivers

- Rising Affluence & Premiumization: Global high-net-worth individual (HNWI) population reached approximately 22.8 million in 2024 per Capgemini. Growing disposable incomes in Asia-Pacific and the Middle East are fueling luxury beauty adoption in previously underpenetrated segments.

- Self-Care and Wellness Culture: Post-pandemic consumers are allocating significantly more budget to personal wellness. The global self-care market projected to reach USD 8.47 Trillion in 2027; luxury cosmetics benefit directly from this trend, especially in the skincare and fragrance categories.

- E-Commerce and DTC Channel Growth: Online luxury beauty sales are expanding at substantial growth rate 2030, outpacing brick-and-mortar retail. Brands like Estée Lauder and L'Oréal are investing heavily in virtual try-on, AI-powered skin analysis tools, and personalized subscription models.

- Organic and Clean Beauty Demand: Regulatory momentum from EU's Cosmetics Regulation and rising consumer awareness around harmful chemicals are accelerating the shift toward organic-certified formulations. The EU introduced stricter ingredient restrictions in Q1 2025, benefiting premium natural beauty brands.

Market Restraints

- Premium Pricing Barriers: High price points limit accessibility to affluent consumer segments in price-sensitive markets such as Southeast Asia, Latin America, and Sub-Saharan Africa, restricting total addressable market penetration.

- Counterfeit and Grey-Market Products: The Organisation for Economic Co-operation and Development estimates global trade in counterfeit cosmetics exceeded significant levels in 2024. Luxury cosmetics brands face reputational risks and revenue dilution from unauthorized distribution channels, particularly in online marketplaces.

- Regulatory Complexity: Divergent cosmetics regulations across the EU (REACH), U.S. (FDA Modernization of Cosmetics Regulation Act 2022), China (NMPA), and ASEAN markets impose significant compliance costs for international brand launches.

Market Opportunities

- Asia-Pacific Premiumization: South Korea, Japan, India, and China collectively represent the highest-potential growth frontier. South Korea's K-beauty influence is elevating prestige skincare adoption globally. India's luxury beauty market is projected to grow at substantial growth rate, driven by rising urban middle-class spending.

- Male Grooming and Gender-Neutral Luxury: The male luxury cosmetics segment is expanding at approximately 10.5% CAGR, driven by growing social acceptance of male grooming rituals, celebrity endorsements, and targeted product lines from brands such as Tom Ford and Dior.

- Sustainability-Driven Brand Differentiation: Consumers are increasingly rewarding brands with verified ESG credentials. Refillable luxury packaging, carbon-neutral formulation pledges, and vegan certifications are becoming key brand differentiation drivers among Gen Z luxury consumers.

Market Challenges

- Ingredient Sourcing Volatility: Rare botanical extracts, oud, and specialty minerals face supply chain vulnerabilities due to climate change and geopolitical disruptions. Sourcing from certified sustainable suppliers often increases raw material costs.

- Digital Channel Saturation: Social media-driven beauty trends shorten product lifecycles. Brands face escalating customer acquisition costs in digital marketing, with luxury beauty CPMs on platforms like Meta Platforms and TikTok increasing significantly year-over-year in 2024.

Emerging Market Trends

1. Clean Beauty and Ingredient Transparency

Consumer demand for natural, non-toxic, and sustainably sourced ingredients is reshaping luxury cosmetic formulations. EU Cosmetics Regulation amendments in 2024-2025 further restricted synthetic preservatives and microplastics.

2. AI-Driven Personalization and Beauty Tech

Artificial intelligence and augmented reality are enabling hyper-personalized luxury beauty experiences. L'Oréal's ModiFace, Estée Lauder's iMatch Virtual Try-On, and Shiseido's AI skin analysis tools are setting industry benchmarks. The global beauty tech market is projected to exceed a substantial valuation by 2030, with luxury brands capturing a premium positioning within this segment.

3. Organic and Bioscience Formulation Innovation

Lab-grown ingredients, biotechnology-derived actives, and clinically validated organic formulations are blurring the line between luxury skincare and cosmeceuticals. Brands such as La Mer, Sisley, and Tatcha are leading investment in bio-fermentation and marine-derived active ingredients.

4. Prestige Fragrance Renaissance

Niche and artisanal luxury fragrances are experiencing a global renaissance. The Middle East fragrance segment is the fastest-growing geographic niche. Major houses including LVMH's Parfums Christian Dior and Puig's Penhaligon's are expanding artisanal fragrance ranges.

5. Omnichannel Retail and Experiential Luxury

Luxury beauty brands are investing in immersive retail flagship experiences combined with seamless digital integration. Sephora's Beauty Insider program and Harrods' Beauty Hall redevelopment in 2024 underscore the convergence of physical experience with digital loyalty ecosystems.

Industry Value Chain Analysis

The global luxury cosmetics industry value chain spans seven integrated stages from rare botanical sourcing through high-end end-consumer touchpoints. Each stage presents distinct competitive dynamics, margin profiles, and innovation requirements relevant to the overall luxury cosmetics market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials & Botanical Sourcing |

Natural extracts (oud, rosehip, hyaluronic acid), rare minerals, essential oils, certified organic botanicals from specialized suppliers in France, India, and Morocco |

|

Ingredient Manufacturers |

Active compound producers, synthetic fragrance houses, specialty chemical formulators in Germany, Switzerland, and Japan |

|

R&D and Formulation Labs |

Proprietary innovation centers, clinical testing labs, patent-protected active complexes |

|

OEM & Contract Manufacturing |

Luxury beauty contract manufacturers in France, Italy, South Korea; specialized glass and eco-packaging producers; high-end filling and assembly |

|

Brand Management & Marketing |

Brand equity management, influencer partnerships, celebrity collaborations, global campaign execution |

|

Distribution Channels |

Specialty beauty retailers, dept. stores, travel retail/duty-free, online DTC, luxury e-commerce platforms |

|

End Consumers |

HNWI individuals, aspirational millennials and Gen Z consumers, beauty enthusiasts, global travelers, corporate gifting |

Brand management and marketing holds the highest strategic value by integrating prestige heritage, celebrity partnerships, and digital storytelling into premium consumer brand perception. Meanwhile, direct-to-consumer and travel retail channels are reshaping distribution, enabling brands to bypass intermediaries and capture higher margins.

Technology Landscape in the Luxury Cosmetics Industry

AI and Personalization Technology

Artificial intelligence is revolutionizing luxury beauty personalization at scale. AI-powered skin diagnostic tools, virtual try-on platforms, and smart recommendation engines are becoming standard competitive differentiation tools. Luxury brands are integrating AI to deliver bespoke formulation recommendations.

Biotechnology and Advanced Formulation Science

Biotechnology is enabling the creation of novel high-performance actives through fermentation, cell culture, and enzymatic synthesis. Lab-grown musk, bio-retinol, and microbiome-balancing prebiotics represent the cutting edge of luxury skincare science.

Sustainable Packaging and Material Innovation

Recyclable glass, biodegradable bioplastics, and refillable luxury compact systems are redefining luxury packaging standards. Chanel's N°5 refillable bottle program and Dior's Prestige La Crème jar redesign in 2024 set industry benchmarks. The EU Packaging and Packaging Waste Regulation (PPWR), effective from 2030.

Digital Commerce and Data Analytics

First-party data ecosystems, loyalty platform analytics, and hyper-personalized CRM are becoming critical luxury beauty competitive advantages. Luxury beauty brands are deploying predictive analytics to optimize product launch timing, influencer selection, and real-time trend responsiveness.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Skincare |

37.8% |

2025 |

|

Type |

Conventional |

70.6% |

2025 |

|

Distribution Channel |

Specialty and Monobrand Stores |

46.5% |

2025 |

|

End User |

Female |

88.9% |

2025 |

|

Region |

Europe |

38.5% |

2025 |

By Type

To access detailed market analysis, Request Sample

Conventional type leads the global luxury cosmetics market with a 70.6% share in 2025. Long-established consumer trust in proven synthetic formulations, brand heritage, and broad product range availability underpin this dominance. Major houses including LVMH, L'Oréal, and Estée Lauder have built multi-decade formulation platforms around conventional active technologies including retinoids, peptides, and AHAs, delivering clinically validated efficacy at premium price points.

By Product Type

Skincare leads the global luxury cosmetics product type segmentation with a 37.8% share in 2025. Demand is driven by growing consumer focus on skin health, anti-aging regimens, and dermatologically endorsed prestige formulations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

Europe |

38.5% |

France's heritage luxury houses, Italy's artisanal beauty tradition, UK's prestige retail innovation |

EU Cosmetics Regulation 2024-2025 ingredient restrictions, PPWR packaging mandates |

|

Asia-Pacific |

27.4% |

K-beauty global influence, Japan anti-aging premiumization, China luxury consumption growth, India aspirational middle class |

China NMPA registration reform 2024, South Korea cruelty-free mandates |

|

North America |

22.6% |

Strong DTC digital commerce, celebrity beauty ventures, post-pandemic self-care investment |

FDA Modernization of Cosmetics Regulation Act 2022 (MoCRA) compliance requirements |

|

Latin America |

6.8% |

Brazil luxury beauty expansion, rising middle-class spending, fragrance culture in Colombia and Argentina |

Brazil ANVISA cosmetics regulatory updates, sustainability labeling requirements |

|

Middle East & Africa |

4.7% |

Premium fragrance (oud, amber) culture in GCC, halal-certified luxury beauty expansion, Africa aspirational urban consumer |

Saudi Arabia Standards Organization (SASO) cosmetics regulations, UAE halal certification |

Europe commands 38.5% global revenue share in 2025. France remains the undisputed luxury cosmetics capital, housing LVMH, L'Oréal, Chanel, and Clarins. The region's rich heritage of fragrance and skincare innovation, supported by world-class R&D infrastructure, sustains its global market leadership. Italy contributes artisanal beauty and luxury packaging expertise, while the UK's Harrods and Selfridges remain iconic luxury beauty retail destinations.

Competitive Landscape

The global luxury cosmetics market's competitive landscape is moderately concentrated at the premium tier, with global conglomerates competing alongside independent prestige houses and rapidly scaling Korean and Brazilian challengers. Leading players compete on brand heritage, formulation innovation, digital commerce capabilities, sustainability credentials, and influencer ecosystem partnerships.

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

L'Oréal Groupe |

Lancôme, Yves Saint Laurent Beauté |

Leader |

Largest beauty conglomerate; AI beauty tech, sustainable innovation |

|

LVMH |

Dior, Givenchy, Guerlain |

Leader |

Fashion-luxury integration, fragrance dominance, heritage brand power |

|

Estée Lauder Companies Inc. |

Estée Lauder, Clinique, La Mer |

Leader |

Prestige skincare expertise, DTC digital ecosystem, Asia-Pacific focus |

|

Kao Corporation |

Kanebo, Sensai, Molton Brown |

Challenger |

Japanese precision beauty science, sustainable R&D investment |

|

Kosé Corporation |

Decorté, Tarte |

Challenger |

Asian premium positioning, global prestige dermatology brand |

|

Puig |

Carolina Herrera, Nina Ricci, Penhaligon's |

Emerging |

Artisanal fragrance leadership, niche luxury expansion strategy |

Strategic acquisitions are reshaping the competitive landscape. LVMH acquired luxury skincare brand Officine Universelle Buly and expanded its Parfums Christian Dior La Collection Privée, significantly strengthening its luxury fragrance and makeup positioning globally.

Key Company Profiles

L'Oréal Groupe

L'Oréal S.A. is the world's largest beauty company, headquartered in Clichy, France. Founded in 1909, it operates across 150+ countries with internationally recognized brands spanning luxury, professional, consumer, and active cosmetics divisions.

- Product & Platform Portfolio: L'Oréal's luxury cosmetics portfolio spans Lancôme, Yves Saint Laurent Beauté, Giorgio Armani Beauty, Valentino Beauty, Kiehl's, Helena Rubinstein, Urban Decay, and IT Cosmetics.

- Recent Developments: In January 2024, L'Oréal Groupe has announced the launch of Miu Miu Beauty, marking the brand’s official entry into the luxury cosmetics segment. The initiative follows a long-term licensing agreement with Prada to develop and distribute Miu Miu’s beauty products globally.

- Strategic Focus: L'Oréal's strategy centers on Beauty Tech integration – merging physical luxury products with digital personalization – sustainable formulation under its L'Oréal for the Future 2030 sustainability program and accelerating presence in the Indian and Southeast Asian luxury beauty markets.

LVMH

LVMH is the world's leading luxury goods conglomerate, headquartered in Paris, France. Its Perfumes & Cosmetics division houses some of the most prestigious luxury beauty brands globally.

- Product & Platform Portfolio: LVMH's luxury cosmetics portfolio includes Parfums Christian Dior, Givenchy Parfums, Guerlain, Benefit Cosmetics, Make Up For Ever, Fresh, Acqua di Parma, and Maison Francis Kurkdjian.

- Recent Developments: In 2025, LVMH has unveiled La Beauté Louis Vuitton, marking its official entry into the luxury cosmetics segment under the leadership of Pat McGrath as Creative Director. The new beauty line introduces a premium collection of lipsticks, balms, and eyeshadows, designed as high-end, refillable products that blend craftsmanship, sustainability, and artistic expression.

- Strategic Focus: LVMH's luxury cosmetics strategy focuses on reinforcing fashion-beauty integration at premium price points, expanding the private collection (La Collection Privée, Kurkdjian) fragrance category, and leveraging its global retail network of over 6,100 stores for exclusive prestige beauty distribution.

Estée Lauder Companies Inc.

Estée Lauder Companies Inc. is a premier global manufacturer and marketer of prestige skincare, makeup, fragrance, and haircare products. Headquartered in New York, USA, founded in 1946, the company operates across more than 150 countries.

- Product & Platform Portfolio: Estée Lauder's portfolio includes Estée Lauder, Clinique, La Mer, MAC, Bobbi Brown, Origins, Jo Malone London, Tom Ford Beauty, Bumble and bumble, Aveda, and Le Labo.

- Recent Developments: In 2023, The Estée Lauder Companies announced the completion of its acquisition of the Tom Ford brand, gaining full ownership of the brand and its intellectual property. The acquisition strengthens Estée Lauder’s position in the global luxury beauty segment and supports the long-term expansion of the Tom Ford brand.

- Strategic Focus: Estée Lauder's strategy centers on luxury skincare leadership, accelerating Asia-Pacific premium market penetration (particularly in China travel retail), expanding DTC digital commerce, and strengthening Tom Ford Beauty as its ultra-luxury flagship brand globally.

Market Concentration Analysis

The global luxury cosmetics market exhibits moderate-to-high concentration at the prestige tier. The top five players – L'Oréal Groupe, LVMH, Estée Lauder Companies Inc., Kao Corporation, and Kosé Corporation – collectively account for an estimated 45-55% of global premium beauty revenue in 2025.

The market is experiencing a bifurcated dynamic. At the luxury tier, consolidation is occurring around brand heritage portfolios, proprietary formulation platforms, and digital commerce capabilities. Simultaneously, the independent prestige segment is generating high-growth challengers – particularly in the niche fragrance, clean skincare, and K-beauty categories – that are disrupting traditional luxury brand positioning. This dual dynamic is intensifying competition across all price tiers through 2034.

Market fragmentation increases progressively at lower price tiers, with the mid-luxury and aspirational luxury segments seeing intense competition from masstige brands. Consolidation through M&A remains a primary growth strategy, with several significant luxury beauty acquisitions occurring annually at the global level, as large conglomerates seek to acquire emerging prestige brand equity.

Investment & Growth Opportunities

Fastest-Growing Segments

Online DTC channels are the highest-growth distribution sub-segment at approximately 14.0% CAGR through 2034. Organic luxury cosmetics are the fastest-growing product type at 7.01% CAGR. Male luxury grooming represents the fastest-growing end-user category at substantial growth rate, driven by growing social acceptance and targeted premium product launches from major houses.

Emerging Market Expansion

India represents the highest-potential emerging luxury cosmetics market, driven by a rapidly growing urban affluent population and aspirational middle-class consumers. The Indian premium beauty market is projected to grow at substantial growth rate. Southeast Asia's luxury hospitality expansion, Saudi Arabia's Vision 2030 retail development initiatives, and Nigeria's growing urban beauty culture collectively represent significant long-term volume opportunity for international prestige brands.

Venture and Strategic Investment Trends

Strategic acquisitions and beauty tech venture capital continue to reshape the competitive landscape. L'Oréal acquired Skinbetter Science in 2022 to enhance its clinical-luxury positioning. Estée Lauder completed the Tom Ford Beauty acquisition in 2023. Venture capital investment in beauty tech startups – focusing on AI personalization, bio-fermentation actives, and sustainable packaging, signaling sustained innovation investment through 2034.

Future Market Outlook (2026-2034)

The global luxury cosmetics market forecast projects sustained value expansion from USD 57.17 Billion in 2025 to USD 80.83 Billion by 2034 at a CAGR of 3.92%. Europe will retain regional leadership while Asia-Pacific will accelerate structurally, achieving its position as the second largest and fastest-growing luxury beauty region by 2028.

Three key shifts will reshape the luxury cosmetics market through 2034. First, AI-driven personalization will evolve from a differentiator to a category standard, embedding bespoke formulation intelligence directly into the consumer purchase journey. Second, sustainability credentials will become a non-negotiable brand requirement as Gen Z achieves peak luxury spending power by 2028-2030, compelling full supply chain transparency and carbon neutrality commitments.

Third, biotechnology-derived actives will progressively replace traditional rare botanical sourcing, improve formulation scalability while reduce environmental footprint across premium skincare and fragrance categories.

The fragrance category is expected to achieve the highest absolute value growth within the product portfolio through 2034, supported by niche and artisanal house expansion and Middle Eastern luxury perfume culture's growing global influence.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with luxury cosmetics industry stakeholders, including brand directors at prestige beauty houses, procurement managers at luxury retailers, category heads at e-commerce platforms, and institutional investors in consumer goods. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include EU Cosmetics Regulation databases, U.S. FDA MoCRA implementation documentation, WHO Global Beauty Industry Health Reports, Capgemini World Wealth Report 2024, company annual reports (L'Oréal, LVMH, Estée Lauder, Coty, Kao), Euromonitor Passport, trade publications including Cosmetics & Toiletries, CEW Beauty Insider, and WWD Beauty.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, HNWI population expansion, urbanization indices, luxury consumption data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative) was performed to account for macroeconomic uncertainty including currency volatility and supply chain disruption risk.

Luxury Cosmetics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Skincare, Haircare, Makeup, Fragrances |

| Types Covered | Organic, Conventional |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty and Monobrand Stores, Online Stores, and Others |

| End Users Covered | Male, Female |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | L'Oréal Groupe, LVMH, Estée Lauder Companies Inc., Kao Corporation, Kosé Corporation, Puig, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the luxury cosmetics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global luxury cosmetics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the luxury cosmetics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Luxury Cosmetics Market Report

The global luxury cosmetics market was valued at USD 57.17 Billion in 2025, driven by rising affluence, premiumization trends, self-care culture, and growing e-commerce penetration globally.

The market is projected to reach USD 80.83 Billion by 2034, growing at a CAGR of 3.92% during 2026-2034, supported by organic beauty expansion, AI personalization, and Asia-Pacific premiumization.

Skincare leads with a 37.8% share in 2025, driven by anti-aging demand, dermatologically validated prestige formulations, and high consumer willingness to invest in skin health globally.

The organic luxury cosmetics segment is the fastest-growing type category, expanding at approximately 7.01% CAGR through 2034, driven by clean beauty regulation and Gen Z affluent consumer preference.

Europe dominates with a 38.5% share in 2025, underpinned by France, Italy, and the UK as global heritage luxury beauty capitals and home to leading conglomerates.

Asia-Pacific is the fastest-growing region, advancing at approximately 4.5% CAGR through 2034, driven by China luxury consumption, K-beauty influence, and India aspirational spending.

Key drivers include rising HNWI population, self-care culture, e-commerce DTC expansion, clean beauty regulatory momentum, AI-driven personalization, and premiumization in emerging markets.

Major players include L'Oréal Groupe, LVMH, Estée Lauder Companies Inc., Kao Corporation, Kosé Corporation, and Puig.

Key opportunities include organic beauty expansion, AI personalization platforms, male grooming luxury segment, India and Southeast Asia premiumization, niche fragrance ventures, and sustainable packaging innovation.

Online DTC channels are growing, with virtual try-on, AI skin analysis, and subscription beauty boxes becoming primary luxury brand engagement tools.

Organic luxury cosmetics account for 29.4% of the global market by type in 2025, with demand accelerating due to EU ingredient restrictions, COSMOS certification adoption, and clean beauty consumer preferences.

The global luxury cosmetics market is projected to reach approximately USD 69.30 Billion by 2030, reflecting sustained CAGR-driven growth from premiumization and Asia-Pacific market expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)